Analysis of Motorcycle Holdings Limited Financial Statements - MA611

VerifiedAdded on 2022/08/28

|16

|3282

|24

Report

AI Summary

This report presents a financial analysis of Motorcycle Holdings Limited, focusing on its performance over three financial years. The analysis includes a review of key financial ratios, such as profitability, liquidity, and leverage, to assess the company's financial health. The report identifies potential risks of material misstatement at both the financial report and assertion levels, discussing the implications of director's integrity, experience and pressures, market conditions, and industry trends. It also outlines relevant substantive audit procedures to address these identified risks, particularly focusing on sales, inventory, and cash balances. The report provides insights into the company's operational performance and strategic planning, offering a comprehensive overview of its financial position and potential vulnerabilities. Finally, the report also acknowledges the growth of the motorcycle industry and its potential impact on the company's future performance.

Running head: MOTORCYCLE HOLDINGS LIMITED

MOTORCYCLE HOLDINGS LIMITED

Name of the Student

Name of the University

Author Note

MOTORCYCLE HOLDINGS LIMITED

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MOTORCYCLE HOLDINGS LIMITED

Executive Summary

The report is presented on the Motorcycle Holdings Limited, upon the analysis of the ratio for

the last three financial years, it was observed that the outcome of ratios is positive upon

which the affect can be seen on the financial statement of Motorcycle Holdings Limited. In

every industry there are certain risk factors that affect the growth of any organization and this

cannot be neglected very easily. So, it is important for the higher authority of Motorcycle

Holdings Limited to create a risk management so that they can control all the risks upon

which they are getting affected. The sales, inventory and cash balance of Motorcycle

Holdings Limited is showing as positive affect. In the financial year 2017-18, the outflow

was much more, but in current financial year it has recovered and has resulted positive.

MOTORCYCLE HOLDINGS LIMITED

Executive Summary

The report is presented on the Motorcycle Holdings Limited, upon the analysis of the ratio for

the last three financial years, it was observed that the outcome of ratios is positive upon

which the affect can be seen on the financial statement of Motorcycle Holdings Limited. In

every industry there are certain risk factors that affect the growth of any organization and this

cannot be neglected very easily. So, it is important for the higher authority of Motorcycle

Holdings Limited to create a risk management so that they can control all the risks upon

which they are getting affected. The sales, inventory and cash balance of Motorcycle

Holdings Limited is showing as positive affect. In the financial year 2017-18, the outflow

was much more, but in current financial year it has recovered and has resulted positive.

2

MOTORCYCLE HOLDINGS LIMITED

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................2

Answer to Question 3:................................................................................................................5

References................................................................................................................................10

Appendix..................................................................................................................................12

MOTORCYCLE HOLDINGS LIMITED

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................2

Answer to Question 3:................................................................................................................5

References................................................................................................................................10

Appendix..................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MOTORCYCLE HOLDINGS LIMITED

Answer to Question 1:

Results of Analytical Procedures

As per the financial report of the Motorcycle Holdings Limited, the ratios that has

been calculated are profitability, liquidity, leverage and operating. The liquidity ratios which

includes current and quick ratio has gradually increase over the years, thus it suggests that the

organization has maintained their liquidity (Sari, Nurlaela & Titisari, 2018). In case of

profitability ratio, which includes gross and net profit has decreased in the current year

compared to the previous year.

Under the efficiency ratio, there is average collection period and stock turnover ratio.

It can be observed that in average collection period the collection period should be reduced

for better operation of the organization. The stock turnover ratio in current year is less

compared to last year which is good for the organization (Hermuningsih, 2019). In leverage

ratio, there is debt and debt to equity ratio, which can be observed decreasing over the year

which signifies that the organization has a positive net worth.

From the above discussion, it can be concluded that, there is a positive change in the

ratio of Motorcycle Holdings Limited that means the management is correctly doing the

operations. There is also a positive effect can be seen in the financial statement of Motorcycle

Holdings Limited.

