MOD005704 - Financial Investment Analysis Report: Investment Analysis

VerifiedAdded on 2023/04/23

|22

|2630

|251

Report

AI Summary

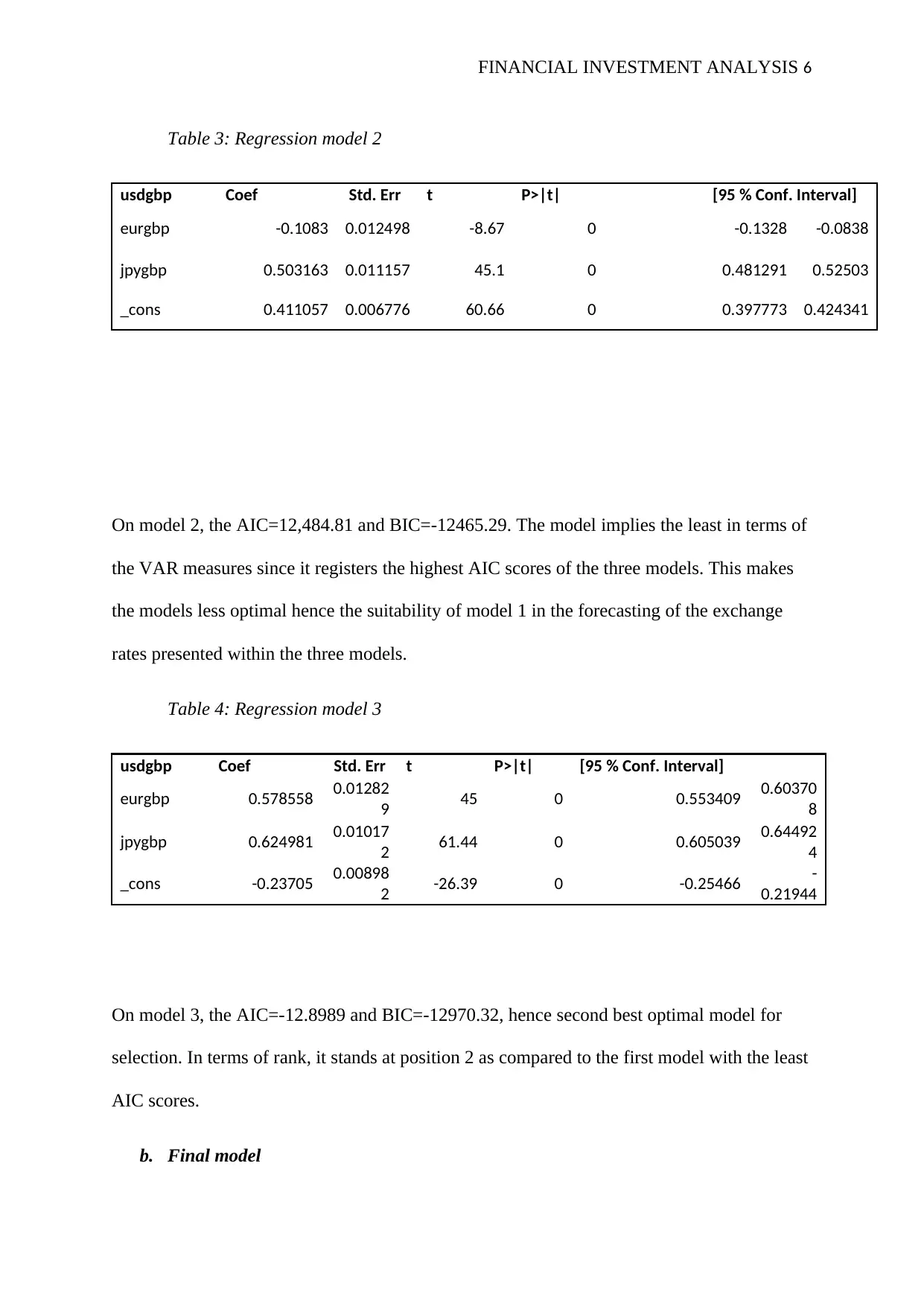

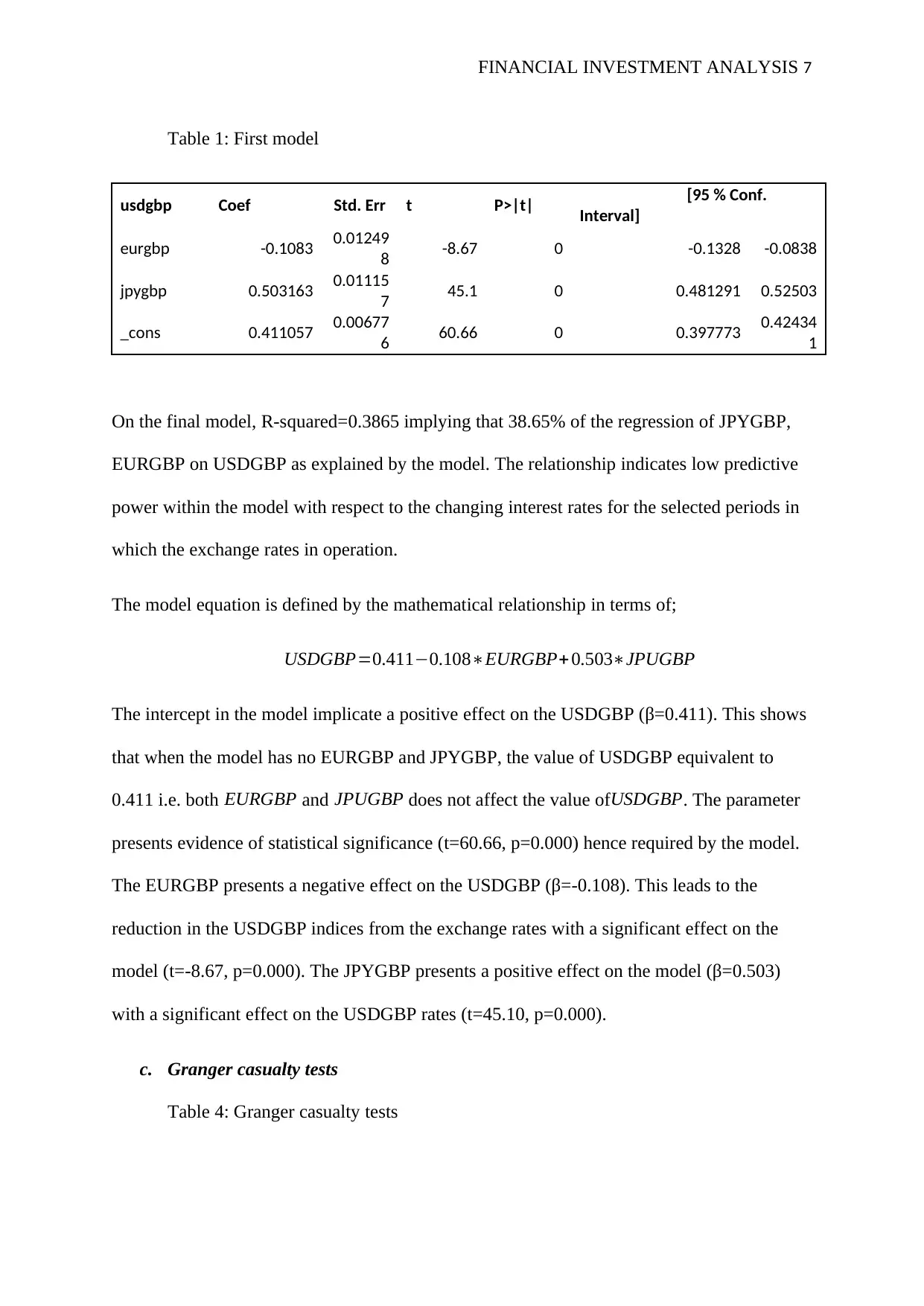

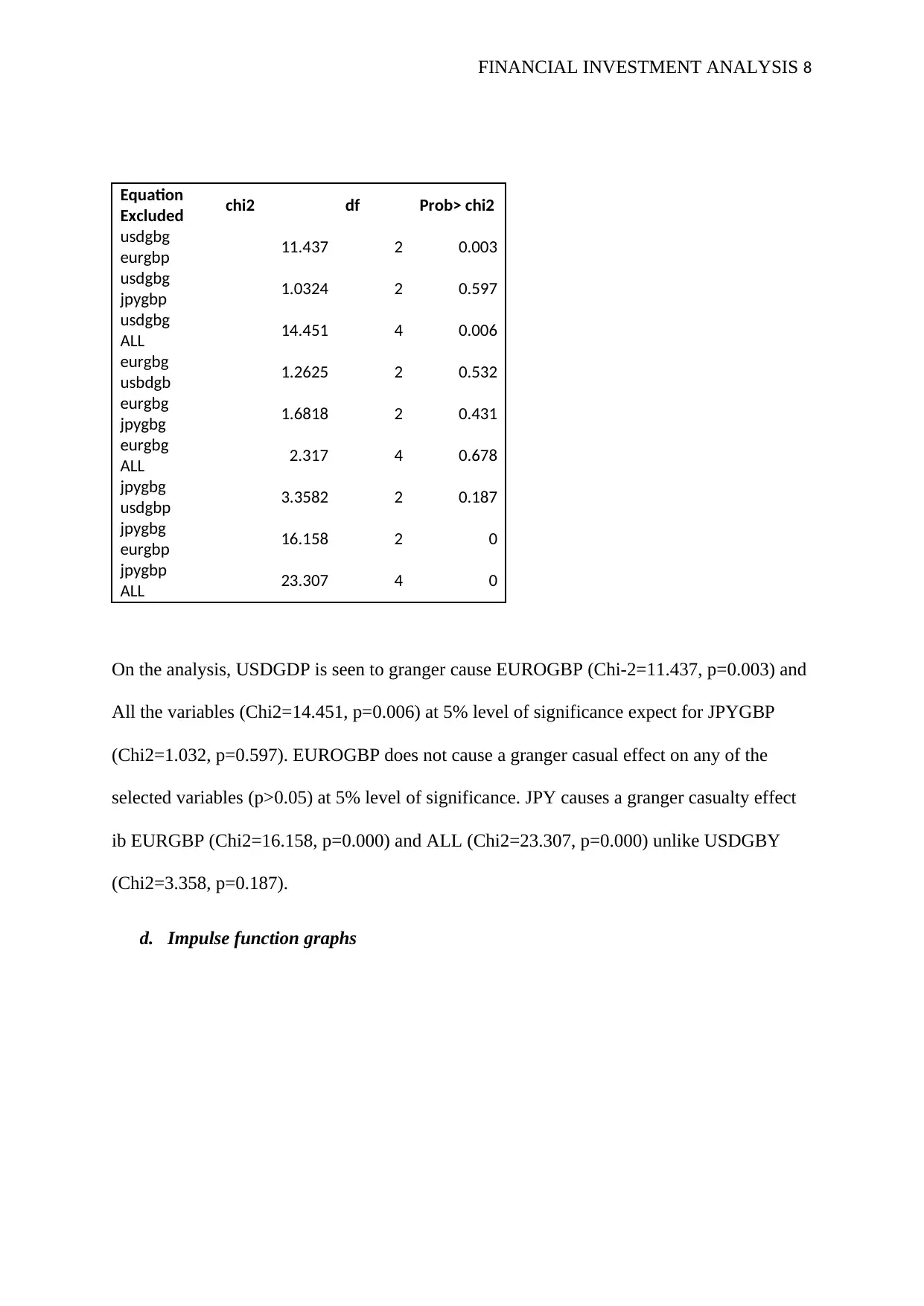

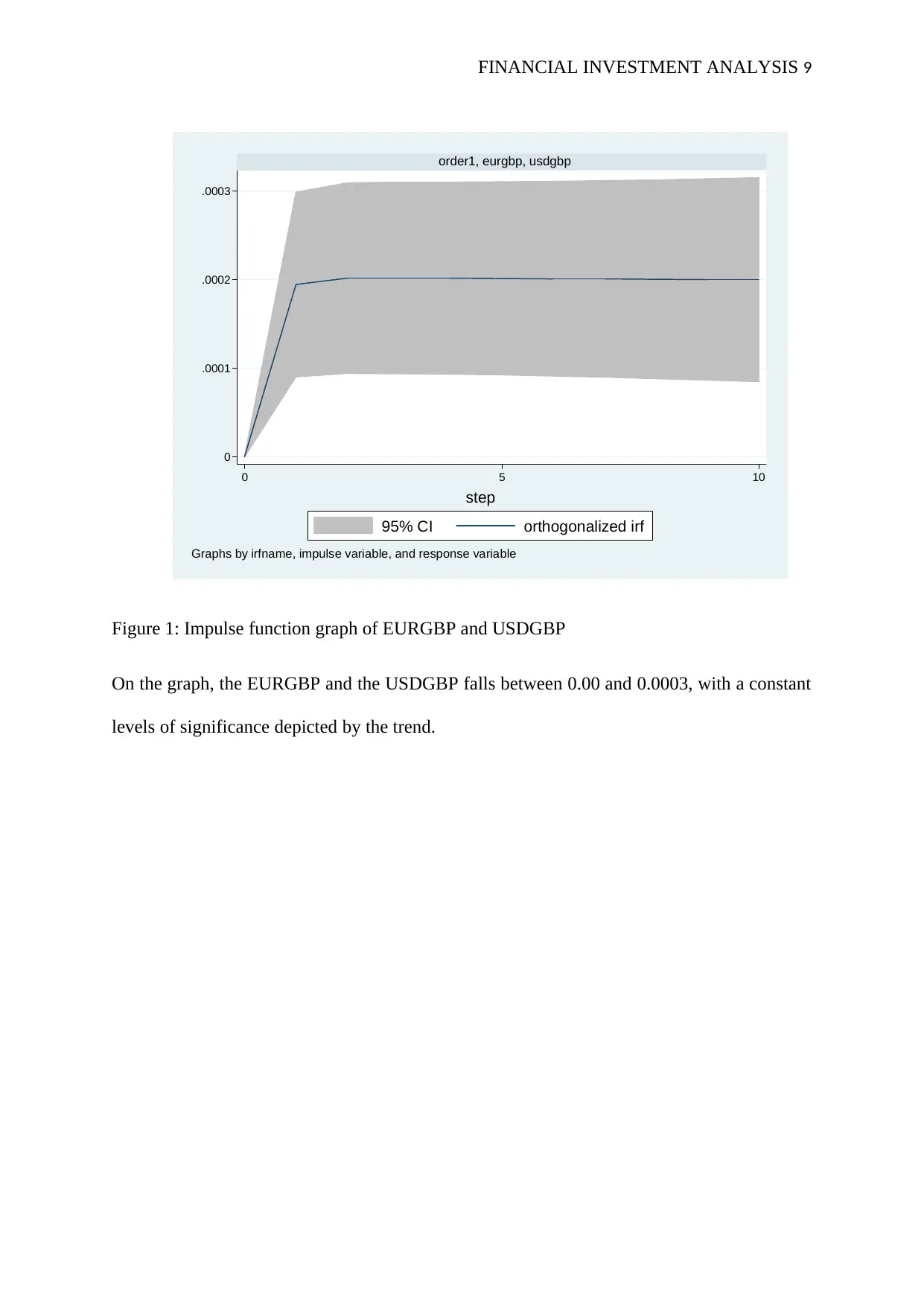

This report provides a financial investment analysis, utilizing the Box-Jenkins methodology to analyze Bitcoin log returns, employing time series plots and correlograms to assess stationarity and autocorrelation. It evaluates continuously compounded rates of return for various currency pairs, identifying EUROGBP as having the highest return from 2000 to 2018. The analysis includes VAR model selection based on the Akaike Information Criterion (AIC), determining that model 1 is the most appropriate for predicting interest rates. Granger causality tests reveal relationships between USDGDP, EUROGBP, and JPYGBP. The report also explores the relationship between future oil prices and spot rates using VAR tests and Engle-Granger 2 step model, concluding with an error correction model and an economic rationale discussing the implications of cointegration or lack thereof on revenue streams and market efficiency. The document is contributed by a student and available on Desklib.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.