Financial Decision Making Report: Analysis of Panini Ltd's Finances

VerifiedAdded on 2023/06/10

|12

|3345

|376

Report

AI Summary

This report delves into the financial decision-making processes of Panini Ltd, a bread manufacturing company. It begins with an overview of the accounting and finance departments, outlining their respective functions, including financial accounting, management accounting, tax, auditing, investment, financing, dividend, and working capital functions. The report then explores potential sources of finance available to the company for expansion. Subsequently, it undertakes a detailed financial analysis, calculating and interpreting eight key financial ratios for both 2018 and 2019, including gross profit margin, operating profit margin, return on capital employed, current ratio, quick ratio, inventory turnover days, debtor’s collection period, and creditor’s collection period. The analysis provides insights into the company's profitability, liquidity, and efficiency, offering a comprehensive view of its financial performance and decision-making.

Financial decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Task 1...............................................................................................................................................3

Part a: Accounting and Finance Department...............................................................................3

Part b: Sources of finance............................................................................................................6

Task 2...............................................................................................................................................7

Part a: Calculating the ratios:.......................................................................................................7

Part b: Analysing the numerical results.......................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Task 1...............................................................................................................................................3

Part a: Accounting and Finance Department...............................................................................3

Part b: Sources of finance............................................................................................................6

Task 2...............................................................................................................................................7

Part a: Calculating the ratios:.......................................................................................................7

Part b: Analysing the numerical results.......................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION

Financial decisions are concerned with undertaking of the decisions that are related to the

effective procurement and allocation of funds by the business organization to earn return and

maximize the wealth of the shareholders. The report will highlight the importance and functions

of the accounting and finance department Panini ltd is a manufacturing company that

manufactures bread and supplies it in the supermarkets of United Kingdom. In this report the

various sources using which medium sized firms acquire funds will be outlined. Various

accounting ratios will be calculated and analysed in this report.

MAIN BODY

Task 1

Part a: Accounting and Finance Department

Accounting Department: The accounting department of the company is responsible for

preparing financial statements, general ledger maintenance, bill payments, customer invoice

preparation, cost accounting, payments to the employees etc. All the economic matters are the

areas that concerns the accounting department of the organization. Accounting department is

present in organization of all levels and sizes (Osakwe and Otuo, 2022). The accounting

department is usually managed and controlled by a controller who reports the chief financial

officer of the organization. Below is the list of the functions that the accounting department is

responsible for in an organization:

a) Financial Accounting Function: Accounting department of the organization performs all

the financial accounting functions. Through financial accounting functions measuring,

processing and communicative functions of the financial information are carried out.

Financial accounting function of accounting department is concerned with all the basic

accounting functions that are identifying, recording, summarizing and analysing the daily

business transactions. This function involves preparing financial statements that are

meant to be used by the various stakeholders for different purposes that concerns them.

b) Management Accounting Function: The management accounting function of accounting

department is concerned with providing the information for the financial and non-

financial decisions that are to be taken by the managers in the daily course of their

business activities (Javed and Zhuquan, 2018). Accounting department gives the

accounting information that provides the provision for the managers to undertake better

Financial decisions are concerned with undertaking of the decisions that are related to the

effective procurement and allocation of funds by the business organization to earn return and

maximize the wealth of the shareholders. The report will highlight the importance and functions

of the accounting and finance department Panini ltd is a manufacturing company that

manufactures bread and supplies it in the supermarkets of United Kingdom. In this report the

various sources using which medium sized firms acquire funds will be outlined. Various

accounting ratios will be calculated and analysed in this report.

MAIN BODY

Task 1

Part a: Accounting and Finance Department

Accounting Department: The accounting department of the company is responsible for

preparing financial statements, general ledger maintenance, bill payments, customer invoice

preparation, cost accounting, payments to the employees etc. All the economic matters are the

areas that concerns the accounting department of the organization. Accounting department is

present in organization of all levels and sizes (Osakwe and Otuo, 2022). The accounting

department is usually managed and controlled by a controller who reports the chief financial

officer of the organization. Below is the list of the functions that the accounting department is

responsible for in an organization:

a) Financial Accounting Function: Accounting department of the organization performs all

the financial accounting functions. Through financial accounting functions measuring,

processing and communicative functions of the financial information are carried out.

