Financial Statement Analysis Project: McPherson's Performance Review

VerifiedAdded on 2020/10/23

|26

|6862

|169

Project

AI Summary

This capstone project provides a comprehensive financial statement analysis of McPherson, a custom manufacturer of precision optical instruments. The analysis focuses on forecasting sales growth, asset turnover, and profit margins from 2019 to 2023 based on 2018 data. Key components include calculating free cash flow, determining dividend payout ratios, and assessing net payments to debt holders. The project also involves forecasting the cost of debt, calculating comprehensive income, and analyzing dividend policy. The analysis aims to identify the company's profitability, growth prospects, and provide insights for stakeholders' decision-making, offering a detailed examination of McPherson's financial performance and future outlook. The project includes the use of financial ratios, forecasting techniques, and valuation methods to assess the company's financial health and potential.

FINANCIAL STATEMENT

ANALYSIS CAPSTONE

ANALYSIS CAPSTONE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Forecasting.............................................................................................................................3

Sales Growth..........................................................................................................................3

Forecasting ATO ( Asset turnover ).......................................................................................5

Forecasting Profit margin (PM).............................................................................................6

Calculate Free Cash flow (NOPAT- Change in NOA ).........................................................7

Dividend Payout ratio.............................................................................................................7

Calculation of net payment to debt holders............................................................................8

Forecast cost of debt and debt balance...................................................................................9

Calculation of comprehensive income.................................................................................10

Calculation of equity............................................................................................................10

Dividend policy....................................................................................................................11

Net cost of debt after tax......................................................................................................12

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................29

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Forecasting.............................................................................................................................3

Sales Growth..........................................................................................................................3

Forecasting ATO ( Asset turnover ).......................................................................................5

Forecasting Profit margin (PM).............................................................................................6

Calculate Free Cash flow (NOPAT- Change in NOA ).........................................................7

Dividend Payout ratio.............................................................................................................7

Calculation of net payment to debt holders............................................................................8

Forecast cost of debt and debt balance...................................................................................9

Calculation of comprehensive income.................................................................................10

Calculation of equity............................................................................................................10

Dividend policy....................................................................................................................11

Net cost of debt after tax......................................................................................................12

CONCLUSION..............................................................................................................................28

REFERENCES..............................................................................................................................29

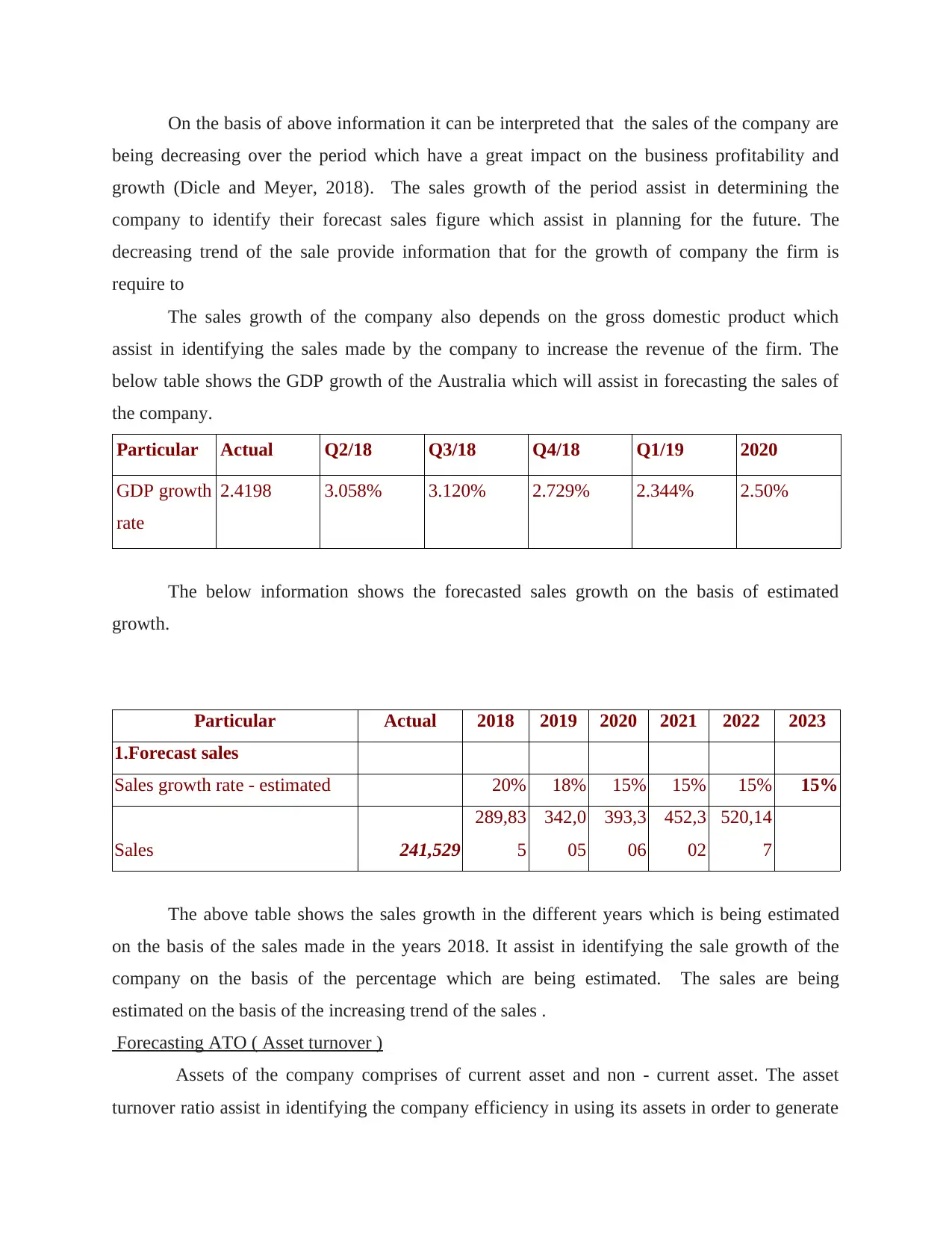

INTRODUCTION

Financial statement analysis of the company assist in identifying the profitability and the

growth of that company which assist in making various decision by the stakeholders of the

organisation. In this assignment, McPherson will be considered which is an custom manufacturer

of precision optical instrument this organisation is operating in Australia and provide products

relating to health and beauty. This assignment will provide understanding about forecasting,

valuation, sensitivity analysis and consulting advice on the basis of the information provided

through the analysis of the company. The Forecasting will be done on the basis of the 2018 data

on the basis of which the forecasting for the 2019 to 2023 will be made and it will assist in

getting the future growth prospects of the company. With the help of this analysis the company

will be able to identify their future growth prospects.

MAIN BODY

Forecasting

The forecasting is the process in which the company forecast the different variables

which are related to the growth and success of the business. The forecast made by the

organisation depend on the past data and the growth of the organisation on the basis of which the

company estimate its future growth prospects.

Sales Growth

The sales growth of the company assist in identifying the revenue generated by the

organisation through sales made by the firm. The growth rate of the sales can be forecasted for

the future on the basis of the the past information which assist in identifying the rate at which the

firm sales in growing (Lin and et.al., 2015). The McPherson annual report of 2014- 2018

provided information regarding the sales revenue which is generated with the help of performing

the different operation of the firm. The below table shows the information regarding the sales

revenue generated by the company through performing its operating activities.

