Financial Analysis, Investment Appraisal and Strategy Report - FIN4001

VerifiedAdded on 2023/06/04

|17

|4066

|229

Report

AI Summary

This report provides a comprehensive financial analysis of a business, encompassing various aspects of financial management. It begins with an introduction to finance and then delves into the calculation and interpretation of key financial ratios, such as gross profit margin, asset usage ratio, current ratio, and debt-to-equity ratio, using data from 2018 and 2019. The report also examines the significance of considering financial statement users during analysis. Furthermore, the report includes a cash flow forecast, break-even point calculations, and margin of safety analysis for two different business strategies. Finally, the report utilizes capital investment appraisal techniques, including payback period, net present value, and average rate of return, to evaluate and compare investment projects, concluding with a discussion of investment appraisal approaches and the most efficient investment option. The report aims to assess the financial health, performance, and investment potential of the business, offering insights into its strengths, weaknesses, and strategic decisions.

FIN4001 Introduction

to Finance

to Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

1.Calculation of ratios for year 2019 and year 2018....................................................................3

2.Significance of taking the users of the financial statements into consideration when

analysing the financials................................................................................................................5

Question 2........................................................................................................................................6

1.The Opening financial position at the start of July 20X5.........................................................6

2.Monthly cash flow forecast.......................................................................................................6

3.Explain the type of additive expenses that the owners of the business should take into

consideration for acquiring the needed financial assistance of overdraft....................................7

Question 3 .......................................................................................................................................8

1. Compute the Break even point (BEP) in units and in sales.....................................................8

2.Margin of safety (MOS) for the year ended 2019 and 2020.....................................................9

3. Critically evaluate and assess the strategy formulated by Jessica.........................................11

Question 4......................................................................................................................................11

1. Compute the Pay back period, Net present value and Average rate of return for every

potential investment project of the business..............................................................................11

2. Determine the most efficient investment as per the computations presented above.............14

3.Critically discuss the approaches to investment appraisal......................................................14

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 1........................................................................................................................................3

1.Calculation of ratios for year 2019 and year 2018....................................................................3

2.Significance of taking the users of the financial statements into consideration when

analysing the financials................................................................................................................5

Question 2........................................................................................................................................6

1.The Opening financial position at the start of July 20X5.........................................................6

2.Monthly cash flow forecast.......................................................................................................6

3.Explain the type of additive expenses that the owners of the business should take into

consideration for acquiring the needed financial assistance of overdraft....................................7

Question 3 .......................................................................................................................................8

1. Compute the Break even point (BEP) in units and in sales.....................................................8

2.Margin of safety (MOS) for the year ended 2019 and 2020.....................................................9

3. Critically evaluate and assess the strategy formulated by Jessica.........................................11

Question 4......................................................................................................................................11

1. Compute the Pay back period, Net present value and Average rate of return for every

potential investment project of the business..............................................................................11

2. Determine the most efficient investment as per the computations presented above.............14

3.Critically discuss the approaches to investment appraisal......................................................14

CONCLUSION .............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Finance which is also termed as financial economics refers to the discipline and study of

money in a financial stable system. It primarily involves dealings of financial funds in between

the borrowers, investors and lenders of the money. The process of finance is attached to

channelling the huge funds that are available in various different forms such as credits, loans or

capital to be invested to businesses and firms which need the finances the most or can utilise

them most efficiently (Bals, 2019). In this report, the financial statements, accounting ratios such

as gross profit margin, assets usage, acid test ratio, inventories holding period, current ratio and

debt to equity ratio and the cash budget of respective businesses have been computed to evaluate

and assess the financial positioning and financial strength of the businesses. The report also

involves computing three different investments of an enterprise to evaluate the most efficient

among the three by utilising the capital investment appraisal techniques.

MAIN BODY

Question 1

1.Calculation of ratios for year 2019 and year 2018.

Gross profit margin = ( Sales - Cost of goods sold ) * 100 / Sales

=(3495 – 2182 ) *100 / 3495

=(1313 / 3495 ) *100

=

Interpretation- The gross profit ratio helps in analysing the gross profitable efficiency of the

business enterprise. This ratio shows the relationship between the gross sales of the business and

the profit of the enterprise. The ideal gross profit ratio stands somewhere between 50-70%, here

the gross profit of the company is 37.57 % which shows that the business profits being generated

are not very good and the company requires to boost its sales and the profits generated therefore

(Hirst, 2020).

Asset Usage Ratio= Total Sales / Average Total Assets

= 3495 / [( 3812 + 2503 ) / 2]

= 3495 / 3157.5

= 1.10 times

Finance which is also termed as financial economics refers to the discipline and study of

money in a financial stable system. It primarily involves dealings of financial funds in between

the borrowers, investors and lenders of the money. The process of finance is attached to

channelling the huge funds that are available in various different forms such as credits, loans or

capital to be invested to businesses and firms which need the finances the most or can utilise

them most efficiently (Bals, 2019). In this report, the financial statements, accounting ratios such

as gross profit margin, assets usage, acid test ratio, inventories holding period, current ratio and

debt to equity ratio and the cash budget of respective businesses have been computed to evaluate

and assess the financial positioning and financial strength of the businesses. The report also

involves computing three different investments of an enterprise to evaluate the most efficient

among the three by utilising the capital investment appraisal techniques.

MAIN BODY

Question 1

1.Calculation of ratios for year 2019 and year 2018.

Gross profit margin = ( Sales - Cost of goods sold ) * 100 / Sales

=(3495 – 2182 ) *100 / 3495

=(1313 / 3495 ) *100

=

Interpretation- The gross profit ratio helps in analysing the gross profitable efficiency of the

business enterprise. This ratio shows the relationship between the gross sales of the business and

the profit of the enterprise. The ideal gross profit ratio stands somewhere between 50-70%, here

the gross profit of the company is 37.57 % which shows that the business profits being generated

are not very good and the company requires to boost its sales and the profits generated therefore

(Hirst, 2020).

