Financial Management Report: Kmart Ltd. and Warehouse NZ Comparison

VerifiedAdded on 2020/04/07

|10

|2172

|40

Report

AI Summary

This report presents a financial analysis of Kmart Ltd. and Warehouse NZ, comparing their performance based on financial ratios from 2014 to 2016. The analysis includes profitability, financial stability, and turnover ratios to assess their financial positions. The report evaluates Kmart's performance, highlighting trends in gross margin, return on assets, and debt-to-equity ratios. It compares Kmart's financial health with that of Warehouse NZ, concluding that while Kmart shows better financial stability, Warehouse NZ demonstrates stronger profitability and turnover. The report also includes pro-forma income statements for 2017 and 2018, and provides recommendations for Kmart to improve its financial performance, and advises Kiwibank Ltd. on the loan extension based on the findings. The data used is sourced from the companies' annual reports.

Running head: FINANCIAL MANAGEMENT

Financial management

Name of the student

Name of the university

Author note

Financial management

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................3

Findings......................................................................................................................................3

Section 1.................................................................................................................................3

Section 2.................................................................................................................................4

Analysis and interpretation........................................................................................................5

Section 1.................................................................................................................................5

Section 2.................................................................................................................................6

Section 3.................................................................................................................................7

Conclusion..................................................................................................................................8

Recommendation........................................................................................................................8

Reference & Bibliography.........................................................................................................9

Table of Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................3

Findings......................................................................................................................................3

Section 1.................................................................................................................................3

Section 2.................................................................................................................................4

Analysis and interpretation........................................................................................................5

Section 1.................................................................................................................................5

Section 2.................................................................................................................................6

Section 3.................................................................................................................................7

Conclusion..................................................................................................................................8

Recommendation........................................................................................................................8

Reference & Bibliography.........................................................................................................9

2FINANCIAL MANAGEMENT

Executive summary

The main objective of this report is to focus on the financial ratios of Kmart Ltd for the

purpose of the loan extension by Kiwibank Ltd. the report will further compare the ratios of

the company with one of the main competitor of the company that is, Warehouse NZ to

analyse the financial position of the company. The financial data of the company is collected

from the annual report for the year 2014, 2015 and 2016 published at their websites. It is

found that with regard to profitability position warehouse NZ is in better position as

compared to that of Kmart Ltd. However, if the financial stability ratios are considered, it can

be identified that Kmart is considerably at better position as compared to Warehouse NZ.

Further, with regard to turnover position Warehouse NZ is in better position as compared to

Kmart Ltd. therefore, it can be concluded that with regard to all over financial performance,

Warehouse NZ is in better position as compared to Kmart. However, if Kiwibank Ltd

considers the financial position to extend the loan, it can be identified that considering

financial position, it will not be a wise decision on the part of Kiwibank to extend the loan.

Executive summary

The main objective of this report is to focus on the financial ratios of Kmart Ltd for the

purpose of the loan extension by Kiwibank Ltd. the report will further compare the ratios of

the company with one of the main competitor of the company that is, Warehouse NZ to

analyse the financial position of the company. The financial data of the company is collected

from the annual report for the year 2014, 2015 and 2016 published at their websites. It is

found that with regard to profitability position warehouse NZ is in better position as

compared to that of Kmart Ltd. However, if the financial stability ratios are considered, it can

be identified that Kmart is considerably at better position as compared to Warehouse NZ.

Further, with regard to turnover position Warehouse NZ is in better position as compared to

Kmart Ltd. therefore, it can be concluded that with regard to all over financial performance,

Warehouse NZ is in better position as compared to Kmart. However, if Kiwibank Ltd

considers the financial position to extend the loan, it can be identified that considering

financial position, it will not be a wise decision on the part of Kiwibank to extend the loan.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

