Financial Management & Control Report: Ratio Analysis and Break-Even

VerifiedAdded on 2021/01/03

|17

|4831

|24

Report

AI Summary

This comprehensive financial management report analyzes the financial performance of Fridge-freezer Plc and Washbug Ltd. It begins with a board report evaluating profitability, liquidity, gearing, asset utilization, and investor potential ratios for Fridge-freezer Plc. The report then calculates and interprets the working capital cycle for the same company. Further, it explores the limitations of ratio analysis in both cross-sectional and time-series comparisons. The report then transitions to Task B, calculating the break-even point and margin of safety for Washbug Ltd for 2017 and 2018, followed by an evaluation of the break-even point model's assumptions. Finally, the report evaluates single sources of internal and external finance and assesses the benefits and limitations of various investment appraisal techniques. The report provides a detailed analysis of financial statements and key financial metrics, offering insights into the companies' financial health and performance.

Financial Management

& Control

& Control

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1. Board Report of Fridge-freezer Plc:...................................................................................3

2. Working Capital Cycle in Days for Fridge-freezer Plc:.....................................................6

3. Limitations of Using Ratio Analysis for both Cross-Sectional and Time-Series

Comparisons:..........................................................................................................................7

TASK B...........................................................................................................................................9

1. Calculation of Break-even point and Margin of safety for the year 2017 and 2018 of

Washbug Ltd..........................................................................................................................9

2. Evaluation of key assumptions of break-even point model, assessing and analysing the

model within the context of today's global business environment.......................................10

PART C .........................................................................................................................................11

1. Evaluation of single source of both internal and external finance: .................................11

2. Evaluation of benefits and limitations of different investment appraisal techniques:......13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

1. Board Report of Fridge-freezer Plc:...................................................................................3

2. Working Capital Cycle in Days for Fridge-freezer Plc:.....................................................6

3. Limitations of Using Ratio Analysis for both Cross-Sectional and Time-Series

Comparisons:..........................................................................................................................7

TASK B...........................................................................................................................................9

1. Calculation of Break-even point and Margin of safety for the year 2017 and 2018 of

Washbug Ltd..........................................................................................................................9

2. Evaluation of key assumptions of break-even point model, assessing and analysing the

model within the context of today's global business environment.......................................10

PART C .........................................................................................................................................11

1. Evaluation of single source of both internal and external finance: .................................11

2. Evaluation of benefits and limitations of different investment appraisal techniques:......13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Financial management means evaluating the efficiency and effectiveness of the money

management. It focuses on ratio calculation, evaluating various investment proposals and taking

investment decisions. For better understanding of financial statements of the company it is very

important to evaluate and analyse ratios. If company want to make investments then they have to

evaluate various investments techniques like internal rate of return method, net present value

method, pay back period method, discounted pay back period method etc.

PART A

1. Board Report of Fridge-freezer Plc:

In this report, evaluation of various ratios is required which is helpful for the company

(Fridge-freezer Plc) for future planning of business. Which are as under:

Profitability Ratio:

Particulars 2017 2018

Gross Profit ratio (%) = 16040/29950*100

= 53.56

= 18760/38550*100

= 48.66

Net Profit ratio (%) = 9725/29950*100 = 5795/38550*100

Financial management means evaluating the efficiency and effectiveness of the money

management. It focuses on ratio calculation, evaluating various investment proposals and taking

investment decisions. For better understanding of financial statements of the company it is very

important to evaluate and analyse ratios. If company want to make investments then they have to

evaluate various investments techniques like internal rate of return method, net present value

method, pay back period method, discounted pay back period method etc.

PART A

1. Board Report of Fridge-freezer Plc:

In this report, evaluation of various ratios is required which is helpful for the company

(Fridge-freezer Plc) for future planning of business. Which are as under:

Profitability Ratio:

Particulars 2017 2018

Gross Profit ratio (%) = 16040/29950*100

= 53.56

= 18760/38550*100

= 48.66

Net Profit ratio (%) = 9725/29950*100 = 5795/38550*100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 32.47 = 15.03

Operating profit ratio (%) =10105/29950*100

= 33.74

= 7485/38550*100

= 19.42

Note: Gross profit ratio = Gross profit/sales*100

Net profit ratio = Net profit/sales*100

Operating profit ratio = Operating profit/sales*100

Comments: In profitability ratios, which are calculated above for two years. By analysis

of these, current profitability ratios are decreasing as compared to previous year. Fridge-freezer

Plc has not capable of being earn higher profits in all types of profits i.e. gross profit, net profit

and operating profits. It means that company incurred high costs as compared to income for

earning revenue for the year. One of reason is that company (Fridge-freezer Plc) has more

interest expenses in year 2018 as compared to previous year due to which its net profit is less

than previous year 2017. Although, there is a more gross profit in year 2018 than in year 2017

but it is not sufficient in context of revenue (Gatti, S., 2012).

Liquidity Ratio:

Particulars 2017 2018

Current Ratio = 8935/6375

= 1.4

= 12125/8480

= 1.43

Quick Ratio = 5060/6375

= 0.79

= 5900/8480

= 0.7

Note: Current ratio = current assets/current liabilities

Quick ratio = quick assets/current liabilities

Note: Quick assets is calculated after deducting closing inventories & prepaid expenses from

current assets.

Comments: In liquidity ratios, which are calculated above for year 2017 & 2018. By

analysis of these, current ratio is increasing as compared to year 2017. This means company has

more short term assets available to pay short term liabilities as compared to previous year (2017).

This is a sign of better utilisation of short term assets in business of Fridge-freezer Plc. But

Operating profit ratio (%) =10105/29950*100

= 33.74

= 7485/38550*100

= 19.42

Note: Gross profit ratio = Gross profit/sales*100

Net profit ratio = Net profit/sales*100

Operating profit ratio = Operating profit/sales*100

Comments: In profitability ratios, which are calculated above for two years. By analysis

of these, current profitability ratios are decreasing as compared to previous year. Fridge-freezer

Plc has not capable of being earn higher profits in all types of profits i.e. gross profit, net profit

and operating profits. It means that company incurred high costs as compared to income for

earning revenue for the year. One of reason is that company (Fridge-freezer Plc) has more

interest expenses in year 2018 as compared to previous year due to which its net profit is less

than previous year 2017. Although, there is a more gross profit in year 2018 than in year 2017

but it is not sufficient in context of revenue (Gatti, S., 2012).

Liquidity Ratio:

Particulars 2017 2018

Current Ratio = 8935/6375

= 1.4

= 12125/8480

= 1.43

Quick Ratio = 5060/6375

= 0.79

= 5900/8480

= 0.7

Note: Current ratio = current assets/current liabilities

Quick ratio = quick assets/current liabilities

Note: Quick assets is calculated after deducting closing inventories & prepaid expenses from

current assets.

