Management Accounting Report for Nisa Firm Analysis

VerifiedAdded on 2020/09/08

|17

|4592

|419

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their practical application within the context of the Nisa firm. It begins by defining management accounting, exploring different types of systems, and detailing various reporting methods. The report then delves into a comparative analysis of marginal and absorption costing techniques, presenting an income statement for Nisa under both methods. Furthermore, it examines various planning tools used for budget control, discussing their advantages and disadvantages. The report concludes with an analysis of how Nisa is adopting management accounting systems, highlighting key financial problems and offering potential solutions. The content covers job costing, inventory management, operating budget, and performance reports and their impact on decision-making and profitability.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Different types of MA and System...................................................................................1

P2 Various method to manage management reporting accounts............................................3

TASK 2............................................................................................................................................5

P3 Income statement for Nisa using marginal and absorption costs of management accounting

techniques...............................................................................................................................5

TASK 3............................................................................................................................................7

P4 Various tools of planning used to control the budget........................................................7

TASK 4..........................................................................................................................................10

P5 How Nisa is adopting management accounting systems................................................10

Conclusion.....................................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Different types of MA and System...................................................................................1

P2 Various method to manage management reporting accounts............................................3

TASK 2............................................................................................................................................5

P3 Income statement for Nisa using marginal and absorption costs of management accounting

techniques...............................................................................................................................5

TASK 3............................................................................................................................................7

P4 Various tools of planning used to control the budget........................................................7

TASK 4..........................................................................................................................................10

P5 How Nisa is adopting management accounting systems................................................10

Conclusion.....................................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is very crucial and important for the business management to

keep their financial and costs problems away and improve the business operations effectively.

The introduction includes the essential requirements of management accounting and different

types systems for management accounting for Nisa organisation. The different methods for

management accounting reporting is also included. The income statement of Nisa by using

appropriate cost techniques in terms of marginal and absorption costs to calculate the net income.

The report also covers the various planning tools to control the budget with their advantages and

disadvantages effectively and how these control can manage the financial problems within Nisa

firm. Finally, the financial problems and their solution with effective use of management

accountant skills and characteristic is included.

TASK 1

P1 Different types of MA and System

MANAGEMENT ACCOUNTING

Management accounting is also known as cost accounting and managerial accounting. It

is a process used for analysing business operations and costs to prepare records, internal financial

reports and accounts to aid managers, decision making process to accomplish organisation goals.

In simple words, it is the act of preparing costing and financial data and translating it to useful

information for management officers within Nisa firm. Management accounting also helps to

achieve better planning and control over the firm. It is useful for all kind of firms including sole

proprietorships, government and non profit organisations. It is a technique, which is focused

upon effective use of business resource to help and assist managers towards task, which enhance

both customers and shareholders values effectively (Armstrong, 2014).

MANAGEMENT ACCOUNTING SYSTEMS

Management accounting system produce the useful information required by managers to

manage and use the business resources for creating value for the organisation Nisa. It is an

important part of wider management information system of a business. It provides relevant

information to satisfy the needs of management in terms of short and long term decision-making.

Management accounting includes the costs of producing services and goods, information to

control operations and planning as well as measuring performance.

1

Management accounting is very crucial and important for the business management to

keep their financial and costs problems away and improve the business operations effectively.

The introduction includes the essential requirements of management accounting and different

types systems for management accounting for Nisa organisation. The different methods for

management accounting reporting is also included. The income statement of Nisa by using

appropriate cost techniques in terms of marginal and absorption costs to calculate the net income.

The report also covers the various planning tools to control the budget with their advantages and

disadvantages effectively and how these control can manage the financial problems within Nisa

firm. Finally, the financial problems and their solution with effective use of management

accountant skills and characteristic is included.

TASK 1

P1 Different types of MA and System

MANAGEMENT ACCOUNTING

Management accounting is also known as cost accounting and managerial accounting. It

is a process used for analysing business operations and costs to prepare records, internal financial

reports and accounts to aid managers, decision making process to accomplish organisation goals.

In simple words, it is the act of preparing costing and financial data and translating it to useful

information for management officers within Nisa firm. Management accounting also helps to

achieve better planning and control over the firm. It is useful for all kind of firms including sole

proprietorships, government and non profit organisations. It is a technique, which is focused

upon effective use of business resource to help and assist managers towards task, which enhance

both customers and shareholders values effectively (Armstrong, 2014).

MANAGEMENT ACCOUNTING SYSTEMS

Management accounting system produce the useful information required by managers to

manage and use the business resources for creating value for the organisation Nisa. It is an

important part of wider management information system of a business. It provides relevant

information to satisfy the needs of management in terms of short and long term decision-making.

