Management Accounting Report: Financial Analysis of Pavestone Company

VerifiedAdded on 2021/01/01

|18

|5307

|436

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within the context of Pavestone, a UK-based manufacturing company. It delves into various aspects of management accounting, including its types, such as cost accounting, price optimization, and inventory management. The report explores different reporting methods, including performance reports, inventory management reports, and job cost reports, and evaluates how these methods can be integrated into organizational processes. It also examines costing techniques, such as marginal costing and absorption costing, with a practical example using Pavestone's cost data. Furthermore, the report discusses budgetary control and various planning tools, along with their advantages and disadvantages. Finally, it addresses how management accounting systems can respond to and resolve financial problems, emphasizing their role in achieving sustainable success. The report is a valuable resource for students seeking to understand the practical application of management accounting in a real-world business setting.

MANAGEMENT

ACCOUNTANTING

ACCOUNTANTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types..................................................................................1

P2: Different methods of management accounting reporting.....................................................2

M1: Benefits of management accounting system and its applications.......................................4

D1: Critically evaluation on how management accounting system and its reporting can be

integrated within organisational process.....................................................................................4

TASK 2............................................................................................................................................5

P3: Calculation of costing...........................................................................................................5

M2: Different types of accounting techniques............................................................................8

D2: Data interpretation................................................................................................................8

TASK 3............................................................................................................................................8

P4: Budgetary control and various types of planning tool with some advantages and

disadvantages used in budgetary control.....................................................................................8

M3: Applications of planning tools for preparing and forecasting budgets with its uses.........10

TASK 4..........................................................................................................................................10

P5: Responses of management accounting system for dealing with financial problems..........10

M4: Management accounting can lead organisation for sustainable success in respect to

financial problems.....................................................................................................................12

D3: How planning tools for accounting respond appropriately to resolve financial problems 12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types..................................................................................1

P2: Different methods of management accounting reporting.....................................................2

M1: Benefits of management accounting system and its applications.......................................4

D1: Critically evaluation on how management accounting system and its reporting can be

integrated within organisational process.....................................................................................4

TASK 2............................................................................................................................................5

P3: Calculation of costing...........................................................................................................5

M2: Different types of accounting techniques............................................................................8

D2: Data interpretation................................................................................................................8

TASK 3............................................................................................................................................8

P4: Budgetary control and various types of planning tool with some advantages and

disadvantages used in budgetary control.....................................................................................8

M3: Applications of planning tools for preparing and forecasting budgets with its uses.........10

TASK 4..........................................................................................................................................10

P5: Responses of management accounting system for dealing with financial problems..........10

M4: Management accounting can lead organisation for sustainable success in respect to

financial problems.....................................................................................................................12

D3: How planning tools for accounting respond appropriately to resolve financial problems 12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is considered as a systematic approach which support major

activities of business by planning, organising, controlling and monitoring. All these processes

help in enhancing performance of organisation in an appropriate manner. Along with this, it also

helps managers in developing their knowledge by which they can take decision related to

investment and finance. This kind of management generally used to prepare financial statements

like balance sheet, income, profit and loss account etc. through which position of business can be

determined during an accounting period. In this context, the report has been prepared on

Pavestone which is a manufacturing company of UK. It deals in construction sector and supply

building materials to other organisations on reasonable price rates (Bodie, 2013). This

assignment has made a discussion on various management accounting systems, some reporting

methods and its benefits for enterprises. Management of this company uses some important cost

methods in order to evaluate product cost. Moreover, an application of different planning tools

for planning and budgetary control are discussed with their benefits drawbacks. For resolving

problems related to finance, the way of adapting management accounting system also have been

discussed in further part.

TASK 1

P1: Management accounting and its types

The term management accounting links with analysing business costs and operations in

order to prepare internal financial report and statements. It supports managers' to take day to day

business decisions and obtain business goals and objectives. Management accounting is an act of

making sense of financial data and translating it into useful information (What is Management

Accounting and its importance. 2017). It increases efficiency of business operations which aids

management of Pavestone in planning controlling as well as coordinating all business activities

by getting standard and assessing actual performance which enables management to perform in

better manner.

Management accounting system helps manager to achieve goals and objectives of the

company. Thus maximum profits can be gained, if capital is invested in business. In addition,

information received through management accounting highlight past trading cycle of company;

with this assistance finance manager can recognise how trade cycle get affected and apply

1

Management accounting is considered as a systematic approach which support major

activities of business by planning, organising, controlling and monitoring. All these processes

help in enhancing performance of organisation in an appropriate manner. Along with this, it also

helps managers in developing their knowledge by which they can take decision related to

investment and finance. This kind of management generally used to prepare financial statements

like balance sheet, income, profit and loss account etc. through which position of business can be

determined during an accounting period. In this context, the report has been prepared on

Pavestone which is a manufacturing company of UK. It deals in construction sector and supply

building materials to other organisations on reasonable price rates (Bodie, 2013). This

assignment has made a discussion on various management accounting systems, some reporting

methods and its benefits for enterprises. Management of this company uses some important cost

methods in order to evaluate product cost. Moreover, an application of different planning tools

for planning and budgetary control are discussed with their benefits drawbacks. For resolving

problems related to finance, the way of adapting management accounting system also have been

discussed in further part.

