Financial Analysis and Ratio Calculations: Military Might Limited

VerifiedAdded on 2023/06/09

|17

|3834

|356

Report

AI Summary

This report presents a comprehensive financial analysis of Military Might Limited, a UK-based company selling outdoor equipment. It begins with the preparation of the company's financial statements, including the Income Statement and Statement of Financial Position for the year ended 31 December 2021. The report then delves into a detailed analysis of financial ratios, including profitability, liquidity, efficiency, and lending ratios, over a four-year period from 2018 to 2021. These ratios are calculated and interpreted to assess the company's performance, identify trends, and evaluate its financial health. The analysis covers key areas such as profit margins, return on investment, current and acid-test ratios, inventory turnover, accounts receivable turnover, and return on assets and equity. The report also includes a discussion of budgetary control and its behavioural aspects. The findings provide insights into the company's strengths and weaknesses, along with recommendations for improvement, focusing on aspects like declining profit margins, efficient asset utilization, and effective collection processes.

Financial and Data

Analysis

Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Task 1:..........................................................................................................................................3

Task 2: Calculation of Financial Ratios for Military Might Limited:..........................................5

.......................................................................................................................................................14

Task 3:........................................................................................................................................15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Task 1:..........................................................................................................................................3

Task 2: Calculation of Financial Ratios for Military Might Limited:..........................................5

.......................................................................................................................................................14

Task 3:........................................................................................................................................15

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

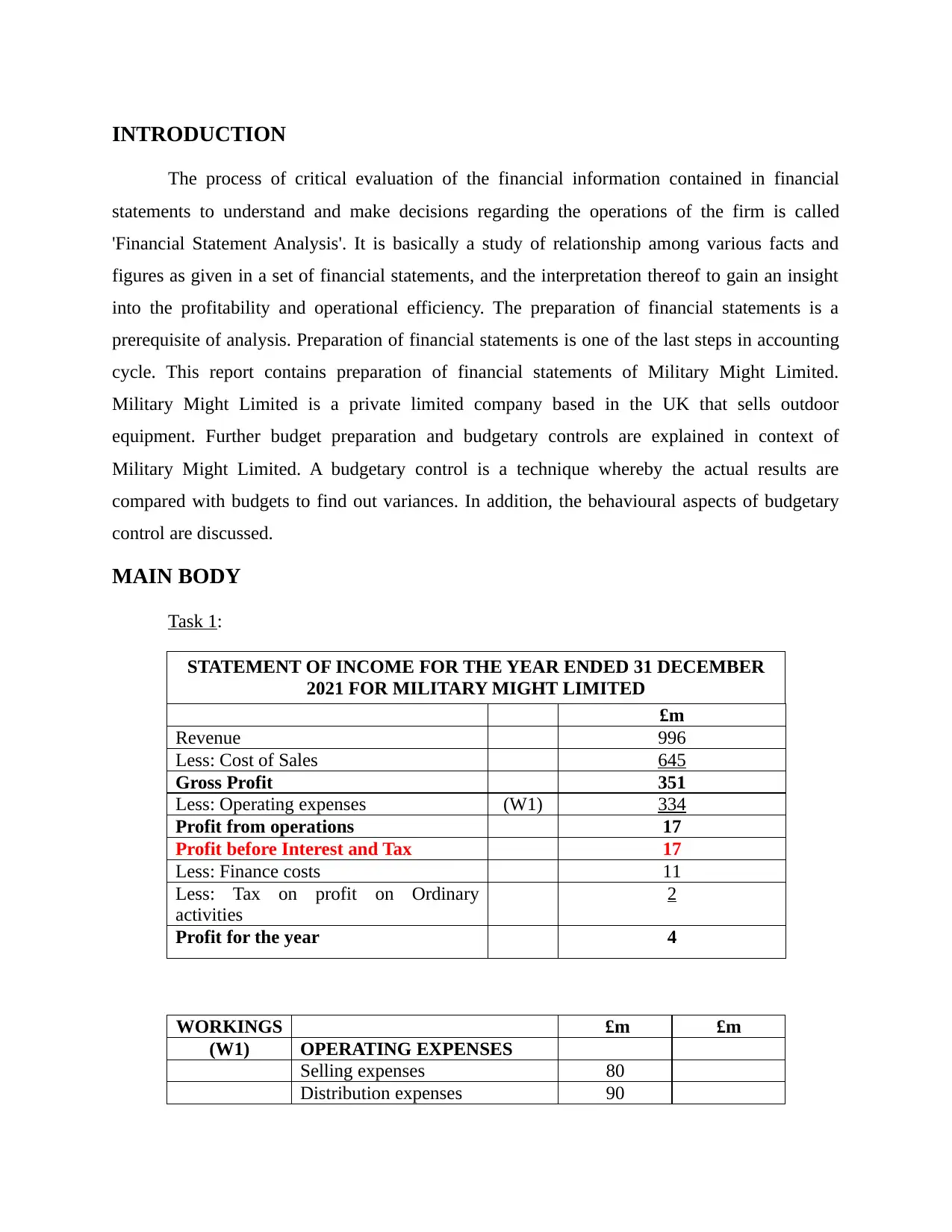

INTRODUCTION

The process of critical evaluation of the financial information contained in financial

statements to understand and make decisions regarding the operations of the firm is called

'Financial Statement Analysis'. It is basically a study of relationship among various facts and

figures as given in a set of financial statements, and the interpretation thereof to gain an insight

into the profitability and operational efficiency. The preparation of financial statements is a

prerequisite of analysis. Preparation of financial statements is one of the last steps in accounting

cycle. This report contains preparation of financial statements of Military Might Limited.

Military Might Limited is a private limited company based in the UK that sells outdoor

equipment. Further budget preparation and budgetary controls are explained in context of

Military Might Limited. A budgetary control is a technique whereby the actual results are

compared with budgets to find out variances. In addition, the behavioural aspects of budgetary

control are discussed.

MAIN BODY

Task 1:

STATEMENT OF INCOME FOR THE YEAR ENDED 31 DECEMBER

2021 FOR MILITARY MIGHT LIMITED

£m

Revenue 996

Less: Cost of Sales 645

Gross Profit 351

Less: Operating expenses (W1) 334

Profit from operations 17

Profit before Interest and Tax 17

Less: Finance costs 11

Less: Tax on profit on Ordinary

activities

2

Profit for the year 4

WORKINGS £m £m

(W1) OPERATING EXPENSES

Selling expenses 80

Distribution expenses 90

The process of critical evaluation of the financial information contained in financial

statements to understand and make decisions regarding the operations of the firm is called

'Financial Statement Analysis'. It is basically a study of relationship among various facts and

figures as given in a set of financial statements, and the interpretation thereof to gain an insight

into the profitability and operational efficiency. The preparation of financial statements is a

prerequisite of analysis. Preparation of financial statements is one of the last steps in accounting

cycle. This report contains preparation of financial statements of Military Might Limited.