Asset Usage Ratio= Total Sales / Average Total Assets

= 3495 / [( 3812 + 2503 ) / 2]

= 3495 / 3157.5

= 1.10 times

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation- This ratio helps to determine the efficiency and the ability of the enterprise with

which it is able to utilise the business assets to generate and increase the sales of the enterprise

(Rudnyckyj, 2018). High the ratio value, better is the efficiency with which the company utilises

its total assets. The ideal ratio is 2.5 and in his case the ratio is 1.10 which shows the inefficiency

of the business in utilising its assets.

Current ratio = Current Assets / Current Liabilities

= 1687 / 744

= 2.27 times

Interpretation- This ratios determine the relationship between the current assets and liabilities of

the company (Ionescu, 2021). It helps to evaluate the short terms efficiency of the business as

how effectively the short term asses of the enterprise can be utilised to pay off the obligations of

the short term liabilities. The ideal ratio is 2 whereas here it is 2.27 which shows very strong

liquidity position of the business and that the business is highly efficient and has assets higher

than the ideal requirement.

Acid Test Ratio = ( Current Assets – Stock ) / Current Liabilities

= (1687 – 150 ) / 744

= 1537 / 744

= 2.06 times

Interpretation- This ratio is also referred as quick ratio and helps to determine the efficiency with

which the business can pay off all the current liabilities of the enterprise by utilising the quick

assets of the business (Parrado-Martínez and Sánchez-Andújar, 2020). The ideal ratio is 1 and

here the ratio is 2.06 which shows a strong liquidity position of the business.

Inventory Holding Period = ( Average Inventory / Cost of goods sold )*365

= [( 150 + 102 ) / 2 ] / 2182 * 365

= ( 126 / 2182 ) * 365

= 21.08 Days

Interpretation- This ratio suggests the total number of days for which the business will hold the

inventory stock before making the sales. The number of days that the business will require in

total to convert the inventory stock into sales.

Debt to Equity Ratio = Total Debts / Total Equity

=170 / 2898

which it is able to utilise the business assets to generate and increase the sales of the enterprise

(Rudnyckyj, 2018). High the ratio value, better is the efficiency with which the company utilises

its total assets. The ideal ratio is 2.5 and in his case the ratio is 1.10 which shows the inefficiency

of the business in utilising its assets.

Current ratio = Current Assets / Current Liabilities

= 1687 / 744

= 2.27 times

Interpretation- This ratios determine the relationship between the current assets and liabilities of

the company (Ionescu, 2021). It helps to evaluate the short terms efficiency of the business as

how effectively the short term asses of the enterprise can be utilised to pay off the obligations of

the short term liabilities. The ideal ratio is 2 whereas here it is 2.27 which shows very strong

liquidity position of the business and that the business is highly efficient and has assets higher

than the ideal requirement.

Acid Test Ratio = ( Current Assets – Stock ) / Current Liabilities

= (1687 – 150 ) / 744

= 1537 / 744

= 2.06 times

Interpretation- This ratio is also referred as quick ratio and helps to determine the efficiency with

which the business can pay off all the current liabilities of the enterprise by utilising the quick

assets of the business (Parrado-Martínez and Sánchez-Andújar, 2020). The ideal ratio is 1 and

here the ratio is 2.06 which shows a strong liquidity position of the business.

Inventory Holding Period = ( Average Inventory / Cost of goods sold )*365

= [( 150 + 102 ) / 2 ] / 2182 * 365

= ( 126 / 2182 ) * 365

= 21.08 Days

Interpretation- This ratio suggests the total number of days for which the business will hold the

inventory stock before making the sales. The number of days that the business will require in

total to convert the inventory stock into sales.

Debt to Equity Ratio = Total Debts / Total Equity

=170 / 2898

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

=0.058 times

Interpretation- This ratio assesses the relationship between the debt and the equity of an

enterprise. It evaluates and compares the organisations debts to its equity as a whole. High D/E

ratio displays higher dependency of the business on its debts whereas lower ratio shows the

business is not highly dependent on its debts (Wang and Hou, 2021). The ideal debt to equity

ratio is somewhere between 2-2.5 whereas here the D/E ratio is .058 which is very low and

shows business is not highly dependent on company debts and has enough equity capital.

2.Significance of taking the users of the financial statements into consideration when analysing

the financials.

The financial statements of an enterprise assist in determining and evaluating the

financial health of the business and evaluate the financial position through insights of company's

performance, its operations and the business cash flows. Financial statements are necessary for

an enterprise as they help in extracting and determining the information regarding the company

revenues, its expenses, debt and business profitability. Through these statements the enterprise

activity and its financial performance can be evaluated easily and effectively. The financial

statement primarily involves company Balance sheet, income statement, cash flows, financial

ratios and the statement of equity (Wang, Li and Wang, 2021). The informations extracted

through these mainly constitute revenues, expenses, profits, company's liquidity positions, debt

load on the enterprise. The users of the financial statements are both internal and external to the

business. The internal users are the management of the company, owner and the employees

whereas the external users of the enterprise include tax authorities, government, investors, banks,

suppliers and shareholders of the business.

Interpretation- This ratio assesses the relationship between the debt and the equity of an

enterprise. It evaluates and compares the organisations debts to its equity as a whole. High D/E

ratio displays higher dependency of the business on its debts whereas lower ratio shows the

business is not highly dependent on its debts (Wang and Hou, 2021). The ideal debt to equity

ratio is somewhere between 2-2.5 whereas here the D/E ratio is .058 which is very low and

shows business is not highly dependent on company debts and has enough equity capital.

2.Significance of taking the users of the financial statements into consideration when analysing

the financials.