Revenue 2014 2015 2016 2017 2018

sales 353386 349069 312586 279458 210430

Interest 27 214 217 46 2

Total operating revenue 353413 349283 312803 279504 210432

Financial statement analysis of the company assist in identifying the profitability and the

growth of that company which assist in making various decision by the stakeholders of the

organisation. In this assignment, McPherson will be considered which is an custom manufacturer

of precision optical instrument this organisation is operating in Australia and provide products

relating to health and beauty. This assignment will provide understanding about forecasting,

valuation, sensitivity analysis and consulting advice on the basis of the information provided

through the analysis of the company. The Forecasting will be done on the basis of the 2018 data

on the basis of which the forecasting for the 2019 to 2023 will be made and it will assist in

getting the future growth prospects of the company. With the help of this analysis the company

will be able to identify their future growth prospects.

MAIN BODY

Forecasting

The forecasting is the process in which the company forecast the different variables

which are related to the growth and success of the business. The forecast made by the

organisation depend on the past data and the growth of the organisation on the basis of which the

company estimate its future growth prospects.

Sales Growth

The sales growth of the company assist in identifying the revenue generated by the

organisation through sales made by the firm. The growth rate of the sales can be forecasted for

the future on the basis of the the past information which assist in identifying the rate at which the

firm sales in growing (Lin and et.al., 2015). The McPherson annual report of 2014- 2018

provided information regarding the sales revenue which is generated with the help of performing

the different operation of the firm. The below table shows the information regarding the sales

revenue generated by the company through performing its operating activities.

Revenue 2014 2015 2016 2017 2018

sales 353386 349069 312586 279458 210430

Interest 27 214 217 46 2

Total operating revenue 353413 349283 312803 279504 210432

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of above information it can be interpreted that the sales of the company are

being decreasing over the period which have a great impact on the business profitability and

growth (Dicle and Meyer, 2018). The sales growth of the period assist in determining the

company to identify their forecast sales figure which assist in planning for the future. The

decreasing trend of the sale provide information that for the growth of company the firm is

require to

The sales growth of the company also depends on the gross domestic product which

assist in identifying the sales made by the company to increase the revenue of the firm. The

below table shows the GDP growth of the Australia which will assist in forecasting the sales of

the company.

Particular Actual Q2/18 Q3/18 Q4/18 Q1/19 2020

GDP growth

rate

2.4198 3.058% 3.120% 2.729% 2.344% 2.50%

The below information shows the forecasted sales growth on the basis of estimated

growth.

Particular Actual 2018 2019 2020 2021 2022 2023

1.Forecast sales

Sales growth rate - estimated 20% 18% 15% 15% 15% 15%

Sales 241,529

289,83

5

342,0

05

393,3

06

452,3

02

520,14

7

The above table shows the sales growth in the different years which is being estimated

on the basis of the sales made in the years 2018. It assist in identifying the sale growth of the

company on the basis of the percentage which are being estimated. The sales are being

estimated on the basis of the increasing trend of the sales .

Forecasting ATO ( Asset turnover )

Assets of the company comprises of current asset and non - current asset. The asset

turnover ratio assist in identifying the company efficiency in using its assets in order to generate

being decreasing over the period which have a great impact on the business profitability and

growth (Dicle and Meyer, 2018). The sales growth of the period assist in determining the

company to identify their forecast sales figure which assist in planning for the future. The

decreasing trend of the sale provide information that for the growth of company the firm is

require to

The sales growth of the company also depends on the gross domestic product which

assist in identifying the sales made by the company to increase the revenue of the firm. The

below table shows the GDP growth of the Australia which will assist in forecasting the sales of

the company.

Particular Actual Q2/18 Q3/18 Q4/18 Q1/19 2020

GDP growth

rate

2.4198 3.058% 3.120% 2.729% 2.344% 2.50%

The below information shows the forecasted sales growth on the basis of estimated

growth.

Particular Actual 2018 2019 2020 2021 2022 2023

1.Forecast sales

Sales growth rate - estimated 20% 18% 15% 15% 15% 15%

Sales 241,529

289,83

5

342,0

05

393,3

06

452,3

02

520,14

7

The above table shows the sales growth in the different years which is being estimated

on the basis of the sales made in the years 2018. It assist in identifying the sale growth of the

company on the basis of the percentage which are being estimated. The sales are being

estimated on the basis of the increasing trend of the sales .

Forecasting ATO ( Asset turnover )

Assets of the company comprises of current asset and non - current asset. The asset

turnover ratio assist in identifying the company efficiency in using its assets in order to generate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

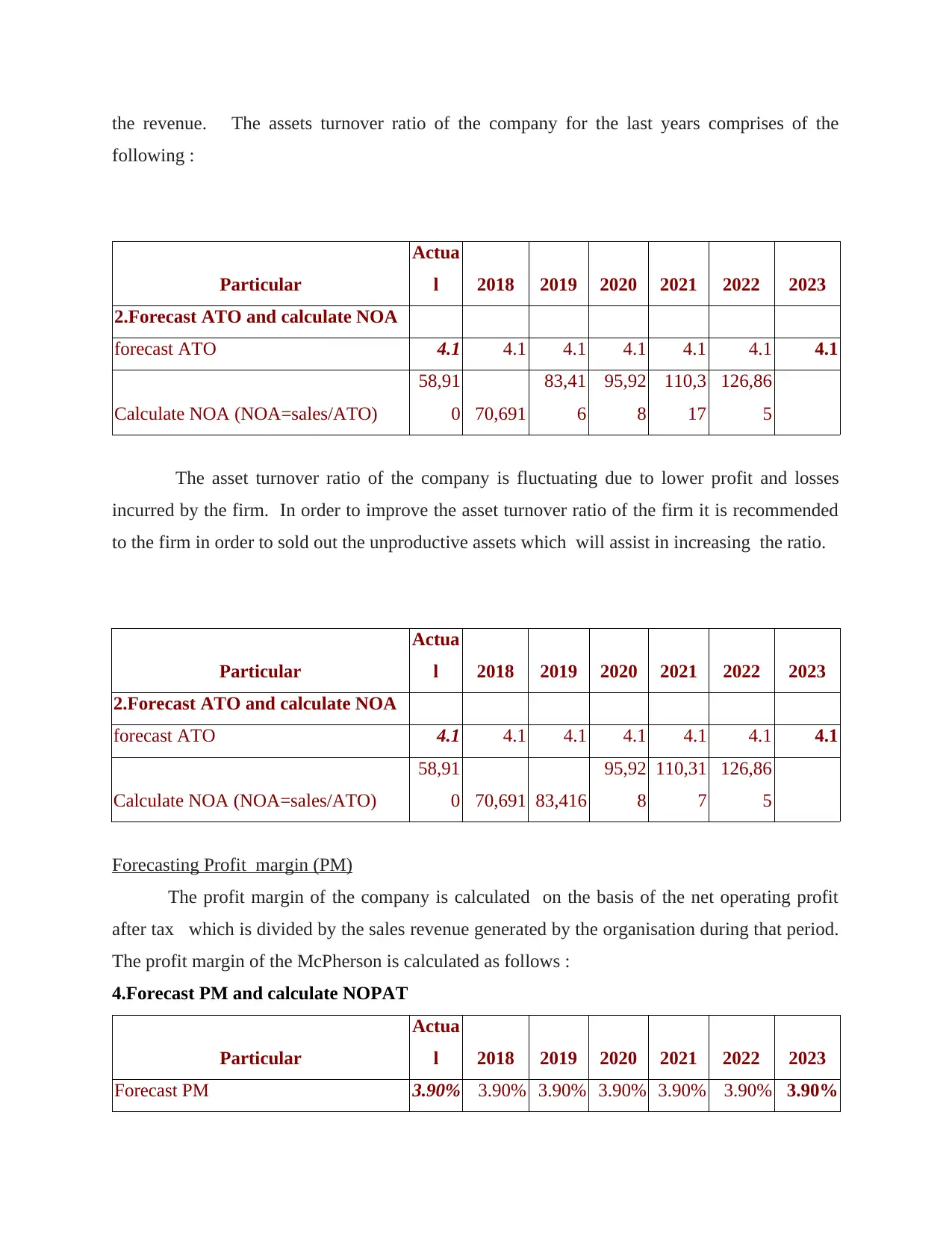

the revenue. The assets turnover ratio of the company for the last years comprises of the

following :

