Comprehensive Financial Analysis Report: MYEG Company Performance

VerifiedAdded on 2023/04/19

|21

|5025

|267

Report

AI Summary

This report presents a detailed financial analysis of MYEG Company, a Malaysian-based e-government services provider. The analysis includes a two-year comparison of the balance sheet and income statement, along with a comprehensive ratio analysis covering liquidity, activity, profitability, and coverage ratios. The report benchmarks MYEG against its peer group, POS Malaysia, and conducts a five-year trend analysis of key financial metrics. Furthermore, it provides recommendations for improving the company's financial performance, particularly in areas such as accounts receivable turnover and sales to fixed assets. The analysis incorporates definitions of key financial statement categories and concludes with a summary of findings and suggestions for future strategic decisions, offering valuable insights into MYEG's financial health and operational efficiency.

Running Head: FINANCE 0

Finance

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 1

Contents

Introduction......................................................................................................................................3

Detailed Ratio Analysis - Two-Year Comparison...........................................................................3

Liquidity Ratios...............................................................................................................................3

Current Ratio............................................................................................................................3

Quick Ratio...............................................................................................................................3

Activity Ratios.................................................................................................................................4

Accounts Receivable Turnover................................................................................................4

Accounts Payable Turnover Ratio............................................................................................4

Sales to Fixed Asset ratio.........................................................................................................5

Profitability Ratios...........................................................................................................................5

Gross Profit...............................................................................................................................5

Net Profit..................................................................................................................................5

Return on Assets.......................................................................................................................6

Return on Equity......................................................................................................................6

Coverage Ratios...............................................................................................................................6

Debt to Equity..........................................................................................................................6

Debt to total Asset....................................................................................................................7

Times Interest Coverage Ratio.................................................................................................7

Contents

Introduction......................................................................................................................................3

Detailed Ratio Analysis - Two-Year Comparison...........................................................................3

Liquidity Ratios...............................................................................................................................3

Current Ratio............................................................................................................................3

Quick Ratio...............................................................................................................................3

Activity Ratios.................................................................................................................................4

Accounts Receivable Turnover................................................................................................4

Accounts Payable Turnover Ratio............................................................................................4

Sales to Fixed Asset ratio.........................................................................................................5

Profitability Ratios...........................................................................................................................5

Gross Profit...............................................................................................................................5

Net Profit..................................................................................................................................5

Return on Assets.......................................................................................................................6

Return on Equity......................................................................................................................6

Coverage Ratios...............................................................................................................................6

Debt to Equity..........................................................................................................................6

Debt to total Asset....................................................................................................................7

Times Interest Coverage Ratio.................................................................................................7

FINANCE 2

Conclusions and Recommendations................................................................................................7

Definitions of the Categories belonging to the balance sheet and the Income Statement...............9

Income Statement.........................................................................................................................9

Balance sheet................................................................................................................................9

References......................................................................................................................................11

Conclusions and Recommendations................................................................................................7

Definitions of the Categories belonging to the balance sheet and the Income Statement...............9

Income Statement.........................................................................................................................9

Balance sheet................................................................................................................................9

References......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 3

Introduction

MYEG Company is the Malaysian based company having a business of the E-

government services or can also be found under the IT management sector of Malaysia. The

current revenue of the company is $371.22 million with the net profit of $201511. Current 40561

employees are working in this organization and tend to expand its business offshore as well

(Morning Star, 2018).

Financial Analysis is an important criterion for determining the strength and the

weakness of the company. This tool indicates both the positive as well as the negative aspects of

the financial statements and also reflects the areas where the management needs to work upon to

improve the areas of the weakness. The variances can also be found out with the help of the ratio

analysis technique which has been discussed below in this report (Vogel, 2014). This report has a

major outlook on the two year comparison of the balance sheet and the income statement of the

MYEG Company based in the Malaysia, the two year detailed ratio analysis, the comparison

against the industry and the peer group. For the peer group analysis the company taken is the

POS Malaysia. Apart from this the five year trend analysis of the balance sheet, income

statement and ratio analysis as well has been undertaken (Morning Star, 2018).