The financial statements of an enterprise assist in determining and evaluating the

financial health of the business and evaluate the financial position through insights of company's

performance, its operations and the business cash flows. Financial statements are necessary for

an enterprise as they help in extracting and determining the information regarding the company

revenues, its expenses, debt and business profitability. Through these statements the enterprise

activity and its financial performance can be evaluated easily and effectively. The financial

statement primarily involves company Balance sheet, income statement, cash flows, financial

ratios and the statement of equity (Wang, Li and Wang, 2021). The informations extracted

through these mainly constitute revenues, expenses, profits, company's liquidity positions, debt

load on the enterprise. The users of the financial statements are both internal and external to the

business. The internal users are the management of the company, owner and the employees

whereas the external users of the enterprise include tax authorities, government, investors, banks,

suppliers and shareholders of the business.

Question 2

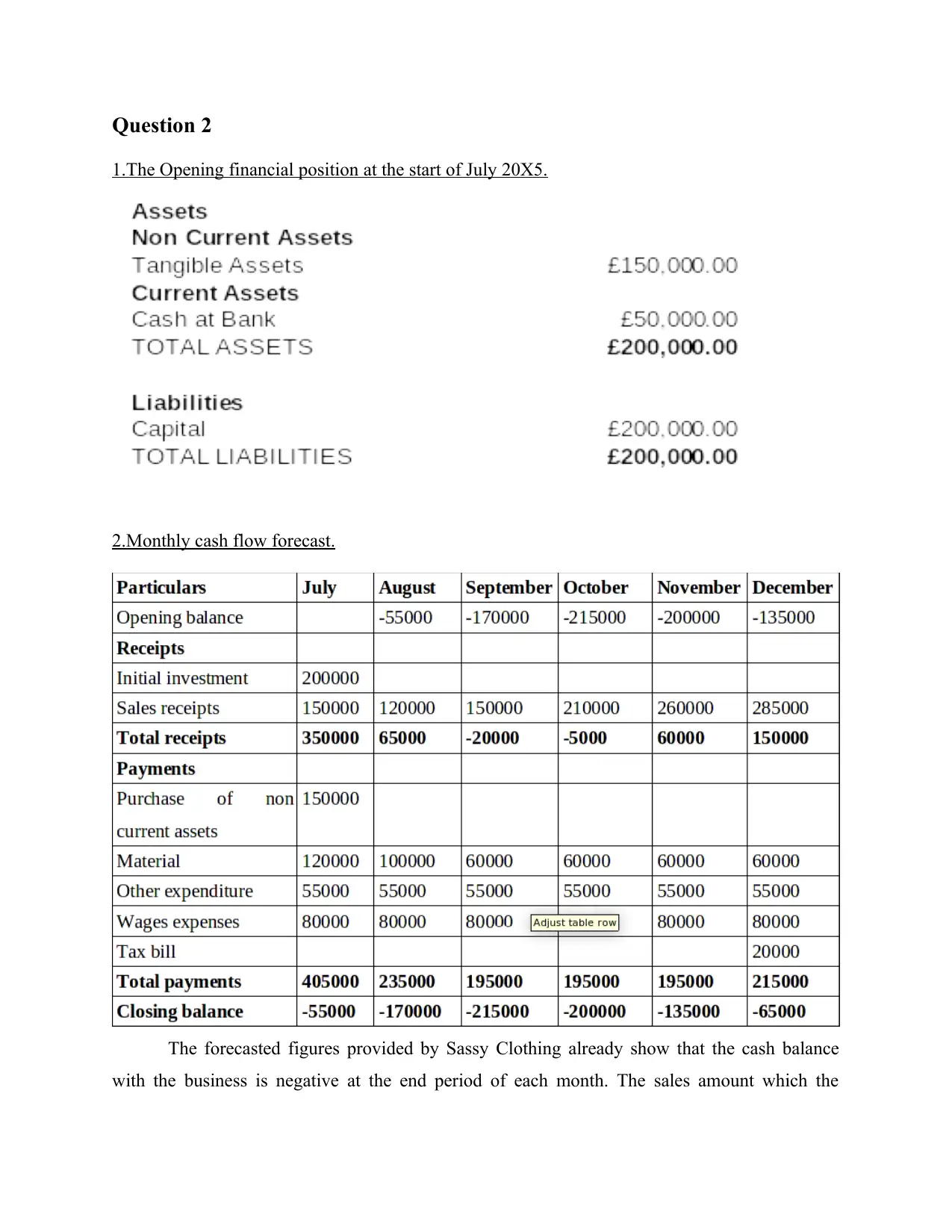

1.The Opening financial position at the start of July 20X5.

2.Monthly cash flow forecast.

The forecasted figures provided by Sassy Clothing already show that the cash balance

with the business is negative at the end period of each month. The sales amount which the

1.The Opening financial position at the start of July 20X5.

2.Monthly cash flow forecast.

The forecasted figures provided by Sassy Clothing already show that the cash balance

with the business is negative at the end period of each month. The sales amount which the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business expects after 6 months of its working is expected to be £1,175,000. It can be evaluated

that the business has had higher expenses that the revenue earned in the months of August,

September, October, November due to which they had to avail the overdraft facilities from the

banks (Berrou, Dessertine and Migliorelli, 2019). The business requires to improve their internal

as well as external performance and operations so that it can utilise the maximum capabilities of

the enterprise and achieve maximum optimisation and effectiveness in the business performance.

The business is required to negotiate with the bank manger for short term loans, approval of the

credit limit desired by the business to avail the loans in shorter times durations also and acquire

loans at lower interest rates. This will help Sassy Clothing to accelerate and improve their

revenues which will then better their cash balances in each month. The cash balances in the

business will be maintained successfully when the business continues to earn high revenues and

make lesser expenses with regards to the business raw materials, reducing unwanted experiences.

3.Explain the type of additive expenses that the owners of the business should take into

consideration for acquiring the needed financial assistance of overdraft.