Particular

Actua

l 2018 2019 2020 2021 2022 2023

2.Forecast ATO and calculate NOA

forecast ATO 4.1 4.1 4.1 4.1 4.1 4.1 4.1

Calculate NOA (NOA=sales/ATO)

58,91

0 70,691

83,41

6

95,92

8

110,3

17

126,86

5

The asset turnover ratio of the company is fluctuating due to lower profit and losses

incurred by the firm. In order to improve the asset turnover ratio of the firm it is recommended

to the firm in order to sold out the unproductive assets which will assist in increasing the ratio.

Particular

Actua

l 2018 2019 2020 2021 2022 2023

2.Forecast ATO and calculate NOA

forecast ATO 4.1 4.1 4.1 4.1 4.1 4.1 4.1

Calculate NOA (NOA=sales/ATO)

58,91

0 70,691 83,416

95,92

8

110,31

7

126,86

5

Forecasting Profit margin (PM)

The profit margin of the company is calculated on the basis of the net operating profit

after tax which is divided by the sales revenue generated by the organisation during that period.

The profit margin of the McPherson is calculated as follows :

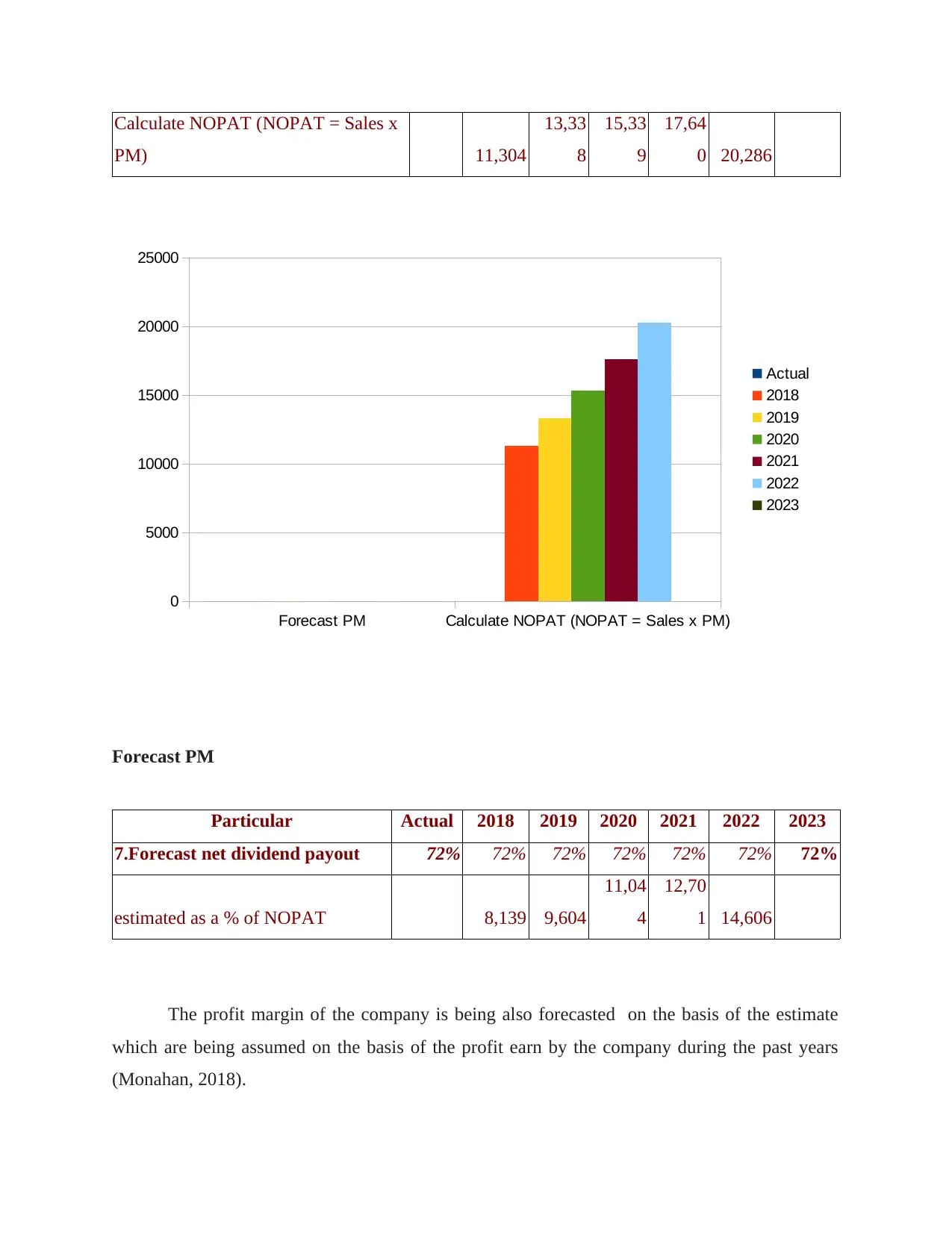

4.Forecast PM and calculate NOPAT

Particular

Actua

l 2018 2019 2020 2021 2022 2023

Forecast PM 3.90% 3.90% 3.90% 3.90% 3.90% 3.90% 3.90%

following :

Particular

Actua

l 2018 2019 2020 2021 2022 2023

2.Forecast ATO and calculate NOA

forecast ATO 4.1 4.1 4.1 4.1 4.1 4.1 4.1

Calculate NOA (NOA=sales/ATO)

58,91

0 70,691

83,41

6

95,92

8

110,3

17

126,86

5

The asset turnover ratio of the company is fluctuating due to lower profit and losses

incurred by the firm. In order to improve the asset turnover ratio of the firm it is recommended

to the firm in order to sold out the unproductive assets which will assist in increasing the ratio.

Particular

Actua

l 2018 2019 2020 2021 2022 2023

2.Forecast ATO and calculate NOA

forecast ATO 4.1 4.1 4.1 4.1 4.1 4.1 4.1

Calculate NOA (NOA=sales/ATO)

58,91

0 70,691 83,416

95,92

8

110,31

7

126,86

5

Forecasting Profit margin (PM)

The profit margin of the company is calculated on the basis of the net operating profit

after tax which is divided by the sales revenue generated by the organisation during that period.

The profit margin of the McPherson is calculated as follows :

4.Forecast PM and calculate NOPAT

Particular

Actua

l 2018 2019 2020 2021 2022 2023

Forecast PM 3.90% 3.90% 3.90% 3.90% 3.90% 3.90% 3.90%

Calculate NOPAT (NOPAT = Sales x

PM) 11,304

13,33

8

15,33

9

17,64

0 20,286

Forecast PM

Particular Actual 2018 2019 2020 2021 2022 2023

7.Forecast net dividend payout 72% 72% 72% 72% 72% 72% 72%

estimated as a % of NOPAT 8,139 9,604

11,04

4

12,70

1 14,606

The profit margin of the company is being also forecasted on the basis of the estimate

which are being assumed on the basis of the profit earn by the company during the past years

(Monahan, 2018).