Detailed Ratio Analysis - Two-Year Comparison

Liquidity Ratios

Liquidity ratios are calculated with an intention to determine the company’s ability to

meet the short term obligations and short term requirements. Such ratio is calculated to match the

ability of the company to convert its assets into cash. Such ratios are very helpful for the

Introduction

MYEG Company is the Malaysian based company having a business of the E-

government services or can also be found under the IT management sector of Malaysia. The

current revenue of the company is $371.22 million with the net profit of $201511. Current 40561

employees are working in this organization and tend to expand its business offshore as well

(Morning Star, 2018).

Financial Analysis is an important criterion for determining the strength and the

weakness of the company. This tool indicates both the positive as well as the negative aspects of

the financial statements and also reflects the areas where the management needs to work upon to

improve the areas of the weakness. The variances can also be found out with the help of the ratio

analysis technique which has been discussed below in this report (Vogel, 2014). This report has a

major outlook on the two year comparison of the balance sheet and the income statement of the

MYEG Company based in the Malaysia, the two year detailed ratio analysis, the comparison

against the industry and the peer group. For the peer group analysis the company taken is the

POS Malaysia. Apart from this the five year trend analysis of the balance sheet, income

statement and ratio analysis as well has been undertaken (Morning Star, 2018).

Detailed Ratio Analysis - Two-Year Comparison

Liquidity Ratios

Liquidity ratios are calculated with an intention to determine the company’s ability to

meet the short term obligations and short term requirements. Such ratio is calculated to match the

ability of the company to convert its assets into cash. Such ratios are very helpful for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 4

creditors as it helps them in finding out the ability of the company for the repayment of loans. It

also helps in predicting whether the company can meet the obligation for the money which was

being lent by the lenders of the company (Baker, Cummings & Jagtiani, 2017).

Current Ratio

One of the liquidity ratios is current ratio and it helps in a fair calculation of the

company’s ability to meet the short-term liabilities. It is a simple comparison of the company’s

current assets and current liabilities. If the result of the comparison indicates the higher number

than it is the indication that the company has a strong base to meet the short term obligations

The current ratio of the company for the year 2017 is 18.5 whereas in the year 2016

financial year is 10.97 indicates that the company is able to pay the obligations in comparison to

the previous year (Yahoo finance, 2018). The current ratio of the POS company is low with

respect to the MYEG thus it explains that the company is performing better than the POS and has

more scope of paying off the obligations as it has sufficient current assets as having by the POS

(Heikal, Khaddafi & Ummah, 2014).

Quick Ratio

It is a type of ratio where a quick comparison is done on the basis of cash in hand,

accounts receivables and marketable securities of the company against the current liabilities of

the company. The result is measured on the basis of a higher number which indicates the strong

position of the company to meet the short term obligations of the company (Saeidi, 2015).

The quick ratio of the MYEG is 5.088 in the previous year and 3.91 in the financial year

2017. The quick ratio has been decreased by 23% in comparison to the previous year. The above

ratio indicates that the company ability to serve the obligations of the short term nature has been

creditors as it helps them in finding out the ability of the company for the repayment of loans. It

also helps in predicting whether the company can meet the obligation for the money which was

being lent by the lenders of the company (Baker, Cummings & Jagtiani, 2017).

Current Ratio

One of the liquidity ratios is current ratio and it helps in a fair calculation of the

company’s ability to meet the short-term liabilities. It is a simple comparison of the company’s

current assets and current liabilities. If the result of the comparison indicates the higher number

than it is the indication that the company has a strong base to meet the short term obligations

The current ratio of the company for the year 2017 is 18.5 whereas in the year 2016

financial year is 10.97 indicates that the company is able to pay the obligations in comparison to

the previous year (Yahoo finance, 2018). The current ratio of the POS company is low with

respect to the MYEG thus it explains that the company is performing better than the POS and has

more scope of paying off the obligations as it has sufficient current assets as having by the POS

(Heikal, Khaddafi & Ummah, 2014).

Quick Ratio

It is a type of ratio where a quick comparison is done on the basis of cash in hand,

accounts receivables and marketable securities of the company against the current liabilities of

the company. The result is measured on the basis of a higher number which indicates the strong

position of the company to meet the short term obligations of the company (Saeidi, 2015).