TASK 1

P1: Management accounting and its types

The term management accounting links with analysing business costs and operations in

order to prepare internal financial report and statements. It supports managers' to take day to day

business decisions and obtain business goals and objectives. Management accounting is an act of

making sense of financial data and translating it into useful information (What is Management

Accounting and its importance. 2017). It increases efficiency of business operations which aids

management of Pavestone in planning controlling as well as coordinating all business activities

by getting standard and assessing actual performance which enables management to perform in

better manner.

Management accounting system helps manager to achieve goals and objectives of the

company. Thus maximum profits can be gained, if capital is invested in business. In addition,

information received through management accounting highlight past trading cycle of company;

with this assistance finance manager can recognise how trade cycle get affected and apply

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

safeguarding for the same. There is defined several methods of management accounting which

are stated as under -

Cost accounting system – It is a procedure of demonstrating the cost of product,

producer and project through systematic tracking, diversifying, interpreting and measuring costs

related with business operations. Then taking several course of action in order to control such

costs. The chosen organisation, Pavestone is developing wide range of pre-cast concrete walling

and paving products which are served over the nation among builders and landscapers (DRURY,

2013). In this manner, it is necessary for top management of the company to make optimal and

efficient utilisation of available resources by eradication of wastage. In addition to this, there are

three types of cost accounting techniques, such as- actual, normal and standard. In which actual

cost is labour, material and overhead costs whereas normal costing is based upon direct cost and

overhead rates.

Price Optimisation system – It is one of the effective management accounting system

which entails that management must follow optimal pricing policies of its products in order to

gain high competitive edge. Pavestone deals in importing, selling and supplying of materials like

– stones and concrete and acquire price optimisation system for creating effective pricing

strategy which may attain large number of customers towards company. Along with this, the

management accounting system increases customer satisfaction level and raise their willingness

to purchase products or services (Mat, Smith and Djajadikerta, 2010). This system recommends

alteration in price strategy which helps in company's progress.

Inventory management system – The accounting is liable to track company's stock

availability in business organisation; in other words, inventory management looks whether or not

employees have enough amount to stock thus to produce products and services. Along with this,

it covers each and everything from warehouses to shipping, manufacturing to retail and further

movement of stock in and out of organisation. These are the main types of inventory

management system, such as – LIFO, FIFO and weighted average. The chosen business

association Pavestone follows system guidelines of inventory management system thus to

manage cash inflows and outflows at workplace and take imperative decisions.

P2: Different methods of management accounting reporting

Management accounting reporting refers to a process of preparing management reports

through which managers of a company can take appropriate decision related to further

2

are stated as under -

Cost accounting system – It is a procedure of demonstrating the cost of product,

producer and project through systematic tracking, diversifying, interpreting and measuring costs

related with business operations. Then taking several course of action in order to control such

costs. The chosen organisation, Pavestone is developing wide range of pre-cast concrete walling

and paving products which are served over the nation among builders and landscapers (DRURY,

2013). In this manner, it is necessary for top management of the company to make optimal and

efficient utilisation of available resources by eradication of wastage. In addition to this, there are

three types of cost accounting techniques, such as- actual, normal and standard. In which actual

cost is labour, material and overhead costs whereas normal costing is based upon direct cost and

overhead rates.

Price Optimisation system – It is one of the effective management accounting system

which entails that management must follow optimal pricing policies of its products in order to

gain high competitive edge. Pavestone deals in importing, selling and supplying of materials like

– stones and concrete and acquire price optimisation system for creating effective pricing

strategy which may attain large number of customers towards company. Along with this, the

management accounting system increases customer satisfaction level and raise their willingness

to purchase products or services (Mat, Smith and Djajadikerta, 2010). This system recommends

alteration in price strategy which helps in company's progress.

Inventory management system – The accounting is liable to track company's stock

availability in business organisation; in other words, inventory management looks whether or not

employees have enough amount to stock thus to produce products and services. Along with this,

it covers each and everything from warehouses to shipping, manufacturing to retail and further

movement of stock in and out of organisation. These are the main types of inventory

management system, such as – LIFO, FIFO and weighted average. The chosen business

association Pavestone follows system guidelines of inventory management system thus to

manage cash inflows and outflows at workplace and take imperative decisions.

P2: Different methods of management accounting reporting

Management accounting reporting refers to a process of preparing management reports

through which managers of a company can take appropriate decision related to further

2

investment (Tools of management and accounting, 2018). It includes availability of cash in

business, sales revenues, current status of finance and more. In context with Pavestone, it deals

in small sector and willing to expand its marketplace in a rapid manner by enhancing customer

base. So, it focuses on improving performance of business more by giving good quality of

products. For maintaining financial reports such as balance sheet, profit or loss a/c, shareholder's

statements and more, this firm has used various methods of management accounting reporting as

given below:-

Performance report: This method of accounting management reporting helps in

determining performance of business during an accounting period. It involves details of project

such as collection and distribution, communication development, utilisation of resources and

forecasting of progress. In this regard, managers of Pavestone prepare performance report to

analyse its performance within all levels of management by comparing estimated production

with actual. It helps in taking necessary actions for variations of business. In order to attract

stakeholders, this company has distributed some major responsibilities for managers of all

departments at individual levels by which performance of business can maximizes.