Management accounting includes the costs of producing services and goods, information to

control operations and planning as well as measuring performance.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system: Cost accounting system estimates and evaluate the cost of

services and goods as well as the cost of business units and resources, such as

department. It provides relevant and important cost data to the managers, which help

them to control the business operation and make strategies and plans for the future within

Nisa firm effectively and efficiently. Cost accounting system is generally used in

organisations such as manufacturers, retailers, wholesalers, sole proprietorships and

government departments.

Benefits:

Cost accounting system determines the cost of products and services which help

managers to take marketing decisions (Bouten, and Hoozée, 2013).

It also helps to determine the selling price of a product effectively.

Cost accounting system analyse the business profitability and meets competition.

Inventory management system: Inventory is a stock of any resource or product which is

used in the business include work which is in progress, raw material and finished

products etc. Inventory management system is a set of plans and policies which manage

and control the monitor levels of inventory and also determines what stock should be

replenished, what levels should be managed and maintained and quantity which

organisation should order effectively and efficiently. Inventory cost is also known as

carrying and holding cost which includes storage costs such as insurance, facilities,

utilities and taxes and capital costs includes opportunity costs. Ordering and setup costs

includes purchase, transportation and shortage costs. Here are some types inventory:

Raw materials: Raw materials is the first step of making any product and supplied by

vendors that do not include any labour by the business for receiving the items.

Finished goods: Finished goods are those products which is completed and ready to sell

but still in the possession of the business which manufactured them.

Work in process: In this process, products which have been partially processed but still

incomplete are included.

Benefits:

Protection against uncertainties, shortage of raw material.

Support strategic plan and take advantage of economy scale

2

services and goods as well as the cost of business units and resources, such as

department. It provides relevant and important cost data to the managers, which help

them to control the business operation and make strategies and plans for the future within

Nisa firm effectively and efficiently. Cost accounting system is generally used in

organisations such as manufacturers, retailers, wholesalers, sole proprietorships and

government departments.

Benefits:

Cost accounting system determines the cost of products and services which help

managers to take marketing decisions (Bouten, and Hoozée, 2013).

It also helps to determine the selling price of a product effectively.

Cost accounting system analyse the business profitability and meets competition.

Inventory management system: Inventory is a stock of any resource or product which is

used in the business include work which is in progress, raw material and finished

products etc. Inventory management system is a set of plans and policies which manage

and control the monitor levels of inventory and also determines what stock should be

replenished, what levels should be managed and maintained and quantity which

organisation should order effectively and efficiently. Inventory cost is also known as

carrying and holding cost which includes storage costs such as insurance, facilities,

utilities and taxes and capital costs includes opportunity costs. Ordering and setup costs

includes purchase, transportation and shortage costs. Here are some types inventory:

Raw materials: Raw materials is the first step of making any product and supplied by

vendors that do not include any labour by the business for receiving the items.

Finished goods: Finished goods are those products which is completed and ready to sell

but still in the possession of the business which manufactured them.

Work in process: In this process, products which have been partially processed but still

incomplete are included.

Benefits:

Protection against uncertainties, shortage of raw material.

Support strategic plan and take advantage of economy scale

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing system: Job costing system is a process of cost recording and accumulation

where the identification of job or any group is presence for which the cost can be

collected or managed. Job costing system is used in businesses, where the production of

a product is 'one off' that is different for an individual customer efficiently. It is suitable

and reliable for organisations where work is undertaken towards a special requirement of

a customer and each order take short duration comparatively.

Benefits:

Cost control, planning, and decision-making is involved for establishing cost.

Calculate selling price and determine profit and loss at workplace.

Price optimising system: It is a plan of action which allows an firm to know the old

clients' sensitivity to change the product price according to the profitability levels within

Nisa firm effectively. Price optimising system use by business to tailor pricing for

various customers based on their response to change in different pricing.

Benefits:

Optimal pricing is beneficial to increase profitability by keeping same levels of customer

retentions (Christ, and Burritt, 2017).

Defines profitability levels based on existing clients' sensitivity to change the price of the

product.

P2 Various method to manage management reporting accounts

MANAGEMENT ACCOUNTING REPORTS

Management accounting report help business management to make informed and

effective decision-making which is vital to the organisations' operation. Such reports also

provide information of various aspect of the firm to managers which helps them to create

effective and efficient decision-making that may have a positive and profound effect on the

organisation.

Job cost reports: Job cost reports shows the cost incurred for a specific project or work.

These reports are usually combined with figuring of revenues that the firm Nisa can

identify their works profitability effectively. These reports also help to identify the areas

from which the business can earn higher which help to focus in efforts instead of wasting

time and money for the jobs who has low profit margins. It is also used to analyse the

3

where the identification of job or any group is presence for which the cost can be

collected or managed. Job costing system is used in businesses, where the production of

a product is 'one off' that is different for an individual customer efficiently. It is suitable

and reliable for organisations where work is undertaken towards a special requirement of

a customer and each order take short duration comparatively.

