Financial Management: Investment Appraisal Techniques and KADLex PLC

VerifiedAdded on 2022/12/30

|15

|3662

|92

Report

AI Summary

This report provides a detailed analysis of investment appraisal techniques, including the payback period, accounting rate of return, net present value, and internal rate of return, to evaluate the economic feasibility of acquiring a machine. It also explores valuation methods such as the price/earnings ratio, discounted cash flow method, and dividend valuation method, recommending their use for KADLex PLC's acquisition. The report discusses the benefits and limitations of each technique, offering a comprehensive overview of financial management principles and their application in investment decisions and mergers. Desklib provides students access to a wealth of solved assignments and past papers for further study.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

a) Calculate using the following investment appraisal techniques, and provide brief

recommendations as to the economic feasibility of acquiring the machine................................3

b) Evaluate the benefits and limitations of each of the differing investment appraisal

techniques....................................................................................................................................6

Task 2...............................................................................................................................................8

a) Price/ earnings ratio................................................................................................................8

b) Discounted cash flow method.................................................................................................8

c) Dividend Valuation Method....................................................................................................9

d) Discuss the problems associated with using the above valuation techniques and recommend

with economic justifications to the board of KADLex PLC to use in this acquisition.............10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

a) Calculate using the following investment appraisal techniques, and provide brief

recommendations as to the economic feasibility of acquiring the machine................................3

b) Evaluate the benefits and limitations of each of the differing investment appraisal

techniques....................................................................................................................................6

Task 2...............................................................................................................................................8

a) Price/ earnings ratio................................................................................................................8

b) Discounted cash flow method.................................................................................................8

c) Dividend Valuation Method....................................................................................................9

d) Discuss the problems associated with using the above valuation techniques and recommend

with economic justifications to the board of KADLex PLC to use in this acquisition.............10

CONCLUSION .............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial management is an essential aspect for the organisation that facilitates planning,

controlling, organising, evaluating and managing its financial resources. These are the activities

performed by the financial manager for achieving the goals and objectives of the firm. It helps in

making financial decisions and managing the scares financial resources of the firm and their

optimum utilisation. The main objective of financial management is to maximise organisation's

value. The three major decision making involved in are the investment decision, financing

decision and dividend decision. This report includes Investment Appraisal techniques which

aims in evaluating the economic feasibility of an investment plan. Investment Appraisal is an

investigation and examination done by the company for assessing the profitability of an

investment plan across the useful life of the asset in consideration with its affordability and

strategic fit (Bleoca, 2016). It helps the businesses in estimating the attractiveness of the

investments or the projects based on the results of various techniques of capital budgeting and

financing. It also includes different valuation methods which are used by the firms in case of

mergers and takeovers. These valuation techniques are used for valuing the organisation's net

worth at the time of mergers and acquisition.

TASK 1

a) Calculate using the following investment appraisal techniques, and provide brief

recommendations as to the economic feasibility of acquiring the machine.

i. The Payback Period

Payback period refers to the amount of time which is expected to recover the cost of

investment. It is like a break even point of investment (Buckle and Thompson, 2020). Therefore,

shorter the payback period is, better it is considered and the investment with shorter payback

would be more attractive and considered better in economic feasibility.

Payback Period Method

Cash outflow for the value of the machine = 2,75,000 320000

Year Cash Inflow Net Cash Flow

Financial management is an essential aspect for the organisation that facilitates planning,

controlling, organising, evaluating and managing its financial resources. These are the activities

performed by the financial manager for achieving the goals and objectives of the firm. It helps in

making financial decisions and managing the scares financial resources of the firm and their

optimum utilisation. The main objective of financial management is to maximise organisation's

value. The three major decision making involved in are the investment decision, financing

decision and dividend decision. This report includes Investment Appraisal techniques which

aims in evaluating the economic feasibility of an investment plan. Investment Appraisal is an

investigation and examination done by the company for assessing the profitability of an

investment plan across the useful life of the asset in consideration with its affordability and

strategic fit (Bleoca, 2016). It helps the businesses in estimating the attractiveness of the

investments or the projects based on the results of various techniques of capital budgeting and

financing. It also includes different valuation methods which are used by the firms in case of

mergers and takeovers. These valuation techniques are used for valuing the organisation's net

worth at the time of mergers and acquisition.

TASK 1

a) Calculate using the following investment appraisal techniques, and provide brief

recommendations as to the economic feasibility of acquiring the machine.

i. The Payback Period

Payback period refers to the amount of time which is expected to recover the cost of

investment. It is like a break even point of investment (Buckle and Thompson, 2020). Therefore,

shorter the payback period is, better it is considered and the investment with shorter payback

would be more attractive and considered better in economic feasibility.

Payback Period Method

Cash outflow for the value of the machine = 2,75,000 320000

Year Cash Inflow Net Cash Flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

