Kerrigan Ltd: Analysis of Breakeven and Management Accounting

VerifiedAdded on 2023/06/18

|9

|1744

|141

Report

AI Summary

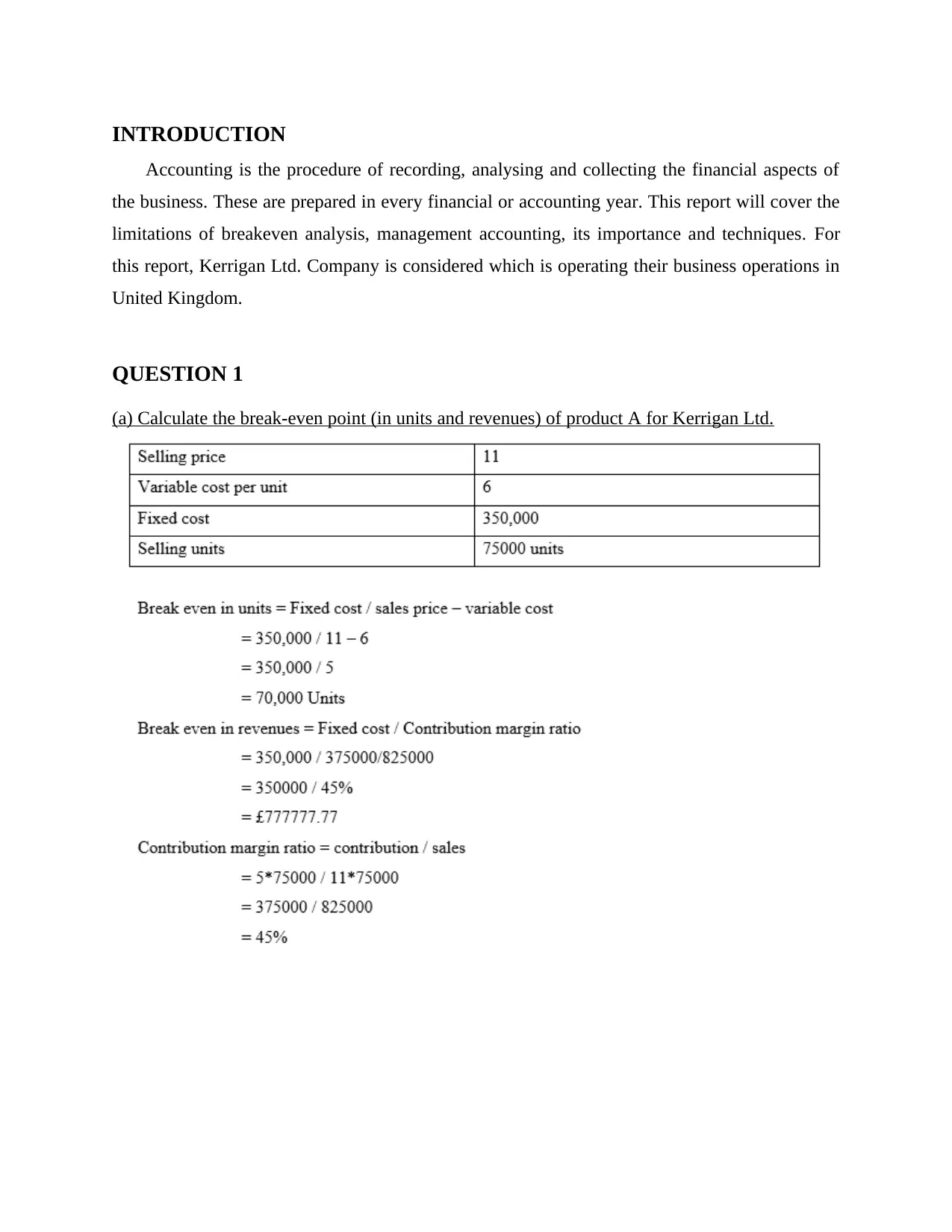

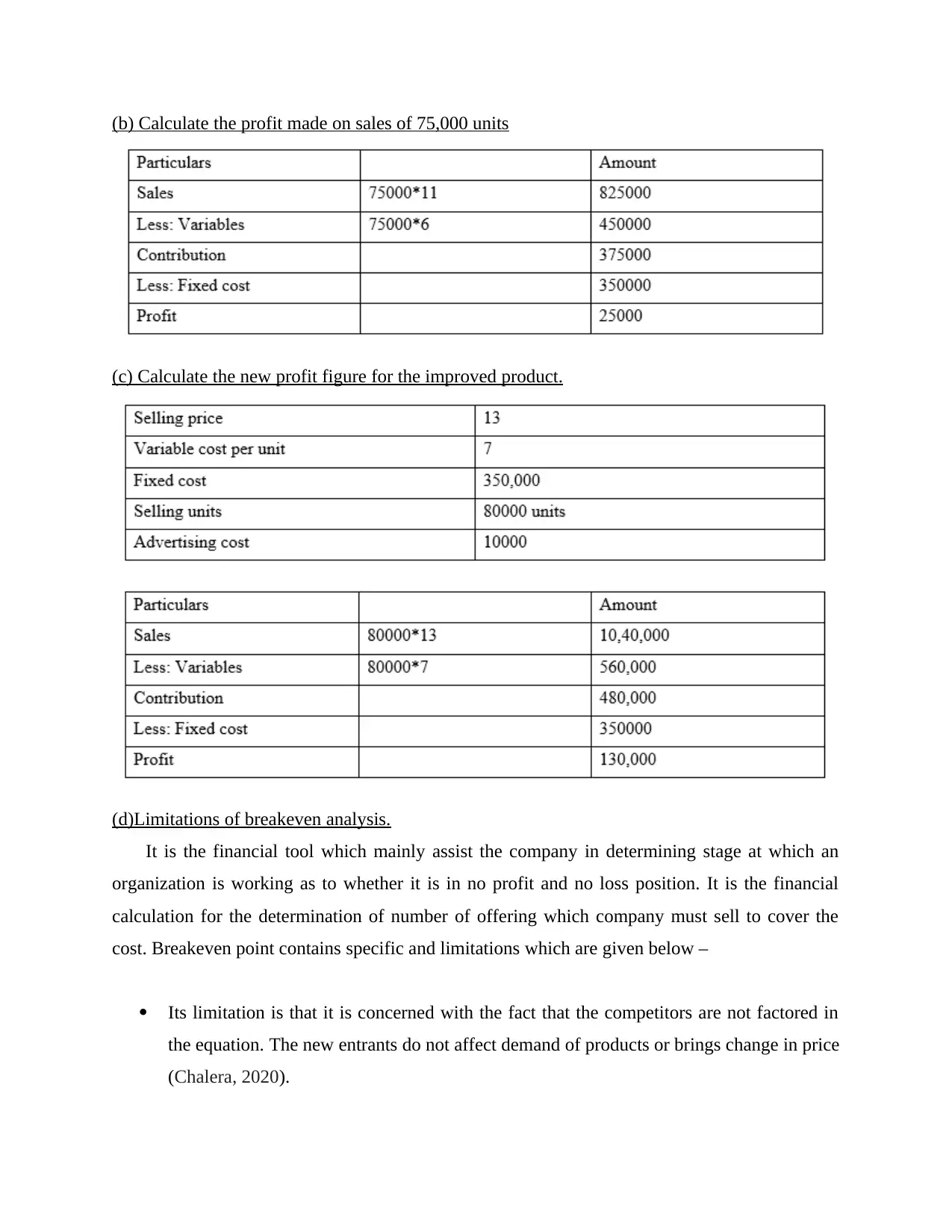

This report provides a comprehensive analysis of breakeven points and management accounting principles, focusing on Kerrigan Ltd. It includes calculations for breakeven points in units and revenues, profit calculations, and the impact of product improvements. The report also discusses the limitations of breakeven analysis, emphasizing factors like competitor influence and cost assumptions. Furthermore, it explores the importance of management accounting in planning, decision-making, issue recognition, and strategic management, contrasting it with financial accounting. Finally, it examines techniques such as cash flow statements, fund flow statements, and graphical presentations used by management accountants to achieve organizational objectives. Desklib offers more solved assignments and past papers for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.