Accounting and Finance: Investment Appraisal, Statements & Analysis

VerifiedAdded on 2023/06/16

|23

|4123

|152

Report

AI Summary

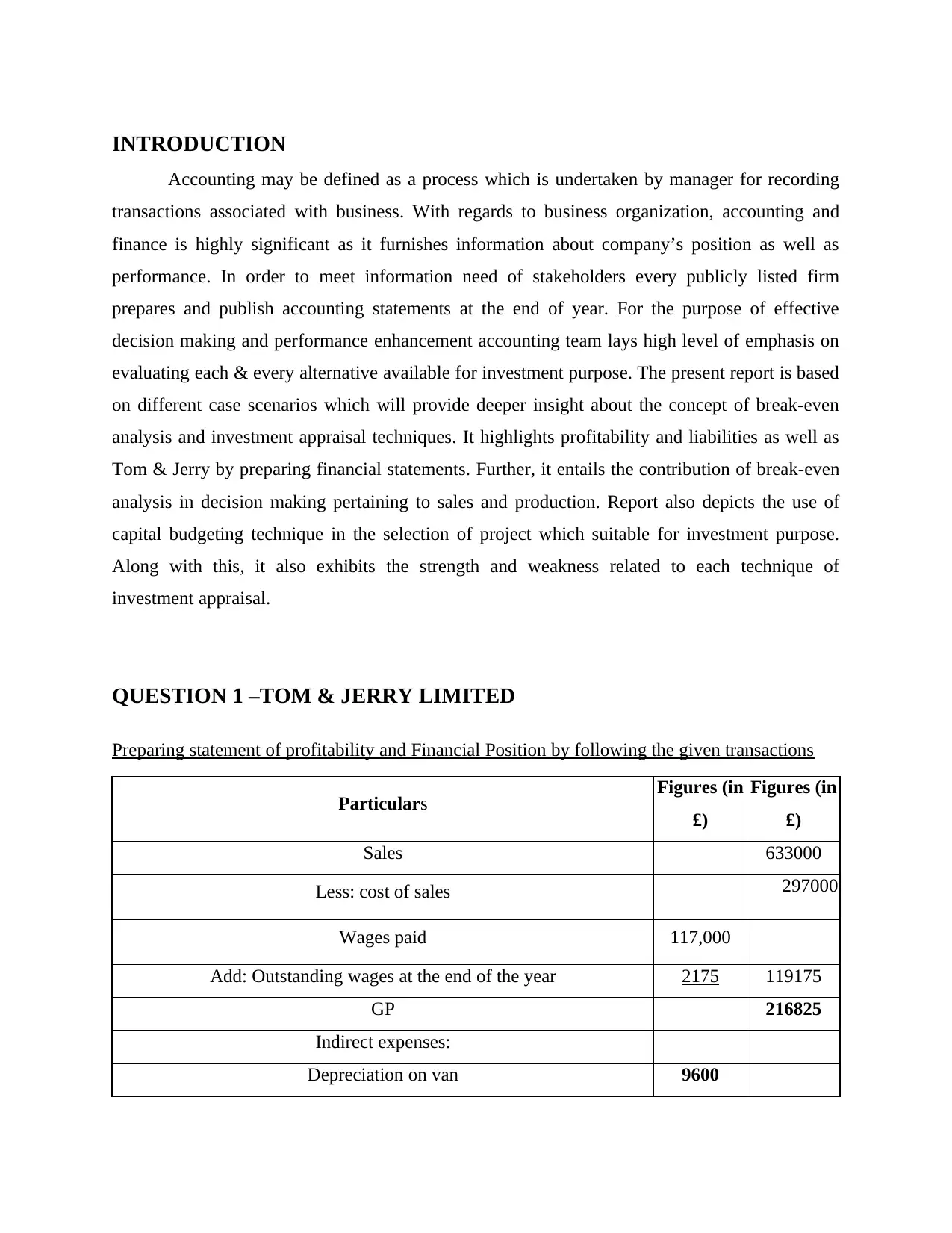