Comments: In liquidity ratios, which are calculated above for year 2017 & 2018. By

analysis of these, current ratio is increasing as compared to year 2017. This means company has

more short term assets available to pay short term liabilities as compared to previous year (2017).

This is a sign of better utilisation of short term assets in business of Fridge-freezer Plc. But

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

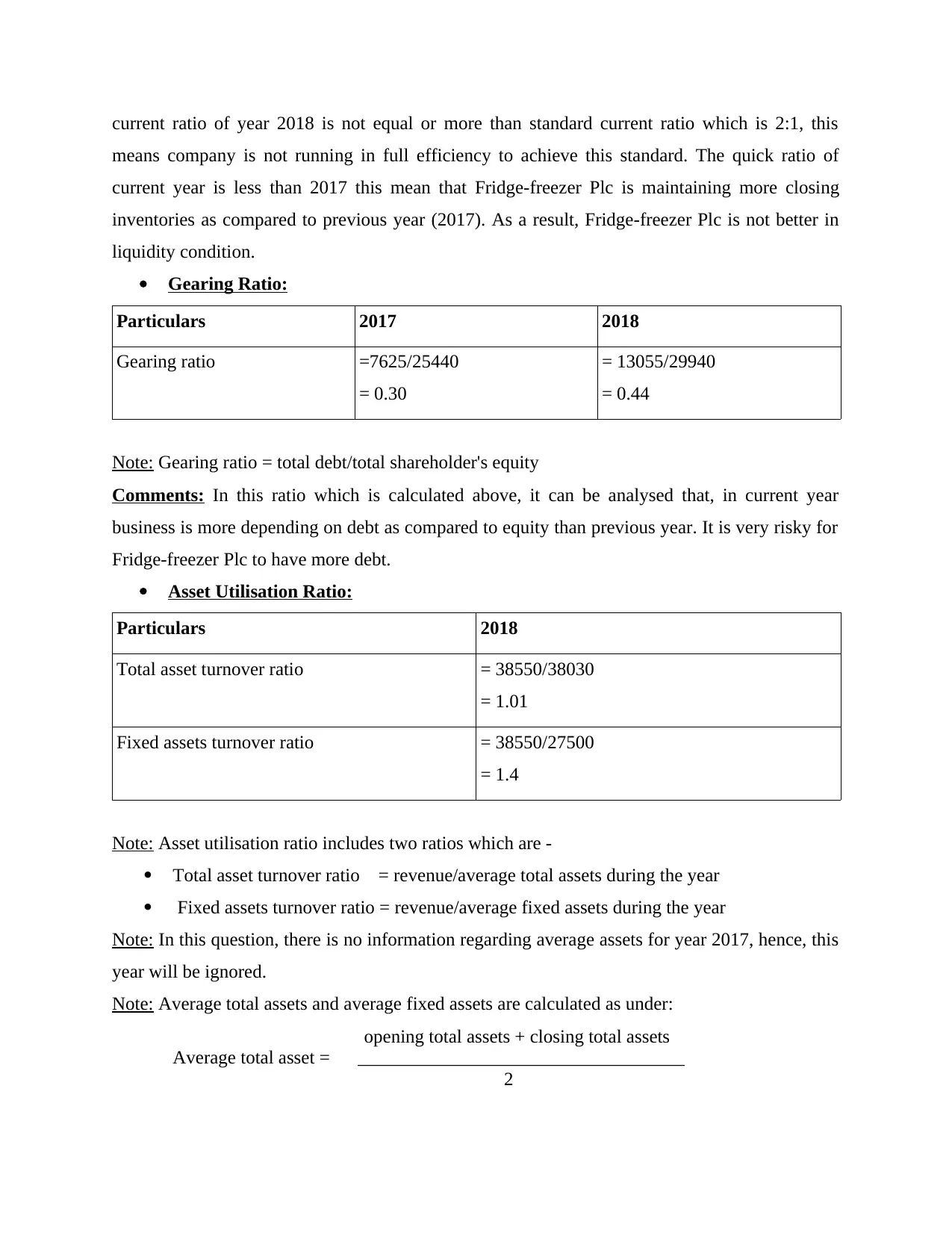

current ratio of year 2018 is not equal or more than standard current ratio which is 2:1, this

means company is not running in full efficiency to achieve this standard. The quick ratio of

current year is less than 2017 this mean that Fridge-freezer Plc is maintaining more closing

inventories as compared to previous year (2017). As a result, Fridge-freezer Plc is not better in

liquidity condition.

Gearing Ratio:

Particulars 2017 2018

Gearing ratio =7625/25440

= 0.30

= 13055/29940

= 0.44

Note: Gearing ratio = total debt/total shareholder's equity

Comments: In this ratio which is calculated above, it can be analysed that, in current year

business is more depending on debt as compared to equity than previous year. It is very risky for

Fridge-freezer Plc to have more debt.

Asset Utilisation Ratio:

Particulars 2018

Total asset turnover ratio = 38550/38030

= 1.01

Fixed assets turnover ratio = 38550/27500

= 1.4

Note: Asset utilisation ratio includes two ratios which are -

Total asset turnover ratio = revenue/average total assets during the year

Fixed assets turnover ratio = revenue/average fixed assets during the year

Note: In this question, there is no information regarding average assets for year 2017, hence, this

year will be ignored.

Note: Average total assets and average fixed assets are calculated as under:

opening total assets + closing total assets

Average total asset = ___________________________________

2

means company is not running in full efficiency to achieve this standard. The quick ratio of

current year is less than 2017 this mean that Fridge-freezer Plc is maintaining more closing

inventories as compared to previous year (2017). As a result, Fridge-freezer Plc is not better in

liquidity condition.

Gearing Ratio:

Particulars 2017 2018

Gearing ratio =7625/25440

= 0.30

= 13055/29940

= 0.44

Note: Gearing ratio = total debt/total shareholder's equity

Comments: In this ratio which is calculated above, it can be analysed that, in current year

business is more depending on debt as compared to equity than previous year. It is very risky for

Fridge-freezer Plc to have more debt.

Asset Utilisation Ratio:

Particulars 2018

Total asset turnover ratio = 38550/38030

= 1.01

Fixed assets turnover ratio = 38550/27500

= 1.4

Note: Asset utilisation ratio includes two ratios which are -

Total asset turnover ratio = revenue/average total assets during the year

Fixed assets turnover ratio = revenue/average fixed assets during the year

Note: In this question, there is no information regarding average assets for year 2017, hence, this

year will be ignored.

