Business Planning Report: Budgeted vs. Actual Financial Statement

VerifiedAdded on 2023/06/12

|17

|3038

|398

Report

AI Summary

This report analyzes a company's financial performance by comparing budgeted and actual figures. It includes a profit and loss statement and a statement of financial position for both budgeted and actual data. The report discusses budgeted and actual costs, sales, gross profit, and operating profit, supported by charts for clarity. Ratio calculations are performed to interpret the company's performance, focusing on profitability and liquidity. The analysis reveals that while the company's performance was generally satisfactory, it did not consistently meet budgeted expectations, particularly in gross profit. The report concludes that the company needs to address inconsistencies in its performance and carefully monitor costs to improve profitability.

BUSINESS PLANNING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTIO..............................................................................................................................3

REPORT SUMMARY.....................................................................................................................3

PREPARATION OF BUDGETED STATEMENT OF PROFIT & LOSS ACCOUNT............3

PREPARATION OF ACTUAL STATEMENT OF PROFIT & LOSS ACCOUNT..................4

PREPARATION OF BUDGETED STATEMENT OF FINANCIAL POSITION FOR THE

FINANCIAL YEAR....................................................................................................................5

PREPARATION OF ACTUAL STATEMENT OF FINANCIAL POSITION FOR THE

FINANCIAL YEAR....................................................................................................................6

COMMENTS ON BUDGETED COST..........................................................................................7

COMMENTS ON ACTUAL COST................................................................................................9

COMMENTS ON SALES, GROSS PROFIT AND OPERATING PROFIT...............................11

RATIO CALCULATION AND INTERPRETATION ON PERFORMANCE OF COMPANY

....................................................................................................................................................12

INTERPRETATION OF LIQUIDITY RATIO-.......................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................14

INTRODUCTIO..............................................................................................................................3

REPORT SUMMARY.....................................................................................................................3

PREPARATION OF BUDGETED STATEMENT OF PROFIT & LOSS ACCOUNT............3

PREPARATION OF ACTUAL STATEMENT OF PROFIT & LOSS ACCOUNT..................4

PREPARATION OF BUDGETED STATEMENT OF FINANCIAL POSITION FOR THE

FINANCIAL YEAR....................................................................................................................5

PREPARATION OF ACTUAL STATEMENT OF FINANCIAL POSITION FOR THE

FINANCIAL YEAR....................................................................................................................6

COMMENTS ON BUDGETED COST..........................................................................................7

COMMENTS ON ACTUAL COST................................................................................................9

COMMENTS ON SALES, GROSS PROFIT AND OPERATING PROFIT...............................11

RATIO CALCULATION AND INTERPRETATION ON PERFORMANCE OF COMPANY

....................................................................................................................................................12

INTERPRETATION OF LIQUIDITY RATIO-.......................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................14

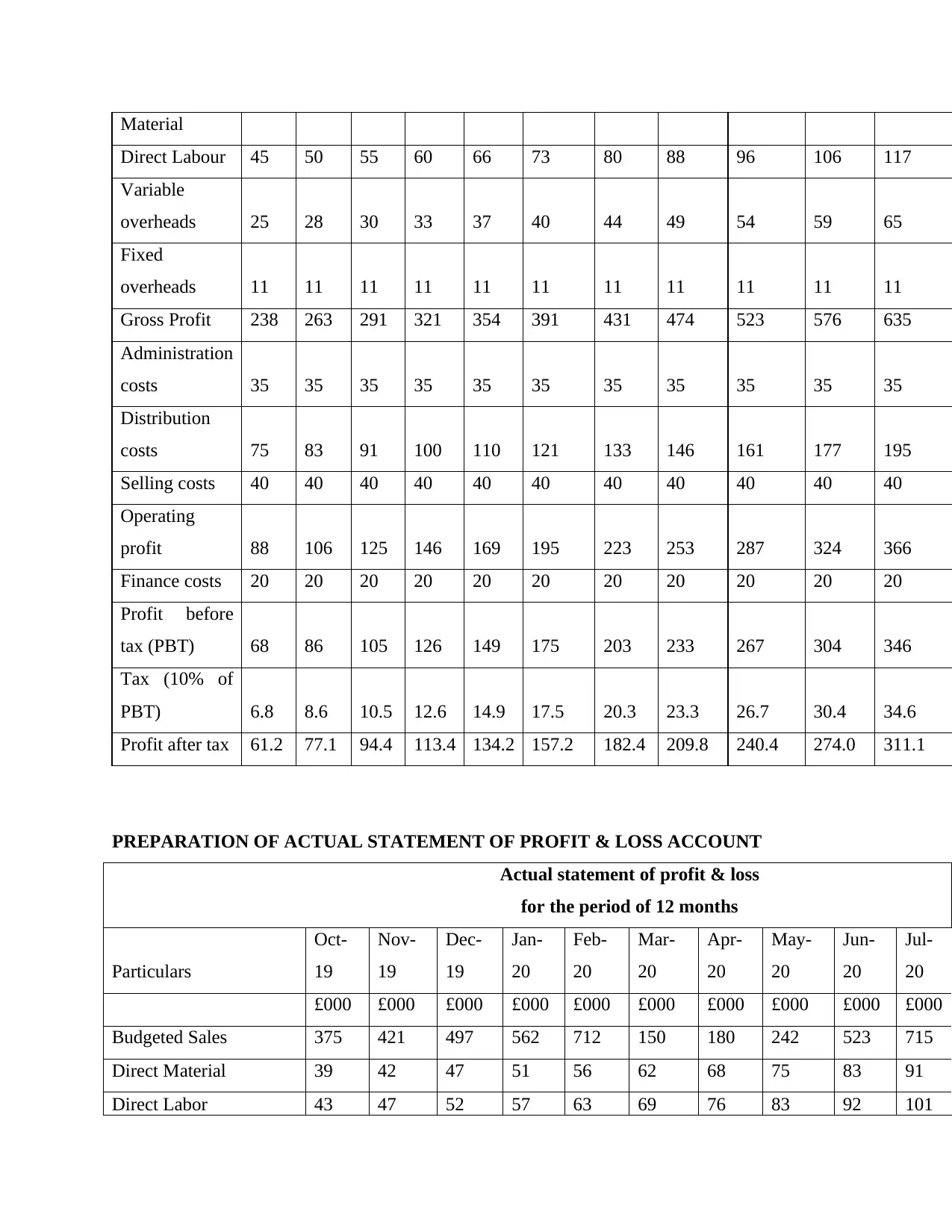

INTRODUCTIO

Business planning is the process of anticipation of future outcomes in order to make an

