Financial Feasibility Analysis of Pinto Ltd Project - ACC00716

VerifiedAdded on 2023/06/11

|6

|1141

|267

Report

AI Summary

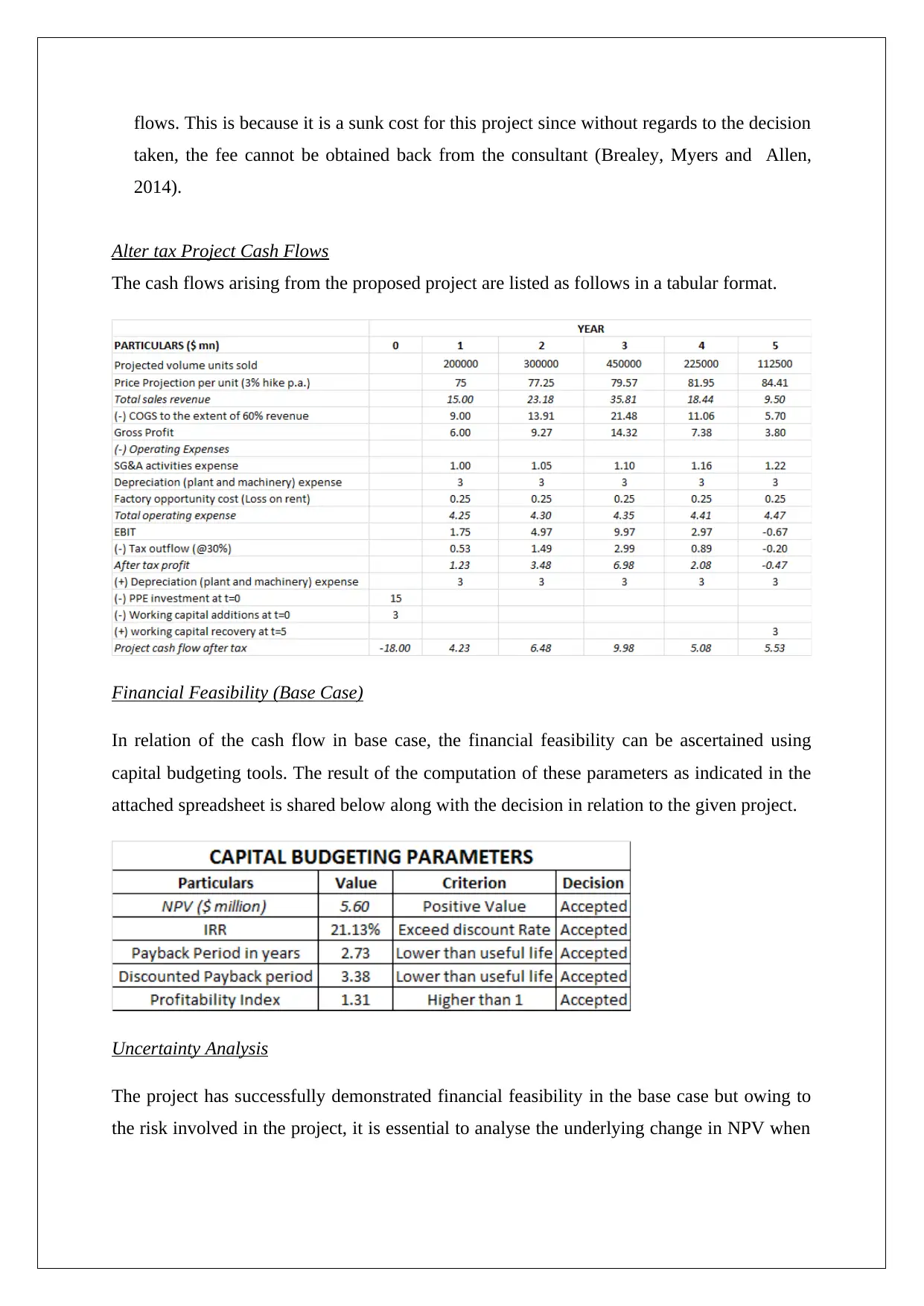

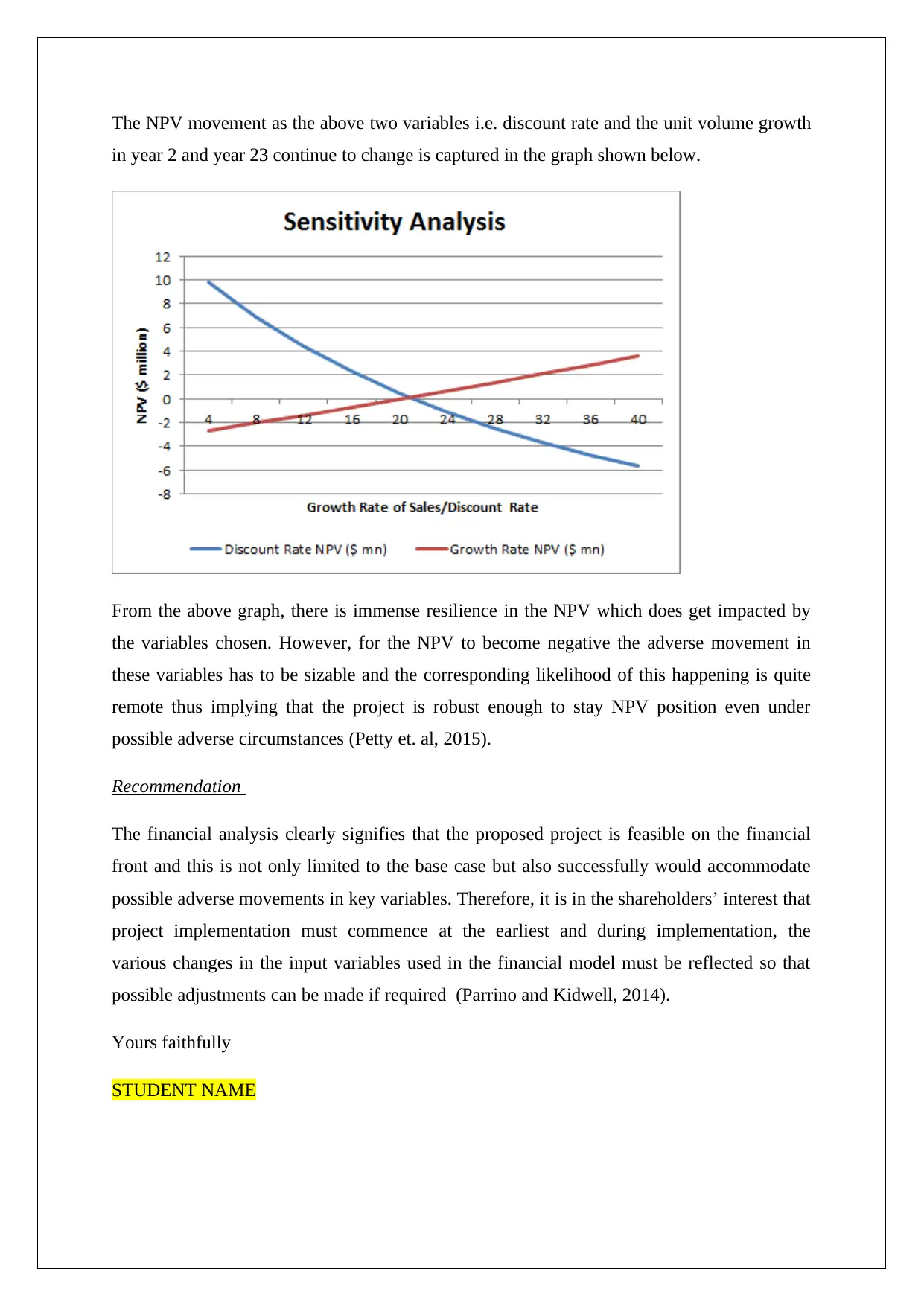

This report provides a financial analysis of Pinto Ltd's proposed new product launch, addressing concerns about increasing competition. It assesses the project's financial feasibility using capital budgeting tools such as NPV, IRR, payback period, discounted payback period, and profitability index. The analysis considers incremental post-tax cash flows, the opportunity cost of using an existing manufacturing base, and sunk costs. Uncertainty analysis, including scenario and sensitivity analyses, examines the project's robustness under varying discount rates and unit sales growth rates. The report concludes with a recommendation to proceed with the project, highlighting its financial viability and resilience to adverse conditions, while emphasizing the importance of ongoing monitoring and adjustments during implementation.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.