Management Accounting Report: Strategies for Nisa Retail's Growth

VerifiedAdded on 2020/02/03

|24

|4708

|434

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application to Nisa Retail, a UK-based grocery store. The report covers various aspects of management accounting, including cost-volume-profit analysis, budgeting, and cash flow statements. It delves into different costing techniques like marginal and absorption costing, along with their implications for financial reporting and decision-making. The report also explores planning tools for budgetary control, compares different management accounting systems, and assesses how an entity can address financial problems. The analysis includes illustrations such as retail performance, break-even points, budgets, and ratio analyses. The report emphasizes the importance of management accounting in providing valuable insights for business decisions and improving financial performance.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explain management accounting and give essential requirements of different types of

management accounting system in the given case scenario...................................................1

P2 Explain different methods used for management accounting reporting...........................8

Task 2.............................................................................................................................................15

P3 calculate cost using different techniques by preparing income statement under marginal

and absorption costing..........................................................................................................15

TASK 3..........................................................................................................................................16

P4 Explain advantages and disadvantages of different types of planning tools for budgetary

control...................................................................................................................................16

P5 Compare how an entity adopt management accounting systems in order to deal with the

financial problems................................................................................................................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explain management accounting and give essential requirements of different types of

management accounting system in the given case scenario...................................................1

P2 Explain different methods used for management accounting reporting...........................8

Task 2.............................................................................................................................................15

P3 calculate cost using different techniques by preparing income statement under marginal

and absorption costing..........................................................................................................15

TASK 3..........................................................................................................................................16

P4 Explain advantages and disadvantages of different types of planning tools for budgetary

control...................................................................................................................................16

P5 Compare how an entity adopt management accounting systems in order to deal with the

financial problems................................................................................................................18

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

Illustration Index

Illustration 1: Retail performance....................................................................................................2

Illustration 2: BEP............................................................................................................................2

Illustration 3: Budget.......................................................................................................................4

Illustration 4: Ratio analysis............................................................................................................8

Illustration 5: Cash flow analysis...................................................................................................10

Illustration 6: Capital budgeting....................................................................................................13

Illustration 1: Retail performance....................................................................................................2

Illustration 2: BEP............................................................................................................................2

Illustration 3: Budget.......................................................................................................................4

Illustration 4: Ratio analysis............................................................................................................8

Illustration 5: Cash flow analysis...................................................................................................10

Illustration 6: Capital budgeting....................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Role of management has increases with the introduction of higher amount of

complexities in the external business environment. Nisa Retail store has been selected for this

project report which is growing gradually in boosting the overall economy of the UK. This report

focuses on management accounting systems and management accounting reporting techniques in

complying all kinds of systems fruitful for the business enterprise. Marginal and absorption

costing has been chosen by an entity in improving the business fall under retail sector in the UK.

TASK 1

P1 Explain management accounting and give essential requirements of different types of

management accounting system in the given case scenario

Background

The current sector is regarded as most important sector in the United Kingdom which

generates higher amount of sales and the revenue every year. The economy is boosted by getting

higher revenue from this particular sector which increases the overall scope of all the businesses

fall under this category (Farías, Torres and Mora Cortez, 2017). There are different kinds of

businesses involves in this sector such as furniture, food and grocery, clothing and accessories

and electronics.

Nisa retail store has been selected in the present report which is small scale entity located

in the United Kingdom. It deals in providing grocery market products or services in order to

facilitate the needs and expectations of all the consumers. Management accountant of Nisa retail

store will take important decisions for the betterment of the current business as their desired

market aim is to achieve all the aims and the objectives within a given span of time. Analytical

ability of a manager gets increases by taking important decisions in their business.

Financial perspective

1

Role of management has increases with the introduction of higher amount of

complexities in the external business environment. Nisa Retail store has been selected for this

project report which is growing gradually in boosting the overall economy of the UK. This report

focuses on management accounting systems and management accounting reporting techniques in

complying all kinds of systems fruitful for the business enterprise. Marginal and absorption

costing has been chosen by an entity in improving the business fall under retail sector in the UK.

TASK 1

P1 Explain management accounting and give essential requirements of different types of

management accounting system in the given case scenario

Background

The current sector is regarded as most important sector in the United Kingdom which

generates higher amount of sales and the revenue every year. The economy is boosted by getting

higher revenue from this particular sector which increases the overall scope of all the businesses

fall under this category (Farías, Torres and Mora Cortez, 2017). There are different kinds of

businesses involves in this sector such as furniture, food and grocery, clothing and accessories

and electronics.

Nisa retail store has been selected in the present report which is small scale entity located

in the United Kingdom. It deals in providing grocery market products or services in order to

facilitate the needs and expectations of all the consumers. Management accountant of Nisa retail

store will take important decisions for the betterment of the current business as their desired

market aim is to achieve all the aims and the objectives within a given span of time. Analytical

ability of a manager gets increases by taking important decisions in their business.