impactful plan to carry out business (Shubita, 2019) The report will be discussing how the entity

has performed relative to the budget. It will be discussing profit and loss statement for the

company for both budgeted and actual figures. Along with its financial position statement would

also be made separately for both budgeted and actual figures, further with regard to the

calculations various charts will also be fabricated to make the picture clearer. At the end of the

report ratios would be calculated and substantiated with interpretation.

REPORT SUMMARY

The performance of the company over the year has been good but not as it was expected

since the budgeted gross profit for the year was 5198 (in 000) but actually it has been 4101

which is less than the budgeted figures. Performance of the company is satisfactory the gross

profits in the initial months were exceeding budgeted figures but after initial five months it took

a sharp turn in adverse direction and from sixth month it came in negative figure. Then it has

shown good recovery and came to positive number and in following months again it started

following the budgeted data but could not over step (Bužinskienė, 2019) At last in the last month

the actual sales crossed the budgeted in great manner. Altogether it can be concluded that the

performance has not shown consistency throughout the year.

PREPARATION OF BUDGETED STATEMENT OF PROFIT & LOSS ACCOUNT

Budgeted statement of profit & loss

for the period of 12 months

Particulars

Oct-

19

Nov-

19

Dec-

19

Jan-

20

Feb-

20

Mar-

20

Apr-

20

May-

20 Jun-20 Jul-20 Aug-20

£000 £000 £000 £000 £000 £000 £000 £000 £000 £000 £000

Budgeted

Sales 354 390 429 472 519 571 628 690 759 835 919

Direct 35 39 42 47 51 56 62 68 75 83 91

Business planning is the process of anticipation of future outcomes in order to make an

impactful plan to carry out business (Shubita, 2019) The report will be discussing how the entity

has performed relative to the budget. It will be discussing profit and loss statement for the

company for both budgeted and actual figures. Along with its financial position statement would

also be made separately for both budgeted and actual figures, further with regard to the

calculations various charts will also be fabricated to make the picture clearer. At the end of the

report ratios would be calculated and substantiated with interpretation.

REPORT SUMMARY

The performance of the company over the year has been good but not as it was expected

since the budgeted gross profit for the year was 5198 (in 000) but actually it has been 4101

which is less than the budgeted figures. Performance of the company is satisfactory the gross

profits in the initial months were exceeding budgeted figures but after initial five months it took

a sharp turn in adverse direction and from sixth month it came in negative figure. Then it has

shown good recovery and came to positive number and in following months again it started

following the budgeted data but could not over step (Bužinskienė, 2019) At last in the last month

the actual sales crossed the budgeted in great manner. Altogether it can be concluded that the

performance has not shown consistency throughout the year.