MOTORCYCLE HOLDINGS LIMITED

Answer to Question 1:

Results of Analytical Procedures

As per the financial report of the Motorcycle Holdings Limited, the ratios that has

been calculated are profitability, liquidity, leverage and operating. The liquidity ratios which

includes current and quick ratio has gradually increase over the years, thus it suggests that the

organization has maintained their liquidity (Sari, Nurlaela & Titisari, 2018). In case of

profitability ratio, which includes gross and net profit has decreased in the current year

compared to the previous year.

Under the efficiency ratio, there is average collection period and stock turnover ratio.

It can be observed that in average collection period the collection period should be reduced

for better operation of the organization. The stock turnover ratio in current year is less

compared to last year which is good for the organization (Hermuningsih, 2019). In leverage

ratio, there is debt and debt to equity ratio, which can be observed decreasing over the year

which signifies that the organization has a positive net worth.

From the above discussion, it can be concluded that, there is a positive change in the

ratio of Motorcycle Holdings Limited that means the management is correctly doing the

operations. There is also a positive effect can be seen in the financial statement of Motorcycle

Holdings Limited.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MOTORCYCLE HOLDINGS LIMITED

Answer to Question 2:

Risk of Material Misstatement (Inherent Risk) at the Financial Report Level

Risk management has become a concerning factor in the corporate industry. There

can be some significant misstatement in the financial reports of this company which the

director should take care of. The most important factors that need to be discussed based on

the financial statements are given below

a. Director’s Integrity

Directors play an essential role in an organization’s integrity. The board of directors

also monitors every regulation and organizational policies. There must be loyalty in

production with integrity; hence many people fail to put their purpose and aim in practice.

The board’s main objective to maintain this integrity includes establishing a connection

between the CEO and directors, understanding the requirements from the management. The

board also needs to be very strategic and should always review any financial activities.

Directors cannot commit themselves to regular risk management; however, they can evaluate

the risk management policies and take necessary steps accordingly (deloitte.wsj.com, 2020).

The directors should be aware of each step that the company seeks to lessen the risk from

within the organization. To improve and diminish the risks, the directors should measure and

establish a clear framework and analyse and the risk material, implement any risk policy,

communicate with all of the managers as well as reviewing the qualification of the directors.

b. Director’s experience

From the previous year, the directors have experienced an increase in overall profit

and revenue. The directors also assumed that the organization is not aware of its

MOTORCYCLE HOLDINGS LIMITED

Answer to Question 2:

Risk of Material Misstatement (Inherent Risk) at the Financial Report Level

Risk management has become a concerning factor in the corporate industry. There

can be some significant misstatement in the financial reports of this company which the

director should take care of. The most important factors that need to be discussed based on

the financial statements are given below

a. Director’s Integrity

Directors play an essential role in an organization’s integrity. The board of directors

also monitors every regulation and organizational policies. There must be loyalty in

production with integrity; hence many people fail to put their purpose and aim in practice.

The board’s main objective to maintain this integrity includes establishing a connection

between the CEO and directors, understanding the requirements from the management. The

board also needs to be very strategic and should always review any financial activities.

Directors cannot commit themselves to regular risk management; however, they can evaluate

the risk management policies and take necessary steps accordingly (deloitte.wsj.com, 2020).

The directors should be aware of each step that the company seeks to lessen the risk from

within the organization. To improve and diminish the risks, the directors should measure and

establish a clear framework and analyse and the risk material, implement any risk policy,

communicate with all of the managers as well as reviewing the qualification of the directors.

b. Director’s experience

From the previous year, the directors have experienced an increase in overall profit

and revenue. The directors also assumed that the organization is not aware of its

5

MOTORCYCLE HOLDINGS LIMITED

environmental changes. It has also been found that no person has applied to the court for

leave to bring proceedings on behalf of the firm.