The company is required to consider the expenses incurred in the months of July and

December which include utility bills, rents, operating expenses and the payment made to the

suppliers of the business. The overdraft facility of the loan helps to furnish the facility of

immediate access to additional financial funds to the enterprise. It also assists to handle any such

mismatch between the timings where the business suffered with unavailability of cash to

continue the business operations and hence maintain effective cash records (Shao and et.al.,

2022). By utilising the bank overdrafts the business can make the necessary organisational

payments and pay off the essential expenses on time avoiding any payment defaults.

that the business has had higher expenses that the revenue earned in the months of August,

September, October, November due to which they had to avail the overdraft facilities from the

banks (Berrou, Dessertine and Migliorelli, 2019). The business requires to improve their internal

as well as external performance and operations so that it can utilise the maximum capabilities of

the enterprise and achieve maximum optimisation and effectiveness in the business performance.

The business is required to negotiate with the bank manger for short term loans, approval of the

credit limit desired by the business to avail the loans in shorter times durations also and acquire

loans at lower interest rates. This will help Sassy Clothing to accelerate and improve their

revenues which will then better their cash balances in each month. The cash balances in the

business will be maintained successfully when the business continues to earn high revenues and

make lesser expenses with regards to the business raw materials, reducing unwanted experiences.

3.Explain the type of additive expenses that the owners of the business should take into

consideration for acquiring the needed financial assistance of overdraft.

The company is required to consider the expenses incurred in the months of July and

December which include utility bills, rents, operating expenses and the payment made to the

suppliers of the business. The overdraft facility of the loan helps to furnish the facility of

immediate access to additional financial funds to the enterprise. It also assists to handle any such

mismatch between the timings where the business suffered with unavailability of cash to

continue the business operations and hence maintain effective cash records (Shao and et.al.,

2022). By utilising the bank overdrafts the business can make the necessary organisational

payments and pay off the essential expenses on time avoiding any payment defaults.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3

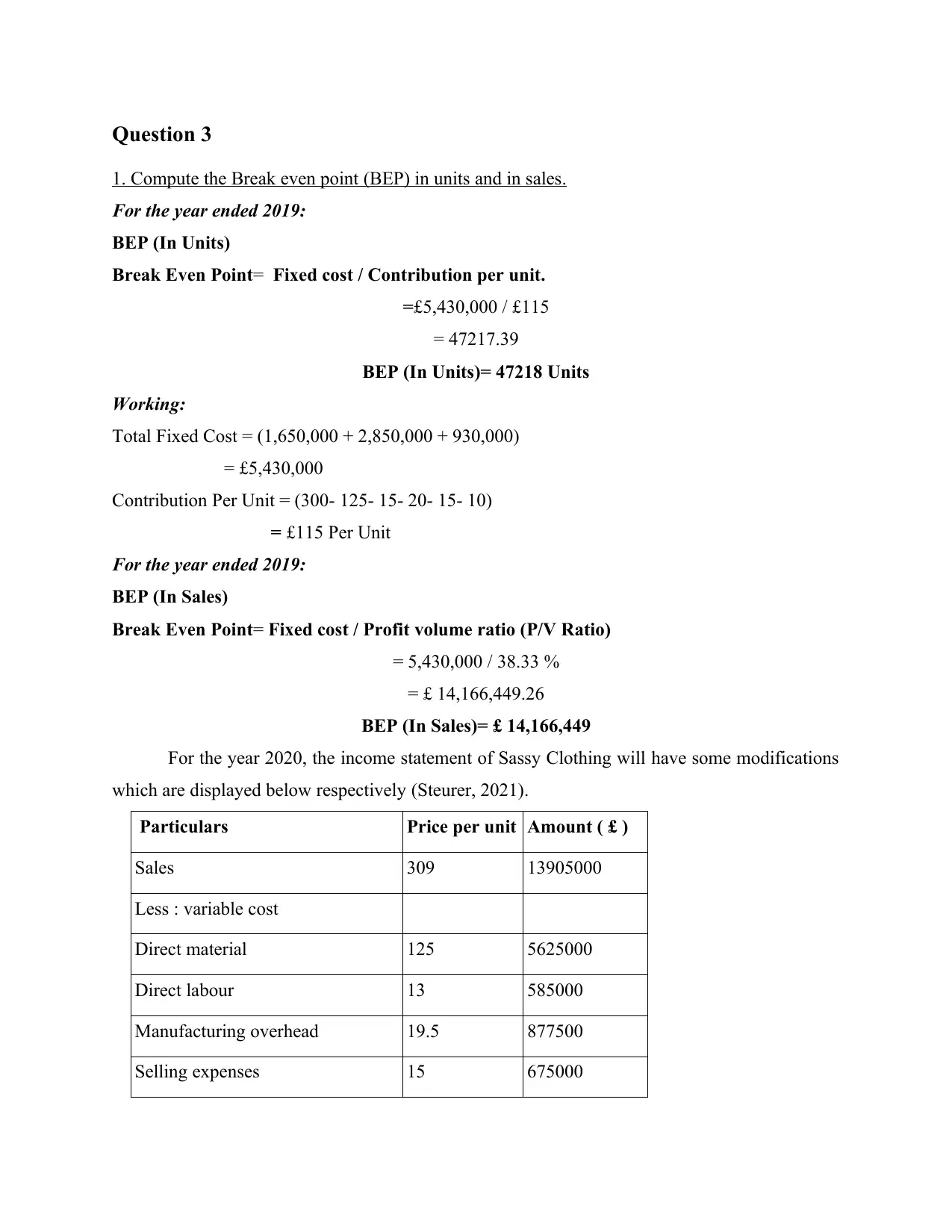

1. Compute the Break even point (BEP) in units and in sales.

For the year ended 2019:

BEP (In Units)

Break Even Point= Fixed cost / Contribution per unit.

