Financial Performance and Investment Decisions at Madison Plc

VerifiedAdded on 2020/01/07

|13

|3710

|206

Report

AI Summary

This report provides a comprehensive financial analysis of Madison Plc, a UK-based public limited company. It examines various sources of funding, including borrowings, retained earnings, leases, share capital, and bank overdrafts, with a recommendation for a bank loan to support its expansion. The report also assesses the impact of efficient working capital management on Madison Plc's cash flow. Furthermore, it delves into investment appraisal techniques, specifically net present value (NPV) and internal rate of return (IRR), to evaluate two software investment proposals, recommending the project with the higher NPV and IRR. Break-even analysis is explained for short-term decision-making. In addition to financial factors, the report considers non-financial factors such as manpower, government regulations, and competitor actions in investment decisions. Finally, it includes a ratio analysis to evaluate Madison Plc's financial performance, offering insights for effective decision-making and long-term survival. The report concludes with recommendations to guide Madison Plc's financial strategies.

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION................................................................................................................................

1. Different sources of funds, advantage and disadvantage with the recommendation to

Madison Plc for planned expansion programme.........................................................................1

2. Impact of efficient working capital on Madison Plc's cash flow.............................................2

3. Investment appraisal techniques..............................................................................................3

4. Explanation of the break-even chart for short-term decision..................................................4

Other factors in investing appraisal techniques:..........................................................................5

5 Ratio Analysis...........................................................................................................................5

Conclusion............................................................................................................................................

References............................................................................................................................................

Appendix..............................................................................................................................................

Cash Flow....................................................................................................................................9

Net Present Value......................................................................................................................10

Internal Rate of Return..............................................................................................................11

Ratio Analysis............................................................................................................................12

INTRODUCTION................................................................................................................................

1. Different sources of funds, advantage and disadvantage with the recommendation to

Madison Plc for planned expansion programme.........................................................................1

2. Impact of efficient working capital on Madison Plc's cash flow.............................................2

3. Investment appraisal techniques..............................................................................................3

4. Explanation of the break-even chart for short-term decision..................................................4

Other factors in investing appraisal techniques:..........................................................................5

5 Ratio Analysis...........................................................................................................................5

Conclusion............................................................................................................................................

References............................................................................................................................................

Appendix..............................................................................................................................................

Cash Flow....................................................................................................................................9

Net Present Value......................................................................................................................10

Internal Rate of Return..............................................................................................................11

Ratio Analysis............................................................................................................................12

INTRODUCTION

Finance is the soul for every business organization because any organization cannot

survive in the market without having sufficient amount of funds (Brealey and et.al, 2012).

Moreover not only the acquisition of appropriate funds but also its proper management is

necessary to compete effectively. Present report is based on the financial management of

Madison Plc. It is a public limited company operating in UK from past 10 years. It provides

intellectual property to Oil and Gas companies, HR consultants, Marketing companies, Tourist

companies and investment property funds all over the UK. The report will discuss various

sources of finance, investment appraisal tools and break-even analysis to take short-term as well

as long-term investment decisions. Moreover, the report will carry out an analysis of financial

performance of Madison Plc through ratio analysis. It will helps to evaluate and examine

business performance and take effective decisions for long term survival.

1. Different sources of funds, advantage and disadvantage with the recommendation to Madison

Plc for planned expansion programme

Present scenario stated that Madison Plc is earning good profit by retaining its previous

clients. However, in order to capture large market, it is planning to expand its operation and need

funds for this purpose. There are different sources that can be used by Madison Plc that are

illustrated below:

Borrowings: Madison Plc can acquire funds through financial institutions such as banks.

They provides funds for different time duration as per the firm's requirement. Bank provide

funds on an implied interest rate. The advantage of using bank loan is it helps to fulfil financial

need for different time duration (Embrechts, Klüppelberg and Mikosch, 2013). Moreover, it

helps to gather large amount of funds for the planned expansion and provide tax benefits also.

However, its disadvantage is Madison Plc need to pay regular interest as their finance cost.

Henceforth, it impose a fixed financial burden to the organization. Moreover, firm need to keep

any of the assets as collateral security against loan taken. If firm fails to meet out its financial

obligations than bank has right to sell collateral security and recover funds.

Retained earnings: Retained earnings is the available surplus after meet out all the

operational expenditures and dividend payment. It is an internal finance sources and Madison Plc

can use its retained earnings for the expansion purpose (Kotz, Kozubowski and Podgorski,

2012). Its benefit is this is cost free finance sources as firm will not have to pay any interest or

1

Finance is the soul for every business organization because any organization cannot

survive in the market without having sufficient amount of funds (Brealey and et.al, 2012).

