Comprehensive Financial Analysis Report: Medibank Private Limited

VerifiedAdded on 2020/10/05

|19

|4322

|425

Report

AI Summary

This report provides a comprehensive financial analysis of Medibank Private Limited, a national health insurer based in Australia. The analysis includes a detailed company description, followed by an in-depth examination of financial ratios, including liquidity, profitability, and turnover ratios, to assess the company's operational performance. The report then explains various cash management instruments, such as treasury bills, certificates of deposit, commercial papers, and repurchase agreements, that Medibank can use to manage its short-term assets effectively. Furthermore, the report conducts a sensitivity analysis of provided data and identifies both systemic and unsystemic risks affecting the company's performance. The dividend payout ratio is calculated and commented on, and finally, a recommendation letter is provided for the company, summarizing the findings and offering strategic insights.

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Description about the corporation...........................................................................................1

Financial analysis of the company..............................................................................................2

2. Ratio analysis .........................................................................................................................2

3. Explaining the cash management instruments........................................................................4

4. Sensitivity analysis of the data provided.................................................................................5

5. Identifying and discussing the systemic and unsystemic risks affecting the company 's

performance.................................................................................................................................7

6. Calculating dividend payout ratio of 3 years & commenting on dividend policy of

company......................................................................................................................................8

7. Recommendation Letter for Company....................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Description about the corporation...........................................................................................1

Financial analysis of the company..............................................................................................2

2. Ratio analysis .........................................................................................................................2

3. Explaining the cash management instruments........................................................................4

4. Sensitivity analysis of the data provided.................................................................................5

5. Identifying and discussing the systemic and unsystemic risks affecting the company 's

performance.................................................................................................................................7

6. Calculating dividend payout ratio of 3 years & commenting on dividend policy of

company......................................................................................................................................8

7. Recommendation Letter for Company....................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Finance refers to the management of the money and involves the activities such as investing,

lending, budgeting, borrowing, forecasting and savings for attaining higher profitability. In other

words, it is the study of the ways in which the money is been managed and the actual process for

acquiring the required funds. It involves the financial services and the financial instruments.

Specifically, there are three sub classification of finance that are corporate finance, personal

finance and the public finance. The present study is based on the Medibank pvt. Ltd., a national

health insurer, headquartered in Australia. Furthermore, the report describes the company in

detail and ratio analysis has been evaluated for analysing the operational performance of the

enterprise. Various instruments for managing the liquidity are also described under the study.

Sensitivity analysis with the identification of the systematic and the unsystematic risks has been

included in the project. The aim of the projects is to assess the financial aspects of the company.

MAIN BODY

1. Description about the corporation

Medibank pvt. Ltd is an integrated private healthcare corporation facilitating private

health insurance and the health solution in the Australia. It operates its business in mainly two

segments that includes Health insurance and the Medibank health. Health insurance section

serves for private products of health insurance that involves Hospital cover which provides the

members with the health cover for treatments in the hospital. In ancillary cover, it offers the

health cover to the members in relation to the healthcare services like optical, physiotherapy and

dental (Company Overview of Medibank Private Limited, 2019). This section also offers the

products of health insurance to the overseas students and the visitors. The health segment of

Medibank facilitates health management and the telehealth services to the corporate customers

and the government. It also distributes the life, pet and travel insurance products. Underwriting

of the health insurance products is made by an entity under Medibank and the ahmother brands.

This corporation was founded during 1976 based in the Docklands, Australia. The purpose of the

organization is to provide better health services to its customers for their better lives. All the

things are functioned within the enterprise with the aim of improving the well being and the

health of the Australians and helping the people for facilitating them with the quality lives.

1

Finance refers to the management of the money and involves the activities such as investing,

lending, budgeting, borrowing, forecasting and savings for attaining higher profitability. In other

words, it is the study of the ways in which the money is been managed and the actual process for

acquiring the required funds. It involves the financial services and the financial instruments.

Specifically, there are three sub classification of finance that are corporate finance, personal

finance and the public finance. The present study is based on the Medibank pvt. Ltd., a national

health insurer, headquartered in Australia. Furthermore, the report describes the company in

detail and ratio analysis has been evaluated for analysing the operational performance of the

enterprise. Various instruments for managing the liquidity are also described under the study.

Sensitivity analysis with the identification of the systematic and the unsystematic risks has been

included in the project. The aim of the projects is to assess the financial aspects of the company.

MAIN BODY

1. Description about the corporation

Medibank pvt. Ltd is an integrated private healthcare corporation facilitating private

health insurance and the health solution in the Australia. It operates its business in mainly two

segments that includes Health insurance and the Medibank health. Health insurance section

serves for private products of health insurance that involves Hospital cover which provides the

members with the health cover for treatments in the hospital. In ancillary cover, it offers the

health cover to the members in relation to the healthcare services like optical, physiotherapy and

dental (Company Overview of Medibank Private Limited, 2019). This section also offers the

products of health insurance to the overseas students and the visitors. The health segment of

Medibank facilitates health management and the telehealth services to the corporate customers

and the government. It also distributes the life, pet and travel insurance products. Underwriting

of the health insurance products is made by an entity under Medibank and the ahmother brands.

This corporation was founded during 1976 based in the Docklands, Australia. The purpose of the

organization is to provide better health services to its customers for their better lives. All the

things are functioned within the enterprise with the aim of improving the well being and the

health of the Australians and helping the people for facilitating them with the quality lives.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