Financial perspective

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

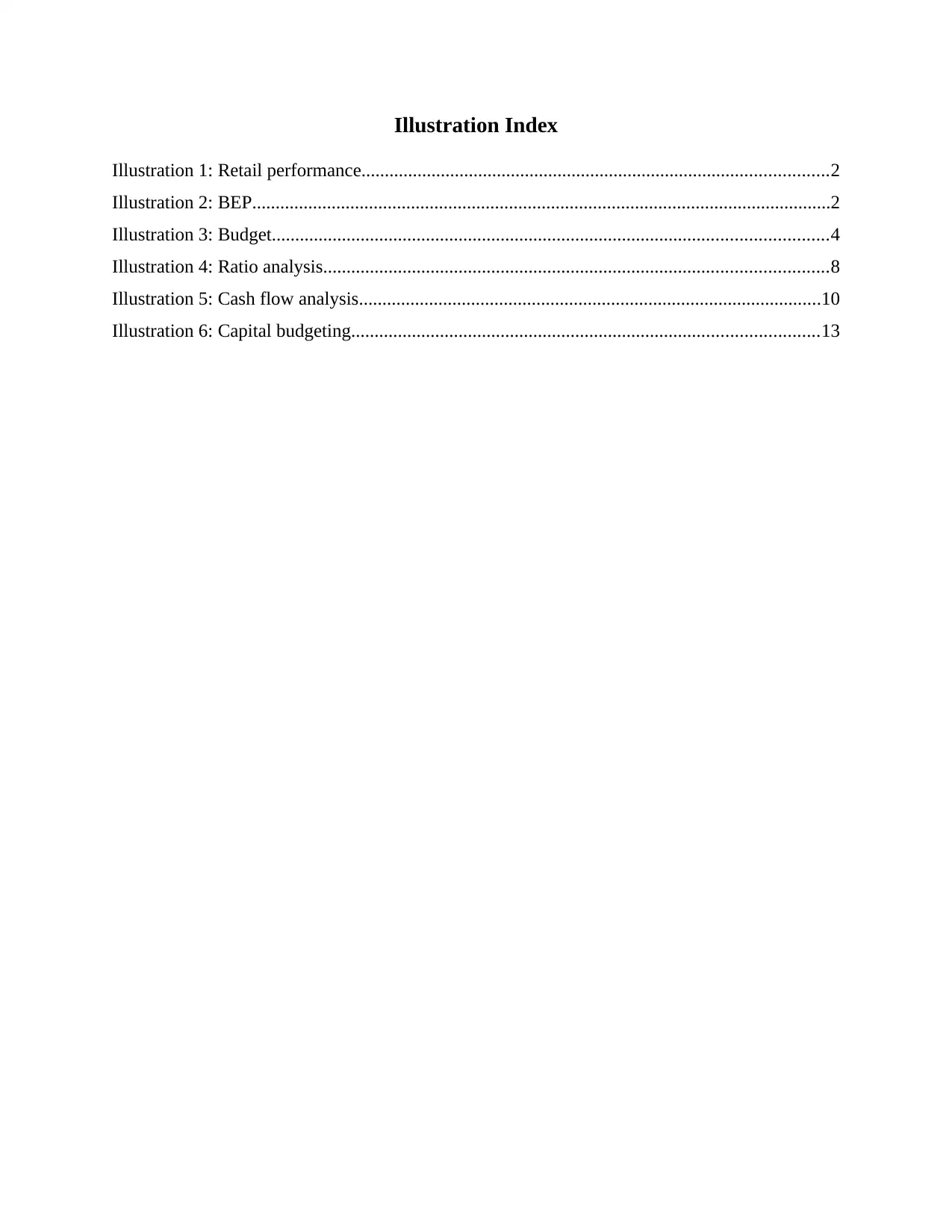

Illustration 1: Retail performance

The current business has generated higher amount of sales and the revenue from this

particular sector which helps in increasing higher scope. The scope will be increases with the

passage of time as this would help in enhancing the value of an entity in relation to its variety of

users. The recent study has revealed that this particular sector has produces 358 Billion GBP

every year. The financing goals of the economy will be accomplishes as this would attract

variety of users in investing lots of investments in different areas of business.

Employee strength

The biggest strength of this sector is an employee who represents an entity by their

actions as every wrong action will further ruin the performance of the business in the external

market. Total base of employees is 2.8 million in this retail sector which is collaboration of

various business enterprises (Tiwari and Debnath, 2017). There are 290315 number of retail

firms in this particular sector will be helpful in gathering large sum of revenue for the current

economy. It has been inferred that almost one third proportion of overall consumer spending

goes to the economy of UK through this kind of retail sector.

Illustration 2: BEP

2

The current business has generated higher amount of sales and the revenue from this

particular sector which helps in increasing higher scope. The scope will be increases with the

passage of time as this would help in enhancing the value of an entity in relation to its variety of

users. The recent study has revealed that this particular sector has produces 358 Billion GBP

every year. The financing goals of the economy will be accomplishes as this would attract

variety of users in investing lots of investments in different areas of business.

Employee strength

The biggest strength of this sector is an employee who represents an entity by their

actions as every wrong action will further ruin the performance of the business in the external

market. Total base of employees is 2.8 million in this retail sector which is collaboration of

various business enterprises (Tiwari and Debnath, 2017). There are 290315 number of retail

firms in this particular sector will be helpful in gathering large sum of revenue for the current

economy. It has been inferred that almost one third proportion of overall consumer spending

goes to the economy of UK through this kind of retail sector.