Military Might Limited is a private limited company based in the UK that sells outdoor

equipment. Further budget preparation and budgetary controls are explained in context of

Military Might Limited. A budgetary control is a technique whereby the actual results are

compared with budgets to find out variances. In addition, the behavioural aspects of budgetary

control are discussed.

MAIN BODY

Task 1:

STATEMENT OF INCOME FOR THE YEAR ENDED 31 DECEMBER

2021 FOR MILITARY MIGHT LIMITED

£m

Revenue 996

Less: Cost of Sales 645

Gross Profit 351

Less: Operating expenses (W1) 334

Profit from operations 17

Profit before Interest and Tax 17

Less: Finance costs 11

Less: Tax on profit on Ordinary

activities

2

Profit for the year 4

WORKINGS £m £m

(W1) OPERATING EXPENSES

Selling expenses 80

Distribution expenses 90

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Other administration expenses 164

Total 334

STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 2021

FOR MILITARY MIGHT LIMITED

£ £

Non-current assets

Property, Plant & Machinery (W2) 524

Long-term investments 24

Total 548

Current assets

Inventory 200

Trade Receivables 185

Cash at Bank 10

395

Current liabilities

Trade Payables 70

Taxation payable 2

72

Net Current Assets (Current Assets – Current

Liabilities)

323

Non-current liabilities

Bank Loans 370

370

Equity and Liabilities

Share Capital 32

Retained Earnings 469

501

Equity and total liabilities 943

WORKINGS £m £m

Total 334

STATEMENT OF FINANCIAL POSITION AS AT 31 DECEMBER 2021

FOR MILITARY MIGHT LIMITED

£ £

Non-current assets

Property, Plant & Machinery (W2) 524

Long-term investments 24

Total 548

Current assets

Inventory 200

Trade Receivables 185

Cash at Bank 10

395

Current liabilities

Trade Payables 70

Taxation payable 2

72

Net Current Assets (Current Assets – Current

Liabilities)

323

Non-current liabilities

Bank Loans 370

370

Equity and Liabilities

Share Capital 32

Retained Earnings 469

501

Equity and total liabilities 943

WORKINGS £m £m

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

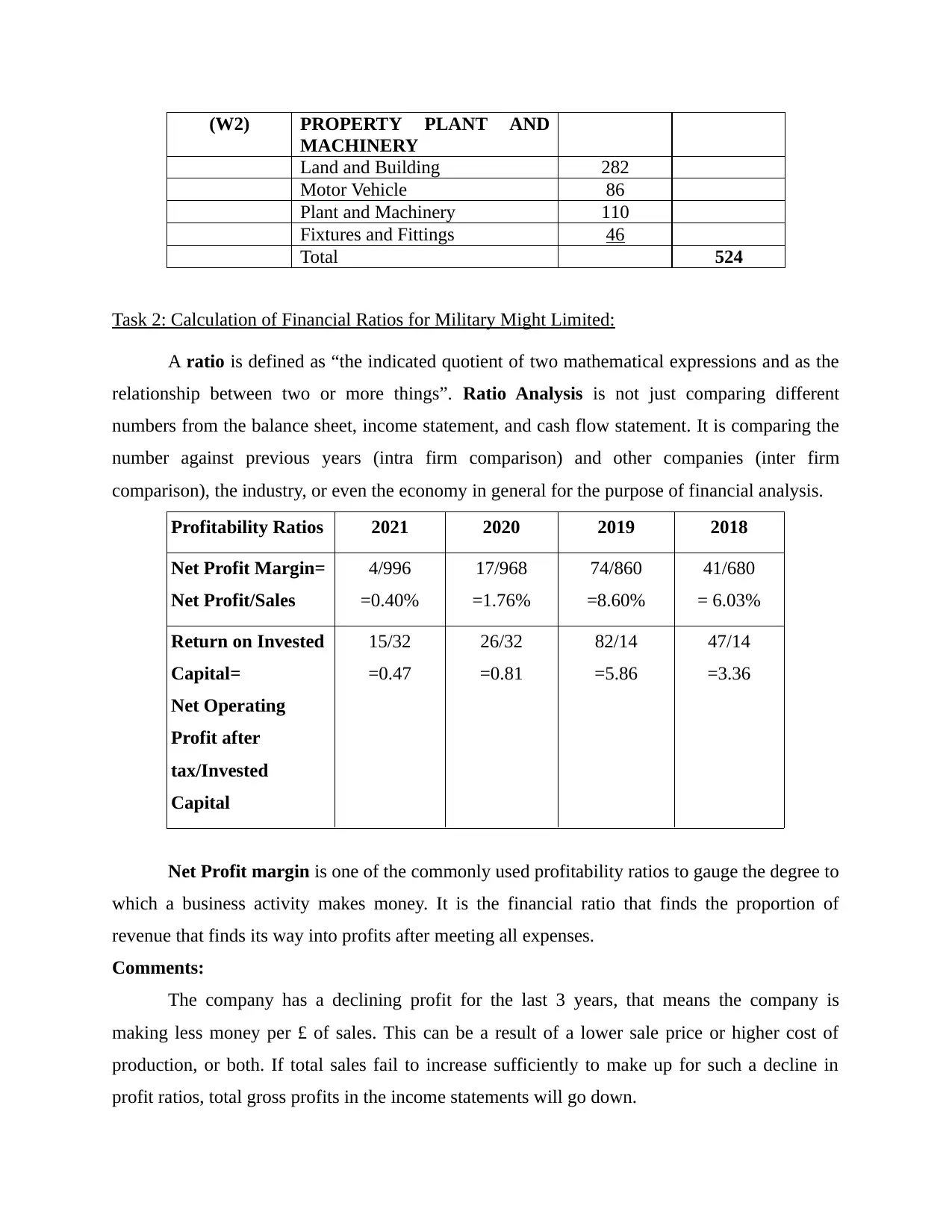

(W2) PROPERTY PLANT AND

MACHINERY

Land and Building 282

Motor Vehicle 86

Plant and Machinery 110

Fixtures and Fittings 46

Total 524

Task 2: Calculation of Financial Ratios for Military Might Limited:

A ratio is defined as “the indicated quotient of two mathematical expressions and as the

relationship between two or more things”. Ratio Analysis is not just comparing different

numbers from the balance sheet, income statement, and cash flow statement. It is comparing the

number against previous years (intra firm comparison) and other companies (inter firm

comparison), the industry, or even the economy in general for the purpose of financial analysis.