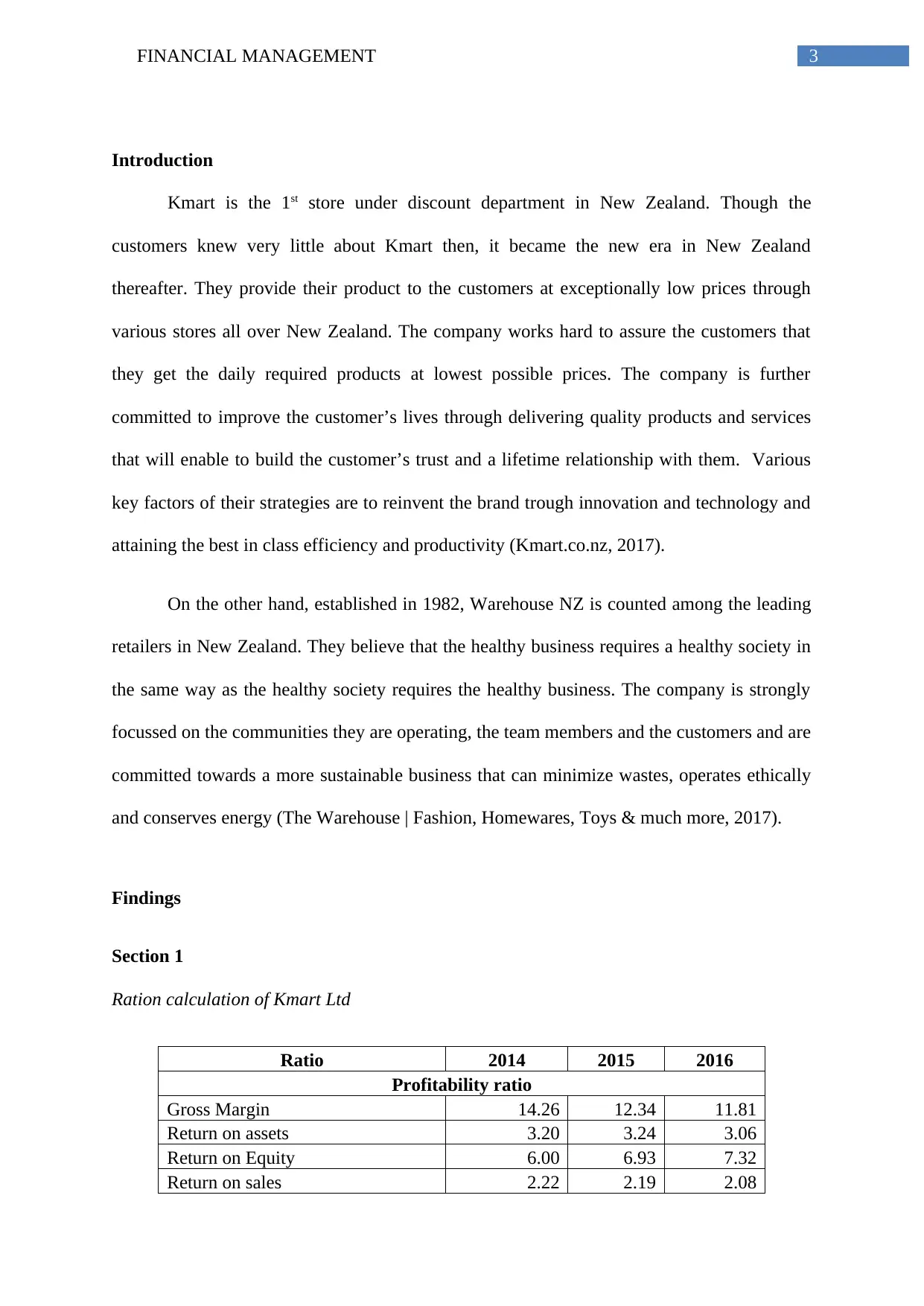

Introduction

Kmart is the 1st store under discount department in New Zealand. Though the

customers knew very little about Kmart then, it became the new era in New Zealand

thereafter. They provide their product to the customers at exceptionally low prices through

various stores all over New Zealand. The company works hard to assure the customers that

they get the daily required products at lowest possible prices. The company is further

committed to improve the customer’s lives through delivering quality products and services

that will enable to build the customer’s trust and a lifetime relationship with them. Various

key factors of their strategies are to reinvent the brand trough innovation and technology and

attaining the best in class efficiency and productivity (Kmart.co.nz, 2017).

On the other hand, established in 1982, Warehouse NZ is counted among the leading

retailers in New Zealand. They believe that the healthy business requires a healthy society in

the same way as the healthy society requires the healthy business. The company is strongly

focussed on the communities they are operating, the team members and the customers and are

committed towards a more sustainable business that can minimize wastes, operates ethically

and conserves energy (The Warehouse | Fashion, Homewares, Toys & much more, 2017).

Findings

Section 1

Ration calculation of Kmart Ltd

Ratio 2014 2015 2016

Profitability ratio

Gross Margin 14.26 12.34 11.81

Return on assets 3.20 3.24 3.06

Return on Equity 6.00 6.93 7.32

Return on sales 2.22 2.19 2.08

Introduction

Kmart is the 1st store under discount department in New Zealand. Though the

customers knew very little about Kmart then, it became the new era in New Zealand

thereafter. They provide their product to the customers at exceptionally low prices through

various stores all over New Zealand. The company works hard to assure the customers that

they get the daily required products at lowest possible prices. The company is further

committed to improve the customer’s lives through delivering quality products and services

that will enable to build the customer’s trust and a lifetime relationship with them. Various

key factors of their strategies are to reinvent the brand trough innovation and technology and

attaining the best in class efficiency and productivity (Kmart.co.nz, 2017).

