Financial Management: PPHE and Andrew Brown-sword Hotels Report

VerifiedAdded on 2020/12/24

|14

|3937

|175

Report

AI Summary

This report presents a financial analysis of two hotel companies, PPHE and Andrew Brown-sword Hotels Limited. It begins with an executive summary and an introduction that provides an overview of both companies, including their establishment, operations, and services. The report delves into a comparative analysis of their financial statements, including key ratios like current ratio, quick ratio, and debt-equity ratio, comparing PPHE with Intercontinental Hotels Group PLC. A significant portion of the report focuses on the cost of capital, specifically the Weighted Average Cost of Capital (WACC), and its application in determining the value and share price of Andrew Brown-sword Hotels Limited, particularly in the context of a potential acquisition by PPHE. The report also calculates the purchase consideration payable by PPHE and assesses the likely impact of the acquisition on PPHE's financial statements. The financial leverage and debt-equity structure of PPHE are also examined, including the proportions of equity and debts in PPHE's capital structure. The report concludes with an assessment of the usefulness, relevance, and weaknesses of using cost of capital figures in financial decision-making.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report summarizes financial report of two companies PPHE, the Dutch based hotel

group, and Andrew Brown-sword Hotels Limited. As financing is one of the most important part

for any business to survive it help mangers to expand their operations and in order to do so

financial management plays an important role as it shows the current position of company. This

report also show detailed analysis of financial statements of both companies. This report

summarized the cost of capital to determine the value and price per share of Andrew Brown-

sword Hotels Limited.

This report summarizes financial report of two companies PPHE, the Dutch based hotel

group, and Andrew Brown-sword Hotels Limited. As financing is one of the most important part

for any business to survive it help mangers to expand their operations and in order to do so

financial management plays an important role as it shows the current position of company. This

report also show detailed analysis of financial statements of both companies. This report

summarized the cost of capital to determine the value and price per share of Andrew Brown-

sword Hotels Limited.

Table of Contents

Executive Summary.........................................................................................................................2

INTRODUCTION...........................................................................................................................1

Overview................................................................................................................................1

Andrew Brown-sword Hotels Limited...................................................................................1

1) Comparative Analysis of Financial Statements.................................................................2

Comparison between PPHE and Intercontinental Hotels Group PLC...................................2

2) Cost of Capital....................................................................................................................3

3. Calculation of purchase consideration payable by PPHE to acquire ABH:.......................5

4. Calculate the likely impact on the financial statements of PPHE following the purchase of

ABH........................................................................................................................................6

5. Share price movements of PPHE.......................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

Executive Summary.........................................................................................................................2

INTRODUCTION...........................................................................................................................1

Overview................................................................................................................................1

Andrew Brown-sword Hotels Limited...................................................................................1

1) Comparative Analysis of Financial Statements.................................................................2

Comparison between PPHE and Intercontinental Hotels Group PLC...................................2

2) Cost of Capital....................................................................................................................3

3. Calculation of purchase consideration payable by PPHE to acquire ABH:.......................5

4. Calculate the likely impact on the financial statements of PPHE following the purchase of

ABH........................................................................................................................................6

5. Share price movements of PPHE.......................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial management is a kind of process which is related to controlling, managing and

directing the all financial activities in a way which is suitable for the organisations (Renz, 2016).

This helps the companies in allocating the fund into different activities. Eventually, it plays a

crucial role in improving the financial position and for this purpose it includes various

calculations like ratio analysis, portfolio of different financial products etc. To understand in

broad sense about the financial report two companies: PPHE and Andrew Brown-sword hotels

limited company are selected. PPHE is an international hospitality estate group. It was founded

in 1989 and its headquarter is in Netherlands. On the other Andrew Brown-sword hotels limited

is Canterbury, Chester and Manchester. This company is involved in providing hospitality

services. It was established in 2003.

Overview

PPHE hotel group

PPHE hotel group is a Dutch based hospitality real estate group which works

internationally with a portfolio of 1.6 billion with a long leasehold assets and freehold in

Europe's resort destinations, urban markets and in leading cities. They also have an exclusive

licence from one of the world's largest hotel group, Radisson Hotel Group, under which they

expanded their business in Middle East and Africa and developed Park Plaza Hotel & Resorts.

They also have controlling ownership interest in one of Croatia,s premier hospitality companies,

Arena Hospitality Group that gives them a strong hold in Istrian Peninsula. It offers various

hospitality services in five different countries, its property portfolio includes 46 properties

offering approx 8800 rooms, 6000 mobile homes and campsite pitches in eight different

campsites.

Andrew Brown-sword Hotels Limited

Andrew Brown-sword Hotels Limited was incorporated in year 2003 on 8th of September.