Illustration 2: BEP

2

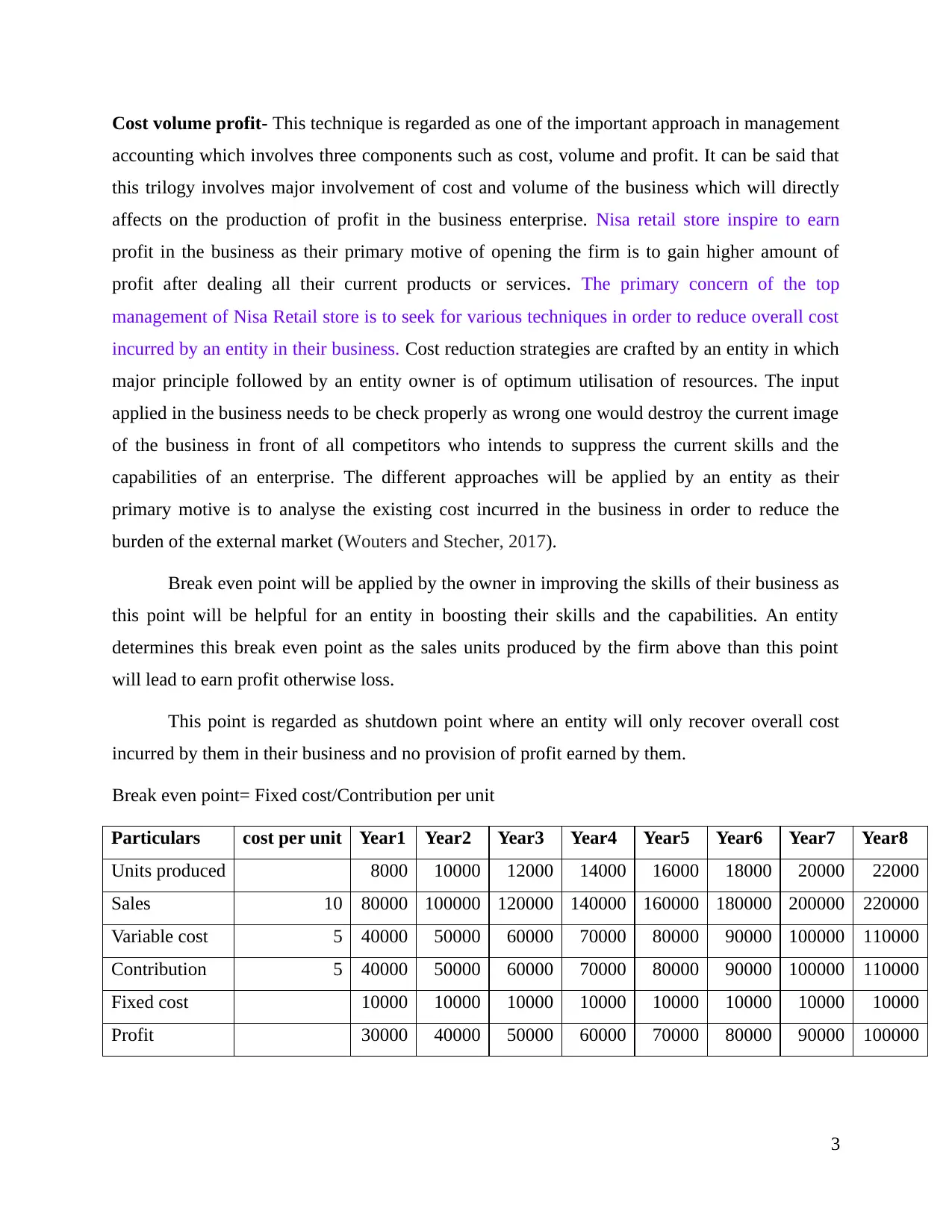

Cost volume profit- This technique is regarded as one of the important approach in management

accounting which involves three components such as cost, volume and profit. It can be said that

this trilogy involves major involvement of cost and volume of the business which will directly

affects on the production of profit in the business enterprise. Nisa retail store inspire to earn

profit in the business as their primary motive of opening the firm is to gain higher amount of

profit after dealing all their current products or services. The primary concern of the top

management of Nisa Retail store is to seek for various techniques in order to reduce overall cost

incurred by an entity in their business. Cost reduction strategies are crafted by an entity in which

major principle followed by an entity owner is of optimum utilisation of resources. The input

applied in the business needs to be check properly as wrong one would destroy the current image

of the business in front of all competitors who intends to suppress the current skills and the

capabilities of an enterprise. The different approaches will be applied by an entity as their

primary motive is to analyse the existing cost incurred in the business in order to reduce the

burden of the external market (Wouters and Stecher, 2017).

Break even point will be applied by the owner in improving the skills of their business as

this point will be helpful for an entity in boosting their skills and the capabilities. An entity

determines this break even point as the sales units produced by the firm above than this point

will lead to earn profit otherwise loss.

This point is regarded as shutdown point where an entity will only recover overall cost

incurred by them in their business and no provision of profit earned by them.