Financial accounting function of accounting department is concerned with all the basic

accounting functions that are identifying, recording, summarizing and analysing the daily

business transactions. This function involves preparing financial statements that are

meant to be used by the various stakeholders for different purposes that concerns them.

b) Management Accounting Function: The management accounting function of accounting

department is concerned with providing the information for the financial and non-

financial decisions that are to be taken by the managers in the daily course of their

business activities (Javed and Zhuquan, 2018). Accounting department gives the

accounting information that provides the provision for the managers to undertake better

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decisions that ensures better management and control over the functions within the

organization. Through the management accounting function, the accounting department

provides the data it prepares while performing the accounting function and modifies it for

communicating the information to the management. Information to the management is

communicated by proper analysis and interpretation of the data. By this function the

accounting department provides qualitative information in addition to the quantitative

information. Management accounting function of accounting department provides

assistance in planning, organizing and decision making process to the management of the

organization. Goals are set up and plans are made for the optimum economic actions and

employee performances are also measured. These are done in order to increase the overall

efficiency of the employees and motivate them. In this function the department

coordinates and controls the entire activities of the business entity.

c) Tax Function: The tax accounting function of accounting department is concerned with

the look after of all the rules following which the taxes are generated. Tax transactions

may result in creation of tax assets or tax liabilities both are recorded the books of

accounts (Jędrzejka, 2019). Internal revenue code is the origin from which the tax

accounting is derived. Sometimes it may happen that the figures generated by the tax

accounting may be different from the income statement of the organization. The

difference is because of the fact that the tax rules, enacted may get speedily or delayed

the recognizing certain type of expenses and generally should be recognized within a

reporting period. This function of accounting department is essential from the legal

perspective of the business entity.

d) Auditing Function: The auditing function of accounting department requires the

information from the financial statements that are prepared during financial accounting

function of the accounting department. The work performed in the financial accounting

function is basically verified by the auditing function of the accounting department. By

this function it is ensured that the financial statements that were prepared represents the

true position of the financial position of the company. The accounting department of the

specific organization performs the internal audit type of the audits. There is a vast range

of functions that are performed by the accounting department auditing is one function

organization. Through the management accounting function, the accounting department

provides the data it prepares while performing the accounting function and modifies it for

communicating the information to the management. Information to the management is

communicated by proper analysis and interpretation of the data. By this function the

accounting department provides qualitative information in addition to the quantitative

information. Management accounting function of accounting department provides

assistance in planning, organizing and decision making process to the management of the

organization. Goals are set up and plans are made for the optimum economic actions and

employee performances are also measured. These are done in order to increase the overall

efficiency of the employees and motivate them. In this function the department

coordinates and controls the entire activities of the business entity.

c) Tax Function: The tax accounting function of accounting department is concerned with

the look after of all the rules following which the taxes are generated. Tax transactions

may result in creation of tax assets or tax liabilities both are recorded the books of

accounts (Jędrzejka, 2019). Internal revenue code is the origin from which the tax

accounting is derived. Sometimes it may happen that the figures generated by the tax

accounting may be different from the income statement of the organization. The

difference is because of the fact that the tax rules, enacted may get speedily or delayed

the recognizing certain type of expenses and generally should be recognized within a

reporting period. This function of accounting department is essential from the legal

perspective of the business entity.

d) Auditing Function: The auditing function of accounting department requires the

information from the financial statements that are prepared during financial accounting

function of the accounting department. The work performed in the financial accounting

function is basically verified by the auditing function of the accounting department. By

this function it is ensured that the financial statements that were prepared represents the

true position of the financial position of the company. The accounting department of the

specific organization performs the internal audit type of the audits. There is a vast range

of functions that are performed by the accounting department auditing is one function

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

from that. Through auditing function accounting department verifies the financial

information for the accuracy.

Finance Department: The finance department at an organization is responsible for the

effective management of working capital more specifically, cash resources that are available

with the company. The department performs the supervisory tasks for managing the accounting

and produce the information vital for managerial control. Financial indicators and margin

calculations are performed by the finance department.

a) Investment Function: The investment function of the finance department is concerned

with the investment decision. One of the main function of the finance department is to

decide where to allocate the limited funds of the business organization to have maximum

benefits. The decision that is taken by the finance department in this particular function is

also known as capital budgeting decision (Okodo, Momoh and Yahaya, 2019). Those

assets are chosen to be invested in that will have maximum future benefits. This function

evaluates the projects in terms of the profitability it has. The most important part in this

function is that the uncertainty of the future makes it difficult to calculate the returns that

are expected from the investment projects.