Profitability Ratios 2021 2020 2019 2018

Net Profit Margin=

Net Profit/Sales

4/996

=0.40%

17/968

=1.76%

74/860

=8.60%

41/680

= 6.03%

Return on Invested

Capital=

Net Operating

Profit after

tax/Invested

Capital

15/32

=0.47

26/32

=0.81

82/14

=5.86

47/14

=3.36

Net Profit margin is one of the commonly used profitability ratios to gauge the degree to

which a business activity makes money. It is the financial ratio that finds the proportion of

revenue that finds its way into profits after meeting all expenses.

Comments:

The company has a declining profit for the last 3 years, that means the company is

making less money per £ of sales. This can be a result of a lower sale price or higher cost of

production, or both. If total sales fail to increase sufficiently to make up for such a decline in

profit ratios, total gross profits in the income statements will go down.

MACHINERY

Land and Building 282

Motor Vehicle 86

Plant and Machinery 110

Fixtures and Fittings 46

Total 524

Task 2: Calculation of Financial Ratios for Military Might Limited:

A ratio is defined as “the indicated quotient of two mathematical expressions and as the

relationship between two or more things”. Ratio Analysis is not just comparing different

numbers from the balance sheet, income statement, and cash flow statement. It is comparing the

number against previous years (intra firm comparison) and other companies (inter firm

comparison), the industry, or even the economy in general for the purpose of financial analysis.

Profitability Ratios 2021 2020 2019 2018

Net Profit Margin=

Net Profit/Sales

4/996

=0.40%

17/968

=1.76%

74/860

=8.60%

41/680

= 6.03%

Return on Invested

Capital=

Net Operating

Profit after

tax/Invested

Capital

15/32

=0.47

26/32

=0.81

82/14

=5.86

47/14

=3.36

Net Profit margin is one of the commonly used profitability ratios to gauge the degree to

which a business activity makes money. It is the financial ratio that finds the proportion of

revenue that finds its way into profits after meeting all expenses.

Comments:

The company has a declining profit for the last 3 years, that means the company is

making less money per £ of sales. This can be a result of a lower sale price or higher cost of

production, or both. If total sales fail to increase sufficiently to make up for such a decline in

profit ratios, total gross profits in the income statements will go down.

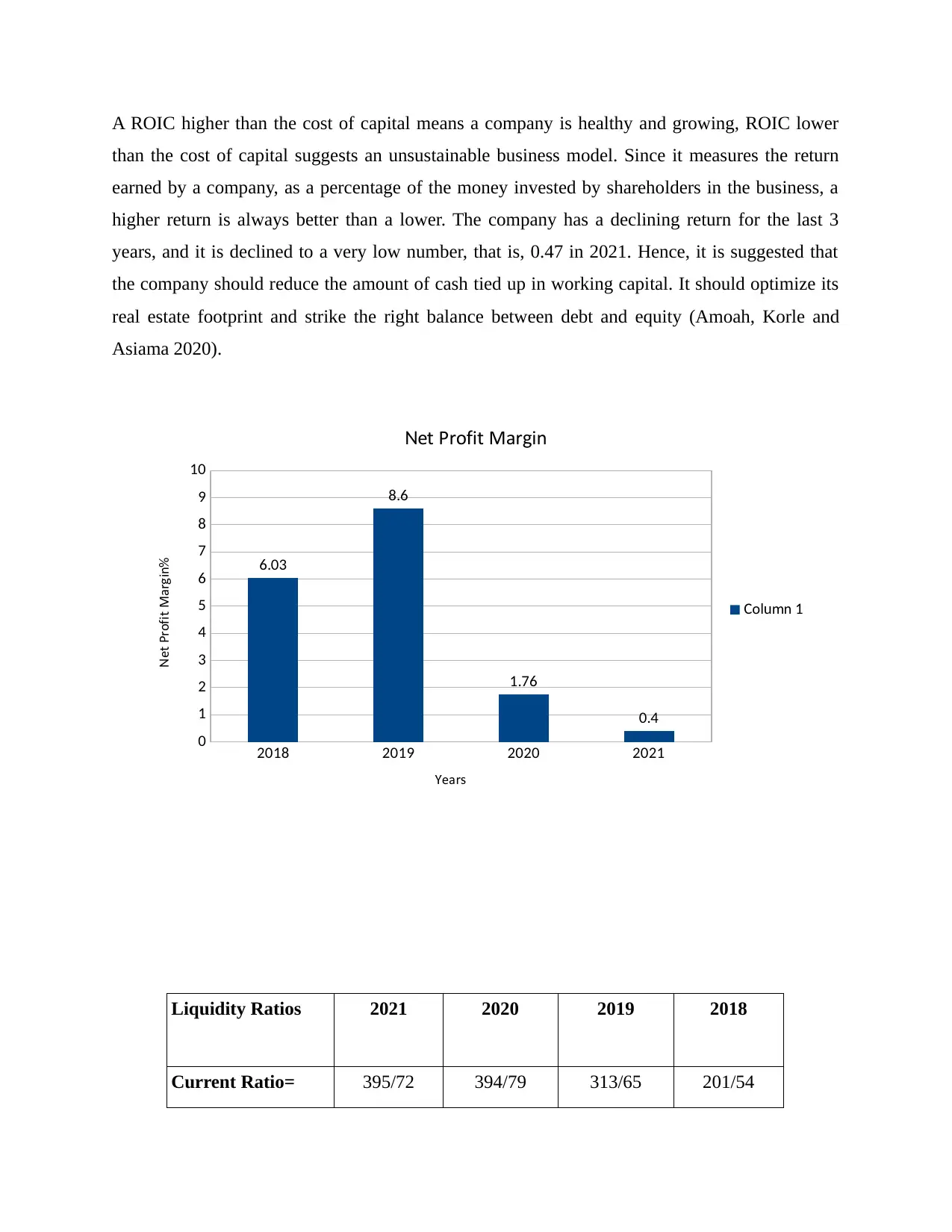

A ROIC higher than the cost of capital means a company is healthy and growing, ROIC lower

than the cost of capital suggests an unsustainable business model. Since it measures the return

earned by a company, as a percentage of the money invested by shareholders in the business, a

higher return is always better than a lower. The company has a declining return for the last 3

years, and it is declined to a very low number, that is, 0.47 in 2021. Hence, it is suggested that

the company should reduce the amount of cash tied up in working capital. It should optimize its

real estate footprint and strike the right balance between debt and equity (Amoah, Korle and

Asiama 2020).