Break even point= Fixed cost/Contribution per unit

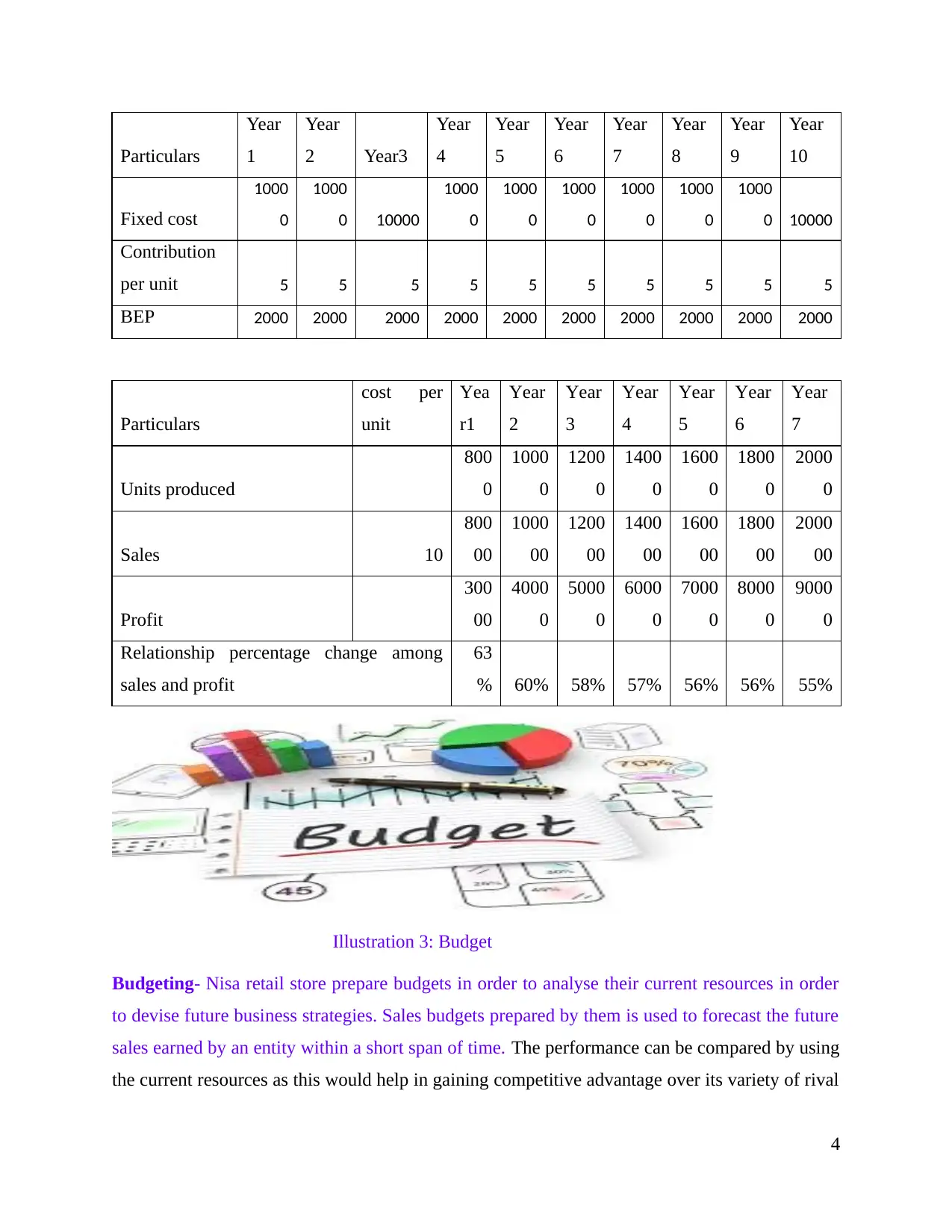

Particulars cost per unit Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8

Units produced 8000 10000 12000 14000 16000 18000 20000 22000

Sales 10 80000 100000 120000 140000 160000 180000 200000 220000

Variable cost 5 40000 50000 60000 70000 80000 90000 100000 110000

Contribution 5 40000 50000 60000 70000 80000 90000 100000 110000

Fixed cost 10000 10000 10000 10000 10000 10000 10000 10000

Profit 30000 40000 50000 60000 70000 80000 90000 100000

3

accounting which involves three components such as cost, volume and profit. It can be said that

this trilogy involves major involvement of cost and volume of the business which will directly

affects on the production of profit in the business enterprise. Nisa retail store inspire to earn

profit in the business as their primary motive of opening the firm is to gain higher amount of

profit after dealing all their current products or services. The primary concern of the top

management of Nisa Retail store is to seek for various techniques in order to reduce overall cost

incurred by an entity in their business. Cost reduction strategies are crafted by an entity in which

major principle followed by an entity owner is of optimum utilisation of resources. The input

applied in the business needs to be check properly as wrong one would destroy the current image

of the business in front of all competitors who intends to suppress the current skills and the

capabilities of an enterprise. The different approaches will be applied by an entity as their

primary motive is to analyse the existing cost incurred in the business in order to reduce the

burden of the external market (Wouters and Stecher, 2017).

Break even point will be applied by the owner in improving the skills of their business as

this point will be helpful for an entity in boosting their skills and the capabilities. An entity

determines this break even point as the sales units produced by the firm above than this point

will lead to earn profit otherwise loss.

This point is regarded as shutdown point where an entity will only recover overall cost

incurred by them in their business and no provision of profit earned by them.

Break even point= Fixed cost/Contribution per unit

Particulars cost per unit Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8

Units produced 8000 10000 12000 14000 16000 18000 20000 22000

Sales 10 80000 100000 120000 140000 160000 180000 200000 220000

Variable cost 5 40000 50000 60000 70000 80000 90000 100000 110000

Contribution 5 40000 50000 60000 70000 80000 90000 100000 110000

Fixed cost 10000 10000 10000 10000 10000 10000 10000 10000

Profit 30000 40000 50000 60000 70000 80000 90000 100000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars

Year

1

Year

2 Year3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Fixed cost

1000

0

1000

0 10000

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0 10000

Contribution

per unit 5 5 5 5 5 5 5 5 5 5

BEP 2000 2000 2000 2000 2000 2000 2000 2000 2000 2000

Particulars

cost per

unit

Yea

r1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Units produced

800

0

1000

0

1200

0

1400

0

1600

0

1800

0

2000

0

Sales 10

800

00

1000

00

1200

00

1400

00

1600

00

1800

00

2000

00

Profit

300

00

4000

0

5000

0

6000

0

7000

0

8000

0

9000

0

Relationship percentage change among

sales and profit

63

% 60% 58% 57% 56% 56% 55%

Illustration 3: Budget

Budgeting- Nisa retail store prepare budgets in order to analyse their current resources in order

to devise future business strategies. Sales budgets prepared by them is used to forecast the future

sales earned by an entity within a short span of time. The performance can be compared by using

the current resources as this would help in gaining competitive advantage over its variety of rival

4

Year

1

Year

2 Year3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Fixed cost

1000

0

1000

0 10000

1000

0

1000

0

1000

0

1000

0

1000

0

1000

0 10000

Contribution

per unit 5 5 5 5 5 5 5 5 5 5

BEP 2000 2000 2000 2000 2000 2000 2000 2000 2000 2000

Particulars

cost per

unit

Yea

r1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Units produced

800

0

1000

0

1200

0

1400

0

1600

0

1800

0

2000

0

Sales 10

800

00

1000

00

1200

00

1400

00

1600

00

1800

00

2000

00

Profit

300

00

4000

0

5000

0

6000

0

7000

0

8000

0

9000

0

Relationship percentage change among

sales and profit

63

% 60% 58% 57% 56% 56% 55%

Illustration 3: Budget

Budgeting- Nisa retail store prepare budgets in order to analyse their current resources in order

to devise future business strategies. Sales budgets prepared by them is used to forecast the future

sales earned by an entity within a short span of time. The performance can be compared by using

the current resources as this would help in gaining competitive advantage over its variety of rival

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

members in the external market. It is regarded as corporate strategy which gives ultimate

direction to different strategic business units just like budgets prepared for different business

departments of an organisation. It can be said an entity will be able to maintain perfect balance

among income and expenditure incurred by them in a particular year. The budget plan prepared

by an entity in regulating all the expenditures incurred by them in accomplishing their goals and

the objectives as their primary motive is to gain higher image in entire external market (Hiebl,

Gärtner and Duller, 2017).