The quick ratio of the MYEG is 5.088 in the previous year and 3.91 in the financial year

2017. The quick ratio has been decreased by 23% in comparison to the previous year. The above

ratio indicates that the company ability to serve the obligations of the short term nature has been

FINANCE 5

reduced and deteriorated (Morning Star, 2018). The Quick ratio on the other hand is more of the

POS Company than MYEG which suggest that though the current assets are sufficient to pay

back the current liabilities yet the cash is generated at the faster pace in case of POS (Nobanee &

Al Hajjar, 2014).

Activity Ratios

An activity ratio generally reflects the ability of the company to reflect the ability and the

power of the company to convert various accounts into the financial statements of the company

in the form of cash or sales (Cable, Healy & Sun, 2018).

Accounts Receivable Turnover

Accounts Receivable Turnover ratio is the key driver that lets the management know

about the dependency of the working capital of the company upon the accounts receivable of the

company. The result is measured on the basis of indication in the numbers if such ratio indicates

a lower number than the working capital of the company is adequate which shows lesser risks of

the business (Bergeron, 2017).

The accounts receivable ratio of the company is 71 days and 76 days from the year 2016 to

2017. Thee inventory turnover ratio of the company is nil as the company has not maintained any

inventory. The sales to fixed assets of the company have decreased from 1.03 to 0.74 from 2016

to 2017 (Morning Star, 2018). There are several suggestions to improve the receivable ratio as

well as the day’s sales in the receivables ratio. The AR ratio in terms of the industry comparison

is 82.25 and whereas the ratio of the MYEG is 76.5 in the year 2017 which is again the positive

impact however to reach to the position of the 2015 at 63.1 there are following recommendations

outlined below (Weygandt, Kimmel & Kieso, 2015).

reduced and deteriorated (Morning Star, 2018). The Quick ratio on the other hand is more of the

POS Company than MYEG which suggest that though the current assets are sufficient to pay

back the current liabilities yet the cash is generated at the faster pace in case of POS (Nobanee &

Al Hajjar, 2014).

Activity Ratios

An activity ratio generally reflects the ability of the company to reflect the ability and the

power of the company to convert various accounts into the financial statements of the company

in the form of cash or sales (Cable, Healy & Sun, 2018).

Accounts Receivable Turnover

Accounts Receivable Turnover ratio is the key driver that lets the management know

about the dependency of the working capital of the company upon the accounts receivable of the

company. The result is measured on the basis of indication in the numbers if such ratio indicates

a lower number than the working capital of the company is adequate which shows lesser risks of

the business (Bergeron, 2017).

The accounts receivable ratio of the company is 71 days and 76 days from the year 2016 to

2017. Thee inventory turnover ratio of the company is nil as the company has not maintained any

inventory. The sales to fixed assets of the company have decreased from 1.03 to 0.74 from 2016

to 2017 (Morning Star, 2018). There are several suggestions to improve the receivable ratio as

well as the day’s sales in the receivables ratio. The AR ratio in terms of the industry comparison

is 82.25 and whereas the ratio of the MYEG is 76.5 in the year 2017 which is again the positive

impact however to reach to the position of the 2015 at 63.1 there are following recommendations

outlined below (Weygandt, Kimmel & Kieso, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 6

The company can start by preparing the aging schedules to interpret for how much time

the receivables are outstanding. The policy of the review can be seen on the constant

basis to identify for the patterns in the delinquent accounts (Flammer, 2015).

Developing a strategy to identify the weak customers and the delinquent accounts can be

one of the policies to improve the performance of the customers (Aldivitto & Rahman,

2016).

Accounts Payable Turnover Ratio

The payable ratio is the ratio which is used to measure the short-term liquidity of the

company. Such ratio is calculated by having a basic comparison between the total purchase from

the supplier or cost of goods sold and the average accounts payable of the company for the

particular period (Mathuva, 2015).

Under this ratio it can be observed that the accounts payable turnover ratio has been

changed drastically over the period of five years as it can be seen form the five year trend

analysis. The ratio reached 7 from 20 as it was in the year 2013. The ratio also helps to deliver

the information about the number of days in which the payment shall be made. The company has

improved the ratio and thereby it is a positive indication from the analysis. In terms of the

industry comparison the ratio has been more favourable on the side of the company whereas the

ratio of the industry is 4.33. Therefore the company is performing better than other companies

(Ukaegbu, 2014).