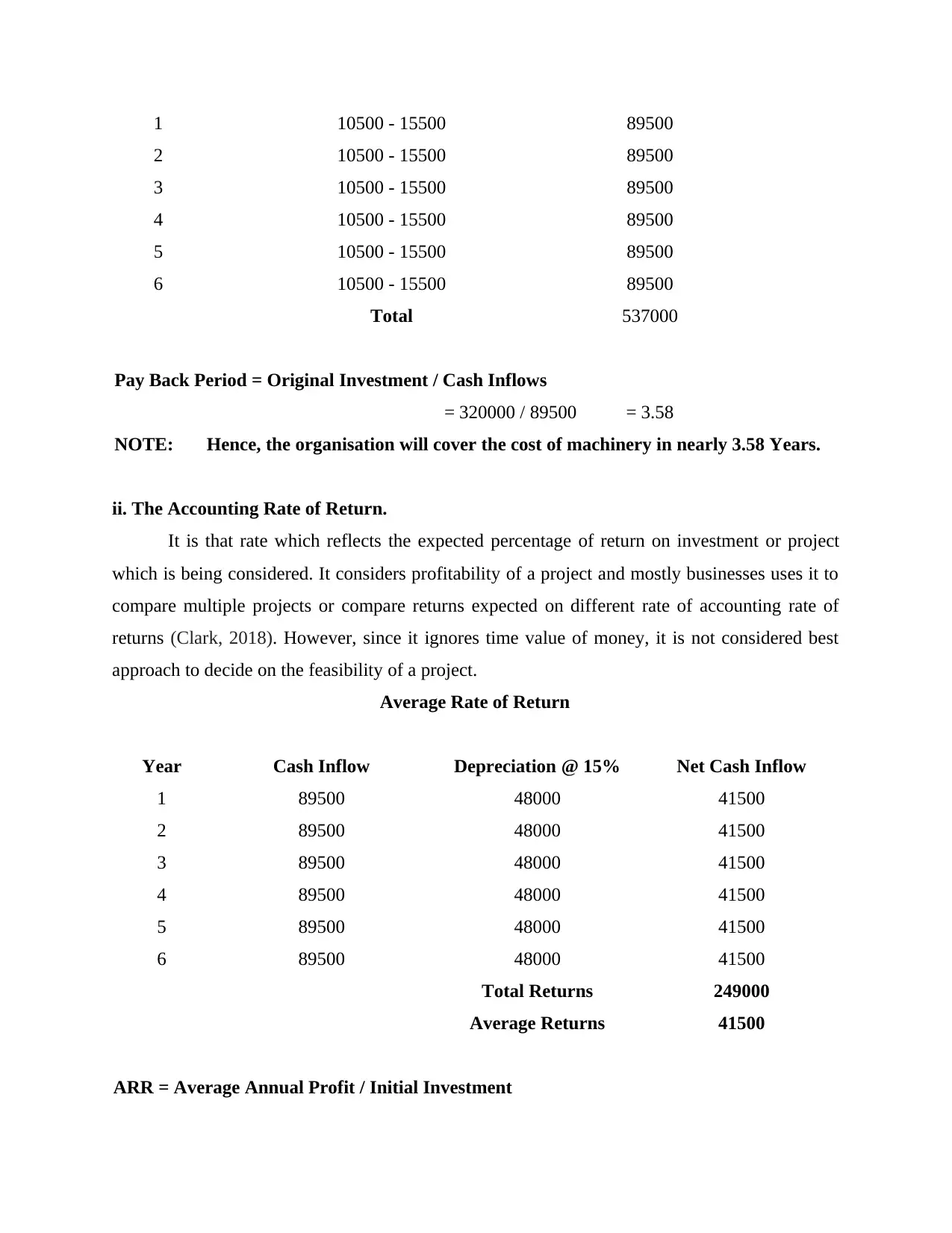

1 10500 - 15500 89500

2 10500 - 15500 89500

3 10500 - 15500 89500

4 10500 - 15500 89500

5 10500 - 15500 89500

6 10500 - 15500 89500

Total 537000

Pay Back Period = Original Investment / Cash Inflows

= 320000 / 89500 = 3.58

NOTE: Hence, the organisation will cover the cost of machinery in nearly 3.58 Years.

ii. The Accounting Rate of Return.

It is that rate which reflects the expected percentage of return on investment or project

which is being considered. It considers profitability of a project and mostly businesses uses it to

compare multiple projects or compare returns expected on different rate of accounting rate of

returns (Clark, 2018). However, since it ignores time value of money, it is not considered best

approach to decide on the feasibility of a project.

Average Rate of Return

Year Cash Inflow Depreciation @ 15% Net Cash Inflow

1 89500 48000 41500

2 89500 48000 41500

3 89500 48000 41500

4 89500 48000 41500

5 89500 48000 41500

6 89500 48000 41500

Total Returns 249000

Average Returns 41500

ARR = Average Annual Profit / Initial Investment

2 10500 - 15500 89500

3 10500 - 15500 89500

4 10500 - 15500 89500

5 10500 - 15500 89500

6 10500 - 15500 89500

Total 537000

Pay Back Period = Original Investment / Cash Inflows

= 320000 / 89500 = 3.58

NOTE: Hence, the organisation will cover the cost of machinery in nearly 3.58 Years.

ii. The Accounting Rate of Return.

It is that rate which reflects the expected percentage of return on investment or project

which is being considered. It considers profitability of a project and mostly businesses uses it to

compare multiple projects or compare returns expected on different rate of accounting rate of

returns (Clark, 2018). However, since it ignores time value of money, it is not considered best

approach to decide on the feasibility of a project.

Average Rate of Return

Year Cash Inflow Depreciation @ 15% Net Cash Inflow

1 89500 48000 41500

2 89500 48000 41500

3 89500 48000 41500

4 89500 48000 41500

5 89500 48000 41500

6 89500 48000 41500

Total Returns 249000

Average Returns 41500

ARR = Average Annual Profit / Initial Investment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

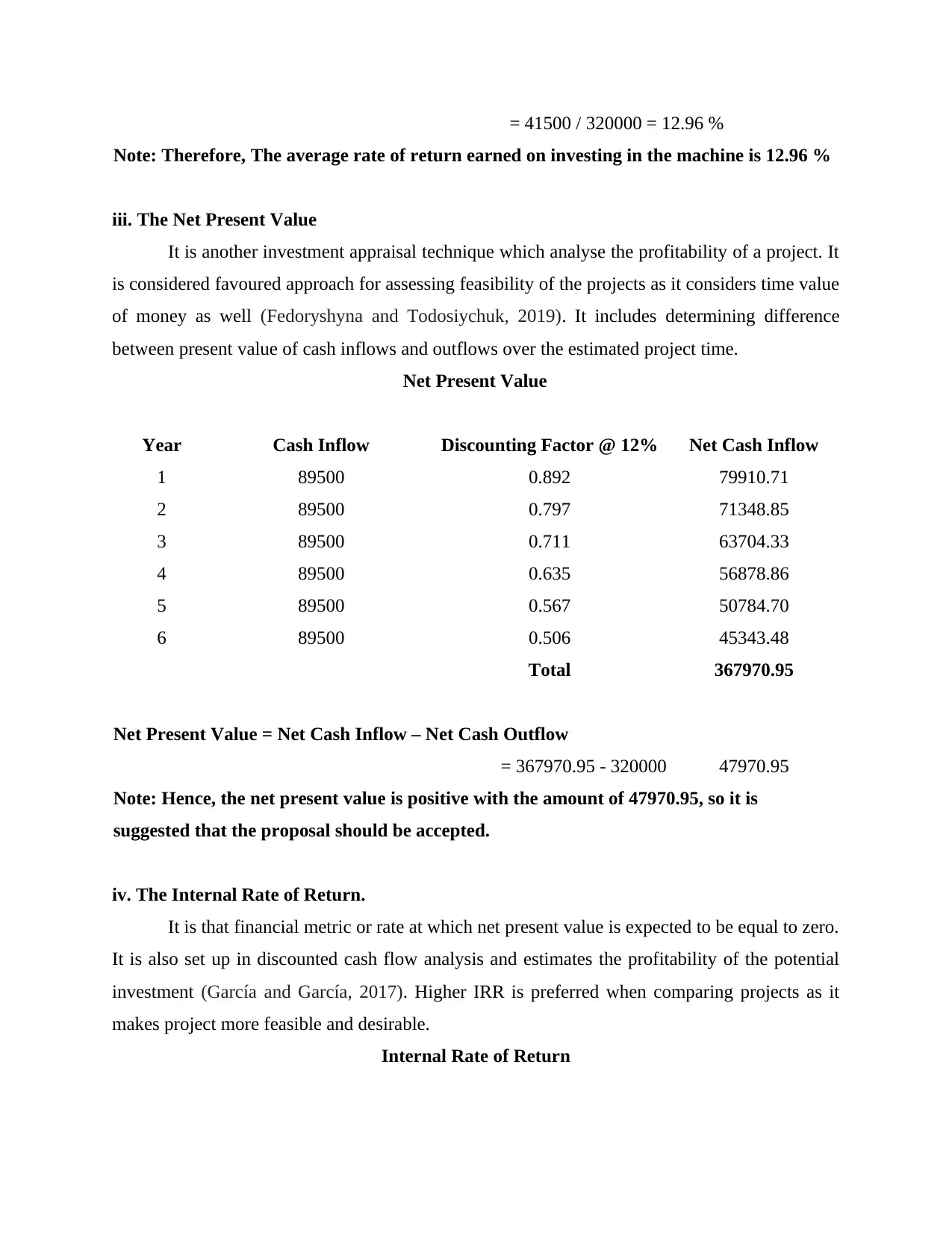

= 41500 / 320000 = 12.96 %

Note: Therefore, The average rate of return earned on investing in the machine is 12.96 %