Cash budget is another important statement of cash flow prepared by Nisa retail store in

order to ensure its current earnings in relation to all the expenditures incurred by them in a

particular financial year. Cash flow of future of Nisa retail store are forecasted as being a

supermarket owner they are required to analyse all the resources or inventory currently utilised in

their business in relation to the future targets of their business. Budgets prepared by an entity

will act as forecasting tool which emphasises on predicting the higher performance of the

business in relation to its external market as their primary motive is to gain the trusts of all the

employees working for the sake of an enterprise. Finance imposed by an entity in meeting their

business requirements can be tracked by preparing the budgets. These budgets can be act as

tracking system which helps an entity in order to make important decisions as delayed actions

can be rectified by preparing budgets.

Particular

s

Jan Feb Mar

ch

Apr

il

Ma

y

Jun

e

Jul

y

Au

g

Sep

t

Oct Nov Dec

Initial cash 5000

0

Bank loan 5500

0

Income

from

online

sales

3200

0

40000 3500

0

380

00

410

00

420

00

360

00

280

00

270

00

275

00

280

00

330

00

Income 2240 56400 5680 571 588 620 664 687 654 600 608 644

5

direction to different strategic business units just like budgets prepared for different business

departments of an organisation. It can be said an entity will be able to maintain perfect balance

among income and expenditure incurred by them in a particular year. The budget plan prepared

by an entity in regulating all the expenditures incurred by them in accomplishing their goals and

the objectives as their primary motive is to gain higher image in entire external market (Hiebl,

Gärtner and Duller, 2017).

Cash budget is another important statement of cash flow prepared by Nisa retail store in

order to ensure its current earnings in relation to all the expenditures incurred by them in a

particular financial year. Cash flow of future of Nisa retail store are forecasted as being a

supermarket owner they are required to analyse all the resources or inventory currently utilised in

their business in relation to the future targets of their business. Budgets prepared by an entity

will act as forecasting tool which emphasises on predicting the higher performance of the

business in relation to its external market as their primary motive is to gain the trusts of all the

employees working for the sake of an enterprise. Finance imposed by an entity in meeting their

business requirements can be tracked by preparing the budgets. These budgets can be act as

tracking system which helps an entity in order to make important decisions as delayed actions

can be rectified by preparing budgets.