On the other hand, established in 1982, Warehouse NZ is counted among the leading

retailers in New Zealand. They believe that the healthy business requires a healthy society in

the same way as the healthy society requires the healthy business. The company is strongly

focussed on the communities they are operating, the team members and the customers and are

committed towards a more sustainable business that can minimize wastes, operates ethically

and conserves energy (The Warehouse | Fashion, Homewares, Toys & much more, 2017).

Findings

Section 1

Ration calculation of Kmart Ltd

Ratio 2014 2015 2016

Profitability ratio

Gross Margin 14.26 12.34 11.81

Return on assets 3.20 3.24 3.06

Return on Equity 6.00 6.93 7.32

Return on sales 2.22 2.19 2.08

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

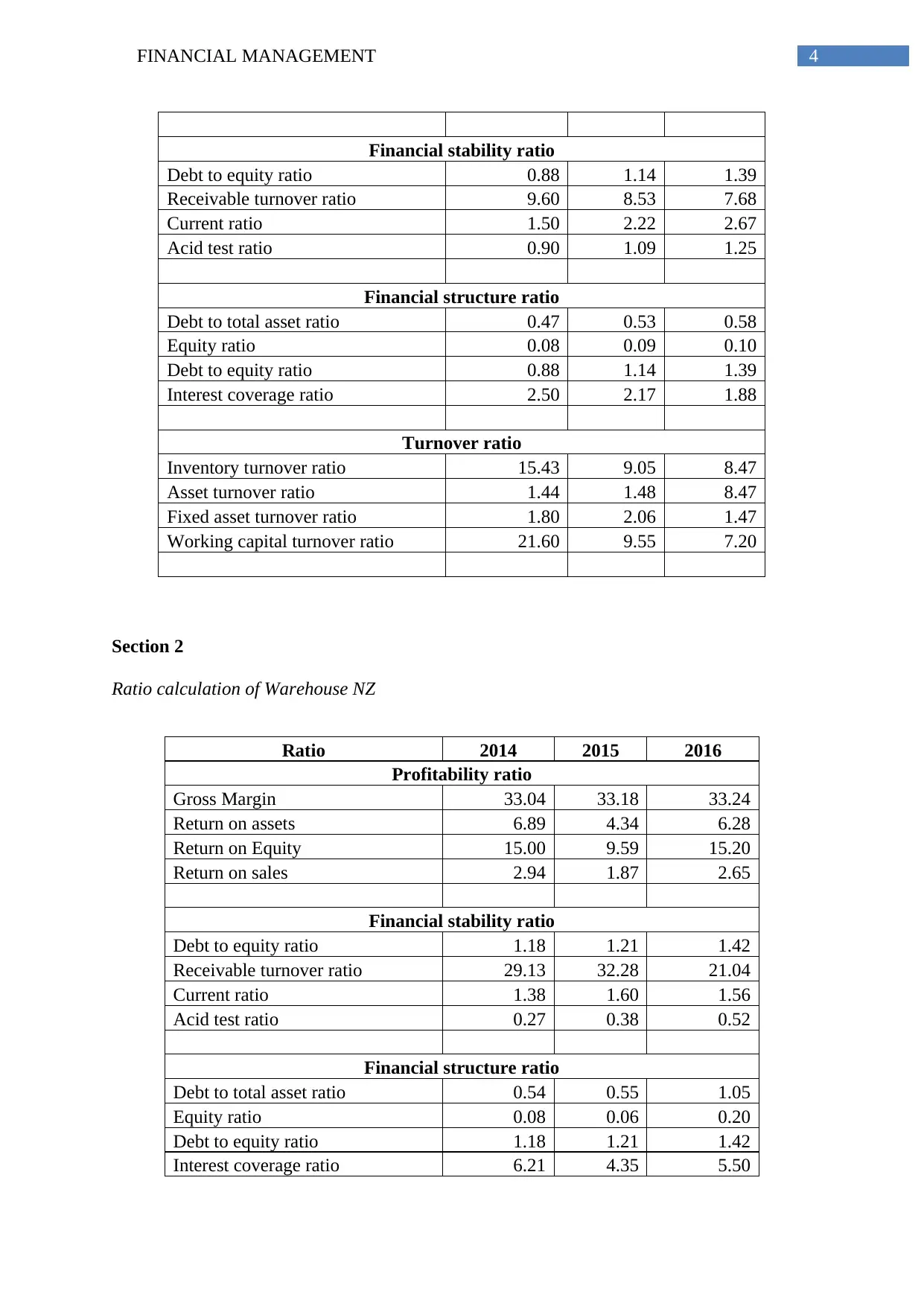

Financial stability ratio

Debt to equity ratio 0.88 1.14 1.39

Receivable turnover ratio 9.60 8.53 7.68

Current ratio 1.50 2.22 2.67

Acid test ratio 0.90 1.09 1.25

Financial structure ratio

Debt to total asset ratio 0.47 0.53 0.58

Equity ratio 0.08 0.09 0.10

Debt to equity ratio 0.88 1.14 1.39

Interest coverage ratio 2.50 2.17 1.88

Turnover ratio

Inventory turnover ratio 15.43 9.05 8.47

Asset turnover ratio 1.44 1.48 8.47

Fixed asset turnover ratio 1.80 2.06 1.47

Working capital turnover ratio 21.60 9.55 7.20

Section 2

Ratio calculation of Warehouse NZ

Ratio 2014 2015 2016

Profitability ratio

Gross Margin 33.04 33.18 33.24

Return on assets 6.89 4.34 6.28

Return on Equity 15.00 9.59 15.20

Return on sales 2.94 1.87 2.65

Financial stability ratio

Debt to equity ratio 1.18 1.21 1.42

Receivable turnover ratio 29.13 32.28 21.04

Current ratio 1.38 1.60 1.56

Acid test ratio 0.27 0.38 0.52

Financial structure ratio

Debt to total asset ratio 0.54 0.55 1.05

Equity ratio 0.08 0.06 0.20

Debt to equity ratio 1.18 1.21 1.42

Interest coverage ratio 6.21 4.35 5.50

Financial stability ratio

Debt to equity ratio 0.88 1.14 1.39