iii. The Net Present Value

It is another investment appraisal technique which analyse the profitability of a project. It

is considered favoured approach for assessing feasibility of the projects as it considers time value

of money as well (Fedoryshyna and Todosiychuk, 2019). It includes determining difference

between present value of cash inflows and outflows over the estimated project time.

Net Present Value

Year Cash Inflow Discounting Factor @ 12% Net Cash Inflow

1 89500 0.892 79910.71

2 89500 0.797 71348.85

3 89500 0.711 63704.33

4 89500 0.635 56878.86

5 89500 0.567 50784.70

6 89500 0.506 45343.48

Total 367970.95

Net Present Value = Net Cash Inflow – Net Cash Outflow

= 367970.95 - 320000 47970.95

Note: Hence, the net present value is positive with the amount of 47970.95, so it is

suggested that the proposal should be accepted.

iv. The Internal Rate of Return.

It is that financial metric or rate at which net present value is expected to be equal to zero.

It is also set up in discounted cash flow analysis and estimates the profitability of the potential

investment (García and García, 2017). Higher IRR is preferred when comparing projects as it

makes project more feasible and desirable.

Internal Rate of Return

Note: Therefore, The average rate of return earned on investing in the machine is 12.96 %

iii. The Net Present Value

It is another investment appraisal technique which analyse the profitability of a project. It

is considered favoured approach for assessing feasibility of the projects as it considers time value

of money as well (Fedoryshyna and Todosiychuk, 2019). It includes determining difference

between present value of cash inflows and outflows over the estimated project time.

Net Present Value

Year Cash Inflow Discounting Factor @ 12% Net Cash Inflow

1 89500 0.892 79910.71

2 89500 0.797 71348.85

3 89500 0.711 63704.33

4 89500 0.635 56878.86

5 89500 0.567 50784.70

6 89500 0.506 45343.48

Total 367970.95

Net Present Value = Net Cash Inflow – Net Cash Outflow

= 367970.95 - 320000 47970.95

Note: Hence, the net present value is positive with the amount of 47970.95, so it is

suggested that the proposal should be accepted.

iv. The Internal Rate of Return.

It is that financial metric or rate at which net present value is expected to be equal to zero.

It is also set up in discounted cash flow analysis and estimates the profitability of the potential

investment (García and García, 2017). Higher IRR is preferred when comparing projects as it

makes project more feasible and desirable.