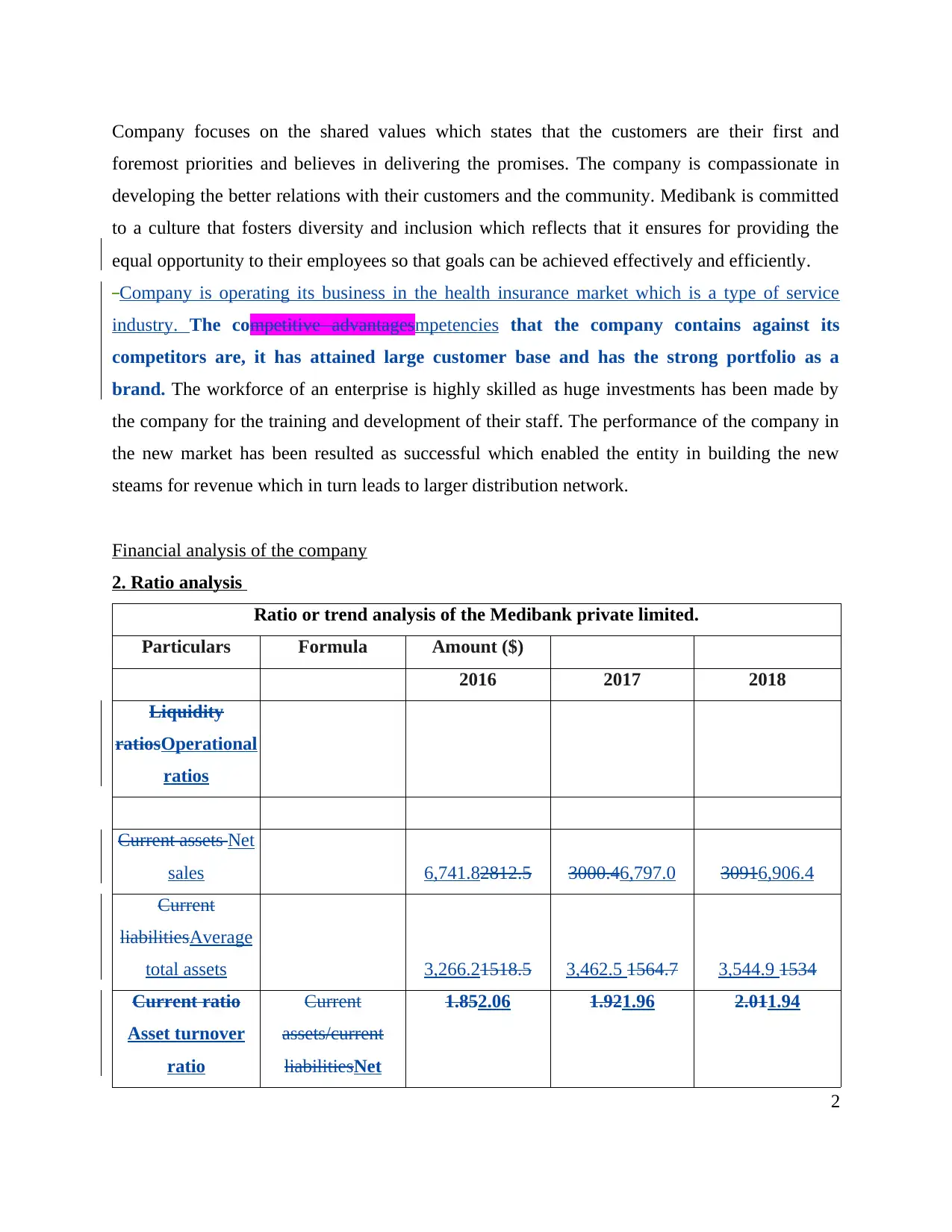

Company focuses on the shared values which states that the customers are their first and

foremost priorities and believes in delivering the promises. The company is compassionate in

developing the better relations with their customers and the community. Medibank is committed

to a culture that fosters diversity and inclusion which reflects that it ensures for providing the

equal opportunity to their employees so that goals can be achieved effectively and efficiently.

Company is operating its business in the health insurance market which is a type of service

industry. The competitive advantagesmpetencies that the company contains against its

competitors are, it has attained large customer base and has the strong portfolio as a

brand. The workforce of an enterprise is highly skilled as huge investments has been made by

the company for the training and development of their staff. The performance of the company in

the new market has been resulted as successful which enabled the entity in building the new

steams for revenue which in turn leads to larger distribution network.

Financial analysis of the company

2. Ratio analysis

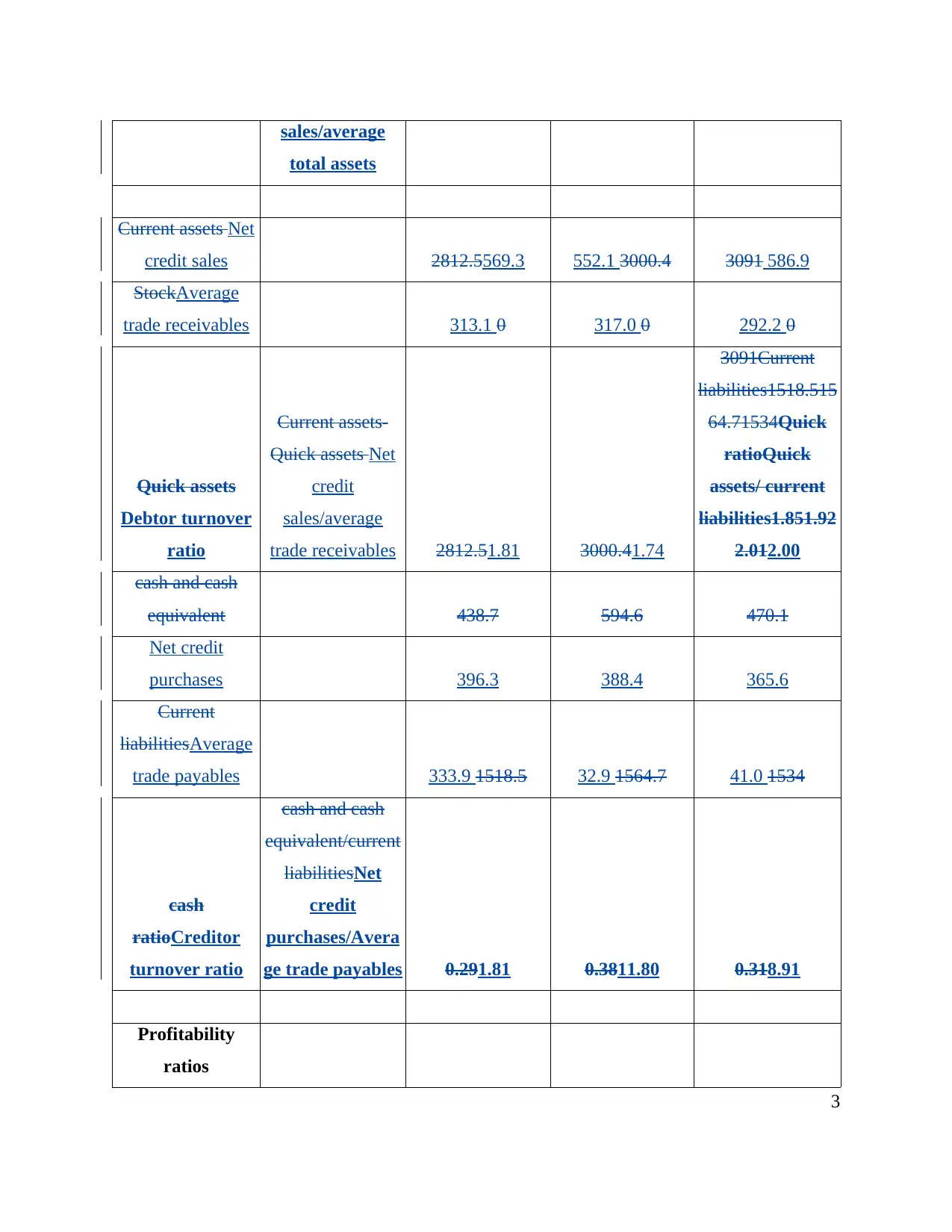

Ratio or trend analysis of the Medibank private limited.

Particulars Formula Amount ($)

2016 2017 2018

Liquidity

ratiosOperational

ratios

Current assets Net

sales 6,741.82812.5 3000.46,797.0 30916,906.4

Current

liabilitiesAverage

total assets 3,266.21518.5 3,462.5 1564.7 3,544.9 1534

Current ratio

Asset turnover

ratio

Current

assets/current

liabilitiesNet

1.852.06 1.921.96 2.011.94

2

foremost priorities and believes in delivering the promises. The company is compassionate in

developing the better relations with their customers and the community. Medibank is committed

to a culture that fosters diversity and inclusion which reflects that it ensures for providing the

equal opportunity to their employees so that goals can be achieved effectively and efficiently.

Company is operating its business in the health insurance market which is a type of service

industry. The competitive advantagesmpetencies that the company contains against its

competitors are, it has attained large customer base and has the strong portfolio as a

brand. The workforce of an enterprise is highly skilled as huge investments has been made by

the company for the training and development of their staff. The performance of the company in

the new market has been resulted as successful which enabled the entity in building the new

steams for revenue which in turn leads to larger distribution network.

Financial analysis of the company

2. Ratio analysis

Ratio or trend analysis of the Medibank private limited.