The organization had $9,175,000 in cash at the bank. Hence the directors decided not

to declare the dividend and began a program to reduce the group’s cost structure, debt and

also took advantage of the current trading environment by improving operational

performance. The directors are focusing on sales of used motorcycles by which the

transaction has also increased. From the 2018 report, the sale of the used motorbike was

17,754 units which have been raised to 18,536 units in the year 2019. The market share of the

company has also increased by 11%. The company should also be focused on improving its

position in the market and the directors are strategically planning to execute in the upcoming

years.

c. Pressure on Directors

Despite there was tremendous pressure on the directors in the previous years, the

directors have managed to make an increase in revenue of 9% of $329,887,000 (Motorcycle

Holding Limited, 2020). The Cassons and MCA which was acquired by the directors, helped

the company maintaining profit margin even though there was a miserable condition in the

current market. The board of directors has established an Audit and Risk committee to

monitor, access and control pressures within the firm. The firms have perfect competition in

the market which can pressurize their directors to plan their future projects accordingly. The

return on capital employed in this company is 8% which was 22% three years ago which has

affected the revenue and investment of the firm. The sale of the new motorcycle has

decreased by 1% and should be increased in the following years. The directors should

provide cost-effective and strategic plans to relieve from such pressures. The market of

MOTORCYCLE HOLDINGS LIMITED

environmental changes. It has also been found that no person has applied to the court for

leave to bring proceedings on behalf of the firm.

The organization had $9,175,000 in cash at the bank. Hence the directors decided not

to declare the dividend and began a program to reduce the group’s cost structure, debt and

also took advantage of the current trading environment by improving operational

performance. The directors are focusing on sales of used motorcycles by which the

transaction has also increased. From the 2018 report, the sale of the used motorbike was

17,754 units which have been raised to 18,536 units in the year 2019. The market share of the

company has also increased by 11%. The company should also be focused on improving its

position in the market and the directors are strategically planning to execute in the upcoming

years.

c. Pressure on Directors

Despite there was tremendous pressure on the directors in the previous years, the

directors have managed to make an increase in revenue of 9% of $329,887,000 (Motorcycle

Holding Limited, 2020). The Cassons and MCA which was acquired by the directors, helped

the company maintaining profit margin even though there was a miserable condition in the

current market. The board of directors has established an Audit and Risk committee to

monitor, access and control pressures within the firm. The firms have perfect competition in

the market which can pressurize their directors to plan their future projects accordingly. The

return on capital employed in this company is 8% which was 22% three years ago which has

affected the revenue and investment of the firm. The sale of the new motorcycle has

decreased by 1% and should be increased in the following years. The directors should

provide cost-effective and strategic plans to relieve from such pressures. The market of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MOTORCYCLE HOLDINGS LIMITED

Motorcycle Holding limited in contracting and it can affect the profit margin of the

organization.

d. Motorcycle: A growing industry

The motorcycle industry is growing worldwide over the years and stable growth has

been seen from the past few years (Hashmi & Biesebroeck, 2016). The industry is evolving in

new inventions are upcoming in this industry. The preferences of consumers over electric and

hybrid vehicles have become a trend. It has also been observed that in rural areas, there is an

increase in the use of two-wheelers(Prnewswire.com, 2020). The global market has the

highest revenue in the motorcycle industry. From the financial report of this company, it can

be seen that there is an increase in the percentage of sales of two-wheelers over the past

years. Though there were some competitions in the market, the company performed well in

sales. Globally, U.S has 26% of share in the automobile industry.

e. Concerning factors of the motorcycle industry

Despite being profitable over the past years, there is some major factor which affects

the motorcycle industry the most. One of the most concerning factors in this industry can be

competition amongst the competitive sectors. Also, market share can affect the industry. The

brand name also affects consumer decisions. The economy of the global market can also

affect the organization. Specific changes in laws, interest rates can also be a concern.

Technological factors can affect the industry. Before the internet, there were lower sales

compared to these years.

From the above discussion, it can be concluded that the risk factors that are in the

industry of motorcycle cannot be neglected easily. The risk management of Motorcycle

Holdings Limited can be controlled by a proper risk management. Moreover, there are certain

MOTORCYCLE HOLDINGS LIMITED

Motorcycle Holding limited in contracting and it can affect the profit margin of the

organization.

d. Motorcycle: A growing industry

The motorcycle industry is growing worldwide over the years and stable growth has

been seen from the past few years (Hashmi & Biesebroeck, 2016). The industry is evolving in

new inventions are upcoming in this industry. The preferences of consumers over electric and

hybrid vehicles have become a trend. It has also been observed that in rural areas, there is an

increase in the use of two-wheelers(Prnewswire.com, 2020). The global market has the

highest revenue in the motorcycle industry. From the financial report of this company, it can

be seen that there is an increase in the percentage of sales of two-wheelers over the past

years. Though there were some competitions in the market, the company performed well in

sales. Globally, U.S has 26% of share in the automobile industry.

e. Concerning factors of the motorcycle industry

Despite being profitable over the past years, there is some major factor which affects

the motorcycle industry the most. One of the most concerning factors in this industry can be

competition amongst the competitive sectors. Also, market share can affect the industry. The

brand name also affects consumer decisions. The economy of the global market can also

affect the organization. Specific changes in laws, interest rates can also be a concern.