It is one of the leading hotel industries in UK the headquartered office is located in Bath,

Somerset. They have various offerings in the hotel industries to provide best in class comfort and

care in their hospitality, it offers various properties some of the offering offered by them is the

Gidleigh Park which provide the sublime food and wine with their exceptional service in

Chagford, Devon, The Bath Priory which is located in a heart of bustling city in Bath, Somerset,

1

Financial management is a kind of process which is related to controlling, managing and

directing the all financial activities in a way which is suitable for the organisations (Renz, 2016).

This helps the companies in allocating the fund into different activities. Eventually, it plays a

crucial role in improving the financial position and for this purpose it includes various

calculations like ratio analysis, portfolio of different financial products etc. To understand in

broad sense about the financial report two companies: PPHE and Andrew Brown-sword hotels

limited company are selected. PPHE is an international hospitality estate group. It was founded

in 1989 and its headquarter is in Netherlands. On the other Andrew Brown-sword hotels limited

is Canterbury, Chester and Manchester. This company is involved in providing hospitality

services. It was established in 2003.

Overview

PPHE hotel group

PPHE hotel group is a Dutch based hospitality real estate group which works

internationally with a portfolio of 1.6 billion with a long leasehold assets and freehold in

Europe's resort destinations, urban markets and in leading cities. They also have an exclusive

licence from one of the world's largest hotel group, Radisson Hotel Group, under which they

expanded their business in Middle East and Africa and developed Park Plaza Hotel & Resorts.

They also have controlling ownership interest in one of Croatia,s premier hospitality companies,

Arena Hospitality Group that gives them a strong hold in Istrian Peninsula. It offers various

hospitality services in five different countries, its property portfolio includes 46 properties

offering approx 8800 rooms, 6000 mobile homes and campsite pitches in eight different

campsites.

Andrew Brown-sword Hotels Limited

Andrew Brown-sword Hotels Limited was incorporated in year 2003 on 8th of September.

It is one of the leading hotel industries in UK the headquartered office is located in Bath,

Somerset. They have various offerings in the hotel industries to provide best in class comfort and

care in their hospitality, it offers various properties some of the offering offered by them is the

Gidleigh Park which provide the sublime food and wine with their exceptional service in

Chagford, Devon, The Bath Priory which is located in a heart of bustling city in Bath, Somerset,

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Amberley Castle a retreat of the medieval age in an idyllic corner of countryside located in Nr.

Arundel, West Sussex, they provide many similar hotel across the different part of the country

with their exceptional service and food.

1) Comparative Analysis of Financial Statements

Financial statements: Financial statements are the statements which show actual

financial position of the company (Michalski, 2012). It help mangers to see and compare their

financial position with their competitors and also to check their growth. It gives a clear image of

company's ability to grow and expand. Managers uses this information to create new strategies

and achieve the competitive advantage over their competitors.

Comparison between PPHE and Intercontinental Hotels Group PLC

Intercontinental Hotels Group PLC is one of the close competitor of PPHE group of

hotels financial statements of both the hotel groups shows that revenue generated by the

Intercontinental Hotel group in year 2017 was 1784 million whereas the revenue generated by

the PPHE group of hotels in year 2017 was recorded at 325 million, in compared of revenue

generation the Intercontinental group is doing very well in the market. To compare both the

groups the key ratios are taken in to consideration such as the liquidity ratio. The current ratio of

the intercontinental group is 0.64 which shows the ability to pay off its current liabilities with

their current ratio it shows that the company,s ability to pay off its current liabilities is not that

good, whereas the current ratio of PPHE is marked at 3.44 which states that company's ability to

pay off his current liabilities is remarkably good and the company can easily pay off its liabilities

at any point of time. The quick ratio shows ability of the company to convert is current assets

into cash within one year, quick ratio of PPHE is at 3.02 which means the company can easily

convert its assets into cash whereas in the case of Intercontinental quick ratio is marked as 0.51

which states that the company is in a difficult position to convert its current assets to cash to set

off its liabilities.

In IHG there is no financial leverage and debt equity ratio is not applicable which shows

the company does not any debts to find out debt equity ratio whereas in the case of PPHE the

financial leverage ratio is recorded at 4.49 it shows that how much financial leverage is available

with it and debt equity ratio of PPHE group is recorded at 0.56 it show the capability of the

shareholder fund to set of available different debts owed by this group. To find which company

is more efficient, efficiency ratio is considered. The receivables turnover ratio of PPHE is

2

Arundel, West Sussex, they provide many similar hotel across the different part of the country

with their exceptional service and food.

1) Comparative Analysis of Financial Statements

Financial statements: Financial statements are the statements which show actual

financial position of the company (Michalski, 2012). It help mangers to see and compare their

financial position with their competitors and also to check their growth. It gives a clear image of

company's ability to grow and expand. Managers uses this information to create new strategies

and achieve the competitive advantage over their competitors.

