Financial Analysis of Audio Pixels Holdings Ltd - Finance Report

VerifiedAdded on 2020/05/16

|13

|2180

|62

Report

AI Summary

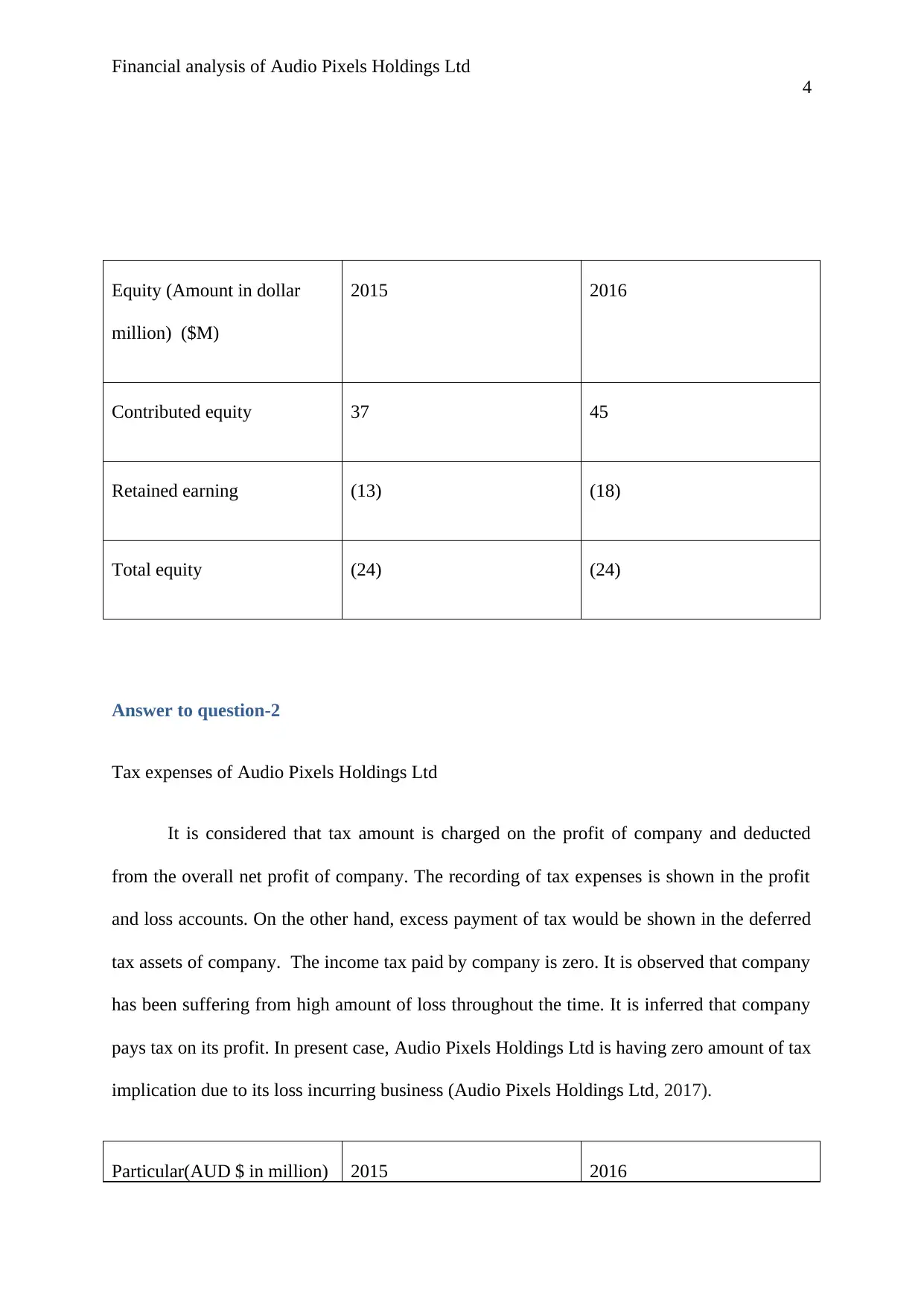

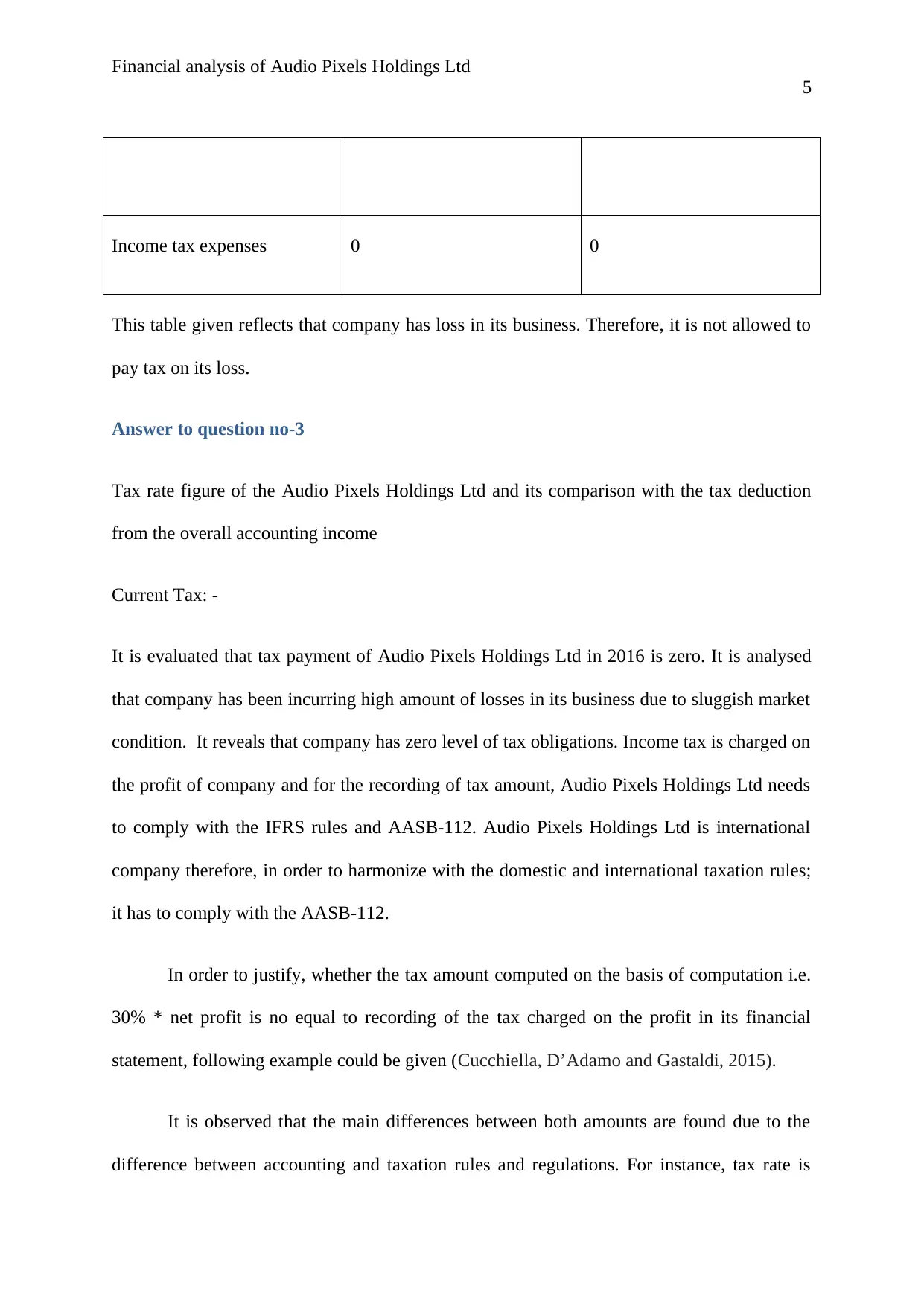

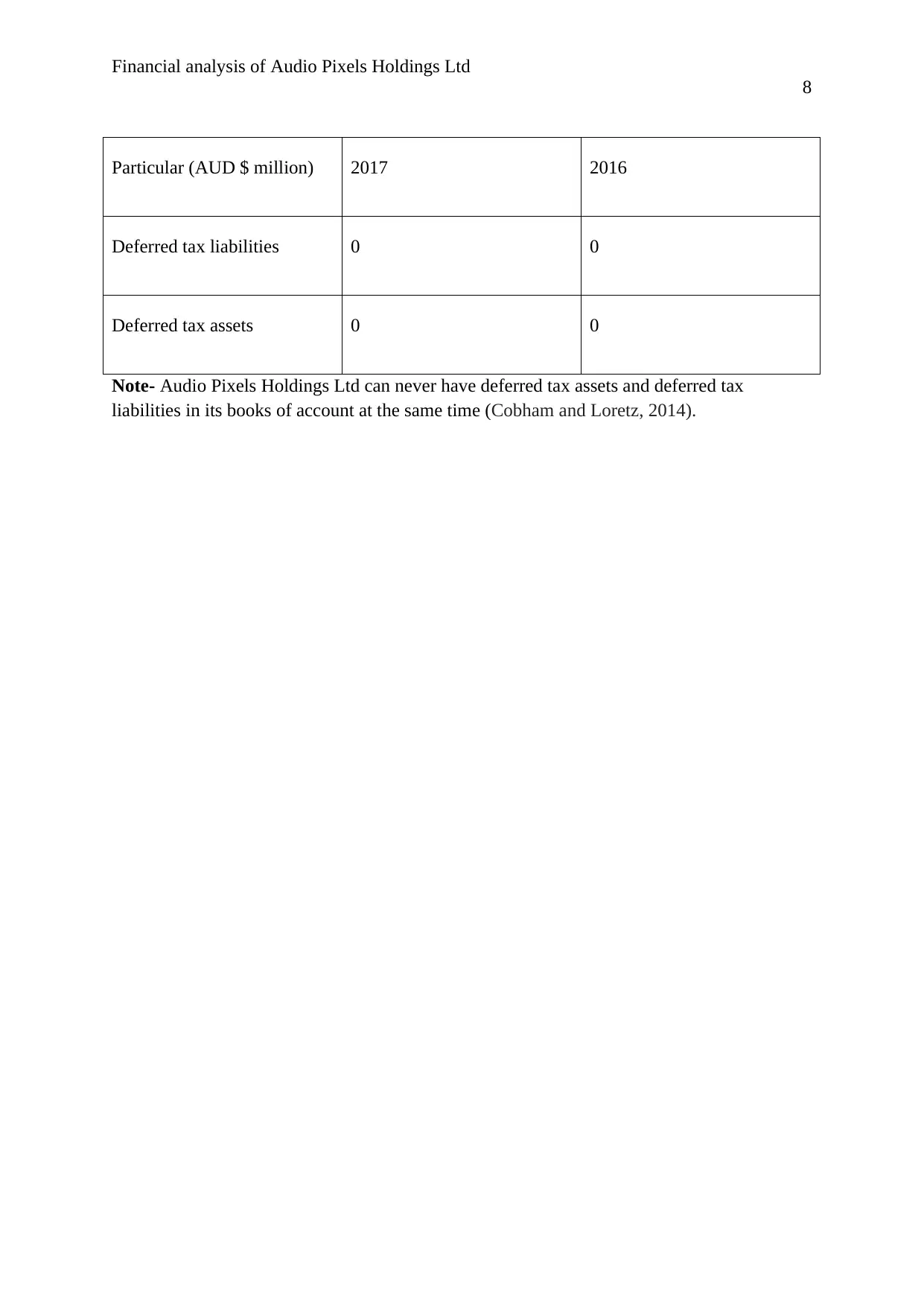

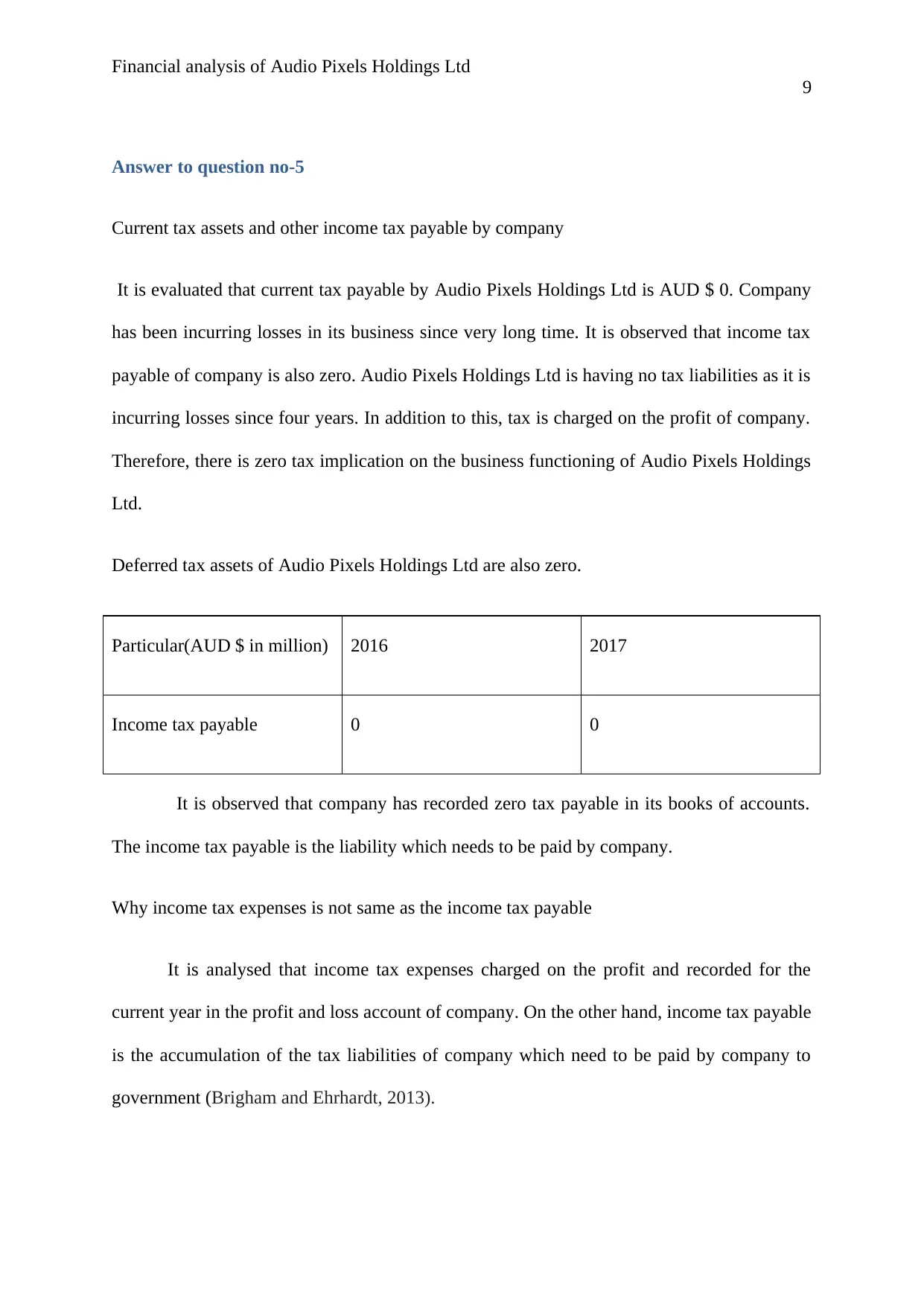

This report presents a financial analysis of Audio Pixels Holdings Ltd, examining various aspects of its financial performance. The analysis delves into the company's equity structure, including contributed capital, owner's equity, and retained earnings, highlighting the impact of losses on equity. It explores the company's tax expenses, noting the absence of income tax payments due to sustained losses. The report also investigates the differences between accounting and taxation rules concerning tax rates and deferred tax assets/liabilities, emphasizing the zero values recorded for deferred tax. Furthermore, it contrasts income tax expenses with income tax payable, differentiating between the current year's tax charges and the accumulated tax liabilities. The cash flow statement is compared to the profit and loss account in terms of tax reporting. Finally, the report discusses the treatment of tax in the company's financial statements, including the challenges and new insights gained from the tax recording process. The report is based on the annual reports of Audio Pixels Holdings Ltd.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.