=£5,430,000 / £115

= 47217.39

BEP (In Units)= 47218 Units

Working:

Total Fixed Cost = (1,650,000 + 2,850,000 + 930,000)

= £5,430,000

Contribution Per Unit = (300- 125- 15- 20- 15- 10)

= £115 Per Unit

For the year ended 2019:

BEP (In Sales)

Break Even Point= Fixed cost / Profit volume ratio (P/V Ratio)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

BEP (In Sales)= £ 14,166,449

For the year 2020, the income statement of Sassy Clothing will have some modifications

which are displayed below respectively (Steurer, 2021).

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

1. Compute the Break even point (BEP) in units and in sales.

For the year ended 2019:

BEP (In Units)

Break Even Point= Fixed cost / Contribution per unit.

=£5,430,000 / £115

= 47217.39

BEP (In Units)= 47218 Units

Working:

Total Fixed Cost = (1,650,000 + 2,850,000 + 930,000)

= £5,430,000

Contribution Per Unit = (300- 125- 15- 20- 15- 10)

= £115 Per Unit

For the year ended 2019:

BEP (In Sales)

Break Even Point= Fixed cost / Profit volume ratio (P/V Ratio)

= 5,430,000 / 38.33 %

= £ 14,166,449.26

BEP (In Sales)= £ 14,166,449

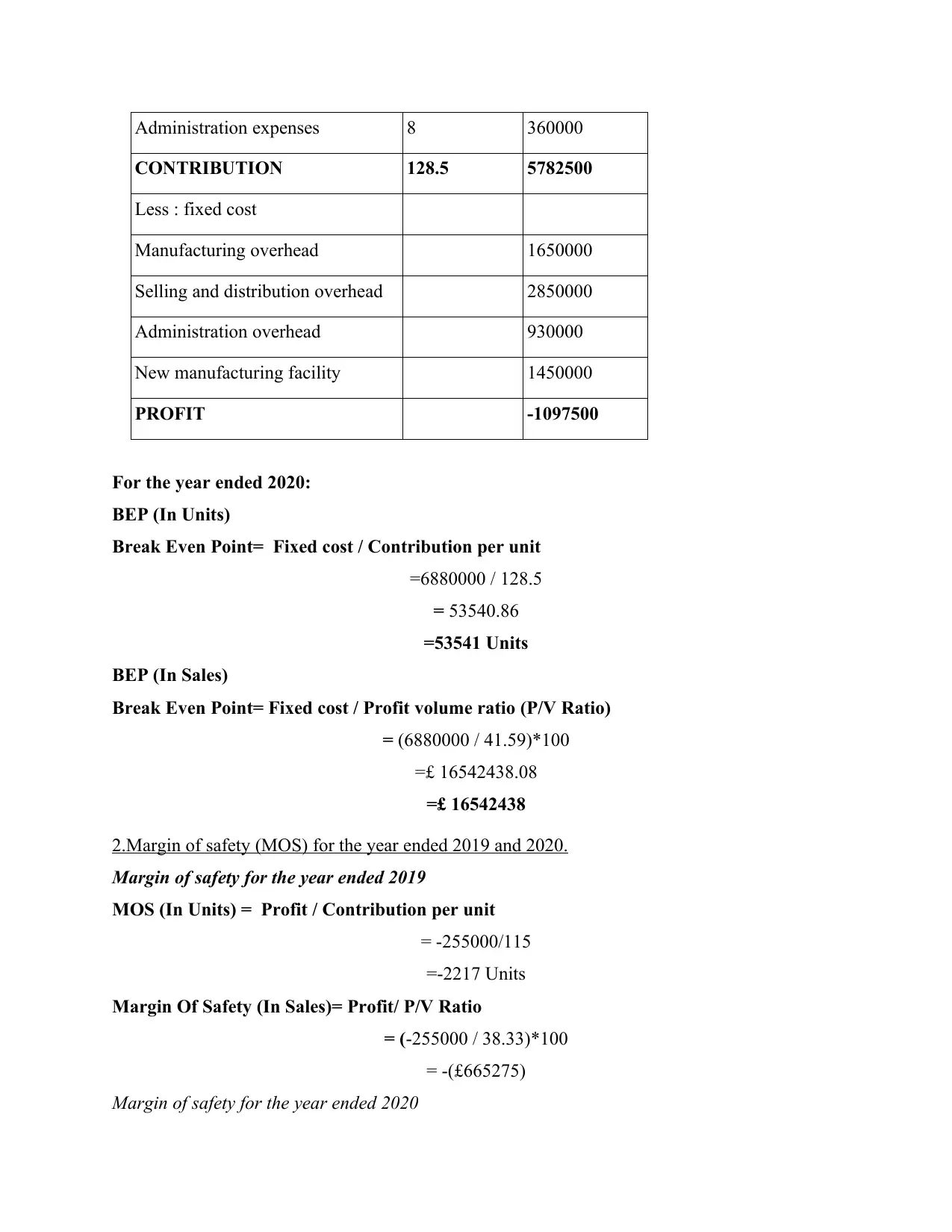

For the year 2020, the income statement of Sassy Clothing will have some modifications

which are displayed below respectively (Steurer, 2021).

Particulars Price per unit Amount ( £ )

Sales 309 13905000

Less : variable cost

Direct material 125 5625000

Direct labour 13 585000

Manufacturing overhead 19.5 877500

Selling expenses 15 675000

Administration expenses 8 360000

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

For the year ended 2020:

BEP (In Units)

Break Even Point= Fixed cost / Contribution per unit

=6880000 / 128.5

= 53540.86

=53541 Units

BEP (In Sales)

Break Even Point= Fixed cost / Profit volume ratio (P/V Ratio)

= (6880000 / 41.59)*100

=£ 16542438.08

=£ 16542438

2.Margin of safety (MOS) for the year ended 2019 and 2020.