Particulars Formula Amount ($)

2016 2017 2018

Liquidity

ratiosOperational

ratios

Current assets Net

sales 6,741.82812.5 3000.46,797.0 30916,906.4

Current

liabilitiesAverage

total assets 3,266.21518.5 3,462.5 1564.7 3,544.9 1534

Current ratio

Asset turnover

ratio

Current

assets/current

liabilitiesNet

1.852.06 1.921.96 2.011.94

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sales/average

total assets

Current assets Net

credit sales 2812.5569.3 552.1 3000.4 3091 586.9

StockAverage

trade receivables 313.1 0 317.0 0 292.2 0

Quick assets

Debtor turnover

ratio

Current assets-

Quick assets Net

credit

sales/average

trade receivables 2812.51.81 3000.41.74

3091Current

liabilities1518.515

64.71534Quick

ratioQuick

assets/ current

liabilities1.851.92

2.012.00

cash and cash

equivalent 438.7 594.6 470.1

Net credit

purchases 396.3 388.4 365.6

Current

liabilitiesAverage

trade payables 333.9 1518.5 32.9 1564.7 41.0 1534

cash

ratioCreditor

turnover ratio

cash and cash

equivalent/current

liabilitiesNet

credit

purchases/Avera

ge trade payables 0.291.81 0.3811.80 0.318.91

Profitability

ratios

3

total assets

Current assets Net

credit sales 2812.5569.3 552.1 3000.4 3091 586.9

StockAverage

trade receivables 313.1 0 317.0 0 292.2 0

Quick assets

Debtor turnover

ratio

Current assets-

Quick assets Net

credit

sales/average

trade receivables 2812.51.81 3000.41.74

3091Current

liabilities1518.515

64.71534Quick

ratioQuick

assets/ current

liabilities1.851.92

2.012.00

cash and cash

equivalent 438.7 594.6 470.1

Net credit

purchases 396.3 388.4 365.6

Current

liabilitiesAverage

trade payables 333.9 1518.5 32.9 1564.7 41.0 1534

cash

ratioCreditor

turnover ratio

cash and cash

equivalent/current

liabilitiesNet

credit

purchases/Avera

ge trade payables 0.291.81 0.3811.80 0.318.91

Profitability

ratios

3

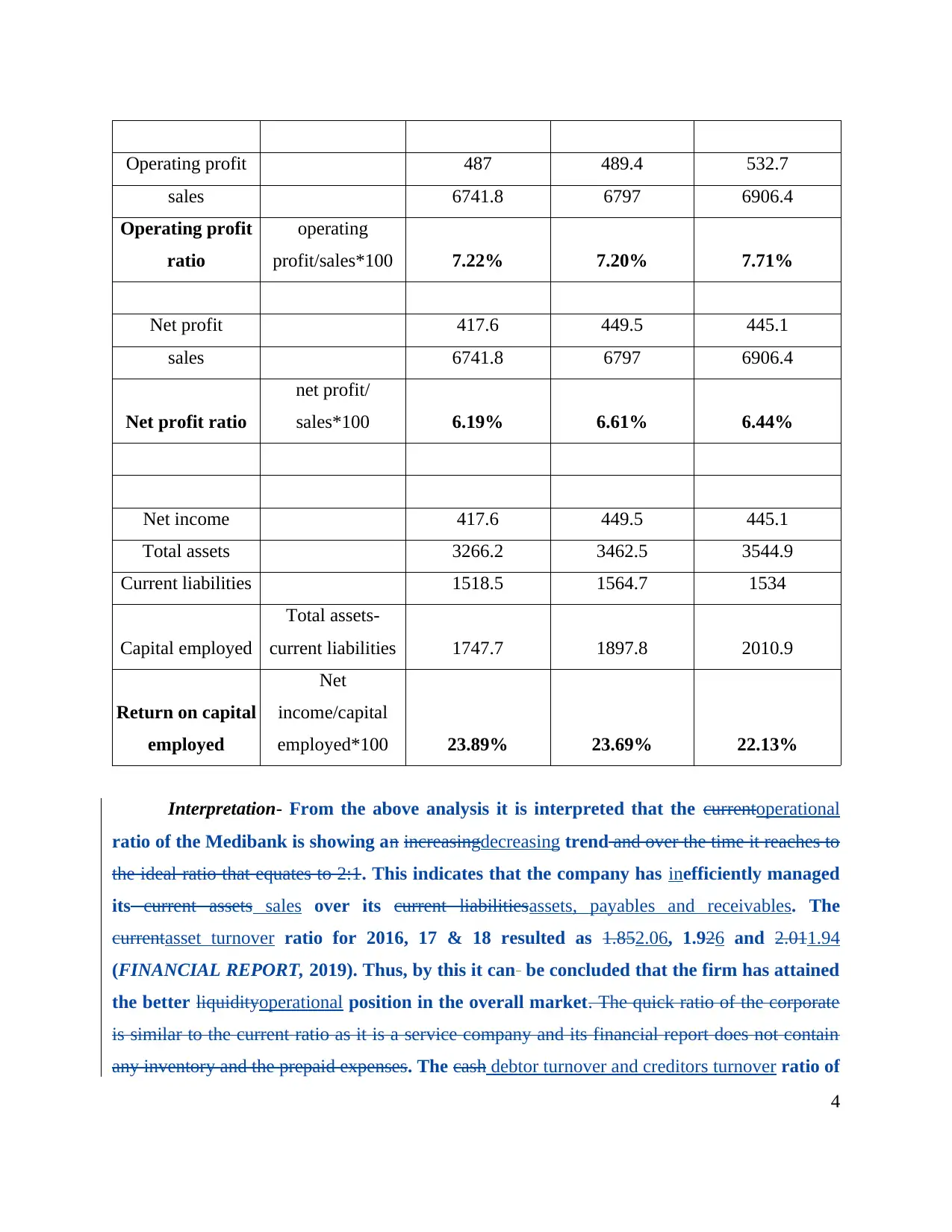

Operating profit 487 489.4 532.7

sales 6741.8 6797 6906.4

Operating profit

ratio

operating

profit/sales*100 7.22% 7.20% 7.71%

Net profit 417.6 449.5 445.1

sales 6741.8 6797 6906.4

Net profit ratio

net profit/

sales*100 6.19% 6.61% 6.44%

Net income 417.6 449.5 445.1

Total assets 3266.2 3462.5 3544.9

Current liabilities 1518.5 1564.7 1534

Capital employed

Total assets-

current liabilities 1747.7 1897.8 2010.9

Return on capital

employed

Net

income/capital

employed*100 23.89% 23.69% 22.13%

Interpretation- From the above analysis it is interpreted that the currentoperational

ratio of the Medibank is showing an increasingdecreasing trend and over the time it reaches to

the ideal ratio that equates to 2:1. This indicates that the company has inefficiently managed

its current assets sales over its current liabilitiesassets, payables and receivables. The

currentasset turnover ratio for 2016, 17 & 18 resulted as 1.852.06, 1.926 and 2.011.94

(FINANCIAL REPORT, 2019). Thus, by this it can be concluded that the firm has attained

the better liquidityoperational position in the overall market. The quick ratio of the corporate

is similar to the current ratio as it is a service company and its financial report does not contain

any inventory and the prepaid expenses. The cash debtor turnover and creditors turnover ratio of

4

sales 6741.8 6797 6906.4

Operating profit

ratio

operating

profit/sales*100 7.22% 7.20% 7.71%

Net profit 417.6 449.5 445.1

sales 6741.8 6797 6906.4

Net profit ratio

net profit/

sales*100 6.19% 6.61% 6.44%

Net income 417.6 449.5 445.1

Total assets 3266.2 3462.5 3544.9

Current liabilities 1518.5 1564.7 1534

Capital employed

Total assets-

current liabilities 1747.7 1897.8 2010.9

Return on capital

employed

Net

income/capital

employed*100 23.89% 23.69% 22.13%

Interpretation- From the above analysis it is interpreted that the currentoperational

ratio of the Medibank is showing an increasingdecreasing trend and over the time it reaches to

the ideal ratio that equates to 2:1. This indicates that the company has inefficiently managed

its current assets sales over its current liabilitiesassets, payables and receivables. The

currentasset turnover ratio for 2016, 17 & 18 resulted as 1.852.06, 1.926 and 2.011.94

(FINANCIAL REPORT, 2019). Thus, by this it can be concluded that the firm has attained

the better liquidityoperational position in the overall market. The quick ratio of the corporate

is similar to the current ratio as it is a service company and its financial report does not contain

any inventory and the prepaid expenses. The cash debtor turnover and creditors turnover ratio of

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

an entity is also reflecting an increasing and the decreasing trend which means company has

effectively managed its cashdebtors resourcesbut has not appropriately managed its creditors so

that adequate cashwhich leads to greater requirement of funds is available in the future for

making further investments and in meeting any uncertainties. The cashcreditors turnover

ratio computed as for the 3 years are 0.291.81, 0.3811.80 and 0.318.91. The profitability ratio

includes the operating ratio which indicates the income earned by the enterprise after paying off

all the direct and indirect expenses. The operating profit ratio of the Medibank has been

increased from 7.22% to 7.71% which means the performance of the firm has been enhanced

over the years. Net profit ratio of the company showing a minute or very little changes in the

results which indicates that the profitability of the company has remained stable over the years.