Liquidity Ratios 2021 2020 2019 2018

Current Ratio= 395/72 394/79 313/65 201/54

2018 2019 2020 2021

0

1

2

3

4

5

6

7

8

9

10

6.03

8.6

1.76

0.4

et Pro it Mar inN f g

ol mnC u 1

earY s

et Pro it Mar inN f g %

than the cost of capital suggests an unsustainable business model. Since it measures the return

earned by a company, as a percentage of the money invested by shareholders in the business, a

higher return is always better than a lower. The company has a declining return for the last 3

years, and it is declined to a very low number, that is, 0.47 in 2021. Hence, it is suggested that

the company should reduce the amount of cash tied up in working capital. It should optimize its

real estate footprint and strike the right balance between debt and equity (Amoah, Korle and

Asiama 2020).

Liquidity Ratios 2021 2020 2019 2018

Current Ratio= 395/72 394/79 313/65 201/54

2018 2019 2020 2021

0

1

2

3

4

5

6

7

8

9

10

6.03

8.6

1.76

0.4

et Pro it Mar inN f g

ol mnC u 1

earY s

et Pro it Mar inN f g %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current

Assets/Current

Liabilities

=5.49 =4.99 =4.82 =3.72

Acid Test Ratio=

Current Assets less

Inventory/Current

Liabilities

(395-200)/72

=2.71

(394-190)/79

=2.58

(313-147)/65

=2.55

(201-78)/54

=2.28

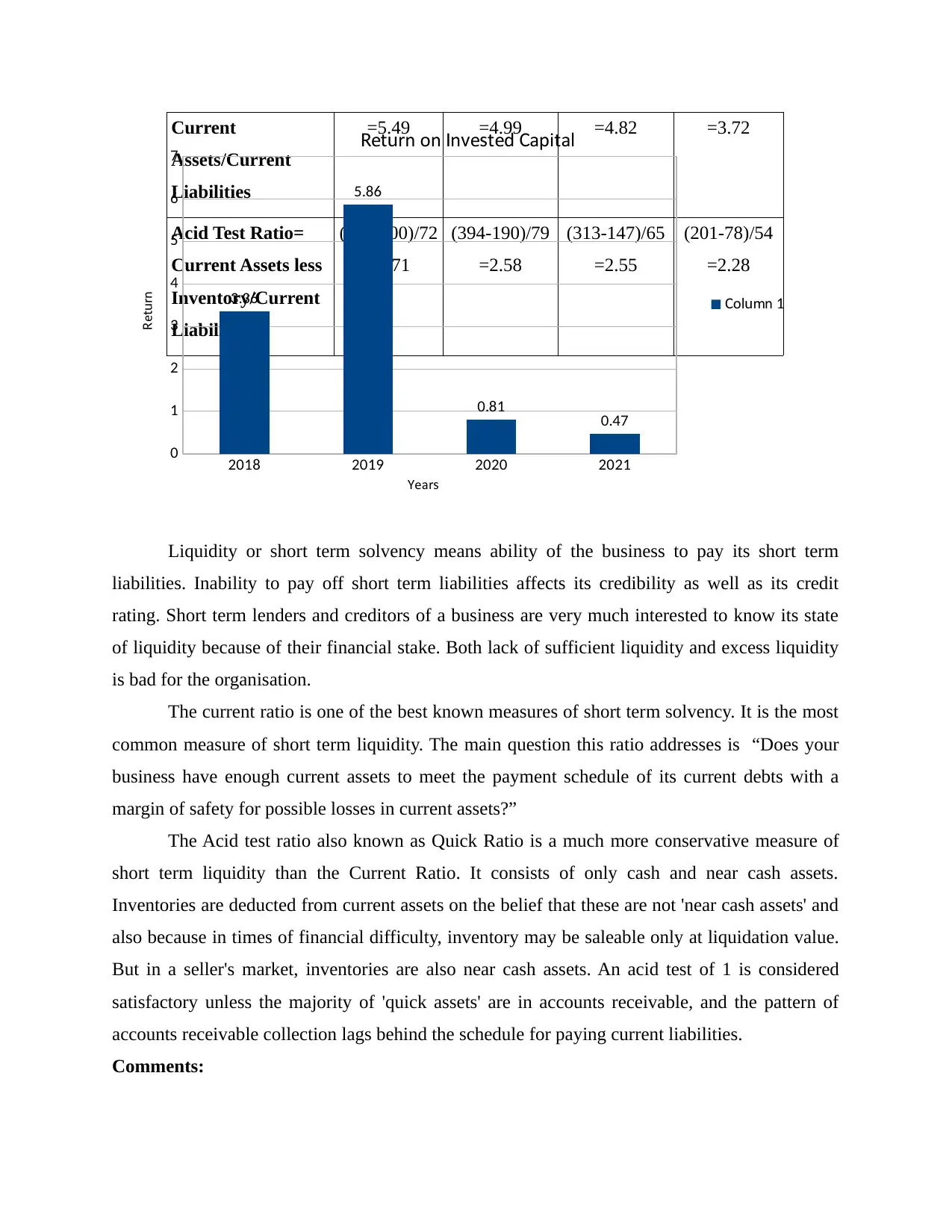

Liquidity or short term solvency means ability of the business to pay its short term

liabilities. Inability to pay off short term liabilities affects its credibility as well as its credit

rating. Short term lenders and creditors of a business are very much interested to know its state

of liquidity because of their financial stake. Both lack of sufficient liquidity and excess liquidity

is bad for the organisation.

The current ratio is one of the best known measures of short term solvency. It is the most

common measure of short term liquidity. The main question this ratio addresses is “Does your

business have enough current assets to meet the payment schedule of its current debts with a

margin of safety for possible losses in current assets?”

The Acid test ratio also known as Quick Ratio is a much more conservative measure of

short term liquidity than the Current Ratio. It consists of only cash and near cash assets.

Inventories are deducted from current assets on the belief that these are not 'near cash assets' and

also because in times of financial difficulty, inventory may be saleable only at liquidation value.

But in a seller's market, inventories are also near cash assets. An acid test of 1 is considered

satisfactory unless the majority of 'quick assets' are in accounts receivable, and the pattern of

accounts receivable collection lags behind the schedule for paying current liabilities.

Comments:

2018 2019 2020 2021

0

1

2

3

4

5

6

7

3.36

5.86

0.81 0.47

et rn on n e ted apitalR u I v s C

ol mnC u 1

earY s

et rnR u

Assets/Current

Liabilities

=5.49 =4.99 =4.82 =3.72

Acid Test Ratio=

Current Assets less

Inventory/Current

Liabilities

(395-200)/72

=2.71

(394-190)/79

=2.58

(313-147)/65

=2.55

(201-78)/54

=2.28

Liquidity or short term solvency means ability of the business to pay its short term

liabilities. Inability to pay off short term liabilities affects its credibility as well as its credit

rating. Short term lenders and creditors of a business are very much interested to know its state

of liquidity because of their financial stake. Both lack of sufficient liquidity and excess liquidity

is bad for the organisation.