Receivable turnover ratio 9.60 8.53 7.68

Current ratio 1.50 2.22 2.67

Acid test ratio 0.90 1.09 1.25

Financial structure ratio

Debt to total asset ratio 0.47 0.53 0.58

Equity ratio 0.08 0.09 0.10

Debt to equity ratio 0.88 1.14 1.39

Interest coverage ratio 2.50 2.17 1.88

Turnover ratio

Inventory turnover ratio 15.43 9.05 8.47

Asset turnover ratio 1.44 1.48 8.47

Fixed asset turnover ratio 1.80 2.06 1.47

Working capital turnover ratio 21.60 9.55 7.20

Section 2

Ratio calculation of Warehouse NZ

Ratio 2014 2015 2016

Profitability ratio

Gross Margin 33.04 33.18 33.24

Return on assets 6.89 4.34 6.28

Return on Equity 15.00 9.59 15.20

Return on sales 2.94 1.87 2.65

Financial stability ratio

Debt to equity ratio 1.18 1.21 1.42

Receivable turnover ratio 29.13 32.28 21.04

Current ratio 1.38 1.60 1.56

Acid test ratio 0.27 0.38 0.52

Financial structure ratio

Debt to total asset ratio 0.54 0.55 1.05

Equity ratio 0.08 0.06 0.20

Debt to equity ratio 1.18 1.21 1.42

Interest coverage ratio 6.21 4.35 5.50

5FINANCIAL MANAGEMENT

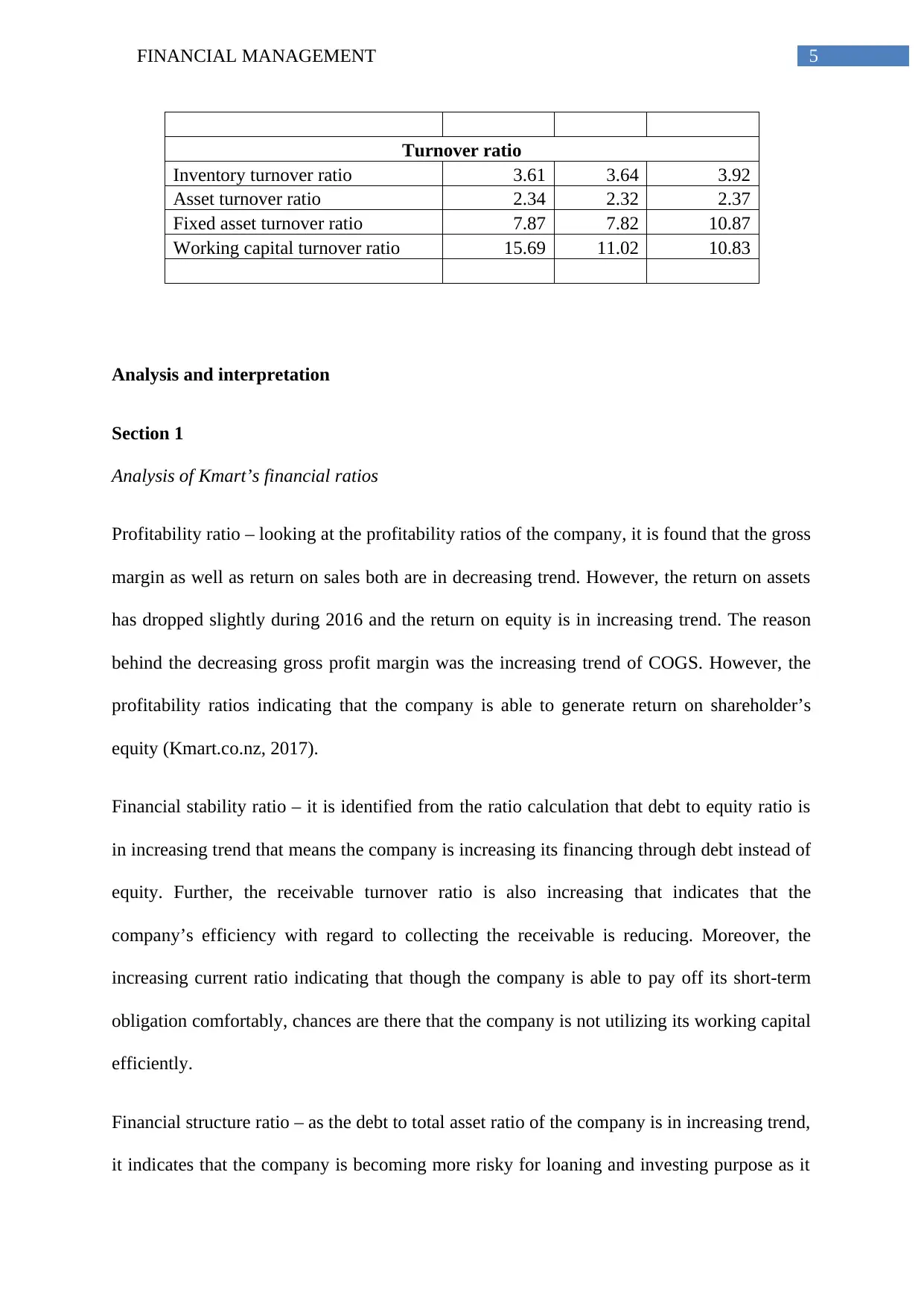

Turnover ratio

Inventory turnover ratio 3.61 3.64 3.92

Asset turnover ratio 2.34 2.32 2.37

Fixed asset turnover ratio 7.87 7.82 10.87

Working capital turnover ratio 15.69 11.02 10.83

Analysis and interpretation

Section 1

Analysis of Kmart’s financial ratios

Profitability ratio – looking at the profitability ratios of the company, it is found that the gross

margin as well as return on sales both are in decreasing trend. However, the return on assets

has dropped slightly during 2016 and the return on equity is in increasing trend. The reason

behind the decreasing gross profit margin was the increasing trend of COGS. However, the

profitability ratios indicating that the company is able to generate return on shareholder’s

equity (Kmart.co.nz, 2017).

Financial stability ratio – it is identified from the ratio calculation that debt to equity ratio is

