Bangor University ASB 4007: Financial Analysis of Mothercare Limited

VerifiedAdded on 2022/08/12

|14

|2398

|15

Report

AI Summary

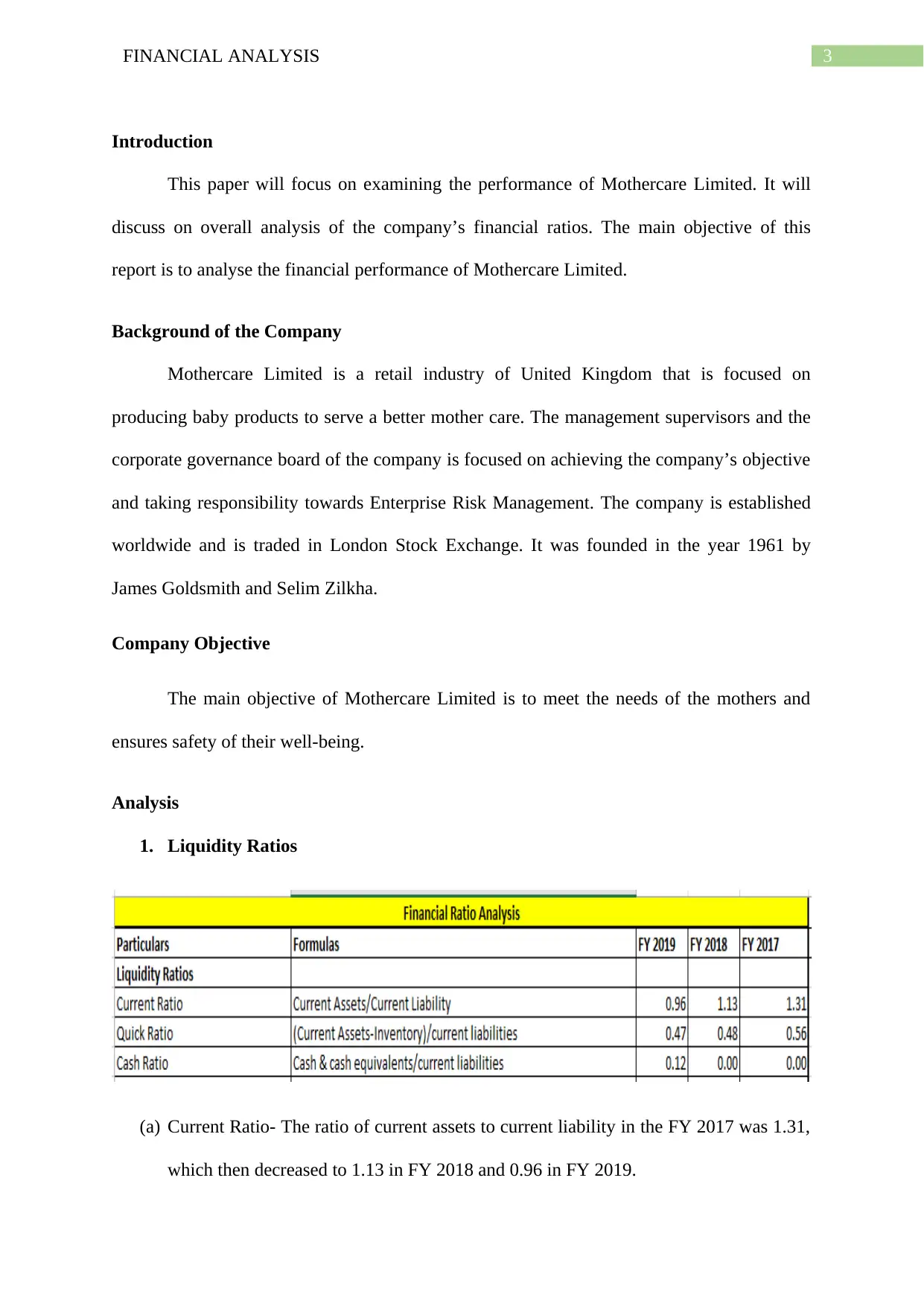

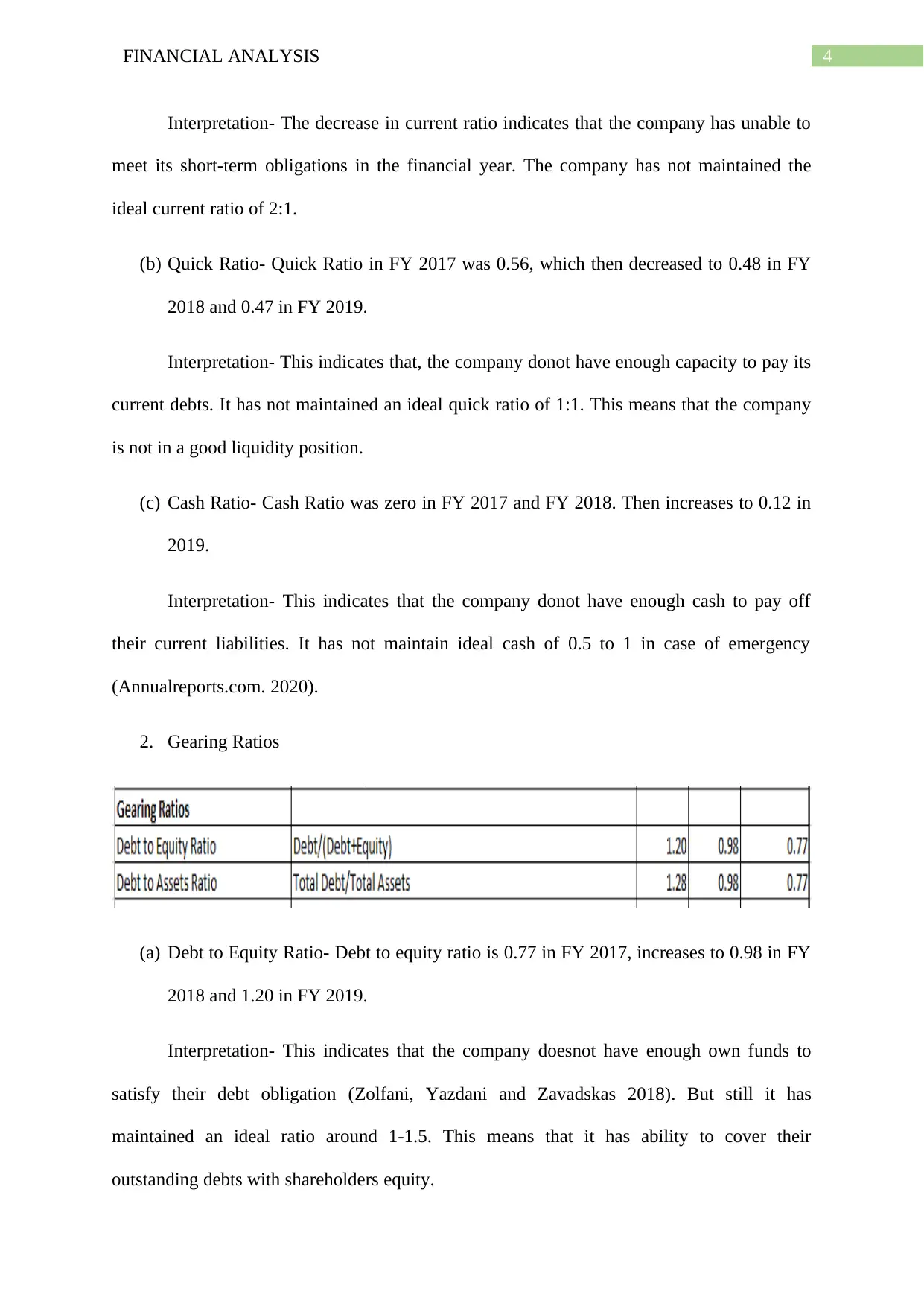

This report presents a financial analysis of Mothercare Limited, examining its performance through various financial ratios. The analysis covers liquidity ratios (current, quick, and cash ratios), gearing ratios (debt to equity and debt to assets), activity ratios (asset turnover, fixed assets turnover, stock turnover, debtor’s turnover, and creditor’s turnover), and profitability ratios (gross profit margin, net profit margin, operating profit margin, return on equity, return on assets, and price to earnings ratio). The report interprets the trends in these ratios over a three-year period (FY 2017-2019), providing insights into the company's financial position, including its ability to meet short-term obligations, manage debt, efficiently utilize assets, and generate profits. The conclusion highlights the increase in share price over the last ten years but notes the company's losses compared to the previous year, emphasizing the need for improved operational management.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.