Moreover not only the acquisition of appropriate funds but also its proper management is

necessary to compete effectively. Present report is based on the financial management of

Madison Plc. It is a public limited company operating in UK from past 10 years. It provides

intellectual property to Oil and Gas companies, HR consultants, Marketing companies, Tourist

companies and investment property funds all over the UK. The report will discuss various

sources of finance, investment appraisal tools and break-even analysis to take short-term as well

as long-term investment decisions. Moreover, the report will carry out an analysis of financial

performance of Madison Plc through ratio analysis. It will helps to evaluate and examine

business performance and take effective decisions for long term survival.

1. Different sources of funds, advantage and disadvantage with the recommendation to Madison

Plc for planned expansion programme

Present scenario stated that Madison Plc is earning good profit by retaining its previous

clients. However, in order to capture large market, it is planning to expand its operation and need

funds for this purpose. There are different sources that can be used by Madison Plc that are

illustrated below:

Borrowings: Madison Plc can acquire funds through financial institutions such as banks.

They provides funds for different time duration as per the firm's requirement. Bank provide

funds on an implied interest rate. The advantage of using bank loan is it helps to fulfil financial

need for different time duration (Embrechts, Klüppelberg and Mikosch, 2013). Moreover, it

helps to gather large amount of funds for the planned expansion and provide tax benefits also.

However, its disadvantage is Madison Plc need to pay regular interest as their finance cost.

Henceforth, it impose a fixed financial burden to the organization. Moreover, firm need to keep

any of the assets as collateral security against loan taken. If firm fails to meet out its financial

obligations than bank has right to sell collateral security and recover funds.

Retained earnings: Retained earnings is the available surplus after meet out all the

operational expenditures and dividend payment. It is an internal finance sources and Madison Plc

can use its retained earnings for the expansion purpose (Kotz, Kozubowski and Podgorski,

2012). Its benefit is this is cost free finance sources as firm will not have to pay any interest or

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other kind of cost on this. However, its disadvantage is excessive ploughing back of returns may

impair the ability to mitigate any financial urgencies. Furthermore, it will be available to a

limited extent.

Lease: Lease is the finance source in which Madison Plc can acquire building on lease.

Its advantage is firm does not need to purchase assets in cash thus, it will reduce the need of high

capital expenditure (Minsky, 2015). However, on the other hand, Madison Plc need to pay

regular rental charges to the lessor which includes some interest charges also. Thus, it bring fixed

financial cost to the Madison Plc.

Share capital: Madison Plc can issue share capital in the market and gather large amount

of funds. Firms can issue both the preference and equity shares and collect appropriate amount of

funds to support its expansion. The advantage is Madison Plc does not need to pay regular return

to the shareholder in terms of dividend (Tirole, 2010). However, its negative point is it diversify

or dilute controlling rights to the shareholders through which they can control business operation.

Moreover, no tax benefits will be available to the business on dividend payment.

Bank overdraft: Bank provide facility to withdraw larger amount than available balance

in the account. Its advantage is it helps to mitigate urgent financial need of Madison Plc while its

disadvantage is firm will need to pay interest charges on the overdraft taken and bank often

charges a high rate of interest on this facility (Mandelbrot, 2013). Moreover, it does not provide

facility to meet our long term finance requirement.

Thus, on the basis of above findings, it can be reported that finance manager of Madison

Plc should gather funds through bank loan. It is because it is earning good profitability hence,

will be able to bear fixed financial burden in terms of interest. Moreover, loan interest is an

allowable expenditure for tax computation hence, it will reduce tax obligations and enhance

profitability as well. Furthermore, it does not dilute controlling rights to the lenders hence, this

rights can be fully secured in the hand of owners.

2. Impact of efficient working capital on Madison Plc's cash flow

Madison Plc will need working capital to support its daily functioning otherwise, it will

not be able to done its operations effectively. For instance, Madison Plc has to pay staff salary,

office expenses such as postage, stationery, advertisement, building rent, insurance, utilities

payment such as electricity bill, telephone charges and so on (Gitman, Juchau and Flanagan,

2010). Thus, firm need to efficiently use its capital structure in order to maintain its cash flow. It

2

impair the ability to mitigate any financial urgencies. Furthermore, it will be available to a

limited extent.

Lease: Lease is the finance source in which Madison Plc can acquire building on lease.

Its advantage is firm does not need to purchase assets in cash thus, it will reduce the need of high

capital expenditure (Minsky, 2015). However, on the other hand, Madison Plc need to pay

regular rental charges to the lessor which includes some interest charges also. Thus, it bring fixed

financial cost to the Madison Plc.