in increasing trend that means the company is increasing its financing through debt instead of

equity. Further, the receivable turnover ratio is also increasing that indicates that the

company’s efficiency with regard to collecting the receivable is reducing. Moreover, the

increasing current ratio indicating that though the company is able to pay off its short-term

obligation comfortably, chances are there that the company is not utilizing its working capital

efficiently.

Financial structure ratio – as the debt to total asset ratio of the company is in increasing trend,

it indicates that the company is becoming more risky for loaning and investing purpose as it

Turnover ratio

Inventory turnover ratio 3.61 3.64 3.92

Asset turnover ratio 2.34 2.32 2.37

Fixed asset turnover ratio 7.87 7.82 10.87

Working capital turnover ratio 15.69 11.02 10.83

Analysis and interpretation

Section 1

Analysis of Kmart’s financial ratios

Profitability ratio – looking at the profitability ratios of the company, it is found that the gross

margin as well as return on sales both are in decreasing trend. However, the return on assets

has dropped slightly during 2016 and the return on equity is in increasing trend. The reason

behind the decreasing gross profit margin was the increasing trend of COGS. However, the

profitability ratios indicating that the company is able to generate return on shareholder’s

equity (Kmart.co.nz, 2017).

Financial stability ratio – it is identified from the ratio calculation that debt to equity ratio is

in increasing trend that means the company is increasing its financing through debt instead of

equity. Further, the receivable turnover ratio is also increasing that indicates that the

company’s efficiency with regard to collecting the receivable is reducing. Moreover, the

increasing current ratio indicating that though the company is able to pay off its short-term

obligation comfortably, chances are there that the company is not utilizing its working capital

efficiently.