Comparison between PPHE and Intercontinental Hotels Group PLC

Intercontinental Hotels Group PLC is one of the close competitor of PPHE group of

hotels financial statements of both the hotel groups shows that revenue generated by the

Intercontinental Hotel group in year 2017 was 1784 million whereas the revenue generated by

the PPHE group of hotels in year 2017 was recorded at 325 million, in compared of revenue

generation the Intercontinental group is doing very well in the market. To compare both the

groups the key ratios are taken in to consideration such as the liquidity ratio. The current ratio of

the intercontinental group is 0.64 which shows the ability to pay off its current liabilities with

their current ratio it shows that the company,s ability to pay off its current liabilities is not that

good, whereas the current ratio of PPHE is marked at 3.44 which states that company's ability to

pay off his current liabilities is remarkably good and the company can easily pay off its liabilities

at any point of time. The quick ratio shows ability of the company to convert is current assets

into cash within one year, quick ratio of PPHE is at 3.02 which means the company can easily

convert its assets into cash whereas in the case of Intercontinental quick ratio is marked as 0.51

which states that the company is in a difficult position to convert its current assets to cash to set

off its liabilities.

In IHG there is no financial leverage and debt equity ratio is not applicable which shows

the company does not any debts to find out debt equity ratio whereas in the case of PPHE the

financial leverage ratio is recorded at 4.49 it shows that how much financial leverage is available

with it and debt equity ratio of PPHE group is recorded at 0.56 it show the capability of the

shareholder fund to set of available different debts owed by this group. To find which company

is more efficient, efficiency ratio is considered. The receivables turnover ratio of PPHE is

2

rerecorded at 25.04 which show that company is considering credit sales and receivables are

paying their amount due to company on time which shows efficiency of this group, whereas IHG

marked its receivables turnover ratio at 4.35 showing its efficiency. Inventory turnover is

recorded at 202.67 whereas of PPHE group is at 53.81.

2) Cost of Capital

Cost of Capital: Cost of capital is a metric which is used by internal management to see

that a capital which a company is investing in is worth it or not (Zietlow and et. al, 2018). In this

company uses a weighted average of company's cost of equity and it cost of capital. Cost of

Capital refers to the required rate of return that a company must have in order to implement a

capital budgeting project successfully. In context of the given scenario, PPHE wants to acquire

Andrew Brownsword Hotel. For this purpose the company wants to ascertain the cost of capital

in order to discount future cash flows so as to ascertain the fair value for such move. For this

purpose the company can use a discounting rate equivalent to the weighted average cost of

capital. The discounting rate must fulfil two criteria viz. It should reflect the effect of time value

of money as well as risk attached to the investment project. The Weighted Average cost of

capital ascertained in order to discount the cash flows ,as per the calculations provided in

Appendices [1] Section, comes to 3% equivalent to the average cost of debt.

Following is the proportions of equity and debts in PPHE's capital structure:

The company has raised its capital from various sources, debts are owed from various sources

and raised its capital from equity. The description of the company's capital is as followed.

Company owes a debts of 627.8 million in the form of debentures which are redeemable

after 5 years and debts which are for less than 5 years are stated at 69.5 million, company also

owes a debts in cash of 217.7 million apart from these other debts company also owes a debts of

479.6 million to bank. Along with these above mentioned debts company has also raised it

capital from various other sources through issuing the equity share capital. The break up of the

share capital of the company is as followed.

Total capital raised through the issue of equity is stated at 1190.5 million which is further

classified into different groups such as market value restatement, equity attributable to

shareholders, reported, market value restatement of equity attributable to non controlling interest,

and non controlling interest (Andreou, Louca and Panayides, 2014). Company raised its capital

through share premium accounts is reported at 130.061 million, company also paid 3.636 million

3

paying their amount due to company on time which shows efficiency of this group, whereas IHG

marked its receivables turnover ratio at 4.35 showing its efficiency. Inventory turnover is

recorded at 202.67 whereas of PPHE group is at 53.81.

2) Cost of Capital

Cost of Capital: Cost of capital is a metric which is used by internal management to see

that a capital which a company is investing in is worth it or not (Zietlow and et. al, 2018). In this

company uses a weighted average of company's cost of equity and it cost of capital. Cost of

Capital refers to the required rate of return that a company must have in order to implement a

capital budgeting project successfully. In context of the given scenario, PPHE wants to acquire

Andrew Brownsword Hotel. For this purpose the company wants to ascertain the cost of capital

in order to discount future cash flows so as to ascertain the fair value for such move. For this

purpose the company can use a discounting rate equivalent to the weighted average cost of

capital. The discounting rate must fulfil two criteria viz. It should reflect the effect of time value

of money as well as risk attached to the investment project. The Weighted Average cost of

capital ascertained in order to discount the cash flows ,as per the calculations provided in

Appendices [1] Section, comes to 3% equivalent to the average cost of debt.