Sales to Fixed Asset ratio

It is a type of ratio which helps in calculating the general performance of the company. Such

type of ratios is calculated with an intention to measure the ability of the company to generate

The company can start by preparing the aging schedules to interpret for how much time

the receivables are outstanding. The policy of the review can be seen on the constant

basis to identify for the patterns in the delinquent accounts (Flammer, 2015).

Developing a strategy to identify the weak customers and the delinquent accounts can be

one of the policies to improve the performance of the customers (Aldivitto & Rahman,

2016).

Accounts Payable Turnover Ratio

The payable ratio is the ratio which is used to measure the short-term liquidity of the

company. Such ratio is calculated by having a basic comparison between the total purchase from

the supplier or cost of goods sold and the average accounts payable of the company for the

particular period (Mathuva, 2015).

Under this ratio it can be observed that the accounts payable turnover ratio has been

changed drastically over the period of five years as it can be seen form the five year trend

analysis. The ratio reached 7 from 20 as it was in the year 2013. The ratio also helps to deliver

the information about the number of days in which the payment shall be made. The company has

improved the ratio and thereby it is a positive indication from the analysis. In terms of the

industry comparison the ratio has been more favourable on the side of the company whereas the

ratio of the industry is 4.33. Therefore the company is performing better than other companies

(Ukaegbu, 2014).

Sales to Fixed Asset ratio

It is a type of ratio which helps in calculating the general performance of the company. Such

type of ratios is calculated with an intention to measure the ability of the company to generate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 7

sales from the fixed assets of the company. The result of such ratios are measured in numbers,

the higher the numbers of such ratio the higher will be efficiency of the company to utilize the

fixed assets of the company (Yahoo finance, 2018). The sale to fixed asset ratio is better of the

POS Company as it can be observed by the comparison table and moreover there are several

recommendations in regards to the sales to fixed asset ratio which can be improved if these

suggestions are followed subsequently by MYEG Company (Hanson, Shleifer Stein & Vishny,

2015).

Instead of purchasing the assets the assets shall be acquired on lease and the

The identification of the assets to determine the assets that are directly affecting the sales

of the assets can be classified easily.

The detailed records of the assets which can classify which whether the current assets are

on lease or purchase (Arnold, Hackbarth & Xenia Puhan, 2017).

Profitability Ratios

It is a ratio which is used to calculate the capacity of the company to generate profits

against the expenses of the company. The result of such ratio is measured in numbers, the higher

the numbers the higher will be the profitability of the company (Laitinen & Laitinen, 2018).

sales from the fixed assets of the company. The result of such ratios are measured in numbers,

the higher the numbers of such ratio the higher will be efficiency of the company to utilize the

fixed assets of the company (Yahoo finance, 2018). The sale to fixed asset ratio is better of the

POS Company as it can be observed by the comparison table and moreover there are several

recommendations in regards to the sales to fixed asset ratio which can be improved if these

suggestions are followed subsequently by MYEG Company (Hanson, Shleifer Stein & Vishny,

2015).

Instead of purchasing the assets the assets shall be acquired on lease and the

The identification of the assets to determine the assets that are directly affecting the sales

of the assets can be classified easily.

The detailed records of the assets which can classify which whether the current assets are

on lease or purchase (Arnold, Hackbarth & Xenia Puhan, 2017).

Profitability Ratios

It is a ratio which is used to calculate the capacity of the company to generate profits

against the expenses of the company. The result of such ratio is measured in numbers, the higher

the numbers the higher will be the profitability of the company (Laitinen & Laitinen, 2018).