PREPARATION OF BUDGETED STATEMENT OF PROFIT & LOSS ACCOUNT

Budgeted statement of profit & loss

for the period of 12 months

Particulars

Oct-

19

Nov-

19

Dec-

19

Jan-

20

Feb-

20

Mar-

20

Apr-

20

May-

20 Jun-20 Jul-20 Aug-20

£000 £000 £000 £000 £000 £000 £000 £000 £000 £000 £000

Budgeted

Sales 354 390 429 472 519 571 628 690 759 835 919

Direct 35 39 42 47 51 56 62 68 75 83 91

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Material

Direct Labour 45 50 55 60 66 73 80 88 96 106 117

Variable

overheads 25 28 30 33 37 40 44 49 54 59 65

Fixed

overheads 11 11 11 11 11 11 11 11 11 11 11

Gross Profit 238 263 291 321 354 391 431 474 523 576 635

Administration

costs 35 35 35 35 35 35 35 35 35 35 35

Distribution

costs 75 83 91 100 110 121 133 146 161 177 195

Selling costs 40 40 40 40 40 40 40 40 40 40 40

Operating

profit 88 106 125 146 169 195 223 253 287 324 366

Finance costs 20 20 20 20 20 20 20 20 20 20 20

Profit before

tax (PBT) 68 86 105 126 149 175 203 233 267 304 346

Tax (10% of

PBT) 6.8 8.6 10.5 12.6 14.9 17.5 20.3 23.3 26.7 30.4 34.6

Profit after tax 61.2 77.1 94.4 113.4 134.2 157.2 182.4 209.8 240.4 274.0 311.1

PREPARATION OF ACTUAL STATEMENT OF PROFIT & LOSS ACCOUNT

Actual statement of profit & loss

for the period of 12 months

Particulars

Oct-

19

Nov-

19

Dec-

19

Jan-

20

Feb-

20

Mar-

20

Apr-

20

May-

20

Jun-

20

Jul-

20

£000 £000 £000 £000 £000 £000 £000 £000 £000 £000

Budgeted Sales 375 421 497 562 712 150 180 242 523 715

Direct Material 39 42 47 51 56 62 68 75 83 91

Direct Labor 43 47 52 57 63 69 76 83 92 101

Direct Labour 45 50 55 60 66 73 80 88 96 106 117

Variable

overheads 25 28 30 33 37 40 44 49 54 59 65

Fixed

overheads 11 11 11 11 11 11 11 11 11 11 11

Gross Profit 238 263 291 321 354 391 431 474 523 576 635

Administration

costs 35 35 35 35 35 35 35 35 35 35 35

Distribution

costs 75 83 91 100 110 121 133 146 161 177 195

Selling costs 40 40 40 40 40 40 40 40 40 40 40

Operating

profit 88 106 125 146 169 195 223 253 287 324 366

Finance costs 20 20 20 20 20 20 20 20 20 20 20

Profit before

tax (PBT) 68 86 105 126 149 175 203 233 267 304 346

Tax (10% of

PBT) 6.8 8.6 10.5 12.6 14.9 17.5 20.3 23.3 26.7 30.4 34.6

Profit after tax 61.2 77.1 94.4 113.4 134.2 157.2 182.4 209.8 240.4 274.0 311.1

PREPARATION OF ACTUAL STATEMENT OF PROFIT & LOSS ACCOUNT

Actual statement of profit & loss

for the period of 12 months

Particulars

Oct-

19

Nov-

19

Dec-

19

Jan-

20

Feb-

20

Mar-

20

Apr-

20

May-

20

Jun-

20

Jul-

20

£000 £000 £000 £000 £000 £000 £000 £000 £000 £000

Budgeted Sales 375 421 497 562 712 150 180 242 523 715

Direct Material 39 42 47 51 56 62 68 75 83 91

Direct Labor 43 47 52 57 63 69 76 83 92 101

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable overheads 24 27 29 32 36 39 43 47 52 57

