Financial Analysis Report: Morrisons PLC & Tesco PLC - 2017

VerifiedAdded on 2021/04/16

|9

|1990

|21

Report

AI Summary

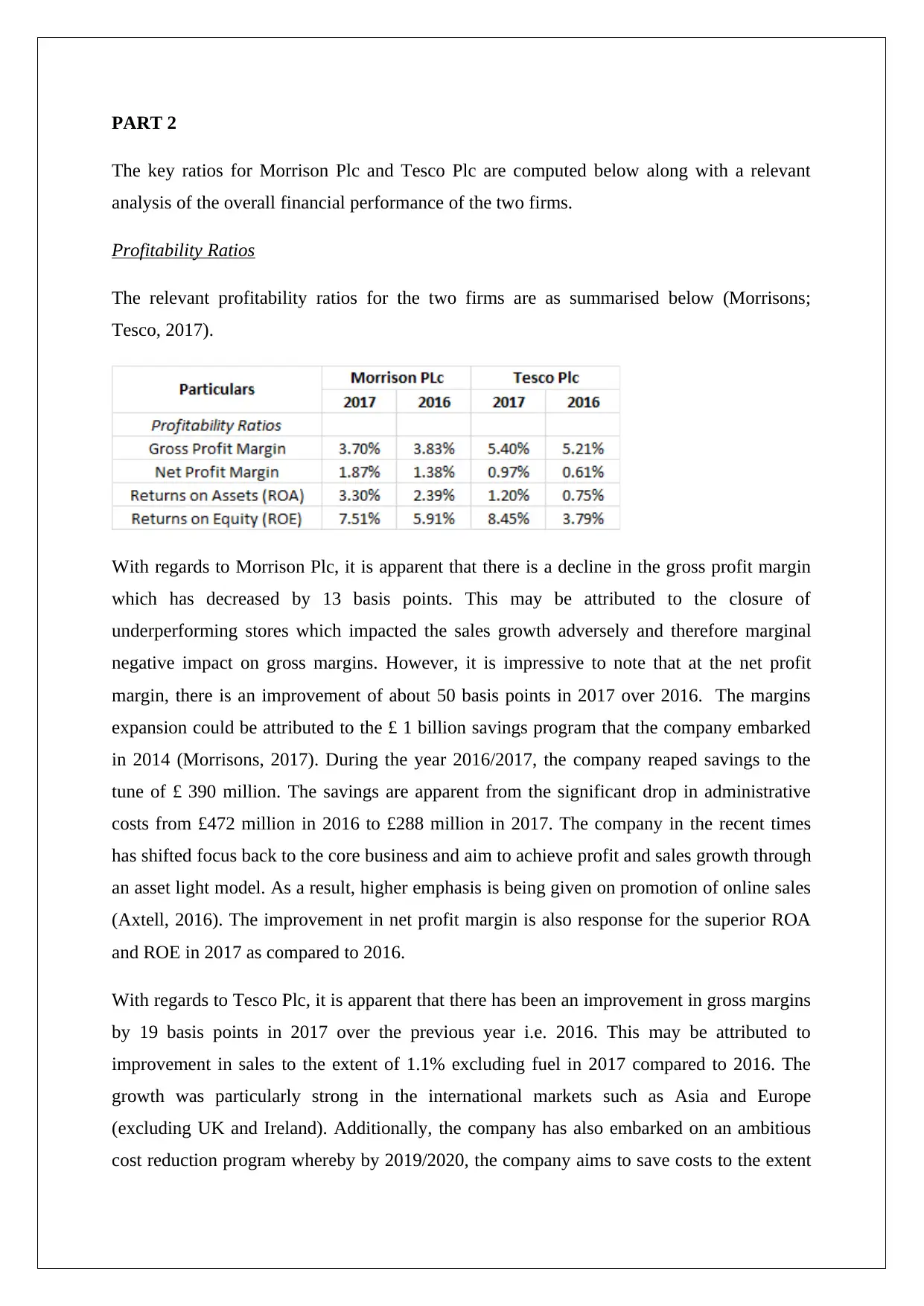

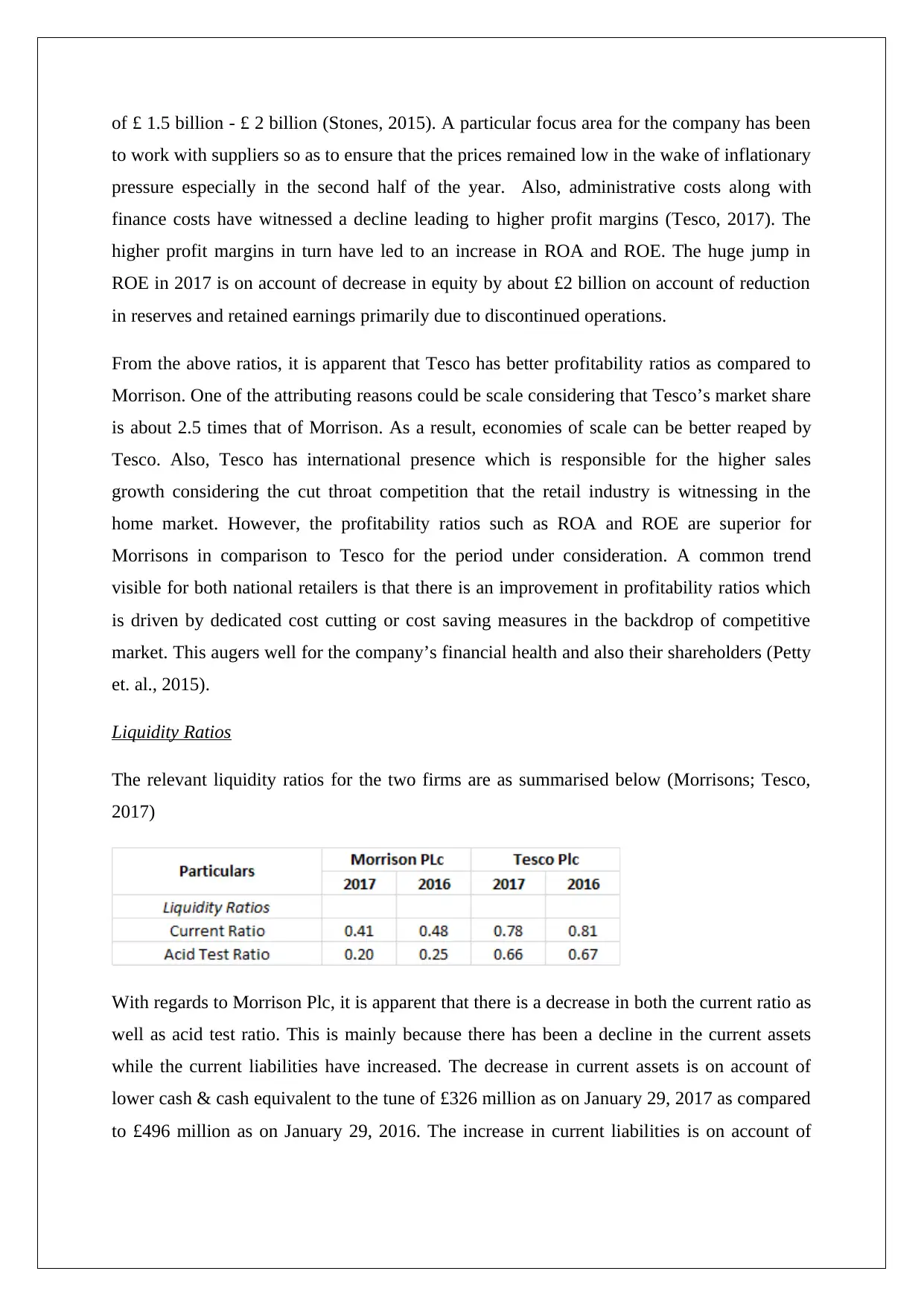

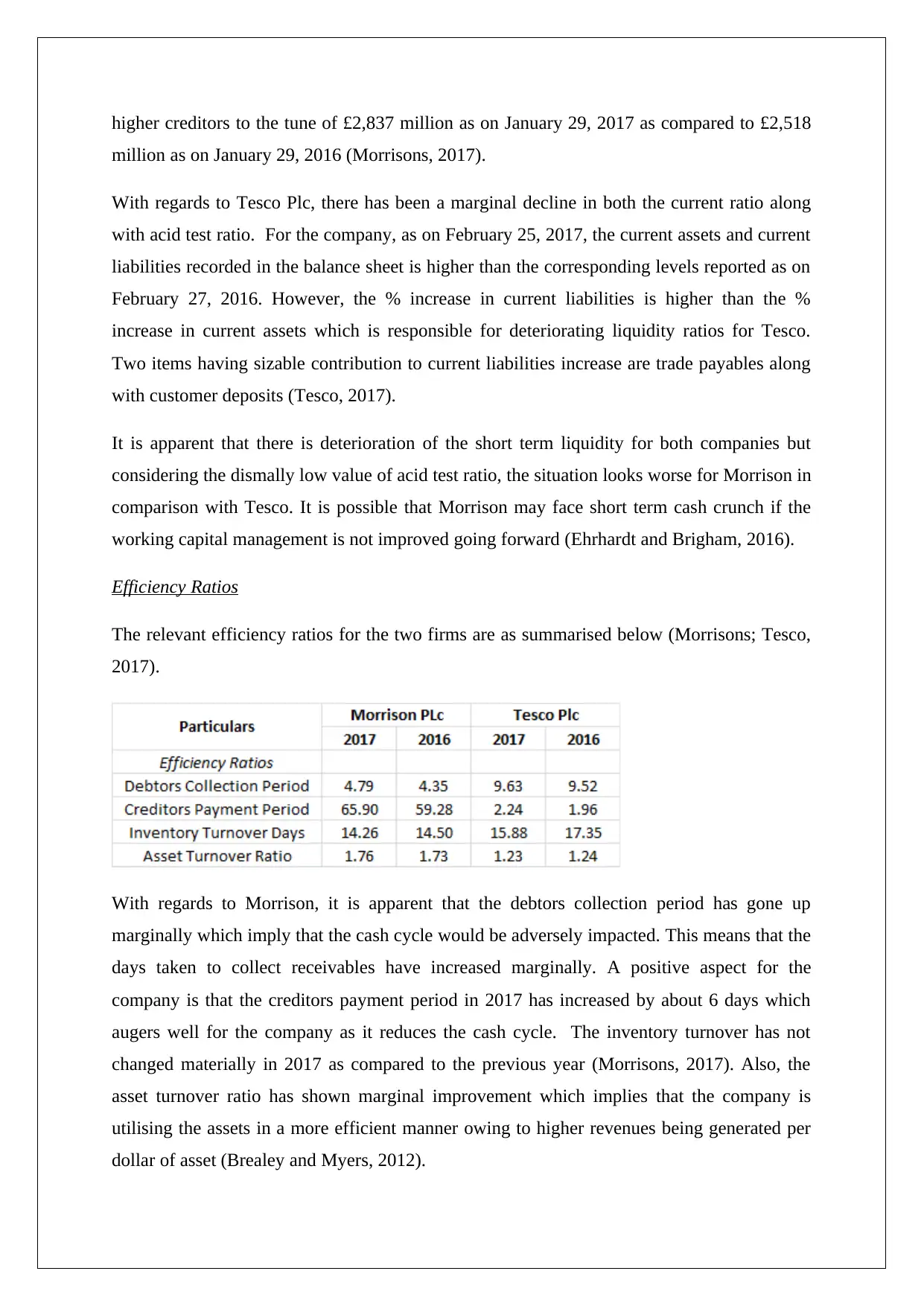

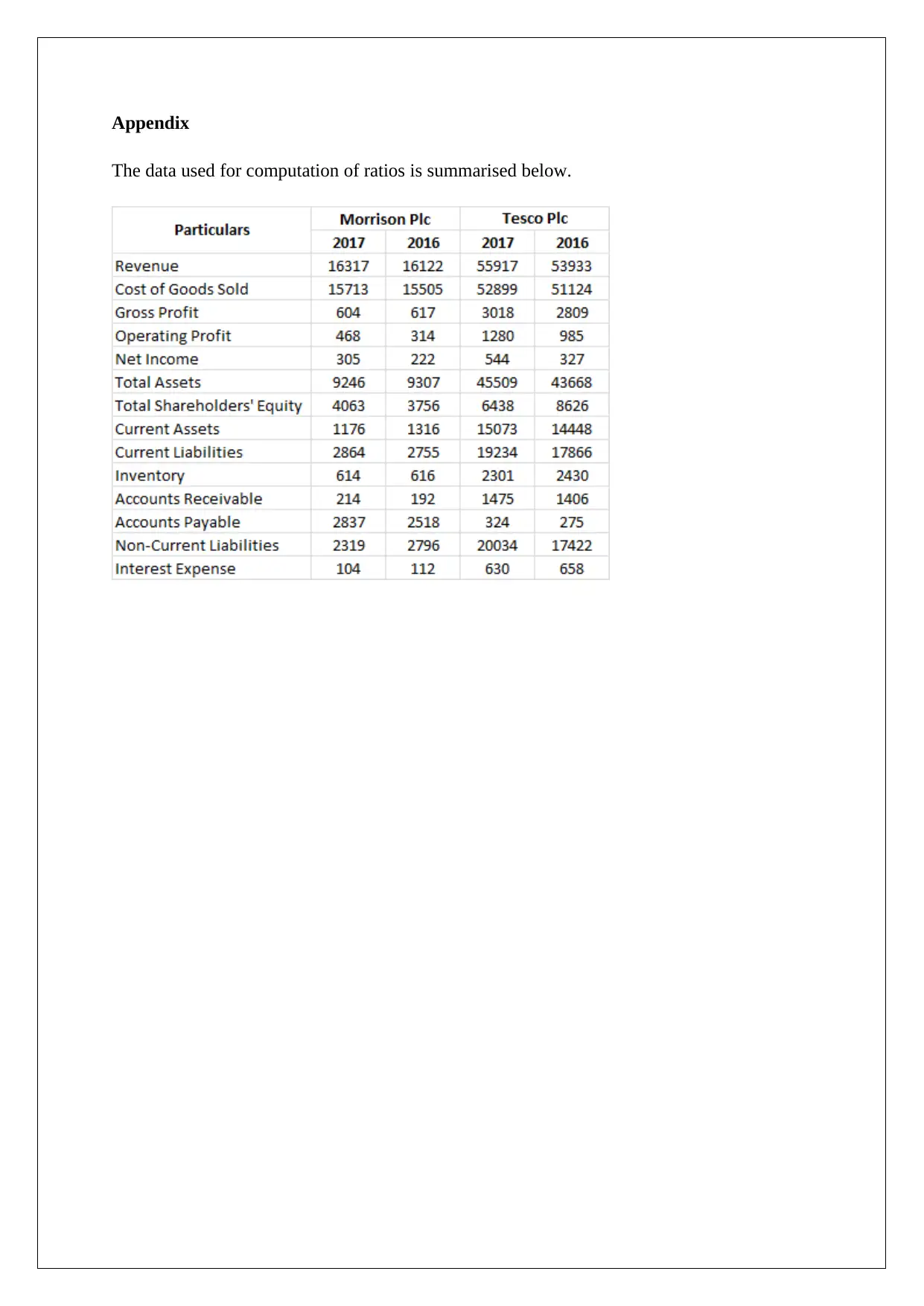