Following is the proportions of equity and debts in PPHE's capital structure:

The company has raised its capital from various sources, debts are owed from various sources

and raised its capital from equity. The description of the company's capital is as followed.

Company owes a debts of 627.8 million in the form of debentures which are redeemable

after 5 years and debts which are for less than 5 years are stated at 69.5 million, company also

owes a debts in cash of 217.7 million apart from these other debts company also owes a debts of

479.6 million to bank. Along with these above mentioned debts company has also raised it

capital from various other sources through issuing the equity share capital. The break up of the

share capital of the company is as followed.

Total capital raised through the issue of equity is stated at 1190.5 million which is further

classified into different groups such as market value restatement, equity attributable to

shareholders, reported, market value restatement of equity attributable to non controlling interest,

and non controlling interest (Andreou, Louca and Panayides, 2014). Company raised its capital

through share premium accounts is reported at 130.061 million, company also paid 3.636 million

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

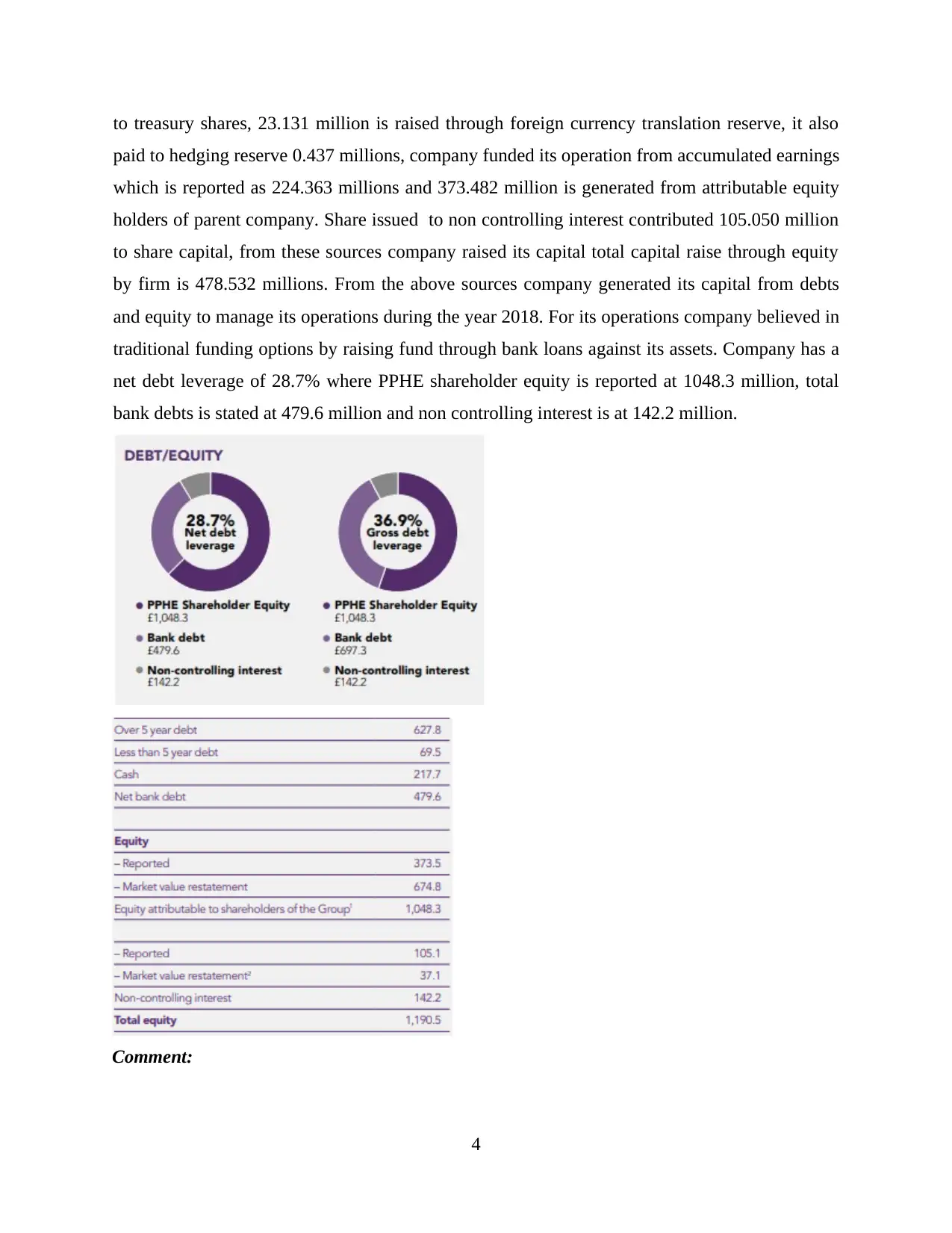

to treasury shares, 23.131 million is raised through foreign currency translation reserve, it also

