Financial Analysis and Investment Appraisal for XYZ PLC Projects

VerifiedAdded on 2023/01/11

|7

|1247

|24

Report

AI Summary

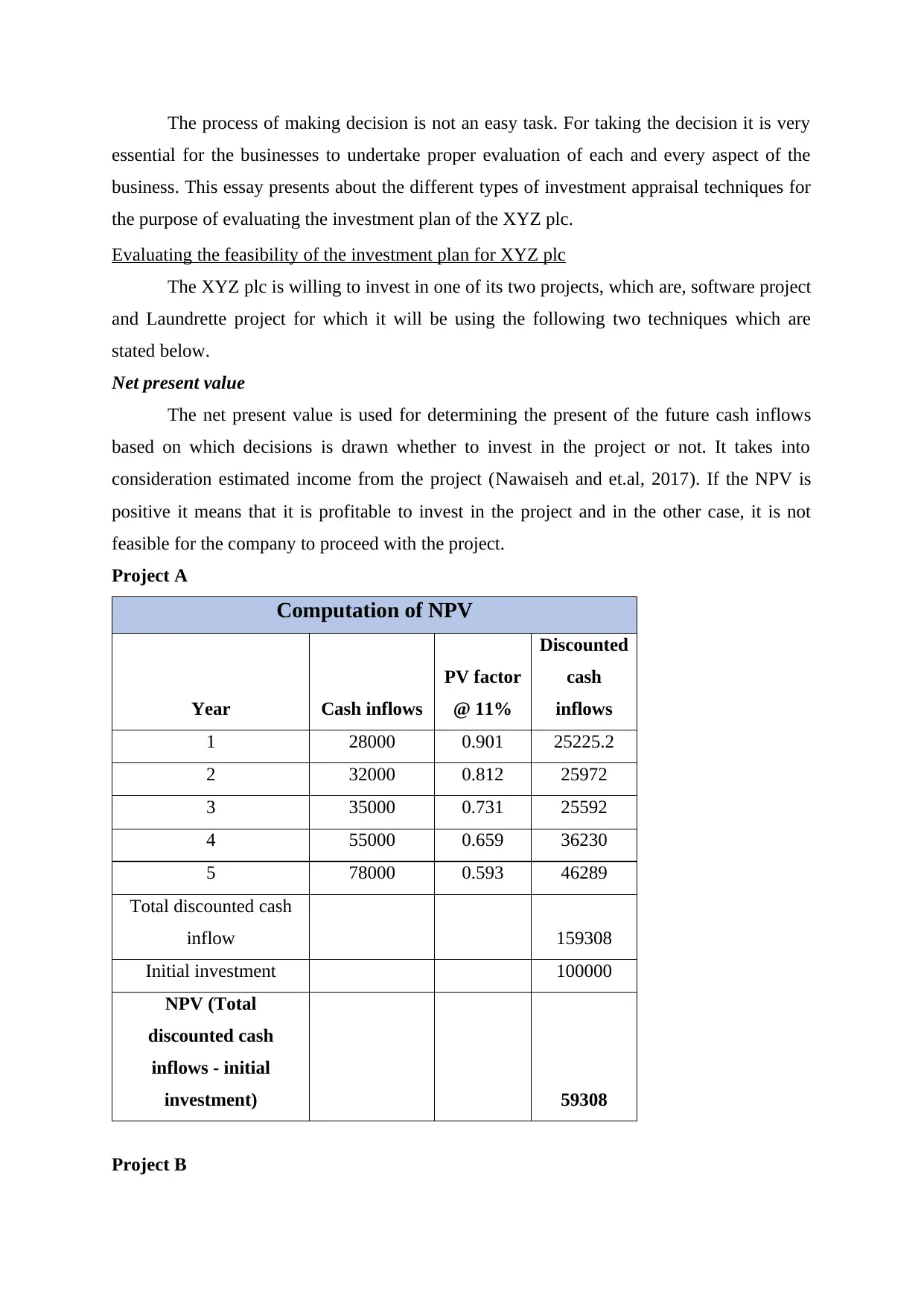

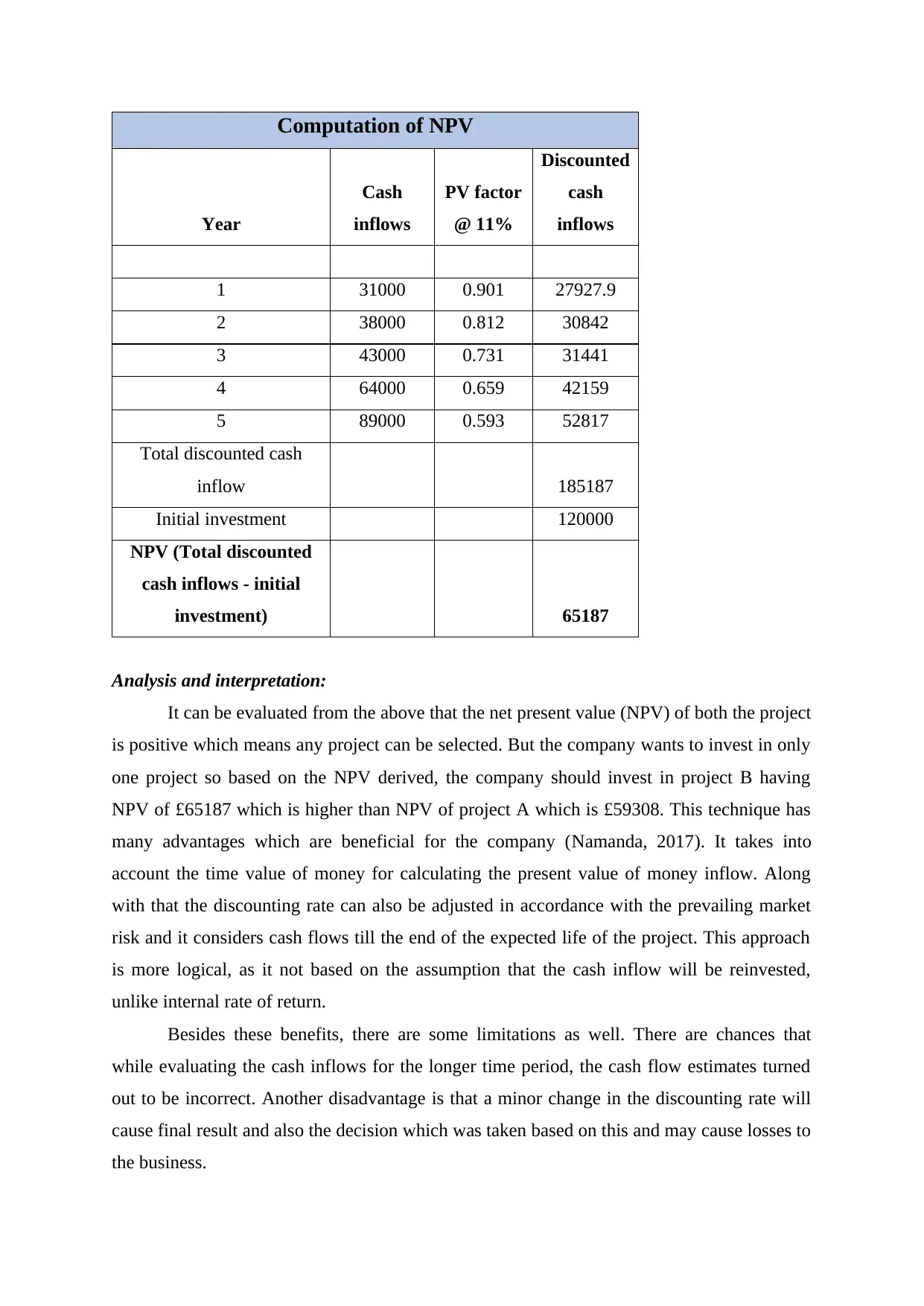

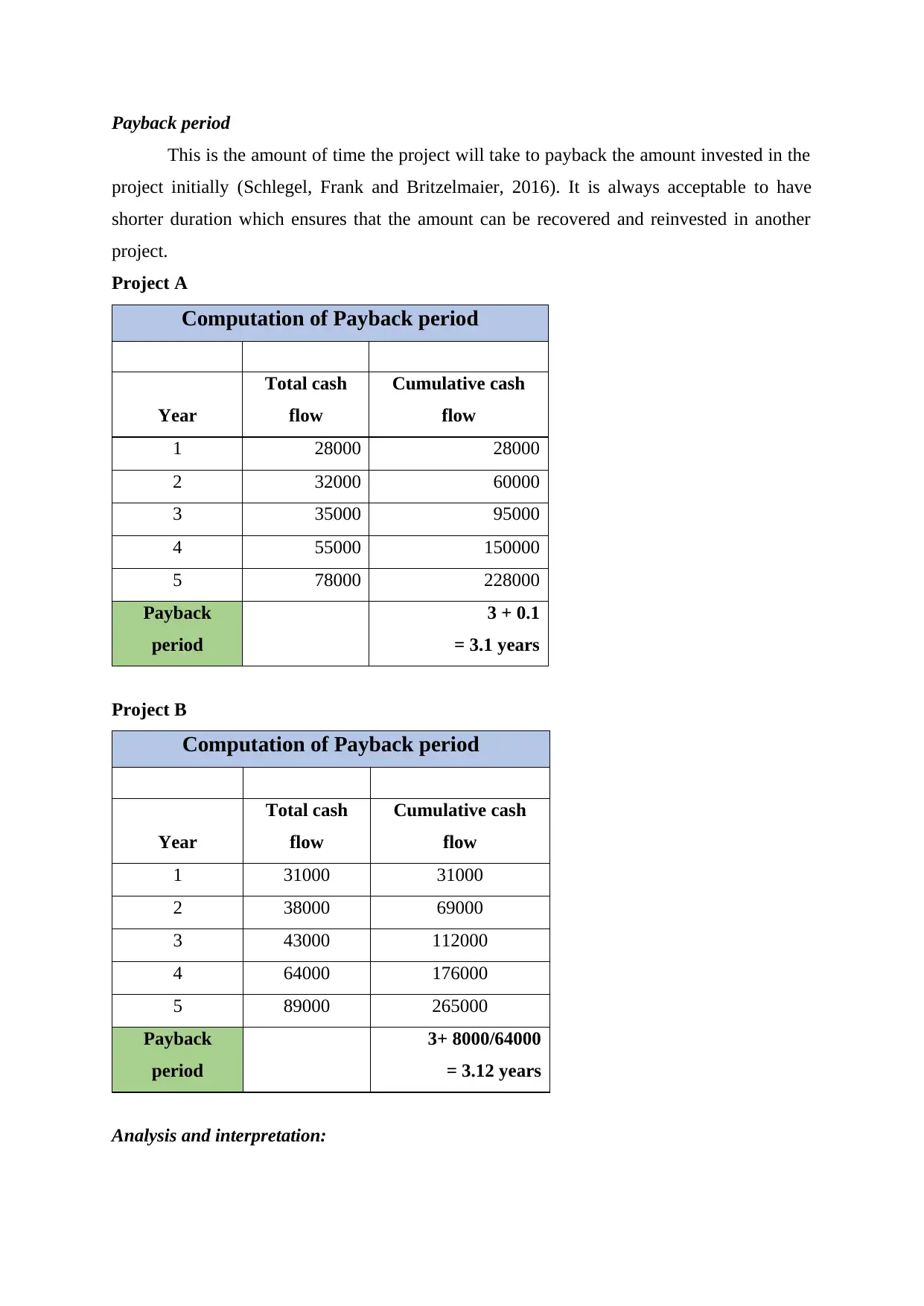

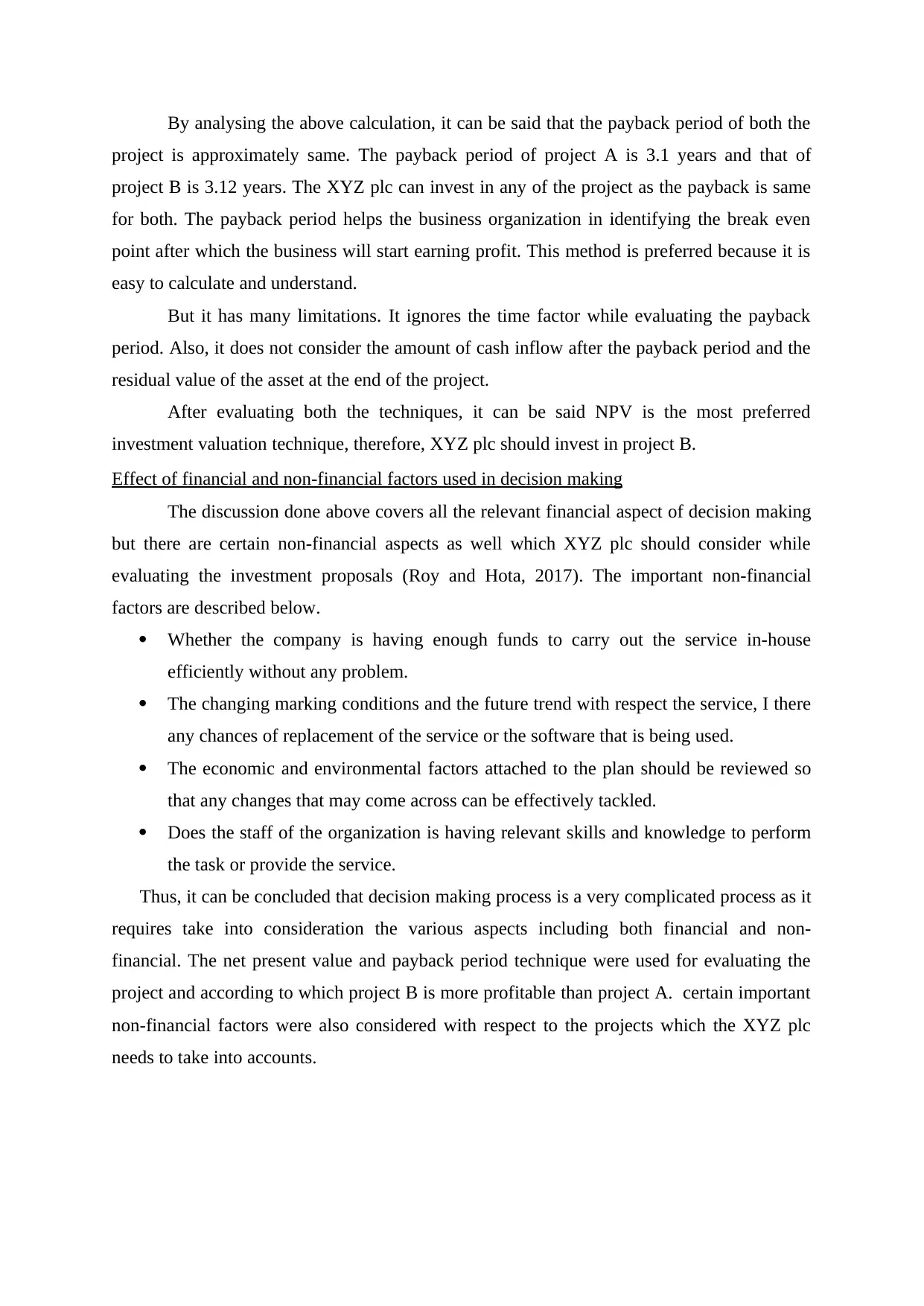

This report provides a comprehensive analysis of investment appraisal techniques applied to two potential projects (Software and Laundrette) for XYZ PLC. It delves into the Net Present Value (NPV) and payback period methods, offering detailed calculations and interpretations to evaluate the financial viability of each project. The NPV analysis reveals that both projects have positive values, but Project B presents a higher NPV (£65187) compared to Project A (£59308), making it the preferred investment option. The report also explores the payback period, which is approximately the same for both projects, highlighting the ease of calculation and understanding of this method. The report emphasizes the limitations of each technique, such as the potential for inaccurate cash flow estimates over longer periods and the disregard for cash inflows after the payback period. Furthermore, the report extends beyond financial factors, discussing crucial non-financial considerations like the availability of in-house resources, market trends, economic and environmental factors, and the skills of the staff. The report concludes that while NPV is the most preferred investment valuation technique, XYZ PLC should carefully consider both financial and non-financial aspects before making a final decision.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.