The current ratio is one of the best known measures of short term solvency. It is the most

common measure of short term liquidity. The main question this ratio addresses is “Does your

business have enough current assets to meet the payment schedule of its current debts with a

margin of safety for possible losses in current assets?”

The Acid test ratio also known as Quick Ratio is a much more conservative measure of

short term liquidity than the Current Ratio. It consists of only cash and near cash assets.

Inventories are deducted from current assets on the belief that these are not 'near cash assets' and

also because in times of financial difficulty, inventory may be saleable only at liquidation value.

But in a seller's market, inventories are also near cash assets. An acid test of 1 is considered

satisfactory unless the majority of 'quick assets' are in accounts receivable, and the pattern of

accounts receivable collection lags behind the schedule for paying current liabilities.

Comments:

2018 2019 2020 2021

0

1

2

3

4

5

6

7

3.36

5.86

0.81 0.47

et rn on n e ted apitalR u I v s C

ol mnC u 1

earY s

et rnR u

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

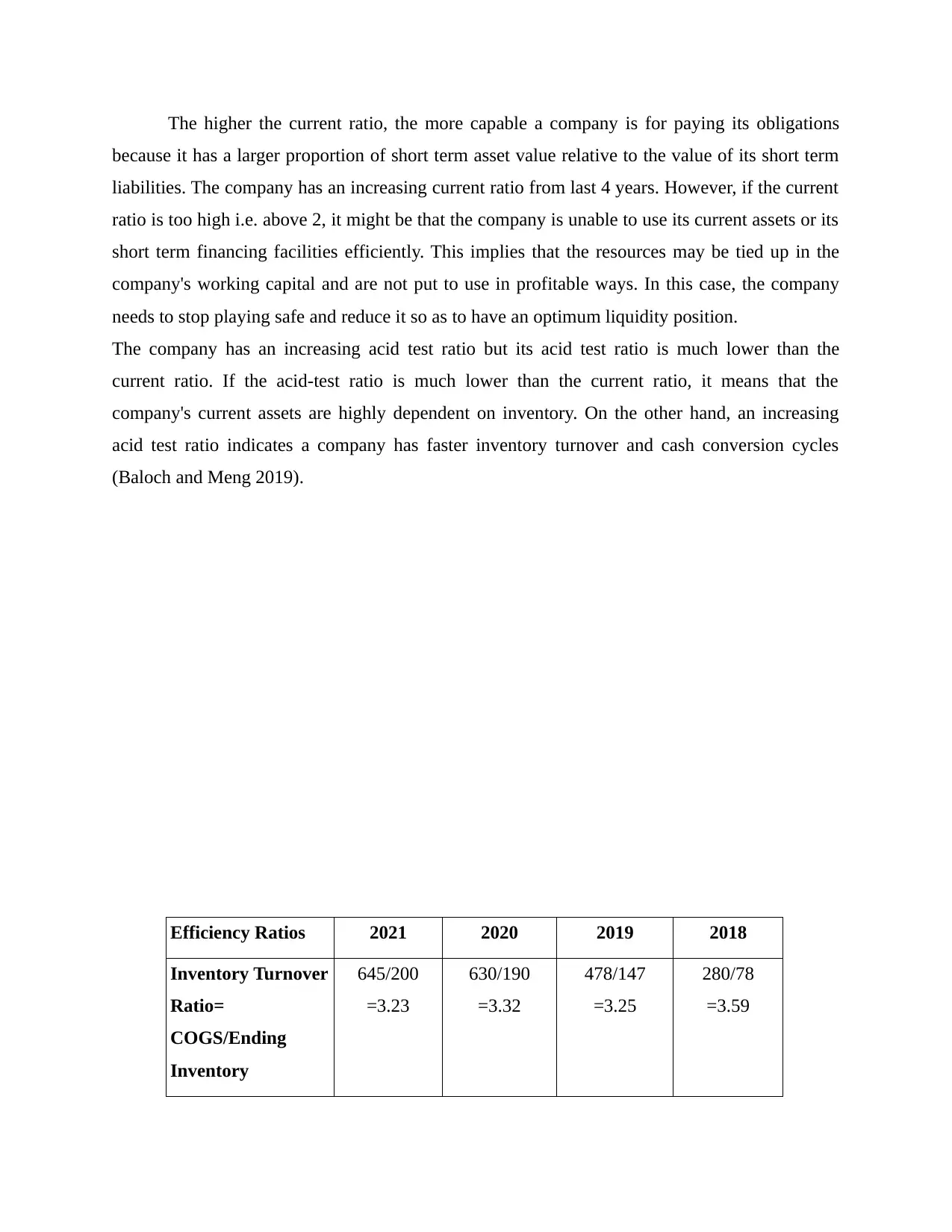

The higher the current ratio, the more capable a company is for paying its obligations

because it has a larger proportion of short term asset value relative to the value of its short term

liabilities. The company has an increasing current ratio from last 4 years. However, if the current

ratio is too high i.e. above 2, it might be that the company is unable to use its current assets or its

short term financing facilities efficiently. This implies that the resources may be tied up in the

company's working capital and are not put to use in profitable ways. In this case, the company

needs to stop playing safe and reduce it so as to have an optimum liquidity position.

The company has an increasing acid test ratio but its acid test ratio is much lower than the

current ratio. If the acid-test ratio is much lower than the current ratio, it means that the

company's current assets are highly dependent on inventory. On the other hand, an increasing

acid test ratio indicates a company has faster inventory turnover and cash conversion cycles

(Baloch and Meng 2019).

