Financial Statement Analysis and Management Accounting Planning

VerifiedAdded on 2024/06/11

|20

|4030

|397

Report

AI Summary

This report provides a comprehensive analysis of management accounting, covering its role, integration within organizations, and benefits. It delves into financial statement analysis of Balfour Beatty and Kier Group, comparing their profitability, liquidity, gearing, market ratios, and efficiency. The report also prepares profit and loss statements using both absorption and marginal costing techniques, illustrated with the example of Areal Ltd. Furthermore, it compares and contrasts three planning tools used in management accounting, evaluating their effectiveness. This document, contributed by a student, is available on Desklib, a platform offering AI-based study tools and a wealth of academic resources for students.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Task 1...............................................................................................................................................3

1. An explanation of the role of management accounting and management accounting systems...3

2. Explanation of how management accounting is integrated within an organisation....................5

3. The benefits of the function to the organisation..........................................................................5

Task 2...............................................................................................................................................7

A. Financial statements analysis......................................................................................................7

B. Profit and loss statements preparation using absorption costing and marginal costing

techniques........................................................................................................................................9

(i) Preparing profit and loss statement using the absorption costing technique..............................9

(ii) Preparing profit and loss statement using the marginal costing technique..............................10

Task 3.............................................................................................................................................11

Compare and contrast three planning tools used in management accounting, indicating how

effective you judge each to be and why.........................................................................................11

Reference list.................................................................................................................................14

Appendix........................................................................................................................................16

2 | P a g e

Task 1...............................................................................................................................................3

1. An explanation of the role of management accounting and management accounting systems...3

2. Explanation of how management accounting is integrated within an organisation....................5

3. The benefits of the function to the organisation..........................................................................5

Task 2...............................................................................................................................................7

A. Financial statements analysis......................................................................................................7

B. Profit and loss statements preparation using absorption costing and marginal costing

techniques........................................................................................................................................9

(i) Preparing profit and loss statement using the absorption costing technique..............................9

(ii) Preparing profit and loss statement using the marginal costing technique..............................10

Task 3.............................................................................................................................................11

Compare and contrast three planning tools used in management accounting, indicating how

effective you judge each to be and why.........................................................................................11

Reference list.................................................................................................................................14

Appendix........................................................................................................................................16

2 | P a g e

Task 1

1. An explanation of the role of management accounting and management accounting systems

Management accounting is a process that involves several systems and activities aiming to

improve the quality of business operations. Management accounting can also be defined as the

group of analytical activities that helps to improve performance standards of the business by

analyzing the current business activities (White, 2015). It was originated at the time of industrial

revolution in the European countries. Management accounting is important for the manufacturing

organization like, Apeks, which is scuba diving equipment manufacturing company in UK. It is

because management accounting helps in developing effective plans for the business. At the

same time, it is also important for developing new control strategies that can help the business

controlling the cost and resource usage level in a better way (Rikhardsson and Yigitbasioglu,

2018). Management accounting is also important because it helps in inventory management.

Management accounting follows some key principles, which are as under:

Principle of trust

Principle of relevance

Principle of need understanding

Principle of diagnosis

Principle of value

Principle of influence (Wanderley

et al., 2017)

Management accounting is much different from the financial accounting system. The differences

are as follows:

Management accounting Financial accounting

Management accounting is very important but not

mandatory for the organizations

Financial accounting is important as well as

mandatory for the organizations

Management accounting evaluates the overall

internal performance standard of the business.

Financial accounting evaluates only the financial

performance standard of the business.

Management accounting is easy to incorporate

because it does not follow any rule or specific

Financial accounting is bit critical because there are

several rules and standards that are required to be

3 | P a g e

1. An explanation of the role of management accounting and management accounting systems

Management accounting is a process that involves several systems and activities aiming to

improve the quality of business operations. Management accounting can also be defined as the

group of analytical activities that helps to improve performance standards of the business by

analyzing the current business activities (White, 2015). It was originated at the time of industrial

revolution in the European countries. Management accounting is important for the manufacturing

organization like, Apeks, which is scuba diving equipment manufacturing company in UK. It is

because management accounting helps in developing effective plans for the business. At the

same time, it is also important for developing new control strategies that can help the business

controlling the cost and resource usage level in a better way (Rikhardsson and Yigitbasioglu,

2018). Management accounting is also important because it helps in inventory management.

Management accounting follows some key principles, which are as under:

Principle of trust

Principle of relevance

Principle of need understanding

Principle of diagnosis

Principle of value

Principle of influence (Wanderley

et al., 2017)

Management accounting is much different from the financial accounting system. The differences

are as follows:

Management accounting Financial accounting

Management accounting is very important but not

mandatory for the organizations

Financial accounting is important as well as

mandatory for the organizations

Management accounting evaluates the overall

internal performance standard of the business.

Financial accounting evaluates only the financial

performance standard of the business.

Management accounting is easy to incorporate

because it does not follow any rule or specific

Financial accounting is bit critical because there are

several rules and standards that are required to be

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

guideline (Tricker and Tricker, 2015). maintained while performing the financial

accounting activities.