Benefits:

Cost control, planning, and decision-making is involved for establishing cost.

Calculate selling price and determine profit and loss at workplace.

Price optimising system: It is a plan of action which allows an firm to know the old

clients' sensitivity to change the product price according to the profitability levels within

Nisa firm effectively. Price optimising system use by business to tailor pricing for

various customers based on their response to change in different pricing.

Benefits:

Optimal pricing is beneficial to increase profitability by keeping same levels of customer

retentions (Christ, and Burritt, 2017).

Defines profitability levels based on existing clients' sensitivity to change the price of the

product.

P2 Various method to manage management reporting accounts

MANAGEMENT ACCOUNTING REPORTS

Management accounting report help business management to make informed and

effective decision-making which is vital to the organisations' operation. Such reports also

provide information of various aspect of the firm to managers which helps them to create

effective and efficient decision-making that may have a positive and profound effect on the

organisation.

Job cost reports: Job cost reports shows the cost incurred for a specific project or work.

These reports are usually combined with figuring of revenues that the firm Nisa can

identify their works profitability effectively. These reports also help to identify the areas

from which the business can earn higher which help to focus in efforts instead of wasting

time and money for the jobs who has low profit margins. It is also used to analyse the

3

different cost while the work is in progression so the management can manage the area of

waste.

Inventory management reports: Business with physical inventory can use the

management accounting reports managing the monitor levels of inventory which helps to

determine the levels which should be preserved, stock which should be refill and amount

which firm should command. Inventory management reports include such item, per unit

overhead cost, labour cost and inventory waste. Business can compare different assembly

line to watch the betterment and to offer reward for the best performing department.

Operating budget report: Budget reports helps Nisa organisation to analyse the

execution of all departments to enable monitoring and controlling the costs of operational

activities. Management of the business use the operational budgeting report to provide

rewards to their employees effectively (Fourie, and et.al.,2015).

Accounts receivable aging reports: ACR reports helps business management to manage

its cash flow in respect of credits which it offers to the customers effectively. This is a

critical tool that breaks down the balance of customer by the time they have owned the

organisation. These reports include separate columns for invoice that are 30, 60 or 90

days late. It helps business to identify the collection process problems effectively. If the

customers are unable to pay their balances, then the business should tighten its credit

policies and plans. Time to time analysing of accounts receivable aging reports also help

business collection department to overlook its old debts effectively and efficiently.

Performance report: Performance report helps business management to access the

product and service performance of groups or departments or segment as well of the

business operating markets. It also helps organisation to undertake profitability analysis

for product lines, market segments and departments so that they gain their benefits and

profits effectively and efficiently. These reports enable firms to corrective measurement

at place in order to manage and control the costs which brings efficiency in the business

operations effectively.

Thus, these managements accounting reports help business to make effective decision-

making and operate its operations effectively and efficiently. The information collected from

these reports help management to make strategies and plans for increasing profitability and

managing work of employees at work place effectively (Järvinen, 2016). It also helps to manage

4

waste.

Inventory management reports: Business with physical inventory can use the

management accounting reports managing the monitor levels of inventory which helps to

determine the levels which should be preserved, stock which should be refill and amount

which firm should command. Inventory management reports include such item, per unit

overhead cost, labour cost and inventory waste. Business can compare different assembly

line to watch the betterment and to offer reward for the best performing department.

Operating budget report: Budget reports helps Nisa organisation to analyse the

execution of all departments to enable monitoring and controlling the costs of operational

activities. Management of the business use the operational budgeting report to provide

rewards to their employees effectively (Fourie, and et.al.,2015).

Accounts receivable aging reports: ACR reports helps business management to manage

its cash flow in respect of credits which it offers to the customers effectively. This is a

critical tool that breaks down the balance of customer by the time they have owned the

organisation. These reports include separate columns for invoice that are 30, 60 or 90

days late. It helps business to identify the collection process problems effectively. If the

customers are unable to pay their balances, then the business should tighten its credit

policies and plans. Time to time analysing of accounts receivable aging reports also help

business collection department to overlook its old debts effectively and efficiently.

Performance report: Performance report helps business management to access the

product and service performance of groups or departments or segment as well of the

business operating markets. It also helps organisation to undertake profitability analysis

for product lines, market segments and departments so that they gain their benefits and

profits effectively and efficiently. These reports enable firms to corrective measurement

at place in order to manage and control the costs which brings efficiency in the business

operations effectively.