Share capital: Madison Plc can issue share capital in the market and gather large amount

of funds. Firms can issue both the preference and equity shares and collect appropriate amount of

funds to support its expansion. The advantage is Madison Plc does not need to pay regular return

to the shareholder in terms of dividend (Tirole, 2010). However, its negative point is it diversify

or dilute controlling rights to the shareholders through which they can control business operation.

Moreover, no tax benefits will be available to the business on dividend payment.

Bank overdraft: Bank provide facility to withdraw larger amount than available balance

in the account. Its advantage is it helps to mitigate urgent financial need of Madison Plc while its

disadvantage is firm will need to pay interest charges on the overdraft taken and bank often

charges a high rate of interest on this facility (Mandelbrot, 2013). Moreover, it does not provide

facility to meet our long term finance requirement.

Thus, on the basis of above findings, it can be reported that finance manager of Madison

Plc should gather funds through bank loan. It is because it is earning good profitability hence,

will be able to bear fixed financial burden in terms of interest. Moreover, loan interest is an

allowable expenditure for tax computation hence, it will reduce tax obligations and enhance

profitability as well. Furthermore, it does not dilute controlling rights to the lenders hence, this

rights can be fully secured in the hand of owners.

2. Impact of efficient working capital on Madison Plc's cash flow

Madison Plc will need working capital to support its daily functioning otherwise, it will

not be able to done its operations effectively. For instance, Madison Plc has to pay staff salary,

office expenses such as postage, stationery, advertisement, building rent, insurance, utilities

payment such as electricity bill, telephone charges and so on (Gitman, Juchau and Flanagan,

2010). Thus, firm need to efficiently use its capital structure in order to maintain its cash flow. It

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can be done by optimum allocation of resources through projection. Madison Plc can determine

potential expenses and incomes through forecasting so that firm will be able to manage its

routine functions. Through this, Madison Plc can estimate future revenues and allocate it in

different operating functions in order to assure maximum utilization of it (Bakand, Hayes and

Dechsakulthorn, 2012). This in turn, it can manage its revenues and control cost so that results in

better availability of working capital and cash flows as well. Thus, it became clear that larger

sales revenues and curtailment of expenditures will assist finance manager to have surplus cash

available to support its routine functions.

3. Investment appraisal techniques

It is also known as capital budgeting tool helps to determine attractiveness of different

investment proposals available and select best proposal. As per the scenario, Madison Plc is

looking to invest in new software product (Wilmott, 2013). Company have two mutually

exclusive proposal available for this that are Madison Super and Madison Platform, having an

equal estimated life of 5 years. Now, firm is intending to invest in one of the two proposals thus,

investment appraisal techniques will greatly assist finance manager to determine most viable

project that will provide more benefits to the organization.

Net present value (NPV): It is the discounted cash flow techniques that forecast future

values of all the potential cash flows during project life time (Buchanan, 2014). However, the

difference between initial project cost and sum of all the discounted value is known as net

present value. The selection criteria of the method says that Madison Plc should invest funds in

the project that have higher NPV compare to other. The most important benefit of this techniques

is that it consider the time value of money and compute actual profit potential of the project.

While, on the other hand, its limitation is considering an appropriate discount rate is very

difficult task. It is because market uncertainties such as interest rate have a direct impact on it

(Chernow, 2010). Thus, incorrect discount rate may lead to harmful business decisions. For the

present scenario, NPV has been computed at 14% and 10% discount rate for Madison Super and

13% and 11% rate for Madison Platform.

Internal rate of return (IRR): It is the rate at which total discounted cash inflows will be

equal to the initial investment. In other words, NPV at this rate will be nil (Damodaran, 2010).

The selection criteria of the method says that Madison Plc should invest funds in project that

have higher IRR than other.

3

potential expenses and incomes through forecasting so that firm will be able to manage its

routine functions. Through this, Madison Plc can estimate future revenues and allocate it in

different operating functions in order to assure maximum utilization of it (Bakand, Hayes and

Dechsakulthorn, 2012). This in turn, it can manage its revenues and control cost so that results in

better availability of working capital and cash flows as well. Thus, it became clear that larger

sales revenues and curtailment of expenditures will assist finance manager to have surplus cash

available to support its routine functions.

3. Investment appraisal techniques

It is also known as capital budgeting tool helps to determine attractiveness of different

investment proposals available and select best proposal. As per the scenario, Madison Plc is

looking to invest in new software product (Wilmott, 2013). Company have two mutually

exclusive proposal available for this that are Madison Super and Madison Platform, having an

equal estimated life of 5 years. Now, firm is intending to invest in one of the two proposals thus,

investment appraisal techniques will greatly assist finance manager to determine most viable

project that will provide more benefits to the organization.