Net profit ratio for the year 2016 equates to 6.19% while in 2017 it evaluated as 6.61% and in the

year 2018 it is calculated as 6.44% which depicts that the corporate earns positive and good

return after the payment of all its cost and tax liability. Return on capital employed of the

Medibank has depicted the declining trend which reflects that returns generated on the capital are

getting lower year by year. Thus, it can be summarized that the operational and profitability

position of the Medibank is improving due to its expansion in the new markets and the products.

3. Explaining the cash management instruments

Short-term cash management instruments are the securities that provides for the safest

investment options to the entity for efficient and effective management of their current assets.

Such marketable securities include the treasury bills, certificate of deposits, commercial papers

and the repurchase agreements. These instruments are indicated as the good option for the

investment in terms of short-term (Bohn, 2015). Such instruments ensure in maintaining better

liquidity position of the Medibank in the overall market.

Treasury bills- It is cash management instrument that has the maturity for a period equals

to or less than one year. Treasury bills are issued by the government at the price which is less

than the face value. The types of the bill reflectsreflect its maturity period such as 14 days T-

bills, 91 days T-bills, 182 days T-bills and 364 days T-bills. The holder, at the time of the

maturity can get it en-cash from the government (Fabozzi and Thurston, 2015). Such securities

are risk-free, marketable and affordable. The security that is associated to the bills generates low

returns.

5

effectively managed its cashdebtors resourcesbut has not appropriately managed its creditors so

that adequate cashwhich leads to greater requirement of funds is available in the future for

making further investments and in meeting any uncertainties. The cashcreditors turnover

ratio computed as for the 3 years are 0.291.81, 0.3811.80 and 0.318.91. The profitability ratio

includes the operating ratio which indicates the income earned by the enterprise after paying off

all the direct and indirect expenses. The operating profit ratio of the Medibank has been

increased from 7.22% to 7.71% which means the performance of the firm has been enhanced

over the years. Net profit ratio of the company showing a minute or very little changes in the

results which indicates that the profitability of the company has remained stable over the years.

Net profit ratio for the year 2016 equates to 6.19% while in 2017 it evaluated as 6.61% and in the

year 2018 it is calculated as 6.44% which depicts that the corporate earns positive and good

return after the payment of all its cost and tax liability. Return on capital employed of the

Medibank has depicted the declining trend which reflects that returns generated on the capital are

getting lower year by year. Thus, it can be summarized that the operational and profitability

position of the Medibank is improving due to its expansion in the new markets and the products.

3. Explaining the cash management instruments

Short-term cash management instruments are the securities that provides for the safest

investment options to the entity for efficient and effective management of their current assets.

Such marketable securities include the treasury bills, certificate of deposits, commercial papers

and the repurchase agreements. These instruments are indicated as the good option for the

investment in terms of short-term (Bohn, 2015). Such instruments ensure in maintaining better

liquidity position of the Medibank in the overall market.

Treasury bills- It is cash management instrument that has the maturity for a period equals

to or less than one year. Treasury bills are issued by the government at the price which is less

than the face value. The types of the bill reflectsreflect its maturity period such as 14 days T-

bills, 91 days T-bills, 182 days T-bills and 364 days T-bills. The holder, at the time of the

maturity can get it en-cash from the government (Fabozzi and Thurston, 2015). Such securities

are risk-free, marketable and affordable. The security that is associated to the bills generates low

returns.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Certificate of deposits- It is the marketable securities that are issued by commercial

banks with the maturity period beginning from 3 months to 5 years. The return ascertained on the

certificate of deposits is much higher than compare to the treasury bills as it contains higher risk

level. Medibank can manage its current assets by purchasing the certificate deposits as it can be

easily convertible into the cash within a shorter period.

Commercial papers- It is the short-term loan that the Medibank can buy from the other

corporation for utilizing in maintaining their financing accounts, inventories and receivable. The

denomination of the commercial papers is higher than the treasury bills and the certificate of

deposits (Gürkaynak, Sack, and Swanson, 2015). Maturity period is maximum of nine months

of the commercial papers. Company can anticipate its financial situation over the time by

purchasing this cash management instrument which leads to the safest investment.

Bankers acceptance- This instrument is guaranteed by the bank and refers to as the short-

term credit note. With the banker's acceptance Medibank can trade in secondary market as it

offers its trading in the capital market. It is majorly used by the corporation in financing the

imports, exports and the other transactions. This instrument provides the option to the holders in

terms of selling it or holding the instrument (Chan and et.al., 2019). It is not necessary to hold it

till the maturity date.

Repurchase agreements- Such agreements are the short-term loans which has the

maturity of minimum 1 day to 2 weeks. Repurchase agreements are arranged by the sale of the

securities to the investor by signing an agreement for repurchasing the instruments at the fixed

price on the specified or fixed date.