It has been mentioned above that management accounting involves several systems. These

systems of management accounting are – cost accounting system, inventory management system,

job-costing system and price-optimization system. These systems are discussed below:

Cost accounting system – This particular management accounting system aims to control the cost

level in the business. In order to control the cost level, this system analyzes the cost requirement

of every business activity and then it allocates the available funds to those activities. There are

different techniques of cost accounting among which Apeks can select the most suitable cost

accounting technique (Otley, 2016). These available techniques are – normal costing, actual

costing and standard costing. The first two costing techniques are more or less same because

under these costing techniques, manufacturing related all material, labor and overhead costs are

considered. On the other hand, under the standard costing system, managers need to set standard

for each activity or cost unit of the business.

Inventory management system – This system takes care of the inventory level of the business. It

helps to maintain the most appropriate inventory level in the business, so that the company can

maintain smooth sales flow in the business. The available techniques of inventory management

that Apeks may follow are – FIFO, LIFO and AVCO (Leelahavarong, 2014).

Job-costing system – Job-costing is also an important system in management accounting. The

job-costing system helps to manage large projects efficiently. The job-costing system may be of

two types – process costing and contract costing. These two job-costing systems are applicable to

different types of projects (Nitzl, 2018). Contract costing is applicable to contract based projects

and process costing is applicable to large projects that are needed to be completed through

different processes.

Price-optimization system – This system is important for determining the right price level for the

products and services. This system determines the price level by analyzing the different factors

like, customers’ purchasing capacity, market demand, competitors’ price range and substitute

products (Le

et al., 2017).

4 | P a g e

accounting activities.

It has been mentioned above that management accounting involves several systems. These

systems of management accounting are – cost accounting system, inventory management system,

job-costing system and price-optimization system. These systems are discussed below:

Cost accounting system – This particular management accounting system aims to control the cost

level in the business. In order to control the cost level, this system analyzes the cost requirement

of every business activity and then it allocates the available funds to those activities. There are

different techniques of cost accounting among which Apeks can select the most suitable cost

accounting technique (Otley, 2016). These available techniques are – normal costing, actual

costing and standard costing. The first two costing techniques are more or less same because

under these costing techniques, manufacturing related all material, labor and overhead costs are

considered. On the other hand, under the standard costing system, managers need to set standard

for each activity or cost unit of the business.

Inventory management system – This system takes care of the inventory level of the business. It

helps to maintain the most appropriate inventory level in the business, so that the company can

maintain smooth sales flow in the business. The available techniques of inventory management

that Apeks may follow are – FIFO, LIFO and AVCO (Leelahavarong, 2014).

Job-costing system – Job-costing is also an important system in management accounting. The

job-costing system helps to manage large projects efficiently. The job-costing system may be of

two types – process costing and contract costing. These two job-costing systems are applicable to

different types of projects (Nitzl, 2018). Contract costing is applicable to contract based projects

and process costing is applicable to large projects that are needed to be completed through

different processes.

Price-optimization system – This system is important for determining the right price level for the

products and services. This system determines the price level by analyzing the different factors

like, customers’ purchasing capacity, market demand, competitors’ price range and substitute

products (Le

et al., 2017).

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Explanation of how management accounting is integrated within an organisation

Management accounting is closely integrated with the business process in the organizations. If

the particular case of Apeks is considered, it can be stated that if the management implements the

management accounting system, organization will require following different systems of

management accounting. Cost management is an important activity of the business and cost

accounting system will help Apeks maintaining and managing the required level of cost. On the

other hand, in order to determine the price level that will help the business attracting more

customers, the company will require following the price-optimization system. At the same time,

the inventory management system will help the business maintaining standard level of inventory

so that the company can meet market demand properly (Tricker and Tricker, 2015).

Therefore, the above discussion is indicating that each important activity of the business is

related to the management accounting systems. Moreover, in this context, it is important to be

mentioned that the management accounting reports like, sales report, production report, cost

report, inventory management report and investment appraisal reports are very important for the

decision-making purposes of the business. Hence, it can be stated that management accounting is

integrated within an organization.

3. The benefits of the function to the organisation

Management accounting within an organization takes care of different activities of the business.

The benefits of the functions to the organization are as follows:

One of the key functions of management accounting is cost control. Due to this activity,

the financial position of the company gets improved because it enhances net profitability

of the business (White, 2015).

Another important function of management accounting is inventory management. This

function is beneficial because it helps to meet market demand efficiently.

Information generation is also important function of management accounting and it is

beneficial because it helps in decision-making purposes (Wanderley

et al., 2017).

Forecasting is also an important function of management accounting. With the help of

forecasting, the management accountant can help the higher authority in decision-making

purposes.

5 | P a g e

Management accounting is closely integrated with the business process in the organizations. If

the particular case of Apeks is considered, it can be stated that if the management implements the

management accounting system, organization will require following different systems of

management accounting. Cost management is an important activity of the business and cost

accounting system will help Apeks maintaining and managing the required level of cost. On the

other hand, in order to determine the price level that will help the business attracting more

customers, the company will require following the price-optimization system. At the same time,

the inventory management system will help the business maintaining standard level of inventory

so that the company can meet market demand properly (Tricker and Tricker, 2015).