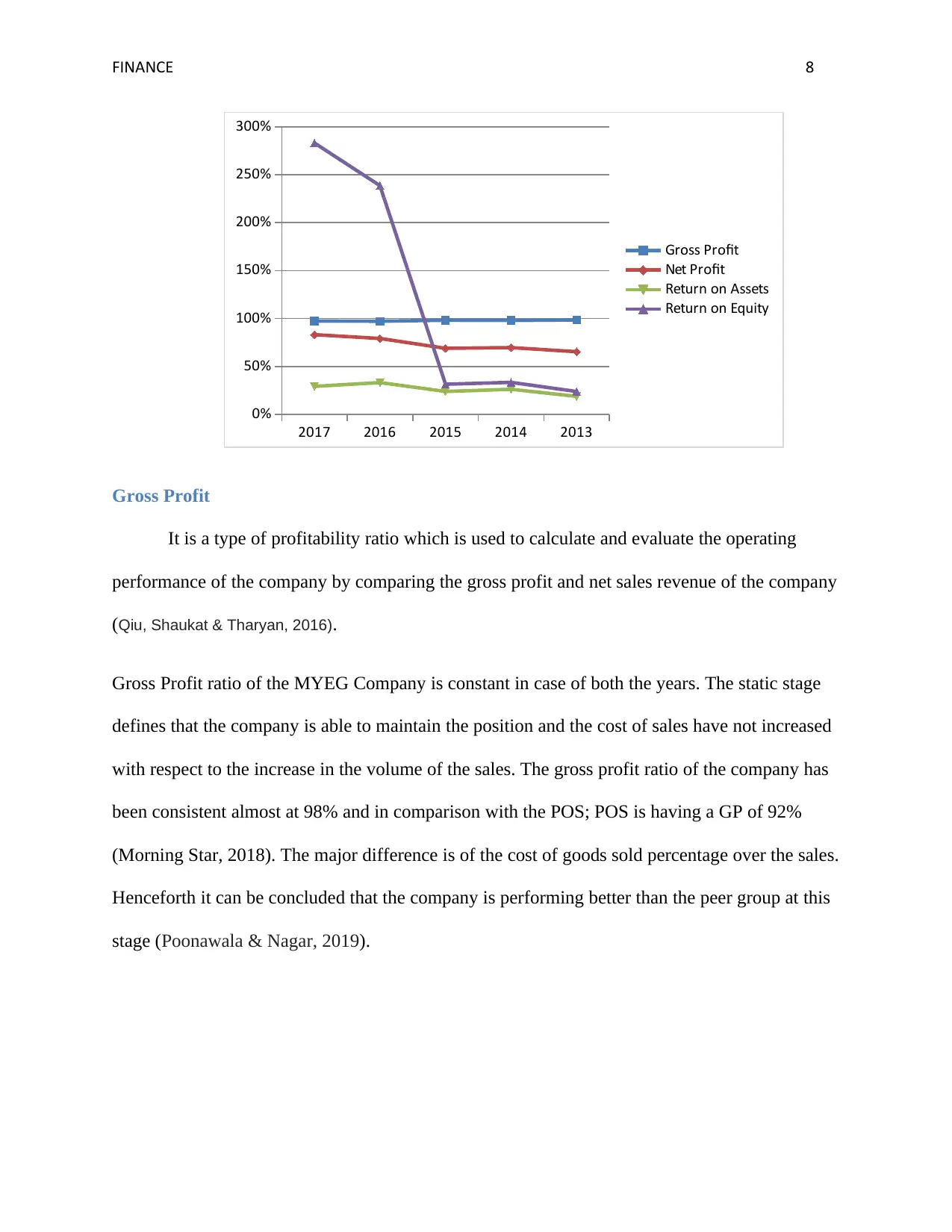

FINANCE 8

2017 2016 2015 2014 2013

0%

50%

100%

150%

200%

250%

300%

Gross Profit

Net Profit

Return on Assets

Return on Equity

Gross Profit

It is a type of profitability ratio which is used to calculate and evaluate the operating

performance of the company by comparing the gross profit and net sales revenue of the company

(Qiu, Shaukat & Tharyan, 2016).

Gross Profit ratio of the MYEG Company is constant in case of both the years. The static stage

defines that the company is able to maintain the position and the cost of sales have not increased

with respect to the increase in the volume of the sales. The gross profit ratio of the company has

been consistent almost at 98% and in comparison with the POS; POS is having a GP of 92%

(Morning Star, 2018). The major difference is of the cost of goods sold percentage over the sales.

Henceforth it can be concluded that the company is performing better than the peer group at this

stage (Poonawala & Nagar, 2019).

2017 2016 2015 2014 2013

0%

50%

100%

150%

200%

250%

300%

Gross Profit

Net Profit

Return on Assets

Return on Equity

Gross Profit

It is a type of profitability ratio which is used to calculate and evaluate the operating

performance of the company by comparing the gross profit and net sales revenue of the company

(Qiu, Shaukat & Tharyan, 2016).