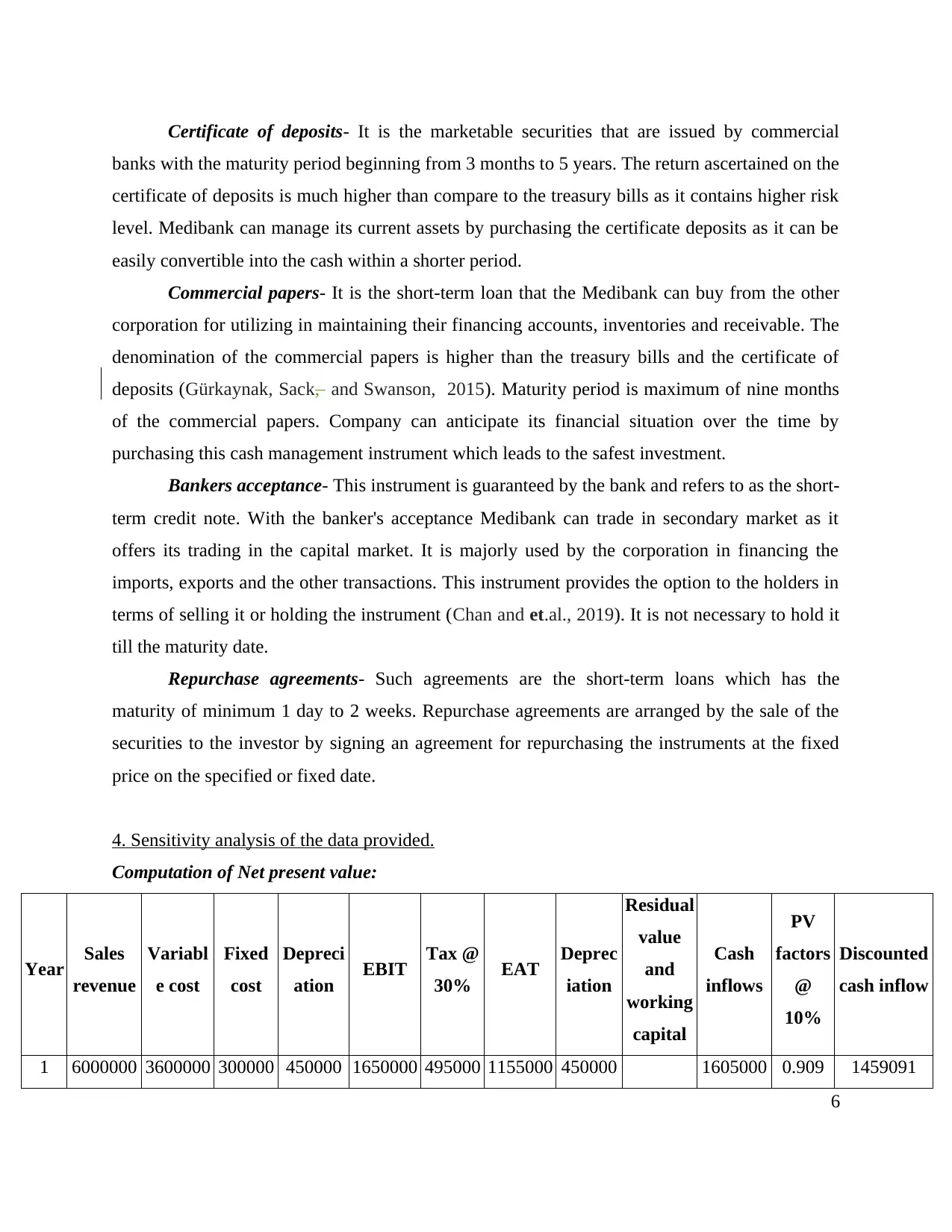

4. Sensitivity analysis of the data provided.

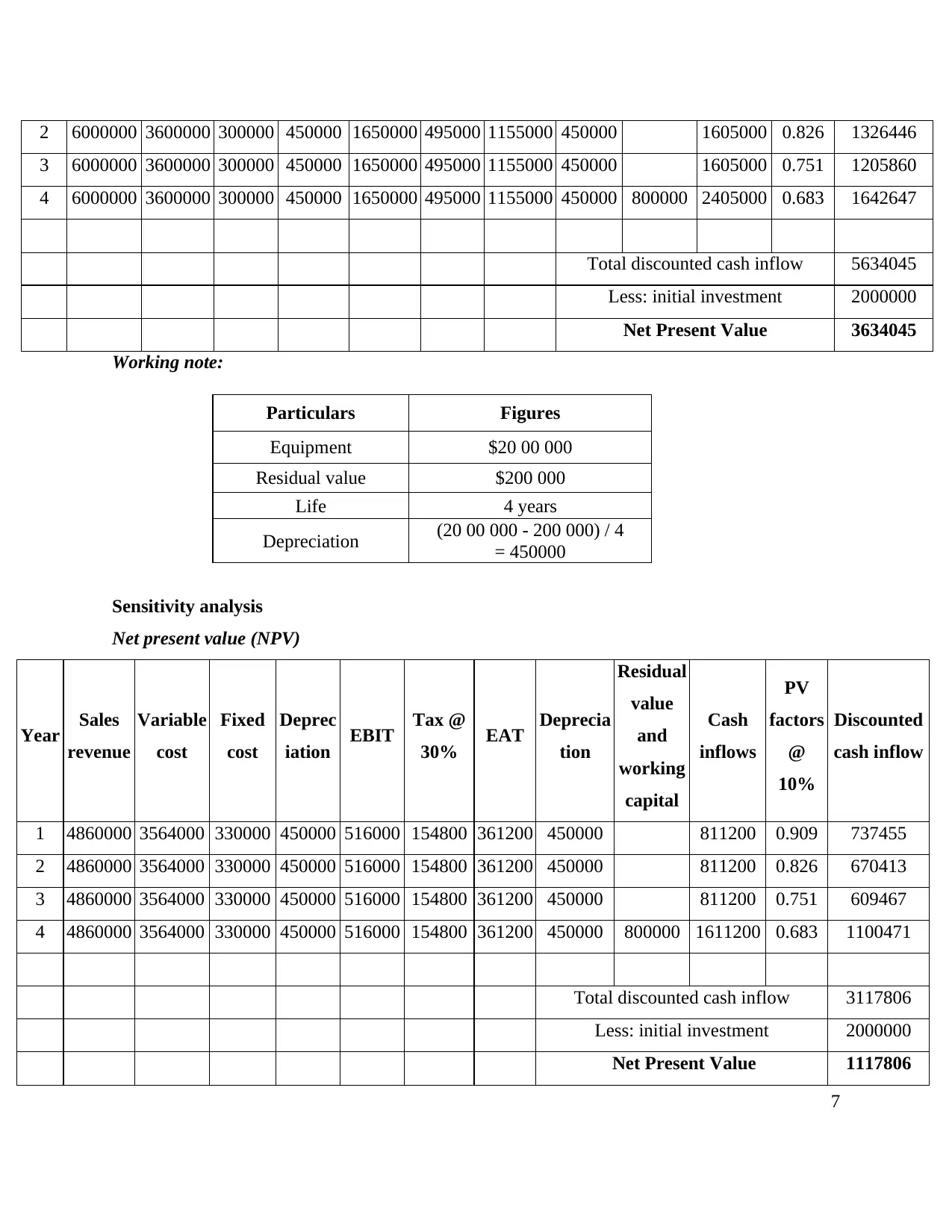

Computation of Net present value:

Year Sales

revenue

Variabl

e cost

Fixed

cost

Depreci

ation EBIT Tax @

30% EAT Deprec

iation

Residual

value

and

working

capital

Cash

inflows

PV

factors

@

10%

Discounted

cash inflow

1 6000000 3600000 300000 450000 1650000 495000 1155000 450000 1605000 0.909 1459091

6

banks with the maturity period beginning from 3 months to 5 years. The return ascertained on the

certificate of deposits is much higher than compare to the treasury bills as it contains higher risk

level. Medibank can manage its current assets by purchasing the certificate deposits as it can be

easily convertible into the cash within a shorter period.

Commercial papers- It is the short-term loan that the Medibank can buy from the other

corporation for utilizing in maintaining their financing accounts, inventories and receivable. The

denomination of the commercial papers is higher than the treasury bills and the certificate of

deposits (Gürkaynak, Sack, and Swanson, 2015). Maturity period is maximum of nine months

of the commercial papers. Company can anticipate its financial situation over the time by

purchasing this cash management instrument which leads to the safest investment.

Bankers acceptance- This instrument is guaranteed by the bank and refers to as the short-

term credit note. With the banker's acceptance Medibank can trade in secondary market as it

offers its trading in the capital market. It is majorly used by the corporation in financing the

imports, exports and the other transactions. This instrument provides the option to the holders in

terms of selling it or holding the instrument (Chan and et.al., 2019). It is not necessary to hold it

till the maturity date.

Repurchase agreements- Such agreements are the short-term loans which has the

maturity of minimum 1 day to 2 weeks. Repurchase agreements are arranged by the sale of the

securities to the investor by signing an agreement for repurchasing the instruments at the fixed

price on the specified or fixed date.