Net present value (NPV): It is the discounted cash flow techniques that forecast future

values of all the potential cash flows during project life time (Buchanan, 2014). However, the

difference between initial project cost and sum of all the discounted value is known as net

present value. The selection criteria of the method says that Madison Plc should invest funds in

the project that have higher NPV compare to other. The most important benefit of this techniques

is that it consider the time value of money and compute actual profit potential of the project.

While, on the other hand, its limitation is considering an appropriate discount rate is very

difficult task. It is because market uncertainties such as interest rate have a direct impact on it

(Chernow, 2010). Thus, incorrect discount rate may lead to harmful business decisions. For the

present scenario, NPV has been computed at 14% and 10% discount rate for Madison Super and

13% and 11% rate for Madison Platform.

Internal rate of return (IRR): It is the rate at which total discounted cash inflows will be

equal to the initial investment. In other words, NPV at this rate will be nil (Damodaran, 2010).

The selection criteria of the method says that Madison Plc should invest funds in project that

have higher IRR than other.

3

Recommendations: Net present value of Madison Super software at 14% rate is £3124724

whilst Madison Platform's NPV at 13% rate is £2524365. NPV is higher in Madison Super

Software henceforth, it can be recommended that Madison Plc should invest funds in this project

because it will provide greater benefits to the organization. Moreover, IRR of both the projects

are 32% and 23%. It is higher in Madison Super software by 11%. Moreover, if firm uses 10%

discount rate for Madison Super and 11% discount rate for Madison Platform than project will

generate NPV of £4192399 and £3186361. Thus, it can be seen that Madison Super Software

will generate larger profits and it enable company to gather large profitability. Thus, it can be

recommended that Madison Plc should invest funds in this project. Through investing in this,

firm will be able to enhance its profitability to a great extent.

4. Explanation of the break-even chart for short-term decision

Break-even point (BEP): It is the point at which total revenues and total business

expenditure of Madison Plc will be equal. In other words, it can be said that there is no profit no

loss situation (Hyman, 2013). Madison plc has to assure that their sales revenue must reach at the

BEP level. It is because, it is the point at where resources are optimally utilized and after that,

every additional unit of sale will results in high profits for Madison Plc.

Break-even point (In units) = Total Fixed cost (TFC)/ contribution per unit

Break-even point (In £) = Total fixed cost/profit volume ratio

For instance, if TFC = £100000

Sales revenue = £250000

Variable cost = £100000

Total units = 10000 units

Total Contribution £250000- £100000 = £50000

Contribution Per Unit £50000/10000 = £5

BEP (In units) £100000/£5 = 20000 units

Profit-Volume Ratio £50000/£250000*100 = 20%

BEP (In £) £100000/20% = £500000

Hence, it became clear that Madison plc has to generate higher sales revenue than BEP of

4

whilst Madison Platform's NPV at 13% rate is £2524365. NPV is higher in Madison Super

Software henceforth, it can be recommended that Madison Plc should invest funds in this project

because it will provide greater benefits to the organization. Moreover, IRR of both the projects

are 32% and 23%. It is higher in Madison Super software by 11%. Moreover, if firm uses 10%

discount rate for Madison Super and 11% discount rate for Madison Platform than project will

generate NPV of £4192399 and £3186361. Thus, it can be seen that Madison Super Software

will generate larger profits and it enable company to gather large profitability. Thus, it can be

recommended that Madison Plc should invest funds in this project. Through investing in this,

firm will be able to enhance its profitability to a great extent.

4. Explanation of the break-even chart for short-term decision

Break-even point (BEP): It is the point at which total revenues and total business

expenditure of Madison Plc will be equal. In other words, it can be said that there is no profit no

loss situation (Hyman, 2013). Madison plc has to assure that their sales revenue must reach at the

BEP level. It is because, it is the point at where resources are optimally utilized and after that,

every additional unit of sale will results in high profits for Madison Plc.

Break-even point (In units) = Total Fixed cost (TFC)/ contribution per unit

Break-even point (In £) = Total fixed cost/profit volume ratio

For instance, if TFC = £100000

Sales revenue = £250000

Variable cost = £100000

Total units = 10000 units

Total Contribution £250000- £100000 = £50000

Contribution Per Unit £50000/10000 = £5

BEP (In units) £100000/£5 = 20000 units

Profit-Volume Ratio £50000/£250000*100 = 20%

BEP (In £) £100000/20% = £500000

Hence, it became clear that Madison plc has to generate higher sales revenue than BEP of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

£500000 so that it can generate profits. However, if this sales target is not achieve than it may

face business loss. Thus, it became clear that break-even analysis helps to take short-term

managerial decisions through getting larger revenues and profitability as well.

