Financial Analysis Report on Accounting Policies and Estimates of PPE

VerifiedAdded on 2022/10/03

|12

|2187

|5

Report

AI Summary

This report provides a detailed financial analysis of accounting policies and estimates related to Property, Plant, and Equipment (PPE), with a focus on the application of AASB 116. The report begins with an executive summary and table of contents, followed by an introduction that establishes the context of PPE accounting treatment according to AASB 116, using Caltex Limited as a case study. The discussion section addresses key questions, including the selection and changes in accounting policies as per AASB 108, the impact of professional judgment, and the specific accounting policies of Caltex Limited, particularly those concerning PPE valuation and depreciation. A critical evaluation of the accounting estimates and policies is presented, examining the impact of PPE on the company's financial position. The report concludes with recommendations for improvements in accounting estimates and policies, and references relevant accounting standards and literature. The report provides a comprehensive analysis of the accounting treatment of PPE, offering insights into the application of accounting standards and the impact on financial reporting.

Running head: ACCOUNTING FINANCIAL ANALYISIS REPORT

Accounting Financial analysis report

Name of Student:

Name of the University:

Authors’ note

Accounting Financial analysis report

Name of Student:

Name of the University:

Authors’ note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING FINANCIAL ANALYISIS REPORT

EXECUTIVE SUMMARY:

This completed report is providing a brief idea about the AASB 16 plant, property and

equipment. The application of AASB on Caltex limited and the probable impacts on overall

financial statements. In the first part of this report is providing the basic idea about

accounting policies and the effects of specific changes in polices. Next to this report is

presenting the annual report of the firm for the year 2018. The accounting estimates and

policies applied by the firm in the plant, property and the equipment have been explained.

The accounting policies implemented by the firm are all appropriate according to the

Australian accounting standard.

EXECUTIVE SUMMARY:

This completed report is providing a brief idea about the AASB 16 plant, property and

equipment. The application of AASB on Caltex limited and the probable impacts on overall

financial statements. In the first part of this report is providing the basic idea about

accounting policies and the effects of specific changes in polices. Next to this report is

presenting the annual report of the firm for the year 2018. The accounting estimates and

policies applied by the firm in the plant, property and the equipment have been explained.

The accounting policies implemented by the firm are all appropriate according to the

Australian accounting standard.

2ACCOUNTING FINANCIAL ANALYISIS REPORT

Table of Contents

Introduction................................................................................................................................3

Discussion:.................................................................................................................................3

Answer to question 1:.............................................................................................................3

Answer to question 2:.............................................................................................................4

Answer to question 3:.............................................................................................................6

Answer to question 4:.............................................................................................................7

Conclusion..................................................................................................................................7

References:.................................................................................................................................9

Appendix:.................................................................................................................................11

Table of Contents

Introduction................................................................................................................................3

Discussion:.................................................................................................................................3

Answer to question 1:.............................................................................................................3

Answer to question 2:.............................................................................................................4

Answer to question 3:.............................................................................................................6

Answer to question 4:.............................................................................................................7

Conclusion..................................................................................................................................7

References:.................................................................................................................................9

Appendix:.................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING FINANCIAL ANALYISIS REPORT

Introduction

According to the provision issued under AASB 116, the accounting treatment for

Plant, Property and Equipment is needed to present in the financial statement for providing

the overall financial condition of an organization during a particular time. The primary issues

for submitting the accounts for Plant, Property and Equipment is to recognize the assets,

determination of carrying amounts of such assets and also the depreciation amount that

charged and impairment losses that to be known about them (Laing and Perrin 2014).

Here for recognition, the plant, property and equipment selected a company which is

named as Caltex Limited. Caltex Limited Company is an oil company, which was established

in the year 1936 with the joint venture between the Texas Company and Standard Oil of

California (Caltex 2018).

Discussion:

Answer to question 1:

Selecting and changing Accounting policies as per AASB 108:

In accordance with the provision issued under AASB 108 paragraph 14, an entity

shall need to change in accounting policies if it is required as per the relevant Australian

accounting standard. The results of financial statements are providing the reliable and more

accurate and reliable information about the effects of transactions, other related events and

conditions on organizations’ financial position, performance or generated cash flows

(Standard 2015).

