Financial Analysis Report: Pizza Franchise Investment Decision

VerifiedAdded on 2021/06/14

|10

|1907

|21

Report

AI Summary

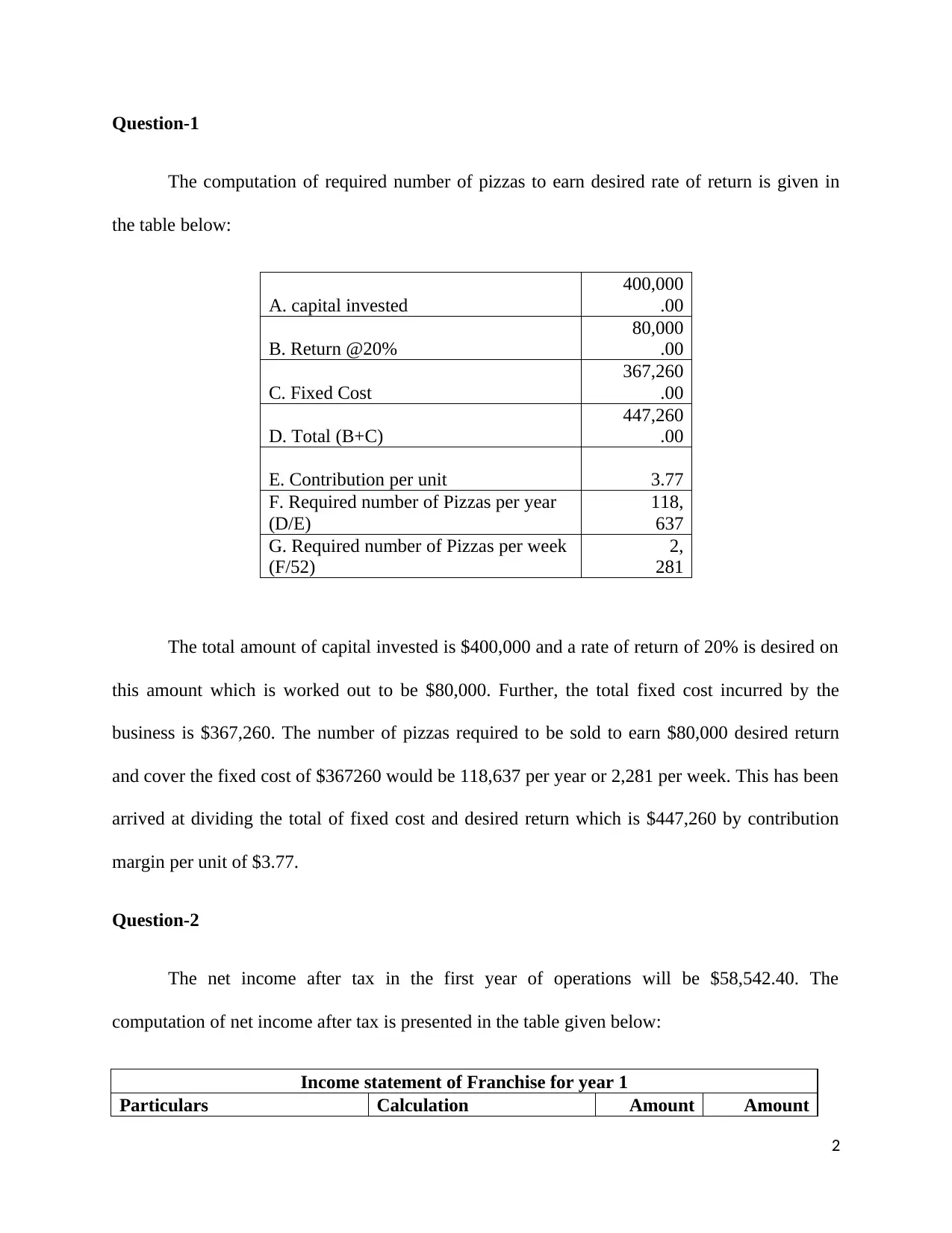

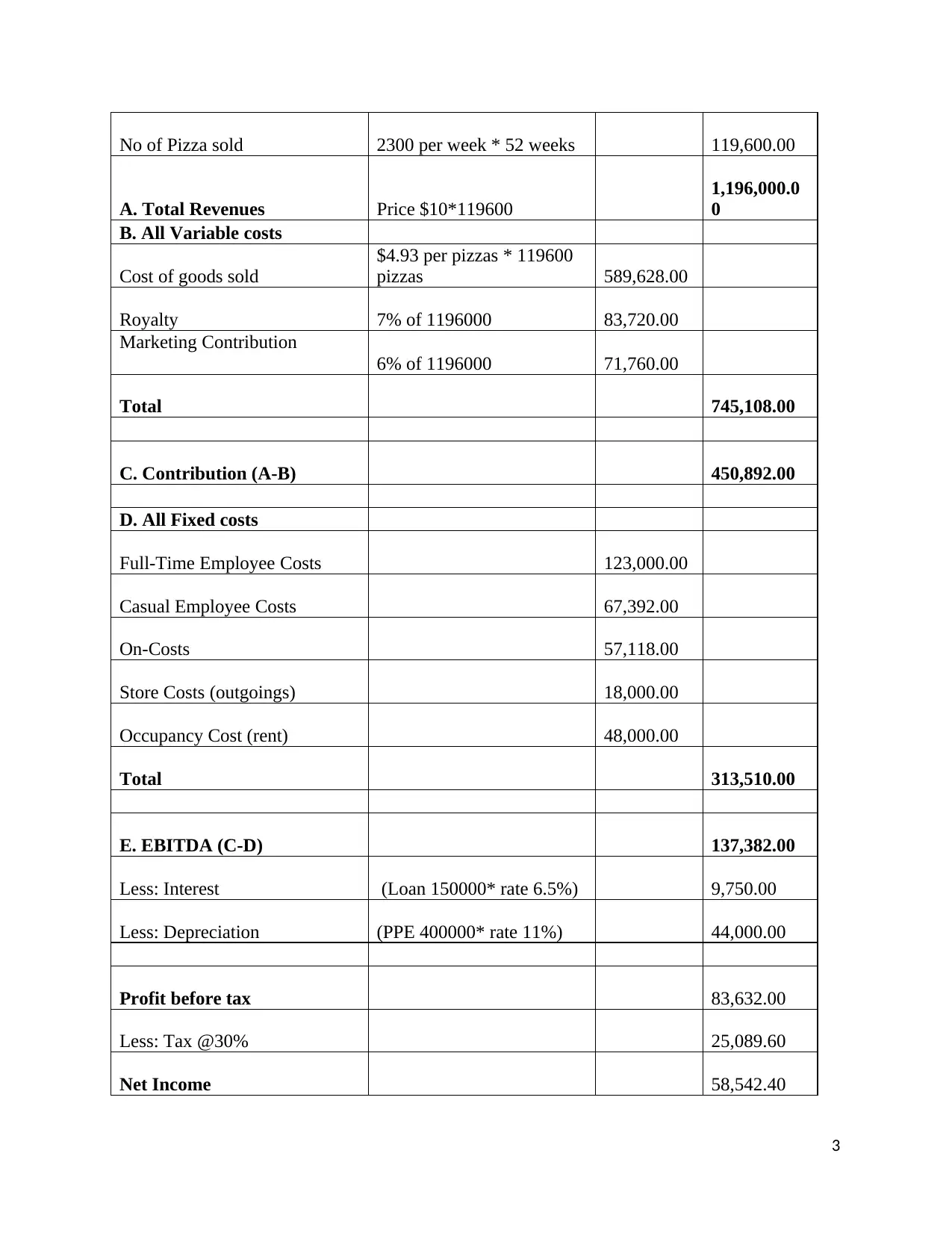