Note: Average total assets and average fixed assets are calculated as under:

opening total assets + closing total assets

Average total asset = ___________________________________

2

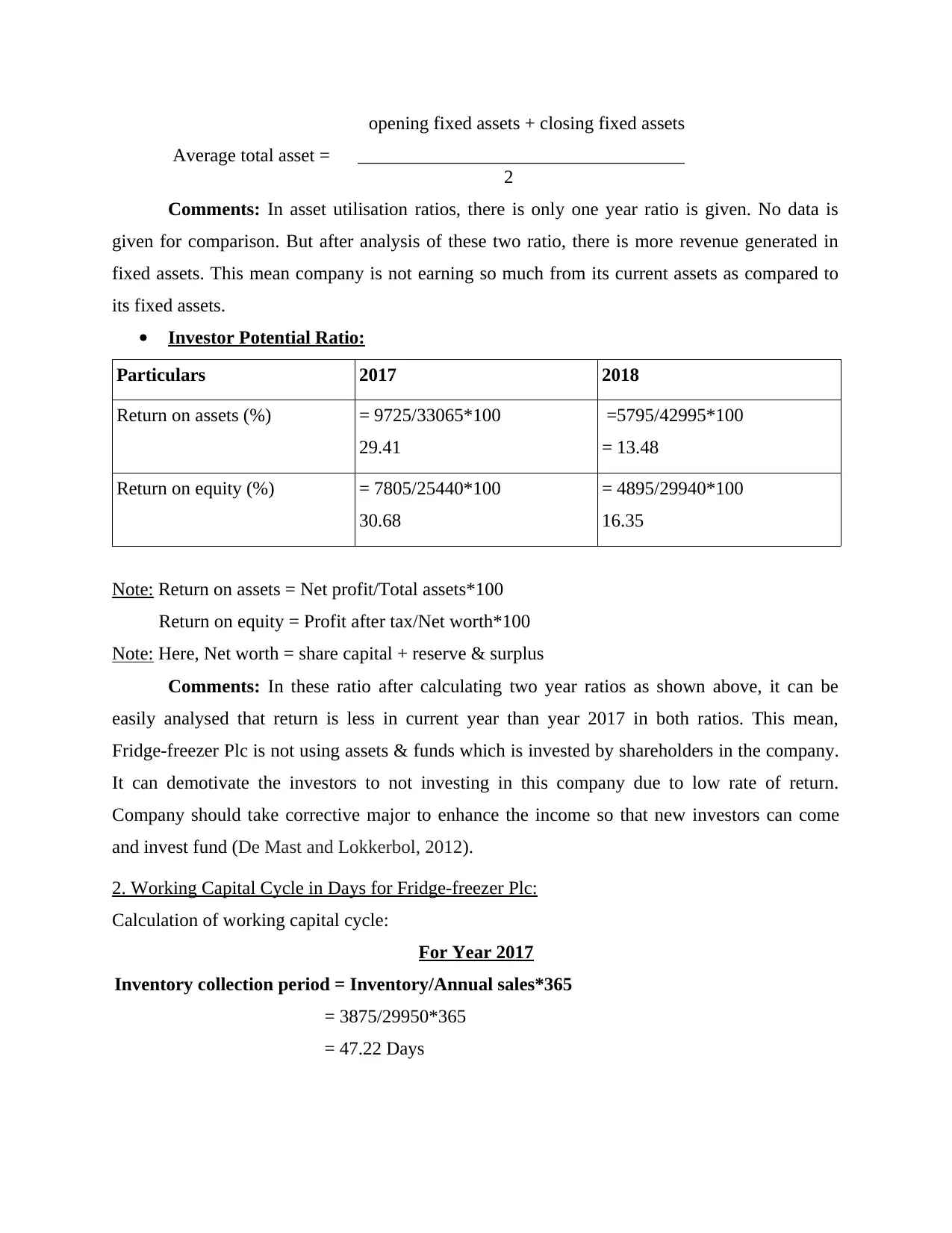

opening fixed assets + closing fixed assets

Average total asset = ___________________________________

2

Comments: In asset utilisation ratios, there is only one year ratio is given. No data is

given for comparison. But after analysis of these two ratio, there is more revenue generated in

fixed assets. This mean company is not earning so much from its current assets as compared to

its fixed assets.

Investor Potential Ratio:

Particulars 2017 2018

Return on assets (%) = 9725/33065*100

29.41

=5795/42995*100

= 13.48

Return on equity (%) = 7805/25440*100

30.68

= 4895/29940*100

16.35

Note: Return on assets = Net profit/Total assets*100

Return on equity = Profit after tax/Net worth*100

Note: Here, Net worth = share capital + reserve & surplus

Comments: In these ratio after calculating two year ratios as shown above, it can be

easily analysed that return is less in current year than year 2017 in both ratios. This mean,

Fridge-freezer Plc is not using assets & funds which is invested by shareholders in the company.

It can demotivate the investors to not investing in this company due to low rate of return.

Company should take corrective major to enhance the income so that new investors can come

and invest fund (De Mast and Lokkerbol, 2012).

2. Working Capital Cycle in Days for Fridge-freezer Plc:

Calculation of working capital cycle:

For Year 2017

Inventory collection period = Inventory/Annual sales*365

= 3875/29950*365

= 47.22 Days

Average total asset = ___________________________________

2

Comments: In asset utilisation ratios, there is only one year ratio is given. No data is

given for comparison. But after analysis of these two ratio, there is more revenue generated in

fixed assets. This mean company is not earning so much from its current assets as compared to

its fixed assets.

Investor Potential Ratio:

Particulars 2017 2018

Return on assets (%) = 9725/33065*100

29.41

=5795/42995*100

= 13.48

Return on equity (%) = 7805/25440*100

30.68

= 4895/29940*100

16.35

Note: Return on assets = Net profit/Total assets*100

Return on equity = Profit after tax/Net worth*100

Note: Here, Net worth = share capital + reserve & surplus

Comments: In these ratio after calculating two year ratios as shown above, it can be

easily analysed that return is less in current year than year 2017 in both ratios. This mean,

Fridge-freezer Plc is not using assets & funds which is invested by shareholders in the company.

It can demotivate the investors to not investing in this company due to low rate of return.

Company should take corrective major to enhance the income so that new investors can come

and invest fund (De Mast and Lokkerbol, 2012).