4. Sensitivity analysis of the data provided.

Computation of Net present value:

Year Sales

revenue

Variabl

e cost

Fixed

cost

Depreci

ation EBIT Tax @

30% EAT Deprec

iation

Residual

value

and

working

capital

Cash

inflows

PV

factors

@

10%

Discounted

cash inflow

1 6000000 3600000 300000 450000 1650000 495000 1155000 450000 1605000 0.909 1459091

6

2 6000000 3600000 300000 450000 1650000 495000 1155000 450000 1605000 0.826 1326446

3 6000000 3600000 300000 450000 1650000 495000 1155000 450000 1605000 0.751 1205860

4 6000000 3600000 300000 450000 1650000 495000 1155000 450000 800000 2405000 0.683 1642647

Total discounted cash inflow 5634045

Less: initial investment 2000000

Net Present Value 3634045

Working note:

Particulars Figures

Equipment $20 00 000

Residual value $200 000

Life 4 years

Depreciation (20 00 000 - 200 000) / 4

= 450000

Sensitivity analysis

Net present value (NPV)

Year Sales

revenue

Variable

cost

Fixed

cost

Deprec

iation EBIT Tax @

30% EAT Deprecia

tion

Residual

value

and

working

capital

Cash

inflows

PV

factors

@

10%

Discounted

cash inflow

1 4860000 3564000 330000 450000 516000 154800 361200 450000 811200 0.909 737455

2 4860000 3564000 330000 450000 516000 154800 361200 450000 811200 0.826 670413

3 4860000 3564000 330000 450000 516000 154800 361200 450000 811200 0.751 609467

4 4860000 3564000 330000 450000 516000 154800 361200 450000 800000 1611200 0.683 1100471

Total discounted cash inflow 3117806

Less: initial investment 2000000

Net Present Value 1117806

7

3 6000000 3600000 300000 450000 1650000 495000 1155000 450000 1605000 0.751 1205860

4 6000000 3600000 300000 450000 1650000 495000 1155000 450000 800000 2405000 0.683 1642647

Total discounted cash inflow 5634045

Less: initial investment 2000000

Net Present Value 3634045

Working note:

Particulars Figures

Equipment $20 00 000

Residual value $200 000

Life 4 years

Depreciation (20 00 000 - 200 000) / 4

= 450000

Sensitivity analysis

Net present value (NPV)

Year Sales

revenue

Variable

cost

Fixed

cost

Deprec

iation EBIT Tax @

30% EAT Deprecia

tion

Residual

value

and

working

capital

Cash

inflows

PV

factors

@

10%

Discounted

cash inflow

1 4860000 3564000 330000 450000 516000 154800 361200 450000 811200 0.909 737455

2 4860000 3564000 330000 450000 516000 154800 361200 450000 811200 0.826 670413

3 4860000 3564000 330000 450000 516000 154800 361200 450000 811200 0.751 609467

4 4860000 3564000 330000 450000 516000 154800 361200 450000 800000 1611200 0.683 1100471

Total discounted cash inflow 3117806

Less: initial investment 2000000

Net Present Value 1117806

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

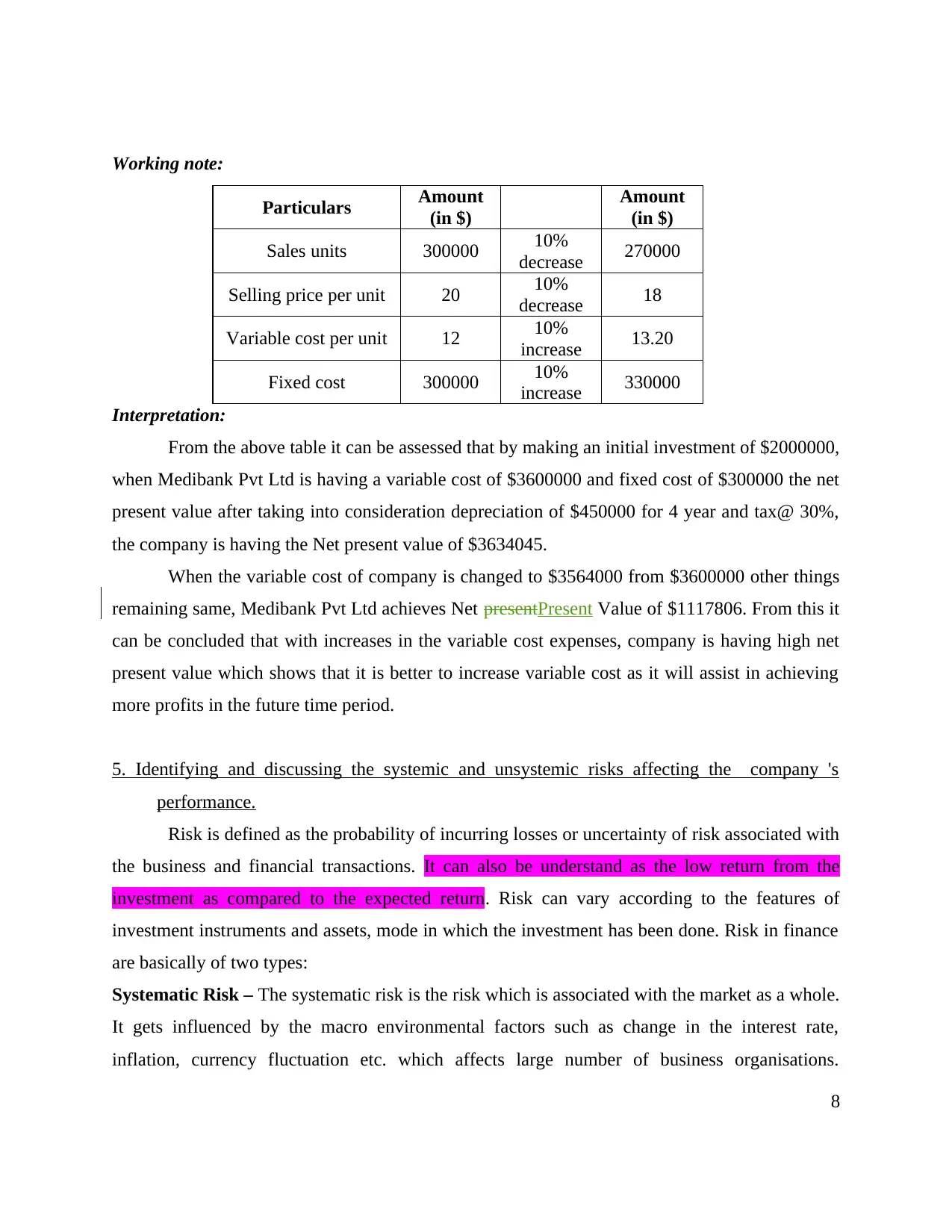

Working note:

Particulars Amount

(in $)

Amount

(in $)

Sales units 300000 10%

decrease 270000

Selling price per unit 20 10%

decrease 18

Variable cost per unit 12 10%

increase 13.20

Fixed cost 300000 10%

increase 330000

Interpretation:

From the above table it can be assessed that by making an initial investment of $2000000,

when Medibank Pvt Ltd is having a variable cost of $3600000 and fixed cost of $300000 the net

present value after taking into consideration depreciation of $450000 for 4 year and tax@ 30%,

the company is having the Net present value of $3634045.

When the variable cost of company is changed to $3564000 from $3600000 other things

remaining same, Medibank Pvt Ltd achieves Net presentPresent Value of $1117806. From this it

can be concluded that with increases in the variable cost expenses, company is having high net

present value which shows that it is better to increase variable cost as it will assist in achieving

more profits in the future time period.

5. Identifying and discussing the systemic and unsystemic risks affecting the company 's

performance.

Risk is defined as the probability of incurring losses or uncertainty of risk associated with

the business and financial transactions. It can also be understand as the low return from the

investment as compared to the expected return. Risk can vary according to the features of

investment instruments and assets, mode in which the investment has been done. Risk in finance

are basically of two types:

Systematic Risk – The systematic risk is the risk which is associated with the market as a whole.

It gets influenced by the macro environmental factors such as change in the interest rate,

inflation, currency fluctuation etc. which affects large number of business organisations.

8

Particulars Amount

(in $)

Amount

(in $)

Sales units 300000 10%

decrease 270000

Selling price per unit 20 10%

decrease 18

Variable cost per unit 12 10%

increase 13.20

Fixed cost 300000 10%

increase 330000

Interpretation:

From the above table it can be assessed that by making an initial investment of $2000000,

when Medibank Pvt Ltd is having a variable cost of $3600000 and fixed cost of $300000 the net

present value after taking into consideration depreciation of $450000 for 4 year and tax@ 30%,

the company is having the Net present value of $3634045.