b) Financing Function; The function evolves around the financial decision undertaking. The

financial manager of the financial department of the organization takes financial decision

as a part of financial function of the department. In the financial decision it is decided

that when, from where and how will the funds be acquired for the fulfilment of the

business needs. Every business performs various kinds of activities that require funds for

their completion. There are various ways using which funds can be acquired. Mainly

there are two broad categories equity and debt. The ratio of equity and debt in the capital

structure of the business entity is decided by the financial department of the business

organization. The main focus of the financial department through this function is to

maximize the wealth of the shareholders. Wealth of the shareholders increases when the

market price of the shares rises. So this function tends to benefit from such situation. The

other source to raise funds is debt. The debt source is riskier as raising funds through this

sources increases the amount of fixed obligation for the firm. but it also results in

information for the accuracy.

Finance Department: The finance department at an organization is responsible for the

effective management of working capital more specifically, cash resources that are available

with the company. The department performs the supervisory tasks for managing the accounting

and produce the information vital for managerial control. Financial indicators and margin

calculations are performed by the finance department.

a) Investment Function: The investment function of the finance department is concerned

with the investment decision. One of the main function of the finance department is to

decide where to allocate the limited funds of the business organization to have maximum

benefits. The decision that is taken by the finance department in this particular function is

also known as capital budgeting decision (Okodo, Momoh and Yahaya, 2019). Those

assets are chosen to be invested in that will have maximum future benefits. This function

evaluates the projects in terms of the profitability it has. The most important part in this

function is that the uncertainty of the future makes it difficult to calculate the returns that

are expected from the investment projects.

b) Financing Function; The function evolves around the financial decision undertaking. The

financial manager of the financial department of the organization takes financial decision

as a part of financial function of the department. In the financial decision it is decided

that when, from where and how will the funds be acquired for the fulfilment of the

business needs. Every business performs various kinds of activities that require funds for

their completion. There are various ways using which funds can be acquired. Mainly

there are two broad categories equity and debt. The ratio of equity and debt in the capital

structure of the business entity is decided by the financial department of the business

organization. The main focus of the financial department through this function is to

maximize the wealth of the shareholders. Wealth of the shareholders increases when the

market price of the shares rises. So this function tends to benefit from such situation. The

other source to raise funds is debt. The debt source is riskier as raising funds through this

sources increases the amount of fixed obligation for the firm. but it also results in

increasing the market price of the shares. The main task of financial department by this

function is to maximize the wealth of the shareholders at the minimum level of risk.

c) Dividend Function: The financial department with this function deals with the taking up

the decision regarding the distribution of the dividends. Pay-out ratio that is optimum or

best suited for the firm is decided in this function. A frim may decide to keep its pay-out

ratio equals to zero meaning that no dividend will be distributed among the shareholders.

The entire earnings after interest and tax may be retained in the organization if it expects

that the cost of capital will be lower than the returns that will be generated from investing

the amount earned instead of distribution of dividends (Smith, 2018). The pay-out ratio

can be decided to be kept as a hundred percent, meaning all the earnings after interest and

tax payment to be distributed as dividend among the shareholders if the cost of capital is

assumed to be high than the returns that will come through investing the amount. The

financial department can alternatively decide that the mix of both is more suitable.

Optimum dividend policy is decided by the finance department in this function.

d) Working Capital Function: Working capital function is concerned with deciding the

liquidity of the firm. Liquidity position is needed to be maintained in order to avoid the

insolvency of the organization. Insolvency is a situation where the firm finds itself unable

to pay for its short term obligations. Working capital function is used to decide the

amount of cash that the company decides to maintain in cash form and invest in the

current assets for the firm. There are three types of situations that can followed while

making this decision. The stringent policy is followed when the entity believes in

investing in the current assets are rather than keeping funds in the liquid / cash form.

Following the lenient policy firm may decide that it will keep the funds in liquid form

more and invest comparatively less in the current assets of the business. By this function

of working capital the financial department of the business entity decides to keep the

liquidity of the firm balance such that it is sufficient enough to pay for the short term

obligations and also maintains an adequate level of inventory.