Internal Rate of Return

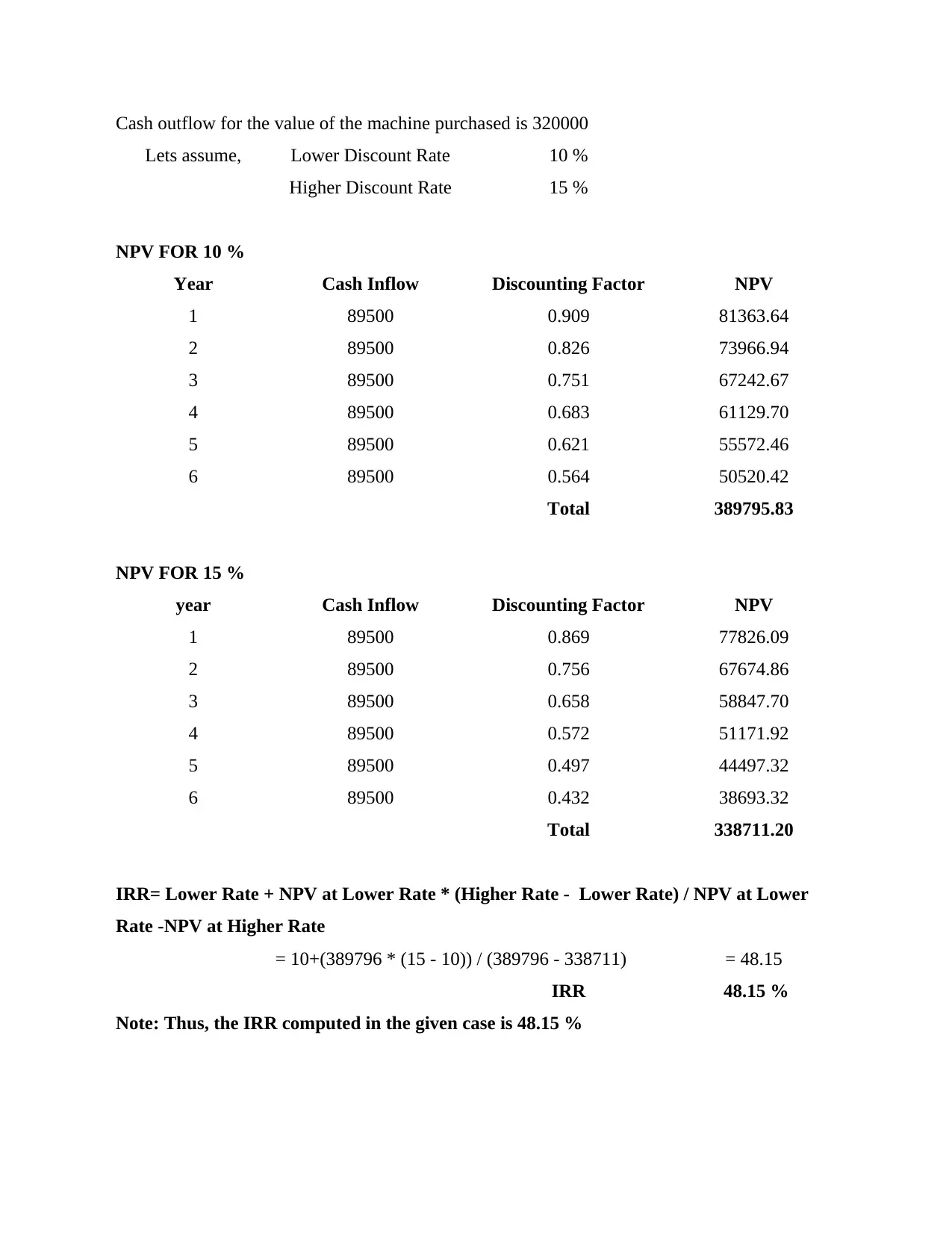

Cash outflow for the value of the machine purchased is 320000

Lets assume, Lower Discount Rate 10 %

Higher Discount Rate 15 %

NPV FOR 10 %

Year Cash Inflow Discounting Factor NPV

1 89500 0.909 81363.64

2 89500 0.826 73966.94

3 89500 0.751 67242.67

4 89500 0.683 61129.70

5 89500 0.621 55572.46

6 89500 0.564 50520.42

Total 389795.83

NPV FOR 15 %

year Cash Inflow Discounting Factor NPV

1 89500 0.869 77826.09

2 89500 0.756 67674.86

3 89500 0.658 58847.70

4 89500 0.572 51171.92

5 89500 0.497 44497.32

6 89500 0.432 38693.32

Total 338711.20

IRR= Lower Rate + NPV at Lower Rate * (Higher Rate - Lower Rate) / NPV at Lower

Rate -NPV at Higher Rate

= 10+(389796 * (15 - 10)) / (389796 - 338711) = 48.15

IRR 48.15 %

Note: Thus, the IRR computed in the given case is 48.15 %

Lets assume, Lower Discount Rate 10 %

Higher Discount Rate 15 %

NPV FOR 10 %

Year Cash Inflow Discounting Factor NPV

1 89500 0.909 81363.64

2 89500 0.826 73966.94

3 89500 0.751 67242.67

4 89500 0.683 61129.70

5 89500 0.621 55572.46

6 89500 0.564 50520.42

Total 389795.83

NPV FOR 15 %

year Cash Inflow Discounting Factor NPV

1 89500 0.869 77826.09

2 89500 0.756 67674.86

3 89500 0.658 58847.70

4 89500 0.572 51171.92

5 89500 0.497 44497.32

6 89500 0.432 38693.32

Total 338711.20

IRR= Lower Rate + NPV at Lower Rate * (Higher Rate - Lower Rate) / NPV at Lower

Rate -NPV at Higher Rate

= 10+(389796 * (15 - 10)) / (389796 - 338711) = 48.15

IRR 48.15 %

Note: Thus, the IRR computed in the given case is 48.15 %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) Evaluate the benefits and limitations of each of the differing investment appraisal techniques.

Payback Period

Payback period is relatively easier to understand and calculate as compared to the other

investment appraisal techniques. It requires very less inputs for calculation and requires

less assumptions to be made. It helps the organisation for making quick decisions for

utilisation of its limited resources (Lucas and Noordewier, 2016). It prefers for the

liquidity, as for small businesses it is important to quickly realise the cost of investment

for reinvesting it in other opportunities. It is beneficial for the industries having uncertain

and rapid technological changes as it reduces the chance of losses due to obsolescence.

The major disadvantage of it is that it does not consider the time value of money factor

which have a crucial importance in business concepts. It sometimes give unrealistic

results, as it does not consider normal business scenarios. Short term projects doesn't

guarantee profitability and ignores the rate of return earned on the project as it is suitable

only for the small businesses and does not provides a complete analysis in terms of

project attractiveness. In some cases cash flows are earned even after the completion of

payback period but this tool forsakes such cash flows.

Average Rate of Return

It is a simple and widely used tool of investment appraisal techniques that can be easily

understood by everyone. It facilitates in true evaluation of the profitability for the

investment as it considers all costs and revenues associated with the investment. It is

based on the accounting information, therefore no other reports are required for its

computation (Madura, 2020). It is based on the accounting profits thus measures

profitability of the investment. It helps in quick decision making as the project with

higher ARR is selected over the project with lower ARR.

It ignores the cash flows of the project, which are most important factor for a business

organisation. Also it does not take into account the terminal of the projects. It considers

all the costs and revenues associated with the investment over a period of time as the

equal value but ignores the reduction in the value of such cash flows. This technique does

not consider the impact of time value of money. This concept tells the worth of money

today, but is uncertain with the same amount of money that it would worth in future.

Net Present Value

Payback Period

Payback period is relatively easier to understand and calculate as compared to the other

investment appraisal techniques. It requires very less inputs for calculation and requires

less assumptions to be made. It helps the organisation for making quick decisions for

utilisation of its limited resources (Lucas and Noordewier, 2016). It prefers for the

liquidity, as for small businesses it is important to quickly realise the cost of investment

for reinvesting it in other opportunities. It is beneficial for the industries having uncertain

and rapid technological changes as it reduces the chance of losses due to obsolescence.

The major disadvantage of it is that it does not consider the time value of money factor

which have a crucial importance in business concepts. It sometimes give unrealistic

results, as it does not consider normal business scenarios. Short term projects doesn't

guarantee profitability and ignores the rate of return earned on the project as it is suitable

only for the small businesses and does not provides a complete analysis in terms of

project attractiveness. In some cases cash flows are earned even after the completion of

payback period but this tool forsakes such cash flows.

Average Rate of Return

It is a simple and widely used tool of investment appraisal techniques that can be easily

understood by everyone. It facilitates in true evaluation of the profitability for the

investment as it considers all costs and revenues associated with the investment. It is

based on the accounting information, therefore no other reports are required for its

computation (Madura, 2020). It is based on the accounting profits thus measures

profitability of the investment. It helps in quick decision making as the project with

higher ARR is selected over the project with lower ARR.

It ignores the cash flows of the project, which are most important factor for a business

organisation. Also it does not take into account the terminal of the projects. It considers

all the costs and revenues associated with the investment over a period of time as the

equal value but ignores the reduction in the value of such cash flows. This technique does

not consider the impact of time value of money. This concept tells the worth of money

today, but is uncertain with the same amount of money that it would worth in future.

Net Present Value

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The primary benefit of NPV is that it considers the impact of time value of money. The

computation of NPV by taking into consideration the discounted cash flows earned on an

investment for determining its viability (Mahpour and Mortaheb, 2018). It also helps the

management of the organisation in taking better decisions because it not only facilitates

evaluation of the size of the project but also helps in analysing the profit or loss making

capability of the project. Another major benefit of NPV is that it maximises the

organisation's earnings by investing in the ventures that ensures maximum returns.

The disadvantage of using NPV is that it is challenging for identifying the accurate

discount rate for representing the true risk premium of the investment. Another

disadvantage is that company may select the cost as per its convenience either too high or

too low, which results in misleading information that increases chances of loosing a

profitable opportunity or invest in the venture which is not worthwhile. The NPV

calculation is done on the basis of the discounting factor but there is no sat criteria for

calculating this rate. Also the NPV can only be used for the comparison of similar sized

projects, it can not be used of comparing projects of different sizes.

Internal Rate of Return

The most important benefit of IRR is that it considers the impact of time value of money

while evaluation of a project or investment. It is very simple to understand, compute and

interpret. There is no requirement of hurdle rate/ required rate for calculating IRR so the

risk of wrong and misleading results are minimised (Melnychenko, 2020). There is no

base or criteria for selection of any particular rate for IRR so there is a uniform ranking

system. Also in this method all the cash flows are given equal importance whether they

are earned earlier or later.