Financial structure ratio – as the debt to total asset ratio of the company is in increasing trend,

it indicates that the company is becoming more risky for loaning and investing purpose as it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

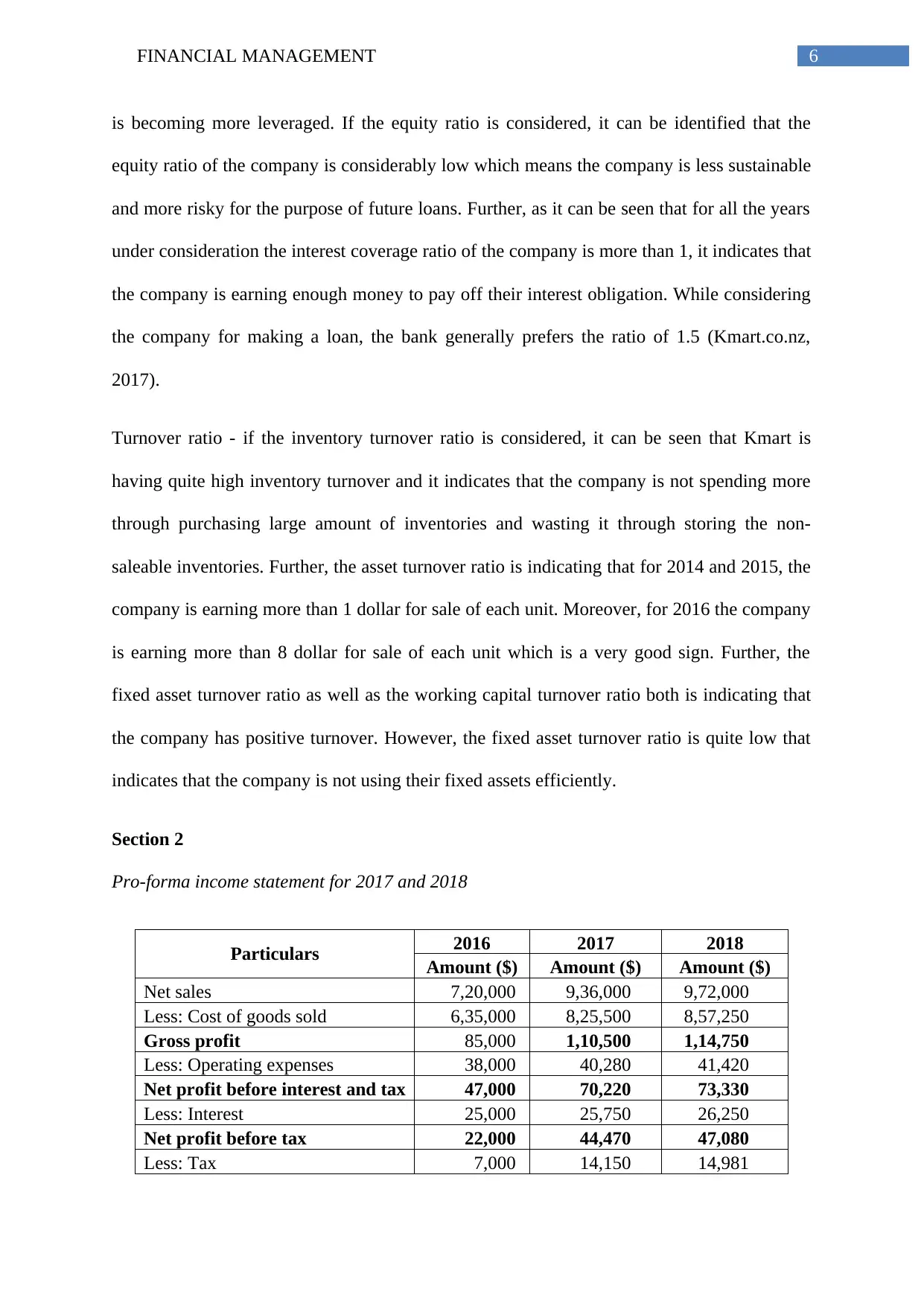

6FINANCIAL MANAGEMENT

is becoming more leveraged. If the equity ratio is considered, it can be identified that the

equity ratio of the company is considerably low which means the company is less sustainable

and more risky for the purpose of future loans. Further, as it can be seen that for all the years

under consideration the interest coverage ratio of the company is more than 1, it indicates that

the company is earning enough money to pay off their interest obligation. While considering

the company for making a loan, the bank generally prefers the ratio of 1.5 (Kmart.co.nz,

2017).

Turnover ratio - if the inventory turnover ratio is considered, it can be seen that Kmart is

having quite high inventory turnover and it indicates that the company is not spending more

through purchasing large amount of inventories and wasting it through storing the non-

saleable inventories. Further, the asset turnover ratio is indicating that for 2014 and 2015, the

company is earning more than 1 dollar for sale of each unit. Moreover, for 2016 the company

is earning more than 8 dollar for sale of each unit which is a very good sign. Further, the

fixed asset turnover ratio as well as the working capital turnover ratio both is indicating that

the company has positive turnover. However, the fixed asset turnover ratio is quite low that

indicates that the company is not using their fixed assets efficiently.