2. Working Capital Cycle in Days for Fridge-freezer Plc:

Calculation of working capital cycle:

For Year 2017

Inventory collection period = Inventory/Annual sales*365

= 3875/29950*365

= 47.22 Days

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

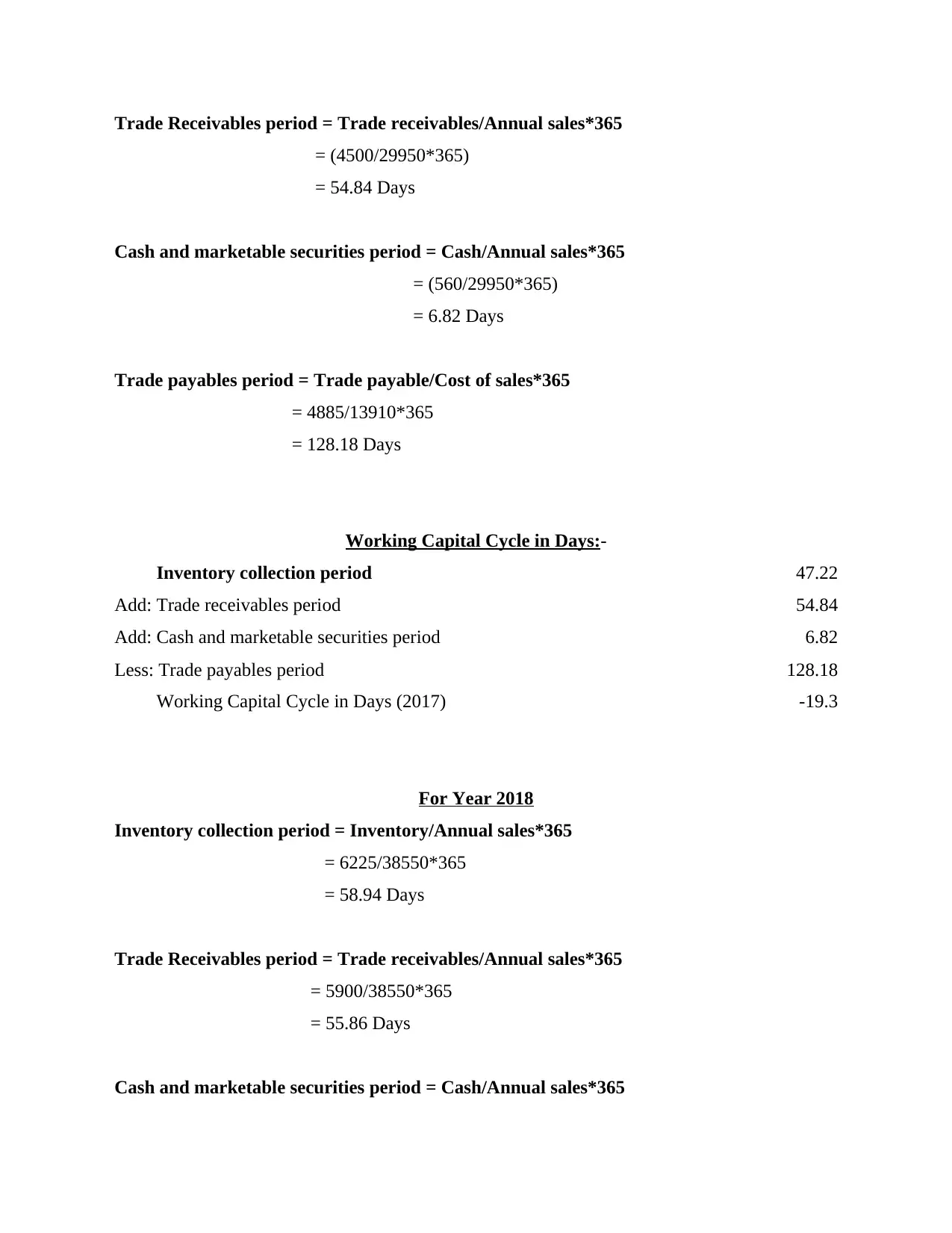

Trade Receivables period = Trade receivables/Annual sales*365

= (4500/29950*365)

= 54.84 Days

Cash and marketable securities period = Cash/Annual sales*365

= (560/29950*365)

= 6.82 Days

Trade payables period = Trade payable/Cost of sales*365

= 4885/13910*365

= 128.18 Days

Working Capital Cycle in Days:-

Inventory collection period 47.22

Add: Trade receivables period 54.84

Add: Cash and marketable securities period 6.82

Less: Trade payables period 128.18

Working Capital Cycle in Days (2017) -19.3

For Year 2018

Inventory collection period = Inventory/Annual sales*365

= 6225/38550*365

= 58.94 Days

Trade Receivables period = Trade receivables/Annual sales*365

= 5900/38550*365

= 55.86 Days

Cash and marketable securities period = Cash/Annual sales*365

= (4500/29950*365)

= 54.84 Days

Cash and marketable securities period = Cash/Annual sales*365

= (560/29950*365)