In this method economies of scale are being ignored as it does not consider the money

value of the benefits. There is no comparison as to which project is more worth. There are

unrealistic assumptions made like reinvestment of the profits earned on the investments at

the similar internal rate of return. It is not a better tool for comparing two or more

projects (Morris and Daley, 2017). Also it does not consider the size of the project, and

simply compares the amount of cash generated. In addition to this, it is only concerned

with projected cash flows and totally ignores the potential cost which can impact the

organisation's profitability.

computation of NPV by taking into consideration the discounted cash flows earned on an

investment for determining its viability (Mahpour and Mortaheb, 2018). It also helps the

management of the organisation in taking better decisions because it not only facilitates

evaluation of the size of the project but also helps in analysing the profit or loss making

capability of the project. Another major benefit of NPV is that it maximises the

organisation's earnings by investing in the ventures that ensures maximum returns.

The disadvantage of using NPV is that it is challenging for identifying the accurate

discount rate for representing the true risk premium of the investment. Another

disadvantage is that company may select the cost as per its convenience either too high or

too low, which results in misleading information that increases chances of loosing a

profitable opportunity or invest in the venture which is not worthwhile. The NPV

calculation is done on the basis of the discounting factor but there is no sat criteria for

calculating this rate. Also the NPV can only be used for the comparison of similar sized

projects, it can not be used of comparing projects of different sizes.

Internal Rate of Return

The most important benefit of IRR is that it considers the impact of time value of money

while evaluation of a project or investment. It is very simple to understand, compute and

interpret. There is no requirement of hurdle rate/ required rate for calculating IRR so the

risk of wrong and misleading results are minimised (Melnychenko, 2020). There is no

base or criteria for selection of any particular rate for IRR so there is a uniform ranking

system. Also in this method all the cash flows are given equal importance whether they

are earned earlier or later.

In this method economies of scale are being ignored as it does not consider the money

value of the benefits. There is no comparison as to which project is more worth. There are

unrealistic assumptions made like reinvestment of the profits earned on the investments at

the similar internal rate of return. It is not a better tool for comparing two or more

projects (Morris and Daley, 2017). Also it does not consider the size of the project, and

simply compares the amount of cash generated. In addition to this, it is only concerned

with projected cash flows and totally ignores the potential cost which can impact the

organisation's profitability.

Task 2

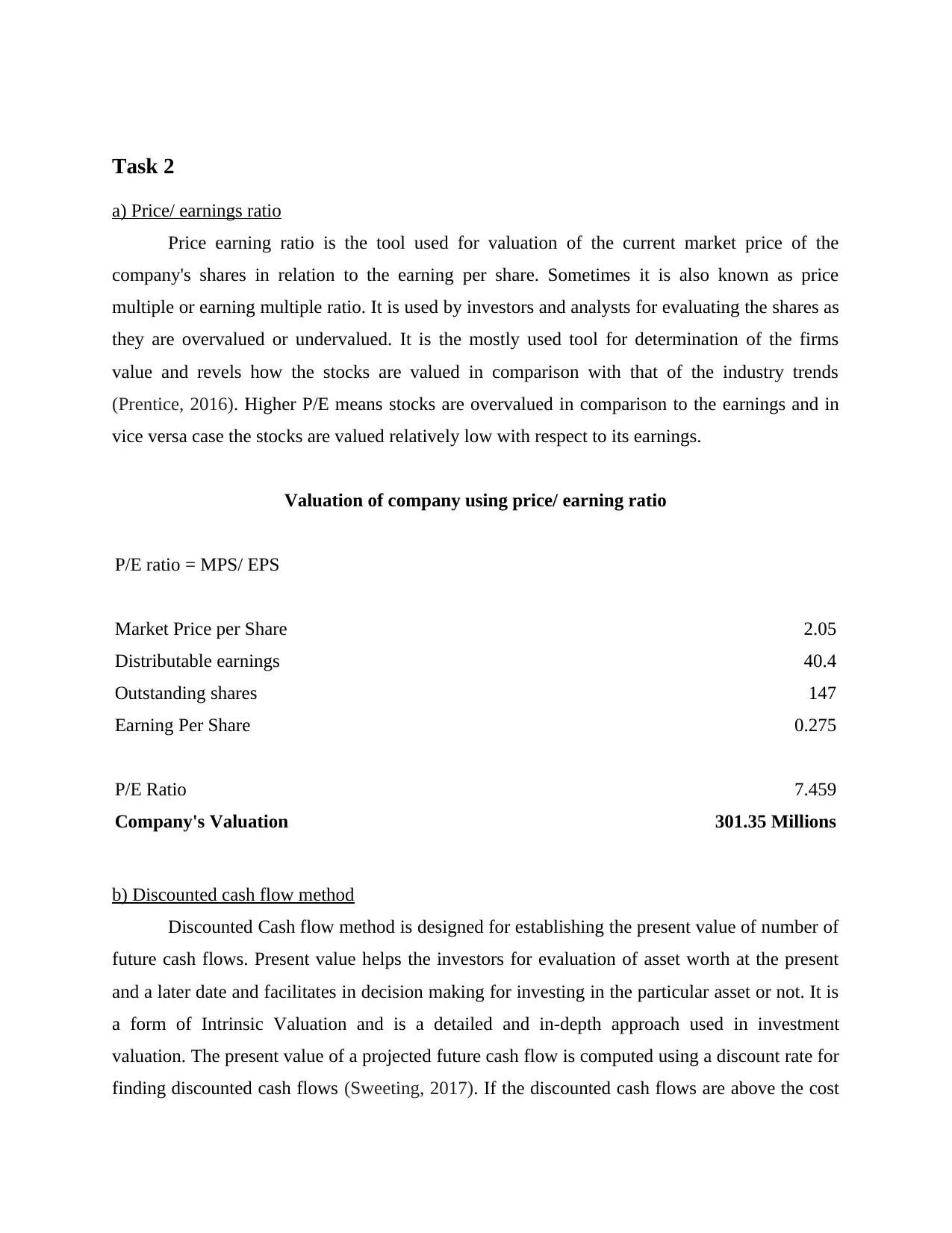

a) Price/ earnings ratio

Price earning ratio is the tool used for valuation of the current market price of the

company's shares in relation to the earning per share. Sometimes it is also known as price

multiple or earning multiple ratio. It is used by investors and analysts for evaluating the shares as

they are overvalued or undervalued. It is the mostly used tool for determination of the firms

value and revels how the stocks are valued in comparison with that of the industry trends

(Prentice, 2016). Higher P/E means stocks are overvalued in comparison to the earnings and in

vice versa case the stocks are valued relatively low with respect to its earnings.