Therefore, the above discussion is indicating that each important activity of the business is

related to the management accounting systems. Moreover, in this context, it is important to be

mentioned that the management accounting reports like, sales report, production report, cost

report, inventory management report and investment appraisal reports are very important for the

decision-making purposes of the business. Hence, it can be stated that management accounting is

integrated within an organization.

3. The benefits of the function to the organisation

Management accounting within an organization takes care of different activities of the business.

The benefits of the functions to the organization are as follows:

One of the key functions of management accounting is cost control. Due to this activity,

the financial position of the company gets improved because it enhances net profitability

of the business (White, 2015).

Another important function of management accounting is inventory management. This

function is beneficial because it helps to meet market demand efficiently.

Information generation is also important function of management accounting and it is

beneficial because it helps in decision-making purposes (Wanderley

et al., 2017).

Forecasting is also an important function of management accounting. With the help of

forecasting, the management accountant can help the higher authority in decision-making

purposes.

5 | P a g e

Management accounting generates different reports to represent the information to the higher

authority. However, it must be noted that the information that is presented through reports must

be in understandable manner. If the information is presented in understandable manner, it

becomes easier for the higher management understanding the overall situation of the business,

which is important for developing effective plans and decision for the business; otherwise, the

strategies will be inappropriate.

6 | P a g e

authority. However, it must be noted that the information that is presented through reports must

be in understandable manner. If the information is presented in understandable manner, it

becomes easier for the higher management understanding the overall situation of the business,

which is important for developing effective plans and decision for the business; otherwise, the

strategies will be inappropriate.

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 2

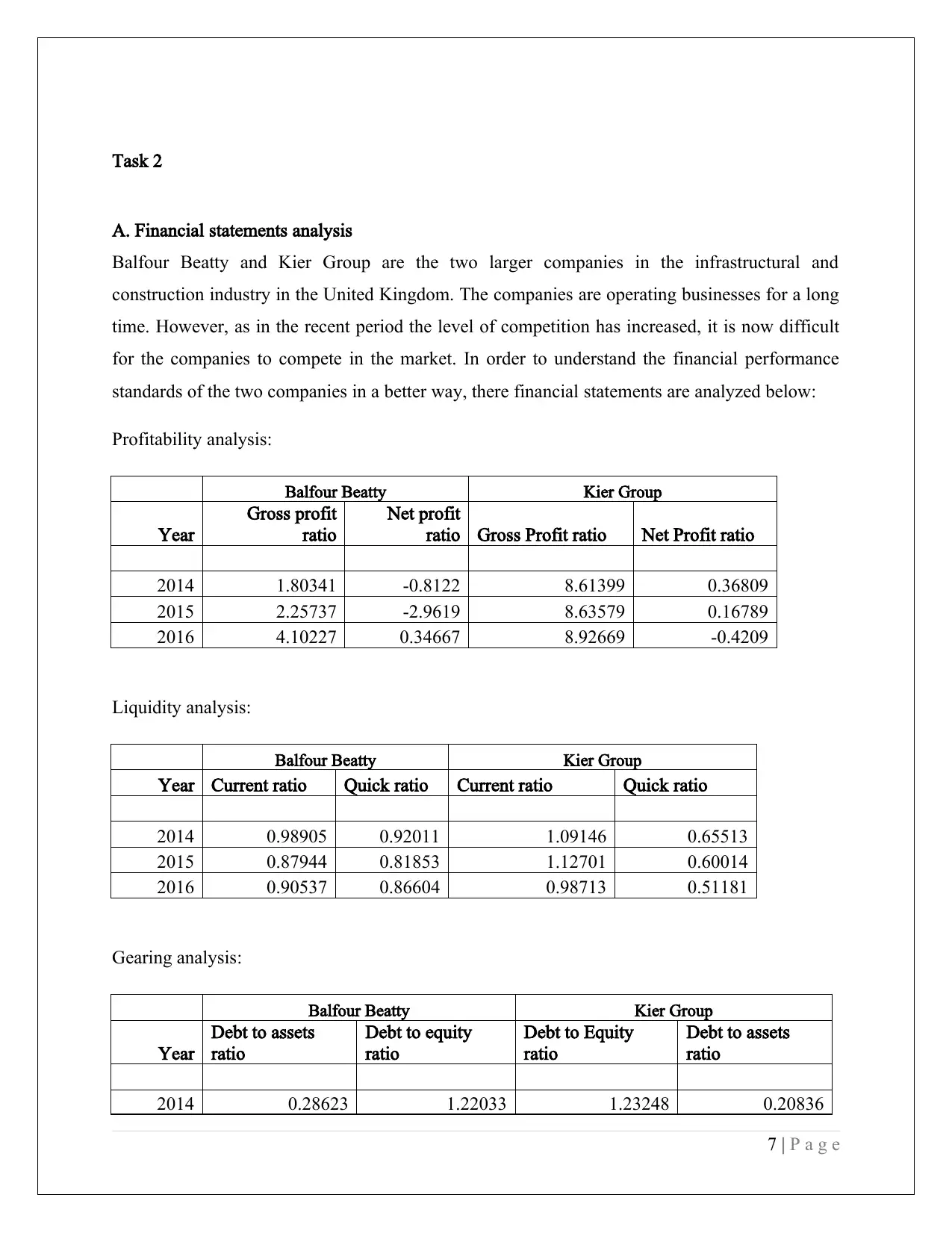

A. Financial statements analysis

Balfour Beatty and Kier Group are the two larger companies in the infrastructural and

construction industry in the United Kingdom. The companies are operating businesses for a long

time. However, as in the recent period the level of competition has increased, it is now difficult

for the companies to compete in the market. In order to understand the financial performance

standards of the two companies in a better way, there financial statements are analyzed below:

Profitability analysis:

Balfour Beatty Kier Group

Year

Gross profit

ratio

Net profit

ratio Gross Profit ratio Net Profit ratio

2014 1.80341 -0.8122 8.61399 0.36809

2015 2.25737 -2.9619 8.63579 0.16789

2016 4.10227 0.34667 8.92669 -0.4209

Liquidity analysis:

Balfour Beatty Kier Group

Year Current ratio Quick ratio Current ratio Quick ratio

2014 0.98905 0.92011 1.09146 0.65513

2015 0.87944 0.81853 1.12701 0.60014

2016 0.90537 0.86604 0.98713 0.51181

Gearing analysis:

Balfour Beatty Kier Group

Year

Debt to assets

ratio

Debt to equity

ratio

Debt to Equity

ratio

Debt to assets

ratio

2014 0.28623 1.22033 1.23248 0.20836

7 | P a g e

A. Financial statements analysis

Balfour Beatty and Kier Group are the two larger companies in the infrastructural and

construction industry in the United Kingdom. The companies are operating businesses for a long

time. However, as in the recent period the level of competition has increased, it is now difficult

for the companies to compete in the market. In order to understand the financial performance

standards of the two companies in a better way, there financial statements are analyzed below:

Profitability analysis:

Balfour Beatty Kier Group

Year

Gross profit

ratio

Net profit

ratio Gross Profit ratio Net Profit ratio

2014 1.80341 -0.8122 8.61399 0.36809

2015 2.25737 -2.9619 8.63579 0.16789

2016 4.10227 0.34667 8.92669 -0.4209

Liquidity analysis:

Balfour Beatty Kier Group

Year Current ratio Quick ratio Current ratio Quick ratio

2014 0.98905 0.92011 1.09146 0.65513

2015 0.87944 0.81853 1.12701 0.60014

2016 0.90537 0.86604 0.98713 0.51181

Gearing analysis:

Balfour Beatty Kier Group

Year

Debt to assets

ratio

Debt to equity

ratio

Debt to Equity

ratio

Debt to assets

ratio

2014 0.28623 1.22033 1.23248 0.20836

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2015 0.3058 1.69518 1.08063 0.23079

2016 0.30291 1.89895 0.8259 0.19127

Market ratio analysis:

Balfour Beatty Kier Group

Year EPS P/E ratio EPS P/E Ratio

2014 -9 -33.698 16.2 118.951

2015 -30.1 -7.0565 40 41.175

2016 3.5 73.54 -18.5 -66.054

Efficiency analysis:

Balfour Beatty Kier Group

Year Inventory turnover ROA

Return on

Assets Inventory turnover ratio

2014 41.9588 0.024981 0.00584 5.64732

2015 47.2083 0.034123 0.00201 4.05665

2016 65.7327 0.059452 -0.0068 5.37816

The above tables are showing financial performances of Balfour Beatty and Kier Group during

the financial years 2014 to 2016. Analyzing the profitability of the two companies, it has been

identified that the performance standard of Kier Group was better than that of Balfour Beatty.

The gross profit and net profit both were higher in the Kier Group, which indicates that the

management of Kier Group has efficiently controlled the cost levels of the business. On the other

hand, if the liquidity positions of the two firms are considered, it can be identified that their

positions were more or less similar. However, in this context, it can be stated that the quick ratios

of Balfour Beatty were higher than that of Kier Group. It means the capacity of paying of the

short-term liabilities is higher in Balfour Beatty.

On the other hand, analyzing the gearing ratios of the two companies, it can be stated that the use

of debt capital was higher at Balfour Beatty than in Kier Group. It is indicating that to the

8 | P a g e

2016 0.30291 1.89895 0.8259 0.19127

Market ratio analysis:

Balfour Beatty Kier Group

Year EPS P/E ratio EPS P/E Ratio

2014 -9 -33.698 16.2 118.951

2015 -30.1 -7.0565 40 41.175

2016 3.5 73.54 -18.5 -66.054

Efficiency analysis:

Balfour Beatty Kier Group

Year Inventory turnover ROA

Return on

Assets Inventory turnover ratio

2014 41.9588 0.024981 0.00584 5.64732

2015 47.2083 0.034123 0.00201 4.05665

2016 65.7327 0.059452 -0.0068 5.37816

The above tables are showing financial performances of Balfour Beatty and Kier Group during

the financial years 2014 to 2016. Analyzing the profitability of the two companies, it has been

identified that the performance standard of Kier Group was better than that of Balfour Beatty.

The gross profit and net profit both were higher in the Kier Group, which indicates that the

management of Kier Group has efficiently controlled the cost levels of the business. On the other

hand, if the liquidity positions of the two firms are considered, it can be identified that their

positions were more or less similar. However, in this context, it can be stated that the quick ratios

of Balfour Beatty were higher than that of Kier Group. It means the capacity of paying of the

short-term liabilities is higher in Balfour Beatty.