Thus, these managements accounting reports help business to make effective decision-

making and operate its operations effectively and efficiently. The information collected from

these reports help management to make strategies and plans for increasing profitability and

managing work of employees at work place effectively (Järvinen, 2016). It also helps to manage

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the different costs of the firm Nisa which leads towards achieving objectives and goals

simultaneously.

TASK 2

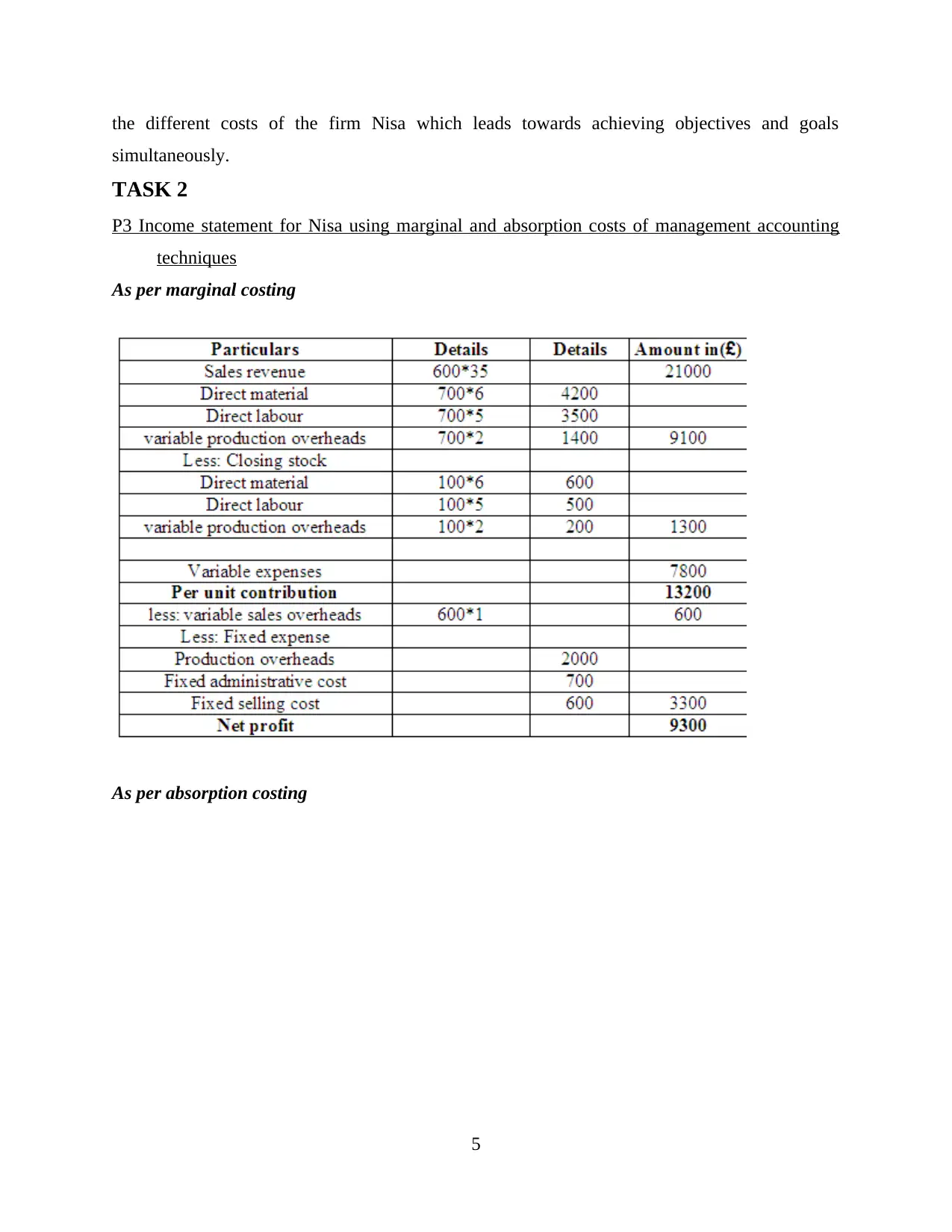

P3 Income statement for Nisa using marginal and absorption costs of management accounting