As per paragraph 15, generally, the users of financial statements are required to be

able to compare the financial statements of an organization’s financial positions, performance

Introduction

According to the provision issued under AASB 116, the accounting treatment for

Plant, Property and Equipment is needed to present in the financial statement for providing

the overall financial condition of an organization during a particular time. The primary issues

for submitting the accounts for Plant, Property and Equipment is to recognize the assets,

determination of carrying amounts of such assets and also the depreciation amount that

charged and impairment losses that to be known about them (Laing and Perrin 2014).

Here for recognition, the plant, property and equipment selected a company which is

named as Caltex Limited. Caltex Limited Company is an oil company, which was established

in the year 1936 with the joint venture between the Texas Company and Standard Oil of

California (Caltex 2018).

Discussion:

Answer to question 1:

Selecting and changing Accounting policies as per AASB 108:

In accordance with the provision issued under AASB 108 paragraph 14, an entity

shall need to change in accounting policies if it is required as per the relevant Australian

accounting standard. The results of financial statements are providing the reliable and more

accurate and reliable information about the effects of transactions, other related events and

conditions on organizations’ financial position, performance or generated cash flows

(Standard 2015).

As per paragraph 15, generally, the users of financial statements are required to be

able to compare the financial statements of an organization’s financial positions, performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING FINANCIAL ANALYISIS REPORT

and generated cash flows. In that case, the same accounting policies are continually applied

unless there is a change is occurred as per the criteria issued under paragraph 14.

As per paragraph 17, the initial application of a relevant policy which is related to the

revaluation of assets in accordance with the AASB 116 Plant, Property and Equipment.

AASB 138 intangible assets are typically changed its accounting policies in the case to deal

with as a revaluation following the standards.

Professional judgment impact accounting policies and estimates:

Generally, the professional judgements are defined as the application of relevant and

accumulated knowledge along with proper experience gained through the using of pertinent

accounting or auditing training. In other words, the standard judgemental power can provide

the favourable impacts in case of selection relevant accounting policies. Through the using of

accounting judgements, an organization can give necessary changes in case of its accounting

policies. With the expertise knowledge and judgements, such as like through the proper

managerial decisions by relevant persons an organization can able to make necessary changes

and implementing new accounting policies that influenced towards the favourable benefits of

the company (Davern et al. 2019).

Answer to question 2:

Accounting Policies of Caltex Limited:

In accordance with the Annual report issued by Caltex Limited 2018, while preparing

the consolidated financial statements, the management makes some relevant judgments,

estimations including some assumptions that affect in case of application of policies and also

reported to the amounts of assets, liabilities, incomes and expenses. Such estimates and

and generated cash flows. In that case, the same accounting policies are continually applied

unless there is a change is occurred as per the criteria issued under paragraph 14.

As per paragraph 17, the initial application of a relevant policy which is related to the

revaluation of assets in accordance with the AASB 116 Plant, Property and Equipment.

AASB 138 intangible assets are typically changed its accounting policies in the case to deal

with as a revaluation following the standards.

Professional judgment impact accounting policies and estimates:

Generally, the professional judgements are defined as the application of relevant and

accumulated knowledge along with proper experience gained through the using of pertinent

accounting or auditing training. In other words, the standard judgemental power can provide

the favourable impacts in case of selection relevant accounting policies. Through the using of

accounting judgements, an organization can give necessary changes in case of its accounting

policies. With the expertise knowledge and judgements, such as like through the proper

managerial decisions by relevant persons an organization can able to make necessary changes

and implementing new accounting policies that influenced towards the favourable benefits of

the company (Davern et al. 2019).

Answer to question 2:

Accounting Policies of Caltex Limited:

In accordance with the Annual report issued by Caltex Limited 2018, while preparing

the consolidated financial statements, the management makes some relevant judgments,

estimations including some assumptions that affect in case of application of policies and also

reported to the amounts of assets, liabilities, incomes and expenses. Such estimates and

5ACCOUNTING FINANCIAL ANALYISIS REPORT

assumptions are generally based on the historical cost experiences and various other factors

that probably influenced the overall organizational operations.