On the other hand, analyzing the gearing ratios of the two companies, it can be stated that the use

of debt capital was higher at Balfour Beatty than in Kier Group. It is indicating that to the

8 | P a g e

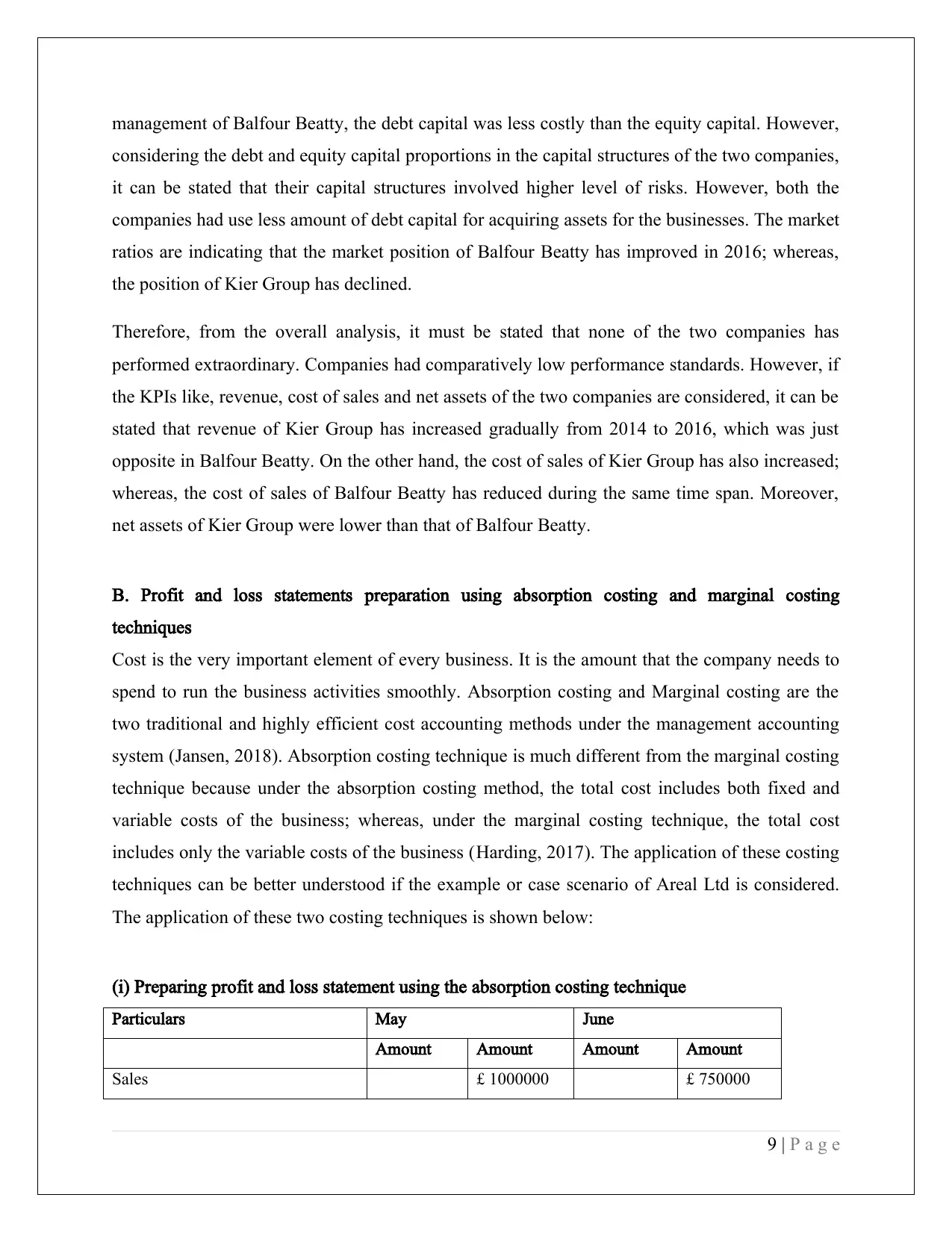

management of Balfour Beatty, the debt capital was less costly than the equity capital. However,

considering the debt and equity capital proportions in the capital structures of the two companies,

it can be stated that their capital structures involved higher level of risks. However, both the

companies had use less amount of debt capital for acquiring assets for the businesses. The market

ratios are indicating that the market position of Balfour Beatty has improved in 2016; whereas,

the position of Kier Group has declined.

Therefore, from the overall analysis, it must be stated that none of the two companies has

performed extraordinary. Companies had comparatively low performance standards. However, if

the KPIs like, revenue, cost of sales and net assets of the two companies are considered, it can be

stated that revenue of Kier Group has increased gradually from 2014 to 2016, which was just

opposite in Balfour Beatty. On the other hand, the cost of sales of Kier Group has also increased;

whereas, the cost of sales of Balfour Beatty has reduced during the same time span. Moreover,

net assets of Kier Group were lower than that of Balfour Beatty.