Section 2

Pro-forma income statement for 2017 and 2018

Particulars 2016 2017 2018

Amount ($) Amount ($) Amount ($)

Net sales 7,20,000 9,36,000 9,72,000

Less: Cost of goods sold 6,35,000 8,25,500 8,57,250

Gross profit 85,000 1,10,500 1,14,750

Less: Operating expenses 38,000 40,280 41,420

Net profit before interest and tax 47,000 70,220 73,330

Less: Interest 25,000 25,750 26,250

Net profit before tax 22,000 44,470 47,080

Less: Tax 7,000 14,150 14,981

is becoming more leveraged. If the equity ratio is considered, it can be identified that the

equity ratio of the company is considerably low which means the company is less sustainable

and more risky for the purpose of future loans. Further, as it can be seen that for all the years

under consideration the interest coverage ratio of the company is more than 1, it indicates that

the company is earning enough money to pay off their interest obligation. While considering

the company for making a loan, the bank generally prefers the ratio of 1.5 (Kmart.co.nz,

2017).

Turnover ratio - if the inventory turnover ratio is considered, it can be seen that Kmart is

having quite high inventory turnover and it indicates that the company is not spending more

through purchasing large amount of inventories and wasting it through storing the non-

saleable inventories. Further, the asset turnover ratio is indicating that for 2014 and 2015, the

company is earning more than 1 dollar for sale of each unit. Moreover, for 2016 the company

is earning more than 8 dollar for sale of each unit which is a very good sign. Further, the

fixed asset turnover ratio as well as the working capital turnover ratio both is indicating that

the company has positive turnover. However, the fixed asset turnover ratio is quite low that

indicates that the company is not using their fixed assets efficiently.

Section 2

Pro-forma income statement for 2017 and 2018

Particulars 2016 2017 2018

Amount ($) Amount ($) Amount ($)

Net sales 7,20,000 9,36,000 9,72,000

Less: Cost of goods sold 6,35,000 8,25,500 8,57,250

Gross profit 85,000 1,10,500 1,14,750

Less: Operating expenses 38,000 40,280 41,420

Net profit before interest and tax 47,000 70,220 73,330

Less: Interest 25,000 25,750 26,250

Net profit before tax 22,000 44,470 47,080

Less: Tax 7,000 14,150 14,981

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

Net profit after tax 15,000 30,320 32,099

Section 3

Comparison of Kmart’s theory with Warehouse

Profitability ratio – it can be identified that all the ratios under profitability that is the gross

margin ratio, return on assets ratio, return on equity ratio and return on sales are better for the

Warehouse NZ as compared to Kmart Ltd. Therefore, Kmart shall take necessary steps to

increase its profitability.

Financial stability ratio – if the financial stability ratios are considered, it can be identified

that Kmart is considerably at better position as compared to Warehouse NZ. The financial

stability indicates that the company is in better position while asking for any loan or when the

investor considers the company for investment purpose (The Warehouse | Fashion,

Homewares, Toys & much more, 2017).

Financial structure ratio - if the financial stability ratios are considered, it can be identified

that Warehouse NZ is considerably at better position as compared to Kmart as Warehouse NZ

is in better position with respect to interest coverage ratio and is in the better position to pay-

off its interests.

Turnover ratio – if the inventory turnover ratio is taken into account, it can be identified that

the inventory turnover ratio of Kmart is better as compared to Warehouse NZ; However, the

other three ratios under turnover that is the asset turnover ratio, working capital turnover ratio

and fixed asset turnover ratio is better for Warehouse NZ is better as compared to that of

Kmart. Therefore, it is evidential that the turnover position of Warehouse NZ is far better

than Kmart (The Warehouse | Fashion, Homewares, Toys & much more, 2017).

Net profit after tax 15,000 30,320 32,099

Section 3

Comparison of Kmart’s theory with Warehouse

Profitability ratio – it can be identified that all the ratios under profitability that is the gross

margin ratio, return on assets ratio, return on equity ratio and return on sales are better for the

Warehouse NZ as compared to Kmart Ltd. Therefore, Kmart shall take necessary steps to

increase its profitability.

Financial stability ratio – if the financial stability ratios are considered, it can be identified

that Kmart is considerably at better position as compared to Warehouse NZ. The financial

stability indicates that the company is in better position while asking for any loan or when the

investor considers the company for investment purpose (The Warehouse | Fashion,

Homewares, Toys & much more, 2017).

Financial structure ratio - if the financial stability ratios are considered, it can be identified

that Warehouse NZ is considerably at better position as compared to Kmart as Warehouse NZ

is in better position with respect to interest coverage ratio and is in the better position to pay-

off its interests.

Turnover ratio – if the inventory turnover ratio is taken into account, it can be identified that

the inventory turnover ratio of Kmart is better as compared to Warehouse NZ; However, the

other three ratios under turnover that is the asset turnover ratio, working capital turnover ratio

and fixed asset turnover ratio is better for Warehouse NZ is better as compared to that of

Kmart. Therefore, it is evidential that the turnover position of Warehouse NZ is far better

than Kmart (The Warehouse | Fashion, Homewares, Toys & much more, 2017).