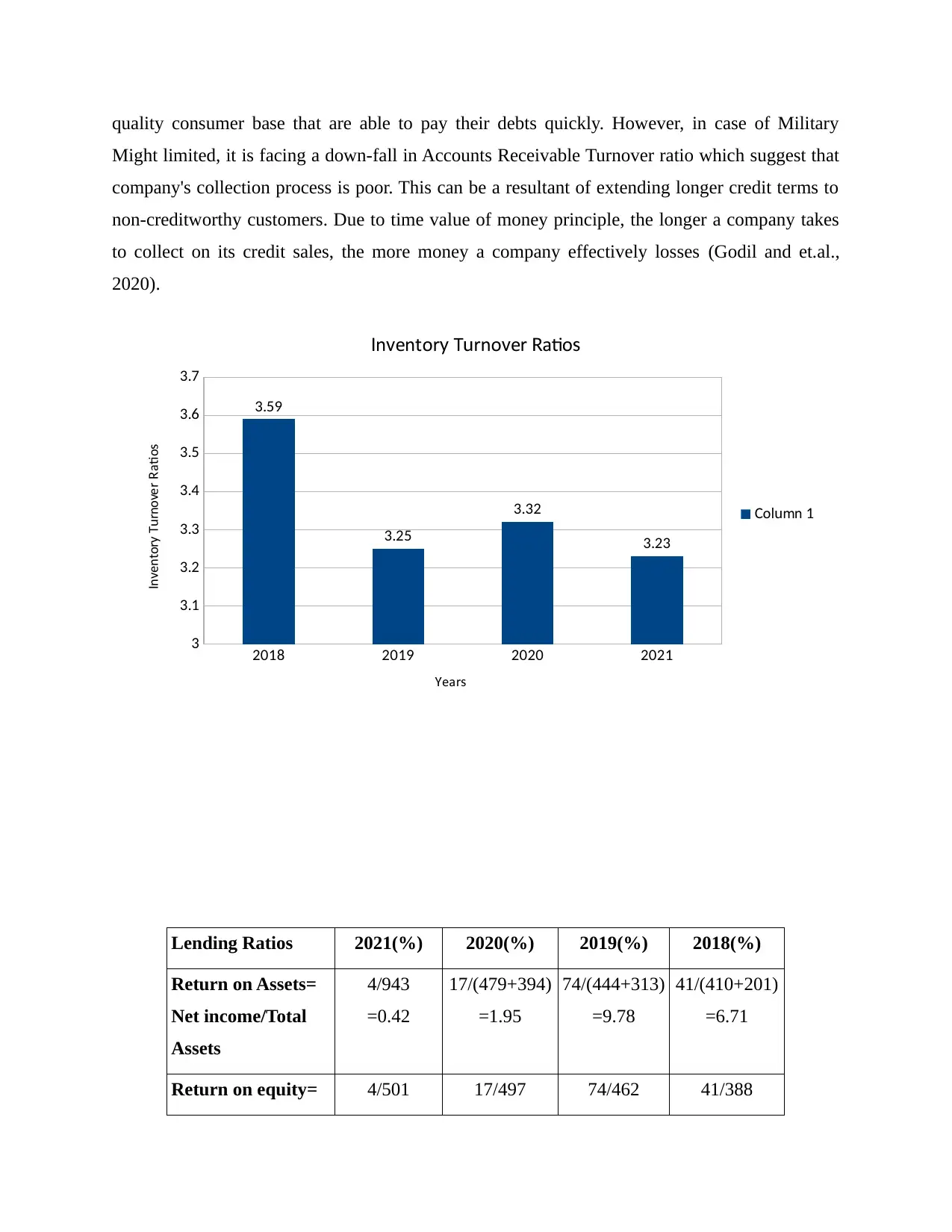

Efficiency Ratios 2021 2020 2019 2018

Inventory Turnover

Ratio=

COGS/Ending

Inventory

645/200

=3.23

630/190

=3.32

478/147

=3.25

280/78

=3.59

because it has a larger proportion of short term asset value relative to the value of its short term

liabilities. The company has an increasing current ratio from last 4 years. However, if the current

ratio is too high i.e. above 2, it might be that the company is unable to use its current assets or its

short term financing facilities efficiently. This implies that the resources may be tied up in the

company's working capital and are not put to use in profitable ways. In this case, the company

needs to stop playing safe and reduce it so as to have an optimum liquidity position.

The company has an increasing acid test ratio but its acid test ratio is much lower than the

current ratio. If the acid-test ratio is much lower than the current ratio, it means that the

company's current assets are highly dependent on inventory. On the other hand, an increasing

acid test ratio indicates a company has faster inventory turnover and cash conversion cycles

(Baloch and Meng 2019).