Fixed overheads 14 14 14 14 14 14 14 14 14 14

Gross Profit 256 291 355 407 543 -34 -21 22 283 452

Administration costs 30 30 30 30 30 30 30 30 30 30

Distribution costs 77 84 93 102 112 123 136 149 164 180

Selling costs 35 35 35 35 35 35 35 35 35 35

Operating profit 114 141 197 240 366 -223 -222 -192 54 207

Finance costs 16 16 16 16 16 16 16 16 16 16

Profit before tax (PBT) 98 125 181 224 350 -239 -238 -208 38 191

Tax (10% of PBT) 9.8 12.5 18.1 22.4 35.0 -23.9 -23.8 -20.8 3.8 19.1

Profit after tax 88.2 112.9 163.3 201.9 315.2 -214.7

-

214.1 -187.0 34.0 171.6

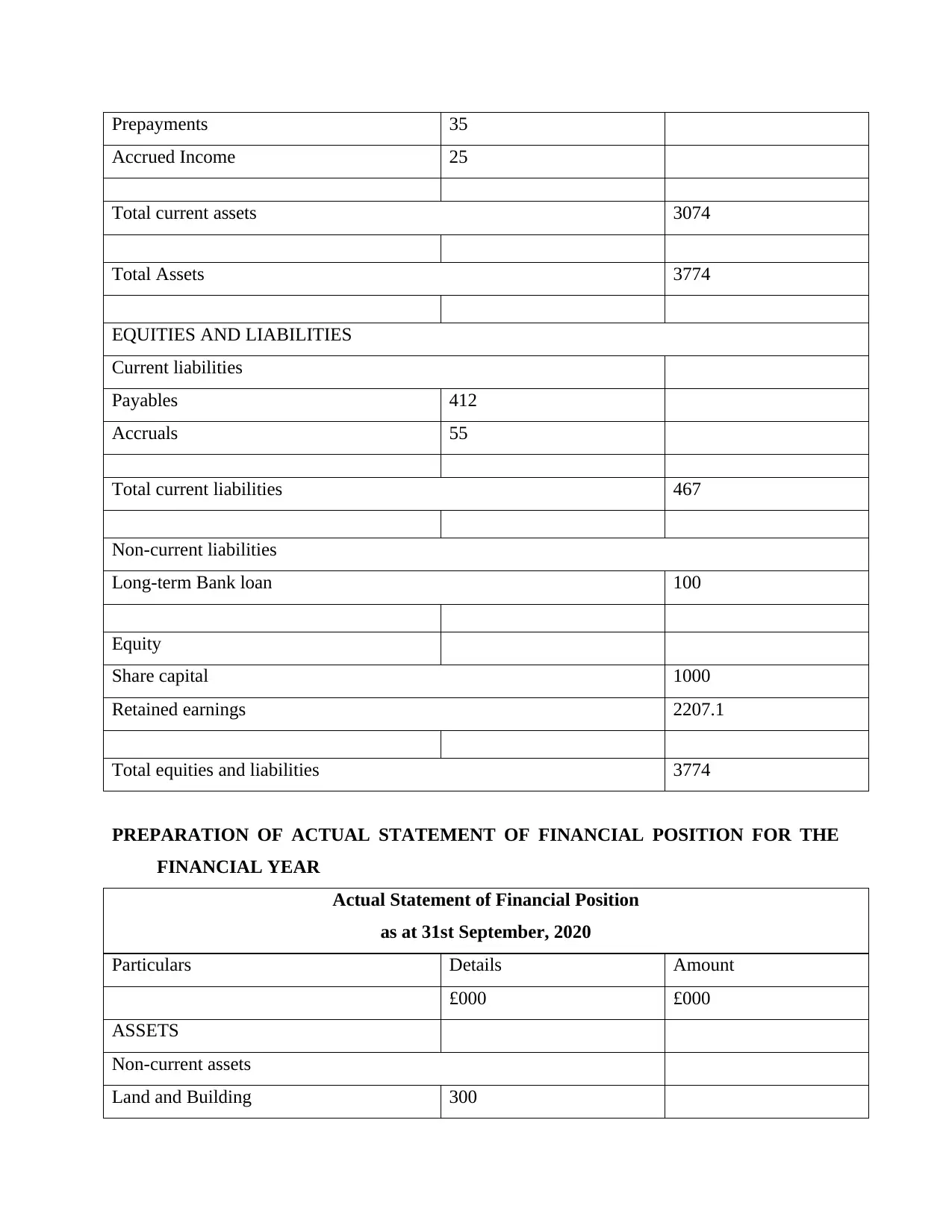

PREPARATION OF BUDGETED STATEMENT OF FINANCIAL POSITION FOR THE

FINANCIAL YEAR

Budgeted Statement of Financial Position

as at 31st September, 2020

Particulars Details Amount

£000 £000

ASSETS

Non-current assets

Land and Building 300

Plant and machinery 400

Total non-current assets 700

Current assets

Cash 500

Receivables 1894

Inventory 620

Fixed overheads 14 14 14 14 14 14 14 14 14 14

Gross Profit 256 291 355 407 543 -34 -21 22 283 452

Administration costs 30 30 30 30 30 30 30 30 30 30

Distribution costs 77 84 93 102 112 123 136 149 164 180

Selling costs 35 35 35 35 35 35 35 35 35 35

Operating profit 114 141 197 240 366 -223 -222 -192 54 207

Finance costs 16 16 16 16 16 16 16 16 16 16

Profit before tax (PBT) 98 125 181 224 350 -239 -238 -208 38 191

Tax (10% of PBT) 9.8 12.5 18.1 22.4 35.0 -23.9 -23.8 -20.8 3.8 19.1

Profit after tax 88.2 112.9 163.3 201.9 315.2 -214.7

-

214.1 -187.0 34.0 171.6

PREPARATION OF BUDGETED STATEMENT OF FINANCIAL POSITION FOR THE

FINANCIAL YEAR

Budgeted Statement of Financial Position

as at 31st September, 2020

Particulars Details Amount

£000 £000

ASSETS

Non-current assets

Land and Building 300

Plant and machinery 400

Total non-current assets 700

Current assets

Cash 500

Receivables 1894

Inventory 620

Prepayments 35

Accrued Income 25

Total current assets 3074

Total Assets 3774

EQUITIES AND LIABILITIES

Current liabilities

Payables 412

Accruals 55

Total current liabilities 467

Non-current liabilities

Long-term Bank loan 100

Equity

Share capital 1000

Retained earnings 2207.1

Total equities and liabilities 3774

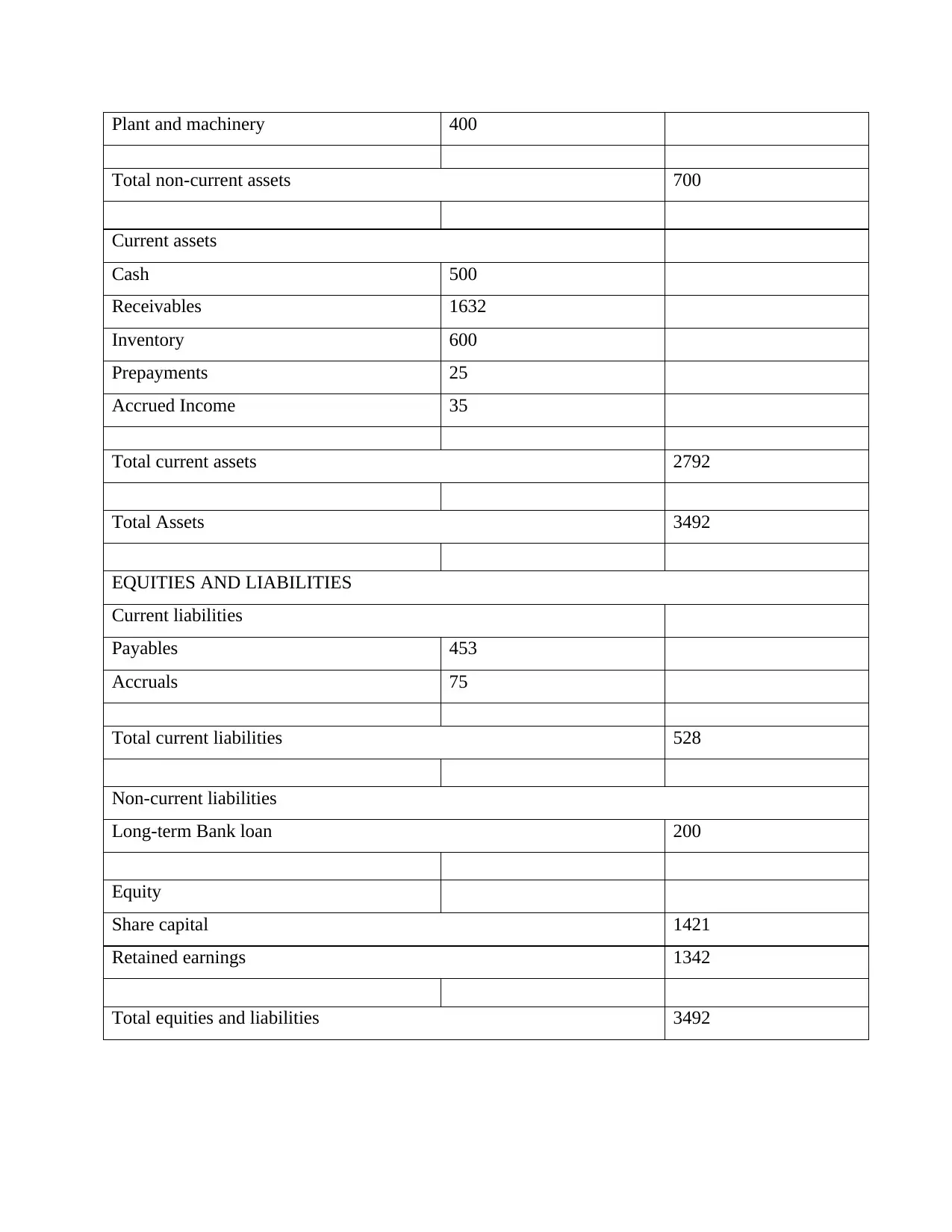

PREPARATION OF ACTUAL STATEMENT OF FINANCIAL POSITION FOR THE

FINANCIAL YEAR

Actual Statement of Financial Position

as at 31st September, 2020

Particulars Details Amount

£000 £000

ASSETS

Non-current assets

Land and Building 300

Accrued Income 25

Total current assets 3074

Total Assets 3774

EQUITIES AND LIABILITIES

Current liabilities

Payables 412

Accruals 55

Total current liabilities 467

Non-current liabilities

Long-term Bank loan 100

Equity

Share capital 1000

Retained earnings 2207.1

Total equities and liabilities 3774

PREPARATION OF ACTUAL STATEMENT OF FINANCIAL POSITION FOR THE

FINANCIAL YEAR

Actual Statement of Financial Position

as at 31st September, 2020

Particulars Details Amount

£000 £000

ASSETS

Non-current assets

Land and Building 300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Plant and machinery 400