paid to hedging reserve 0.437 millions, company funded its operation from accumulated earnings

which is reported as 224.363 millions and 373.482 million is generated from attributable equity

holders of parent company. Share issued to non controlling interest contributed 105.050 million

to share capital, from these sources company raised its capital total capital raise through equity

by firm is 478.532 millions. From the above sources company generated its capital from debts

and equity to manage its operations during the year 2018. For its operations company believed in

traditional funding options by raising fund through bank loans against its assets. Company has a

net debt leverage of 28.7% where PPHE shareholder equity is reported at 1048.3 million, total

bank debts is stated at 479.6 million and non controlling interest is at 142.2 million.

Comment:

4

paid to hedging reserve 0.437 millions, company funded its operation from accumulated earnings

which is reported as 224.363 millions and 373.482 million is generated from attributable equity

holders of parent company. Share issued to non controlling interest contributed 105.050 million

to share capital, from these sources company raised its capital total capital raise through equity

by firm is 478.532 millions. From the above sources company generated its capital from debts

and equity to manage its operations during the year 2018. For its operations company believed in

traditional funding options by raising fund through bank loans against its assets. Company has a

net debt leverage of 28.7% where PPHE shareholder equity is reported at 1048.3 million, total

bank debts is stated at 479.6 million and non controlling interest is at 142.2 million.

Comment:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Even though PPHE uses a discount rate falling between 11% to 15%, it is important to

ascertain the discount rate using a capital budgeting method such as WACC which involves the

proportionate allocation of market risk by applying appropriate weights to the components

forming capital structure (Fabozzi and Drake, 2010). Thus, giving the valuator an accurate

measure to ascertain the feasibility and acceptability of a proposed project or investment. Hence,

for the proposed acquisition of ABH, the company should use 3% as its discounting rate.

Debt-Equity Structure of PPHE: Looking at the Debt-Equity of the structure, PPHE is

essentially a debt-financed company with its 69% of sources of finance being financial lending

institutions such as Bank whereas only 31% of its working capital requirements are fulfilled by

Equity Finance Sources.

Comment:

As per the Note 15 of Notes to Consolidated Financial Statements provided in Annual

Report of 2018, the company has been having a borrowing majorly falling under fixed interest

rate purview of the non-current liabilities. These especially include debt taken from Banks. A

heavily debt-financed organization such as PPHE will be able to undertake more of expansion

related activities without worrying about dilution of ownership of its shareholders. Hence, in the

case of proposing ABH's acquisition, the company can retain its ownership as well as control

over the operational activities of the hotel it aims to acquire without having to worry about its

investors. Also, the hotel would be able to have greater freedom and flexibility.

Comment on Usefulness, Relevance and Weakness of Using Cost of Capital Figures:

Cost of Capital or WACC, undertaken in the context of given scenario, acts as a hurdle or

discounting rate while evaluating the feasibility of a given investment or project (Lee and et .al,

2014). However it is only relevant for PPHE until and unless the capital structure of the hotel

does not change. This also proves to be a weakness for these capital budgeting techniques as it is

nearly impossible to maintain the same capital structure for PPHE or be it any other organization

as the organizational needs are dynamic in nature and keep on changing with time.

Also, the cost of capital can only reflect the true image if its able to capture time value of

money as well as the risks associated with the given project. It is worthy to note that, cost of

capital figure would be rendered useless if the business discovers a new risk associated with the

project which it had not been able to foresee during the initial stage of proposed project.

3. Calculation of purchase consideration payable by PPHE to acquire ABH:

Purchase consideration is net amount payable by acquirer company to acquiring

company (Chen and Chang, 2012). Most popular and wildly accepted method is net asset

method. Although amount of purchase consideration can be decided by mutual consent and

agreement between them. Following are the major methods to calculate purchase consideration

amount, as follows:

5

ascertain the discount rate using a capital budgeting method such as WACC which involves the

proportionate allocation of market risk by applying appropriate weights to the components

forming capital structure (Fabozzi and Drake, 2010). Thus, giving the valuator an accurate

measure to ascertain the feasibility and acceptability of a proposed project or investment. Hence,

for the proposed acquisition of ABH, the company should use 3% as its discounting rate.

Debt-Equity Structure of PPHE: Looking at the Debt-Equity of the structure, PPHE is

essentially a debt-financed company with its 69% of sources of finance being financial lending

institutions such as Bank whereas only 31% of its working capital requirements are fulfilled by

Equity Finance Sources.

