Financial Statement Analysis: A Report on Kedison and Chocco PLC

VerifiedAdded on 2023/06/18

|17

|2779

|239

Report

AI Summary

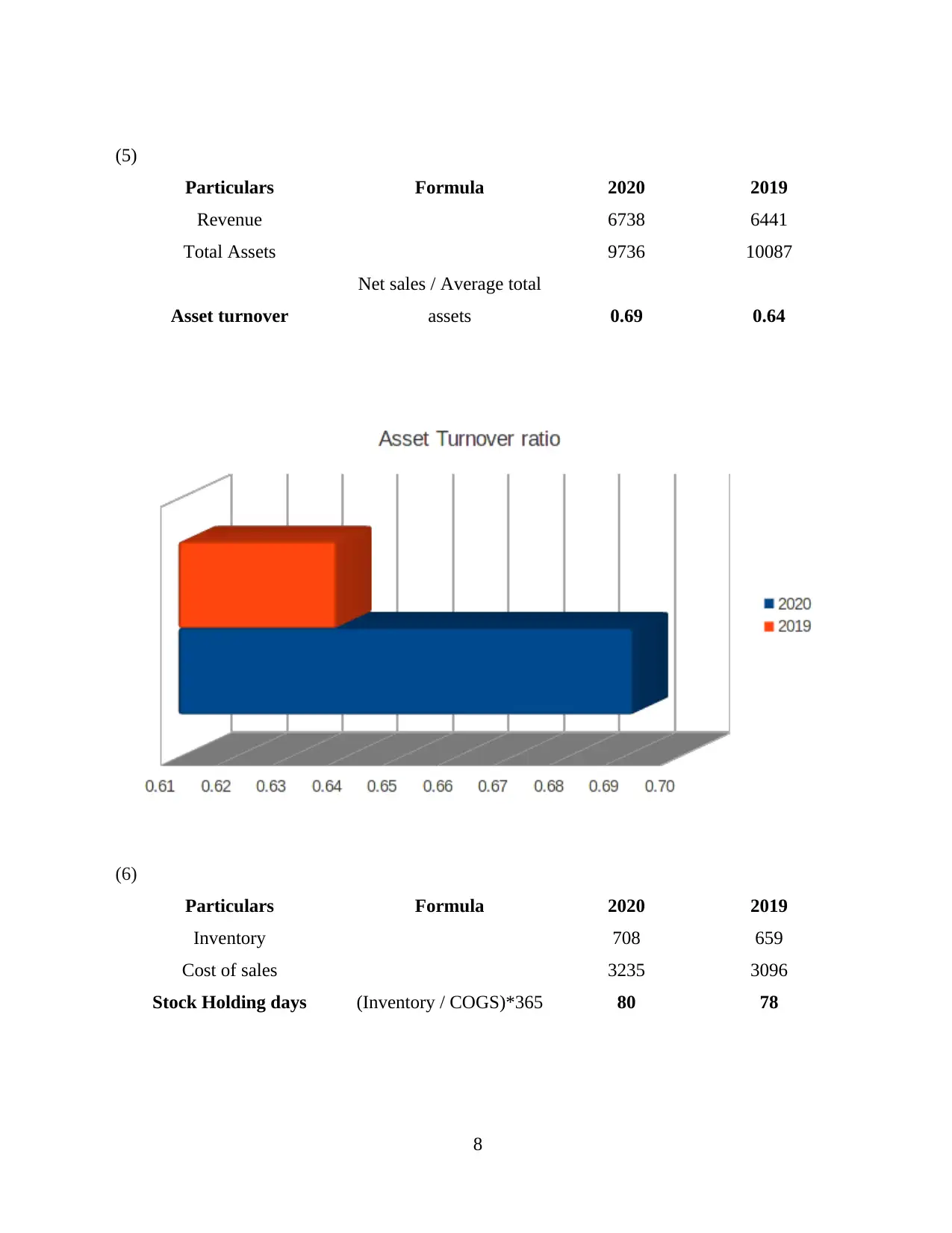

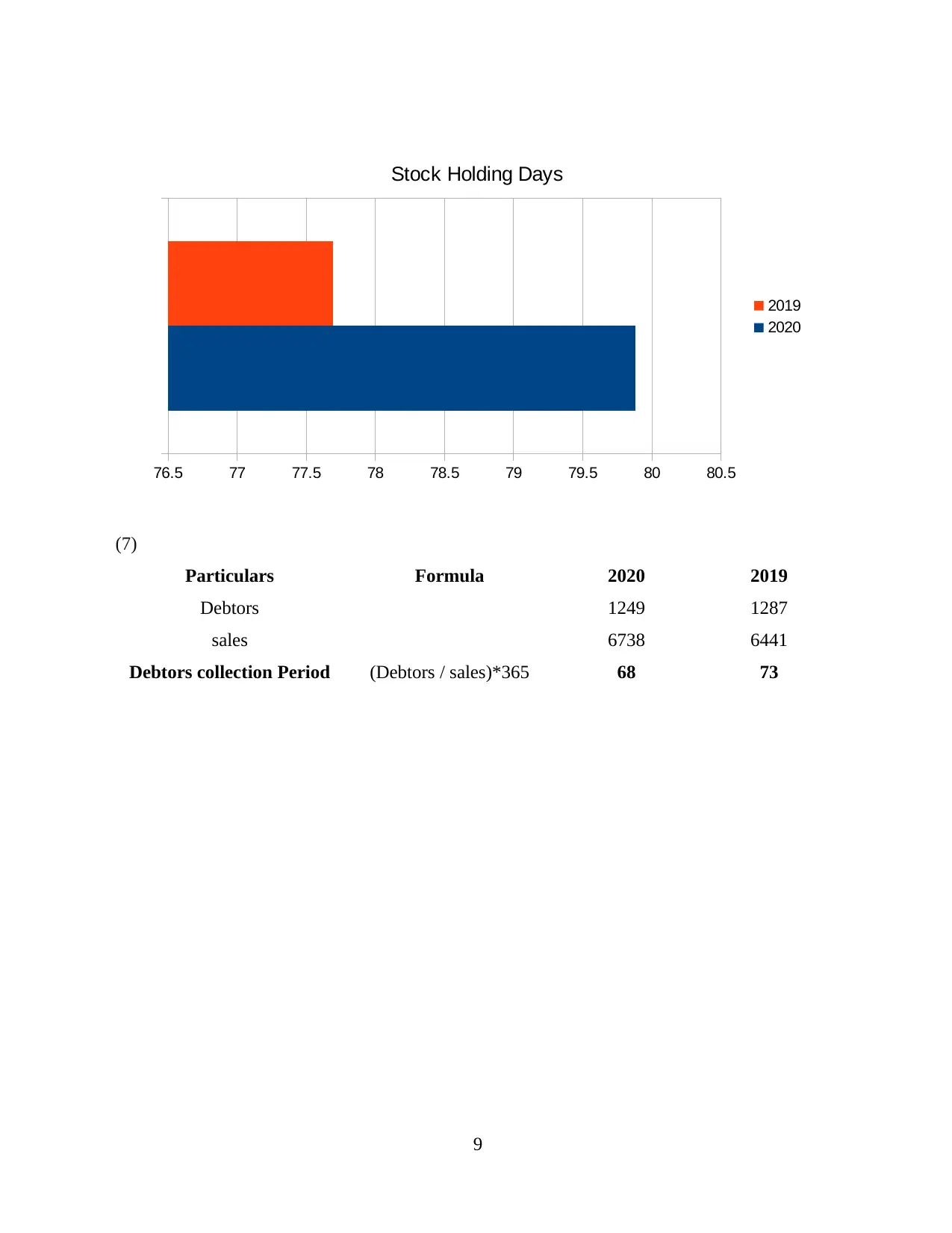

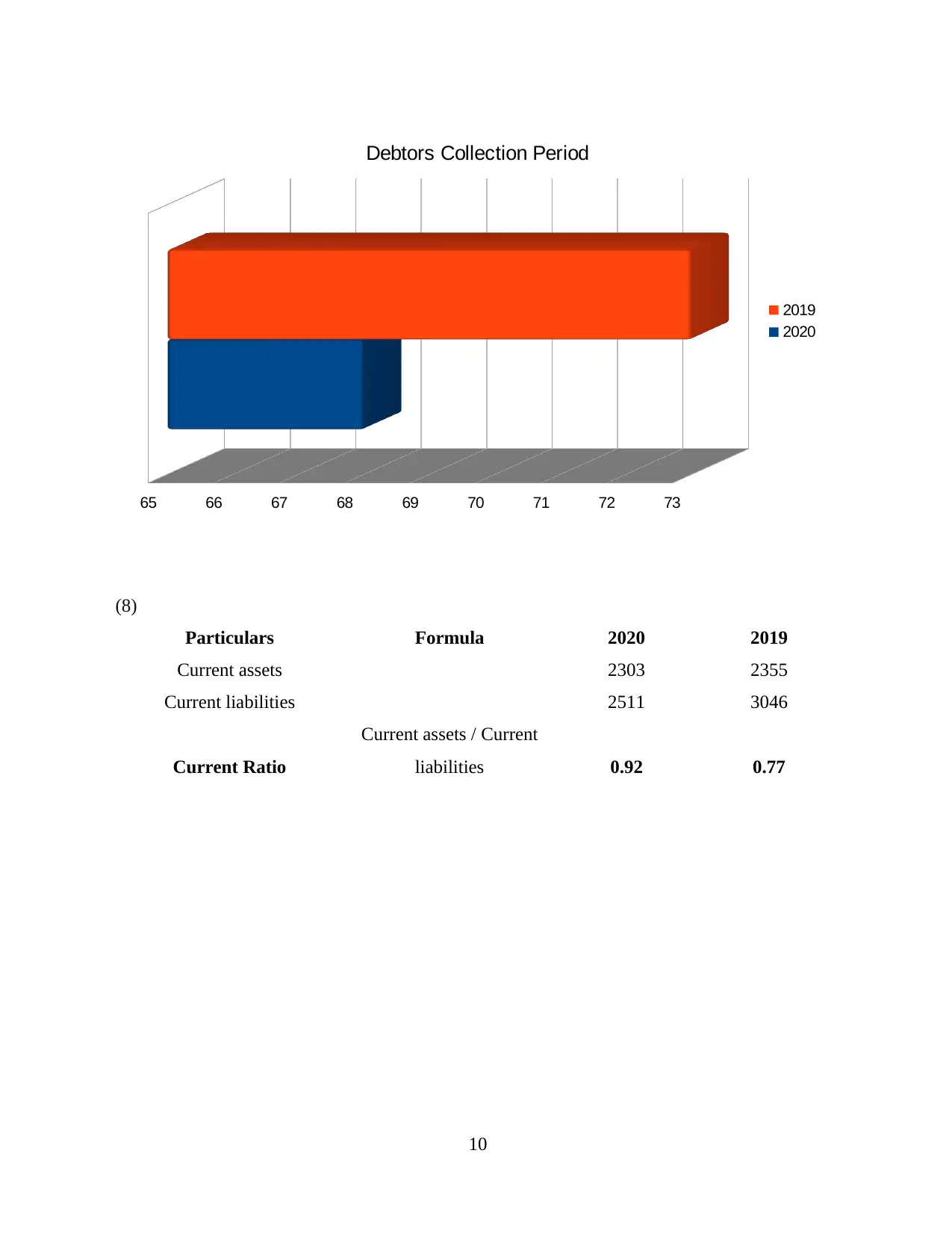

This report provides a comprehensive financial analysis of Kedison PLC and Chocco PLC. It includes the preparation of financial statements for Kedison PLC, such as the profit and loss statement and balance sheet, along with detailed working notes. The report also presents a ratio analysis for Chocco PLC for the years 2020 and 2019, calculating key ratios like ROCE, ROE, EPS, net profit margin, asset turnover, stock holding days, debtors collection period, current ratio, gearing ratio, and inventory turnover. Furthermore, it offers insightful comments on the financial performance and position of Chocco PLC, evaluating various aspects such as profitability, efficiency, and liquidity based on the calculated ratios. This document helps in understanding the financial health and performance of both companies through detailed analysis and calculations.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.