Forecast PM Calculate NOPAT (NOPAT = Sales x PM)

0

5000

10000

15000

20000

25000

Actual

2018

2019

2020

2021

2022

2023

PM) 11,304

13,33

8

15,33

9

17,64

0 20,286

Forecast PM

Particular Actual 2018 2019 2020 2021 2022 2023

7.Forecast net dividend payout 72% 72% 72% 72% 72% 72% 72%

estimated as a % of NOPAT 8,139 9,604

11,04

4

12,70

1 14,606

The profit margin of the company is being also forecasted on the basis of the estimate

which are being assumed on the basis of the profit earn by the company during the past years

(Monahan, 2018).

Forecast PM Calculate NOPAT (NOPAT = Sales x PM)

0

5000

10000

15000

20000

25000

Actual

2018

2019

2020

2021

2022

2023

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

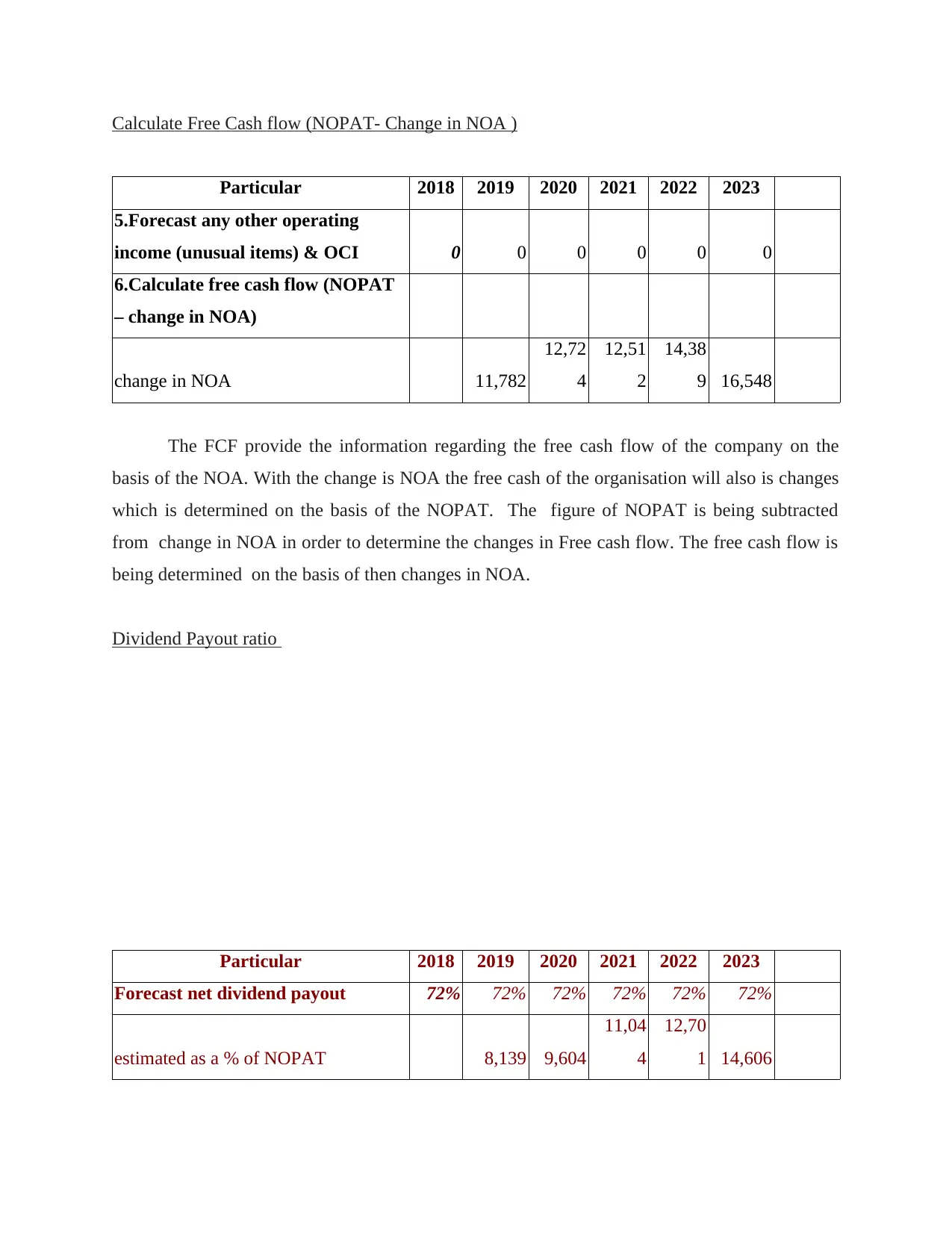

Calculate Free Cash flow (NOPAT- Change in NOA )

Particular 2018 2019 2020 2021 2022 2023

5.Forecast any other operating

income (unusual items) & OCI 0 0 0 0 0 0

6.Calculate free cash flow (NOPAT

– change in NOA)

change in NOA 11,782

12,72

4

12,51

2

14,38

9 16,548

The FCF provide the information regarding the free cash flow of the company on the

basis of the NOA. With the change is NOA the free cash of the organisation will also is changes

which is determined on the basis of the NOPAT. The figure of NOPAT is being subtracted

from change in NOA in order to determine the changes in Free cash flow. The free cash flow is

being determined on the basis of then changes in NOA.

Dividend Payout ratio

Particular 2018 2019 2020 2021 2022 2023

Forecast net dividend payout 72% 72% 72% 72% 72% 72%

estimated as a % of NOPAT 8,139 9,604

11,04

4

12,70

1 14,606

Particular 2018 2019 2020 2021 2022 2023

5.Forecast any other operating

income (unusual items) & OCI 0 0 0 0 0 0

6.Calculate free cash flow (NOPAT

– change in NOA)

change in NOA 11,782

12,72

4

12,51

2

14,38

9 16,548

The FCF provide the information regarding the free cash flow of the company on the

basis of the NOA. With the change is NOA the free cash of the organisation will also is changes

which is determined on the basis of the NOPAT. The figure of NOPAT is being subtracted

from change in NOA in order to determine the changes in Free cash flow. The free cash flow is

being determined on the basis of then changes in NOA.

Dividend Payout ratio

Particular 2018 2019 2020 2021 2022 2023

Forecast net dividend payout 72% 72% 72% 72% 72% 72%

estimated as a % of NOPAT 8,139 9,604

11,04

4

12,70

1 14,606

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is the amount which is being paid by the organisation as dividend to the shareholders

relative to the amount of total net income of the organisation. The dividend payout ratio of

McPearson was 72%. It means the firm provide the 72% of the net income as divined to the

shareholders. The main cause behind maintaining the same dividend payout ratio is the rapid

increase in the retained earnings of the business. As the retained earning is nothing but amount

left with the company from profit after payment of dividend.

On the basis of the above information the forecast is being made for the dividend payout

ratio as percentage of the net income. The dividend payout ratio of the forecasted years is being

same as the actual dividend payout ratio of 2018. It is being identified that the company will

pay the shareholders with dividend at the percentage of this to the net income.