Comment:

As per the Note 15 of Notes to Consolidated Financial Statements provided in Annual

Report of 2018, the company has been having a borrowing majorly falling under fixed interest

rate purview of the non-current liabilities. These especially include debt taken from Banks. A

heavily debt-financed organization such as PPHE will be able to undertake more of expansion

related activities without worrying about dilution of ownership of its shareholders. Hence, in the

case of proposing ABH's acquisition, the company can retain its ownership as well as control

over the operational activities of the hotel it aims to acquire without having to worry about its

investors. Also, the hotel would be able to have greater freedom and flexibility.

Comment on Usefulness, Relevance and Weakness of Using Cost of Capital Figures:

Cost of Capital or WACC, undertaken in the context of given scenario, acts as a hurdle or

discounting rate while evaluating the feasibility of a given investment or project (Lee and et .al,

2014). However it is only relevant for PPHE until and unless the capital structure of the hotel

does not change. This also proves to be a weakness for these capital budgeting techniques as it is

nearly impossible to maintain the same capital structure for PPHE or be it any other organization

as the organizational needs are dynamic in nature and keep on changing with time.

Also, the cost of capital can only reflect the true image if its able to capture time value of

money as well as the risks associated with the given project. It is worthy to note that, cost of

capital figure would be rendered useless if the business discovers a new risk associated with the

project which it had not been able to foresee during the initial stage of proposed project.

3. Calculation of purchase consideration payable by PPHE to acquire ABH:

Purchase consideration is net amount payable by acquirer company to acquiring

company (Chen and Chang, 2012). Most popular and wildly accepted method is net asset

method. Although amount of purchase consideration can be decided by mutual consent and

agreement between them. Following are the major methods to calculate purchase consideration

amount, as follows:

5

Net asset method: as per this method amount of Purchase consideration = total net asset of

transferor company.

PC= Aggregate amount of asset – aggregate amount of liabilities

Net payment method: according to this method amount paid to shareholders of transferor

company would be in form of cash, shares or debentures (Akgün and et. al, 2014).

Lump sum method: In this method a Fixed amount is determined and paid by transferee

company to the transferor company. Such method not require any calculation because amount is

determined by mutual consent.

Intrinsic value/ Share exchange method: Under this method amount of Purchase

consideration is calculated by dividing the net asset value of transferor company by price of one

share of transferee company (Jain, Singh and Yadav, 2013).

4. Calculate the likely impact on the financial statements of PPHE following the purchase of

ABH

Here in given case scenario calculation is done as per net asset method. As per this method

net assets of acquired company is considered as purchase consideration to be payable, thus in

order to calculate purchase consideration first net asset is calculated by deducting current

liabilities and provision from total amount of assets. To obtain price per share is to be payable

amount of net purchase consideration is divided by total number of shares of acquiring company.

ABH Limited reported total fixed asset is of 69195285 and current liabilities and provision is of

2951547 and 1625511 respectively, so net purchase consideration payable would be 64618227

and equivalent price per share is 1.005.

5. Share price movements of PPHE

Market share price fluctuation is one of the challenging phase for an organization to

address the requirement of business in ethical manner. The process affect the share price

fluctuation and market position in the stock market (). Transformative investment price and set is

mainly based upon the consolidation and management process that helps in constructing the data

in various form. Transformative venture is set progressively to profit PPHE. Fast approaching

extension in London (c 900 rooms) and broad redesigns ought to bring a stage change in

development opportunity While combination of its Croatian retreat organizations is now

satisfying (twofold digit ascend in room rate in Q3. In the interim, PPHE's Q3 exchanging update

communicated certainty it should keep on overcoming headwinds to live up to its 2016 outcomes

desires. Solid funds are obvious in August's exceptional profit of 100p/share and effective

6

transferor company.

PC= Aggregate amount of asset – aggregate amount of liabilities

Net payment method: according to this method amount paid to shareholders of transferor

company would be in form of cash, shares or debentures (Akgün and et. al, 2014).

Lump sum method: In this method a Fixed amount is determined and paid by transferee

company to the transferor company. Such method not require any calculation because amount is

determined by mutual consent.

Intrinsic value/ Share exchange method: Under this method amount of Purchase

consideration is calculated by dividing the net asset value of transferor company by price of one

share of transferee company (Jain, Singh and Yadav, 2013).

4. Calculate the likely impact on the financial statements of PPHE following the purchase of

ABH

Here in given case scenario calculation is done as per net asset method. As per this method

net assets of acquired company is considered as purchase consideration to be payable, thus in

order to calculate purchase consideration first net asset is calculated by deducting current

liabilities and provision from total amount of assets. To obtain price per share is to be payable

amount of net purchase consideration is divided by total number of shares of acquiring company.

ABH Limited reported total fixed asset is of 69195285 and current liabilities and provision is of

2951547 and 1625511 respectively, so net purchase consideration payable would be 64618227

and equivalent price per share is 1.005.