Other factors in investing appraisal techniques:

In investment appraisal, it is not the only requirement to consider all the financial factors

there are also some non-financial factors that must be consider while taking investment

decisions. Some of the non-financial factors that Madison Plc should evaluate are enumerated

below:

Manpower: In this, Madison Plc need to make sure that he has enough manpower

available in the business or not to operate its new software (Duchin, Ozbas and Sensoy, 2010).

Workforce must be highly able, skilled and experienced so that they can operate new equipment

easily. Otherwise, it may face operational difficulties to a great extent. It is essential for the

Madison Plc to recruit talented manpower so that software can be operated by them. Training

program provides a great assistance to enhance personnel skills.

Government regulations: Before making any investment, Madison Plc should analyse the

governmental rules and regulations because all the organizations are strictly abided to comply

with the legislation and governmental policies (Yescombe, 2011). With reference to Madison

Plc, firm must anticipate potential threats that can be incur due to changing government

regulations and have a significant impact of investment decisions. They should analyse current

and future legislation which must be followed by Madison Plc.

Competitor’s action: In the present age, fierce level of competition exists in the market.

Henceforth, it became necessary for Madison Plc to analyze their competitor’s actions and

identify what software are using by the competitions. It will help to take better investment

decisions. Determination of future threats in order to protect intellectual property from the

potential competition it essential for Madison Plc.

5 Ratio Analysis

Puteaux France:

Net profit ratio reflects firm ability to control its indirect expenses and it also indicate

proportion of sales that is covered by the net profit. It can be seen from the table that in 2011 net

profit ratio was 17.63% and in next fiscal year it become 20.32%. This reflects that firm maintain

5

face business loss. Thus, it became clear that break-even analysis helps to take short-term

managerial decisions through getting larger revenues and profitability as well.

Other factors in investing appraisal techniques:

In investment appraisal, it is not the only requirement to consider all the financial factors

there are also some non-financial factors that must be consider while taking investment

decisions. Some of the non-financial factors that Madison Plc should evaluate are enumerated

below:

Manpower: In this, Madison Plc need to make sure that he has enough manpower

available in the business or not to operate its new software (Duchin, Ozbas and Sensoy, 2010).

Workforce must be highly able, skilled and experienced so that they can operate new equipment

easily. Otherwise, it may face operational difficulties to a great extent. It is essential for the

Madison Plc to recruit talented manpower so that software can be operated by them. Training

program provides a great assistance to enhance personnel skills.

Government regulations: Before making any investment, Madison Plc should analyse the

governmental rules and regulations because all the organizations are strictly abided to comply

with the legislation and governmental policies (Yescombe, 2011). With reference to Madison

Plc, firm must anticipate potential threats that can be incur due to changing government

regulations and have a significant impact of investment decisions. They should analyse current

and future legislation which must be followed by Madison Plc.

Competitor’s action: In the present age, fierce level of competition exists in the market.

Henceforth, it became necessary for Madison Plc to analyze their competitor’s actions and

identify what software are using by the competitions. It will help to take better investment

decisions. Determination of future threats in order to protect intellectual property from the

potential competition it essential for Madison Plc.

5 Ratio Analysis

Puteaux France:

Net profit ratio reflects firm ability to control its indirect expenses and it also indicate

proportion of sales that is covered by the net profit. It can be seen from the table that in 2011 net

profit ratio was 17.63% and in next fiscal year it become 20.32%. This reflects that firm maintain

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

good control on its indirect expenses. Gross profit ratio like above ratio also increased from

25.45% to 29.31%. This reflects that firm maintain stiff control on its direct expenses. Hence, it

can be said that Puteaux give magnificent performance in its business. Current ratio indicate firm

capability to pay its current liability by using current assets. Current ratio of the firm increased

from 1.8 to 3 which indicate that firm have sufficient amount of current assets and it can pay its

current liabilities on time. In case of return of asset also firm give good performance and it can

be seen that return on assets get increased in 2012 from 21.06% to 21.82%. Hence, it can be said

that firm make best use of its assets. Firm is earning good return on equity and it is positive

performance from investor’s point of view. Thus, on the basis of results of ratios it can be said

that firm gives excellent performance in its business.