Total non-current assets 700

Current assets

Cash 500

Receivables 1632

Inventory 600

Prepayments 25

Accrued Income 35

Total current assets 2792

Total Assets 3492

EQUITIES AND LIABILITIES

Current liabilities

Payables 453

Accruals 75

Total current liabilities 528

Non-current liabilities

Long-term Bank loan 200

Equity

Share capital 1421

Retained earnings 1342

Total equities and liabilities 3492

Total non-current assets 700

Current assets

Cash 500

Receivables 1632

Inventory 600

Prepayments 25

Accrued Income 35

Total current assets 2792

Total Assets 3492

EQUITIES AND LIABILITIES

Current liabilities

Payables 453

Accruals 75

Total current liabilities 528

Non-current liabilities

Long-term Bank loan 200

Equity

Share capital 1421

Retained earnings 1342

Total equities and liabilities 3492

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

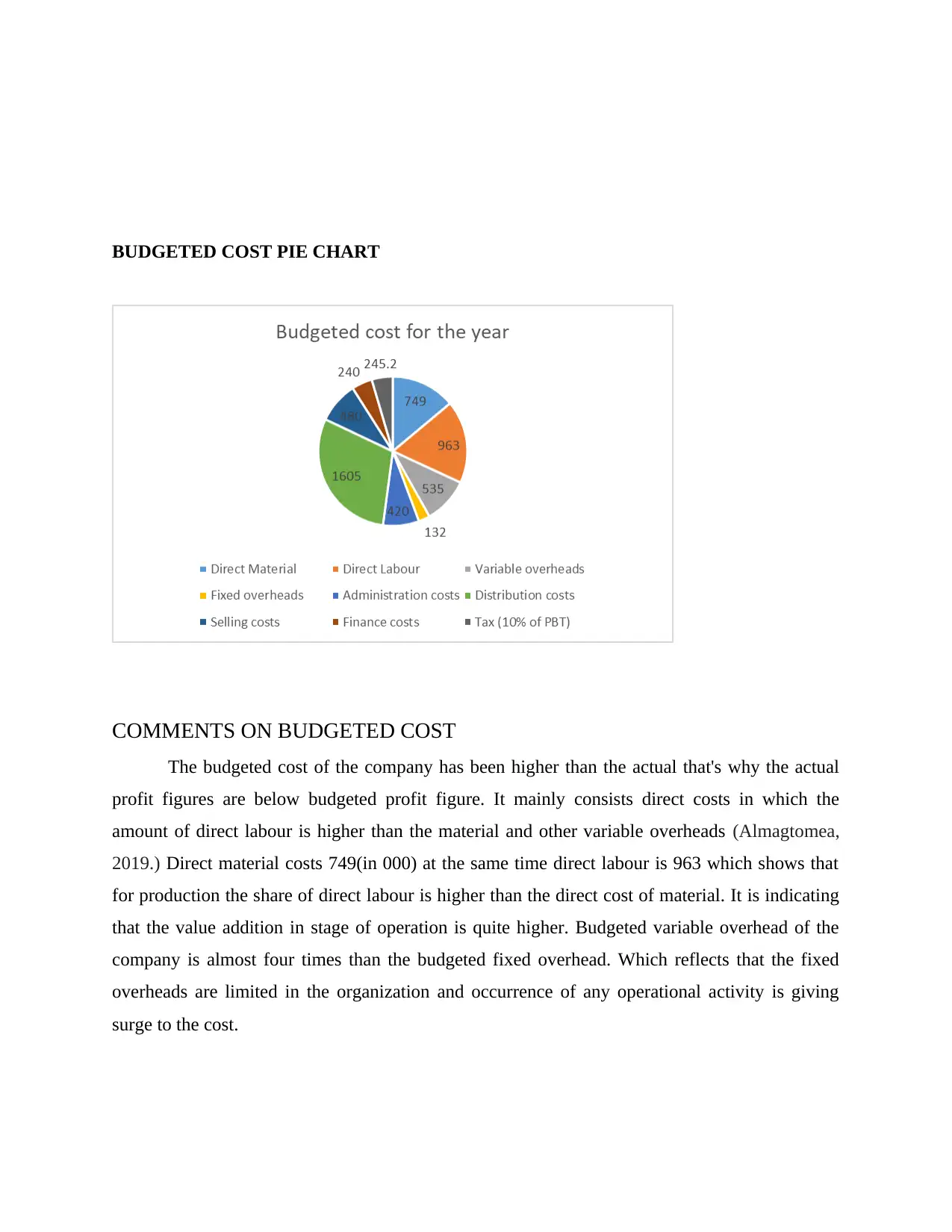

BUDGETED COST PIE CHART

COMMENTS ON BUDGETED COST

The budgeted cost of the company has been higher than the actual that's why the actual

profit figures are below budgeted profit figure. It mainly consists direct costs in which the

amount of direct labour is higher than the material and other variable overheads (Almagtomea,

2019.) Direct material costs 749(in 000) at the same time direct labour is 963 which shows that

for production the share of direct labour is higher than the direct cost of material. It is indicating

that the value addition in stage of operation is quite higher. Budgeted variable overhead of the

company is almost four times than the budgeted fixed overhead. Which reflects that the fixed

overheads are limited in the organization and occurrence of any operational activity is giving

surge to the cost.

COMMENTS ON BUDGETED COST

The budgeted cost of the company has been higher than the actual that's why the actual

profit figures are below budgeted profit figure. It mainly consists direct costs in which the

amount of direct labour is higher than the material and other variable overheads (Almagtomea,

2019.) Direct material costs 749(in 000) at the same time direct labour is 963 which shows that

for production the share of direct labour is higher than the direct cost of material. It is indicating

that the value addition in stage of operation is quite higher. Budgeted variable overhead of the

company is almost four times than the budgeted fixed overhead. Which reflects that the fixed

overheads are limited in the organization and occurrence of any operational activity is giving

surge to the cost.