Part b: Sources of finance

Retained Profit: In this source of finance the business enterprise earns the profit but does

not distribute it among its shareholders. The earnings that are kept within the business and is not

distributed among the shareholders is termed as retained earnings. A firm may do so as a part of

function is to maximize the wealth of the shareholders at the minimum level of risk.

c) Dividend Function: The financial department with this function deals with the taking up

the decision regarding the distribution of the dividends. Pay-out ratio that is optimum or

best suited for the firm is decided in this function. A frim may decide to keep its pay-out

ratio equals to zero meaning that no dividend will be distributed among the shareholders.

The entire earnings after interest and tax may be retained in the organization if it expects

that the cost of capital will be lower than the returns that will be generated from investing

the amount earned instead of distribution of dividends (Smith, 2018). The pay-out ratio

can be decided to be kept as a hundred percent, meaning all the earnings after interest and

tax payment to be distributed as dividend among the shareholders if the cost of capital is

assumed to be high than the returns that will come through investing the amount. The

financial department can alternatively decide that the mix of both is more suitable.

Optimum dividend policy is decided by the finance department in this function.

d) Working Capital Function: Working capital function is concerned with deciding the

liquidity of the firm. Liquidity position is needed to be maintained in order to avoid the

insolvency of the organization. Insolvency is a situation where the firm finds itself unable

to pay for its short term obligations. Working capital function is used to decide the

amount of cash that the company decides to maintain in cash form and invest in the

current assets for the firm. There are three types of situations that can followed while

making this decision. The stringent policy is followed when the entity believes in

investing in the current assets are rather than keeping funds in the liquid / cash form.

Following the lenient policy firm may decide that it will keep the funds in liquid form

more and invest comparatively less in the current assets of the business. By this function

of working capital the financial department of the business entity decides to keep the

liquidity of the firm balance such that it is sufficient enough to pay for the short term

obligations and also maintains an adequate level of inventory.

Part b: Sources of finance

Retained Profit: In this source of finance the business enterprise earns the profit but does

not distribute it among its shareholders. The earnings that are kept within the business and is not

distributed among the shareholders is termed as retained earnings. A firm may do so as a part of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

its dividend policy. The decision to retain the profits instead to distributing it among the

shareholders is taken for the purpose of reinvesting the amount in some business investment

project (Amornkitvikai and Harvie, 2018). The source is considered best for expansion purpose

as no interest charges incur on this type of business source to acquire funds.

Share Issue: In order to raise fund, the firm may use external source and raise funds by

issuing share in the market. In this source the company sells its ownership in exchange of money.

Task 2

Part a: Calculating the ratios:

(i) Gross Profit Margin

Panini limited

Particulars Formula 2019 2018

Gross Profit Ratio

Gross Profit/Net Sales X

100 28.39%

35.00

%

Gross Profit 3265 3500

Sales 11500 10000

(ii) Operating profit margin

Panini limited

Particulars Formula 2019 2018

Operating Profit Ratio

Operating Profit/Net Sales

X 100 20.04%

27.65

%

Operating Profit 2305 2765

Sales 11500 10000

(iii) Return on Capital employed

Panini limited

Particulars Formula 2019 2018

Return on Capital

Employed Ratio

Net Profit after Taxes/

Gross Capital Employed X

100 12.30%

23.13

%

Net Profit after Taxes 1256 2025

Gross Capital Employed

Total Assets – Current

Liabilities 10211 8755

Total Assets

Noncurrent assets + current

assets 10723 9725

Non-current assets 8613 8550

Current Assets 2110 1175

shareholders is taken for the purpose of reinvesting the amount in some business investment

project (Amornkitvikai and Harvie, 2018). The source is considered best for expansion purpose

as no interest charges incur on this type of business source to acquire funds.

Share Issue: In order to raise fund, the firm may use external source and raise funds by

issuing share in the market. In this source the company sells its ownership in exchange of money.

