Financial Analysis and Management Report: Nissan's Performance

VerifiedAdded on 2022/11/28

|16

|2494

|416

Report

AI Summary

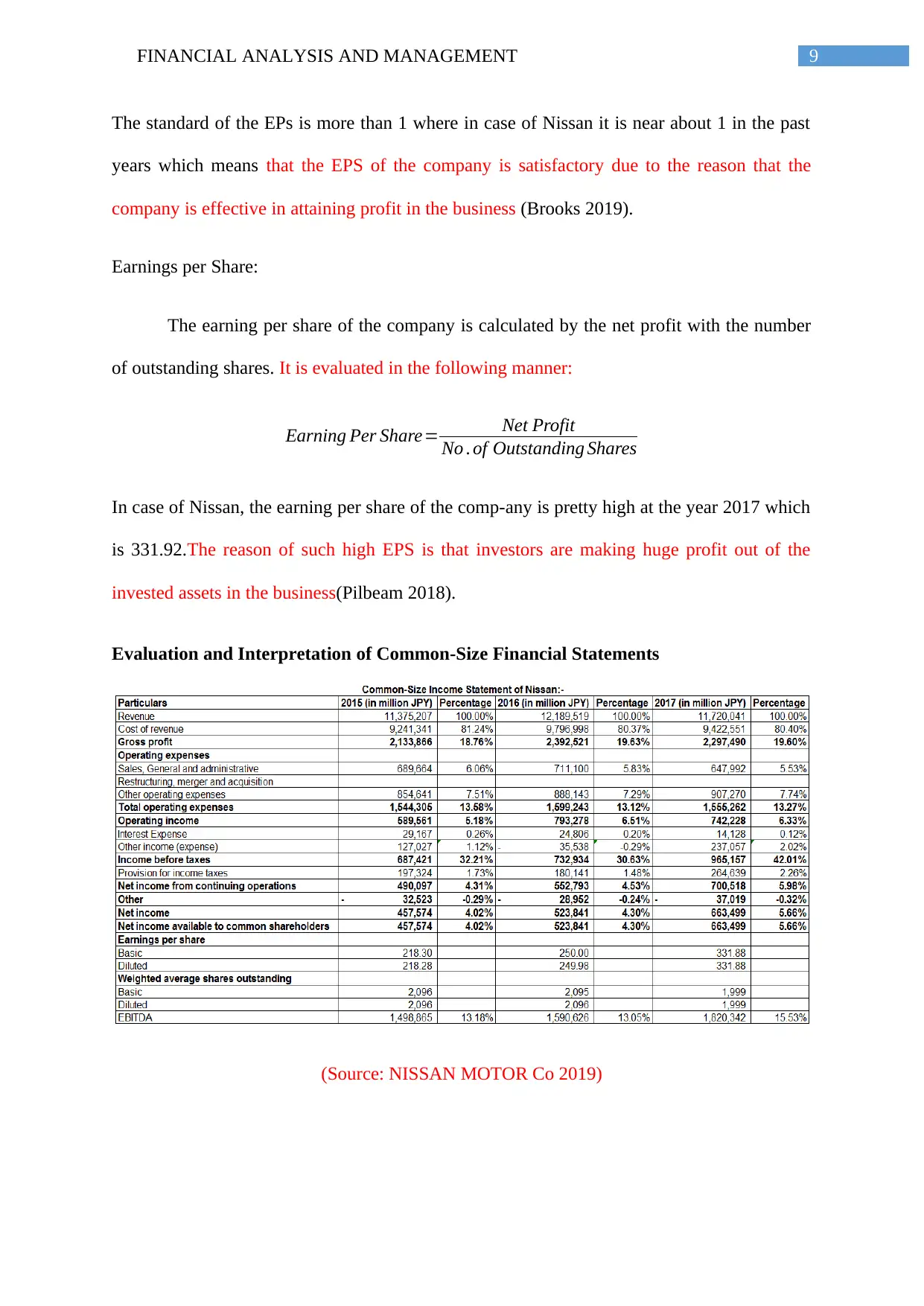

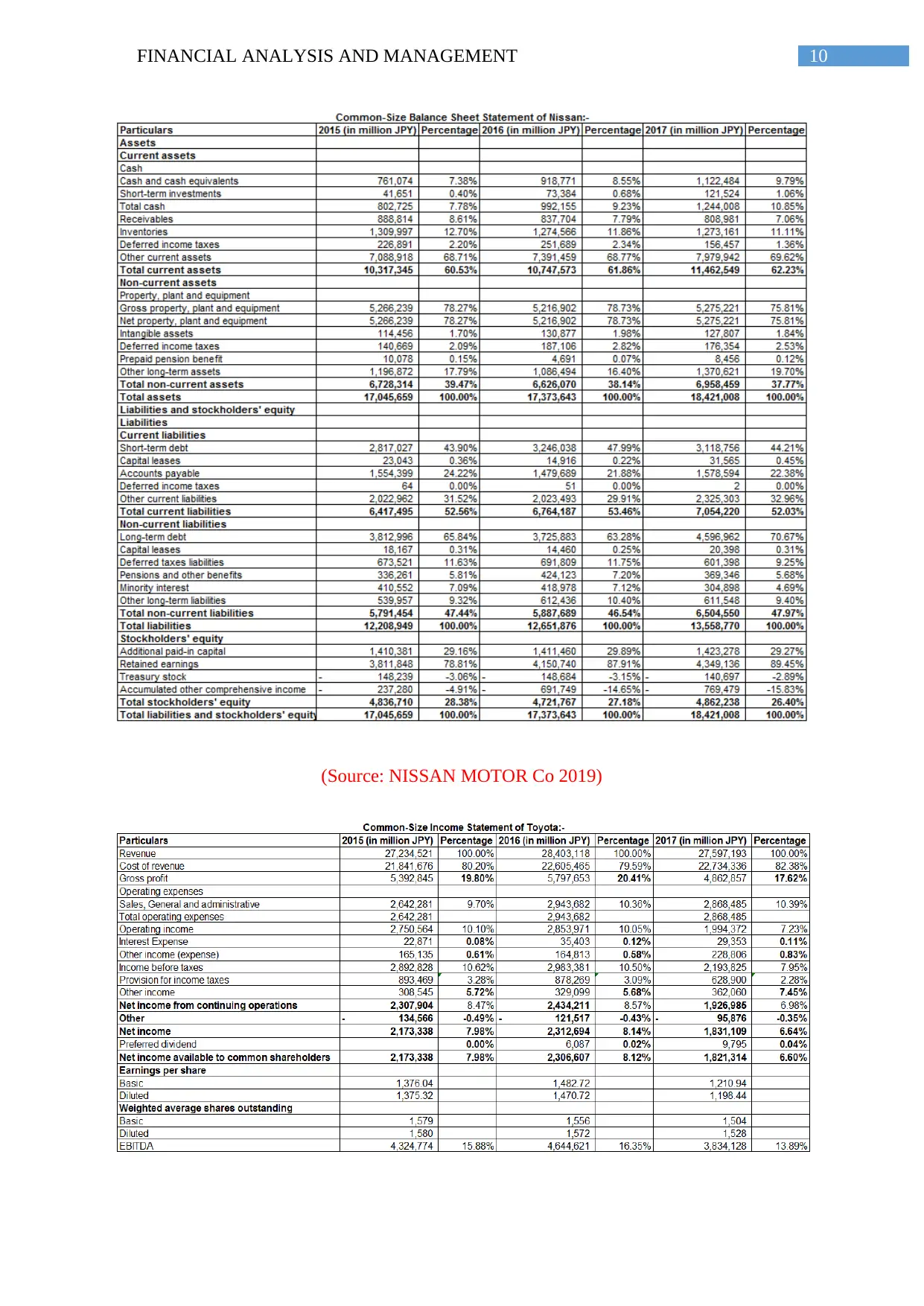

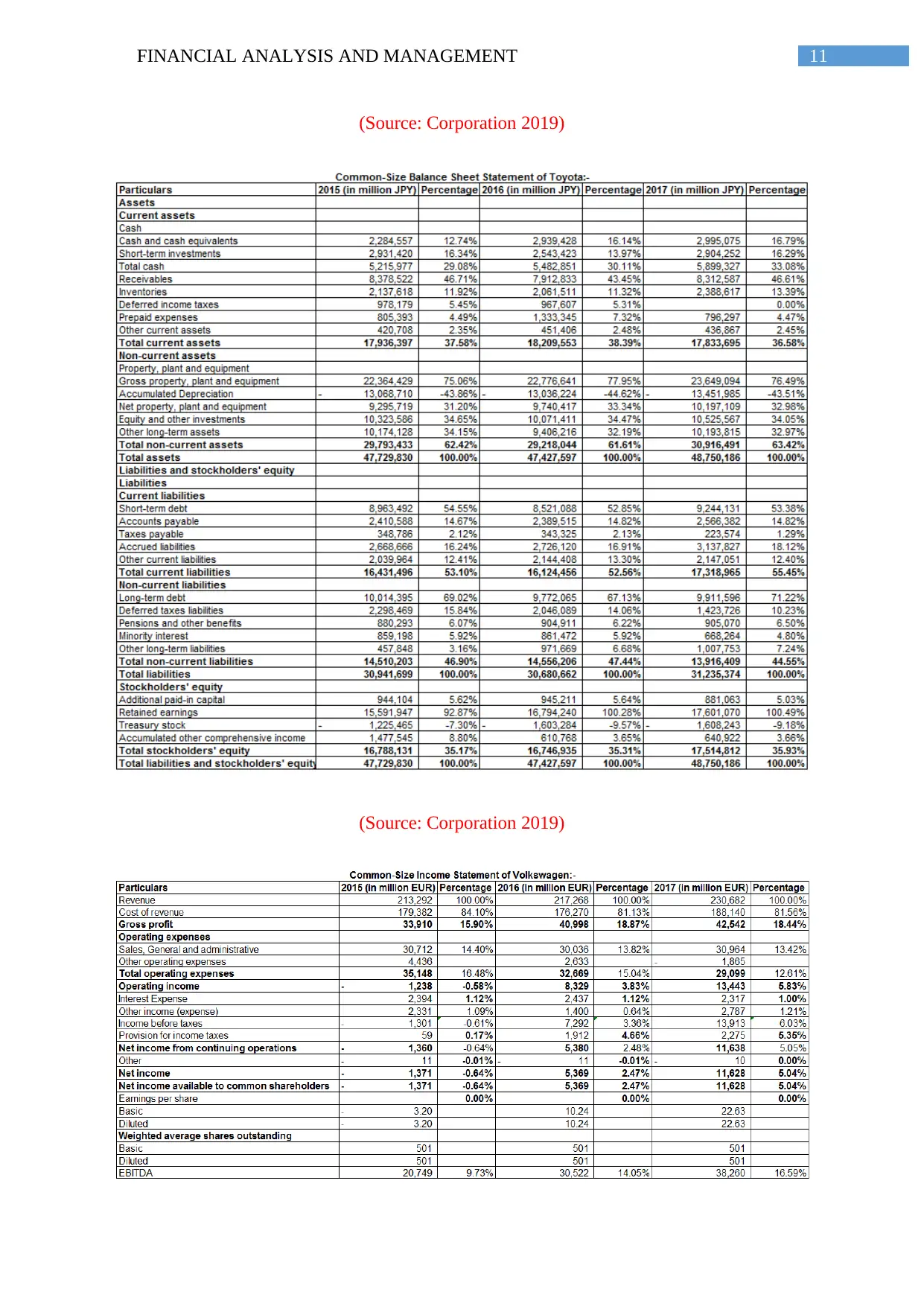

This report provides a comprehensive financial analysis of Nissan's performance from 2015 to 2017, fulfilling the requirements of a Financial Analysis and Management assignment. It begins with a background on Nissan, outlining its corporate objectives, key opportunities, and challenges. The core of the report involves an evaluation of Nissan's financial statements, calculating and interpreting key financial ratios such as gross profit margin, operating profit margin, net profit margin, current ratio, acid-test ratio, inventory turnover, debtor’s turnover, creditor’s turnover, return on asset, gearing ratio, interest coverage ratio, price-earnings ratio, and earnings per share. The report also includes a comparative analysis using common-size financial statements, comparing Nissan's performance to Toyota and Volkswagen. The analysis provides insights into the company's financial health, profitability, liquidity, and solvency, culminating in a conclusion summarizing Nissan's financial strengths and weaknesses, along with recommendations for future strategic improvements. The report is written as a consultant's analysis for potential investors.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.