Margin of safety for the year ended 2019

MOS (In Units) = Profit / Contribution per unit

= -255000/115

=-2217 Units

Margin Of Safety (In Sales)= Profit/ P/V Ratio

= (-255000 / 38.33)*100

= -(£665275)

Margin of safety for the year ended 2020

CONTRIBUTION 128.5 5782500

Less : fixed cost

Manufacturing overhead 1650000

Selling and distribution overhead 2850000

Administration overhead 930000

New manufacturing facility 1450000

PROFIT -1097500

For the year ended 2020:

BEP (In Units)

Break Even Point= Fixed cost / Contribution per unit

=6880000 / 128.5

= 53540.86

=53541 Units

BEP (In Sales)

Break Even Point= Fixed cost / Profit volume ratio (P/V Ratio)

= (6880000 / 41.59)*100

=£ 16542438.08

=£ 16542438

2.Margin of safety (MOS) for the year ended 2019 and 2020.

Margin of safety for the year ended 2019

MOS (In Units) = Profit / Contribution per unit

= -255000/115

=-2217 Units

Margin Of Safety (In Sales)= Profit/ P/V Ratio

= (-255000 / 38.33)*100

= -(£665275)

Margin of safety for the year ended 2020

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

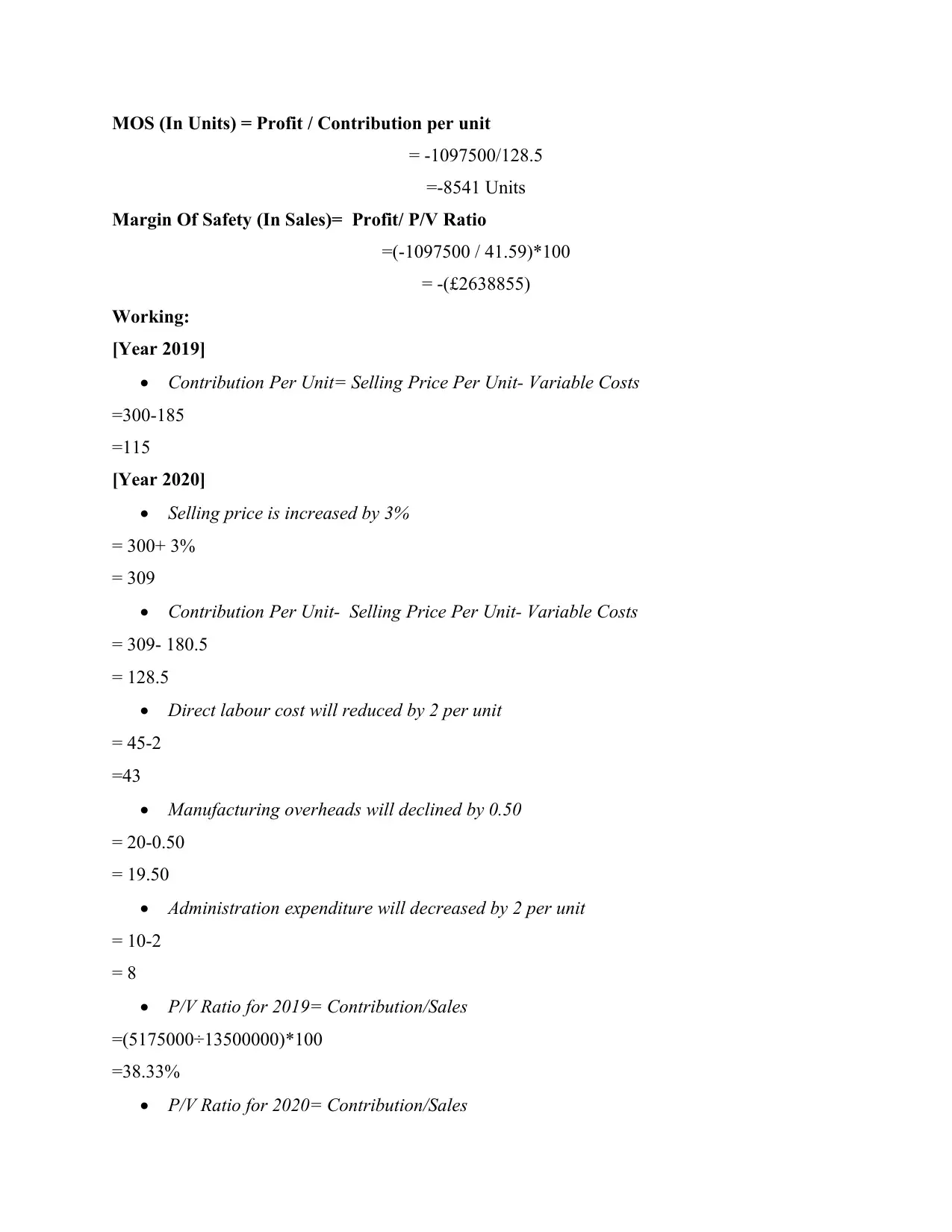

MOS (In Units) = Profit / Contribution per unit

= -1097500/128.5

=-8541 Units

Margin Of Safety (In Sales)= Profit/ P/V Ratio

=(-1097500 / 41.59)*100

= -(£2638855)

Working:

[Year 2019]

Contribution Per Unit= Selling Price Per Unit- Variable Costs

=300-185

=115

[Year 2020]

Selling price is increased by 3%

= 300+ 3%

= 309

Contribution Per Unit- Selling Price Per Unit- Variable Costs

= 309- 180.5

= 128.5

Direct labour cost will reduced by 2 per unit

= 45-2

=43

Manufacturing overheads will declined by 0.50

= 20-0.50

= 19.50

Administration expenditure will decreased by 2 per unit

= 10-2

= 8

P/V Ratio for 2019= Contribution/Sales

=(5175000÷13500000)*100

=38.33%

P/V Ratio for 2020= Contribution/Sales

= -1097500/128.5

=-8541 Units

Margin Of Safety (In Sales)= Profit/ P/V Ratio

=(-1097500 / 41.59)*100

= -(£2638855)

Working:

[Year 2019]

Contribution Per Unit= Selling Price Per Unit- Variable Costs

=300-185

=115

[Year 2020]