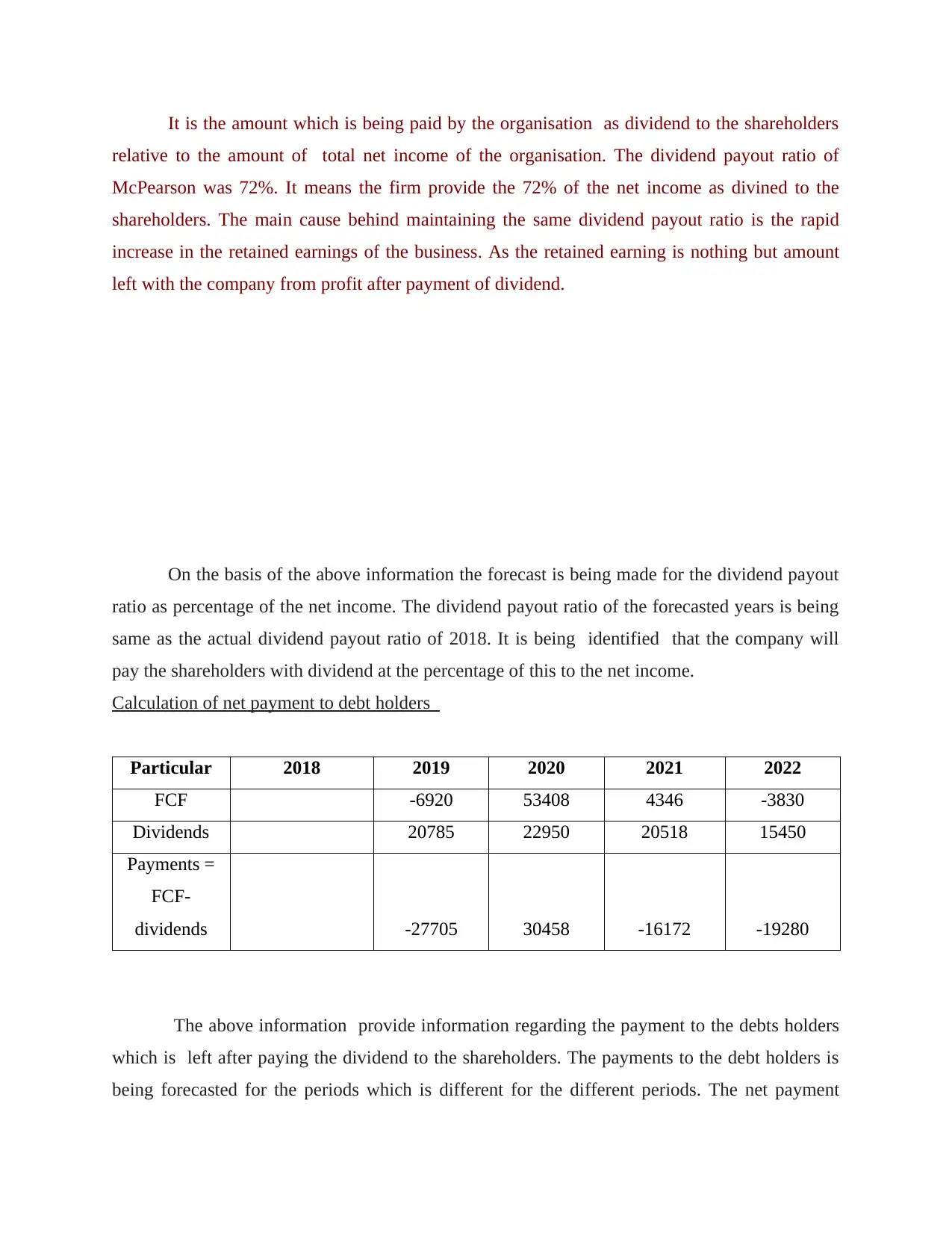

Calculation of net payment to debt holders

Particular 2018 2019 2020 2021 2022

FCF -6920 53408 4346 -3830

Dividends 20785 22950 20518 15450

Payments =

FCF-

dividends -27705 30458 -16172 -19280

The above information provide information regarding the payment to the debts holders

which is left after paying the dividend to the shareholders. The payments to the debt holders is

being forecasted for the periods which is different for the different periods. The net payment

relative to the amount of total net income of the organisation. The dividend payout ratio of

McPearson was 72%. It means the firm provide the 72% of the net income as divined to the

shareholders. The main cause behind maintaining the same dividend payout ratio is the rapid

increase in the retained earnings of the business. As the retained earning is nothing but amount

left with the company from profit after payment of dividend.

On the basis of the above information the forecast is being made for the dividend payout

ratio as percentage of the net income. The dividend payout ratio of the forecasted years is being

same as the actual dividend payout ratio of 2018. It is being identified that the company will

pay the shareholders with dividend at the percentage of this to the net income.

Calculation of net payment to debt holders

Particular 2018 2019 2020 2021 2022

FCF -6920 53408 4346 -3830

Dividends 20785 22950 20518 15450

Payments =

FCF-

dividends -27705 30458 -16172 -19280

The above information provide information regarding the payment to the debts holders

which is left after paying the dividend to the shareholders. The payments to the debt holders is

being forecasted for the periods which is different for the different periods. The net payment

which is required to be made to the debt holders is being calculated on the basis of free cash

flow in which the payment required to be made is calculated by subtracting dividend from free

cash flow.