techniques

As per marginal costing

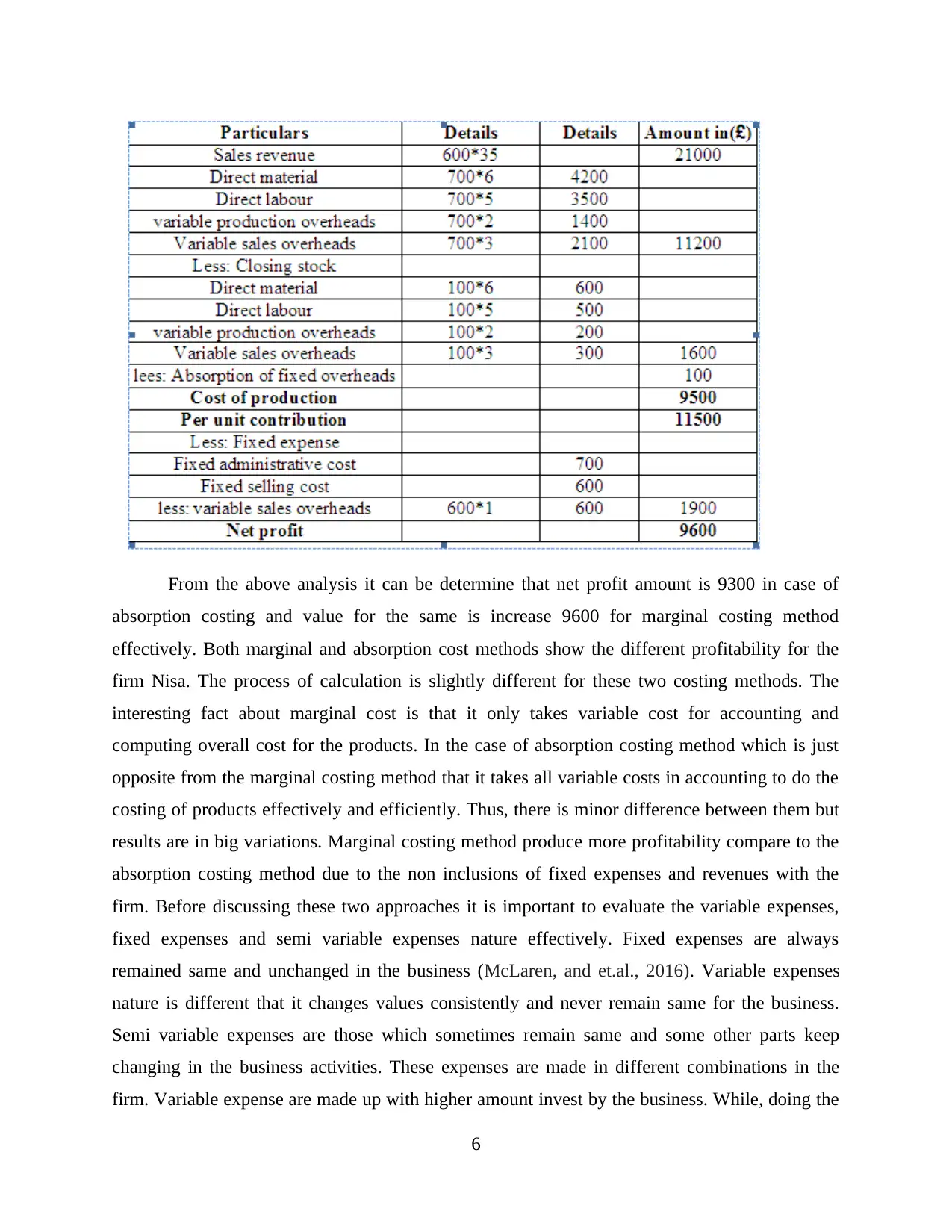

As per absorption costing

5

simultaneously.

TASK 2

P3 Income statement for Nisa using marginal and absorption costs of management accounting

techniques

As per marginal costing

As per absorption costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above analysis it can be determine that net profit amount is 9300 in case of

absorption costing and value for the same is increase 9600 for marginal costing method

effectively. Both marginal and absorption cost methods show the different profitability for the

firm Nisa. The process of calculation is slightly different for these two costing methods. The

interesting fact about marginal cost is that it only takes variable cost for accounting and

computing overall cost for the products. In the case of absorption costing method which is just

opposite from the marginal costing method that it takes all variable costs in accounting to do the

costing of products effectively and efficiently. Thus, there is minor difference between them but

results are in big variations. Marginal costing method produce more profitability compare to the

absorption costing method due to the non inclusions of fixed expenses and revenues with the

firm. Before discussing these two approaches it is important to evaluate the variable expenses,

fixed expenses and semi variable expenses nature effectively. Fixed expenses are always

remained same and unchanged in the business (McLaren, and et.al., 2016). Variable expenses

nature is different that it changes values consistently and never remain same for the business.