Task 2

Part a: Calculating the ratios:

(i) Gross Profit Margin

Panini limited

Particulars Formula 2019 2018

Gross Profit Ratio

Gross Profit/Net Sales X

100 28.39%

35.00

%

Gross Profit 3265 3500

Sales 11500 10000

(ii) Operating profit margin

Panini limited

Particulars Formula 2019 2018

Operating Profit Ratio

Operating Profit/Net Sales

X 100 20.04%

27.65

%

Operating Profit 2305 2765

Sales 11500 10000

(iii) Return on Capital employed

Panini limited

Particulars Formula 2019 2018

Return on Capital

Employed Ratio

Net Profit after Taxes/

Gross Capital Employed X

100 12.30%

23.13

%

Net Profit after Taxes 1256 2025

Gross Capital Employed

Total Assets – Current

Liabilities 10211 8755

Total Assets

Noncurrent assets + current

assets 10723 9725

Non-current assets 8613 8550

Current Assets 2110 1175

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

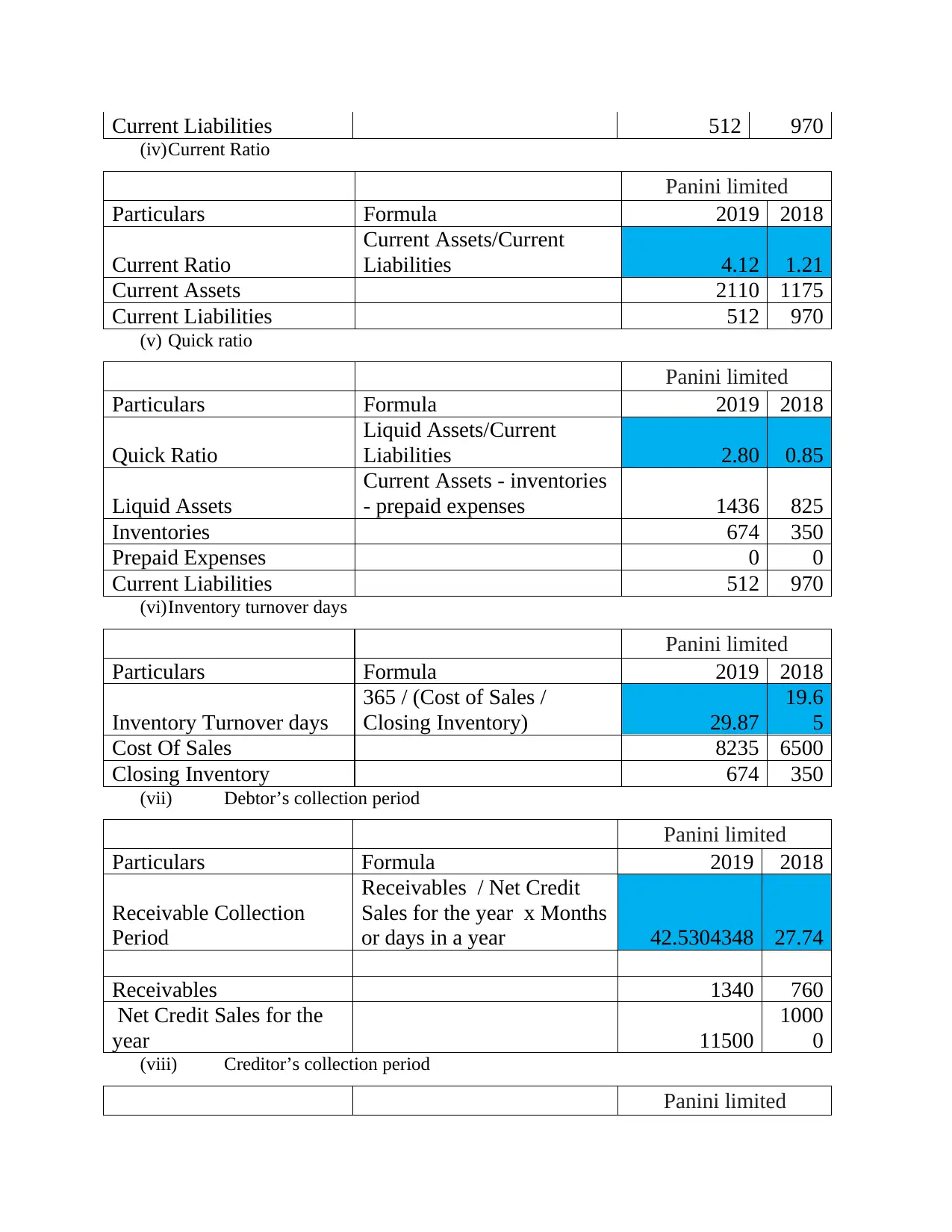

Current Liabilities 512 970

(iv)Current Ratio

Panini limited

Particulars Formula 2019 2018

Current Ratio

Current Assets/Current

Liabilities 4.12 1.21

Current Assets 2110 1175

Current Liabilities 512 970

(v) Quick ratio

Panini limited

Particulars Formula 2019 2018

Quick Ratio

Liquid Assets/Current

Liabilities 2.80 0.85

Liquid Assets

Current Assets - inventories

- prepaid expenses 1436 825

Inventories 674 350

Prepaid Expenses 0 0

Current Liabilities 512 970

(vi)Inventory turnover days

Panini limited

Particulars Formula 2019 2018

Inventory Turnover days

365 / (Cost of Sales /

Closing Inventory) 29.87

19.6

5

Cost Of Sales 8235 6500

Closing Inventory 674 350

(vii) Debtor’s collection period

Panini limited

Particulars Formula 2019 2018

Receivable Collection

Period

Receivables / Net Credit

Sales for the year x Months

or days in a year 42.5304348 27.74

Receivables 1340 760

Net Credit Sales for the

year 11500

1000

0

(viii) Creditor’s collection period

Panini limited

(iv)Current Ratio

Panini limited

Particulars Formula 2019 2018

Current Ratio

Current Assets/Current

Liabilities 4.12 1.21

Current Assets 2110 1175

Current Liabilities 512 970

(v) Quick ratio

Panini limited

Particulars Formula 2019 2018

Quick Ratio

Liquid Assets/Current

Liabilities 2.80 0.85

Liquid Assets

Current Assets - inventories

- prepaid expenses 1436 825

Inventories 674 350

Prepaid Expenses 0 0

Current Liabilities 512 970

(vi)Inventory turnover days

Panini limited

Particulars Formula 2019 2018

Inventory Turnover days

365 / (Cost of Sales /

Closing Inventory) 29.87

19.6

5

Cost Of Sales 8235 6500

Closing Inventory 674 350

(vii) Debtor’s collection period

Panini limited

Particulars Formula 2019 2018

Receivable Collection

Period

Receivables / Net Credit

Sales for the year x Months

or days in a year 42.5304348 27.74

Receivables 1340 760

Net Credit Sales for the

year 11500

1000

0

(viii) Creditor’s collection period

Panini limited

Particulars Formula 2019 2018

Payable Payment Period

(Trade Payables / Cost of