Inventory management reports: Companies which deals in product-oriented business

always seek to manage and maintain inventories at optimum levels. In this regard, there is going

on a tug-of-war consideration between need of sufficient products for fulfilment of customer's

demand with desire avoiding costly pitfalls related to overstocking. Thus, in this context,

inventory management reports help in comparing the holding cost with profitability. It provides

information related to inventories through which managers can take sensible decisions for

managing production and operations (Lukka and Vinnari, 2014). As Pavestone supplies stone,

concrete and other materials to construction companies so, for maintain inventories in sufficient

manner, it ie required by managers to prepare inventory management report on quarterly basis.

They can use some effective methods like Economic order quantity and ABC analysis for further

classification of inventory management reporting. In this regard, EOQ is considered as best

reporting method bas it states quantity order which helps in holding inventory cost.

Job cost reporting: This system of reporting system helps in assembling costs by

different job. For determining total cost of job, this report track actual amount related to costs of

direct material, equipments, labour and subcontract. In context with Pavestone, its managers use

3

business, sales revenues, current status of finance and more. In context with Pavestone, it deals

in small sector and willing to expand its marketplace in a rapid manner by enhancing customer

base. So, it focuses on improving performance of business more by giving good quality of

products. For maintaining financial reports such as balance sheet, profit or loss a/c, shareholder's

statements and more, this firm has used various methods of management accounting reporting as

given below:-

Performance report: This method of accounting management reporting helps in

determining performance of business during an accounting period. It involves details of project

such as collection and distribution, communication development, utilisation of resources and

forecasting of progress. In this regard, managers of Pavestone prepare performance report to

analyse its performance within all levels of management by comparing estimated production

with actual. It helps in taking necessary actions for variations of business. In order to attract

stakeholders, this company has distributed some major responsibilities for managers of all

departments at individual levels by which performance of business can maximizes.

Inventory management reports: Companies which deals in product-oriented business

always seek to manage and maintain inventories at optimum levels. In this regard, there is going

on a tug-of-war consideration between need of sufficient products for fulfilment of customer's

demand with desire avoiding costly pitfalls related to overstocking. Thus, in this context,

inventory management reports help in comparing the holding cost with profitability. It provides

information related to inventories through which managers can take sensible decisions for

managing production and operations (Lukka and Vinnari, 2014). As Pavestone supplies stone,

concrete and other materials to construction companies so, for maintain inventories in sufficient

manner, it ie required by managers to prepare inventory management report on quarterly basis.

They can use some effective methods like Economic order quantity and ABC analysis for further

classification of inventory management reporting. In this regard, EOQ is considered as best

reporting method bas it states quantity order which helps in holding inventory cost.

Job cost reporting: This system of reporting system helps in assembling costs by

different job. For determining total cost of job, this report track actual amount related to costs of

direct material, equipments, labour and subcontract. In context with Pavestone, its managers use

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost report for identifying cost of each particular job order by comparing with investment on

production of the same. It will help in avoiding extra expenses and minimising wastage also.