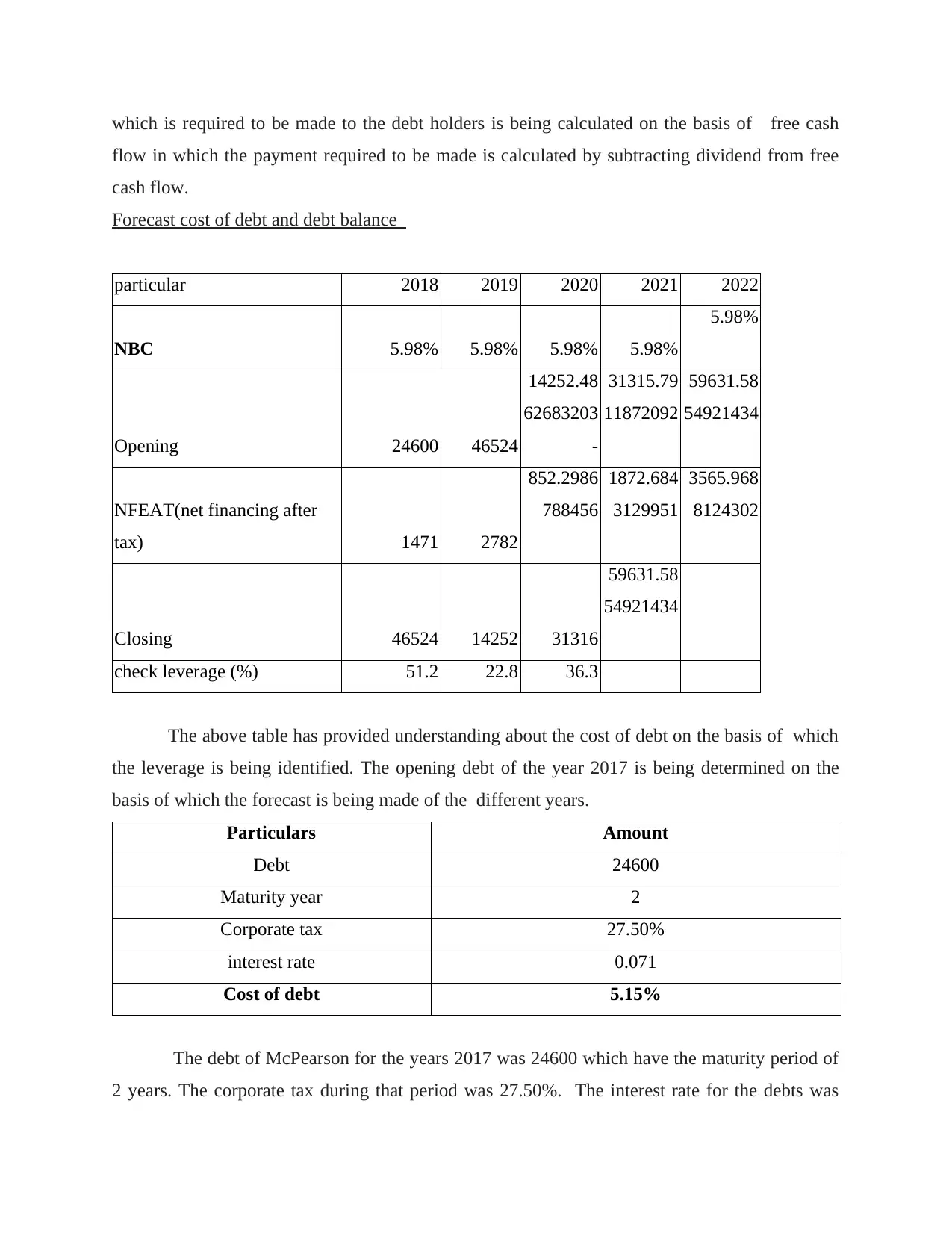

Forecast cost of debt and debt balance

particular 2018 2019 2020 2021 2022

NBC 5.98% 5.98% 5.98% 5.98%

5.98%

Opening 24600 46524

14252.48

62683203

-

31315.79

11872092

59631.58

54921434

NFEAT(net financing after

tax) 1471 2782

852.2986

788456

1872.684

3129951

3565.968

8124302

Closing 46524 14252 31316

59631.58

54921434

check leverage (%) 51.2 22.8 36.3

The above table has provided understanding about the cost of debt on the basis of which

the leverage is being identified. The opening debt of the year 2017 is being determined on the

basis of which the forecast is being made of the different years.

Particulars Amount

Debt 24600

Maturity year 2

Corporate tax 27.50%

interest rate 0.071

Cost of debt 5.15%

The debt of McPearson for the years 2017 was 24600 which have the maturity period of

2 years. The corporate tax during that period was 27.50%. The interest rate for the debts was

flow in which the payment required to be made is calculated by subtracting dividend from free

cash flow.

Forecast cost of debt and debt balance

particular 2018 2019 2020 2021 2022

NBC 5.98% 5.98% 5.98% 5.98%

5.98%

Opening 24600 46524

14252.48

62683203

-

31315.79

11872092

59631.58

54921434

NFEAT(net financing after

tax) 1471 2782

852.2986

788456

1872.684

3129951

3565.968

8124302

Closing 46524 14252 31316

59631.58

54921434

check leverage (%) 51.2 22.8 36.3

The above table has provided understanding about the cost of debt on the basis of which

the leverage is being identified. The opening debt of the year 2017 is being determined on the

basis of which the forecast is being made of the different years.

Particulars Amount

Debt 24600

Maturity year 2

Corporate tax 27.50%

interest rate 0.071

Cost of debt 5.15%

The debt of McPearson for the years 2017 was 24600 which have the maturity period of

2 years. The corporate tax during that period was 27.50%. The interest rate for the debts was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7.10%. On the basis of which the cost of debt determined is 5.15 which is before applying the

tax.

v (Total assets) 113086 after tax

Weight of equity 78.25% 4.25%

Weight of debt 21.75% 5.98%

For calculating the cost of debts after tax the weighted average cost of equity is being

calculated in which the weights of the equity and debts are determined on the basis of the total

assets for the year 2017.

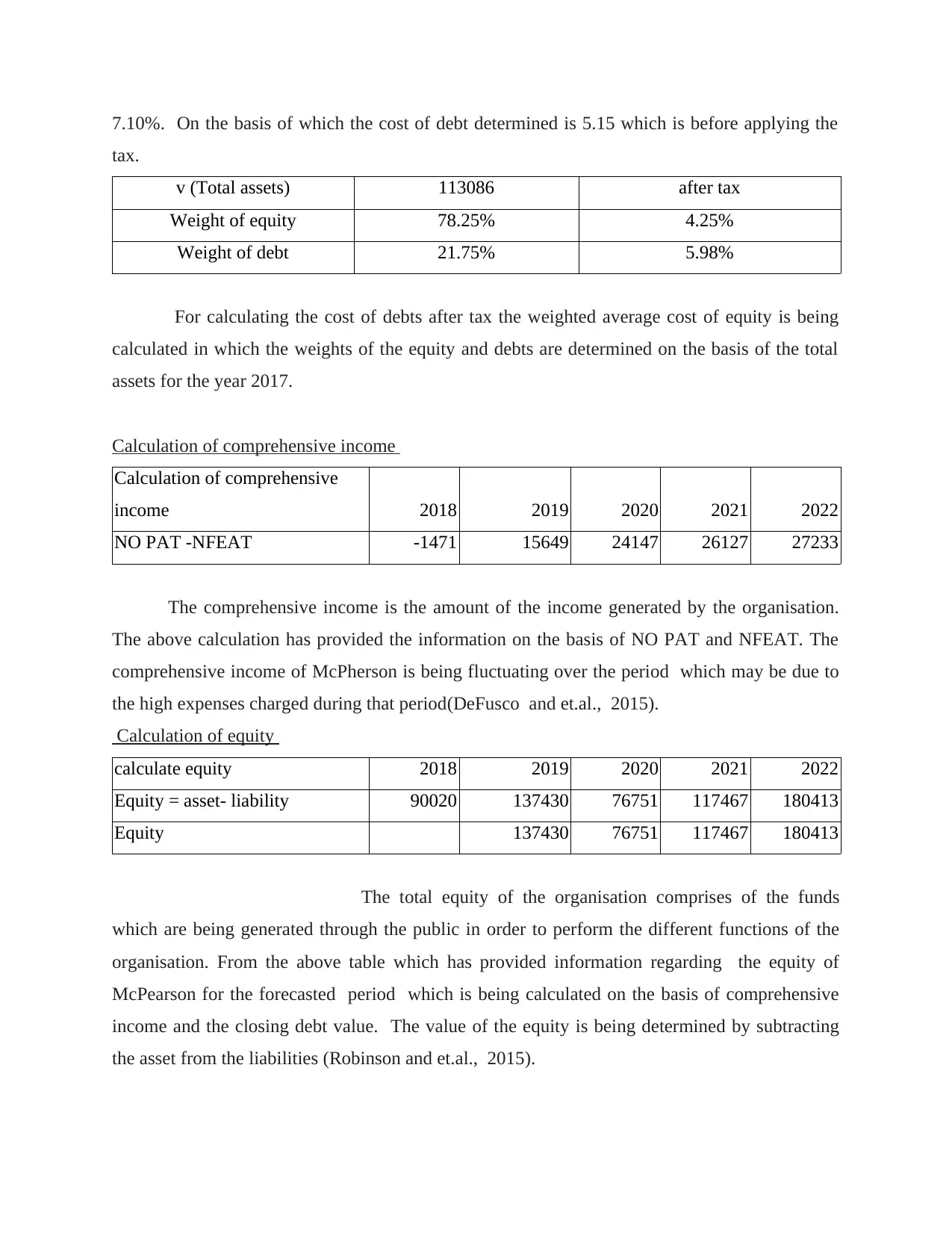

Calculation of comprehensive income

Calculation of comprehensive

income 2018 2019 2020 2021 2022

NO PAT -NFEAT -1471 15649 24147 26127 27233

The comprehensive income is the amount of the income generated by the organisation.