B. Profit and loss statements preparation using absorption costing and marginal costing

techniques

Cost is the very important element of every business. It is the amount that the company needs to

spend to run the business activities smoothly. Absorption costing and Marginal costing are the

two traditional and highly efficient cost accounting methods under the management accounting

system (Jansen, 2018). Absorption costing technique is much different from the marginal costing

technique because under the absorption costing method, the total cost includes both fixed and

variable costs of the business; whereas, under the marginal costing technique, the total cost

includes only the variable costs of the business (Harding, 2017). The application of these costing

techniques can be better understood if the example or case scenario of Areal Ltd is considered.

The application of these two costing techniques is shown below:

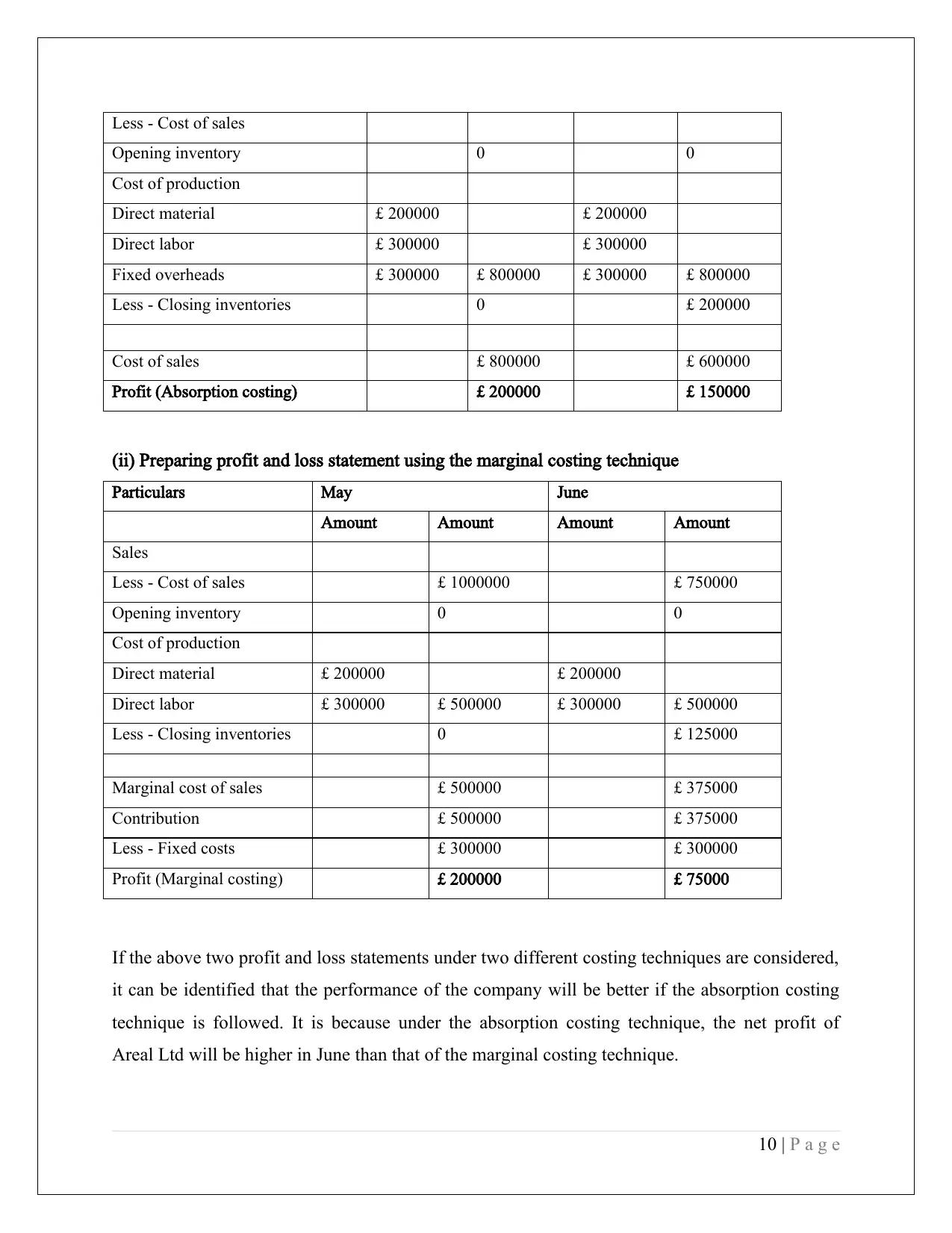

(i) Preparing profit and loss statement using the absorption costing technique

Particulars May June

Amount Amount Amount Amount

Sales £ 1000000 £ 750000

9 | P a g e

considering the debt and equity capital proportions in the capital structures of the two companies,

it can be stated that their capital structures involved higher level of risks. However, both the

companies had use less amount of debt capital for acquiring assets for the businesses. The market

ratios are indicating that the market position of Balfour Beatty has improved in 2016; whereas,

the position of Kier Group has declined.

Therefore, from the overall analysis, it must be stated that none of the two companies has

performed extraordinary. Companies had comparatively low performance standards. However, if

the KPIs like, revenue, cost of sales and net assets of the two companies are considered, it can be

stated that revenue of Kier Group has increased gradually from 2014 to 2016, which was just

opposite in Balfour Beatty. On the other hand, the cost of sales of Kier Group has also increased;

whereas, the cost of sales of Balfour Beatty has reduced during the same time span. Moreover,

net assets of Kier Group were lower than that of Balfour Beatty.