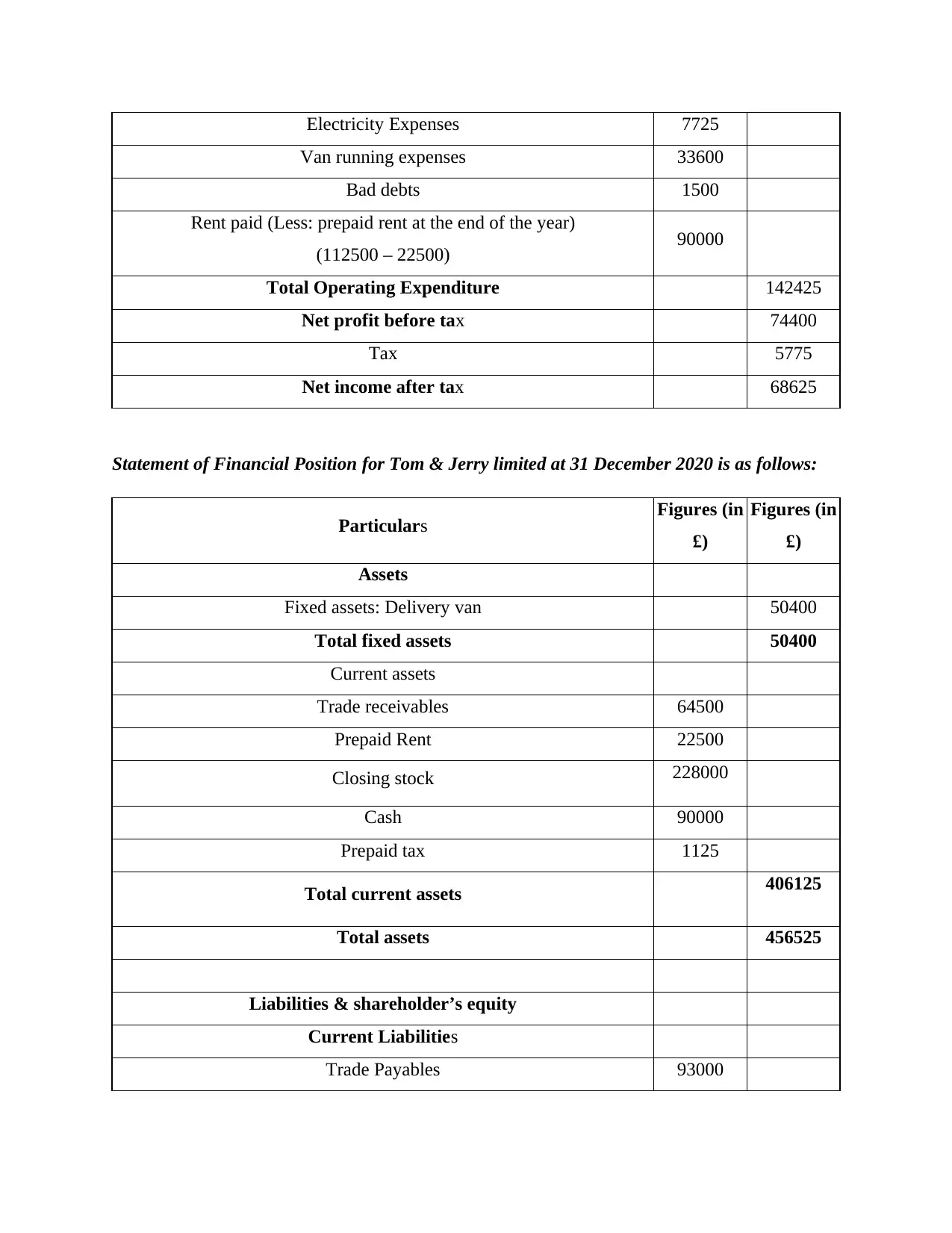

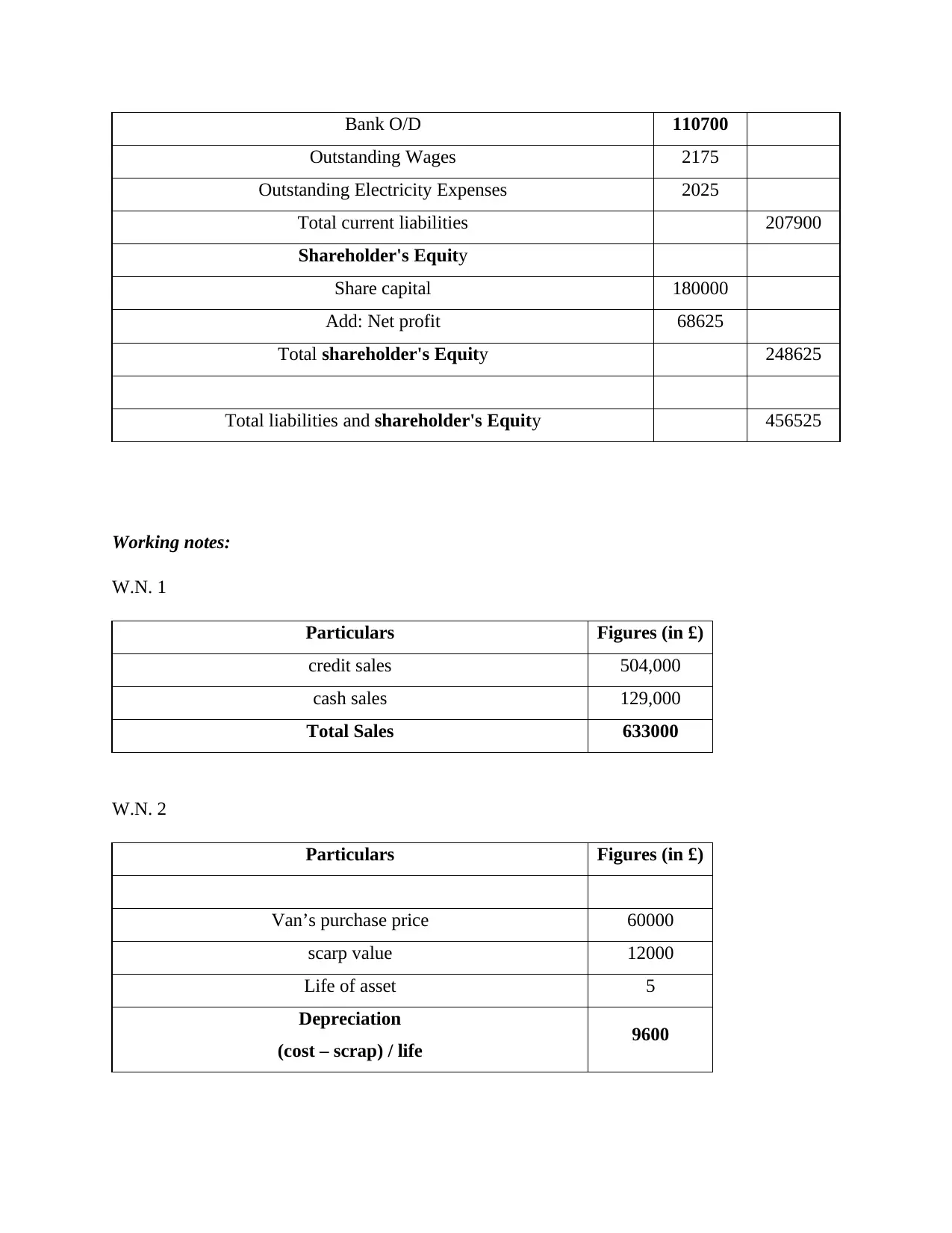

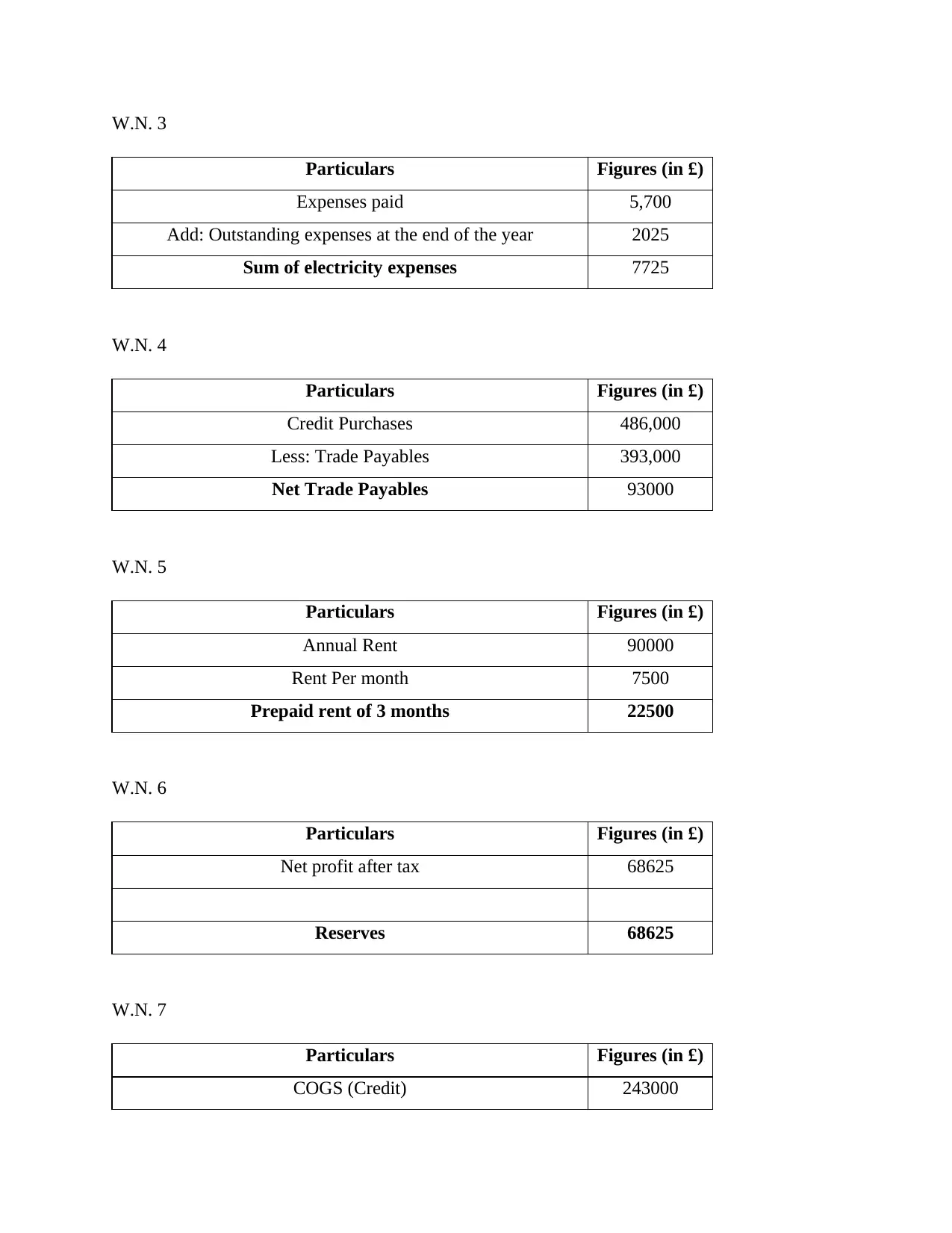

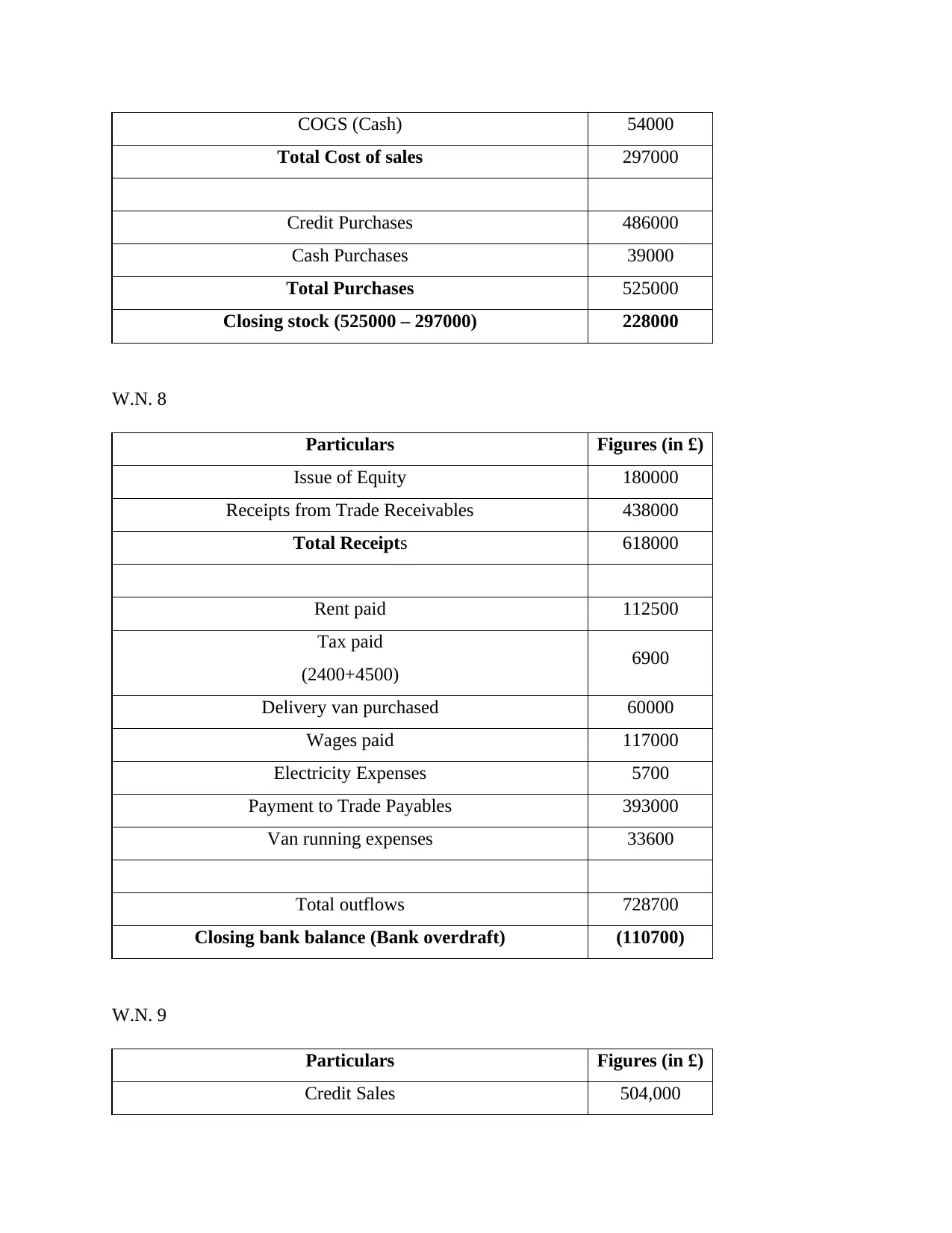

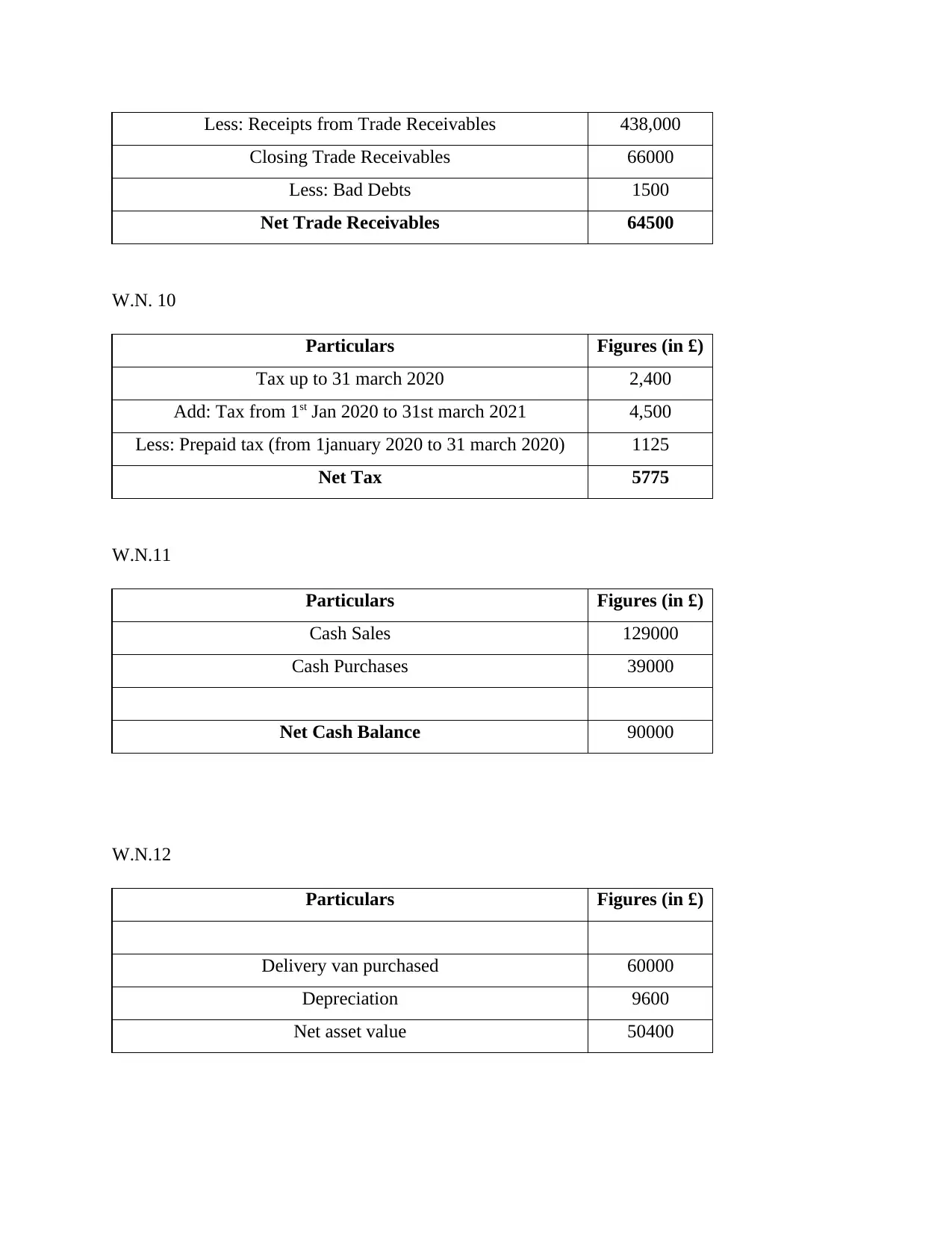