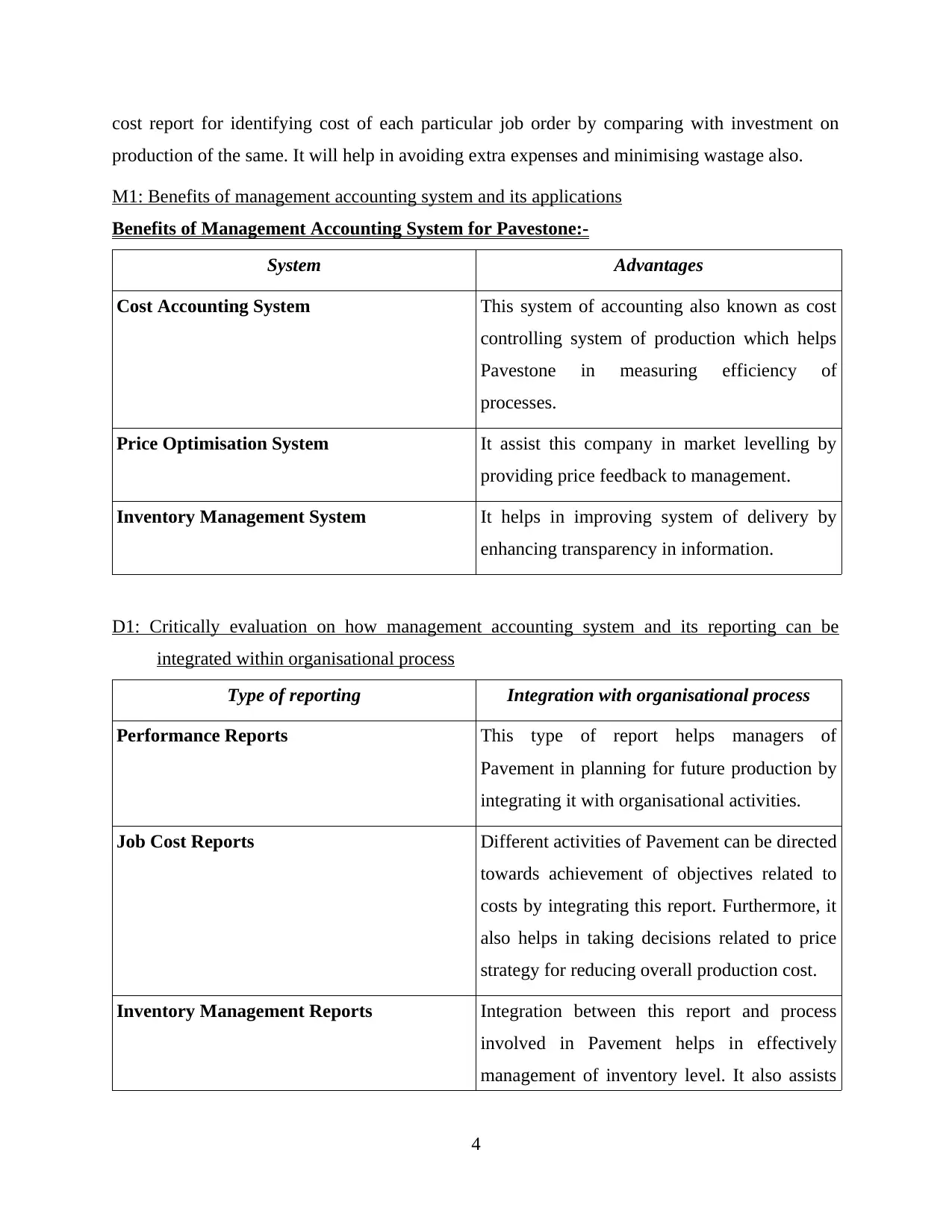

M1: Benefits of management accounting system and its applications

Benefits of Management Accounting System for Pavestone:-

System Advantages

Cost Accounting System This system of accounting also known as cost

controlling system of production which helps

Pavestone in measuring efficiency of

processes.

Price Optimisation System It assist this company in market levelling by

providing price feedback to management.

Inventory Management System It helps in improving system of delivery by

enhancing transparency in information.

D1: Critically evaluation on how management accounting system and its reporting can be

integrated within organisational process

Type of reporting Integration with organisational process

Performance Reports This type of report helps managers of

Pavement in planning for future production by

integrating it with organisational activities.

Job Cost Reports Different activities of Pavement can be directed

towards achievement of objectives related to

costs by integrating this report. Furthermore, it

also helps in taking decisions related to price

strategy for reducing overall production cost.

Inventory Management Reports Integration between this report and process

involved in Pavement helps in effectively

management of inventory level. It also assists

4

production of the same. It will help in avoiding extra expenses and minimising wastage also.

M1: Benefits of management accounting system and its applications

Benefits of Management Accounting System for Pavestone:-

System Advantages

Cost Accounting System This system of accounting also known as cost

controlling system of production which helps

Pavestone in measuring efficiency of

processes.

Price Optimisation System It assist this company in market levelling by

providing price feedback to management.

Inventory Management System It helps in improving system of delivery by

enhancing transparency in information.

D1: Critically evaluation on how management accounting system and its reporting can be

integrated within organisational process

Type of reporting Integration with organisational process

Performance Reports This type of report helps managers of

Pavement in planning for future production by

integrating it with organisational activities.

Job Cost Reports Different activities of Pavement can be directed

towards achievement of objectives related to

costs by integrating this report. Furthermore, it

also helps in taking decisions related to price

strategy for reducing overall production cost.

Inventory Management Reports Integration between this report and process

involved in Pavement helps in effectively

management of inventory level. It also assists

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in managing manufacturing costs at the time of

placing different purchasing orders.

TASK 2

P3: Calculation of costing

Costs refers to an amount which has to be paid by a purchaser to seller at the time of

buying a product. It represents value of a product which includes price of raw materials used for

manufacturing, labours price, risk incurred and overall process of production. In terms of

business, cost can be distinguished as fixed and variable. Under this, costs which doesn't change

with variation and remains constant for a particular level of output refers to fixed costs. While

costs which change with variation is termed as variable costs which increases with enhancement

of production level. But in context with fixed cost, it decrease with increase in production cost.

For enhancing customer base it is necessary for managers of Pavestone to set price of

each product in right manner (Qian, Burritt and Chen, 2015). If price of products is not attractive

and under purchasing power of customers then it will affect sales performance and profitability

of business in a large manner.

Marginal costing- It refers to costing technique which helps in measuring marginal cost

of a company. It is considered as best source for decision-making procedures of a company

under which variable costs are allocated to unit of cost. But in this technique, fixed costs is

written off fully for the period to aggregate contribution.