Along with such policies valuation details, the annual report is also providing some

relevant changes regarding the accounting policies. Such changes are in Revenue generated

from the customers. In contrast, per the provisions of AASB 15, the company need to review

all the revenues and incomes, including sales relating to the contracts across different

significant customers. In case of such company followed the provisions issued under AASB

15 franchisees fees would be distinct in the balance sheet and recognized in the income

statements generally over the term of agreements with relating to franchisees. Another

accounting policy that influenced the accounting treatment of the company is followed the

provision AASB 9 recognizing and measuring the financial assets, liabilities, including some

character of buying or sell non-financial items. Here the company is performed with a review

of its current classification and measurement of financial assets and liabilities for compliance

with the requirements of the new standard. Another significant essential policies that

influenced the accounting treatment is the fair value system (Rahman 2013).

Estimates relating to PPE:

The Caltex limited generally had freehold land, buildings, leasehold property, plant

and equipment, capital projects in progress etc. generally in case of owned assets the

company measured the value of such assets through cost less accumulated depreciation and

impairment losses. Cost representing the general expenses that directly attributable to the

acquisitions of assets. Major cyclical maintenance expenditure is basically separate

capitalised as an asset component to the extent that it is probable that future economic

benefits, in excess of the originally assessed standard of performance (Weil, Schipper and

Francis 2013). The company in general followed the straight line method system in case to

assumptions are generally based on the historical cost experiences and various other factors

that probably influenced the overall organizational operations.

Along with such policies valuation details, the annual report is also providing some

relevant changes regarding the accounting policies. Such changes are in Revenue generated

from the customers. In contrast, per the provisions of AASB 15, the company need to review

all the revenues and incomes, including sales relating to the contracts across different

significant customers. In case of such company followed the provisions issued under AASB

15 franchisees fees would be distinct in the balance sheet and recognized in the income

statements generally over the term of agreements with relating to franchisees. Another

accounting policy that influenced the accounting treatment of the company is followed the

provision AASB 9 recognizing and measuring the financial assets, liabilities, including some

character of buying or sell non-financial items. Here the company is performed with a review

of its current classification and measurement of financial assets and liabilities for compliance

with the requirements of the new standard. Another significant essential policies that

influenced the accounting treatment is the fair value system (Rahman 2013).

Estimates relating to PPE:

The Caltex limited generally had freehold land, buildings, leasehold property, plant

and equipment, capital projects in progress etc. generally in case of owned assets the

company measured the value of such assets through cost less accumulated depreciation and

impairment losses. Cost representing the general expenses that directly attributable to the

acquisitions of assets. Major cyclical maintenance expenditure is basically separate

capitalised as an asset component to the extent that it is probable that future economic

benefits, in excess of the originally assessed standard of performance (Weil, Schipper and

Francis 2013). The company in general followed the straight line method system in case to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING FINANCIAL ANALYISIS REPORT

compute depreciation amount. The normal Depreciation rate followed by the company for

assets are as follows;

For Freehold buildings 2%, Leasehold property 2% to 10%, Plant and equipment 3% to 25%

and for Leased plant and equipment 3% to 25%.

Answer to question 3:

Critical evaluation of whether the accounting estimates and policies:

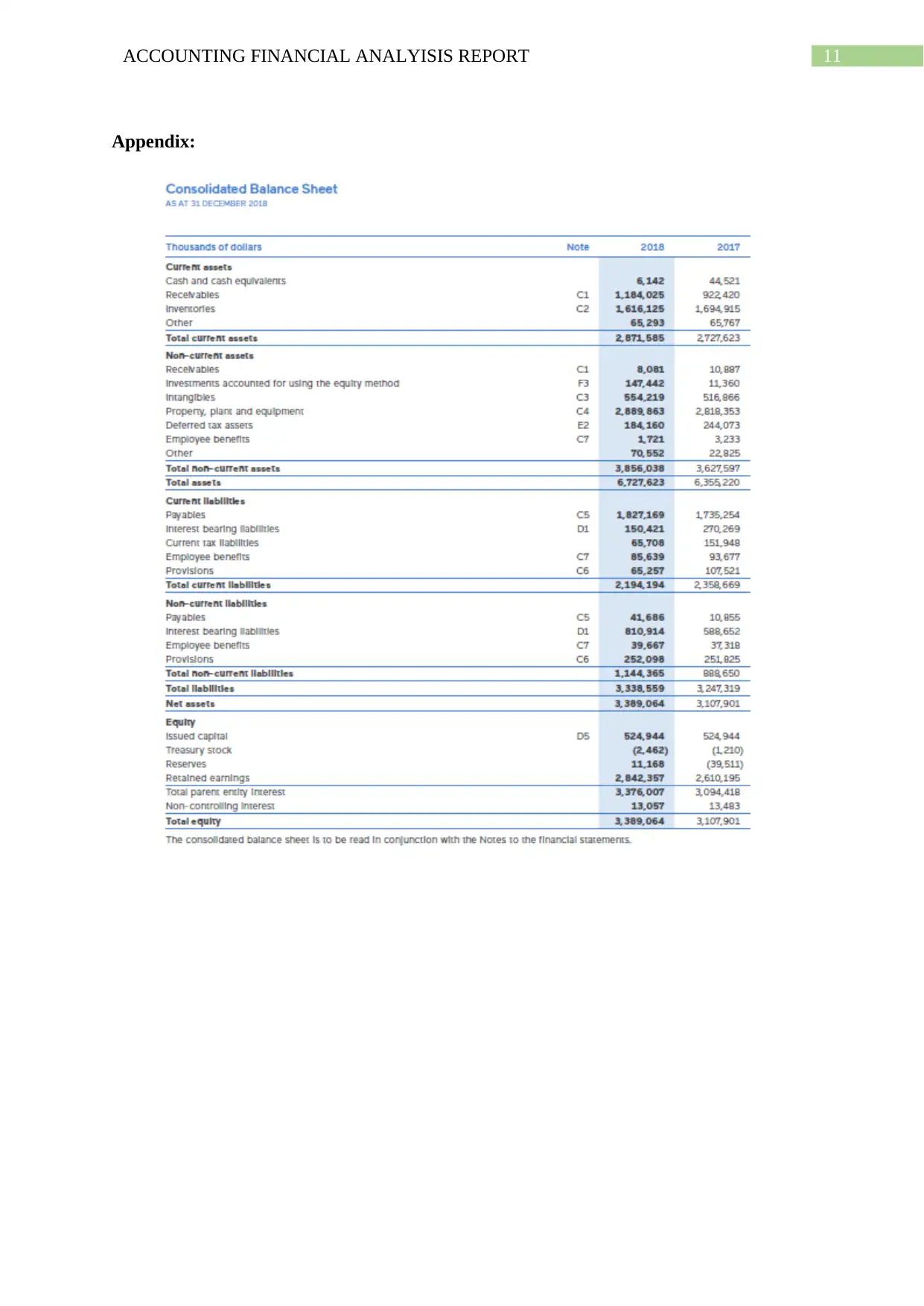

The PPE is usually mean the plants, property and the equipment of a business. This is

located in the balance sheet of a firm. This is grouped together at an original cost less the net

accumulated depreciation of the PPE of the firm. This are basically the tangible assets of the

firm which have a life span of more than one year. These kinds of goods are basically used in

the manufacturing or supply of the particular goods and the services. The accounting policies

are basically the particular principles, bases, protocol, rules and practices applied by the firm

while preparing and introducing the monetary statements in the annual report. The relevant

changes in the accounting estimate is an relevant adjustment of the carrying amount of the

resources and the relevant expenses incurred by the firm resulting from the re-examining the

expected future benefits and the obligations that are related with resources of the firm

(Caltex, 2018). The disclosures related to the changes in the accounting policy are including

the interpretation or the title of the standard cause the change, relevant changes in the

accounting policies, and descriptions of the transitional provision of the firm. The plant

property and the equipment of the firm identified in the consolidated financial report that is

2,889,863. The amount of property plant and equipment of the previous year of the firm is

2818353. The PPE includes the freehold land, buildings, leasehold property, plant and

equipment and the capital projects that were in progress by the firm. The PPE amount of the

year 2018 was measured at a cost less accumulated depreciation and impairment losses. The

compute depreciation amount. The normal Depreciation rate followed by the company for

assets are as follows;

For Freehold buildings 2%, Leasehold property 2% to 10%, Plant and equipment 3% to 25%

and for Leased plant and equipment 3% to 25%.