= 6.82 Days

Trade payables period = Trade payable/Cost of sales*365

= 4885/13910*365

= 128.18 Days

Working Capital Cycle in Days:-

Inventory collection period 47.22

Add: Trade receivables period 54.84

Add: Cash and marketable securities period 6.82

Less: Trade payables period 128.18

Working Capital Cycle in Days (2017) -19.3

For Year 2018

Inventory collection period = Inventory/Annual sales*365

= 6225/38550*365

= 58.94 Days

Trade Receivables period = Trade receivables/Annual sales*365

= 5900/38550*365

= 55.86 Days

Cash and marketable securities period = Cash/Annual sales*365

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

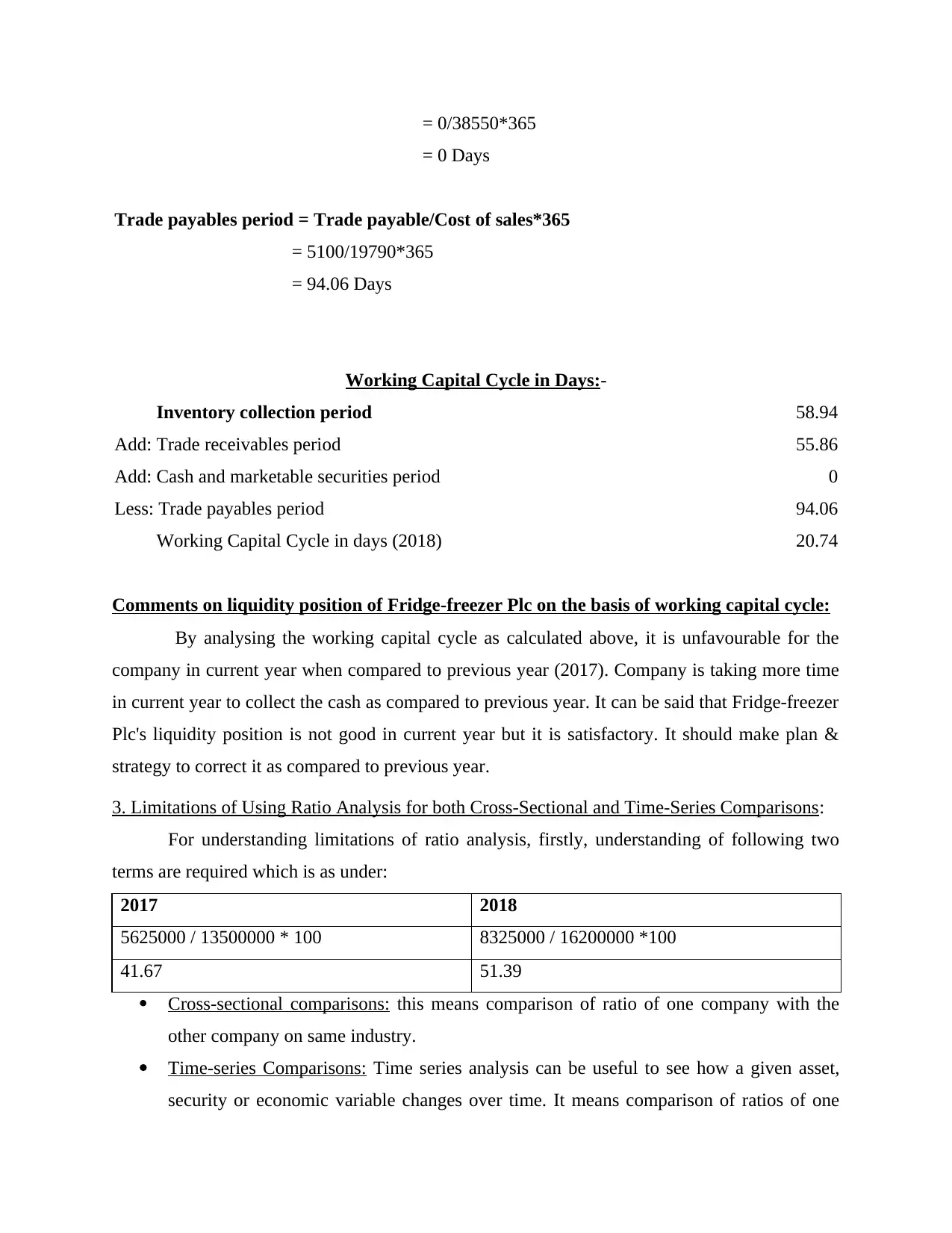

= 0/38550*365

= 0 Days

Trade payables period = Trade payable/Cost of sales*365

= 5100/19790*365

= 94.06 Days

Working Capital Cycle in Days:-

Inventory collection period 58.94

Add: Trade receivables period 55.86

Add: Cash and marketable securities period 0

Less: Trade payables period 94.06

Working Capital Cycle in days (2018) 20.74

Comments on liquidity position of Fridge-freezer Plc on the basis of working capital cycle:

By analysing the working capital cycle as calculated above, it is unfavourable for the

company in current year when compared to previous year (2017). Company is taking more time

in current year to collect the cash as compared to previous year. It can be said that Fridge-freezer

Plc's liquidity position is not good in current year but it is satisfactory. It should make plan &

strategy to correct it as compared to previous year.

3. Limitations of Using Ratio Analysis for both Cross-Sectional and Time-Series Comparisons:

For understanding limitations of ratio analysis, firstly, understanding of following two

terms are required which is as under:

2017 2018

5625000 / 13500000 * 100 8325000 / 16200000 *100

41.67 51.39

Cross-sectional comparisons: this means comparison of ratio of one company with the

other company on same industry.

Time-series Comparisons: Time series analysis can be useful to see how a given asset,

security or economic variable changes over time. It means comparison of ratios of one

= 0 Days

Trade payables period = Trade payable/Cost of sales*365

= 5100/19790*365

= 94.06 Days

Working Capital Cycle in Days:-

Inventory collection period 58.94

Add: Trade receivables period 55.86

Add: Cash and marketable securities period 0

Less: Trade payables period 94.06

Working Capital Cycle in days (2018) 20.74

Comments on liquidity position of Fridge-freezer Plc on the basis of working capital cycle:

By analysing the working capital cycle as calculated above, it is unfavourable for the

company in current year when compared to previous year (2017). Company is taking more time

in current year to collect the cash as compared to previous year. It can be said that Fridge-freezer

Plc's liquidity position is not good in current year but it is satisfactory. It should make plan &

strategy to correct it as compared to previous year.

3. Limitations of Using Ratio Analysis for both Cross-Sectional and Time-Series Comparisons:

For understanding limitations of ratio analysis, firstly, understanding of following two

terms are required which is as under:

2017 2018

5625000 / 13500000 * 100 8325000 / 16200000 *100

41.67 51.39

Cross-sectional comparisons: this means comparison of ratio of one company with the

other company on same industry.

Time-series Comparisons: Time series analysis can be useful to see how a given asset,

security or economic variable changes over time. It means comparison of ratios of one

company (in this case Fridge-freezer Plc) of current year with the ratios of same company

of previous year(s).

Limitations for Time-Series Comparison:

Historical: The information which is derived to calculate the ratio is based on actual

historical results. It cannot be interpreted that same results will be come in the future

context.

Inflation: If there is any change in rate of inflation in any of periods under review, then it

is not comparable. For example, if inflation was 100% in current year then sales becomes

doubled as compared to previous year this mean but in fact sales does not change at all.

Operational changes: A company may change its underlying operational structure to such

an extent that a ratio calculated several years ago and compared to the same ratio today

would allow a misguide interpretation.

Limitations for Cross-sectional Comparison:

Accounting policies: Comparison between two companies by the help of ratio analysis is

not right, because different companies may have different policies for recording the same

accounting transactions. This means comparing the ratio results of different companies

may be like apples & oranges (Bloom and et. al., 2013).

Company strategy: It can be risky to carry out a ratio analysis comparison between two

companies that are work towards distinct strategies.

Historic cost: If companies are of different ages i.e. companies are incorporated at

different years. In this case, their financial statements are included non-current assets

which are purchased at different period of time and generally recorded at historic cost.

This mean distinct companies have different book values of asset, even if businesses are

almost same. In this case, ratios cannot give right results for comparison.