Sales) * 365 15.7108696 33.58

Trade Payables 495 920

Cost of Sales 11500

1000

0

Part b: Analysing the numerical results

(i) Gross Profit Margin: It is a measure of company’s profitability. Cross profit is the

amount that is left with the organization after the payment is made for the labours and materials

used. Labour and material used in the goods are also known with the term cost of goods sold

abbreviated as COGS (Haralayya, 2021). The gross profit margin of the is lower than the ideal

ratio. The firm’s gross margin reduced in the current year in comparison with the previous year.

The possible reason is the inefficient control of the firm on the expenses incurred. Buying

materials from the alternate sources at lower prices will help in improving the ratio.

(ii) Operating profit margin: The operating profit margin is calculated to measure the amount

of profit a company generates by selling a unit worth of currency after making the payments for

its variable costs incurred in the production. Company’s operating income is divided by its net

sales for this purpose. The operating profit margin of the firm is good and higher than the ideal

one. In the current year the company experienced low operating margins as compared to

previous year. There is fall of 7.61% in the current year. Increasing the volume of sales along

with the control over the operating expenses can improve the ratio.

(iii) Return On Capital Employed: Commonly abbreviated as ROCE is a kind of financial

ratio that is used to assess the profitability of the company and tells about the efficiency of a

company in utilising its capital. The ratio provides information regarding the company that

whether it is generating profits from the capital; that has been invested or not. The ROCE of the

company is very poor as compared to the previous year. This indicates the inefficiency of the

company in optimum utilization of its resources employed (Liu and et.al 2019). Increasing the

production capacity along with the sales volume is the solution for the issue.

(iv) Current ratio: It is a kind of liquidity ratio that is calculated in order to know about the

ability of the company to provide for its short term obligations. The current ratio of the company

is below than the ideal ratio that is 2:1. Indicating the inefficiency to pay for its short term

Payable Payment Period

(Trade Payables / Cost of

Sales) * 365 15.7108696 33.58

Trade Payables 495 920

Cost of Sales 11500

1000

0

Part b: Analysing the numerical results

(i) Gross Profit Margin: It is a measure of company’s profitability. Cross profit is the

amount that is left with the organization after the payment is made for the labours and materials

used. Labour and material used in the goods are also known with the term cost of goods sold

abbreviated as COGS (Haralayya, 2021). The gross profit margin of the is lower than the ideal

ratio. The firm’s gross margin reduced in the current year in comparison with the previous year.