B. Profit and loss statements preparation using absorption costing and marginal costing

techniques

Cost is the very important element of every business. It is the amount that the company needs to

spend to run the business activities smoothly. Absorption costing and Marginal costing are the

two traditional and highly efficient cost accounting methods under the management accounting

system (Jansen, 2018). Absorption costing technique is much different from the marginal costing

technique because under the absorption costing method, the total cost includes both fixed and

variable costs of the business; whereas, under the marginal costing technique, the total cost

includes only the variable costs of the business (Harding, 2017). The application of these costing

techniques can be better understood if the example or case scenario of Areal Ltd is considered.

The application of these two costing techniques is shown below:

(i) Preparing profit and loss statement using the absorption costing technique

Particulars May June

Amount Amount Amount Amount

Sales £ 1000000 £ 750000

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less - Cost of sales

Opening inventory 0 0

Cost of production

Direct material £ 200000 £ 200000

Direct labor £ 300000 £ 300000

Fixed overheads £ 300000 £ 800000 £ 300000 £ 800000

Less - Closing inventories 0 £ 200000

Cost of sales £ 800000 £ 600000

Profit (Absorption costing) £ 200000 £ 150000

(ii) Preparing profit and loss statement using the marginal costing technique

Particulars May June

Amount Amount Amount Amount

Sales

Less - Cost of sales £ 1000000 £ 750000

Opening inventory 0 0

Cost of production

Direct material £ 200000 £ 200000

Direct labor £ 300000 £ 500000 £ 300000 £ 500000

Less - Closing inventories 0 £ 125000

Marginal cost of sales £ 500000 £ 375000

Contribution £ 500000 £ 375000

Less - Fixed costs £ 300000 £ 300000

Profit (Marginal costing) £ 200000 £ 75000

If the above two profit and loss statements under two different costing techniques are considered,

it can be identified that the performance of the company will be better if the absorption costing

technique is followed. It is because under the absorption costing technique, the net profit of

Areal Ltd will be higher in June than that of the marginal costing technique.

10 | P a g e

Opening inventory 0 0

Cost of production

Direct material £ 200000 £ 200000

Direct labor £ 300000 £ 300000

Fixed overheads £ 300000 £ 800000 £ 300000 £ 800000

Less - Closing inventories 0 £ 200000

Cost of sales £ 800000 £ 600000

Profit (Absorption costing) £ 200000 £ 150000

(ii) Preparing profit and loss statement using the marginal costing technique

Particulars May June

Amount Amount Amount Amount

Sales

Less - Cost of sales £ 1000000 £ 750000

Opening inventory 0 0

Cost of production

Direct material £ 200000 £ 200000

Direct labor £ 300000 £ 500000 £ 300000 £ 500000

Less - Closing inventories 0 £ 125000

Marginal cost of sales £ 500000 £ 375000

Contribution £ 500000 £ 375000

Less - Fixed costs £ 300000 £ 300000

Profit (Marginal costing) £ 200000 £ 75000

If the above two profit and loss statements under two different costing techniques are considered,

it can be identified that the performance of the company will be better if the absorption costing

technique is followed. It is because under the absorption costing technique, the net profit of

Areal Ltd will be higher in June than that of the marginal costing technique.

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3

Compare and contrast three planning tools used in management accounting, indicating how

effective you judge each to be and why

Management accounting provides a systematic procedure to improve the performance standard

of the business through proper planning and control. It means the system of management

accounting definitely uses some planning tools for developing better plans for the business.

Considering the particular business case of Apeks is considered, it can be stated that there are

mainly three planning tools of management accounting that the company may consider for better

decision making and planning. However, in order to select the most suitable planning tool, the

company needs to analyze and compare each planning tool properly. The analysis and

comparison are done below:

Standard costing is one of the planning tools that are available to the management of Apeks. This

particular tool is used by the organizations in order to understand in which area the company is

lacking behind. Under this particular planning tool, the company needs to set particular standards

for each manufacturing and operating activity of the business (Greenberg and Wilner, 2015).

After setting the standards, the actual performance or activities are started and after finishing the

activities, the actual cost level is compared with the standard cost level and if there is negative

difference that can be considered as the area in which the company is lacking behind. It means

gap identification is easier in this planning tool. The major advantage of this tool is that the tool

allows critical analysis of the activities, which is important for developing better cost plans for

the business (Bento

et al., 2018). At the same time, the standard costing technique is also

efficient in encouraging the employees as well as managers for better performance. However, it

is true that the standard costing method needs specialized knowledge and expertise because it

involves several calculations. Due to this, sometimes, companies face difficulties while

following the standard costing as a management accounting planning tool.

However, if the standard costing technique is compared with another management accounting

planning tool that is

Tree diagram, it can be stated that standard costing is an old planning tool.

Tree diagram is one of the most effective modern management accounting planning tool that

11 | P a g e

Compare and contrast three planning tools used in management accounting, indicating how

effective you judge each to be and why

Management accounting provides a systematic procedure to improve the performance standard

of the business through proper planning and control. It means the system of management

accounting definitely uses some planning tools for developing better plans for the business.