TASK B

1. Calculation of Break-even point and Margin of safety for the year 2017 and 2018 of Washbug

Ltd

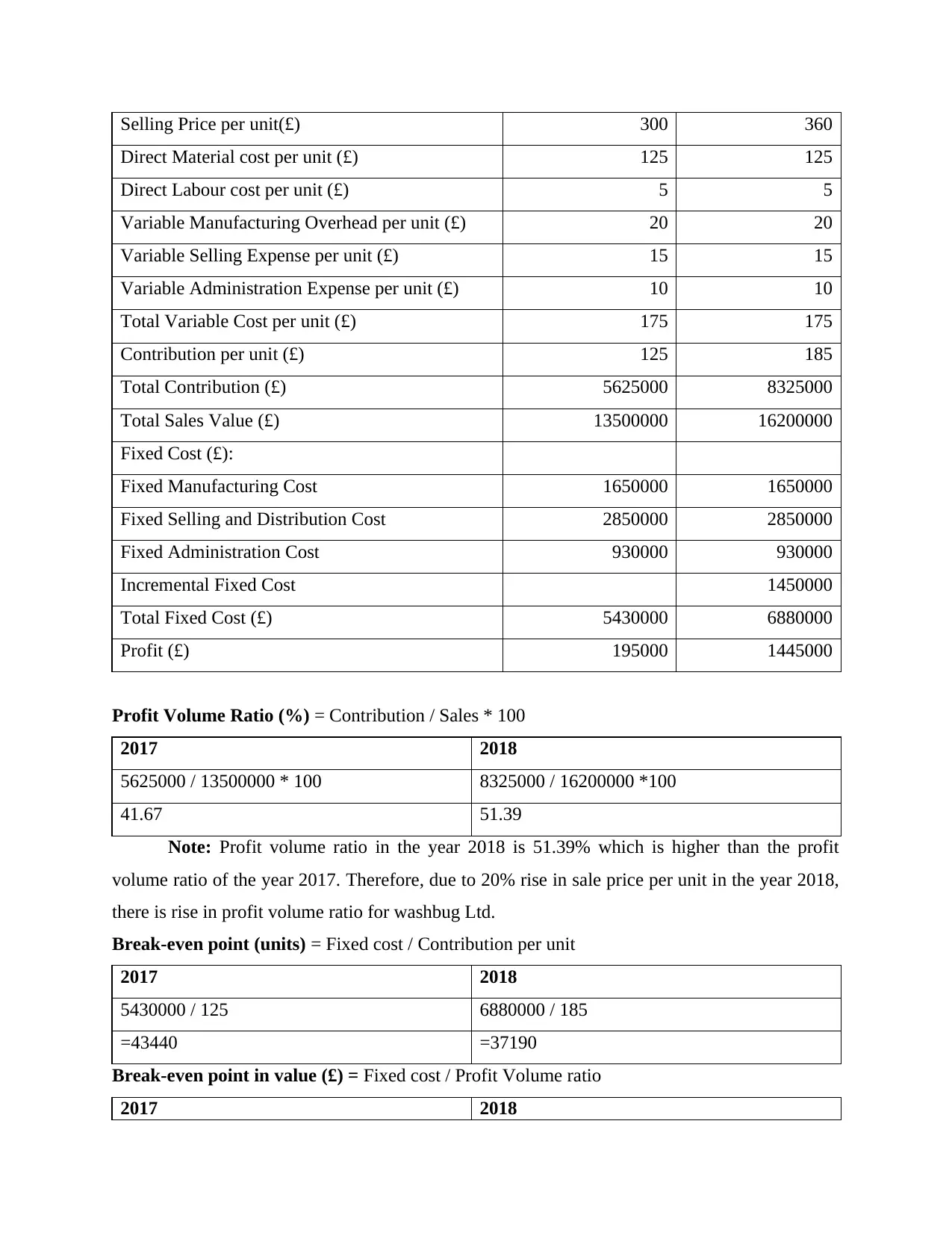

Particulars 2017 2018

Unit sold 45000 45000

of previous year(s).

Limitations for Time-Series Comparison:

Historical: The information which is derived to calculate the ratio is based on actual

historical results. It cannot be interpreted that same results will be come in the future

context.

Inflation: If there is any change in rate of inflation in any of periods under review, then it

is not comparable. For example, if inflation was 100% in current year then sales becomes

doubled as compared to previous year this mean but in fact sales does not change at all.

Operational changes: A company may change its underlying operational structure to such

an extent that a ratio calculated several years ago and compared to the same ratio today

would allow a misguide interpretation.

Limitations for Cross-sectional Comparison:

Accounting policies: Comparison between two companies by the help of ratio analysis is

not right, because different companies may have different policies for recording the same

accounting transactions. This means comparing the ratio results of different companies

may be like apples & oranges (Bloom and et. al., 2013).

Company strategy: It can be risky to carry out a ratio analysis comparison between two

companies that are work towards distinct strategies.

Historic cost: If companies are of different ages i.e. companies are incorporated at

different years. In this case, their financial statements are included non-current assets

which are purchased at different period of time and generally recorded at historic cost.

This mean distinct companies have different book values of asset, even if businesses are

almost same. In this case, ratios cannot give right results for comparison.

TASK B

1. Calculation of Break-even point and Margin of safety for the year 2017 and 2018 of Washbug

Ltd

Particulars 2017 2018

Unit sold 45000 45000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Selling Price per unit(£) 300 360

Direct Material cost per unit (£) 125 125

Direct Labour cost per unit (£) 5 5

Variable Manufacturing Overhead per unit (£) 20 20

Variable Selling Expense per unit (£) 15 15

Variable Administration Expense per unit (£) 10 10

Total Variable Cost per unit (£) 175 175

Contribution per unit (£) 125 185

Total Contribution (£) 5625000 8325000

Total Sales Value (£) 13500000 16200000

Fixed Cost (£):

Fixed Manufacturing Cost 1650000 1650000

Fixed Selling and Distribution Cost 2850000 2850000

Fixed Administration Cost 930000 930000

Incremental Fixed Cost 1450000

Total Fixed Cost (£) 5430000 6880000

Profit (£) 195000 1445000

Profit Volume Ratio (%) = Contribution / Sales * 100

2017 2018

5625000 / 13500000 * 100 8325000 / 16200000 *100

41.67 51.39

Note: Profit volume ratio in the year 2018 is 51.39% which is higher than the profit

volume ratio of the year 2017. Therefore, due to 20% rise in sale price per unit in the year 2018,

there is rise in profit volume ratio for washbug Ltd.

Break-even point (units) = Fixed cost / Contribution per unit

2017 2018

5430000 / 125 6880000 / 185

=43440 =37190

Break-even point in value (£) = Fixed cost / Profit Volume ratio

2017 2018

Direct Material cost per unit (£) 125 125

Direct Labour cost per unit (£) 5 5

Variable Manufacturing Overhead per unit (£) 20 20

Variable Selling Expense per unit (£) 15 15

Variable Administration Expense per unit (£) 10 10

Total Variable Cost per unit (£) 175 175

Contribution per unit (£) 125 185

Total Contribution (£) 5625000 8325000

Total Sales Value (£) 13500000 16200000

Fixed Cost (£):

Fixed Manufacturing Cost 1650000 1650000

Fixed Selling and Distribution Cost 2850000 2850000

Fixed Administration Cost 930000 930000

Incremental Fixed Cost 1450000

Total Fixed Cost (£) 5430000 6880000

Profit (£) 195000 1445000

Profit Volume Ratio (%) = Contribution / Sales * 100

2017 2018

5625000 / 13500000 * 100 8325000 / 16200000 *100

41.67 51.39

Note: Profit volume ratio in the year 2018 is 51.39% which is higher than the profit

volume ratio of the year 2017. Therefore, due to 20% rise in sale price per unit in the year 2018,

there is rise in profit volume ratio for washbug Ltd.