The possible reason is the inefficient control of the firm on the expenses incurred. Buying

materials from the alternate sources at lower prices will help in improving the ratio.

(ii) Operating profit margin: The operating profit margin is calculated to measure the amount

of profit a company generates by selling a unit worth of currency after making the payments for

its variable costs incurred in the production. Company’s operating income is divided by its net

sales for this purpose. The operating profit margin of the firm is good and higher than the ideal

one. In the current year the company experienced low operating margins as compared to

previous year. There is fall of 7.61% in the current year. Increasing the volume of sales along

with the control over the operating expenses can improve the ratio.

(iii) Return On Capital Employed: Commonly abbreviated as ROCE is a kind of financial

ratio that is used to assess the profitability of the company and tells about the efficiency of a

company in utilising its capital. The ratio provides information regarding the company that

whether it is generating profits from the capital; that has been invested or not. The ROCE of the

company is very poor as compared to the previous year. This indicates the inefficiency of the

company in optimum utilization of its resources employed (Liu and et.al 2019). Increasing the

production capacity along with the sales volume is the solution for the issue.

(iv) Current ratio: It is a kind of liquidity ratio that is calculated in order to know about the

ability of the company to provide for its short term obligations. The current ratio of the company

is below than the ideal ratio that is 2:1. Indicating the inefficiency to pay for its short term

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

obligations. Current year’s current ratio is indicating the inefficient utilization of the company’s

resources.

(v) Quick ratio: It is also a kind of liquidity ratio. This ratio tells about the capability of a

company to pay for its short term obligations with its liquid assets. The liquid ratio of 1:1 is

considered as ideal. Firm is having excess of liquid assets that can be utilized efficiently to

increase the profitability of the firm. In the previous year the firm had low liquid ratio.

(vi) Inventory turnover days: The ratio shows how many times in a year does the inventory of

the organization gets replaced. Firm replaces its inventory in 30 days approximately. That is

higher by around 10 days as compared to previous year. It indicates the weak sales by the

company. More advertisement expenditure will increase the sales volume of the company.

(vii) Debtor’s collection period: The debtors’ collection period shows in number of months or

number of days the company get back the credit sales amount on an average from the date it

sales the goods on credit. The average time taken by the company to collect the amount from its

debtors increased by 15 days in the current year. It is not good for the company as it increases the

risk of debtors being bad and blocks the working capital of the firm. to improve the situation

early payment discount can be provided to the customers.

(viii) Creditor’s collection period: The creditors’ collection period gives result in the months or

number of days taken on an average by the firm to pay for its obligations against the suppliers of

the firm supplying materials on credit. Creditors collection period is considered good the more it

is. But the firm’s creditor collection period reduced to 15 days from 33 days in the current year

(Choi and et.al., 2018). Building up good relations with the suppliers will help the firm to take

the advantage of getting materials on credit for longer duration.

CONCLUSION

Based on the report the meaning and importance of financial decision making has been

understood. The various functions and the importance of accounting and finance department has

been highlighted in the report. Different sources for raising funds for the medium sized firm has

been seen. Through the report the calculation of eight different accounting ratios has been done.

The report has analysed the ratios for the Panini ltd.

resources.

(v) Quick ratio: It is also a kind of liquidity ratio. This ratio tells about the capability of a

company to pay for its short term obligations with its liquid assets. The liquid ratio of 1:1 is

considered as ideal. Firm is having excess of liquid assets that can be utilized efficiently to

increase the profitability of the firm. In the previous year the firm had low liquid ratio.

(vi) Inventory turnover days: The ratio shows how many times in a year does the inventory of

the organization gets replaced. Firm replaces its inventory in 30 days approximately. That is

higher by around 10 days as compared to previous year. It indicates the weak sales by the

company. More advertisement expenditure will increase the sales volume of the company.

(vii) Debtor’s collection period: The debtors’ collection period shows in number of months or

number of days the company get back the credit sales amount on an average from the date it

sales the goods on credit. The average time taken by the company to collect the amount from its

debtors increased by 15 days in the current year. It is not good for the company as it increases the

risk of debtors being bad and blocks the working capital of the firm. to improve the situation

early payment discount can be provided to the customers.