Efficiency Ratios 2021 2020 2019 2018

Inventory Turnover

Ratio=

COGS/Ending

Inventory

645/200

=3.23

630/190

=3.32

478/147

=3.25

280/78

=3.59

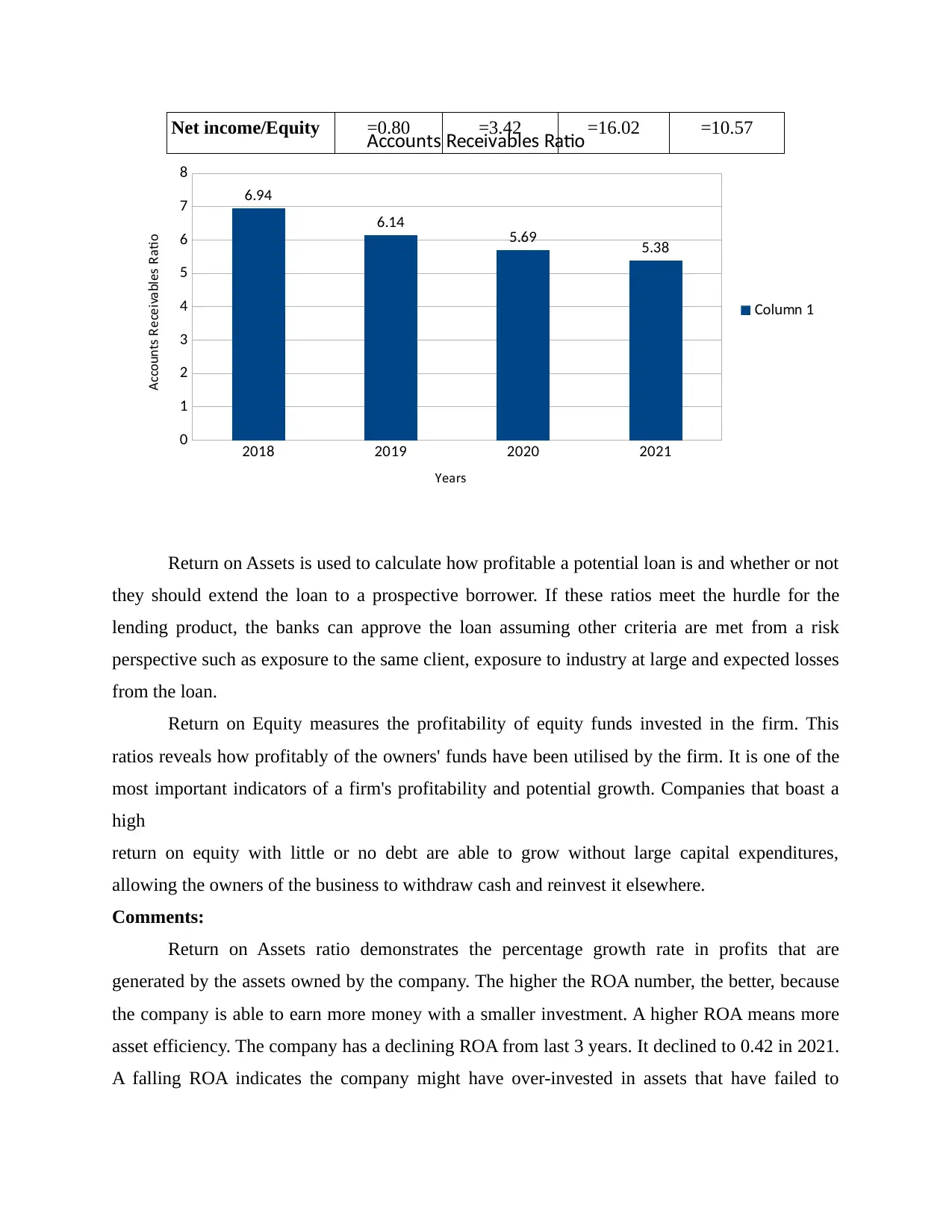

Accounts

Receivable

Turnover

Ratio=Net Credit

Sales/ Accounts

Receivables

996/185

=5.38

968/170

=5.69

860/140

=6.14

680/98

=6.94

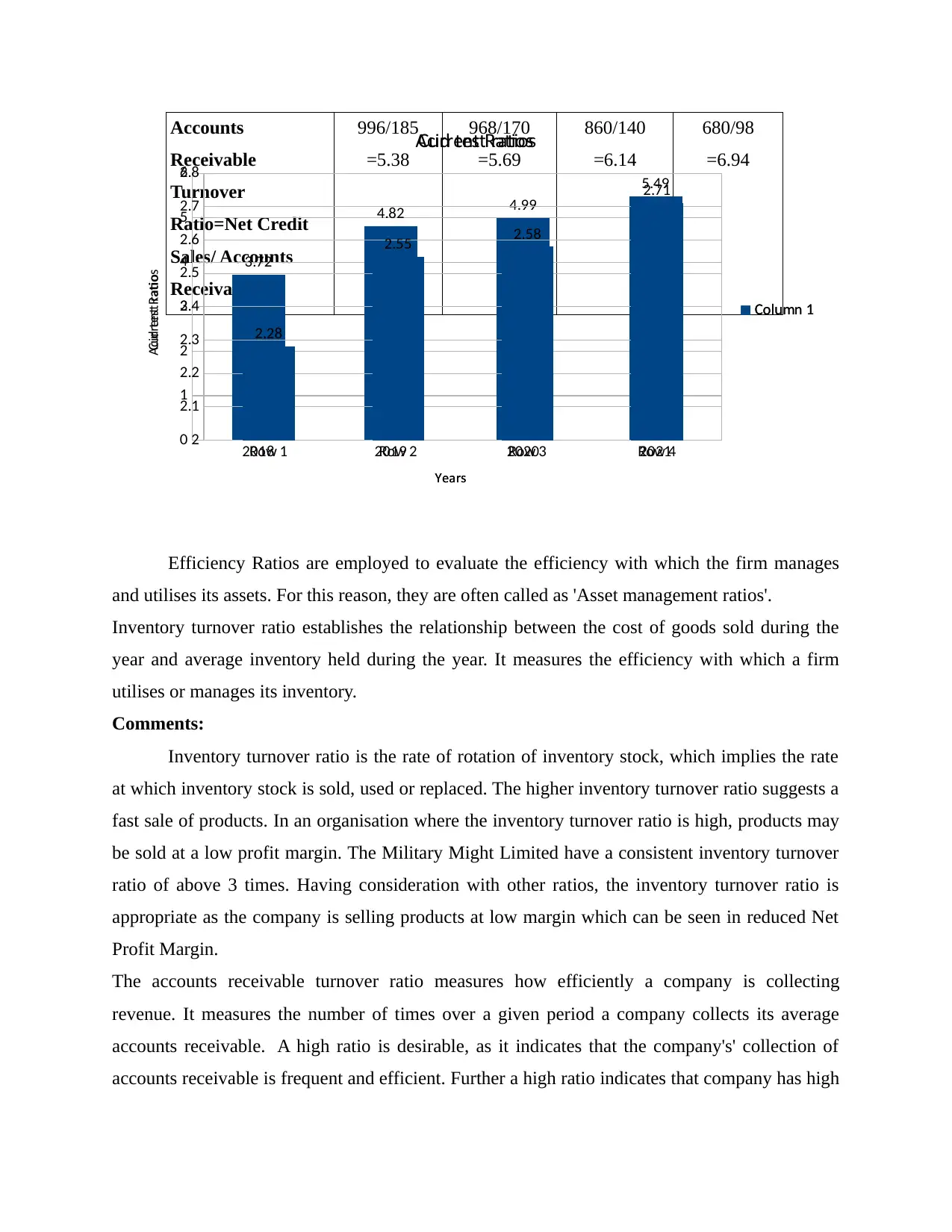

Efficiency Ratios are employed to evaluate the efficiency with which the firm manages

and utilises its assets. For this reason, they are often called as 'Asset management ratios'.

Inventory turnover ratio establishes the relationship between the cost of goods sold during the

year and average inventory held during the year. It measures the efficiency with which a firm

utilises or manages its inventory.

Comments:

Inventory turnover ratio is the rate of rotation of inventory stock, which implies the rate

at which inventory stock is sold, used or replaced. The higher inventory turnover ratio suggests a

fast sale of products. In an organisation where the inventory turnover ratio is high, products may

be sold at a low profit margin. The Military Might Limited have a consistent inventory turnover

ratio of above 3 times. Having consideration with other ratios, the inventory turnover ratio is

appropriate as the company is selling products at low margin which can be seen in reduced Net

Profit Margin.

The accounts receivable turnover ratio measures how efficiently a company is collecting

revenue. It measures the number of times over a given period a company collects its average

accounts receivable. A high ratio is desirable, as it indicates that the company's' collection of

accounts receivable is frequent and efficient. Further a high ratio indicates that company has high

2018 2019 2020 2021

0

1

2

3

4

5

6

3.72

4.82 4.99

5.49

rrent atioCu R s

ol mnC u 1

earY s

rrent atioCu R

oR w 1 oR w 2 oR w 3 oR w 4

2

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.28

2.55 2.58

2.71

Acid te t ratios s

ol mnC u 1

earY s

Acid te t ratios s

Receivable

Turnover

Ratio=Net Credit

Sales/ Accounts

Receivables

996/185

=5.38

968/170

=5.69

860/140

=6.14

680/98

=6.94

Efficiency Ratios are employed to evaluate the efficiency with which the firm manages

and utilises its assets. For this reason, they are often called as 'Asset management ratios'.

Inventory turnover ratio establishes the relationship between the cost of goods sold during the

year and average inventory held during the year. It measures the efficiency with which a firm

utilises or manages its inventory.