Technological factors can affect the industry. Before the internet, there were lower sales

compared to these years.

From the above discussion, it can be concluded that the risk factors that are in the

industry of motorcycle cannot be neglected easily. The risk management of Motorcycle

Holdings Limited can be controlled by a proper risk management. Moreover, there are certain

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MOTORCYCLE HOLDINGS LIMITED

misstatements that can be avoided easily with a suitable strategic planning for Motorcycle

Holdings Limited.

MOTORCYCLE HOLDINGS LIMITED

misstatements that can be avoided easily with a suitable strategic planning for Motorcycle

Holdings Limited.

8

MOTORCYCLE HOLDINGS LIMITED

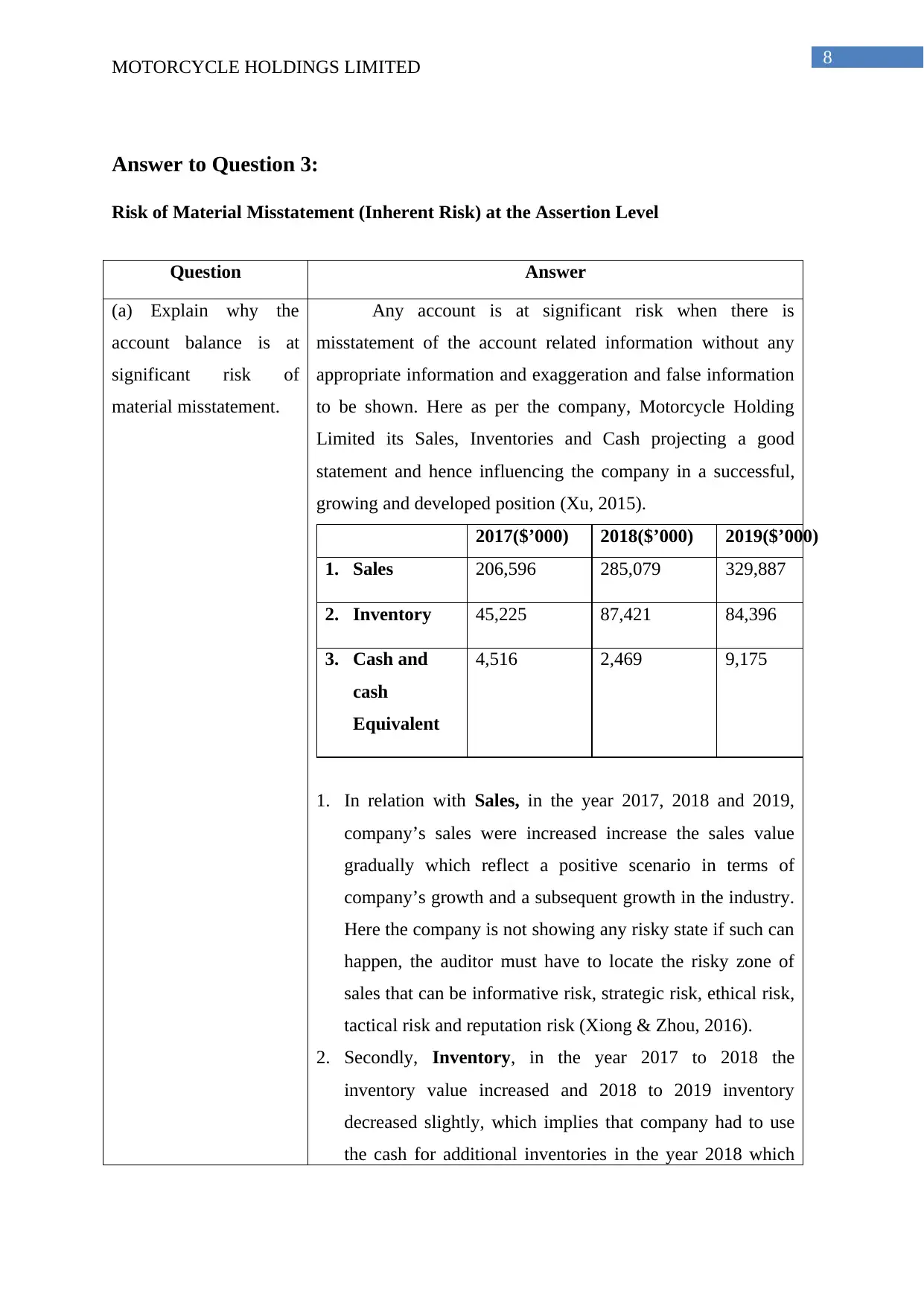

Answer to Question 3:

Risk of Material Misstatement (Inherent Risk) at the Assertion Level

Question Answer

(a) Explain why the

account balance is at

significant risk of

material misstatement.

Any account is at significant risk when there is

misstatement of the account related information without any

appropriate information and exaggeration and false information

to be shown. Here as per the company, Motorcycle Holding

Limited its Sales, Inventories and Cash projecting a good

statement and hence influencing the company in a successful,

growing and developed position (Xu, 2015).

2017($’000) 2018($’000) 2019($’000)

1. Sales 206,596 285,079 329,887

2. Inventory 45,225 87,421 84,396

3. Cash and

cash

Equivalent

4,516 2,469 9,175

1. In relation with Sales, in the year 2017, 2018 and 2019,

company’s sales were increased increase the sales value

gradually which reflect a positive scenario in terms of

company’s growth and a subsequent growth in the industry.

Here the company is not showing any risky state if such can

happen, the auditor must have to locate the risky zone of

sales that can be informative risk, strategic risk, ethical risk,

tactical risk and reputation risk (Xiong & Zhou, 2016).

2. Secondly, Inventory, in the year 2017 to 2018 the

inventory value increased and 2018 to 2019 inventory

decreased slightly, which implies that company had to use

the cash for additional inventories in the year 2018 which

MOTORCYCLE HOLDINGS LIMITED