Selling price is increased by 3%

= 300+ 3%

= 309

Contribution Per Unit- Selling Price Per Unit- Variable Costs

= 309- 180.5

= 128.5

Direct labour cost will reduced by 2 per unit

= 45-2

=43

Manufacturing overheads will declined by 0.50

= 20-0.50

= 19.50

Administration expenditure will decreased by 2 per unit

= 10-2

= 8

P/V Ratio for 2019= Contribution/Sales

=(5175000÷13500000)*100

=38.33%

P/V Ratio for 2020= Contribution/Sales

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

=(5782500÷13905000)*100

=41.58%

3. Critically evaluate and assess the strategy formulated by Jessica.

The two respective strategies have been evaluated in the computations made above. It is

hence evaluated that the new strategy formulated incurs higher financial risk. The BEP of the

previous strategy of 2019 comes as 47218 and of the new strategy of 2020 comes to be 53541 in

units. The MOS in sales of the two strategies as of 2019 is -£665275 and of 2020 is -£26388550.

Both the strategies displayed very low and negative margin of safety (Zhang, Zhang and Managi,

2019). But it can be assessed looking at the numbers that the new strategy made the MOS worse

as 2019. Hence the business should think upon to apply effective growth strategies, accelerate

the organisational sales and boost the business growth through intense promotion and other

effective tools. To attain additional growth, the business has already spent an additional amount

of £1,450,000 on its fixed costs which is also a primary reason why the business is facing high

costs and losses.

Question 4

1. Compute the Pay back period, Net present value and Average rate of return for every potential

investment project of the business.

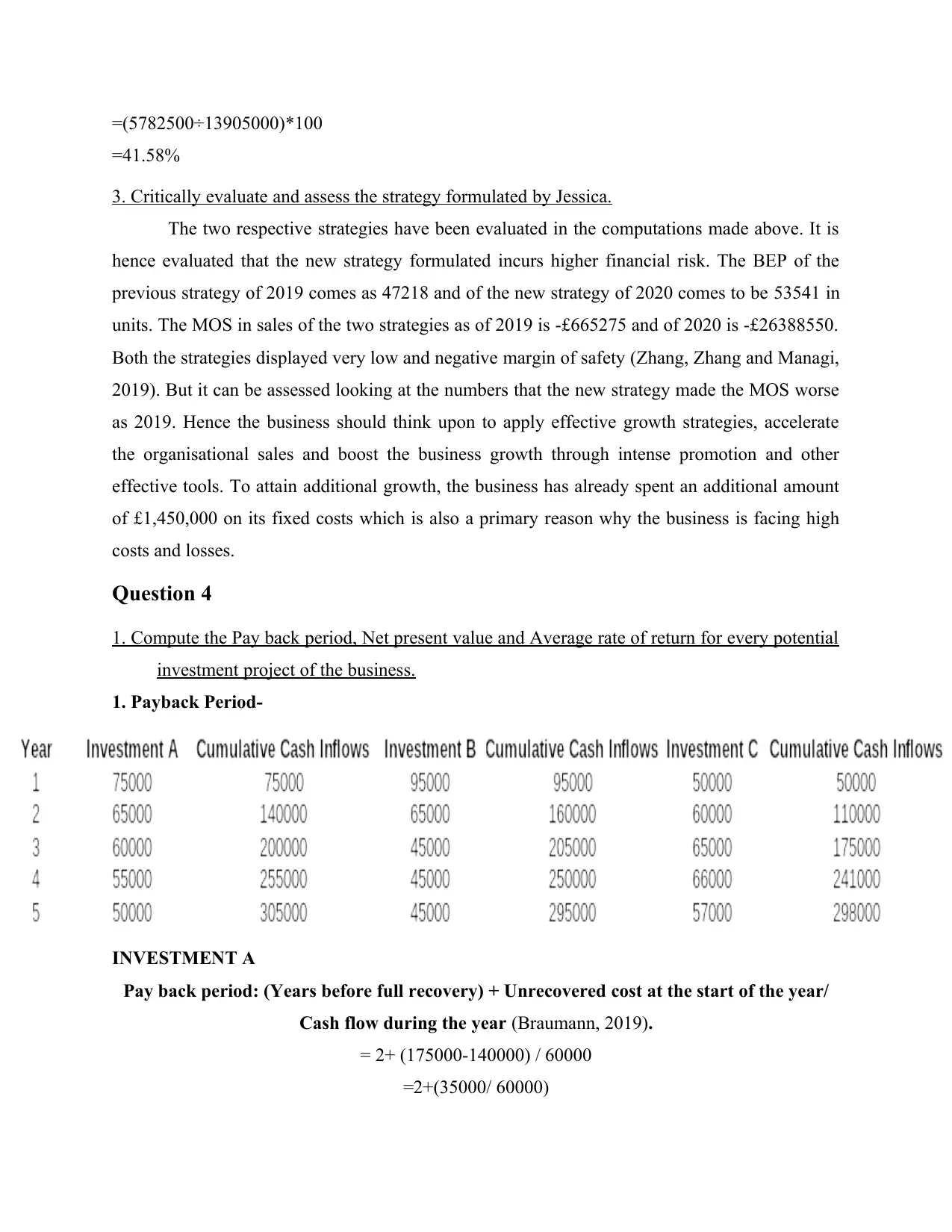

1. Payback Period-

INVESTMENT A

Pay back period: (Years before full recovery) + Unrecovered cost at the start of the year/

Cash flow during the year (Braumann, 2019).

= 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=41.58%

3. Critically evaluate and assess the strategy formulated by Jessica.

The two respective strategies have been evaluated in the computations made above. It is

hence evaluated that the new strategy formulated incurs higher financial risk. The BEP of the

previous strategy of 2019 comes as 47218 and of the new strategy of 2020 comes to be 53541 in

units. The MOS in sales of the two strategies as of 2019 is -£665275 and of 2020 is -£26388550.