Semi variable expenses are those which sometimes remain same and some other parts keep

changing in the business activities. These expenses are made in different combinations in the

firm. Variable expense are made up with higher amount invest by the business. While, doing the

6

absorption costing and value for the same is increase 9600 for marginal costing method

effectively. Both marginal and absorption cost methods show the different profitability for the

firm Nisa. The process of calculation is slightly different for these two costing methods. The

interesting fact about marginal cost is that it only takes variable cost for accounting and

computing overall cost for the products. In the case of absorption costing method which is just

opposite from the marginal costing method that it takes all variable costs in accounting to do the

costing of products effectively and efficiently. Thus, there is minor difference between them but

results are in big variations. Marginal costing method produce more profitability compare to the

absorption costing method due to the non inclusions of fixed expenses and revenues with the

firm. Before discussing these two approaches it is important to evaluate the variable expenses,

fixed expenses and semi variable expenses nature effectively. Fixed expenses are always

remained same and unchanged in the business (McLaren, and et.al., 2016). Variable expenses

nature is different that it changes values consistently and never remain same for the business.

Semi variable expenses are those which sometimes remain same and some other parts keep

changing in the business activities. These expenses are made in different combinations in the

firm. Variable expense are made up with higher amount invest by the business. While, doing the

6

business calculations, one question always occur for the managers that they need to use one of

these approaches to find better calculations. It is very difficult for the business managers to

determine which method they have to use between marginal and absorption costing for effective

calculation process in the business. The both methods are important and crucial for the firms.

Absorption costing method use the fixed expenses to take consideration with variable expenses

effectively. This can be observed that purchase of fixed assets every year is not done for making

crucial contribution towards entire production procedures. In this case marginal costing method

is useful for the firm because inclusion of fixed assets does not make any sense for the firm

operations. On the other side marginal costing consider one thing that even fixed assets are not

incurred directly in relation to the production process. It is the cost which covers the business

cost out of cash flows. From this point of view the consideration of fixed expenses seems right

for the business. Thus, it can be easily said that both marginal and absorption methods of costs

are useful and important for the businesses. It is beneficial for the managers that the use of

marginal costs methods helps them to determine the amount of profit which is business

generating, if only those expense are taken as a consideration that are contributing much to the

production process of the firm. The use of absorption costing methods helps managers to

evaluate the profits earned by the business with using both expenses into account respectively

and effectively. This will help to determine the revenue computed and helps managers to be

more effective in their decision-making effectively and in proper manner. Thus, business should

use both approaches at workplace that it arises few positive and negative points associated with

these approaches. According to the need of these approaches which must used effectively at

workplace and gives proper evaluation of expense done in the business. This will also help

business managers to make effective decision and made operations successfully and can be

governed in appropriate and proper manner effectively and efficiently.

TASK 3

P4 Various tools of planning used to control the budget

Budgeting is the preparation of strategies in numerical terms towards the future period.

Nisa business should set up budget for its units, divisions, department and for the whole

organisation effectively. The normal time period for a budget is one year and it is generally,

verbalised in financial terms. Budget has 4 control procedures given below:

It determines and define the standards required in all control system.

7

these approaches to find better calculations. It is very difficult for the business managers to

determine which method they have to use between marginal and absorption costing for effective

calculation process in the business. The both methods are important and crucial for the firms.

Absorption costing method use the fixed expenses to take consideration with variable expenses

effectively. This can be observed that purchase of fixed assets every year is not done for making

crucial contribution towards entire production procedures. In this case marginal costing method

is useful for the firm because inclusion of fixed assets does not make any sense for the firm

operations. On the other side marginal costing consider one thing that even fixed assets are not

incurred directly in relation to the production process. It is the cost which covers the business

cost out of cash flows. From this point of view the consideration of fixed expenses seems right

for the business. Thus, it can be easily said that both marginal and absorption methods of costs

are useful and important for the businesses. It is beneficial for the managers that the use of

marginal costs methods helps them to determine the amount of profit which is business

generating, if only those expense are taken as a consideration that are contributing much to the

production process of the firm. The use of absorption costing methods helps managers to

evaluate the profits earned by the business with using both expenses into account respectively

and effectively. This will help to determine the revenue computed and helps managers to be

more effective in their decision-making effectively and in proper manner. Thus, business should

use both approaches at workplace that it arises few positive and negative points associated with

these approaches. According to the need of these approaches which must used effectively at

workplace and gives proper evaluation of expense done in the business. This will also help

business managers to make effective decision and made operations successfully and can be

governed in appropriate and proper manner effectively and efficiently.

TASK 3

P4 Various tools of planning used to control the budget

Budgeting is the preparation of strategies in numerical terms towards the future period.

Nisa business should set up budget for its units, divisions, department and for the whole

organisation effectively. The normal time period for a budget is one year and it is generally,

verbalised in financial terms. Budget has 4 control procedures given below:

It determines and define the standards required in all control system.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps to provide clear and unambiguous guideline about the business expectations and

resources effectively (Mokhtar, Jusoh, and Zulkifli, 2016).

It helps to evaluate the performance of managers and units.