5. Share price movements of PPHE

Market share price fluctuation is one of the challenging phase for an organization to

address the requirement of business in ethical manner. The process affect the share price

fluctuation and market position in the stock market (). Transformative investment price and set is

mainly based upon the consolidation and management process that helps in constructing the data

in various form. Transformative venture is set progressively to profit PPHE. Fast approaching

extension in London (c 900 rooms) and broad redesigns ought to bring a stage change in

development opportunity While combination of its Croatian retreat organizations is now

satisfying (twofold digit ascend in room rate in Q3. In the interim, PPHE's Q3 exchanging update

communicated certainty it should keep on overcoming headwinds to live up to its 2016 outcomes

desires. Solid funds are obvious in August's exceptional profit of 100p/share and effective

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

lodging refinancing, which underline generous shrouded saves ('reasonable esteem' change of c

1,000p/offer to detailed 803p NAV). The share fluctuation indicates towards changes and

multiplications of both the existing and new shares.

There is an opportunity find out in Croatia share market. PPHE has selected this

particular form of business in more strategic and contingent manner. The profits from the

anticipated £115m improvement spend incorporated into our conjectures may accumulate in full

just past the extent of this audit. For one year from now, the benefit driver remains the new

rooms in London since expenses may be relied upon still to be an issue and the main

consideration of misfortune making Q1 will discourage Croatia. New development activity in

Croatia The proposed improvement of Are naturist, PPHE's recorded Croatian venture, into a

"generous Central and Eastern European relaxation and accommodation organization" is a

conceivably energizing supplement to PPHE's demonstrated spotlight on full-administration

"reasonable extravagance" inns with a decent geographic and visitor blend in European door

urban areas.

Corporate governance: significant changes development and changes was introduced

during the year 2018. A new premium segment of the main market of London Stock Market

initiated for making investor base stronger. New policies and streams were initiated and

improvise related to different sections and benefits for managing the report in different phases.

Creating value for investors and managing the operations also remained consistent for all the

operations and business improvements.

Market efficiency: Efficient share market is the main aspect considered essential in

terms of managing the effective flow of shares (Ahammad and Glaister, 2013). PPHE group has

initiated many partnership operations and businesses and are stable with the growth with

intensified corporation with Radisson hotel group. The unique central reservation system mainly

aligned with the perpetuity of maintaining the effective market position. The position mainly

associated with deploying the changes in various form as group’s interest and performance with

7

1,000p/offer to detailed 803p NAV). The share fluctuation indicates towards changes and

multiplications of both the existing and new shares.

There is an opportunity find out in Croatia share market. PPHE has selected this

particular form of business in more strategic and contingent manner. The profits from the

anticipated £115m improvement spend incorporated into our conjectures may accumulate in full

just past the extent of this audit. For one year from now, the benefit driver remains the new

rooms in London since expenses may be relied upon still to be an issue and the main

consideration of misfortune making Q1 will discourage Croatia. New development activity in

Croatia The proposed improvement of Are naturist, PPHE's recorded Croatian venture, into a

"generous Central and Eastern European relaxation and accommodation organization" is a

conceivably energizing supplement to PPHE's demonstrated spotlight on full-administration

"reasonable extravagance" inns with a decent geographic and visitor blend in European door

urban areas.

Corporate governance: significant changes development and changes was introduced

during the year 2018. A new premium segment of the main market of London Stock Market

initiated for making investor base stronger. New policies and streams were initiated and

improvise related to different sections and benefits for managing the report in different phases.

Creating value for investors and managing the operations also remained consistent for all the

operations and business improvements.

Market efficiency: Efficient share market is the main aspect considered essential in

terms of managing the effective flow of shares (Ahammad and Glaister, 2013). PPHE group has

initiated many partnership operations and businesses and are stable with the growth with

intensified corporation with Radisson hotel group. The unique central reservation system mainly

aligned with the perpetuity of maintaining the effective market position. The position mainly

associated with deploying the changes in various form as group’s interest and performance with

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

collective performance. The development in e commerce and distribution analyzed with

managing the flow of violability. Growth can be measurable by analyzing the annual Adjusted

EPS (Pence), it states that shareholders’ earning from operational activities with effective

adjustments. Changes are calculated with 4% of the group’s total and expected average cost was

to keep the real estate in effective form.

CONCLUSION

The above report concise the concept of financial management. It conclude the impact and

results of merger and acquisition done by organisation in various forms. Cost of capital, share

price payable by PPHE for the purchase of Andrew Brown sword Hotels limited cited in various

forms. It is resulted that after acquainting ABH limited the share price and market cap get

increased in London stock market. There is a positive impact reflected after the acquisition of

ABH limited.