Considering the particular business case of Apeks is considered, it can be stated that there are

mainly three planning tools of management accounting that the company may consider for better

decision making and planning. However, in order to select the most suitable planning tool, the

company needs to analyze and compare each planning tool properly. The analysis and

comparison are done below:

Standard costing is one of the planning tools that are available to the management of Apeks. This

particular tool is used by the organizations in order to understand in which area the company is

lacking behind. Under this particular planning tool, the company needs to set particular standards

for each manufacturing and operating activity of the business (Greenberg and Wilner, 2015).

After setting the standards, the actual performance or activities are started and after finishing the

activities, the actual cost level is compared with the standard cost level and if there is negative

difference that can be considered as the area in which the company is lacking behind. It means

gap identification is easier in this planning tool. The major advantage of this tool is that the tool

allows critical analysis of the activities, which is important for developing better cost plans for

the business (Bento

et al., 2018). At the same time, the standard costing technique is also

efficient in encouraging the employees as well as managers for better performance. However, it

is true that the standard costing method needs specialized knowledge and expertise because it

involves several calculations. Due to this, sometimes, companies face difficulties while

following the standard costing as a management accounting planning tool.

However, if the standard costing technique is compared with another management accounting

planning tool that is

Tree diagram, it can be stated that standard costing is an old planning tool.

Tree diagram is one of the most effective modern management accounting planning tool that

11 | P a g e

efficiently develops plans to meet specific objectives of the business. This planning tool is highly

efficient in meeting the goals of the business. The major advantage that the company may enjoy

by using the tree diagram planning tool is that the company may develop creative ideas for

improving the standard of performance of the business (Eldenburg

et al., 2017). In this context, it

must be noted that the tree diagram makes the business process unique and helps to adopt new

techniques and projects for improving the current performance standards of the business.

However, in this context, it is important to be mentioned that the tree diagram is not very simple

to use and this planning tool takes a long time to develop a new plan for the business.

Pricing is another important planning tool that the management of Apeks needs to follow for

developing better plans related to the price level of the business. In order to develop the right

pricing strategies, the company needs to rely on the price optimization system. The pricing

strategies can be of different types like, cost-led pricing, market-led pricing and ROI pricing

(Chiwamit

et al., 2017). If the company considers the cost-led pricing strategy, it will require

considering the cost level of the business as the base for pricing. The company needs to add the

profit percentage with the total cost of the business to determine the final price level of the

products and services. The ROI pricing strategy is much like the cost-led pricing. However, if the

company selects the market-led pricing strategy, it will require consider the purchasing power of

the customers to determine the price range for the business. However, while using this particular

planning tool, the company needs to involve a long time to determine the final price of the

products and services and this process is very complicated because it needs considering different

factors (Ax and Greve, 2017).

If the comparison is made among the three available planning tools under the system of

management accounting, it can be stated that the tree diagram tool will be the most efficient tool

that the managers at Apeks may follow for developing better plans for the business. It is because

the tree diagram tool helps in developing unique strategies for the business. It provides

innovative decisions that can improve the performance standards of the business from different

perspectives. If this tool is compared with the other two tools, it can be identified that the

standard costing tool is not able to show the reasons behind the performance gaps in the business

(Eldenburg

et al., 2017). Hence, if the management of Apeks selects the Tree diagram tool, they

can manage the performance standards of the business in a better way and the company can

12 | P a g e

efficient in meeting the goals of the business. The major advantage that the company may enjoy

by using the tree diagram planning tool is that the company may develop creative ideas for

improving the standard of performance of the business (Eldenburg

et al., 2017). In this context, it

must be noted that the tree diagram makes the business process unique and helps to adopt new

techniques and projects for improving the current performance standards of the business.

However, in this context, it is important to be mentioned that the tree diagram is not very simple

to use and this planning tool takes a long time to develop a new plan for the business.

Pricing is another important planning tool that the management of Apeks needs to follow for

developing better plans related to the price level of the business. In order to develop the right

pricing strategies, the company needs to rely on the price optimization system. The pricing

strategies can be of different types like, cost-led pricing, market-led pricing and ROI pricing

(Chiwamit

et al., 2017). If the company considers the cost-led pricing strategy, it will require

considering the cost level of the business as the base for pricing. The company needs to add the

profit percentage with the total cost of the business to determine the final price level of the

products and services. The ROI pricing strategy is much like the cost-led pricing. However, if the

company selects the market-led pricing strategy, it will require consider the purchasing power of

the customers to determine the price range for the business. However, while using this particular

planning tool, the company needs to involve a long time to determine the final price of the

products and services and this process is very complicated because it needs considering different

factors (Ax and Greve, 2017).

If the comparison is made among the three available planning tools under the system of

management accounting, it can be stated that the tree diagram tool will be the most efficient tool

that the managers at Apeks may follow for developing better plans for the business. It is because

the tree diagram tool helps in developing unique strategies for the business. It provides

innovative decisions that can improve the performance standards of the business from different

perspectives. If this tool is compared with the other two tools, it can be identified that the

standard costing tool is not able to show the reasons behind the performance gaps in the business

(Eldenburg

et al., 2017). Hence, if the management of Apeks selects the Tree diagram tool, they

can manage the performance standards of the business in a better way and the company can

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.