(viii) Creditor’s collection period: The creditors’ collection period gives result in the months or

number of days taken on an average by the firm to pay for its obligations against the suppliers of

the firm supplying materials on credit. Creditors collection period is considered good the more it

is. But the firm’s creditor collection period reduced to 15 days from 33 days in the current year

(Choi and et.al., 2018). Building up good relations with the suppliers will help the firm to take

the advantage of getting materials on credit for longer duration.

CONCLUSION

Based on the report the meaning and importance of financial decision making has been

understood. The various functions and the importance of accounting and finance department has

been highlighted in the report. Different sources for raising funds for the medium sized firm has

been seen. Through the report the calculation of eight different accounting ratios has been done.

The report has analysed the ratios for the Panini ltd.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Amornkitvikai, Y. and Harvie, C., 2018. Sources of finance and export performance: Evidence

from Thai manufacturing SMEs. The Singapore Economic Review. 63(01). pp.83-109.

Choi, K. B. and et.al., 2018. Amplification ratio analysis of a bridge-type mechanical

amplification mechanism based on a fully compliant model. Mechanism and Machine

Theory. 121. pp.355-372.

Haralayya, B., 2021. Ratio Analysis at NSSK, Bidar. Iconic Research And Engineering

Journals. 4(12). pp.170-182.

Javed, M. and Zhuquan, W., 2018. Analysis of accounting reforms in the public sector of

Pakistan and adoption of cash basis IPSAS. Universal Journal of Accounting and

Finance. 6(2). pp.47-53.

Jędrzejka, D., 2019. Robotic process automation and its impact on accounting. Zeszyty

Teoretyczne Rachunkowości, (105), pp.137-166.

Liu, X. and et.al 2019. Peak-to-average power ratio analysis for OFDM-based mixed-

numerology transmissions. IEEE Transactions on Vehicular Technology. 69(2). pp.1802-

1812.

Okodo, D., Momoh, M. A. and Yahaya, A. O., 2019. Assessing the Reliability of Internal Audit

Functions: The Issues. Journal of Contemporary Research in Business, Economics and

Finance. 1(1). pp.46-55.

Osakwe, P. C. and Otuo, E.I., 2022. Department of Accounting and Finance University of

Nigeria Nsukka, Enugu. Global Journal of Auditing and Finance| GJAF. 1(1). pp.13-29.

Smith, S. S., 2018. Digitization and financial reporting–how technology innovation may drive

the shift toward continuous accounting. Accounting and Finance Research. 7(3). pp.240-

250.

1

Books and Journals

Amornkitvikai, Y. and Harvie, C., 2018. Sources of finance and export performance: Evidence

from Thai manufacturing SMEs. The Singapore Economic Review. 63(01). pp.83-109.

Choi, K. B. and et.al., 2018. Amplification ratio analysis of a bridge-type mechanical

amplification mechanism based on a fully compliant model. Mechanism and Machine

Theory. 121. pp.355-372.

Haralayya, B., 2021. Ratio Analysis at NSSK, Bidar. Iconic Research And Engineering

Journals. 4(12). pp.170-182.

Javed, M. and Zhuquan, W., 2018. Analysis of accounting reforms in the public sector of

Pakistan and adoption of cash basis IPSAS. Universal Journal of Accounting and

Finance. 6(2). pp.47-53.

Jędrzejka, D., 2019. Robotic process automation and its impact on accounting. Zeszyty

Teoretyczne Rachunkowości, (105), pp.137-166.

Liu, X. and et.al 2019. Peak-to-average power ratio analysis for OFDM-based mixed-

numerology transmissions. IEEE Transactions on Vehicular Technology. 69(2). pp.1802-

1812.

Okodo, D., Momoh, M. A. and Yahaya, A. O., 2019. Assessing the Reliability of Internal Audit

Functions: The Issues. Journal of Contemporary Research in Business, Economics and

Finance. 1(1). pp.46-55.

Osakwe, P. C. and Otuo, E.I., 2022. Department of Accounting and Finance University of

Nigeria Nsukka, Enugu. Global Journal of Auditing and Finance| GJAF. 1(1). pp.13-29.

Smith, S. S., 2018. Digitization and financial reporting–how technology innovation may drive

the shift toward continuous accounting. Accounting and Finance Research. 7(3). pp.240-

250.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.