Valuation of company using price/ earning ratio

P/E ratio = MPS/ EPS

Market Price per Share 2.05

Distributable earnings 40.4

Outstanding shares 147

Earning Per Share 0.275

P/E Ratio 7.459

Company's Valuation 301.35 Millions

b) Discounted cash flow method

Discounted Cash flow method is designed for establishing the present value of number of

future cash flows. Present value helps the investors for evaluation of asset worth at the present

and a later date and facilitates in decision making for investing in the particular asset or not. It is

a form of Intrinsic Valuation and is a detailed and in-depth approach used in investment

valuation. The present value of a projected future cash flow is computed using a discount rate for

finding discounted cash flows (Sweeting, 2017). If the discounted cash flows are above the cost

a) Price/ earnings ratio

Price earning ratio is the tool used for valuation of the current market price of the

company's shares in relation to the earning per share. Sometimes it is also known as price

multiple or earning multiple ratio. It is used by investors and analysts for evaluating the shares as

they are overvalued or undervalued. It is the mostly used tool for determination of the firms

value and revels how the stocks are valued in comparison with that of the industry trends

(Prentice, 2016). Higher P/E means stocks are overvalued in comparison to the earnings and in

vice versa case the stocks are valued relatively low with respect to its earnings.

Valuation of company using price/ earning ratio

P/E ratio = MPS/ EPS

Market Price per Share 2.05

Distributable earnings 40.4

Outstanding shares 147

Earning Per Share 0.275

P/E Ratio 7.459

Company's Valuation 301.35 Millions

b) Discounted cash flow method

Discounted Cash flow method is designed for establishing the present value of number of

future cash flows. Present value helps the investors for evaluation of asset worth at the present

and a later date and facilitates in decision making for investing in the particular asset or not. It is

a form of Intrinsic Valuation and is a detailed and in-depth approach used in investment

valuation. The present value of a projected future cash flow is computed using a discount rate for

finding discounted cash flows (Sweeting, 2017). If the discounted cash flows are above the cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

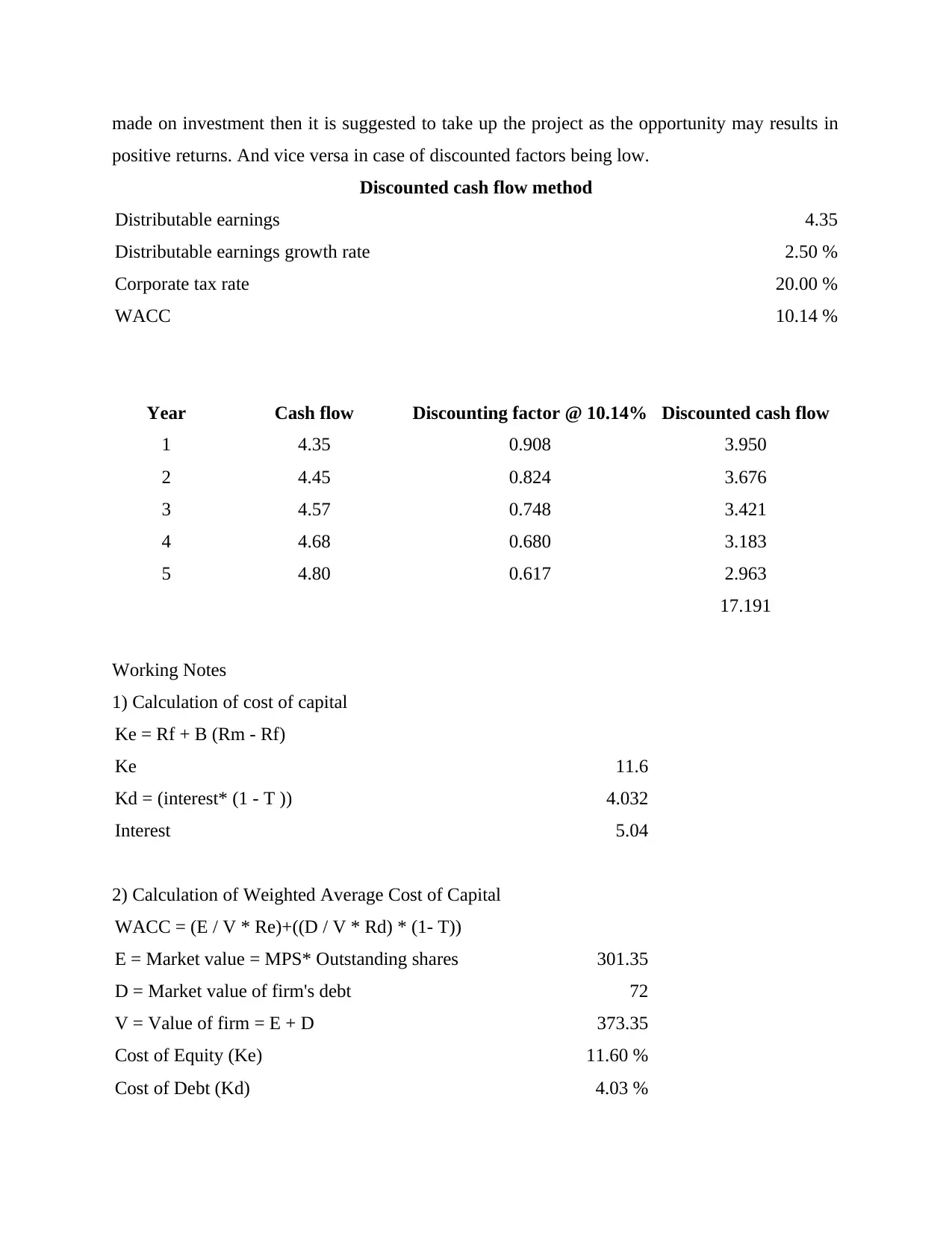

made on investment then it is suggested to take up the project as the opportunity may results in

positive returns. And vice versa in case of discounted factors being low.

Discounted cash flow method

Distributable earnings 4.35

Distributable earnings growth rate 2.50 %

Corporate tax rate 20.00 %

WACC 10.14 %

Year Cash flow Discounting factor @ 10.14% Discounted cash flow

1 4.35 0.908 3.950

2 4.45 0.824 3.676

3 4.57 0.748 3.421

4 4.68 0.680 3.183

5 4.80 0.617 2.963

17.191

Working Notes

1) Calculation of cost of capital

Ke = Rf + B (Rm - Rf)

Ke 11.6

Kd = (interest* (1 - T )) 4.032

Interest 5.04

2) Calculation of Weighted Average Cost of Capital

WACC = (E / V * Re)+((D / V * Rd) * (1- T))

E = Market value = MPS* Outstanding shares 301.35

D = Market value of firm's debt 72

V = Value of firm = E + D 373.35

Cost of Equity (Ke) 11.60 %

Cost of Debt (Kd) 4.03 %

positive returns. And vice versa in case of discounted factors being low.