Mella Spain:

According to the computation of ratio analysis various prospects of financial position of

Mella Spain Company has been identified. However, on the basis of analysis it can be said that

comparing the cited firm through Puteaux France the position of Mella Spain is not so good. It is

because of the fact that, net profit ratio of company is showing constant results which are also on

the lower side as in 2011 8.93% while following years 8.94% and 8.93% respectively. Further,

gross profit ratio of the firm indicates that same outcomes of 9% throughout the functioning of

three years. Thereafter, current ratio of the firm is relatively on the lower side as compared to its

competitors which are 0.6, 0.5 and 0.4 in 2011 to 2013. In addition to it, return on assets

indicates that company is making optimum utilization of its assets in terms of generating the

revenue as its ROA is 28.25% in 2011 which increased tremendously in following years to

48.11% and 123.68% respectively. Lastly, return on equity shows better outcomes for the

shareholders as company is able to provide suitable returns of its shareholders on its invested

amount as it shows ROE of 0.28, 0.48 and 1.24 in 2011 to 2013.

CONCLUSION

In conclusion to the above report it can be said that there are several sources of finance

available for the Madison plc that manager has to evaluate and analyze. Further, through the

means of different investment appraisal techniques it has been evaluated that project Madison

Super has been recommended to the top level management of Madison Plc. Lastly through the

means of ratio analysis comparison between two organization Puteaux France and Mella Spain

6

25.45% to 29.31%. This reflects that firm maintain stiff control on its direct expenses. Hence, it

can be said that Puteaux give magnificent performance in its business. Current ratio indicate firm

capability to pay its current liability by using current assets. Current ratio of the firm increased

from 1.8 to 3 which indicate that firm have sufficient amount of current assets and it can pay its

current liabilities on time. In case of return of asset also firm give good performance and it can

be seen that return on assets get increased in 2012 from 21.06% to 21.82%. Hence, it can be said

that firm make best use of its assets. Firm is earning good return on equity and it is positive

performance from investor’s point of view. Thus, on the basis of results of ratios it can be said

that firm gives excellent performance in its business.

Mella Spain:

According to the computation of ratio analysis various prospects of financial position of

Mella Spain Company has been identified. However, on the basis of analysis it can be said that

comparing the cited firm through Puteaux France the position of Mella Spain is not so good. It is

because of the fact that, net profit ratio of company is showing constant results which are also on

the lower side as in 2011 8.93% while following years 8.94% and 8.93% respectively. Further,

gross profit ratio of the firm indicates that same outcomes of 9% throughout the functioning of

three years. Thereafter, current ratio of the firm is relatively on the lower side as compared to its

competitors which are 0.6, 0.5 and 0.4 in 2011 to 2013. In addition to it, return on assets

indicates that company is making optimum utilization of its assets in terms of generating the

revenue as its ROA is 28.25% in 2011 which increased tremendously in following years to

48.11% and 123.68% respectively. Lastly, return on equity shows better outcomes for the

shareholders as company is able to provide suitable returns of its shareholders on its invested

amount as it shows ROE of 0.28, 0.48 and 1.24 in 2011 to 2013.

CONCLUSION

In conclusion to the above report it can be said that there are several sources of finance

available for the Madison plc that manager has to evaluate and analyze. Further, through the

means of different investment appraisal techniques it has been evaluated that project Madison

Super has been recommended to the top level management of Madison Plc. Lastly through the

means of ratio analysis comparison between two organization Puteaux France and Mella Spain

6

has been evaluated and on the basis of this tool it has been identified that Puteaux France have

better financial position in comparison to the Mella Spain.

7

better financial position in comparison to the Mella Spain.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Bakand, S., Hayes, A. and Dechsakulthorn, F., 2012. Nanoparticles: a review of particle

toxicology following inhalation exposure. Inhalation toxicology. 24(2). pp.125-135.

Brealey, R.A. and et.al., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Buchanan, J.M., 2014. Public finance in democratic process: Fiscal institutions and individual

choice. UNC Press Books.

Chernow, R., 2010. The house of Morgan: An American banking dynasty and the rise of modern

finance. Grove/Atlantic, Inc..

Damodaran, A., 2010. Applied corporate finance. John Wiley & Sons.

Duchin, R., Ozbas, O. and Sensoy, B.A., 2010. Costly external finance, corporate investment,

and the subprime mortgage credit crisis. Journal of Financial Economics. 97(3). pp.418-

435.

Embrechts, P., Klüppelberg, C. and Mikosch, T., 2013. Modelling extremal events: for insurance

and finance. Springer Science & Business Media.

Gitman, L.J., Juchau, R. and Flanagan, J., 2010. Principles of managerial finance. Pearson

Higher Education AU.