The administrative cost of the entity is 420(in 000) which is more than three times of

fixed overhead which shows that the company has budgeted higher amount to its administrative

actions. It may be seen from different angle as well since if it is seen relatively yet the

administrative cost is quite higher than fixed overhead. The biggest component of the budgeted

cost is distribution cost. Which is in four figures and constituting a huge share of total budgeted

cost of the company. It is 1605 which is almost double or more than double of direct material

and almost three times of variable overhead. It shows that as per the anticoagulation of the entity

they are looking for most efforts in distribution. If we compare it with the prime cost yet it is

significant (Gamayuni, 2018.)

The budgeted prime cost is 1712 which is a bit more than the budgeted distribution cost.

Budgeted selling cost of the company is around fourth part of the distribution cost. It shows that

the company wants to pay more attention to its selling and distribution functions. Financial cost

of the organization is just 240 which is satisfactory since shows that the company is more relying

on equity so the fixed costs are expected lower. But it would impact while paying tax because the

amount paid to load providers is exempted and this is the reason company is anticipating to pay

around 245.2 as tax.

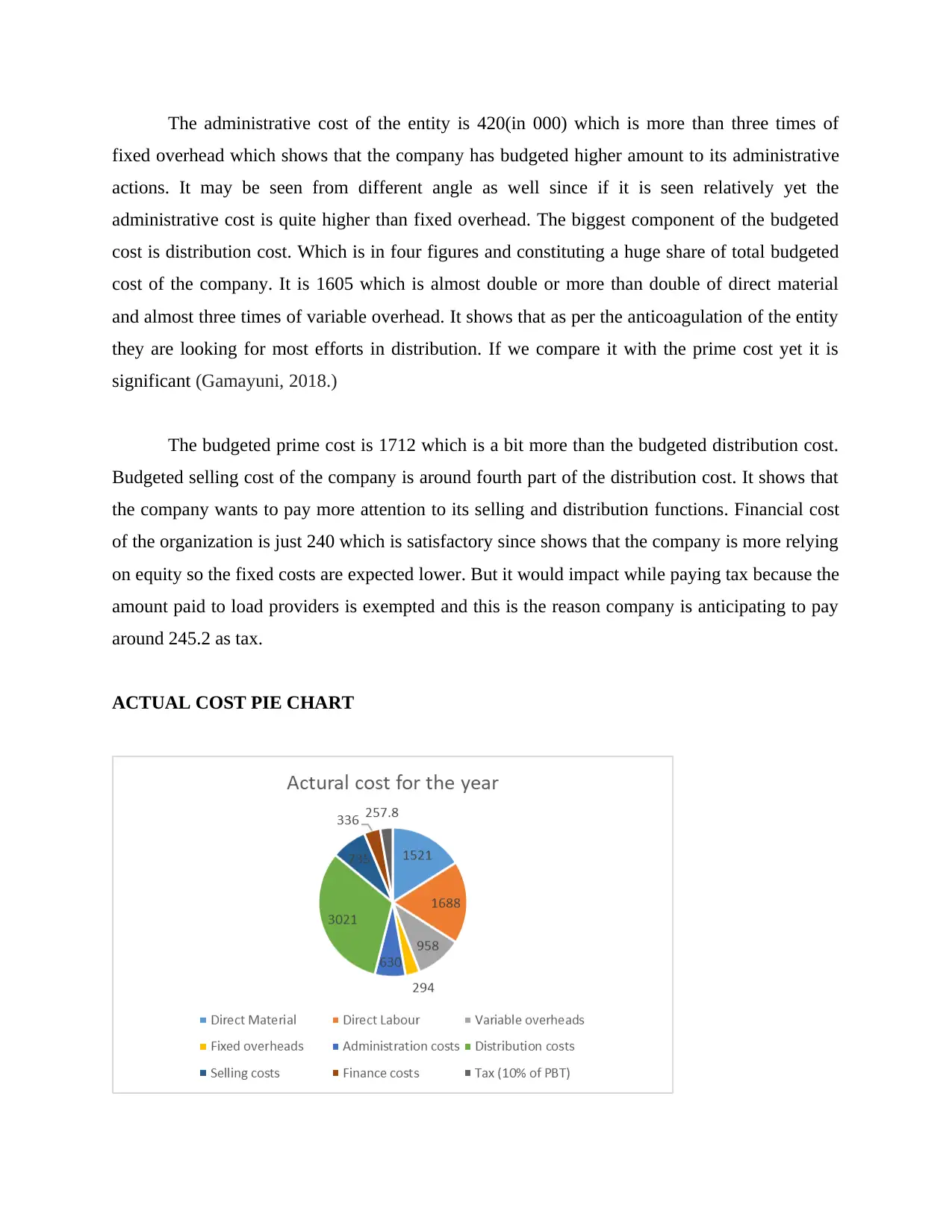

ACTUAL COST PIE CHART

fixed overhead which shows that the company has budgeted higher amount to its administrative

actions. It may be seen from different angle as well since if it is seen relatively yet the

administrative cost is quite higher than fixed overhead. The biggest component of the budgeted

cost is distribution cost. Which is in four figures and constituting a huge share of total budgeted

cost of the company. It is 1605 which is almost double or more than double of direct material

and almost three times of variable overhead. It shows that as per the anticoagulation of the entity

they are looking for most efforts in distribution. If we compare it with the prime cost yet it is

significant (Gamayuni, 2018.)

The budgeted prime cost is 1712 which is a bit more than the budgeted distribution cost.

Budgeted selling cost of the company is around fourth part of the distribution cost. It shows that

the company wants to pay more attention to its selling and distribution functions. Financial cost

of the organization is just 240 which is satisfactory since shows that the company is more relying

on equity so the fixed costs are expected lower. But it would impact while paying tax because the

amount paid to load providers is exempted and this is the reason company is anticipating to pay

around 245.2 as tax.