Gross Profit ratio of the MYEG Company is constant in case of both the years. The static stage

defines that the company is able to maintain the position and the cost of sales have not increased

with respect to the increase in the volume of the sales. The gross profit ratio of the company has

been consistent almost at 98% and in comparison with the POS; POS is having a GP of 92%

(Morning Star, 2018). The major difference is of the cost of goods sold percentage over the sales.

Henceforth it can be concluded that the company is performing better than the peer group at this

stage (Poonawala & Nagar, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE 9

Net Profit

The net profit of the company is calculated on the basis of the net sales of the company.

The net profit reveals the deep comparison between the net profit after tax and net sales of the

company (Epstein, Buhovac & Yuthas, 2015).

The net profit of the company has increased by 5% and it is a green sign that the

company is improving its performance with respect to the previous year. The net profit is the

core value of which determines the ability of the company to sustain for the longer duration. The

net profit of MYEG over the period of five years have been increased and improved efficiently

from 65% to 83%, whereas in comparison to the peer group and industry, it is 12% more than the

peer group and in case of industry it is 10% less overall (Căpraru & Ihnatov, 2014).

Therefore it can be said that though the ratio is better than the POS yet to survive against

the rest of the competitors the company needs to work upon the strategies to improve the same

(Ashraf Rizwan & L’Huillier, 2016).

Return on Assets

It is a type of an indicator which is used to calculate the profitability of the company in

relation to the total assets of the company. Such ratio helps in analysing the efficiency of the

management of the business organisation to generate profitability (Idawati & Wahyudi, 2015).

The return on assets of the company has been decreased from 33% to 29% from 2016 to

2017 which reflects a downfall of the 11% (Yahoo finance, 2018). The low return on assets

indicates that the assets that the company owns is not of the enough value and are failing to

generate the value of the company. Henceforth it is advised that the company shall focus on

getting rid of the obsolete assets to improve the productivity of the business. The negotiation

Net Profit

The net profit of the company is calculated on the basis of the net sales of the company.

The net profit reveals the deep comparison between the net profit after tax and net sales of the

company (Epstein, Buhovac & Yuthas, 2015).

The net profit of the company has increased by 5% and it is a green sign that the

company is improving its performance with respect to the previous year. The net profit is the

core value of which determines the ability of the company to sustain for the longer duration. The

net profit of MYEG over the period of five years have been increased and improved efficiently

from 65% to 83%, whereas in comparison to the peer group and industry, it is 12% more than the

peer group and in case of industry it is 10% less overall (Căpraru & Ihnatov, 2014).

Therefore it can be said that though the ratio is better than the POS yet to survive against

the rest of the competitors the company needs to work upon the strategies to improve the same

(Ashraf Rizwan & L’Huillier, 2016).

Return on Assets

It is a type of an indicator which is used to calculate the profitability of the company in

relation to the total assets of the company. Such ratio helps in analysing the efficiency of the

management of the business organisation to generate profitability (Idawati & Wahyudi, 2015).

The return on assets of the company has been decreased from 33% to 29% from 2016 to

2017 which reflects a downfall of the 11% (Yahoo finance, 2018). The low return on assets

indicates that the assets that the company owns is not of the enough value and are failing to

generate the value of the company. Henceforth it is advised that the company shall focus on

getting rid of the obsolete assets to improve the productivity of the business. The negotiation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE 10

with the vendors shall be also one of the most important steps to lower down the basic costs and

ensures the high bid capacity of the company in the future capital expenditure. The liquidation of

the underutilized assets is again the favorable option to increase the profitability ratios of the

company (Agha, 2014).

Return on Equity

Return on Equity is a ratio which calculated to measure the financial performance of the

business organisation. Such ratio is calculated with an intention to measure the ability of the

business organisation to generate profits from the investments made by the investors of the

company

Return on equity on the other hand increased by 19% as can be observed from table and

therefore it a plus point for the company still there are certain ways through which the company

can improve the profitability ratios. The return on equity is 25% less in case of POS and in case

of the industry it is low by almost 30% (Anwar, Fathoni & Gagah, 2018).

Coverage Ratios

Coverage ratios are generally calculated to measure the ability of the company to service

the debt of the company and to meet the financial obligation of the company. The coverage ratio

forms the category of the debt to equity, debt to total assets and interest coverage ratio (Gozzi &

Schmukler, 2015).