Hyman, D., 2013. Public finance: A contemporary application of theory to policy. Cengage

Learning.

Kotz, S., Kozubowski, T. and Podgorski, K., 2012. The Laplace distribution and

generalizations: a revisit with applications to communications, economics, engineering,

and finance. Springer Science & Business Media.

Mandelbrot, B.B., 2013. Fractals and Scaling in Finance: Discontinuity, Concentration, Risk.

Selecta Volume E. Springer Science & Business Media.

Minsky, H.P., 2015. Can" it" happen again?: essays on instability and finance. Routledge.

Tirole, J., 2010. The theory of corporate finance. Princeton University Press.

Wilmott, P., 2013. Paul Wilmott on quantitative finance. John Wiley & Sons.

8

Bakand, S., Hayes, A. and Dechsakulthorn, F., 2012. Nanoparticles: a review of particle

toxicology following inhalation exposure. Inhalation toxicology. 24(2). pp.125-135.

Brealey, R.A. and et.al., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Buchanan, J.M., 2014. Public finance in democratic process: Fiscal institutions and individual

choice. UNC Press Books.

Chernow, R., 2010. The house of Morgan: An American banking dynasty and the rise of modern

finance. Grove/Atlantic, Inc..

Damodaran, A., 2010. Applied corporate finance. John Wiley & Sons.

Duchin, R., Ozbas, O. and Sensoy, B.A., 2010. Costly external finance, corporate investment,

and the subprime mortgage credit crisis. Journal of Financial Economics. 97(3). pp.418-

435.

Embrechts, P., Klüppelberg, C. and Mikosch, T., 2013. Modelling extremal events: for insurance

and finance. Springer Science & Business Media.

Gitman, L.J., Juchau, R. and Flanagan, J., 2010. Principles of managerial finance. Pearson

Higher Education AU.

Hyman, D., 2013. Public finance: A contemporary application of theory to policy. Cengage

Learning.

Kotz, S., Kozubowski, T. and Podgorski, K., 2012. The Laplace distribution and

generalizations: a revisit with applications to communications, economics, engineering,

and finance. Springer Science & Business Media.

Mandelbrot, B.B., 2013. Fractals and Scaling in Finance: Discontinuity, Concentration, Risk.

Selecta Volume E. Springer Science & Business Media.

Minsky, H.P., 2015. Can" it" happen again?: essays on instability and finance. Routledge.

Tirole, J., 2010. The theory of corporate finance. Princeton University Press.

Wilmott, P., 2013. Paul Wilmott on quantitative finance. John Wiley & Sons.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Yescombe, E.R., 2011. Public-private partnerships: principles of policy and finance.

Butterworth-Heinemann.

9

Butterworth-Heinemann.