Break-even point (units) = Fixed cost / Contribution per unit

2017 2018

5430000 / 125 6880000 / 185

=43440 =37190

Break-even point in value (£) = Fixed cost / Profit Volume ratio

2017 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

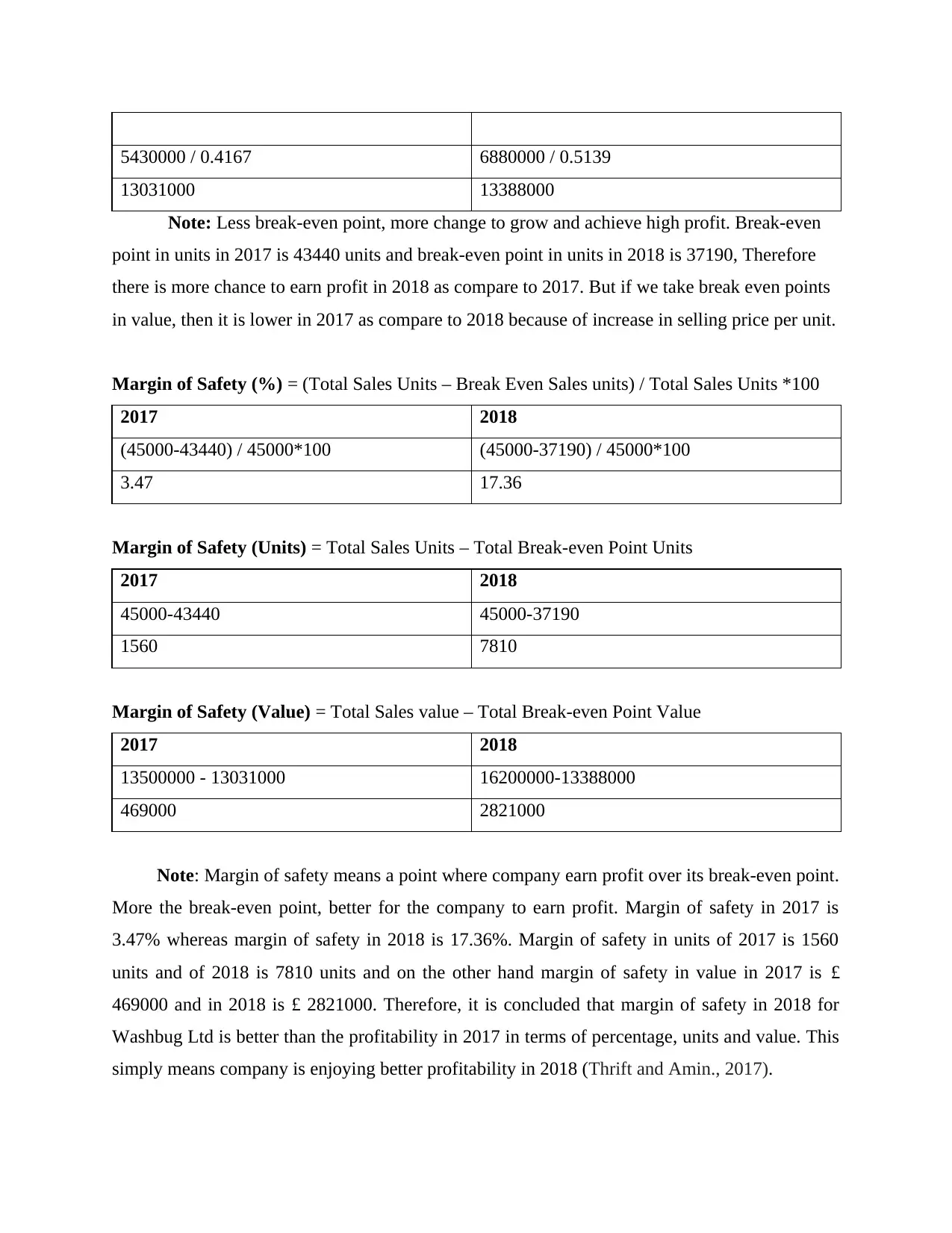

5430000 / 0.4167 6880000 / 0.5139

13031000 13388000

Note: Less break-even point, more change to grow and achieve high profit. Break-even

point in units in 2017 is 43440 units and break-even point in units in 2018 is 37190, Therefore

there is more chance to earn profit in 2018 as compare to 2017. But if we take break even points

in value, then it is lower in 2017 as compare to 2018 because of increase in selling price per unit.

Margin of Safety (%) = (Total Sales Units – Break Even Sales units) / Total Sales Units *100

2017 2018

(45000-43440) / 45000*100 (45000-37190) / 45000*100

3.47 17.36

Margin of Safety (Units) = Total Sales Units – Total Break-even Point Units

2017 2018

45000-43440 45000-37190

1560 7810

Margin of Safety (Value) = Total Sales value – Total Break-even Point Value

2017 2018

13500000 - 13031000 16200000-13388000

469000 2821000

Note: Margin of safety means a point where company earn profit over its break-even point.

More the break-even point, better for the company to earn profit. Margin of safety in 2017 is

3.47% whereas margin of safety in 2018 is 17.36%. Margin of safety in units of 2017 is 1560

units and of 2018 is 7810 units and on the other hand margin of safety in value in 2017 is £

469000 and in 2018 is £ 2821000. Therefore, it is concluded that margin of safety in 2018 for

Washbug Ltd is better than the profitability in 2017 in terms of percentage, units and value. This

simply means company is enjoying better profitability in 2018 (Thrift and Amin., 2017).

13031000 13388000

Note: Less break-even point, more change to grow and achieve high profit. Break-even

point in units in 2017 is 43440 units and break-even point in units in 2018 is 37190, Therefore

there is more chance to earn profit in 2018 as compare to 2017. But if we take break even points

in value, then it is lower in 2017 as compare to 2018 because of increase in selling price per unit.

Margin of Safety (%) = (Total Sales Units – Break Even Sales units) / Total Sales Units *100

2017 2018

(45000-43440) / 45000*100 (45000-37190) / 45000*100

3.47 17.36

Margin of Safety (Units) = Total Sales Units – Total Break-even Point Units

2017 2018

45000-43440 45000-37190

1560 7810

Margin of Safety (Value) = Total Sales value – Total Break-even Point Value

2017 2018

13500000 - 13031000 16200000-13388000

469000 2821000

Note: Margin of safety means a point where company earn profit over its break-even point.

More the break-even point, better for the company to earn profit. Margin of safety in 2017 is

3.47% whereas margin of safety in 2018 is 17.36%. Margin of safety in units of 2017 is 1560

units and of 2018 is 7810 units and on the other hand margin of safety in value in 2017 is £

469000 and in 2018 is £ 2821000. Therefore, it is concluded that margin of safety in 2018 for

Washbug Ltd is better than the profitability in 2017 in terms of percentage, units and value. This

simply means company is enjoying better profitability in 2018 (Thrift and Amin., 2017).