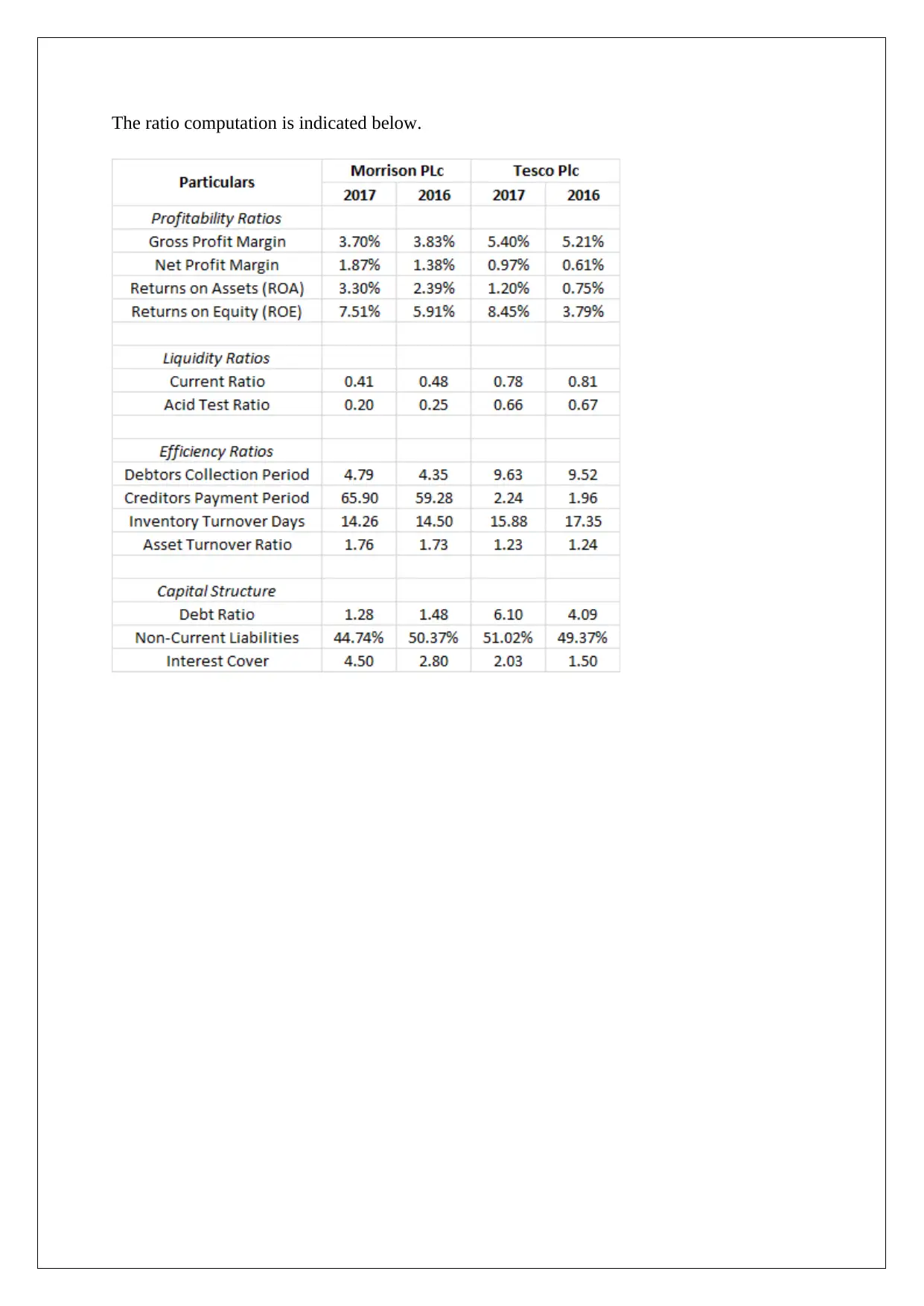

This report presents a comprehensive financial analysis of Morrisons PLC and Tesco PLC, focusing on their performance in 2017. The analysis encompasses key financial ratios, including profitability (gross profit margin, net profit margin, ROA, ROE), liquidity (current ratio, acid test ratio), efficiency (debtors collection period, inventory turnover, creditors payment period, asset turnover), and capital structure (debt ratio, interest cover). The report compares the two companies, highlighting their strengths and weaknesses based on the computed ratios and trends. It notes that Tesco generally demonstrates better profitability ratios, while Morrisons exhibits superior ROA and ROE. Both companies are seen to be improving profitability through cost-cutting measures. The analysis also reveals that both companies have reduced their debt levels and improved interest coverage, with Morrisons showing greater deleveraging. The report utilizes data from the companies' annual reports and provides relevant references to support the analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.