ACTUAL COST PIE CHART

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COMMENTS ON ACTUAL COST

The company had generated fewer profits due to many reasons like lower sales than

budgeted and in a few areas occurred more costs as well. The cost of direct material has been

higher than it was budgeted which impacted the prime cost figures of the entity. On the other

side as it can be seen in the chart the actual cost of direct labour is lower than the budgeted which

has been a positive in operation phase. Company also showed its better control on variable

overhead management since it is directly related to the functional stage where controlling is a

tougher thing yet it has been lower than the budgeted figure but the fixed overheads of the

company has been higher than anticipation it was expected to be 132 (in 000) but in reality it was

168. Here it is prominent for the organization to put this thing into consideration and examine the

key factors which might have impacted the predictions (Pamungkas, 2018.)

Distribution cost of the company is 1637 whereas the budgeted was 1605 so there is not

such a substantial variation yet it is matter of contemplation. Last three components of the

company has been good since they are better than they were supposed. Selling cost, financial

cost and tax are orderly 420, 192, 149.1 by seeing the high amount of operational costs such

figures are better (Adrianto and Wahyuni, 2019)

If we see it from the comparison point of view, then it is matter of joy for the business

because all these components are lower than the budgeted costs. But here it is important to take

one thing into focus that these figures are lower due to a reason and it is lower sales which is

leading it. The actual sales of the company have been lower than anticipation and selling cost,

tax amounts are directly related to the amount of sales so be seeing the chart and relevant figures

it can be said that these figures are lower not due to better control but vastly due to lower sales.

COMPARISION OF BUDGETED AND ACTUAL SALES, GROSS PROFIT AND

OPERATIONAL PROFIT

The company had generated fewer profits due to many reasons like lower sales than

budgeted and in a few areas occurred more costs as well. The cost of direct material has been

higher than it was budgeted which impacted the prime cost figures of the entity. On the other

side as it can be seen in the chart the actual cost of direct labour is lower than the budgeted which

has been a positive in operation phase. Company also showed its better control on variable

overhead management since it is directly related to the functional stage where controlling is a

tougher thing yet it has been lower than the budgeted figure but the fixed overheads of the

company has been higher than anticipation it was expected to be 132 (in 000) but in reality it was

168. Here it is prominent for the organization to put this thing into consideration and examine the

key factors which might have impacted the predictions (Pamungkas, 2018.)

Distribution cost of the company is 1637 whereas the budgeted was 1605 so there is not

such a substantial variation yet it is matter of contemplation. Last three components of the

company has been good since they are better than they were supposed. Selling cost, financial

cost and tax are orderly 420, 192, 149.1 by seeing the high amount of operational costs such

figures are better (Adrianto and Wahyuni, 2019)

If we see it from the comparison point of view, then it is matter of joy for the business

because all these components are lower than the budgeted costs. But here it is important to take

one thing into focus that these figures are lower due to a reason and it is lower sales which is

leading it. The actual sales of the company have been lower than anticipation and selling cost,

tax amounts are directly related to the amount of sales so be seeing the chart and relevant figures

it can be said that these figures are lower not due to better control but vastly due to lower sales.

COMPARISION OF BUDGETED AND ACTUAL SALES, GROSS PROFIT AND

OPERATIONAL PROFIT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

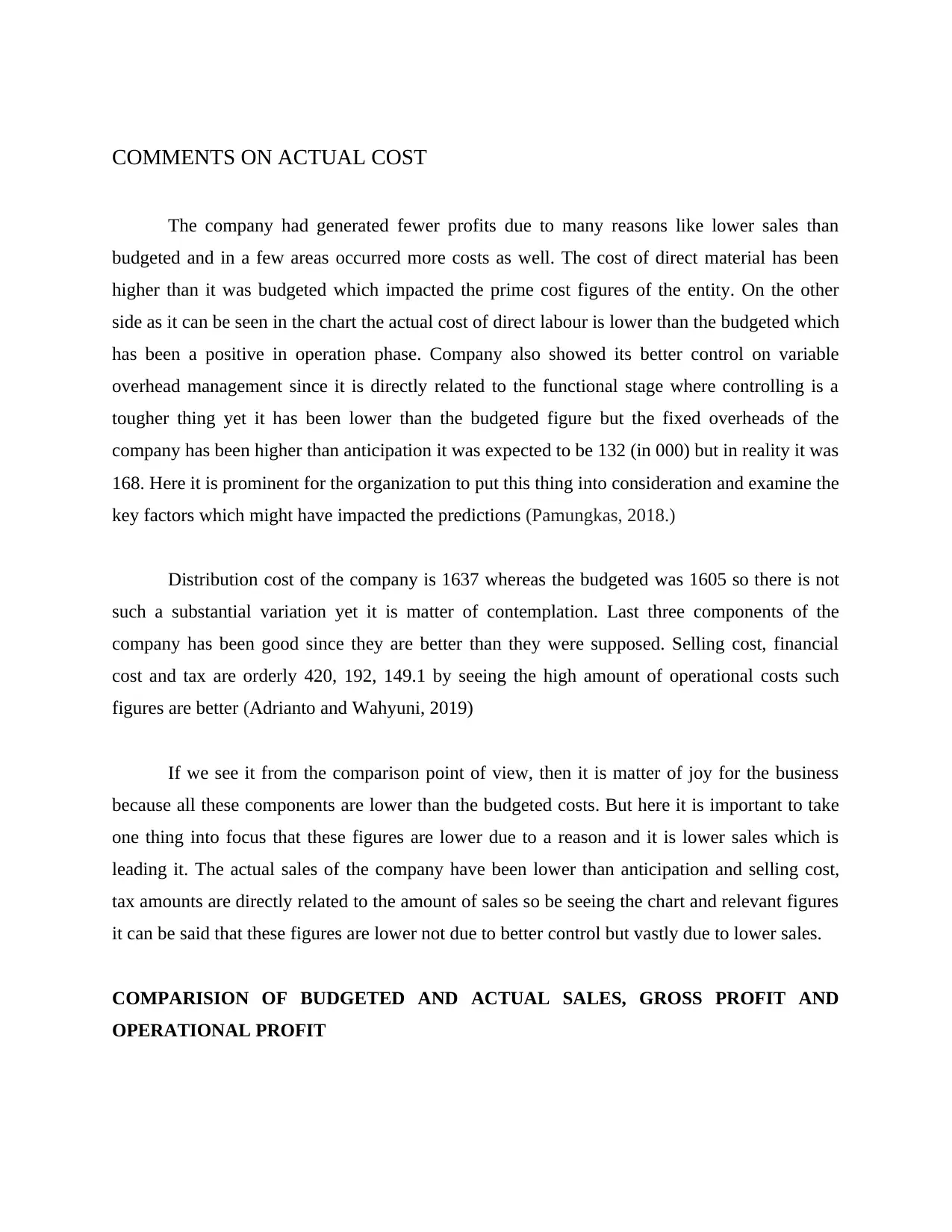

COMMENTS ON SALES, GROSS PROFIT AND OPERATING PROFIT

The sales line graphs of the company are showing a drastic variation between budgeted