The above calculation has provided the information on the basis of NO PAT and NFEAT. The

comprehensive income of McPherson is being fluctuating over the period which may be due to

the high expenses charged during that period(DeFusco and et.al., 2015).

Calculation of equity

calculate equity 2018 2019 2020 2021 2022

Equity = asset- liability 90020 137430 76751 117467 180413

Equity 137430 76751 117467 180413

The total equity of the organisation comprises of the funds

which are being generated through the public in order to perform the different functions of the

organisation. From the above table which has provided information regarding the equity of

McPearson for the forecasted period which is being calculated on the basis of comprehensive

income and the closing debt value. The value of the equity is being determined by subtracting

the asset from the liabilities (Robinson and et.al., 2015).

tax.

v (Total assets) 113086 after tax

Weight of equity 78.25% 4.25%

Weight of debt 21.75% 5.98%

For calculating the cost of debts after tax the weighted average cost of equity is being

calculated in which the weights of the equity and debts are determined on the basis of the total

assets for the year 2017.

Calculation of comprehensive income

Calculation of comprehensive

income 2018 2019 2020 2021 2022

NO PAT -NFEAT -1471 15649 24147 26127 27233

The comprehensive income is the amount of the income generated by the organisation.

The above calculation has provided the information on the basis of NO PAT and NFEAT. The

comprehensive income of McPherson is being fluctuating over the period which may be due to

the high expenses charged during that period(DeFusco and et.al., 2015).

Calculation of equity

calculate equity 2018 2019 2020 2021 2022

Equity = asset- liability 90020 137430 76751 117467 180413

Equity 137430 76751 117467 180413

The total equity of the organisation comprises of the funds

which are being generated through the public in order to perform the different functions of the

organisation. From the above table which has provided information regarding the equity of

McPearson for the forecasted period which is being calculated on the basis of comprehensive

income and the closing debt value. The value of the equity is being determined by subtracting

the asset from the liabilities (Robinson and et.al., 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

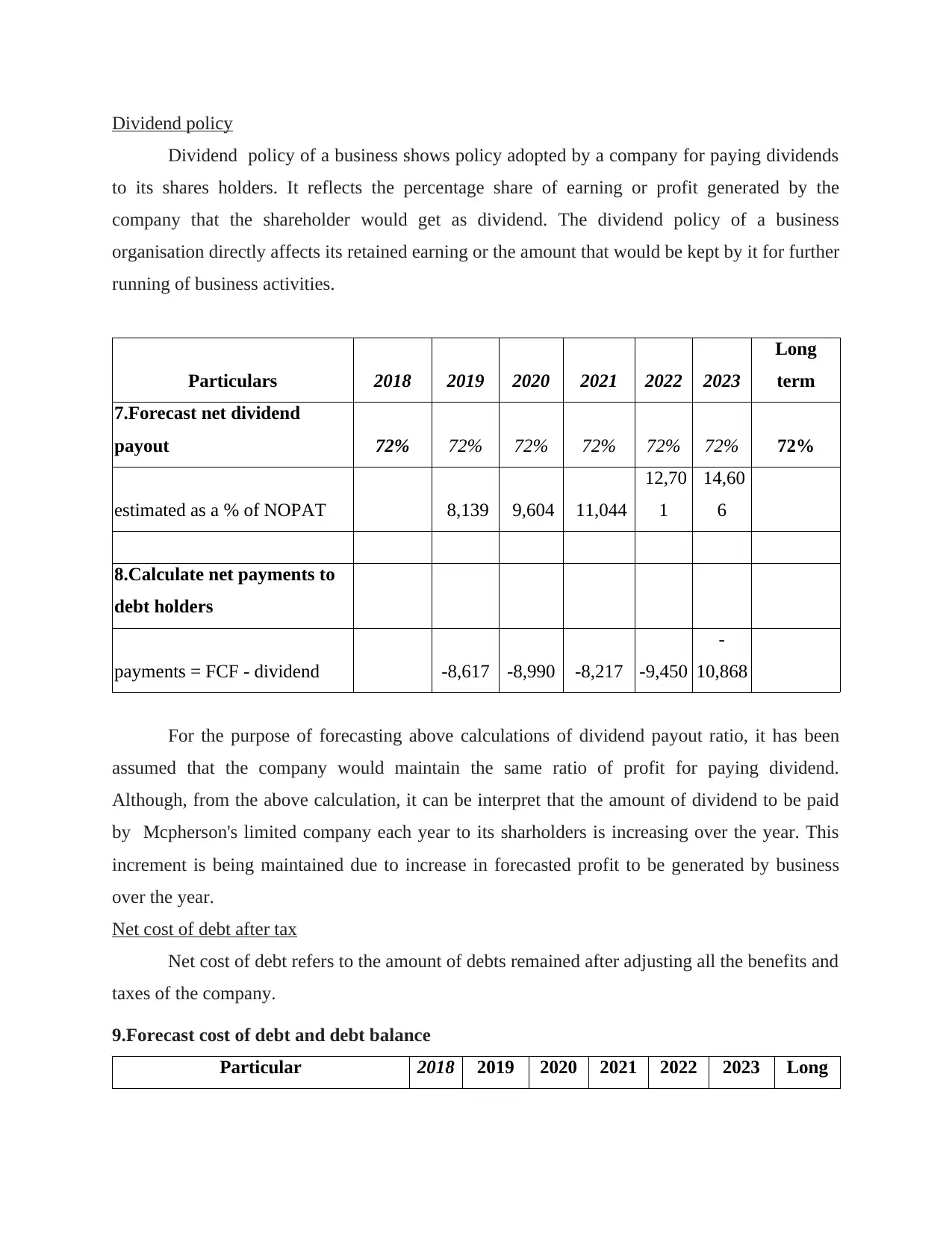

Dividend policy

Dividend policy of a business shows policy adopted by a company for paying dividends

to its shares holders. It reflects the percentage share of earning or profit generated by the

company that the shareholder would get as dividend. The dividend policy of a business

organisation directly affects its retained earning or the amount that would be kept by it for further

running of business activities.

Particulars 2018 2019 2020 2021 2022 2023

Long

term

7.Forecast net dividend

payout 72% 72% 72% 72% 72% 72% 72%

estimated as a % of NOPAT 8,139 9,604 11,044

12,70

1

14,60

6

8.Calculate net payments to

debt holders

payments = FCF - dividend -8,617 -8,990 -8,217 -9,450

-

10,868

For the purpose of forecasting above calculations of dividend payout ratio, it has been

assumed that the company would maintain the same ratio of profit for paying dividend.

Although, from the above calculation, it can be interpret that the amount of dividend to be paid

by Mcpherson's limited company each year to its sharholders is increasing over the year. This

increment is being maintained due to increase in forecasted profit to be generated by business

over the year.