8

managing the flow of violability. Growth can be measurable by analyzing the annual Adjusted

EPS (Pence), it states that shareholders’ earning from operational activities with effective

adjustments. Changes are calculated with 4% of the group’s total and expected average cost was

to keep the real estate in effective form.

CONCLUSION

The above report concise the concept of financial management. It conclude the impact and

results of merger and acquisition done by organisation in various forms. Cost of capital, share

price payable by PPHE for the purchase of Andrew Brown sword Hotels limited cited in various

forms. It is resulted that after acquainting ABH limited the share price and market cap get

increased in London stock market. There is a positive impact reflected after the acquisition of

ABH limited.

8

REFERENCES

Books and journals

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Zietlow, J., and e.t.all, 2018. Financial management for nonprofit organizations: policies and

practices. John Wiley & Sons.

Michalski, G., 2012. Accounts receivable management in nonprofit organizations. Zeszyty

Teoretyczne Rachunkowości, 68(124), pp.83-96.

Andreou, P. C., Louca, C. and Panayides, P. M., 2014. Corporate governance, financial

management decisions and firm performance: Evidence from the maritime

industry. Transportation Research Part E: Logistics and Transportation Review, 63,

pp.59-78.

Jain, P. K., Singh, S. and Yadav, S. S., 2013. Financial management practices. In An empirical

study of Indian corporates (Vol. 3, pp. 265-278). Springer New Delhi.

Akgün, A. E. and e.t.all, 2014. The mediator role of learning capability and business

innovativeness between total quality management and financial

performance. International Journal of Production Research, 52(3), pp.888-901.

Chen, C. M. and Chang, K. L., 2012. Diversification strategy and financial performance in the

Taiwanese hotel industry. International Journal of Hospitality Management, 31(3),

pp.1030-1032.

Lee, J. J., and e.t.all, 2014. The financial impact of loyalty programs in the hotel industry: A

social exchange theory perspective. Journal of Business Research, 67(10), pp.2139-

2146.

Fabozzi, F. J. and Drake, P. P., 2009. Finance: capital markets, financial management, and

investment management (Vol. 178). John Wiley & Sons.

Ahammad, M. F. and Glaister, K. W., 2013. The pre-acquisition evaluation of target firms and

cross border acquisition performance. International Business Review, 22(5), pp.894-

904.

Malmström, M., Wincent, J. and Johansson, J., 2013. Managing competence acquisition and

financial performance: An empirical study of how small firms use competence

acquisition strategies. Journal of engineering and technology management, 30(4),

pp.327-349.

Hasnan, S., Rahman, R. A. and Mahenthiran, S., 2012. Management motive, weak governance,

earnings management, and fraudulent financial reporting: Malaysian evidence. Journal

of International Accounting Research, 12(1), pp.1-27.

9

Books and journals

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Zietlow, J., and e.t.all, 2018. Financial management for nonprofit organizations: policies and

practices. John Wiley & Sons.

Michalski, G., 2012. Accounts receivable management in nonprofit organizations. Zeszyty

Teoretyczne Rachunkowości, 68(124), pp.83-96.

Andreou, P. C., Louca, C. and Panayides, P. M., 2014. Corporate governance, financial

management decisions and firm performance: Evidence from the maritime

industry. Transportation Research Part E: Logistics and Transportation Review, 63,

pp.59-78.

Jain, P. K., Singh, S. and Yadav, S. S., 2013. Financial management practices. In An empirical

study of Indian corporates (Vol. 3, pp. 265-278). Springer New Delhi.

Akgün, A. E. and e.t.all, 2014. The mediator role of learning capability and business

innovativeness between total quality management and financial

performance. International Journal of Production Research, 52(3), pp.888-901.

Chen, C. M. and Chang, K. L., 2012. Diversification strategy and financial performance in the

Taiwanese hotel industry. International Journal of Hospitality Management, 31(3),

pp.1030-1032.

Lee, J. J., and e.t.all, 2014. The financial impact of loyalty programs in the hotel industry: A

social exchange theory perspective. Journal of Business Research, 67(10), pp.2139-

2146.

Fabozzi, F. J. and Drake, P. P., 2009. Finance: capital markets, financial management, and

investment management (Vol. 178). John Wiley & Sons.

Ahammad, M. F. and Glaister, K. W., 2013. The pre-acquisition evaluation of target firms and

cross border acquisition performance. International Business Review, 22(5), pp.894-

904.

Malmström, M., Wincent, J. and Johansson, J., 2013. Managing competence acquisition and

financial performance: An empirical study of how small firms use competence

acquisition strategies. Journal of engineering and technology management, 30(4),

pp.327-349.

Hasnan, S., Rahman, R. A. and Mahenthiran, S., 2012. Management motive, weak governance,

earnings management, and fraudulent financial reporting: Malaysian evidence. Journal

of International Accounting Research, 12(1), pp.1-27.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.