Answer to Question 3:

Risk of Material Misstatement (Inherent Risk) at the Assertion Level

Question Answer

(a) Explain why the

account balance is at

significant risk of

material misstatement.

Any account is at significant risk when there is

misstatement of the account related information without any

appropriate information and exaggeration and false information

to be shown. Here as per the company, Motorcycle Holding

Limited its Sales, Inventories and Cash projecting a good

statement and hence influencing the company in a successful,

growing and developed position (Xu, 2015).

2017($’000) 2018($’000) 2019($’000)

1. Sales 206,596 285,079 329,887

2. Inventory 45,225 87,421 84,396

3. Cash and

cash

Equivalent

4,516 2,469 9,175

1. In relation with Sales, in the year 2017, 2018 and 2019,

company’s sales were increased increase the sales value

gradually which reflect a positive scenario in terms of

company’s growth and a subsequent growth in the industry.

Here the company is not showing any risky state if such can

happen, the auditor must have to locate the risky zone of

sales that can be informative risk, strategic risk, ethical risk,

tactical risk and reputation risk (Xiong & Zhou, 2016).

2. Secondly, Inventory, in the year 2017 to 2018 the

inventory value increased and 2018 to 2019 inventory

decreased slightly, which implies that company had to use

the cash for additional inventories in the year 2018 which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MOTORCYCLE HOLDINGS LIMITED

leads outflow of cash on this purchase and thus implies a

negative effect on the company’s cash balance. However,

decrease in inventories result in lower cost of goods sold

and the cash balance effect the company and increase the

risk factor in a misstatement.

3. Thirdly, Cash and the cash equivalent, in the year 2017 to

2018, cash amount decreased may be due to additional

purchase however, in 2019 increased a good amount can be

due to sales, overdue collection, expense control and

financial and investing activity in financial statement

resulting improvement in company’s profit and decrease in

cash leads to shortfall in liquidity ratio and increase the

purchasing of the company which again emerges the side of

risk statement.