Debt to Equity

Such ratios are calculated on the basis of the figures which are allocated on the balance

sheet of the company. Such ratios are calculated by comparing total liabilities and the

shareholders equity of the company (Schneider, 2015).

with the vendors shall be also one of the most important steps to lower down the basic costs and

ensures the high bid capacity of the company in the future capital expenditure. The liquidation of

the underutilized assets is again the favorable option to increase the profitability ratios of the

company (Agha, 2014).

Return on Equity

Return on Equity is a ratio which calculated to measure the financial performance of the

business organisation. Such ratio is calculated with an intention to measure the ability of the

business organisation to generate profits from the investments made by the investors of the

company

Return on equity on the other hand increased by 19% as can be observed from table and

therefore it a plus point for the company still there are certain ways through which the company

can improve the profitability ratios. The return on equity is 25% less in case of POS and in case

of the industry it is low by almost 30% (Anwar, Fathoni & Gagah, 2018).

Coverage Ratios

Coverage ratios are generally calculated to measure the ability of the company to service

the debt of the company and to meet the financial obligation of the company. The coverage ratio

forms the category of the debt to equity, debt to total assets and interest coverage ratio (Gozzi &

Schmukler, 2015).

Debt to Equity

Such ratios are calculated on the basis of the figures which are allocated on the balance

sheet of the company. Such ratios are calculated by comparing total liabilities and the

shareholders equity of the company (Schneider, 2015).

FINANCE 11

The debt to equity ratio of MYEG have been increased by 4% ensuring the debentures

have been financed more in comparison to the previous year to avail the benefit of the tax

advantage. The ratio increased from 0.18 to 0.19 and therefore the firm feels secure towards the

debentures (Coleman, Cotei & Farhat, 2016).

Debt to total Asset

It is a leverage ratio which is calculated to measure the total amount of debt in relation to

the assets of the company. Therefore this ratio explains the proportion of debt with the total

assets acquired by the company (Reid, 2018).

The debt to total asset ratio of MYEG has also increased by 6% in comparison to the

previous year from 2016 to 2017 and can happily sustain with the fact that the company has the

strong capital structure and financing through the right ways (Bradley & Roberts, 2015). The

debt to total asset of the company was consistent over the period of five years at 0.16 (Morning

Star, 2018).

Times Interest Coverage Ratio

This type of ratio is a measure which is used to calculate the interest paying capacity of

the company on the amount of outstanding debt of the company (Cheng, et al 2016).

The times interest coverage ratio of the company has fallen drastically from 75 to 53

times. Therefore it can be inferred that the company is not having the enough capacity to pay

back the interest expense and the company’s interest coverage is not sure and enough from the

point of view of the company coverage. The interest coverage ratio is better in case of POS and

in case of the industry as well (Du, Tepper & Verdelhan, 2018).

The following steps can be covered and instilled to improve the coverage ratios of the company.

The debt to equity ratio of MYEG have been increased by 4% ensuring the debentures

have been financed more in comparison to the previous year to avail the benefit of the tax

advantage. The ratio increased from 0.18 to 0.19 and therefore the firm feels secure towards the

debentures (Coleman, Cotei & Farhat, 2016).

Debt to total Asset

It is a leverage ratio which is calculated to measure the total amount of debt in relation to

the assets of the company. Therefore this ratio explains the proportion of debt with the total

assets acquired by the company (Reid, 2018).

The debt to total asset ratio of MYEG has also increased by 6% in comparison to the

previous year from 2016 to 2017 and can happily sustain with the fact that the company has the

strong capital structure and financing through the right ways (Bradley & Roberts, 2015). The

debt to total asset of the company was consistent over the period of five years at 0.16 (Morning

Star, 2018).

Times Interest Coverage Ratio

This type of ratio is a measure which is used to calculate the interest paying capacity of

the company on the amount of outstanding debt of the company (Cheng, et al 2016).

The times interest coverage ratio of the company has fallen drastically from 75 to 53

times. Therefore it can be inferred that the company is not having the enough capacity to pay

back the interest expense and the company’s interest coverage is not sure and enough from the

point of view of the company coverage. The interest coverage ratio is better in case of POS and

in case of the industry as well (Du, Tepper & Verdelhan, 2018).

The following steps can be covered and instilled to improve the coverage ratios of the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.