Particular

s

Jan Feb Mar

ch

Apr

il

Ma

y

Jun

e

Jul

y

Au

g

Sep

t

Oct Nov Dec

Initial cash 5000

0

Bank loan 5500

0

Income

from

online

sales

3200

0

40000 3500

0

380

00

410

00

420

00

360

00

280

00

270

00

275

00

280

00

330

00

Income 2240 56400 5680 571 588 620 664 687 654 600 608 644

5

from in-

store sales

0 0 00 00 00 00 00 00 00 00 00

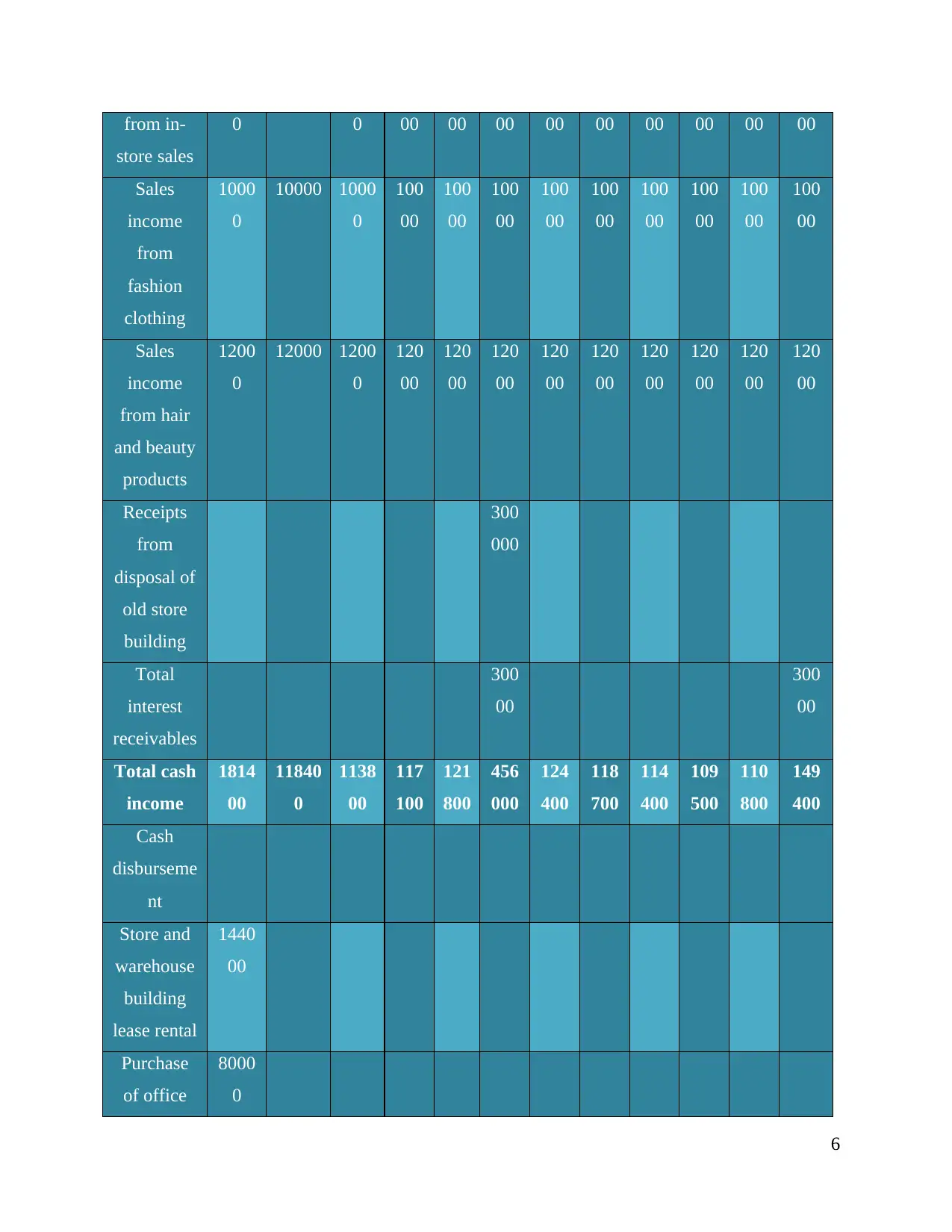

Sales

income

from

fashion

clothing

1000

0

10000 1000

0

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

Sales

income

from hair

and beauty

products

1200

0

12000 1200

0

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

Receipts

from

disposal of

old store

building

300

000

Total

interest

receivables

300

00

300

00

Total cash

income

1814

00

11840

0

1138

00

117

100

121

800

456

000

124

400

118

700

114

400

109

500

110

800

149

400

Cash

disburseme

nt

Store and

warehouse

building

lease rental

1440

00

Purchase

of office

8000

0

6

store sales

0 0 00 00 00 00 00 00 00 00 00

Sales

income

from

fashion

clothing

1000

0

10000 1000

0

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

Sales

income

from hair

and beauty

products

1200

0

12000 1200

0

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

Receipts

from

disposal of

old store

building

300

000

Total

interest

receivables

300

00

300

00

Total cash

income

1814

00

11840

0

1138

00

117

100

121

800

456

000

124

400

118

700

114

400

109

500

110

800

149

400

Cash

disburseme

nt

Store and

warehouse

building

lease rental

1440

00

Purchase

of office

8000

0

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

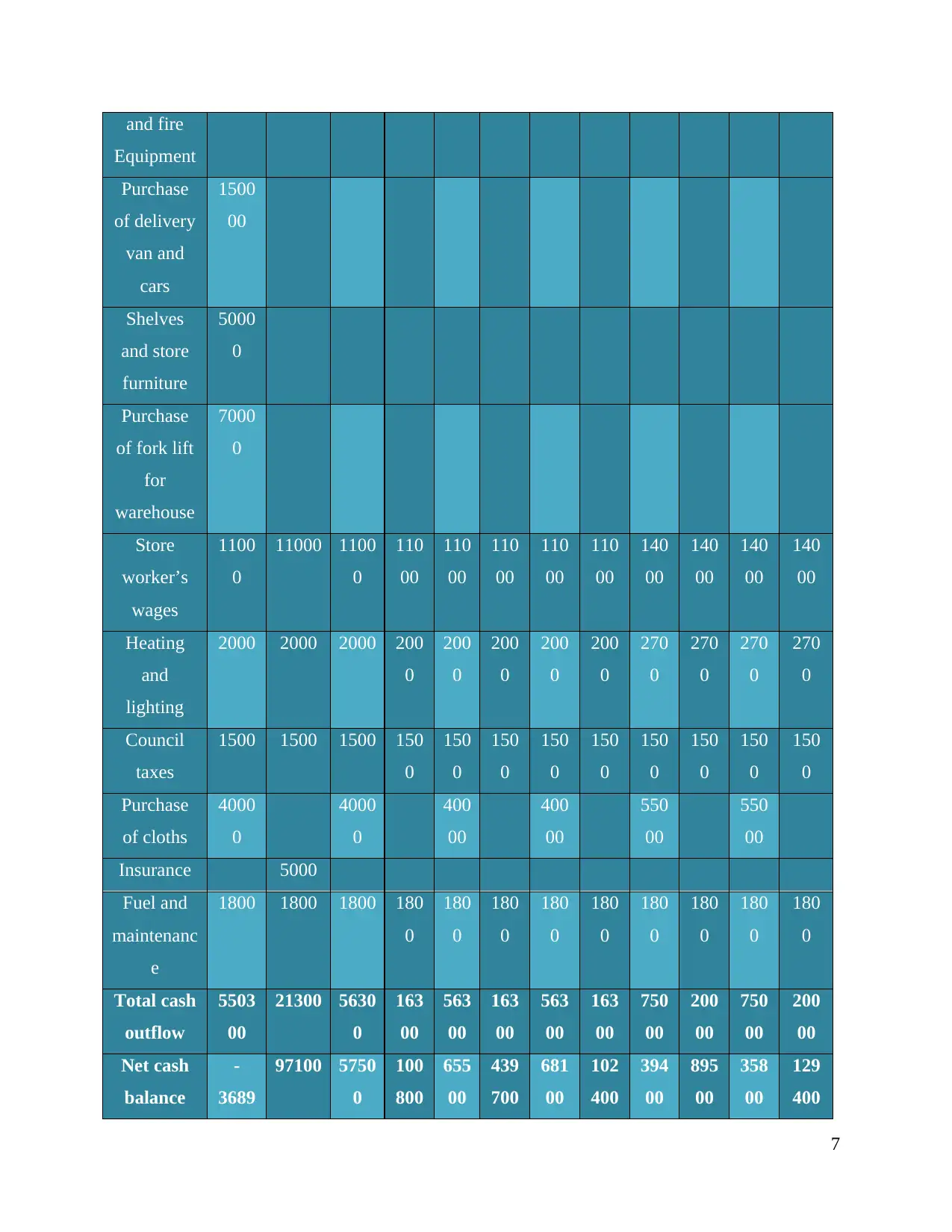

and fire

Equipment

Purchase

of delivery

van and

cars

1500

00

Shelves

and store

furniture

5000

0

Purchase

of fork lift

for

warehouse

7000

0

Store

worker’s

wages

1100

0

11000 1100

0

110

00

110

00

110

00

110

00

110

00

140

00

140

00

140

00

140

00

Heating

and

lighting

2000 2000 2000 200

0

200

0

200

0

200

0

200

0

270

0

270

0

270

0

270

0

Council

taxes

1500 1500 1500 150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

Purchase

of cloths

4000

0

4000

0

400

00

400

00

550

00

550

00

Insurance 5000

Fuel and

maintenanc

e

1800 1800 1800 180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

Total cash

outflow

5503

00

21300 5630

0

163

00

563

00

163

00

563

00

163

00

750

00

200

00

750

00

200

00

Net cash

balance

-

3689

97100 5750

0

100

800

655

00

439

700

681

00

102

400

394

00

895

00

358

00

129

400

7

Equipment

Purchase

of delivery

van and

cars

1500

00

Shelves

and store

furniture

5000

0

Purchase

of fork lift

for

warehouse

7000

0

Store

worker’s

wages

1100

0

11000 1100

0

110

00

110

00

110

00

110

00

110

00

140

00

140

00

140

00

140

00

Heating

and

lighting

2000 2000 2000 200

0

200

0

200

0

200

0

200

0

270

0

270

0

270

0

270

0

Council

taxes

1500 1500 1500 150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

Purchase

of cloths

4000

0

4000

0

400

00

400

00

550

00

550

00

Insurance 5000

Fuel and

maintenanc

e

1800 1800 1800 180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