Absorption costing – This technique used to treat overall cost of production as product

cost by taking underpinning all the resources and expenses of the same. It includes direct labour,

direct material as well as both variable and fixed cost of overhead expenses.

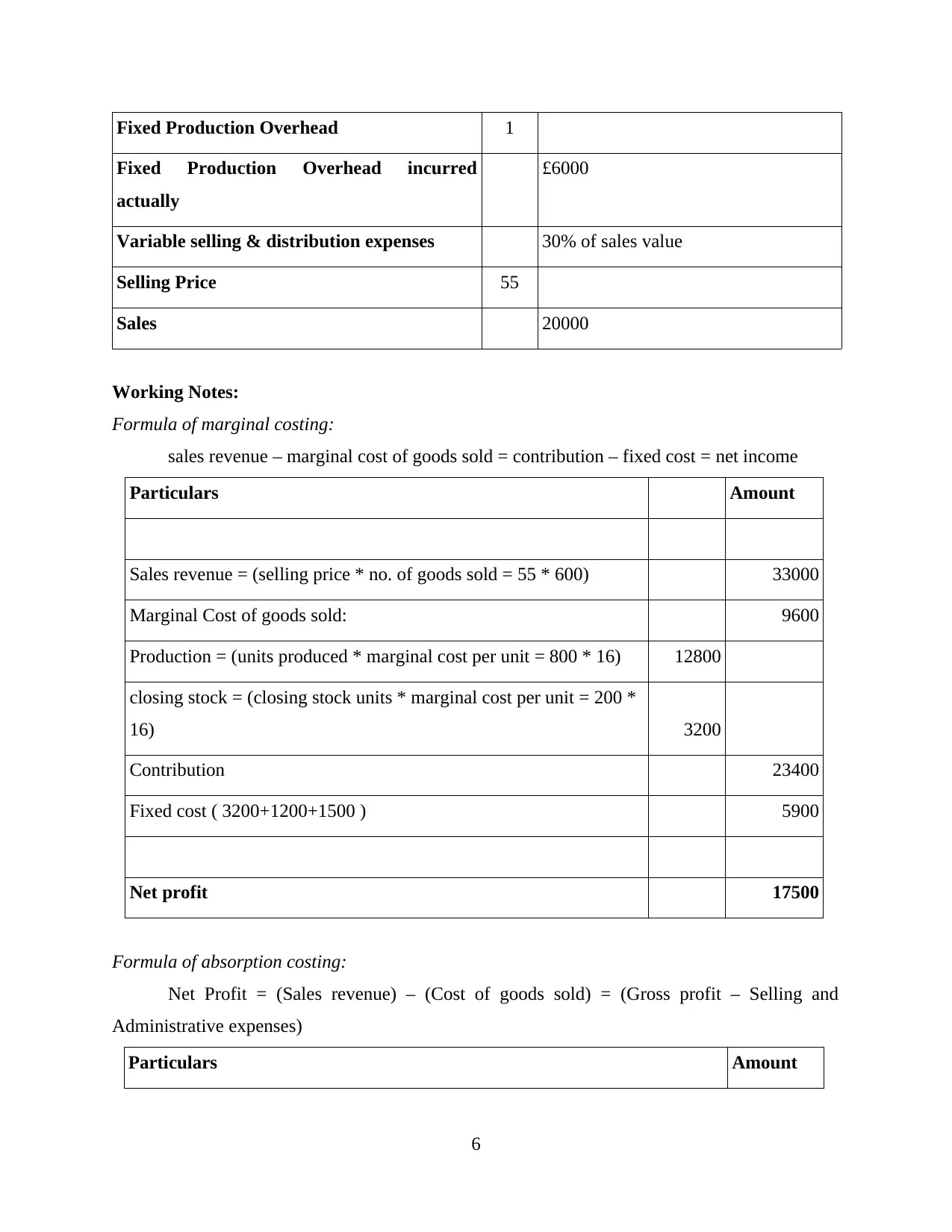

According to case study, the cost card of Pavement is given as beneath:-

£

Direct Labour 6

Direct Material 7

Variable Production Overhead 2

5

placing different purchasing orders.

TASK 2

P3: Calculation of costing

Costs refers to an amount which has to be paid by a purchaser to seller at the time of

buying a product. It represents value of a product which includes price of raw materials used for

manufacturing, labours price, risk incurred and overall process of production. In terms of

business, cost can be distinguished as fixed and variable. Under this, costs which doesn't change

with variation and remains constant for a particular level of output refers to fixed costs. While

costs which change with variation is termed as variable costs which increases with enhancement

of production level. But in context with fixed cost, it decrease with increase in production cost.

For enhancing customer base it is necessary for managers of Pavestone to set price of

each product in right manner (Qian, Burritt and Chen, 2015). If price of products is not attractive

and under purchasing power of customers then it will affect sales performance and profitability

of business in a large manner.

Marginal costing- It refers to costing technique which helps in measuring marginal cost

of a company. It is considered as best source for decision-making procedures of a company

under which variable costs are allocated to unit of cost. But in this technique, fixed costs is

written off fully for the period to aggregate contribution.