Comments:

Inventory turnover ratio is the rate of rotation of inventory stock, which implies the rate

at which inventory stock is sold, used or replaced. The higher inventory turnover ratio suggests a

fast sale of products. In an organisation where the inventory turnover ratio is high, products may

be sold at a low profit margin. The Military Might Limited have a consistent inventory turnover

ratio of above 3 times. Having consideration with other ratios, the inventory turnover ratio is

appropriate as the company is selling products at low margin which can be seen in reduced Net

Profit Margin.

The accounts receivable turnover ratio measures how efficiently a company is collecting

revenue. It measures the number of times over a given period a company collects its average

accounts receivable. A high ratio is desirable, as it indicates that the company's' collection of

accounts receivable is frequent and efficient. Further a high ratio indicates that company has high

2018 2019 2020 2021

0

1

2

3

4

5

6

3.72

4.82 4.99

5.49

rrent atioCu R s

ol mnC u 1

earY s

rrent atioCu R

oR w 1 oR w 2 oR w 3 oR w 4

2

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.28

2.55 2.58

2.71

Acid te t ratios s

ol mnC u 1

earY s

Acid te t ratios s

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

quality consumer base that are able to pay their debts quickly. However, in case of Military

Might limited, it is facing a down-fall in Accounts Receivable Turnover ratio which suggest that

company's collection process is poor. This can be a resultant of extending longer credit terms to

non-creditworthy customers. Due to time value of money principle, the longer a company takes

to collect on its credit sales, the more money a company effectively losses (Godil and et.al.,

2020).

Lending Ratios 2021(%) 2020(%) 2019(%) 2018(%)

Return on Assets=

Net income/Total

Assets

4/943

=0.42

17/(479+394)

=1.95

74/(444+313)

=9.78

41/(410+201)

=6.71

Return on equity= 4/501 17/497 74/462 41/388

2018 2019 2020 2021

3

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.59

3.25

3.32

3.23

n entor T rno er atioI v y u v R s

ol mnC u 1

earY s

n entor T rno er atioI v y u v R s

Might limited, it is facing a down-fall in Accounts Receivable Turnover ratio which suggest that

company's collection process is poor. This can be a resultant of extending longer credit terms to

non-creditworthy customers. Due to time value of money principle, the longer a company takes

to collect on its credit sales, the more money a company effectively losses (Godil and et.al.,

2020).

Lending Ratios 2021(%) 2020(%) 2019(%) 2018(%)

Return on Assets=

Net income/Total

Assets

4/943

=0.42

17/(479+394)

=1.95

74/(444+313)

=9.78

41/(410+201)

=6.71

Return on equity= 4/501 17/497 74/462 41/388

2018 2019 2020 2021

3

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.59

3.25

3.32

3.23

n entor T rno er atioI v y u v R s

ol mnC u 1

earY s

n entor T rno er atioI v y u v R s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net income/Equity =0.80 =3.42 =16.02 =10.57

Return on Assets is used to calculate how profitable a potential loan is and whether or not

they should extend the loan to a prospective borrower. If these ratios meet the hurdle for the

lending product, the banks can approve the loan assuming other criteria are met from a risk

perspective such as exposure to the same client, exposure to industry at large and expected losses

from the loan.

Return on Equity measures the profitability of equity funds invested in the firm. This

ratios reveals how profitably of the owners' funds have been utilised by the firm. It is one of the

most important indicators of a firm's profitability and potential growth. Companies that boast a

high

return on equity with little or no debt are able to grow without large capital expenditures,

allowing the owners of the business to withdraw cash and reinvest it elsewhere.

Comments:

Return on Assets ratio demonstrates the percentage growth rate in profits that are

generated by the assets owned by the company. The higher the ROA number, the better, because

the company is able to earn more money with a smaller investment. A higher ROA means more

asset efficiency. The company has a declining ROA from last 3 years. It declined to 0.42 in 2021.

A falling ROA indicates the company might have over-invested in assets that have failed to

2018 2019 2020 2021

0

1

2

3

4

5

6

7

8

6.94

6.14 5.69 5.38

Acco nt ecei a le atiou s R v b s R

ol mnC u 1

earY s

Acco nt ecei a le atiou s R v b s R

Return on Assets is used to calculate how profitable a potential loan is and whether or not

they should extend the loan to a prospective borrower. If these ratios meet the hurdle for the

lending product, the banks can approve the loan assuming other criteria are met from a risk

perspective such as exposure to the same client, exposure to industry at large and expected losses

from the loan.

Return on Equity measures the profitability of equity funds invested in the firm. This

ratios reveals how profitably of the owners' funds have been utilised by the firm. It is one of the

most important indicators of a firm's profitability and potential growth. Companies that boast a

high

return on equity with little or no debt are able to grow without large capital expenditures,

allowing the owners of the business to withdraw cash and reinvest it elsewhere.

Comments:

Return on Assets ratio demonstrates the percentage growth rate in profits that are

generated by the assets owned by the company. The higher the ROA number, the better, because

the company is able to earn more money with a smaller investment. A higher ROA means more

asset efficiency. The company has a declining ROA from last 3 years. It declined to 0.42 in 2021.

A falling ROA indicates the company might have over-invested in assets that have failed to

2018 2019 2020 2021

0

1

2

3

4

5

6

7

8

6.94

6.14 5.69 5.38

Acco nt ecei a le atiou s R v b s R

ol mnC u 1

earY s

Acco nt ecei a le atiou s R v b s R

produce revenue growth, a sign the company may be trouble. The company should take the

necessary steps to improve the efficiency of its current and fixed assets.

The higher a company's ROE, the better. A higher percentage indicates the company is more

effective at generating profit from its existing assets. A company that sees increases in its ROE

over time is likely getting more efficient. Military Might Limited has a declining ROE from last

3 years. Declining ROE suggests the company is becoming less efficient at creating profits and

increasing shareholder value. The company can finance themselves with debt and equity capital.

By increasing the amount of debt capital relative to its equity capital, company can increase its

ROE (Ibrahim and et.al., 2020).

2018 2019 2020 2021

0

2

4

6

8

10

12

6.71

9.78

1.95

0.42

et rn on A etR u ss s

ol mnC u 1

earY s

et rn on A etR u ss s

necessary steps to improve the efficiency of its current and fixed assets.

The higher a company's ROE, the better. A higher percentage indicates the company is more

effective at generating profit from its existing assets. A company that sees increases in its ROE

over time is likely getting more efficient. Military Might Limited has a declining ROE from last

3 years. Declining ROE suggests the company is becoming less efficient at creating profits and

increasing shareholder value. The company can finance themselves with debt and equity capital.

By increasing the amount of debt capital relative to its equity capital, company can increase its

ROE (Ibrahim and et.al., 2020).

2018 2019 2020 2021

0

2

4

6

8

10

12

6.71

9.78

1.95

0.42

et rn on A etR u ss s

ol mnC u 1

earY s

et rn on A etR u ss s

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.