FINANCIAL BUDGETS

Financial budgets defines the business expectations of improving cash revenue for the

coming time period and how the organisation plans to spend it as a benefit. Normally, sources of

cash such as sales of assets, loans, issuance of stock and sales revenue is included. On the other

side common use of cash is to purchase new assets, repay debts, pay dividends and pay expenses.

Financial budget includes:

Cash budget: Cash budget is important for the Nisa firm that it controls incoming and

outgoing cash into monthly, weekly or daily periods. This will help business to ensure

that it is able to meet the current obligations effectively. Cash budgeting also help to

show the availability of excess cash in the business.

Capital expenditure budget: Such financial budgets concentrate upon some major

assets of the business such as land or machinery and new plants. Business acquire such

assets through securities or long term bonds. All the organisations pays a close attention

towards this budget because of the large investments associated with capital expenditure.

Balance sheet budget: It helps to forecast the business balance sheet if all budgets are

meeting the needs. It also helps to serve the purpose of controlling to ensure the other

budgets mesh appropriately. This will produce results that are best in interests of the firm

effectively.

OPERATING BUDGETS

Operating budgets are the expression of business planning operations for a specific

period. The types of operating budgets are given below:

Sales and revenue budget: This budget focus upon income which an organisation

expects to receive from the operations. It becomes important for the managers that they

understand the financial position of the firm in the future.

Expense budget: This budget helps organisation to outline the anticipated expenses in a

particular time period. It also helps manager to prepare for upcoming expense in the firm

Nisa effectively and efficiently (Schaltegger, Gibassier, and Zvezdov, 2013).

8

resources effectively (Mokhtar, Jusoh, and Zulkifli, 2016).

It helps to evaluate the performance of managers and units.

FINANCIAL BUDGETS

Financial budgets defines the business expectations of improving cash revenue for the

coming time period and how the organisation plans to spend it as a benefit. Normally, sources of

cash such as sales of assets, loans, issuance of stock and sales revenue is included. On the other

side common use of cash is to purchase new assets, repay debts, pay dividends and pay expenses.

Financial budget includes:

Cash budget: Cash budget is important for the Nisa firm that it controls incoming and

outgoing cash into monthly, weekly or daily periods. This will help business to ensure

that it is able to meet the current obligations effectively. Cash budgeting also help to

show the availability of excess cash in the business.

Capital expenditure budget: Such financial budgets concentrate upon some major

assets of the business such as land or machinery and new plants. Business acquire such

assets through securities or long term bonds. All the organisations pays a close attention

towards this budget because of the large investments associated with capital expenditure.

Balance sheet budget: It helps to forecast the business balance sheet if all budgets are

meeting the needs. It also helps to serve the purpose of controlling to ensure the other

budgets mesh appropriately. This will produce results that are best in interests of the firm

effectively.

OPERATING BUDGETS

Operating budgets are the expression of business planning operations for a specific

period. The types of operating budgets are given below:

Sales and revenue budget: This budget focus upon income which an organisation

expects to receive from the operations. It becomes important for the managers that they

understand the financial position of the firm in the future.

Expense budget: This budget helps organisation to outline the anticipated expenses in a

particular time period. It also helps manager to prepare for upcoming expense in the firm

Nisa effectively and efficiently (Schaltegger, Gibassier, and Zvezdov, 2013).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Project budget: Project budget focused upon differences between revenue or sales and

expenses profits. In the situation, where anticipated profit is too small, some actions

needed to increase the sales and revenue budget and control upon expense budget.

FIXED AND VARIABLE BUDGETS

Fixed and variable budget regardless of the business purpose must account for the three

costs which is following below:

Fixed cost: These are the fix expenses, which the business incurs whether in operations

or not. Managers and employees salary is the best example of fixed cost.

Variable cost: Variable costs are depends on the scope of business operations. Raw

materials used in production is the best example of variable costs. If worth of raw

material is $5 per unit than 10 units would cost $50 and 20 will cost $100 and so on

effectively.

ADVANTAGES DISADVANTAGES

Budget control coordinates business activities

in different departments

A major problem occurs when budget used

rigidly and mechanically

It helps business strategies and plans into

actions

lack of participation will demotivate workers

in the firm effectively.

Budget provides an excellent record of

business activities and operations

It can also cause perceptions of unfairness

It improves and develop the communication

level with employees in the firm

Budgets can make competition for politics and

resources

Budget clarify and justify all requests to

improve allocation of resources in the firm

A mechanically and rigidly budget can reduce

the innovation and initiative at lower level

It is a natural complement for strategies and

planning

It is time consuming and however, hampers

change, flexibility of plans and development

EFFECTIVE BUDGETARY CONTROL

Effective budget control can help Nisa business to reduce financial problems and

effective use of cost and revenues in operational activities. Setting appropriate standard is a key

9

expenses profits. In the situation, where anticipated profit is too small, some actions

needed to increase the sales and revenue budget and control upon expense budget.