Absorption costing – This technique used to treat overall cost of production as product

cost by taking underpinning all the resources and expenses of the same. It includes direct labour,

direct material as well as both variable and fixed cost of overhead expenses.

According to case study, the cost card of Pavement is given as beneath:-

£

Direct Labour 6

Direct Material 7

Variable Production Overhead 2

5

Fixed Production Overhead 1

Fixed Production Overhead incurred

actually

£6000

Variable selling & distribution expenses 30% of sales value

Selling Price 55

Sales 20000

Working Notes:

Formula of marginal costing:

sales revenue – marginal cost of goods sold = contribution – fixed cost = net income

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Formula of absorption costing:

Net Profit = (Sales revenue) – (Cost of goods sold) = (Gross profit – Selling and

Administrative expenses)

Particulars Amount

6

Fixed Production Overhead incurred

actually

£6000

Variable selling & distribution expenses 30% of sales value

Selling Price 55

Sales 20000

Working Notes:

Formula of marginal costing:

sales revenue – marginal cost of goods sold = contribution – fixed cost = net income

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Formula of absorption costing:

Net Profit = (Sales revenue) – (Cost of goods sold) = (Gross profit – Selling and

Administrative expenses)

Particulars Amount

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

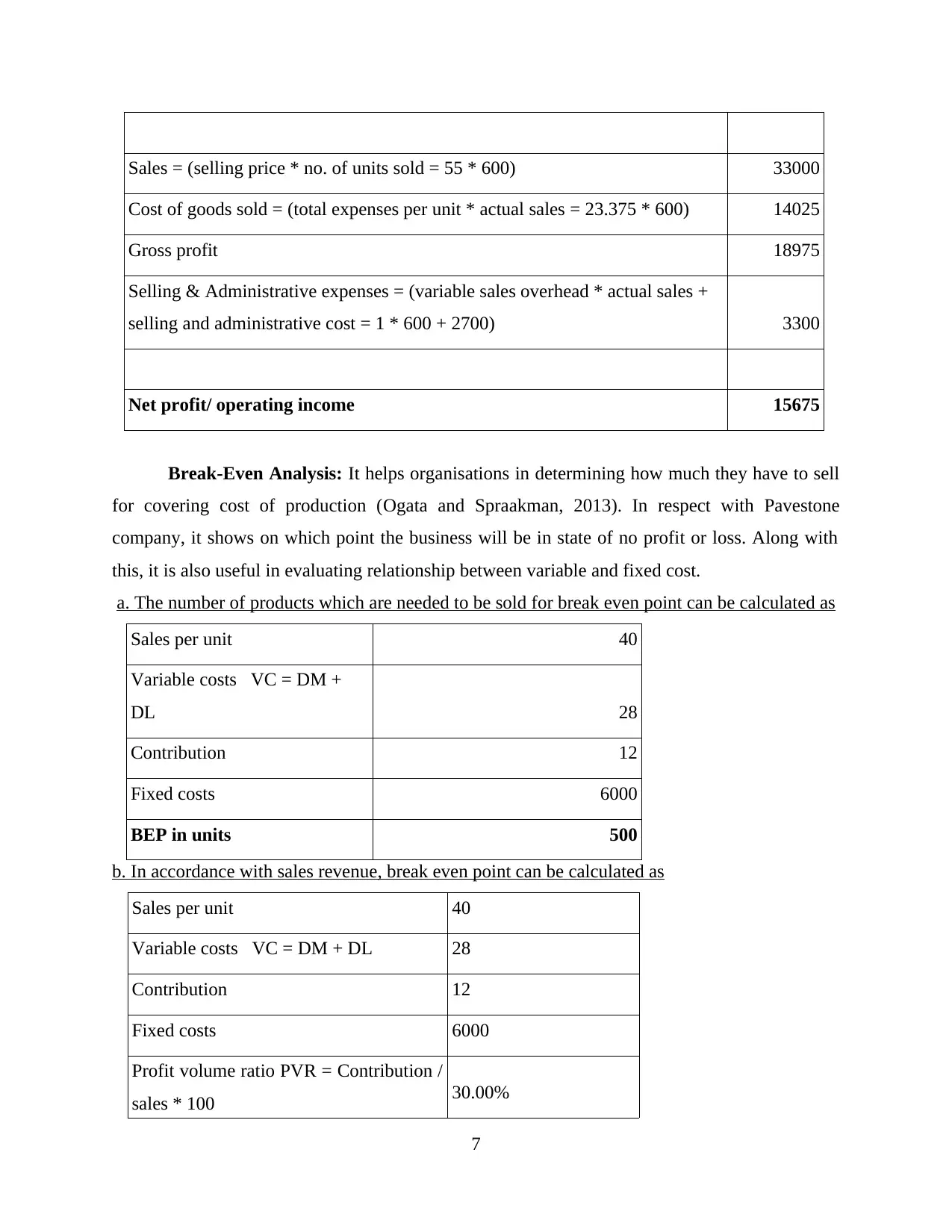

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-Even Analysis: It helps organisations in determining how much they have to sell

for covering cost of production (Ogata and Spraakman, 2013). In respect with Pavestone

company, it shows on which point the business will be in state of no profit or loss. Along with

this, it is also useful in evaluating relationship between variable and fixed cost.