(b) Explain the key

assertion at risk of not

being valid.

Key assertion at risk of not being valid:

i. In the case of sales, the assertion risk in this account

will be due to manipulation of sales, stocks mostly

overstating the sales amount or it included in a different

account or unclassified account and no documents or

evidence for the same shown. Hence the sales assertion

will not be valid in such circumstances (Xiong & Zhou,

2016).

ii. In the case of inventory, the assertion at risk mostly

when the valuation or any material items get obsolete

and impaired every year and for the merchants, it

appears to be difficult to sell due to special packaging,

branding and promotional changes each year and it

appears to be out dated. However, inventory valuation is

not valid. Another riskiest nature of inventory is

prepayment, in a large industry payment are made in

6month advance when the order for any item placed.

There is a risk of any item shown as purchased from the

supplier not received and items sold that have not been

MOTORCYCLE HOLDINGS LIMITED

leads outflow of cash on this purchase and thus implies a

negative effect on the company’s cash balance. However,

decrease in inventories result in lower cost of goods sold

and the cash balance effect the company and increase the

risk factor in a misstatement.

3. Thirdly, Cash and the cash equivalent, in the year 2017 to

2018, cash amount decreased may be due to additional

purchase however, in 2019 increased a good amount can be

due to sales, overdue collection, expense control and

financial and investing activity in financial statement

resulting improvement in company’s profit and decrease in

cash leads to shortfall in liquidity ratio and increase the

purchasing of the company which again emerges the side of

risk statement.

(b) Explain the key

assertion at risk of not

being valid.

Key assertion at risk of not being valid:

i. In the case of sales, the assertion risk in this account

will be due to manipulation of sales, stocks mostly

overstating the sales amount or it included in a different

account or unclassified account and no documents or

evidence for the same shown. Hence the sales assertion

will not be valid in such circumstances (Xiong & Zhou,

2016).

ii. In the case of inventory, the assertion at risk mostly

when the valuation or any material items get obsolete

and impaired every year and for the merchants, it

appears to be difficult to sell due to special packaging,

branding and promotional changes each year and it

appears to be out dated. However, inventory valuation is

not valid. Another riskiest nature of inventory is

prepayment, in a large industry payment are made in

6month advance when the order for any item placed.

There is a risk of any item shown as purchased from the

supplier not received and items sold that have not been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MOTORCYCLE HOLDINGS LIMITED

removed from the inventory account by the supplier.

Hence prepayment also not valid in this respect.

iii. In respect of cash balance, the assertion can be correct

and fair value, cut off amount, existence, completeness,

presentation and classification. The risk of assertion in

cash occurs when the individual cannot meet the short

term debt obligations and unable to convert asset into

cash. There are different scenarios to assess cash based

on its existence in the financial statement with correct

amount and date. It must be stated correctly in the

account at the end of the year and in the cash flow

statement to if there will be any misstated account and

value in operating, financing and investing activities

then the cash will never able to match the activities and

thus the assertion will not be valid (Xiong & Zhou,

2016).

(c) Detail one (1)

relevant substantive

audit procedure to

address the assertion at

risk as identified in b)

above.

Audit procedures in assertion at risk: Auditor should

work according to its provisions and guidelines. To identify any

assertion in material misstatements, auditor has to obtain all the

necessary and sufficient information from the company’s

financial statement as evidence and to analysis the true and fair

means in company’s accounts. Auditor must have to perform in

guidance with the financial statement (Knechel & Salterio,

2016).

Audit procedure in response to material misstatement

Evaluating the true and fair mean audit evidence

Overall Guidance and facts checking

1. In case of sales: Substantive audit procedure for sales can

be done by verifying the sales and its related documents as

an evidence to relate items, stocks, cash, fixed assets,

revenue, expenses, profit and recorded sales transaction of

the financial statement of the given company (Lessambo,

MOTORCYCLE HOLDINGS LIMITED

removed from the inventory account by the supplier.