and actual sales. In the initial months the actual sales were riding over the budgeted sales but

from February it dived and then it took more than six months for getting its position back. At last

in august it again crossed the budgeted line, After January the only month in which it has shown

sharp upside growth is September (Setiyani, 2018. )

The graph of budgeted and actual gross profit is showing the same pattern as sales

showed due to direct relationship of sales and gross profit of an organization. The gross profit is

also following the same trend and having direct implications of sales of the company. That's why

actual gross profit of the entity has been lower till the time when sales have been in negative

figure.

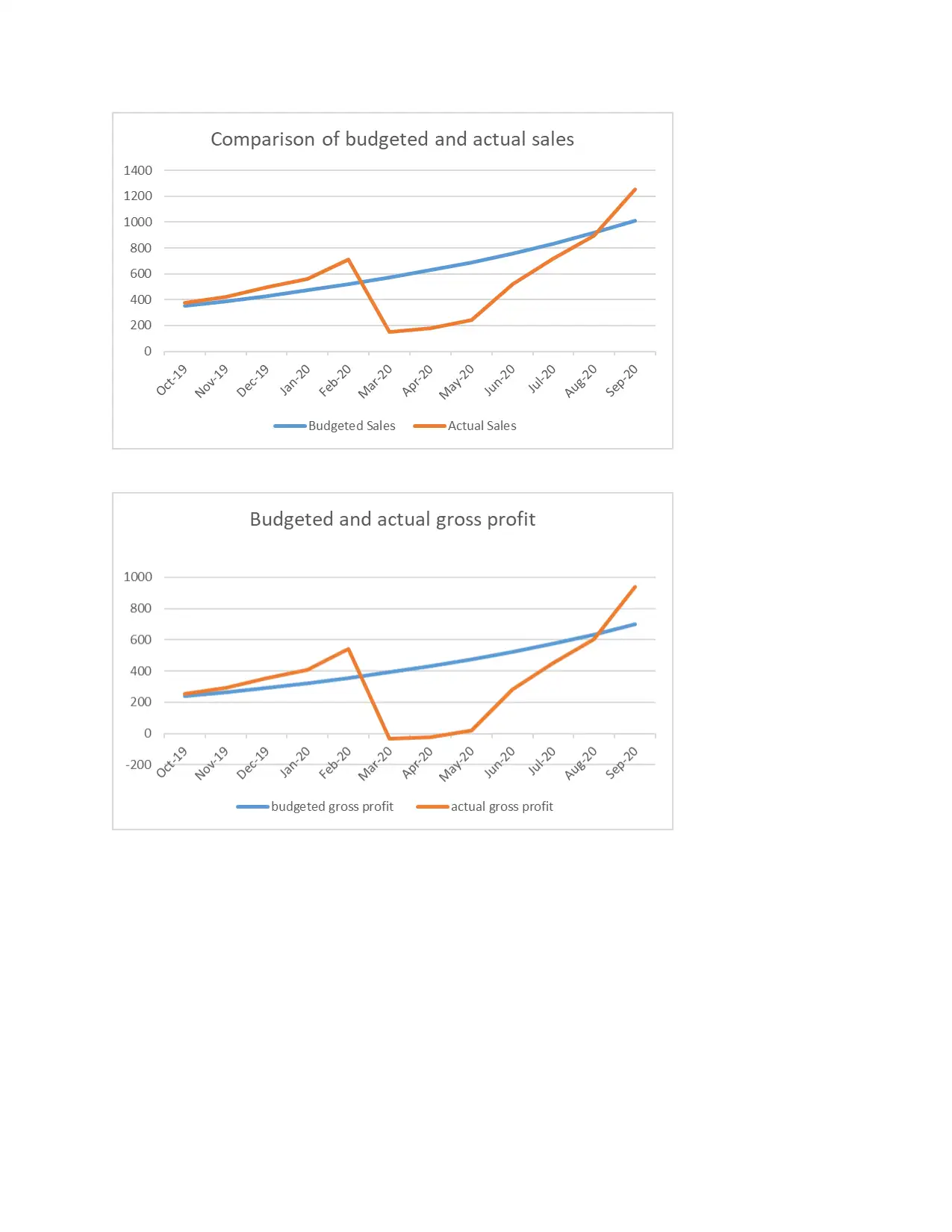

Operational profits of an organization depend on the operational efficiency of the entity.

In the graph it can be seen that from march to august in which company could not able to achieve

its budgeted operational performance and which caused low amount of operational profits to the

organization.

The sales line graphs of the company are showing a drastic variation between budgeted

and actual sales. In the initial months the actual sales were riding over the budgeted sales but

from February it dived and then it took more than six months for getting its position back. At last

in august it again crossed the budgeted line, After January the only month in which it has shown

sharp upside growth is September (Setiyani, 2018. )

The graph of budgeted and actual gross profit is showing the same pattern as sales

showed due to direct relationship of sales and gross profit of an organization. The gross profit is

also following the same trend and having direct implications of sales of the company. That's why

actual gross profit of the entity has been lower till the time when sales have been in negative

figure.

Operational profits of an organization depend on the operational efficiency of the entity.

In the graph it can be seen that from march to august in which company could not able to achieve

its budgeted operational performance and which caused low amount of operational profits to the

organization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.