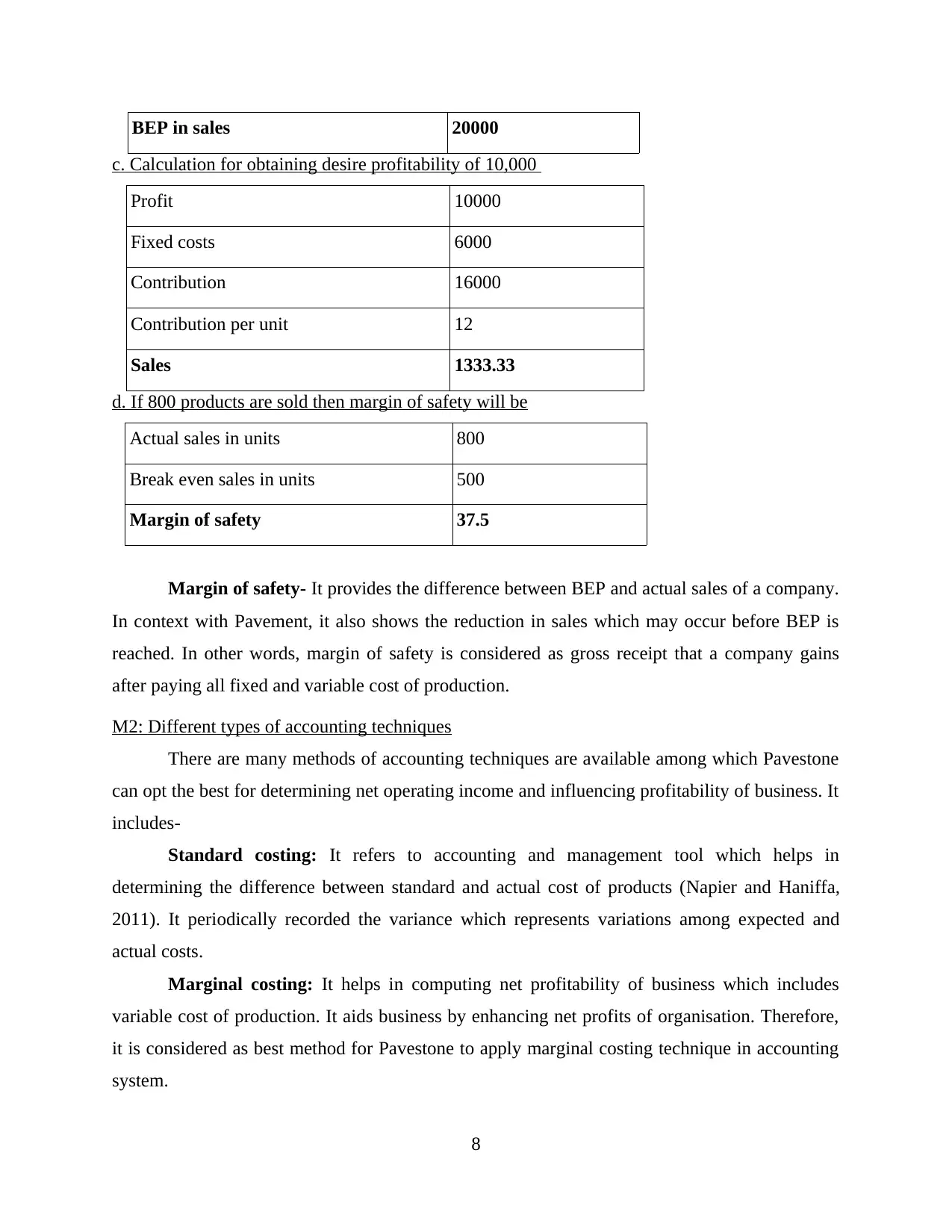

a. The number of products which are needed to be sold for break even point can be calculated as

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. In accordance with sales revenue, break even point can be calculated as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

7

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-Even Analysis: It helps organisations in determining how much they have to sell

for covering cost of production (Ogata and Spraakman, 2013). In respect with Pavestone

company, it shows on which point the business will be in state of no profit or loss. Along with

this, it is also useful in evaluating relationship between variable and fixed cost.

a. The number of products which are needed to be sold for break even point can be calculated as

Sales per unit 40

Variable costs VC = DM +

DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. In accordance with sales revenue, break even point can be calculated as

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BEP in sales 20000

c. Calculation for obtaining desire profitability of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

d. If 800 products are sold then margin of safety will be

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety- It provides the difference between BEP and actual sales of a company.

In context with Pavement, it also shows the reduction in sales which may occur before BEP is

reached. In other words, margin of safety is considered as gross receipt that a company gains

after paying all fixed and variable cost of production.