Answer to question 3:

Critical evaluation of whether the accounting estimates and policies:

The PPE is usually mean the plants, property and the equipment of a business. This is

located in the balance sheet of a firm. This is grouped together at an original cost less the net

accumulated depreciation of the PPE of the firm. This are basically the tangible assets of the

firm which have a life span of more than one year. These kinds of goods are basically used in

the manufacturing or supply of the particular goods and the services. The accounting policies

are basically the particular principles, bases, protocol, rules and practices applied by the firm

while preparing and introducing the monetary statements in the annual report. The relevant

changes in the accounting estimate is an relevant adjustment of the carrying amount of the

resources and the relevant expenses incurred by the firm resulting from the re-examining the

expected future benefits and the obligations that are related with resources of the firm

(Caltex, 2018). The disclosures related to the changes in the accounting policy are including

the interpretation or the title of the standard cause the change, relevant changes in the

accounting policies, and descriptions of the transitional provision of the firm. The plant

property and the equipment of the firm identified in the consolidated financial report that is

2,889,863. The amount of property plant and equipment of the previous year of the firm is

2818353. The PPE includes the freehold land, buildings, leasehold property, plant and

equipment and the capital projects that were in progress by the firm. The PPE amount of the

year 2018 was measured at a cost less accumulated depreciation and impairment losses. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING FINANCIAL ANALYISIS REPORT

carrying amount of PPE for the year 2018 is 1,561,662 and the amount in the previous year

was 1,473,458. This means that the financial position of the firm increases from before. The

preparation of the consolidated financial report of the firm is done in accordance with AASBs

(Australian Accounting Standards Board 2015). The estimation and the underlying

assumptions amount of the firm are reviewed on an ongoing basis. The judgments and the

estimates made by the management in the application of the AASB have a significant impact

in the consolidated balance sheet of the firm and the estimates with a significant risk of

material adjustment in the financial years of the firm (Weil, Schipper and Francis, 2013).

Answer to question 4:

Recommendation:

The firm can provide the audit guidance of the PPE of the firm. The revised

accounting standards should be considered by the firm while preparing the financial

statements of the firm (Rahman, 2013). The firm have shown the disclosures properly

however, the firm can disclose the restriction on the title and items pledged as security for

liabilities, the contractual commitments for the acquisition of the plant, property and

equipment of the firm (Buculescu and Velicescu, 2014). The relevant compensation from the

third parties for the items of the PPE that were impaired and included in the profit and loss

statement of the firm. These are the relevant improvement in the accounting estimates and the

policies in PPE that can be followed by the firm.

Conclusion

It can be concluded from the above discussions that, this completed report is

providing a brief idea about the AASB 16 plant, property and equipment. The application of

AASB on Caltex limited and the probable impacts on overall financial statements. In the first

part of this report is providing the basic idea about accounting policies and the effects of

carrying amount of PPE for the year 2018 is 1,561,662 and the amount in the previous year

was 1,473,458. This means that the financial position of the firm increases from before. The

preparation of the consolidated financial report of the firm is done in accordance with AASBs

(Australian Accounting Standards Board 2015). The estimation and the underlying

assumptions amount of the firm are reviewed on an ongoing basis. The judgments and the

estimates made by the management in the application of the AASB have a significant impact

in the consolidated balance sheet of the firm and the estimates with a significant risk of

material adjustment in the financial years of the firm (Weil, Schipper and Francis, 2013).

Answer to question 4:

Recommendation:

The firm can provide the audit guidance of the PPE of the firm. The revised

accounting standards should be considered by the firm while preparing the financial

statements of the firm (Rahman, 2013). The firm have shown the disclosures properly

however, the firm can disclose the restriction on the title and items pledged as security for

liabilities, the contractual commitments for the acquisition of the plant, property and

equipment of the firm (Buculescu and Velicescu, 2014). The relevant compensation from the

third parties for the items of the PPE that were impaired and included in the profit and loss

statement of the firm. These are the relevant improvement in the accounting estimates and the

policies in PPE that can be followed by the firm.

