Accounting Financial Analysis Report: Impairment Loss and Allocation

VerifiedAdded on 2023/06/05

|6

|1413

|442

Report

AI Summary

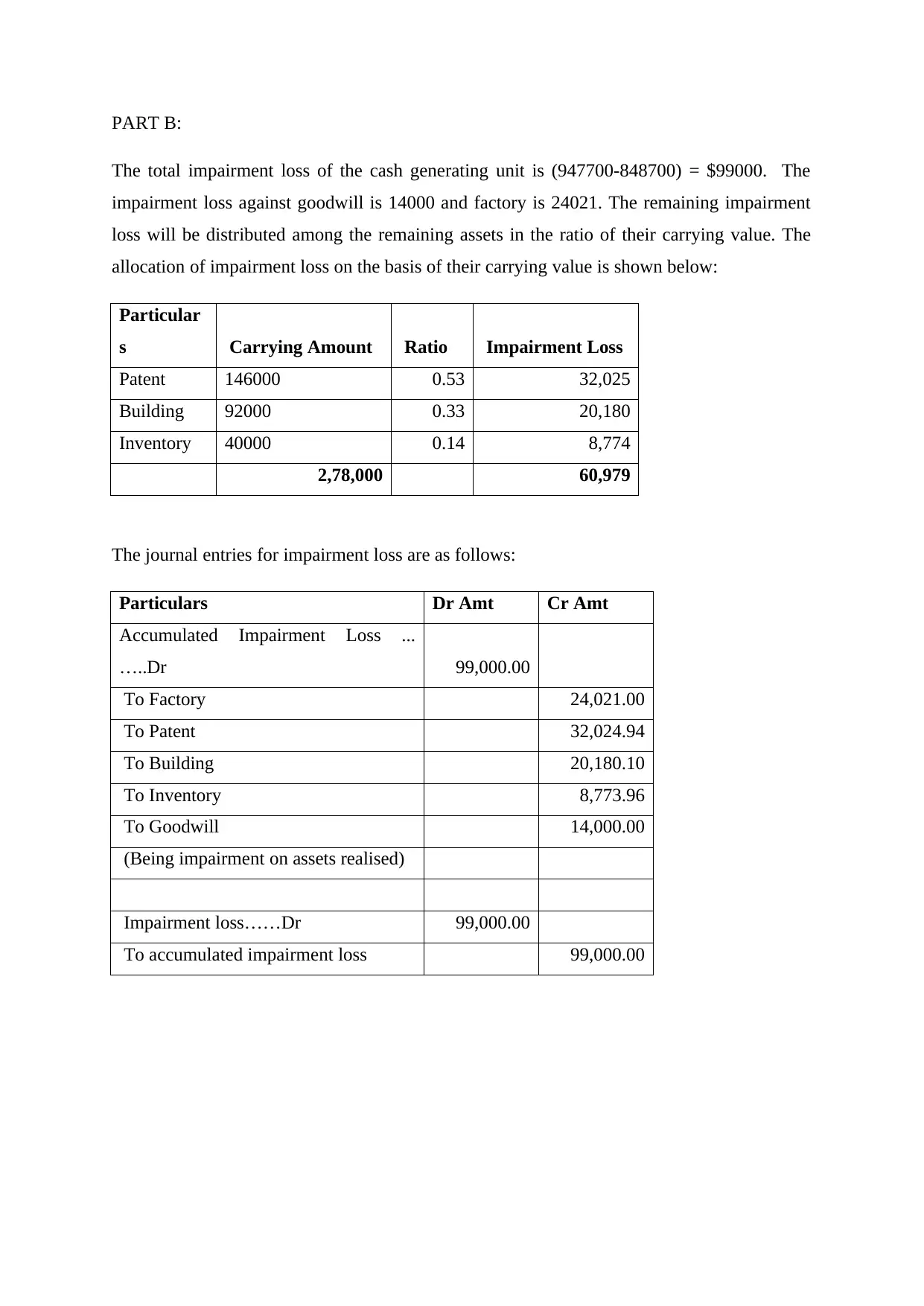

This financial analysis report discusses impairment tests, which identify and record assets with carrying values exceeding their recoverable amounts. It explains the process of determining the recoverable amount for cash-generating units (CGUs) and the factors influencing it, such as cash generation and management efficiency. The report details the methodology for impairment testing, involving a comparison between recoverable and carrying amounts, and the distribution of impairment losses among CGU assets. It also covers calculating the recoverable amount using fair value and value in use, including estimating future cash flows and determining appropriate discount rates. The analysis includes considerations for cash flow estimation, exclusions like tax and borrowing costs, and the use of traditional and cash flow approaches for present value calculations. The report further explains fair value less cost of sell and concludes with a practical example of impairment loss allocation and corresponding journal entries, illustrating the accounting treatment of impaired assets. Desklib offers a wide range of resources, including past papers and solved assignments, to support students in their academic endeavors.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.