Discounted cash flow method

Distributable earnings 4.35

Distributable earnings growth rate 2.50 %

Corporate tax rate 20.00 %

WACC 10.14 %

Year Cash flow Discounting factor @ 10.14% Discounted cash flow

1 4.35 0.908 3.950

2 4.45 0.824 3.676

3 4.57 0.748 3.421

4 4.68 0.680 3.183

5 4.80 0.617 2.963

17.191

Working Notes

1) Calculation of cost of capital

Ke = Rf + B (Rm - Rf)

Ke 11.6

Kd = (interest* (1 - T )) 4.032

Interest 5.04

2) Calculation of Weighted Average Cost of Capital

WACC = (E / V * Re)+((D / V * Rd) * (1- T))

E = Market value = MPS* Outstanding shares 301.35

D = Market value of firm's debt 72

V = Value of firm = E + D 373.35

Cost of Equity (Ke) 11.60 %

Cost of Debt (Kd) 4.03 %

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

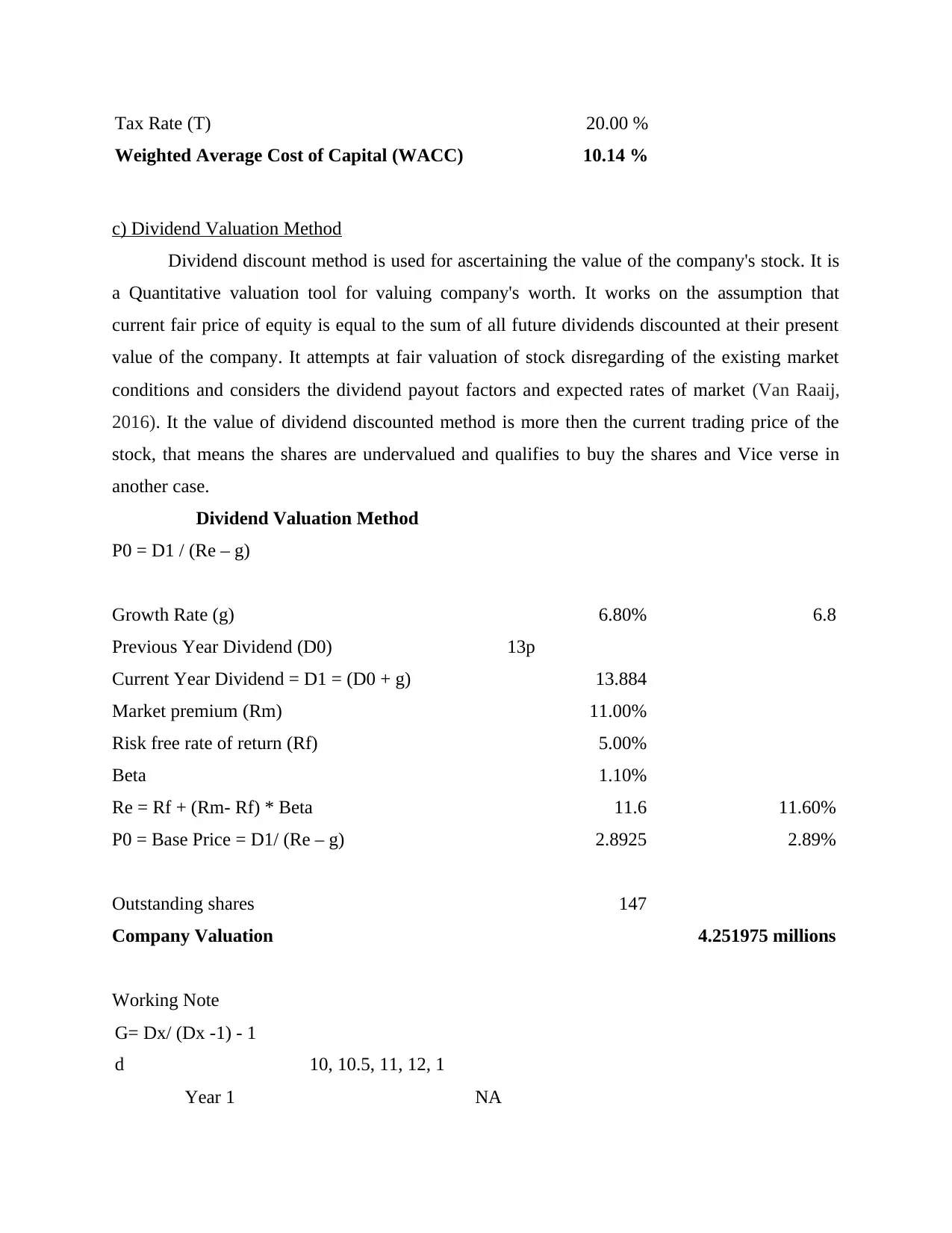

Tax Rate (T) 20.00 %

Weighted Average Cost of Capital (WACC) 10.14 %

c) Dividend Valuation Method

Dividend discount method is used for ascertaining the value of the company's stock. It is

a Quantitative valuation tool for valuing company's worth. It works on the assumption that

current fair price of equity is equal to the sum of all future dividends discounted at their present

value of the company. It attempts at fair valuation of stock disregarding of the existing market

conditions and considers the dividend payout factors and expected rates of market (Van Raaij,

2016). It the value of dividend discounted method is more then the current trading price of the

stock, that means the shares are undervalued and qualifies to buy the shares and Vice verse in

another case.

Dividend Valuation Method

P0 = D1 / (Re – g)

Growth Rate (g) 6.80% 6.8

Previous Year Dividend (D0) 13p

Current Year Dividend = D1 = (D0 + g) 13.884

Market premium (Rm) 11.00%

Risk free rate of return (Rf) 5.00%

Beta 1.10%

Re = Rf + (Rm- Rf) * Beta 11.6 11.60%

P0 = Base Price = D1/ (Re – g) 2.8925 2.89%

Outstanding shares 147

Company Valuation 4.251975 millions

Working Note

G= Dx/ (Dx -1) - 1

d 10, 10.5, 11, 12, 1

Year 1 NA

Weighted Average Cost of Capital (WACC) 10.14 %

c) Dividend Valuation Method

Dividend discount method is used for ascertaining the value of the company's stock. It is

a Quantitative valuation tool for valuing company's worth. It works on the assumption that

current fair price of equity is equal to the sum of all future dividends discounted at their present

value of the company. It attempts at fair valuation of stock disregarding of the existing market

conditions and considers the dividend payout factors and expected rates of market (Van Raaij,

2016). It the value of dividend discounted method is more then the current trading price of the

stock, that means the shares are undervalued and qualifies to buy the shares and Vice verse in

another case.