Total cash

outflow

5503

00

21300 5630

0

163

00

563

00

163

00

563

00

163

00

750

00

200

00

750

00

200

00

Net cash

balance

-

3689

97100 5750

0

100

800

655

00

439

700

681

00

102

400

394

00

895

00

358

00

129

400

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

00

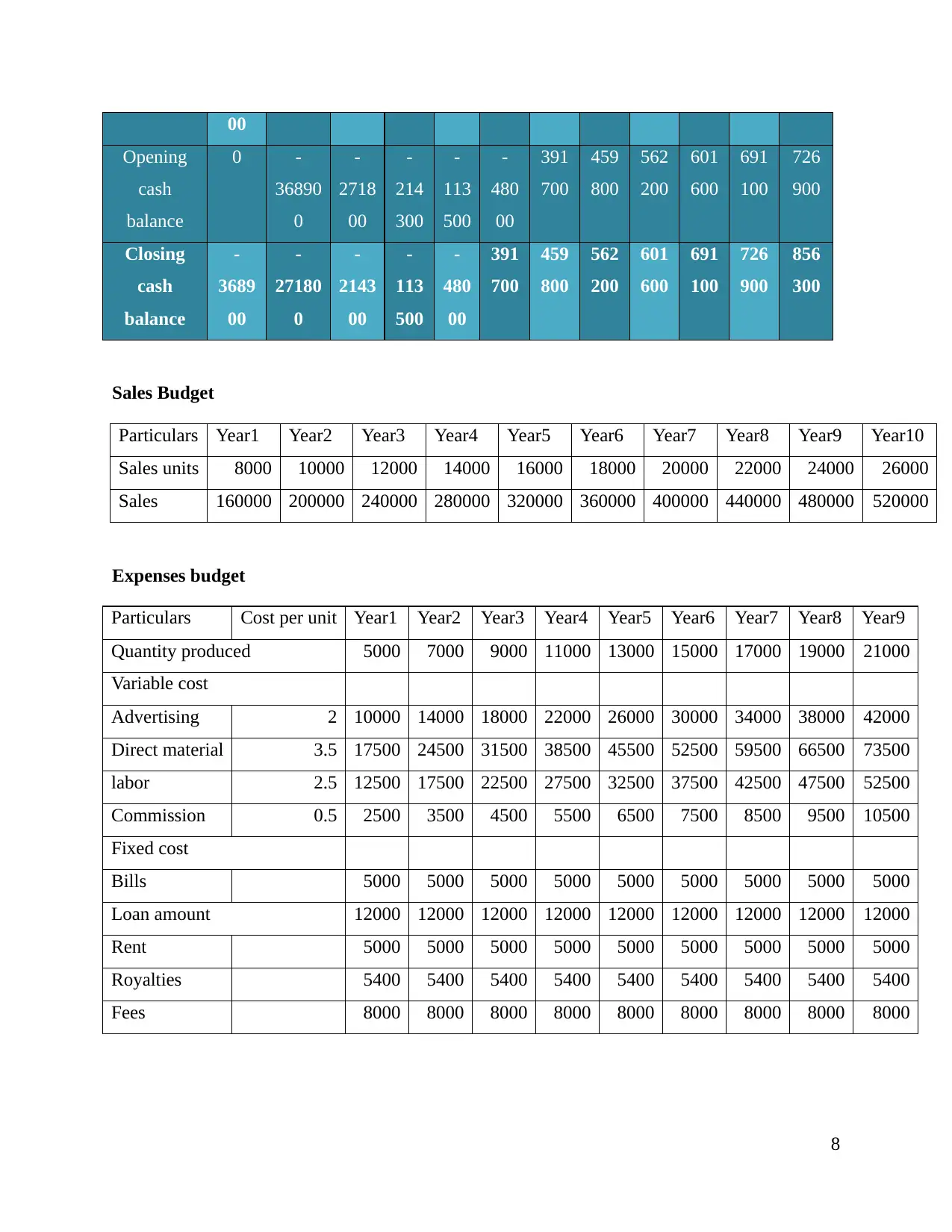

Opening

cash

balance

0 -

36890

0

-

2718

00

-

214

300

-

113

500

-

480

00

391

700

459

800

562

200

601

600

691

100

726

900

Closing

cash

balance

-

3689

00

-

27180

0

-

2143

00

-

113

500

-

480

00

391

700

459

800

562

200

601

600

691

100

726

900

856

300

Sales Budget

Particulars Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9 Year10

Sales units 8000 10000 12000 14000 16000 18000 20000 22000 24000 26000

Sales 160000 200000 240000 280000 320000 360000 400000 440000 480000 520000

Expenses budget

Particulars Cost per unit Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9

Quantity produced 5000 7000 9000 11000 13000 15000 17000 19000 21000

Variable cost

Advertising 2 10000 14000 18000 22000 26000 30000 34000 38000 42000

Direct material 3.5 17500 24500 31500 38500 45500 52500 59500 66500 73500

labor 2.5 12500 17500 22500 27500 32500 37500 42500 47500 52500

Commission 0.5 2500 3500 4500 5500 6500 7500 8500 9500 10500

Fixed cost

Bills 5000 5000 5000 5000 5000 5000 5000 5000 5000

Loan amount 12000 12000 12000 12000 12000 12000 12000 12000 12000

Rent 5000 5000 5000 5000 5000 5000 5000 5000 5000

Royalties 5400 5400 5400 5400 5400 5400 5400 5400 5400

Fees 8000 8000 8000 8000 8000 8000 8000 8000 8000

8

Opening

cash

balance

0 -

36890

0

-

2718

00

-

214

300

-

113

500

-

480

00

391

700

459

800

562

200

601

600

691

100

726

900

Closing

cash

balance

-

3689

00

-

27180

0

-

2143

00

-

113

500

-

480

00

391

700

459

800

562

200

601

600

691

100

726

900

856

300

Sales Budget

Particulars Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9 Year10

Sales units 8000 10000 12000 14000 16000 18000 20000 22000 24000 26000

Sales 160000 200000 240000 280000 320000 360000 400000 440000 480000 520000

Expenses budget

Particulars Cost per unit Year1 Year2 Year3 Year4 Year5 Year6 Year7 Year8 Year9

Quantity produced 5000 7000 9000 11000 13000 15000 17000 19000 21000

Variable cost

Advertising 2 10000 14000 18000 22000 26000 30000 34000 38000 42000

Direct material 3.5 17500 24500 31500 38500 45500 52500 59500 66500 73500

labor 2.5 12500 17500 22500 27500 32500 37500 42500 47500 52500

Commission 0.5 2500 3500 4500 5500 6500 7500 8500 9500 10500

Fixed cost

Bills 5000 5000 5000 5000 5000 5000 5000 5000 5000

Loan amount 12000 12000 12000 12000 12000 12000 12000 12000 12000

Rent 5000 5000 5000 5000 5000 5000 5000 5000 5000

Royalties 5400 5400 5400 5400 5400 5400 5400 5400 5400

Fees 8000 8000 8000 8000 8000 8000 8000 8000 8000

8

P2 Explain different methods used for management accounting reporting

Financial accounting method

Illustration 4: Ratio analysis

Ratio analysis- Comparative performance measurement tool that analysed the current

performance of an enterprise in accordance with its previous year performance in uplifting their

current conditions of the business. The ratio analysis is widely used technique of assessing the