9

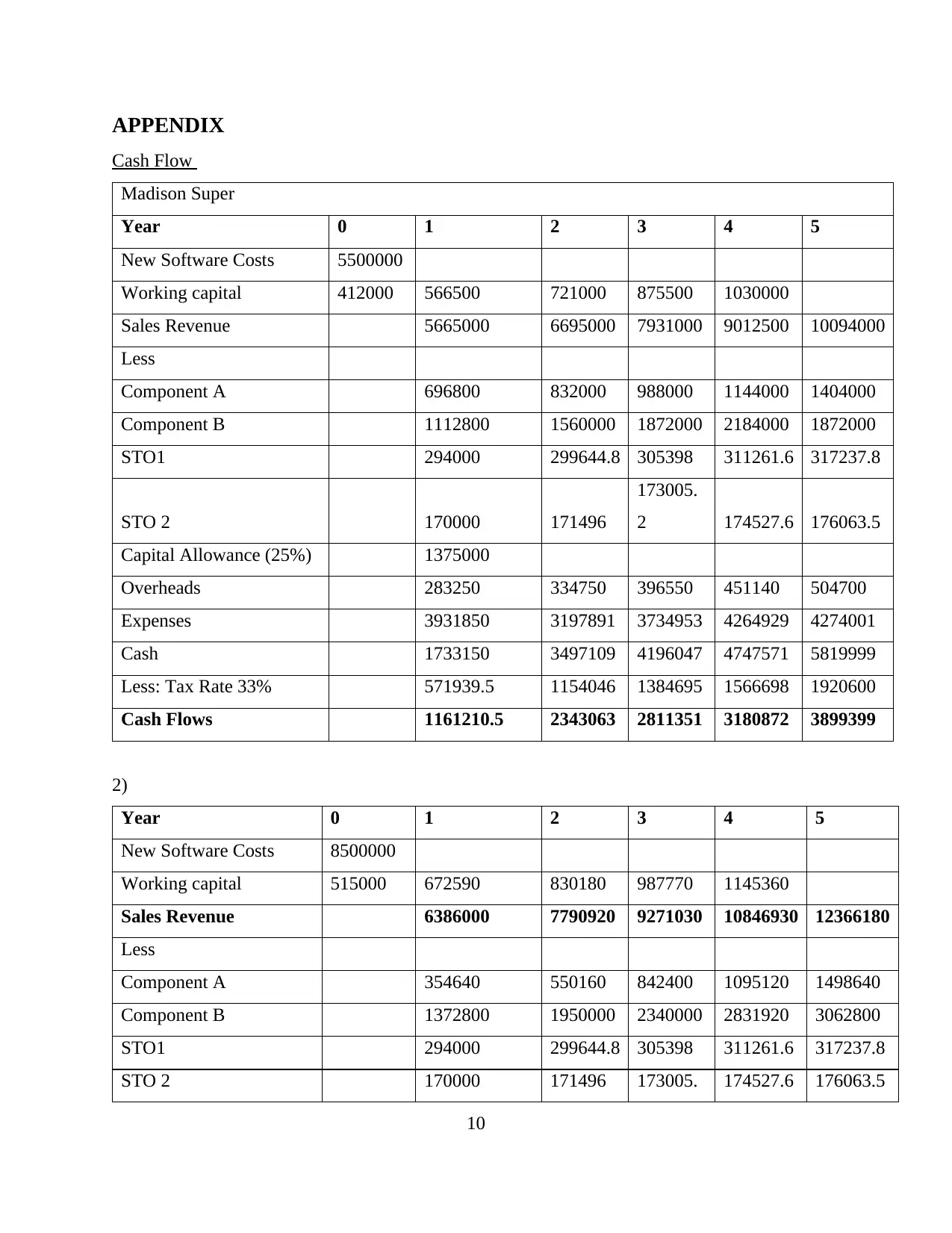

APPENDIX

Cash Flow

Madison Super

Year 0 1 2 3 4 5

New Software Costs 5500000

Working capital 412000 566500 721000 875500 1030000

Sales Revenue 5665000 6695000 7931000 9012500 10094000

Less

Component A 696800 832000 988000 1144000 1404000

Component B 1112800 1560000 1872000 2184000 1872000

STO1 294000 299644.8 305398 311261.6 317237.8

STO 2 170000 171496

173005.

2 174527.6 176063.5

Capital Allowance (25%) 1375000

Overheads 283250 334750 396550 451140 504700

Expenses 3931850 3197891 3734953 4264929 4274001

Cash 1733150 3497109 4196047 4747571 5819999

Less: Tax Rate 33% 571939.5 1154046 1384695 1566698 1920600

Cash Flows 1161210.5 2343063 2811351 3180872 3899399

2)

Year 0 1 2 3 4 5

New Software Costs 8500000

Working capital 515000 672590 830180 987770 1145360

Sales Revenue 6386000 7790920 9271030 10846930 12366180

Less

Component A 354640 550160 842400 1095120 1498640

Component B 1372800 1950000 2340000 2831920 3062800

STO1 294000 299644.8 305398 311261.6 317237.8

STO 2 170000 171496 173005. 174527.6 176063.5

10

Cash Flow

Madison Super

Year 0 1 2 3 4 5

New Software Costs 5500000

Working capital 412000 566500 721000 875500 1030000

Sales Revenue 5665000 6695000 7931000 9012500 10094000

Less

Component A 696800 832000 988000 1144000 1404000

Component B 1112800 1560000 1872000 2184000 1872000

STO1 294000 299644.8 305398 311261.6 317237.8

STO 2 170000 171496

173005.

2 174527.6 176063.5

Capital Allowance (25%) 1375000

Overheads 283250 334750 396550 451140 504700

Expenses 3931850 3197891 3734953 4264929 4274001

Cash 1733150 3497109 4196047 4747571 5819999

Less: Tax Rate 33% 571939.5 1154046 1384695 1566698 1920600

Cash Flows 1161210.5 2343063 2811351 3180872 3899399

2)

Year 0 1 2 3 4 5

New Software Costs 8500000

Working capital 515000 672590 830180 987770 1145360

Sales Revenue 6386000 7790920 9271030 10846930 12366180

Less

Component A 354640 550160 842400 1095120 1498640

Component B 1372800 1950000 2340000 2831920 3062800

STO1 294000 299644.8 305398 311261.6 317237.8

STO 2 170000 171496 173005. 174527.6 176063.5

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.