Dividend Valuation Method

P0 = D1 / (Re – g)

Growth Rate (g) 6.80% 6.8

Previous Year Dividend (D0) 13p

Current Year Dividend = D1 = (D0 + g) 13.884

Market premium (Rm) 11.00%

Risk free rate of return (Rf) 5.00%

Beta 1.10%

Re = Rf + (Rm- Rf) * Beta 11.6 11.60%

P0 = Base Price = D1/ (Re – g) 2.8925 2.89%

Outstanding shares 147

Company Valuation 4.251975 millions

Working Note

G= Dx/ (Dx -1) - 1

d 10, 10.5, 11, 12, 1

Year 1 NA

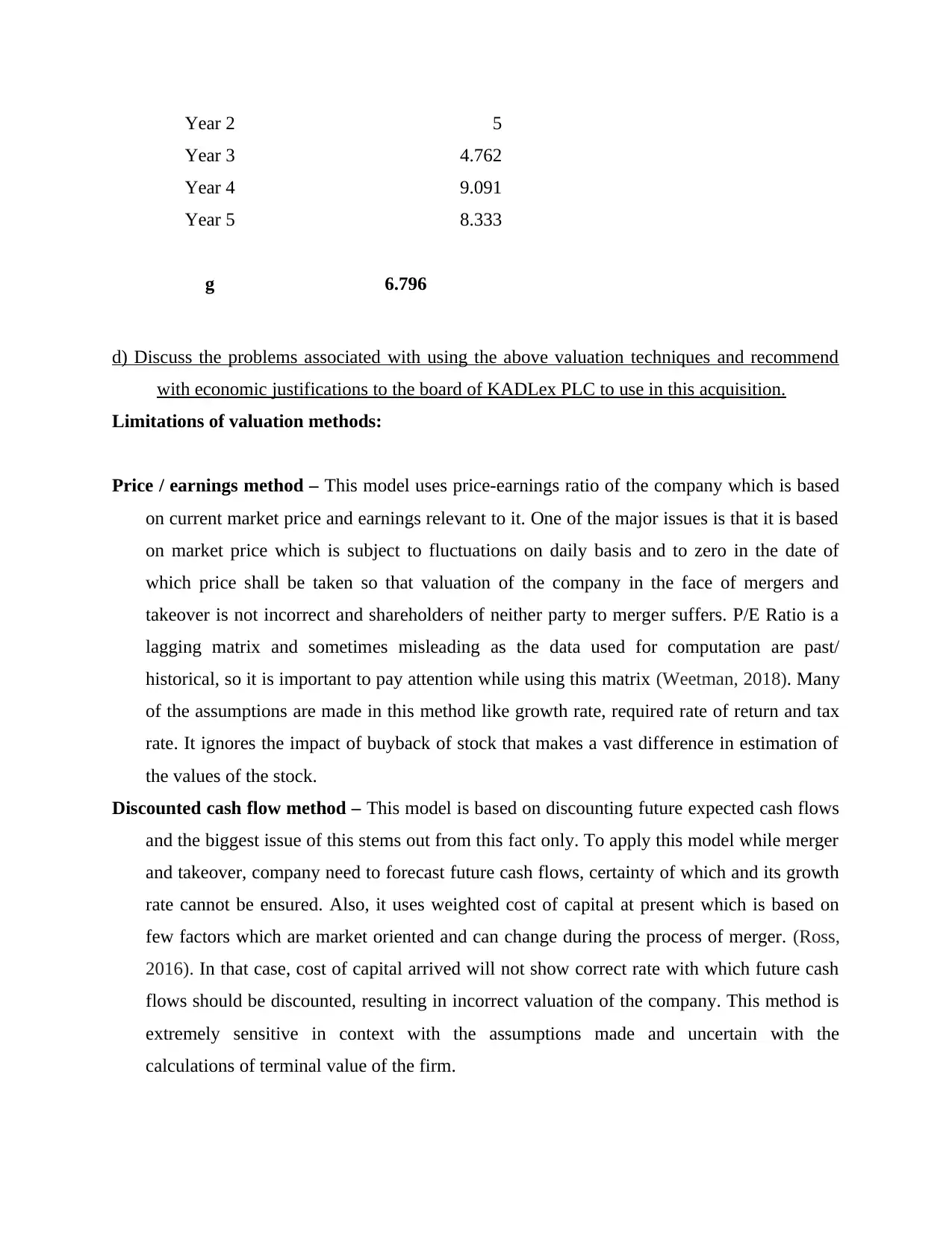

Year 2 5

Year 3 4.762

Year 4 9.091

Year 5 8.333

g 6.796

d) Discuss the problems associated with using the above valuation techniques and recommend

with economic justifications to the board of KADLex PLC to use in this acquisition.

Limitations of valuation methods:

Price / earnings method – This model uses price-earnings ratio of the company which is based

on current market price and earnings relevant to it. One of the major issues is that it is based

on market price which is subject to fluctuations on daily basis and to zero in the date of

which price shall be taken so that valuation of the company in the face of mergers and

takeover is not incorrect and shareholders of neither party to merger suffers. P/E Ratio is a

lagging matrix and sometimes misleading as the data used for computation are past/

historical, so it is important to pay attention while using this matrix (Weetman, 2018). Many

of the assumptions are made in this method like growth rate, required rate of return and tax

rate. It ignores the impact of buyback of stock that makes a vast difference in estimation of

the values of the stock.

Discounted cash flow method – This model is based on discounting future expected cash flows

and the biggest issue of this stems out from this fact only. To apply this model while merger

and takeover, company need to forecast future cash flows, certainty of which and its growth

rate cannot be ensured. Also, it uses weighted cost of capital at present which is based on

few factors which are market oriented and can change during the process of merger. (Ross,

2016). In that case, cost of capital arrived will not show correct rate with which future cash

flows should be discounted, resulting in incorrect valuation of the company. This method is

extremely sensitive in context with the assumptions made and uncertain with the

calculations of terminal value of the firm.

Year 3 4.762

Year 4 9.091

Year 5 8.333

g 6.796

d) Discuss the problems associated with using the above valuation techniques and recommend

with economic justifications to the board of KADLex PLC to use in this acquisition.

Limitations of valuation methods:

Price / earnings method – This model uses price-earnings ratio of the company which is based

on current market price and earnings relevant to it. One of the major issues is that it is based

on market price which is subject to fluctuations on daily basis and to zero in the date of

which price shall be taken so that valuation of the company in the face of mergers and

takeover is not incorrect and shareholders of neither party to merger suffers. P/E Ratio is a

lagging matrix and sometimes misleading as the data used for computation are past/

historical, so it is important to pay attention while using this matrix (Weetman, 2018). Many

of the assumptions are made in this method like growth rate, required rate of return and tax

rate. It ignores the impact of buyback of stock that makes a vast difference in estimation of

the values of the stock.

Discounted cash flow method – This model is based on discounting future expected cash flows

and the biggest issue of this stems out from this fact only. To apply this model while merger

and takeover, company need to forecast future cash flows, certainty of which and its growth

rate cannot be ensured. Also, it uses weighted cost of capital at present which is based on

few factors which are market oriented and can change during the process of merger. (Ross,

2016). In that case, cost of capital arrived will not show correct rate with which future cash

flows should be discounted, resulting in incorrect valuation of the company. This method is

extremely sensitive in context with the assumptions made and uncertain with the

calculations of terminal value of the firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.