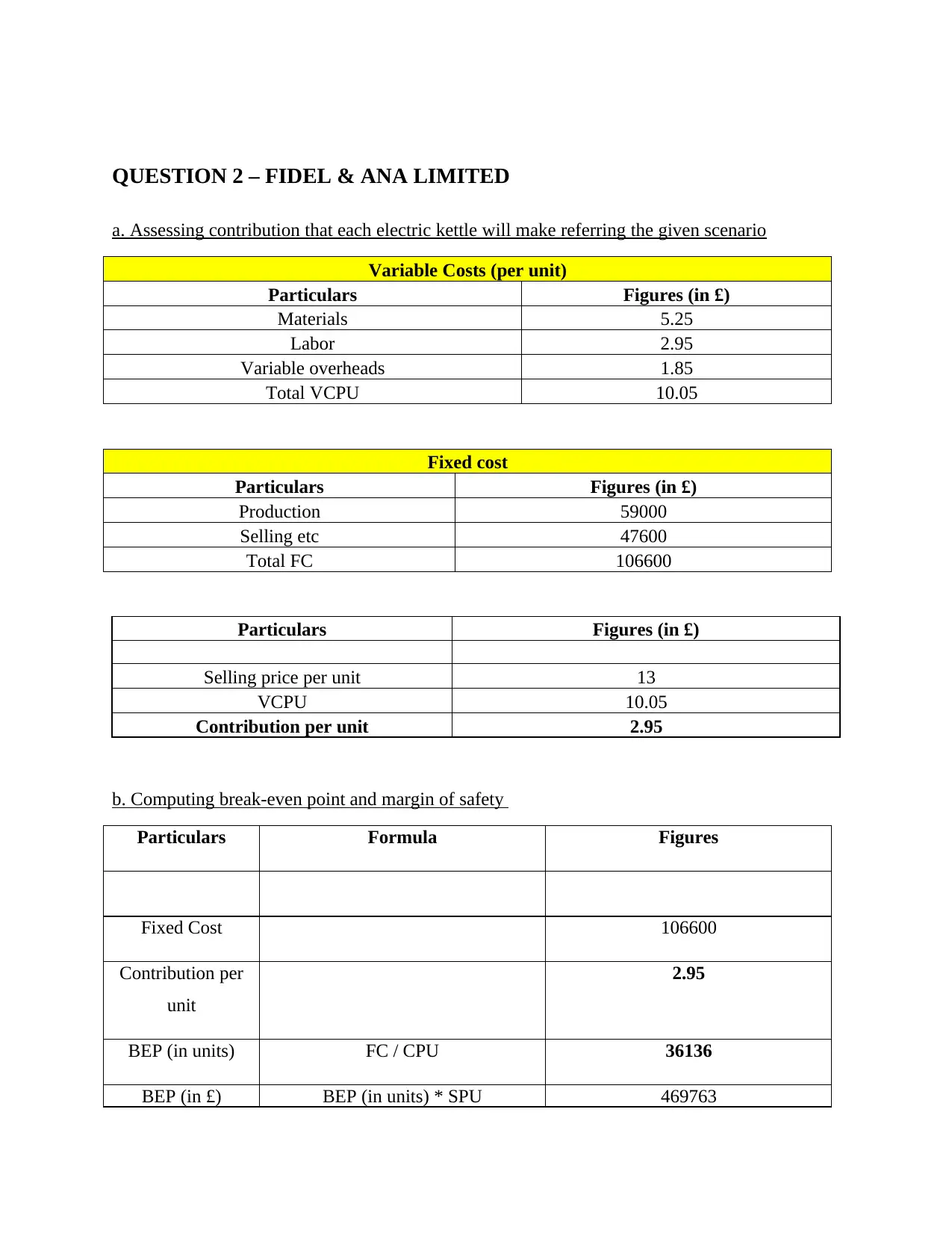

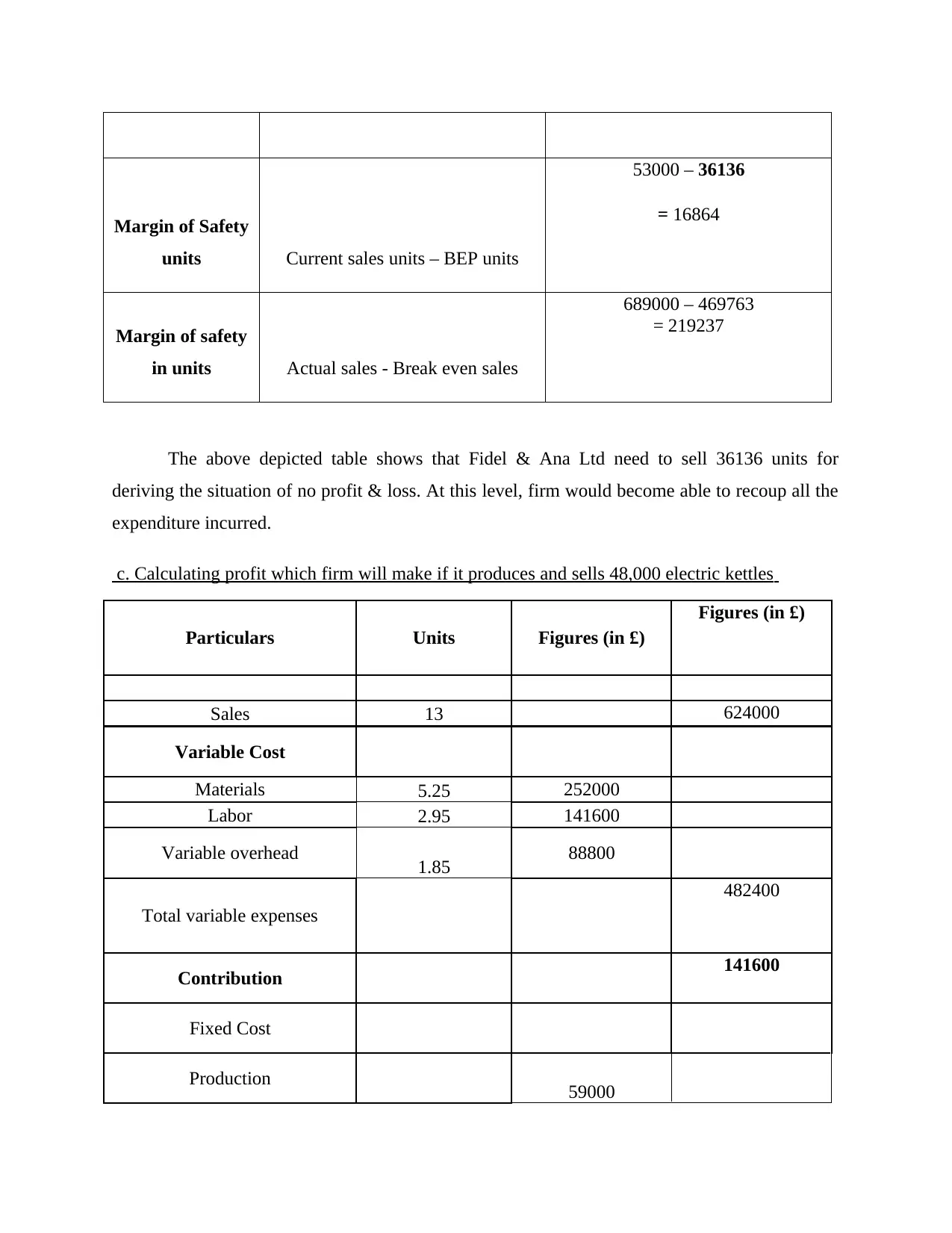

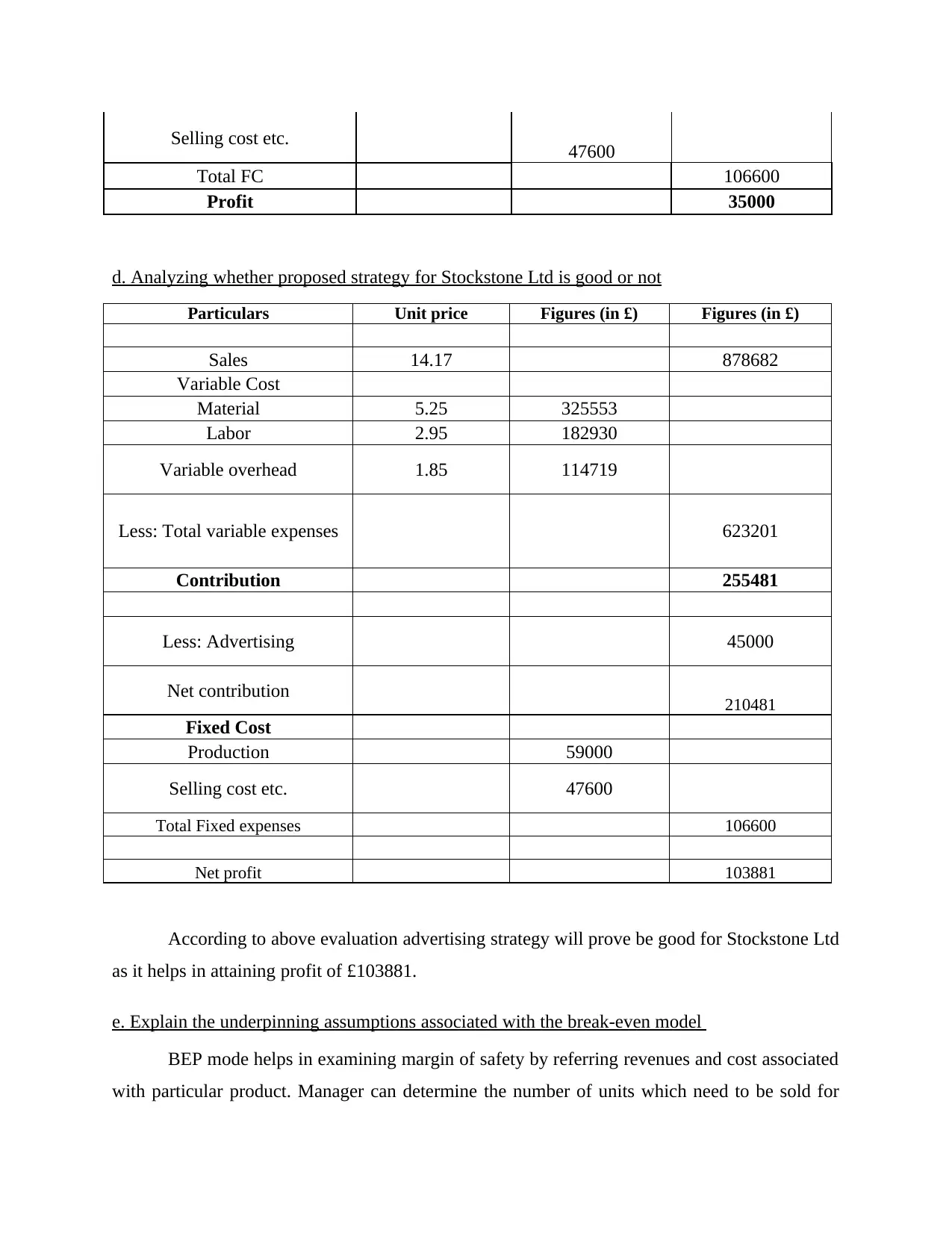

This report provides a comprehensive analysis of accounting and finance concepts through various case scenarios. It begins with the preparation of financial statements for Tom & Jerry Limited, detailing profitability and financial position based on provided transactions. The report then delves into break-even analysis for Fidel & Ana Limited, assessing contribution margins, break-even points, and the impact of strategic decisions like advertising. Furthermore, it evaluates the viability of a new machine for Bimbagu Plc using investment appraisal tools such as payback period, net present value, and average rate of return, discussing the merits and limitations of each technique. The report also explores the benefits and limitations of budgets as strategic planning tools, providing a holistic view of financial decision-making in business contexts. Desklib offers this and many other solved assignments for students.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.