When the variable cost of company is changed to $3564000 from $3600000 other things

remaining same, Medibank Pvt Ltd achieves Net presentPresent Value of $1117806. From this it

can be concluded that with increases in the variable cost expenses, company is having high net

present value which shows that it is better to increase variable cost as it will assist in achieving

more profits in the future time period.

5. Identifying and discussing the systemic and unsystemic risks affecting the company 's

performance.

Risk is defined as the probability of incurring losses or uncertainty of risk associated with

the business and financial transactions. It can also be understand as the low return from the

investment as compared to the expected return. Risk can vary according to the features of

investment instruments and assets, mode in which the investment has been done. Risk in finance

are basically of two types:

Systematic Risk – The systematic risk is the risk which is associated with the market as a whole.

It gets influenced by the macro environmental factors such as change in the interest rate,

inflation, currency fluctuation etc. which affects large number of business organisations.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

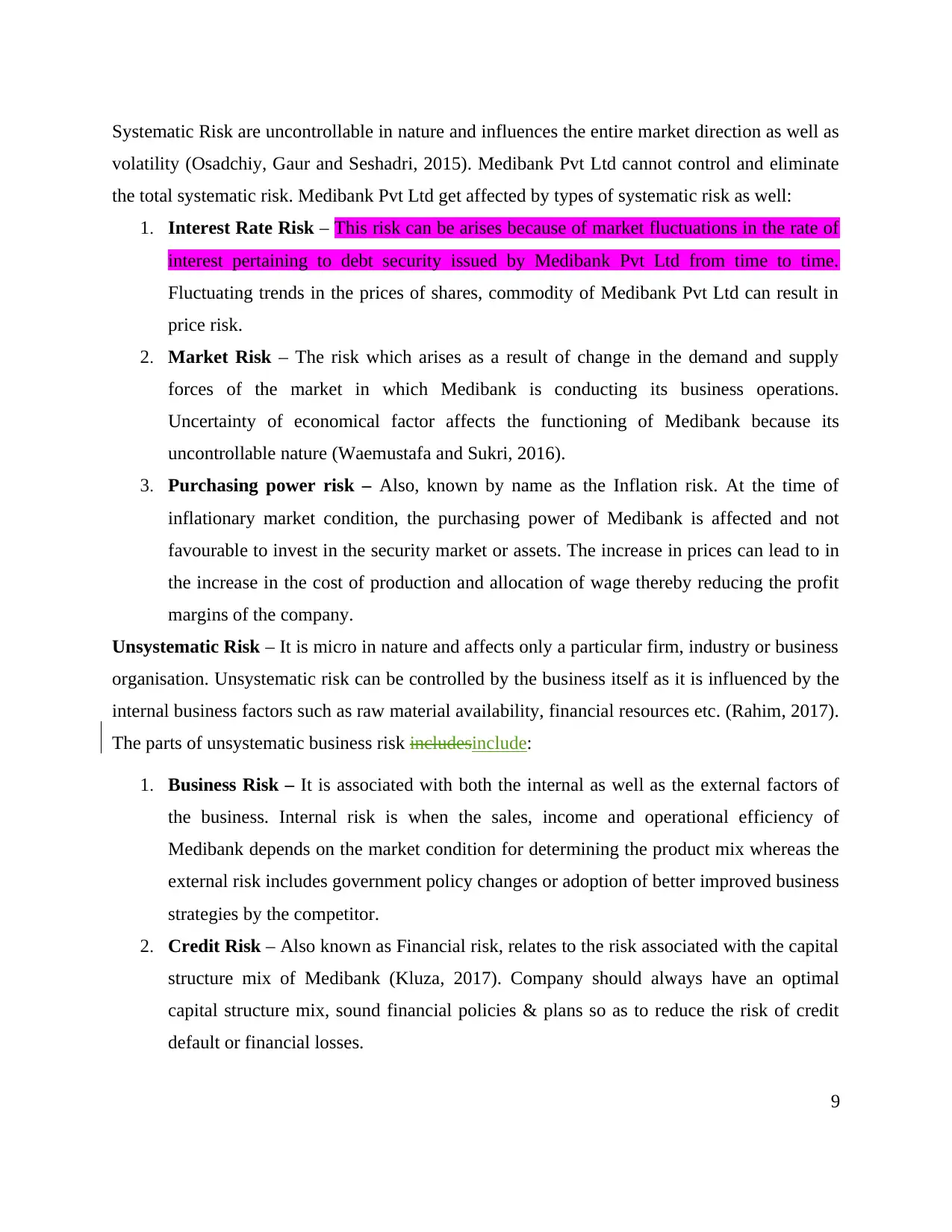

Systematic Risk are uncontrollable in nature and influences the entire market direction as well as

volatility (Osadchiy, Gaur and Seshadri, 2015). Medibank Pvt Ltd cannot control and eliminate

the total systematic risk. Medibank Pvt Ltd get affected by types of systematic risk as well:

1. Interest Rate Risk – This risk can be arises because of market fluctuations in the rate of

interest pertaining to debt security issued by Medibank Pvt Ltd from time to time.

Fluctuating trends in the prices of shares, commodity of Medibank Pvt Ltd can result in

price risk.

2. Market Risk – The risk which arises as a result of change in the demand and supply

forces of the market in which Medibank is conducting its business operations.

Uncertainty of economical factor affects the functioning of Medibank because its

uncontrollable nature (Waemustafa and Sukri, 2016).

3. Purchasing power risk – Also, known by name as the Inflation risk. At the time of

inflationary market condition, the purchasing power of Medibank is affected and not

favourable to invest in the security market or assets. The increase in prices can lead to in

the increase in the cost of production and allocation of wage thereby reducing the profit

margins of the company.

Unsystematic Risk – It is micro in nature and affects only a particular firm, industry or business

organisation. Unsystematic risk can be controlled by the business itself as it is influenced by the

internal business factors such as raw material availability, financial resources etc. (Rahim, 2017).

The parts of unsystematic business risk includesinclude:

1. Business Risk – It is associated with both the internal as well as the external factors of

the business. Internal risk is when the sales, income and operational efficiency of

Medibank depends on the market condition for determining the product mix whereas the

external risk includes government policy changes or adoption of better improved business

strategies by the competitor.

2. Credit Risk – Also known as Financial risk, relates to the risk associated with the capital

structure mix of Medibank (Kluza, 2017). Company should always have an optimal

capital structure mix, sound financial policies & plans so as to reduce the risk of credit

default or financial losses.

9

volatility (Osadchiy, Gaur and Seshadri, 2015). Medibank Pvt Ltd cannot control and eliminate

the total systematic risk. Medibank Pvt Ltd get affected by types of systematic risk as well:

1. Interest Rate Risk – This risk can be arises because of market fluctuations in the rate of

interest pertaining to debt security issued by Medibank Pvt Ltd from time to time.

Fluctuating trends in the prices of shares, commodity of Medibank Pvt Ltd can result in

price risk.

2. Market Risk – The risk which arises as a result of change in the demand and supply

forces of the market in which Medibank is conducting its business operations.

Uncertainty of economical factor affects the functioning of Medibank because its

uncontrollable nature (Waemustafa and Sukri, 2016).

3. Purchasing power risk – Also, known by name as the Inflation risk. At the time of

inflationary market condition, the purchasing power of Medibank is affected and not

favourable to invest in the security market or assets. The increase in prices can lead to in

the increase in the cost of production and allocation of wage thereby reducing the profit

margins of the company.

Unsystematic Risk – It is micro in nature and affects only a particular firm, industry or business

organisation. Unsystematic risk can be controlled by the business itself as it is influenced by the

internal business factors such as raw material availability, financial resources etc. (Rahim, 2017).