8FINANCIAL MANAGEMENT

Conclusion

From the above analysis and interpretation of Kmart Ltd. as well as Warehouse NZ, it

is found that both the companies are among the leading retailers in New Zealand and hold a

large amount of market share. However, from the financial analysis of both the companies it

is found that with regard to profitability position warehouse NZ is in better position as

compared to that of Kmart Ltd. However, if the financial stability ratios are considered, it can

be identified that Kmart is considerably at better position as compared to Warehouse NZ.

Further, Warehouse NZ is in better position to pay off their interest. Further, with regard to

turnover position Warehouse NZ is in better position as compared to Kmart Ltd. therefore, it

can be concluded that with regard to all over financial performance, Warehouse NZ is in

better position as compared to Kmart.

Recommendation

It can be recommended that Kmart shall try to reduce their operating expenses as well

as COGS to improve its profitability position. Further, the company shall take necessary steps

to increase its sales, so that it can achieve better turnover position. However, if Kiwibank Ltd

considers the financial position to extend the loan, it can be identified that considering

financial position, as the debt to total asset ratio of the company is in increasing trend, it

indicates that the company is becoming more risky for loaning and investing purpose as it is

becoming more leveraged. Further, if the equity ratio is considered, it can be identified that

the equity ratio of the company is considerably low which means the company is less

sustainable and more risky for the purpose of future loans. Therefore, it will not be a wise

decision on the part of Kiwibank to extend the loan.

Conclusion

From the above analysis and interpretation of Kmart Ltd. as well as Warehouse NZ, it

is found that both the companies are among the leading retailers in New Zealand and hold a

large amount of market share. However, from the financial analysis of both the companies it

is found that with regard to profitability position warehouse NZ is in better position as

compared to that of Kmart Ltd. However, if the financial stability ratios are considered, it can

be identified that Kmart is considerably at better position as compared to Warehouse NZ.

Further, Warehouse NZ is in better position to pay off their interest. Further, with regard to

turnover position Warehouse NZ is in better position as compared to Kmart Ltd. therefore, it

can be concluded that with regard to all over financial performance, Warehouse NZ is in

better position as compared to Kmart.

Recommendation

It can be recommended that Kmart shall try to reduce their operating expenses as well

as COGS to improve its profitability position. Further, the company shall take necessary steps

to increase its sales, so that it can achieve better turnover position. However, if Kiwibank Ltd

considers the financial position to extend the loan, it can be identified that considering

financial position, as the debt to total asset ratio of the company is in increasing trend, it

indicates that the company is becoming more risky for loaning and investing purpose as it is

becoming more leveraged. Further, if the equity ratio is considered, it can be identified that

the equity ratio of the company is considerably low which means the company is less

sustainable and more risky for the purpose of future loans. Therefore, it will not be a wise

decision on the part of Kiwibank to extend the loan.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

Reference & Bibliography

Bodie, Z. (2013). Investments. McGraw-Hill.

Collier, P. M. (2015). Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Ecer, F., & Boyukaslan, A. (2014). Measuring performances of football clubs using financial

ratios: the gray relational analysis approach. American Journal of Economics, 4(1),

62-71.

Innocent, E. C., Mary, O. I., & Matthew, O. M. (2013). Financial ratio analysis as a

determinant of profitability in Nigerian pharmaceutical industry. International journal

of business and management, 8(8), 107.

Kmart.co.nz. (2017). Kmart.co.nz. Retrieved 1 October 2017, from http://www.kmart.co.nz/

Ogiela, L. (2013). Data management in cognitive financial systems. International Journal of

Information Management, 33(2), 263-270.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

The Warehouse | Fashion, Homewares, Toys & much more. (2017). Thewarehouse.co.nz.

Retrieved 1 October 2017, from http://www.thewarehouse.co.nz/

Reference & Bibliography

Bodie, Z. (2013). Investments. McGraw-Hill.

Collier, P. M. (2015). Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Ecer, F., & Boyukaslan, A. (2014). Measuring performances of football clubs using financial

ratios: the gray relational analysis approach. American Journal of Economics, 4(1),

62-71.

Innocent, E. C., Mary, O. I., & Matthew, O. M. (2013). Financial ratio analysis as a

determinant of profitability in Nigerian pharmaceutical industry. International journal

of business and management, 8(8), 107.

Kmart.co.nz. (2017). Kmart.co.nz. Retrieved 1 October 2017, from http://www.kmart.co.nz/

Ogiela, L. (2013). Data management in cognitive financial systems. International Journal of

Information Management, 33(2), 263-270.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

The Warehouse | Fashion, Homewares, Toys & much more. (2017). Thewarehouse.co.nz.

Retrieved 1 October 2017, from http://www.thewarehouse.co.nz/

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.