current financial statements. Different forms of financial statement of several stores of Nisa retail

store are compared in relation to the headquarter of its supermarket to determine their current

performance. Income statement of all the stores contain sales and the revenue which are

compared in relation to the common goals framed by the main branch of the supermarket store in

order to ascertain the financial performance in order to gain higher competitive advantage.

Different variety of the ratio analysis states that it ascertains the performance of the business in

relation to various parameters such as profitability and liquidity (Müller-Stewens and Möller,

2017). The favourable or adverse results of all these ratios to the notice of the management as the

adverse results can be rectified by the management by making important decisions in order to

regulate their performance. The performance of an entity can be managed or regulated by

removing the causes of incurring adverse ratios. The deficiency from the management can be

rectified by focusing on capabilities of the business as an enterprise owner focuses on reducing

their weaknesses. Cost of sales and taxation are those deficiencies that reduce the capability of an

entity which will be regulated. On the other hand, liquidity is essential for the management as

expenses incurred in the business can be managed

Profitability ratios

Particulars Formula 2015 2016

9

Financial accounting method

Illustration 4: Ratio analysis

Ratio analysis- Comparative performance measurement tool that analysed the current

performance of an enterprise in accordance with its previous year performance in uplifting their

current conditions of the business. The ratio analysis is widely used technique of assessing the

current financial statements. Different forms of financial statement of several stores of Nisa retail

store are compared in relation to the headquarter of its supermarket to determine their current

performance. Income statement of all the stores contain sales and the revenue which are

compared in relation to the common goals framed by the main branch of the supermarket store in

order to ascertain the financial performance in order to gain higher competitive advantage.

Different variety of the ratio analysis states that it ascertains the performance of the business in

relation to various parameters such as profitability and liquidity (Müller-Stewens and Möller,

2017). The favourable or adverse results of all these ratios to the notice of the management as the

adverse results can be rectified by the management by making important decisions in order to

regulate their performance. The performance of an entity can be managed or regulated by

removing the causes of incurring adverse ratios. The deficiency from the management can be

rectified by focusing on capabilities of the business as an enterprise owner focuses on reducing

their weaknesses. Cost of sales and taxation are those deficiencies that reduce the capability of an

entity which will be regulated. On the other hand, liquidity is essential for the management as

expenses incurred in the business can be managed

Profitability ratios

Particulars Formula 2015 2016

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.