Conclusion

It can be concluded from the above discussions that, this completed report is

providing a brief idea about the AASB 16 plant, property and equipment. The application of

AASB on Caltex limited and the probable impacts on overall financial statements. In the first

part of this report is providing the basic idea about accounting policies and the effects of

8ACCOUNTING FINANCIAL ANALYISIS REPORT

specific changes in polices. Next to this report is presenting the annual report of the firm for

the year 2018. The accounting estimates and the policies applied by the firm in the plant,

property and the equipment have been analysed. The accounting policies implemented by the

firm are all appropriate according to the Australian accounting standard. The actions for

better improvement of the accounting estimates and policies in PPE of the firm have also

been recommended in the report.

specific changes in polices. Next to this report is presenting the annual report of the firm for

the year 2018. The accounting estimates and the policies applied by the firm in the plant,

property and the equipment have been analysed. The accounting policies implemented by the

firm are all appropriate according to the Australian accounting standard. The actions for

better improvement of the accounting estimates and policies in PPE of the firm have also

been recommended in the report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING FINANCIAL ANALYISIS REPORT

References:

Australian Accounting Standards Board 2015. Property, Plant and Equipment. [ebook]

Australia: Australian Accounting Standards Board, p.22. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPoct15_01-18.pdf

[Accessed 30 Sep. 2019].

Buculescu, M.M. and Velicescu, B.N., 2014. An analysis of the convergence level of tangible

assets (PPE) according to Romanian national accounting regulation and IFRS for

SMEs. Accounting and Management Information Systems, 13(4), pp.774-799.

Caltex 2018. 2018 Annual Report | Caltex Australia. [online] Caltex. Available at:

https://www.caltex.com.au/annual-report-2018 [Accessed 30 Sep. 2019].

Davern, M., Gyles, N., Potter, B. and Yang, V., 2019. Implementing AASB 15 revenue from

contracts with customers: the preparer perspective. Accounting Research Journal, (just-

accepted), pp.00-00.

Juárez, F.E.R.N.A.N.D.O., 2016. The Dual Aspect of Accounting Transaction and the Assets

Claims on Assets Equivalence. International Journal of Economics and Management

Systems, 1, pp.39-43.

Laing, G. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB 116

non-current asset measurement models. International Journal of Critical Accounting, 6(5/6),

pp.509-519.

Rahman, A.R., 2013. The Australian Accounting Standards Review Board (RLE

Accounting): The Establishment of its Participative Review Process. Routledge.

Standard, I.A., 2015. Presentation of Financial Statements. Balance Sheet, 54, p.80A.

References:

Australian Accounting Standards Board 2015. Property, Plant and Equipment. [ebook]

Australia: Australian Accounting Standards Board, p.22. Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPoct15_01-18.pdf

[Accessed 30 Sep. 2019].

Buculescu, M.M. and Velicescu, B.N., 2014. An analysis of the convergence level of tangible

assets (PPE) according to Romanian national accounting regulation and IFRS for

SMEs. Accounting and Management Information Systems, 13(4), pp.774-799.

Caltex 2018. 2018 Annual Report | Caltex Australia. [online] Caltex. Available at:

https://www.caltex.com.au/annual-report-2018 [Accessed 30 Sep. 2019].

Davern, M., Gyles, N., Potter, B. and Yang, V., 2019. Implementing AASB 15 revenue from

contracts with customers: the preparer perspective. Accounting Research Journal, (just-

accepted), pp.00-00.

Juárez, F.E.R.N.A.N.D.O., 2016. The Dual Aspect of Accounting Transaction and the Assets

Claims on Assets Equivalence. International Journal of Economics and Management

Systems, 1, pp.39-43.

Laing, G. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB 116

non-current asset measurement models. International Journal of Critical Accounting, 6(5/6),

pp.509-519.

Rahman, A.R., 2013. The Australian Accounting Standards Review Board (RLE

Accounting): The Establishment of its Participative Review Process. Routledge.

Standard, I.A., 2015. Presentation of Financial Statements. Balance Sheet, 54, p.80A.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING FINANCIAL ANALYISIS REPORT

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

11ACCOUNTING FINANCIAL ANALYISIS REPORT

Appendix:

Appendix:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.