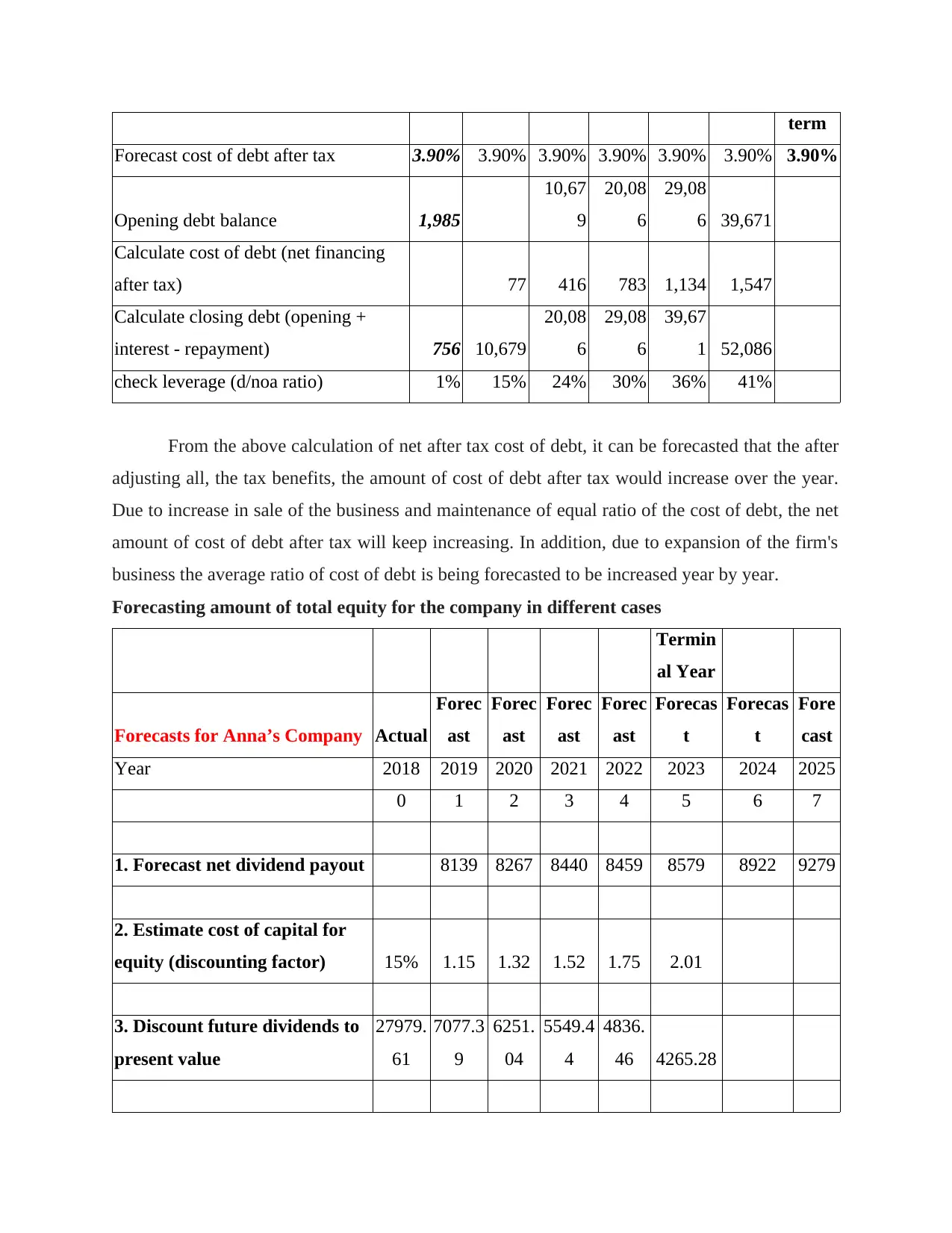

Net cost of debt after tax

Net cost of debt refers to the amount of debts remained after adjusting all the benefits and

taxes of the company.

9.Forecast cost of debt and debt balance

Particular 2018 2019 2020 2021 2022 2023 Long

Dividend policy of a business shows policy adopted by a company for paying dividends

to its shares holders. It reflects the percentage share of earning or profit generated by the

company that the shareholder would get as dividend. The dividend policy of a business

organisation directly affects its retained earning or the amount that would be kept by it for further

running of business activities.

Particulars 2018 2019 2020 2021 2022 2023

Long

term

7.Forecast net dividend

payout 72% 72% 72% 72% 72% 72% 72%

estimated as a % of NOPAT 8,139 9,604 11,044

12,70

1

14,60

6

8.Calculate net payments to

debt holders

payments = FCF - dividend -8,617 -8,990 -8,217 -9,450

-

10,868

For the purpose of forecasting above calculations of dividend payout ratio, it has been

assumed that the company would maintain the same ratio of profit for paying dividend.

Although, from the above calculation, it can be interpret that the amount of dividend to be paid

by Mcpherson's limited company each year to its sharholders is increasing over the year. This

increment is being maintained due to increase in forecasted profit to be generated by business

over the year.

Net cost of debt after tax

Net cost of debt refers to the amount of debts remained after adjusting all the benefits and

taxes of the company.

9.Forecast cost of debt and debt balance

Particular 2018 2019 2020 2021 2022 2023 Long

term

Forecast cost of debt after tax 3.90% 3.90% 3.90% 3.90% 3.90% 3.90% 3.90%

Opening debt balance 1,985

10,67

9

20,08

6

29,08

6 39,671

Calculate cost of debt (net financing

after tax) 77 416 783 1,134 1,547

Calculate closing debt (opening +

interest - repayment) 756 10,679

20,08

6

29,08

6

39,67

1 52,086

check leverage (d/noa ratio) 1% 15% 24% 30% 36% 41%

From the above calculation of net after tax cost of debt, it can be forecasted that the after

adjusting all, the tax benefits, the amount of cost of debt after tax would increase over the year.

Due to increase in sale of the business and maintenance of equal ratio of the cost of debt, the net

amount of cost of debt after tax will keep increasing. In addition, due to expansion of the firm's

business the average ratio of cost of debt is being forecasted to be increased year by year.

Forecasting amount of total equity for the company in different cases

Termin

al Year

Forecasts for Anna’s Company Actual

Forec

ast

Forec

ast

Forec

ast

Forec

ast

Forecas

t

Forecas

t

Fore

cast

Year 2018 2019 2020 2021 2022 2023 2024 2025

0 1 2 3 4 5 6 7

1. Forecast net dividend payout 8139 8267 8440 8459 8579 8922 9279

2. Estimate cost of capital for

equity (discounting factor) 15% 1.15 1.32 1.52 1.75 2.01

3. Discount future dividends to

present value

27979.

61

7077.3

9

6251.

04

5549.4

4

4836.

46 4265.28

Forecast cost of debt after tax 3.90% 3.90% 3.90% 3.90% 3.90% 3.90% 3.90%

Opening debt balance 1,985

10,67

9

20,08

6

29,08

6 39,671

Calculate cost of debt (net financing

after tax) 77 416 783 1,134 1,547

Calculate closing debt (opening +

interest - repayment) 756 10,679

20,08

6

29,08

6

39,67

1 52,086

check leverage (d/noa ratio) 1% 15% 24% 30% 36% 41%

From the above calculation of net after tax cost of debt, it can be forecasted that the after

adjusting all, the tax benefits, the amount of cost of debt after tax would increase over the year.

Due to increase in sale of the business and maintenance of equal ratio of the cost of debt, the net

amount of cost of debt after tax will keep increasing. In addition, due to expansion of the firm's

business the average ratio of cost of debt is being forecasted to be increased year by year.

Forecasting amount of total equity for the company in different cases

Termin

al Year

Forecasts for Anna’s Company Actual

Forec

ast

Forec

ast

Forec

ast

Forec

ast

Forecas

t

Forecas

t

Fore

cast

Year 2018 2019 2020 2021 2022 2023 2024 2025

0 1 2 3 4 5 6 7

1. Forecast net dividend payout 8139 8267 8440 8459 8579 8922 9279

2. Estimate cost of capital for

equity (discounting factor) 15% 1.15 1.32 1.52 1.75 2.01

3. Discount future dividends to

present value

27979.

61

7077.3

9

6251.

04

5549.4

4

4836.

46 4265.28

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.