FIXED AND VARIABLE BUDGETS

Fixed and variable budget regardless of the business purpose must account for the three

costs which is following below:

Fixed cost: These are the fix expenses, which the business incurs whether in operations

or not. Managers and employees salary is the best example of fixed cost.

Variable cost: Variable costs are depends on the scope of business operations. Raw

materials used in production is the best example of variable costs. If worth of raw

material is $5 per unit than 10 units would cost $50 and 20 will cost $100 and so on

effectively.

ADVANTAGES DISADVANTAGES

Budget control coordinates business activities

in different departments

A major problem occurs when budget used

rigidly and mechanically

It helps business strategies and plans into

actions

lack of participation will demotivate workers

in the firm effectively.

Budget provides an excellent record of

business activities and operations

It can also cause perceptions of unfairness

It improves and develop the communication

level with employees in the firm

Budgets can make competition for politics and

resources

Budget clarify and justify all requests to

improve allocation of resources in the firm

A mechanically and rigidly budget can reduce

the innovation and initiative at lower level

It is a natural complement for strategies and

planning

It is time consuming and however, hampers

change, flexibility of plans and development

EFFECTIVE BUDGETARY CONTROL

Effective budget control can help Nisa business to reduce financial problems and

effective use of cost and revenues in operational activities. Setting appropriate standard is a key

9

for successful budgeting, ensuring top management support requires departments and divisions

to make and defend their own budgets. Participation by users in budget preparation also help top

management to control the lower level activities and providing information to managers about

performance under budget also make effective budgetary control for the business (Thomas,

2016).

FIVE FORCES ANALYSIS FROM PORTER'S

Threats of new entrance: This force determines the easy entrance of new industries in

the market that when more businesses compete for the same market, profit of the Nisa

organisation start to fall. It is important for the Nisa business to create high barriers to

enter to deter new entrants with managing its budgeting and costs which increase its

profitability and capital.

Bargaining power of suppliers: Strong power of bargaining allows suppliers to sell law

quality products on high prices. This will affect the profitability of the firm that they have

to pay more for their materials. The Nisa firm should manage its financial position that it

can be able to purchase necessary material for operations and should try to manage the

bargaining power of suppliers which help it to manage its raw material costs.

Bargaining power of buyers: Customers have power to demand lower prices with high

quality product which affect the revenues of the firm. Buyers are price sensitive that

business should set a price which manage its revenues and quality of the products and

services effectively.

Threats of substitutes: This force especially threatening when customers finds easy

substitutes for their products with attractive prices and better quality. The Nisa business

should make its product and services unique from others with managing budget and costs

will reduce the threat of substitutes and increase the profitability. This will help business

to make its financial position good among others (Van der Stede, 2015).

Rivalry among existing competitors: This force determines, how a business is

profitable and competitive that there are so many competitors in market share. The

business CIAM should improve its growth and customer loyalty which helps it to

compete other in the market and make a goodwill of the firm.

10

to make and defend their own budgets. Participation by users in budget preparation also help top

management to control the lower level activities and providing information to managers about

performance under budget also make effective budgetary control for the business (Thomas,

2016).

FIVE FORCES ANALYSIS FROM PORTER'S

Threats of new entrance: This force determines the easy entrance of new industries in

the market that when more businesses compete for the same market, profit of the Nisa

organisation start to fall. It is important for the Nisa business to create high barriers to

enter to deter new entrants with managing its budgeting and costs which increase its

profitability and capital.

Bargaining power of suppliers: Strong power of bargaining allows suppliers to sell law

quality products on high prices. This will affect the profitability of the firm that they have

to pay more for their materials. The Nisa firm should manage its financial position that it

can be able to purchase necessary material for operations and should try to manage the

bargaining power of suppliers which help it to manage its raw material costs.

Bargaining power of buyers: Customers have power to demand lower prices with high

quality product which affect the revenues of the firm. Buyers are price sensitive that

business should set a price which manage its revenues and quality of the products and

services effectively.

Threats of substitutes: This force especially threatening when customers finds easy

substitutes for their products with attractive prices and better quality. The Nisa business

should make its product and services unique from others with managing budget and costs

will reduce the threat of substitutes and increase the profitability. This will help business

to make its financial position good among others (Van der Stede, 2015).

Rivalry among existing competitors: This force determines, how a business is

profitable and competitive that there are so many competitors in market share. The

business CIAM should improve its growth and customer loyalty which helps it to

compete other in the market and make a goodwill of the firm.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.