Both the strategies displayed very low and negative margin of safety (Zhang, Zhang and Managi,

2019). But it can be assessed looking at the numbers that the new strategy made the MOS worse

as 2019. Hence the business should think upon to apply effective growth strategies, accelerate

the organisational sales and boost the business growth through intense promotion and other

effective tools. To attain additional growth, the business has already spent an additional amount

of £1,450,000 on its fixed costs which is also a primary reason why the business is facing high

costs and losses.

Question 4

1. Compute the Pay back period, Net present value and Average rate of return for every potential

investment project of the business.

1. Payback Period-

INVESTMENT A

Pay back period: (Years before full recovery) + Unrecovered cost at the start of the year/

Cash flow during the year (Braumann, 2019).

= 2+ (175000-140000) / 60000

=2+(35000/ 60000)

=2+0.58

=2.58 years

INVESTMENT B

Pay back period: (Years before full recovery) + Unrecovered cost at the start of the year/

Cash flow during the year

=2 + (195000 – 160000) / 45000

=2+(35000 / 450000)

=2+0.77

=2.77 years

INVESTMENT C

Pay back period: (Years before full recovery) + Unrecovered cost at the start of the year/

Cash flow during the year

= 3 +(190000-1750000 / 66000

= 3+(15000 / 66000)

=3+0.22

=3.22 years

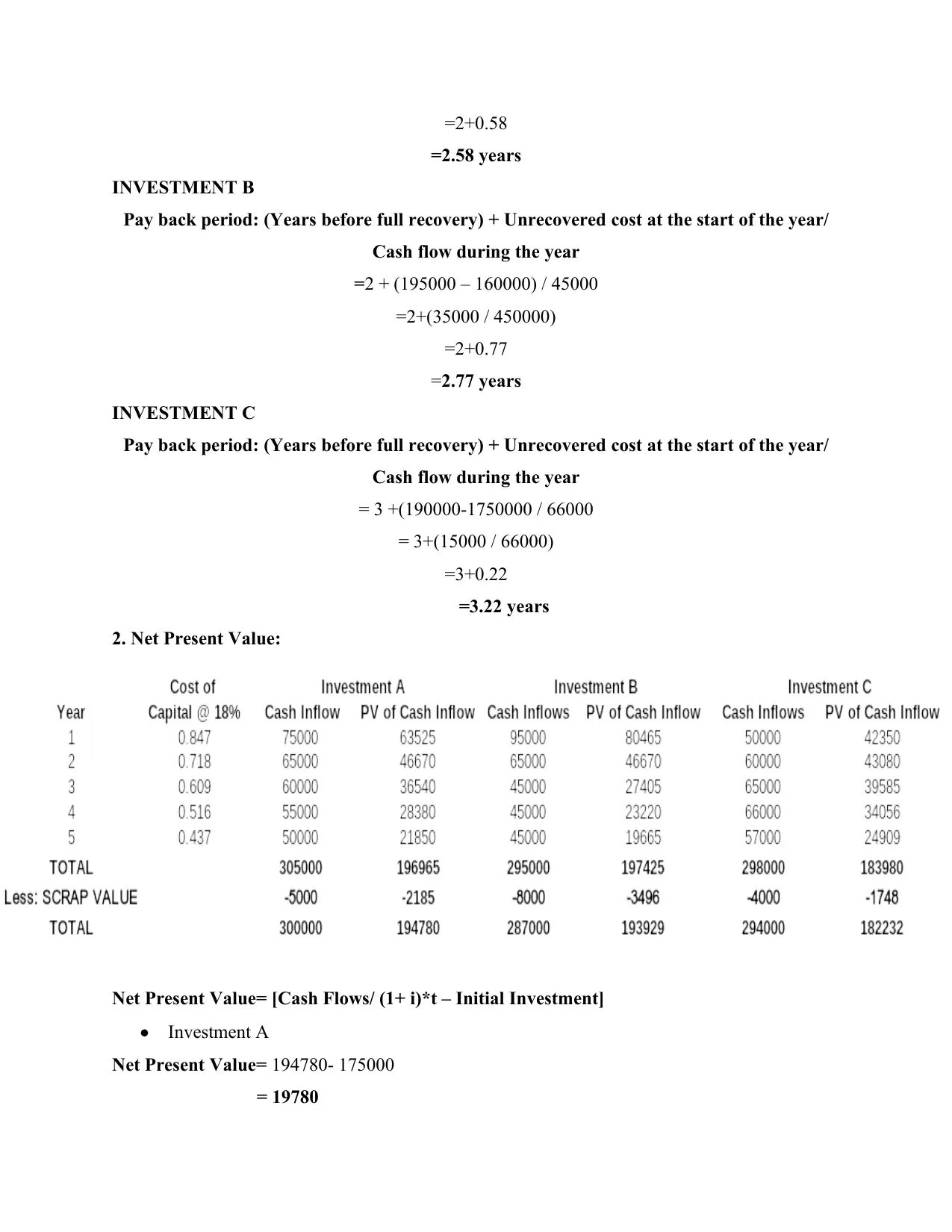

2. Net Present Value:

Net Present Value= [Cash Flows/ (1+ i)*t – Initial Investment]

Investment A

Net Present Value= 194780- 175000

= 19780

=2.58 years

INVESTMENT B

Pay back period: (Years before full recovery) + Unrecovered cost at the start of the year/

Cash flow during the year

=2 + (195000 – 160000) / 45000

=2+(35000 / 450000)

=2+0.77

=2.77 years

INVESTMENT C

Pay back period: (Years before full recovery) + Unrecovered cost at the start of the year/

Cash flow during the year

= 3 +(190000-1750000 / 66000

= 3+(15000 / 66000)

=3+0.22

=3.22 years

2. Net Present Value:

Net Present Value= [Cash Flows/ (1+ i)*t – Initial Investment]

Investment A

Net Present Value= 194780- 175000

= 19780

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.