M2: Different types of accounting techniques

There are many methods of accounting techniques are available among which Pavestone

can opt the best for determining net operating income and influencing profitability of business. It

includes-

Standard costing: It refers to accounting and management tool which helps in

determining the difference between standard and actual cost of products (Napier and Haniffa,

2011). It periodically recorded the variance which represents variations among expected and

actual costs.

Marginal costing: It helps in computing net profitability of business which includes

variable cost of production. It aids business by enhancing net profits of organisation. Therefore,

it is considered as best method for Pavestone to apply marginal costing technique in accounting

system.

8

c. Calculation for obtaining desire profitability of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

d. If 800 products are sold then margin of safety will be

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

Margin of safety- It provides the difference between BEP and actual sales of a company.

In context with Pavement, it also shows the reduction in sales which may occur before BEP is

reached. In other words, margin of safety is considered as gross receipt that a company gains

after paying all fixed and variable cost of production.

M2: Different types of accounting techniques

There are many methods of accounting techniques are available among which Pavestone

can opt the best for determining net operating income and influencing profitability of business. It

includes-

Standard costing: It refers to accounting and management tool which helps in

determining the difference between standard and actual cost of products (Napier and Haniffa,

2011). It periodically recorded the variance which represents variations among expected and

actual costs.

Marginal costing: It helps in computing net profitability of business which includes

variable cost of production. It aids business by enhancing net profits of organisation. Therefore,

it is considered as best method for Pavestone to apply marginal costing technique in accounting

system.

8

D2: Data interpretation

Interpretation of Data:

It has been interpreted from above mentioned data that as compared with other

accounting techniques, marginal costing refers to most useful method for Pavestone. The main

reason behind this is that it helps in growth of profitability. As per calculation, by marginal

costing, net profit results to £17500 while absorption technique obtains £15675. Hence, in this

context, the difference among both cost has arise because of fluctuations in variable costs.

Furthermore, in BEP analysis, it has evaluated that 500 units are required to be sold for reaching

a break-even point i.e. 20,000. Along with this, for earning profitability near about £10,000,

employers of Pavestone are required to sale approximate 1333 units with 37.5 as a margin of

safety in case of selling 800 units.

TASK 3

P4: Budgetary control and various types of planning tool with some advantages and

disadvantages used in budgetary control

Budgetary control – It consists with financial process of managing income and

expenditures of a business organisation. Budgetary control is acquired by management in order

to compare actual revenues and disbursals to forecasting revenues and disbursals. The method

aids to track financial information of the company, i.e. how much money inflow and outflow is

taking place as well as need of investments then apply accordingly necessary changes if required

(Murray Lindsay, 2012). Along with this, Budgetary control method is acquired by Pavestone

thus to prepare an effective budget for future and compare it with future perspectives.

Budgetary control is required in policy formulation and controlling; it act as an

instrument of coordination. The prime objective of this system is to make plan for future by

setting different budgets, requirements and expected performance is anticipated for an enterprise.

It aids to eliminate wastages and increases profitability, centralise the control system and

corrections of deviations from established standards. While developing a budget, it is necessary

for management of Pavestone to determine actual budget needs and then allocate the amount to

be spend in various working activities. After this, management is required to compare, assess and

interpret the actual performance thus to meet business goals and objectives (Arroyo, 2012).

9

Interpretation of Data:

It has been interpreted from above mentioned data that as compared with other

accounting techniques, marginal costing refers to most useful method for Pavestone. The main

reason behind this is that it helps in growth of profitability. As per calculation, by marginal

costing, net profit results to £17500 while absorption technique obtains £15675. Hence, in this

context, the difference among both cost has arise because of fluctuations in variable costs.

Furthermore, in BEP analysis, it has evaluated that 500 units are required to be sold for reaching

a break-even point i.e. 20,000. Along with this, for earning profitability near about £10,000,

employers of Pavestone are required to sale approximate 1333 units with 37.5 as a margin of

safety in case of selling 800 units.

TASK 3

P4: Budgetary control and various types of planning tool with some advantages and

disadvantages used in budgetary control

Budgetary control – It consists with financial process of managing income and

expenditures of a business organisation. Budgetary control is acquired by management in order

to compare actual revenues and disbursals to forecasting revenues and disbursals. The method

aids to track financial information of the company, i.e. how much money inflow and outflow is

taking place as well as need of investments then apply accordingly necessary changes if required

(Murray Lindsay, 2012). Along with this, Budgetary control method is acquired by Pavestone

thus to prepare an effective budget for future and compare it with future perspectives.

Budgetary control is required in policy formulation and controlling; it act as an

instrument of coordination. The prime objective of this system is to make plan for future by

setting different budgets, requirements and expected performance is anticipated for an enterprise.

It aids to eliminate wastages and increases profitability, centralise the control system and

corrections of deviations from established standards. While developing a budget, it is necessary

for management of Pavestone to determine actual budget needs and then allocate the amount to

be spend in various working activities. After this, management is required to compare, assess and

interpret the actual performance thus to meet business goals and objectives (Arroyo, 2012).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.