Hence prepayment also not valid in this respect.

iii. In respect of cash balance, the assertion can be correct

and fair value, cut off amount, existence, completeness,

presentation and classification. The risk of assertion in

cash occurs when the individual cannot meet the short

term debt obligations and unable to convert asset into

cash. There are different scenarios to assess cash based

on its existence in the financial statement with correct

amount and date. It must be stated correctly in the

account at the end of the year and in the cash flow

statement to if there will be any misstated account and

value in operating, financing and investing activities

then the cash will never able to match the activities and

thus the assertion will not be valid (Xiong & Zhou,

2016).

(c) Detail one (1)

relevant substantive

audit procedure to

address the assertion at

risk as identified in b)

above.

Audit procedures in assertion at risk: Auditor should

work according to its provisions and guidelines. To identify any

assertion in material misstatements, auditor has to obtain all the

necessary and sufficient information from the company’s

financial statement as evidence and to analysis the true and fair

means in company’s accounts. Auditor must have to perform in

guidance with the financial statement (Knechel & Salterio,

2016).

Audit procedure in response to material misstatement

Evaluating the true and fair mean audit evidence

Overall Guidance and facts checking

1. In case of sales: Substantive audit procedure for sales can

be done by verifying the sales and its related documents as

an evidence to relate items, stocks, cash, fixed assets,

revenue, expenses, profit and recorded sales transaction of

the financial statement of the given company (Lessambo,

11

MOTORCYCLE HOLDINGS LIMITED

2018).

2. In case of inventory: Substantive audit procedure in

inventory verifies in two methods:

Analytical procedure:

i. Comparing the gross margin with the last year.

ii. Comparing inventory turnover ratio with the last year.

iii. Comparing the unit cost of inventory with the last year.

Test of detail balance: The auditor has to observe the

inventory count.

3. In the case of cash: Substantive audit procedure in cash is

to verifying cash and confirming cash balance. Checking

the reconciled bank statement of the respective month and

bank account which include general ledge and check the

deposits and expense on the account (Akter, 2014).

(d) Detail one (1)

relevant practical

internal control that

would mitigate the risk

in relation to the

assertion at risk as

identified in b) above

For sales: one internal control measures for sales return is to

identify the specific individual and not to process returns until

the approval by the designated person. However, as per the

company there was no sales return occurred so the journal entry

will be:

Sales A/c…. Debit (x)

to Accounts Receivable/cash A/c…...Credit (x)

For Sales account:

Accounts Receivable/cash A/c… Debit ()

To sales A/c…. Credit ()

Hence if the company had sales return, then it should be

deducted from sales or revenue to generate net sales. the journal

entry will be:

Sales return A/c …. Debit (x)

To Account receivables/ cash A/c…. Credit (x)

For inventories: one internal control measures for inventories

to identify and rectify the errors, misstatement and to prevent

from losses. Industry using inventory must verify and tag them

to identify as correct and not damaged. All the failed and

MOTORCYCLE HOLDINGS LIMITED

2018).

2. In case of inventory: Substantive audit procedure in

inventory verifies in two methods:

Analytical procedure:

i. Comparing the gross margin with the last year.

ii. Comparing inventory turnover ratio with the last year.

iii. Comparing the unit cost of inventory with the last year.

Test of detail balance: The auditor has to observe the

inventory count.

3. In the case of cash: Substantive audit procedure in cash is

to verifying cash and confirming cash balance. Checking

the reconciled bank statement of the respective month and

bank account which include general ledge and check the

deposits and expense on the account (Akter, 2014).

(d) Detail one (1)

relevant practical

internal control that

would mitigate the risk

in relation to the

assertion at risk as

identified in b) above

For sales: one internal control measures for sales return is to

identify the specific individual and not to process returns until

the approval by the designated person. However, as per the

company there was no sales return occurred so the journal entry

will be:

Sales A/c…. Debit (x)

to Accounts Receivable/cash A/c…...Credit (x)

For Sales account:

Accounts Receivable/cash A/c… Debit ()

To sales A/c…. Credit ()

Hence if the company had sales return, then it should be

deducted from sales or revenue to generate net sales. the journal

entry will be:

Sales return A/c …. Debit (x)

To Account receivables/ cash A/c…. Credit (x)

For inventories: one internal control measures for inventories

to identify and rectify the errors, misstatement and to prevent

from losses. Industry using inventory must verify and tag them

to identify as correct and not damaged. All the failed and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.