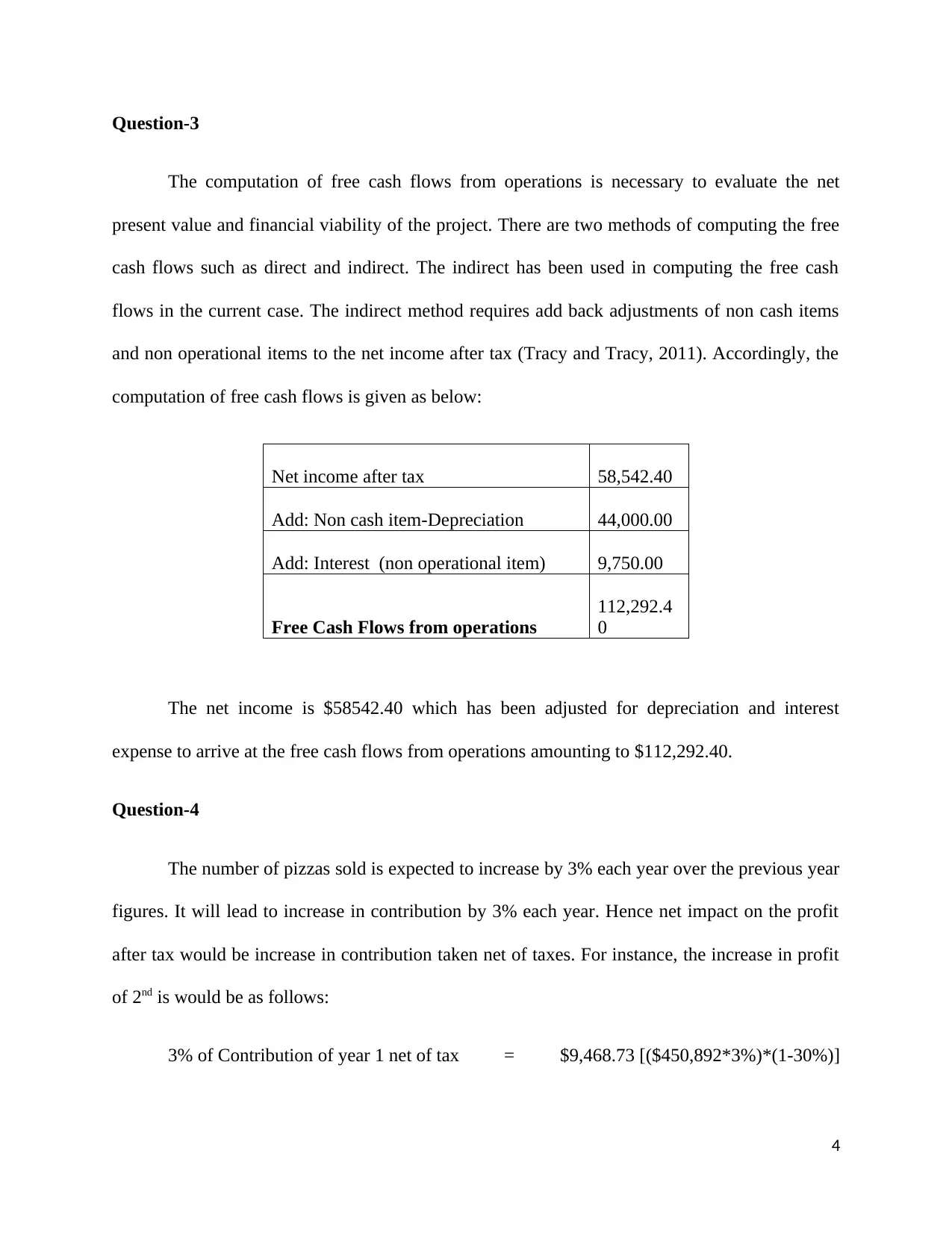

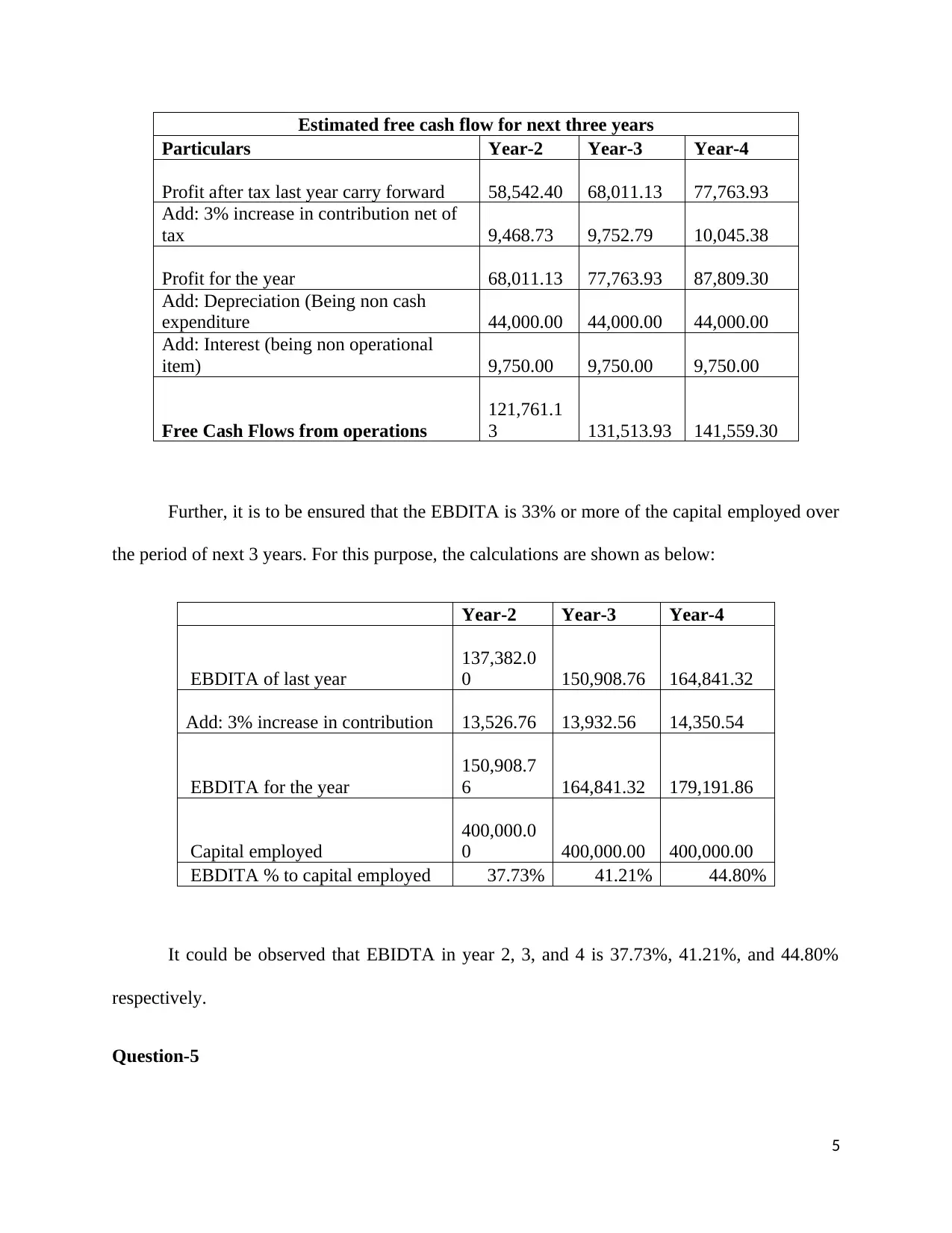

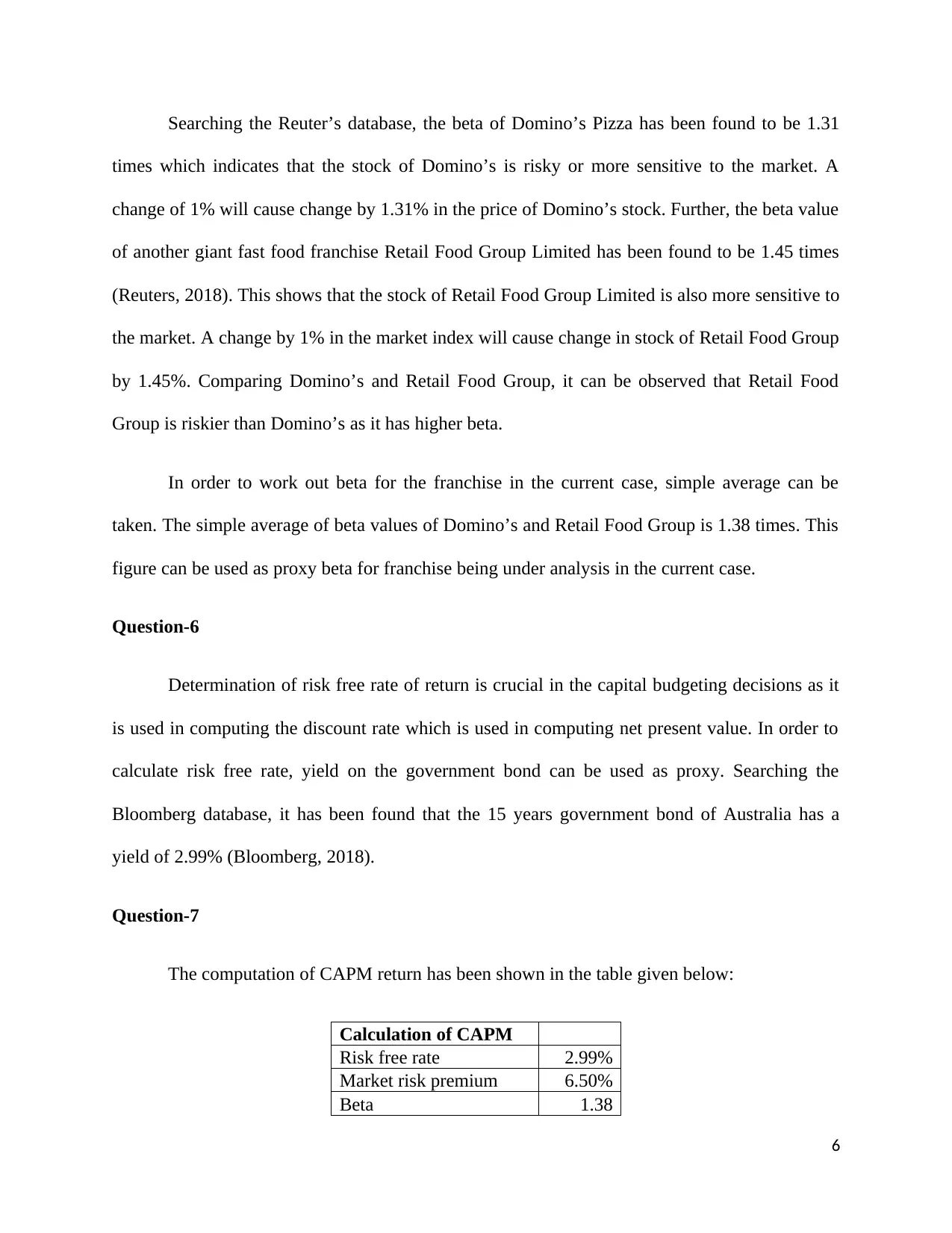

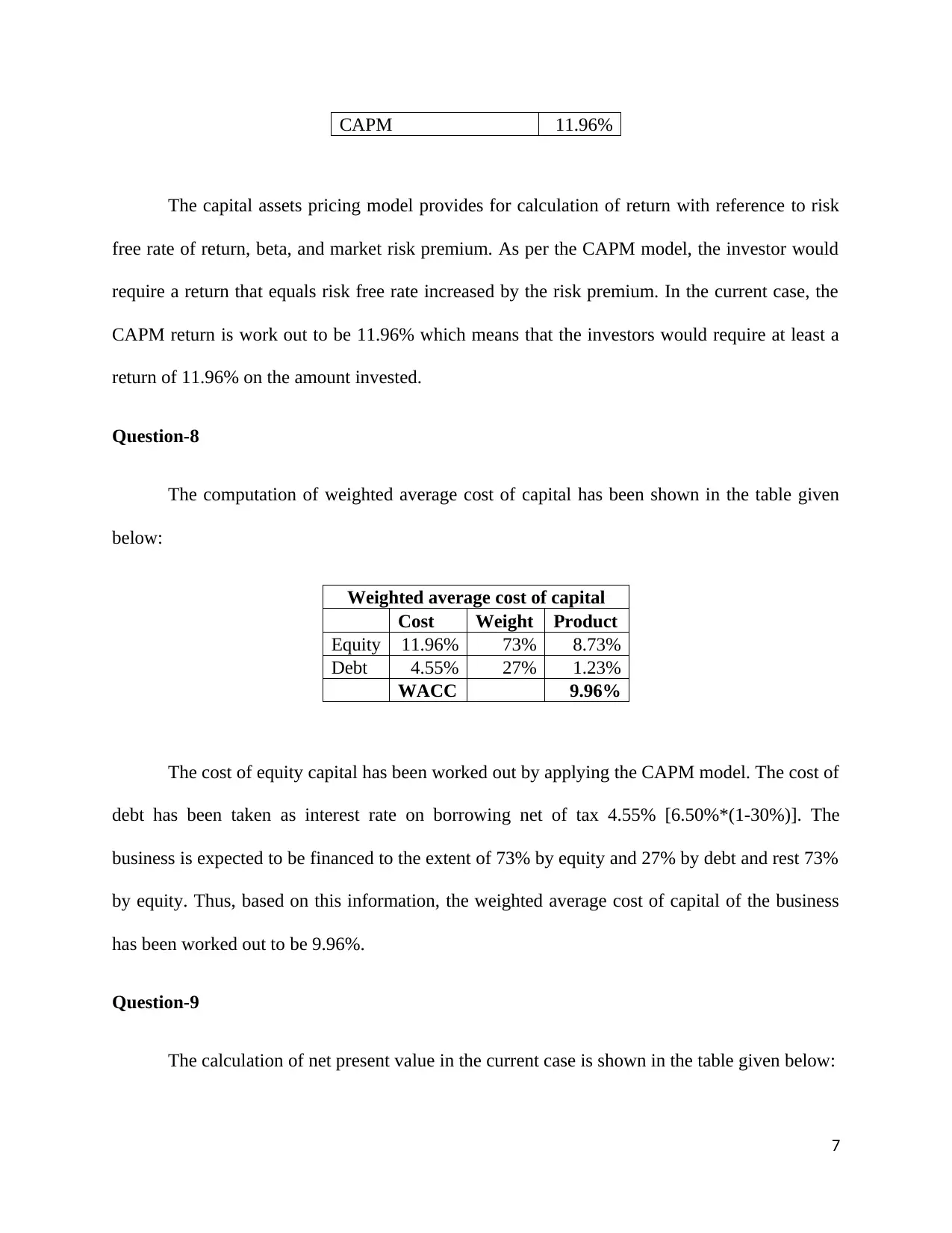

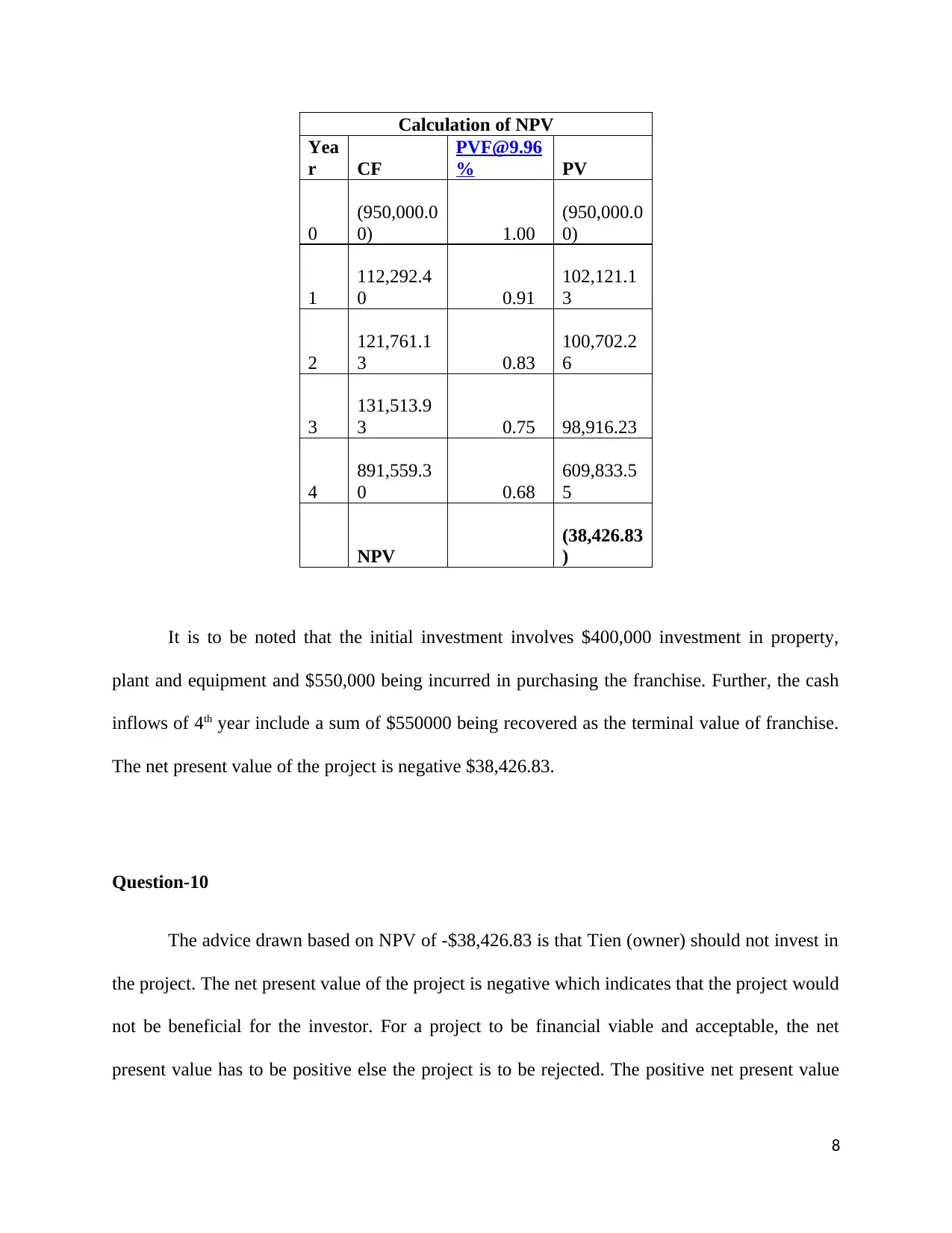

This report presents a comprehensive financial analysis of a proposed pizza franchise investment. It begins by calculating the required number of pizzas to achieve a desired rate of return, considering capital invested, fixed costs, and contribution margin. The report then projects the franchise's income statement for the first year, detailing revenues, variable costs, fixed costs, and net income after tax. Free cash flows from operations are computed using the indirect method, and projections are made for the subsequent three years, considering a 3% annual increase in pizza sales and contribution. The analysis also includes the determination of beta, risk-free rate, and market risk premium to calculate the Capital Asset Pricing Model (CAPM) return and Weighted Average Cost of Capital (WACC). Finally, the Net Present Value (NPV) of the project is calculated, leading to the conclusion that the investment should not be undertaken due to a negative NPV. The report also discusses various risk considerations and provides a list of references.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.