The parts of unsystematic business risk includesinclude:

1. Business Risk – It is associated with both the internal as well as the external factors of

the business. Internal risk is when the sales, income and operational efficiency of

Medibank depends on the market condition for determining the product mix whereas the

external risk includes government policy changes or adoption of better improved business

strategies by the competitor.

2. Credit Risk – Also known as Financial risk, relates to the risk associated with the capital

structure mix of Medibank (Kluza, 2017). Company should always have an optimal

capital structure mix, sound financial policies & plans so as to reduce the risk of credit

default or financial losses.

9

Medibank Pvt Ltd can protect its business operations from Systematic risk by making

proper allocation of the assets whereas the Unsystematic risk can be hedged and eliminated by

making diversification or rebalancing in the business portfolio.

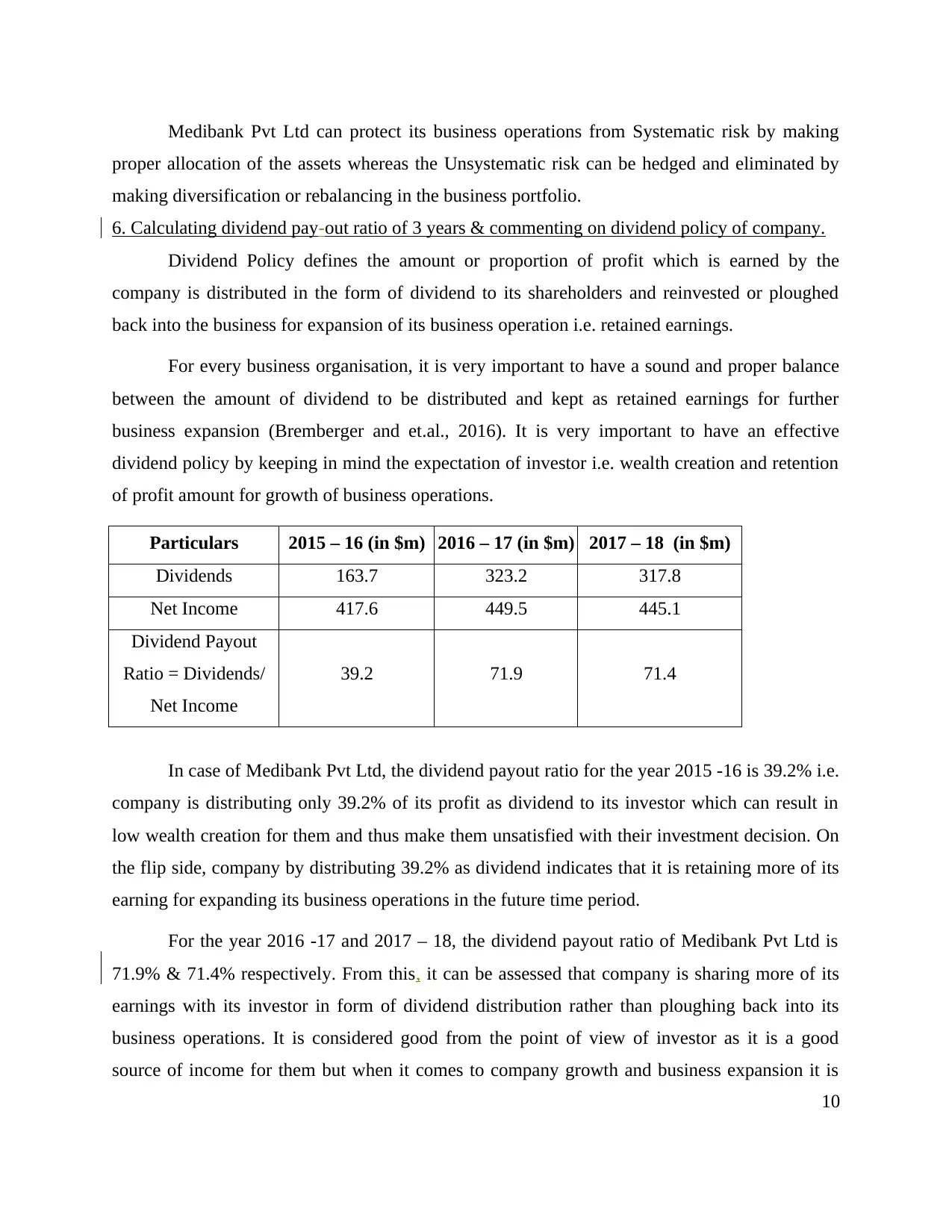

6. Calculating dividend pay-out ratio of 3 years & commenting on dividend policy of company.

Dividend Policy defines the amount or proportion of profit which is earned by the

company is distributed in the form of dividend to its shareholders and reinvested or ploughed

back into the business for expansion of its business operation i.e. retained earnings.

For every business organisation, it is very important to have a sound and proper balance

between the amount of dividend to be distributed and kept as retained earnings for further

business expansion (Bremberger and et.al., 2016). It is very important to have an effective

dividend policy by keeping in mind the expectation of investor i.e. wealth creation and retention

of profit amount for growth of business operations.

Particulars 2015 – 16 (in $m) 2016 – 17 (in $m) 2017 – 18 (in $m)

Dividends 163.7 323.2 317.8

Net Income 417.6 449.5 445.1

Dividend Payout

Ratio = Dividends/

Net Income

39.2 71.9 71.4

In case of Medibank Pvt Ltd, the dividend payout ratio for the year 2015 -16 is 39.2% i.e.

company is distributing only 39.2% of its profit as dividend to its investor which can result in

low wealth creation for them and thus make them unsatisfied with their investment decision. On

the flip side, company by distributing 39.2% as dividend indicates that it is retaining more of its

earning for expanding its business operations in the future time period.

For the year 2016 -17 and 2017 – 18, the dividend payout ratio of Medibank Pvt Ltd is

71.9% & 71.4% respectively. From this, it can be assessed that company is sharing more of its

earnings with its investor in form of dividend distribution rather than ploughing back into its

business operations. It is considered good from the point of view of investor as it is a good

source of income for them but when it comes to company growth and business expansion it is

10

proper allocation of the assets whereas the Unsystematic risk can be hedged and eliminated by

making diversification or rebalancing in the business portfolio.

6. Calculating dividend pay-out ratio of 3 years & commenting on dividend policy of company.

Dividend Policy defines the amount or proportion of profit which is earned by the

company is distributed in the form of dividend to its shareholders and reinvested or ploughed

back into the business for expansion of its business operation i.e. retained earnings.

For every business organisation, it is very important to have a sound and proper balance

between the amount of dividend to be distributed and kept as retained earnings for further

business expansion (Bremberger and et.al., 2016). It is very important to have an effective

dividend policy by keeping in mind the expectation of investor i.e. wealth creation and retention

of profit amount for growth of business operations.

Particulars 2015 – 16 (in $m) 2016 – 17 (in $m) 2017 – 18 (in $m)

Dividends 163.7 323.2 317.8

Net Income 417.6 449.5 445.1

Dividend Payout

Ratio = Dividends/

Net Income

39.2 71.9 71.4

In case of Medibank Pvt Ltd, the dividend payout ratio for the year 2015 -16 is 39.2% i.e.

company is distributing only 39.2% of its profit as dividend to its investor which can result in

low wealth creation for them and thus make them unsatisfied with their investment decision. On

the flip side, company by distributing 39.2% as dividend indicates that it is retaining more of its

earning for expanding its business operations in the future time period.

For the year 2016 -17 and 2017 – 18, the dividend payout ratio of Medibank Pvt Ltd is

71.9% & 71.4% respectively. From this, it can be assessed that company is sharing more of its

earnings with its investor in form of dividend distribution rather than ploughing back into its

business operations. It is considered good from the point of view of investor as it is a good

source of income for them but when it comes to company growth and business expansion it is

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.