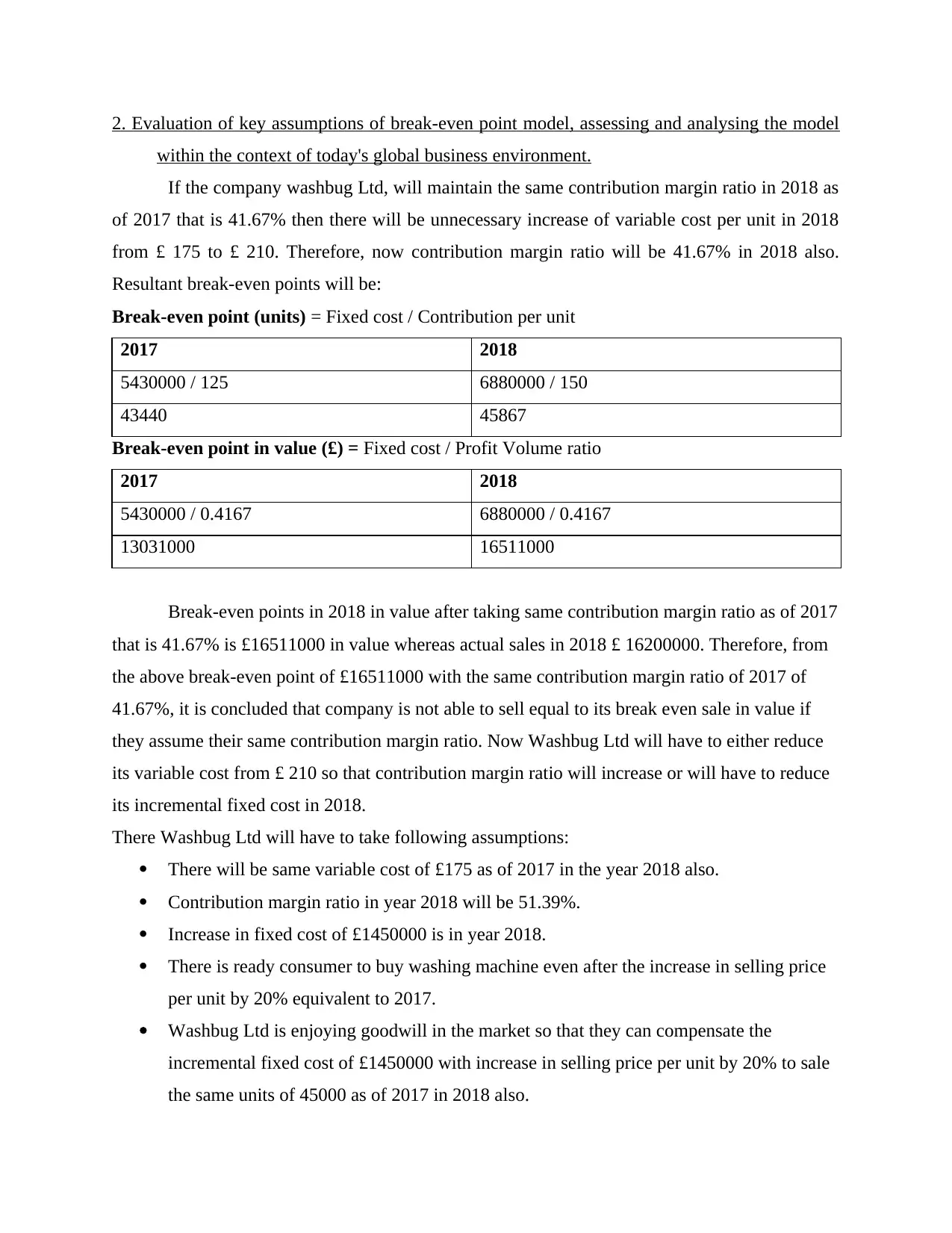

2. Evaluation of key assumptions of break-even point model, assessing and analysing the model

within the context of today's global business environment.

If the company washbug Ltd, will maintain the same contribution margin ratio in 2018 as

of 2017 that is 41.67% then there will be unnecessary increase of variable cost per unit in 2018

from £ 175 to £ 210. Therefore, now contribution margin ratio will be 41.67% in 2018 also.

Resultant break-even points will be:

Break-even point (units) = Fixed cost / Contribution per unit

2017 2018

5430000 / 125 6880000 / 150

43440 45867

Break-even point in value (£) = Fixed cost / Profit Volume ratio

2017 2018

5430000 / 0.4167 6880000 / 0.4167

13031000 16511000

Break-even points in 2018 in value after taking same contribution margin ratio as of 2017

that is 41.67% is £16511000 in value whereas actual sales in 2018 £ 16200000. Therefore, from

the above break-even point of £16511000 with the same contribution margin ratio of 2017 of

41.67%, it is concluded that company is not able to sell equal to its break even sale in value if

they assume their same contribution margin ratio. Now Washbug Ltd will have to either reduce

its variable cost from £ 210 so that contribution margin ratio will increase or will have to reduce

its incremental fixed cost in 2018.

There Washbug Ltd will have to take following assumptions:

There will be same variable cost of £175 as of 2017 in the year 2018 also.

Contribution margin ratio in year 2018 will be 51.39%.

Increase in fixed cost of £1450000 is in year 2018.

There is ready consumer to buy washing machine even after the increase in selling price

per unit by 20% equivalent to 2017.

Washbug Ltd is enjoying goodwill in the market so that they can compensate the

incremental fixed cost of £1450000 with increase in selling price per unit by 20% to sale

the same units of 45000 as of 2017 in 2018 also.

within the context of today's global business environment.

If the company washbug Ltd, will maintain the same contribution margin ratio in 2018 as

of 2017 that is 41.67% then there will be unnecessary increase of variable cost per unit in 2018

from £ 175 to £ 210. Therefore, now contribution margin ratio will be 41.67% in 2018 also.

Resultant break-even points will be:

Break-even point (units) = Fixed cost / Contribution per unit

2017 2018

5430000 / 125 6880000 / 150

43440 45867

Break-even point in value (£) = Fixed cost / Profit Volume ratio

2017 2018

5430000 / 0.4167 6880000 / 0.4167

13031000 16511000

Break-even points in 2018 in value after taking same contribution margin ratio as of 2017

that is 41.67% is £16511000 in value whereas actual sales in 2018 £ 16200000. Therefore, from

the above break-even point of £16511000 with the same contribution margin ratio of 2017 of

41.67%, it is concluded that company is not able to sell equal to its break even sale in value if

they assume their same contribution margin ratio. Now Washbug Ltd will have to either reduce

its variable cost from £ 210 so that contribution margin ratio will increase or will have to reduce

its incremental fixed cost in 2018.

There Washbug Ltd will have to take following assumptions:

There will be same variable cost of £175 as of 2017 in the year 2018 also.

Contribution margin ratio in year 2018 will be 51.39%.

Increase in fixed cost of £1450000 is in year 2018.

There is ready consumer to buy washing machine even after the increase in selling price

per unit by 20% equivalent to 2017.

Washbug Ltd is enjoying goodwill in the market so that they can compensate the

incremental fixed cost of £1450000 with increase in selling price per unit by 20% to sale

the same units of 45000 as of 2017 in 2018 also.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.