Financial Project: WACC and NPV Analysis and Recommendations

VerifiedAdded on 2020/10/22

|4

|691

|119

Project

AI Summary

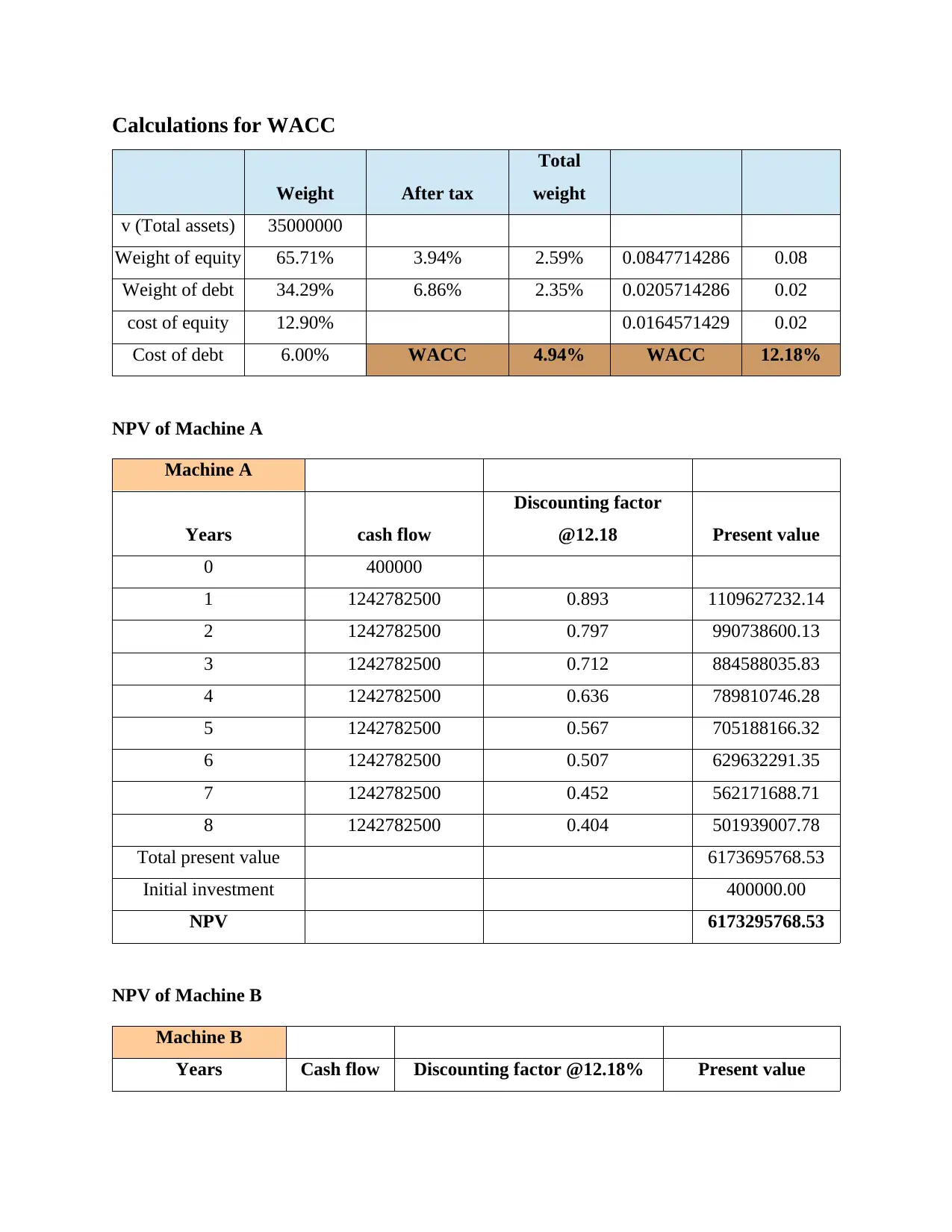

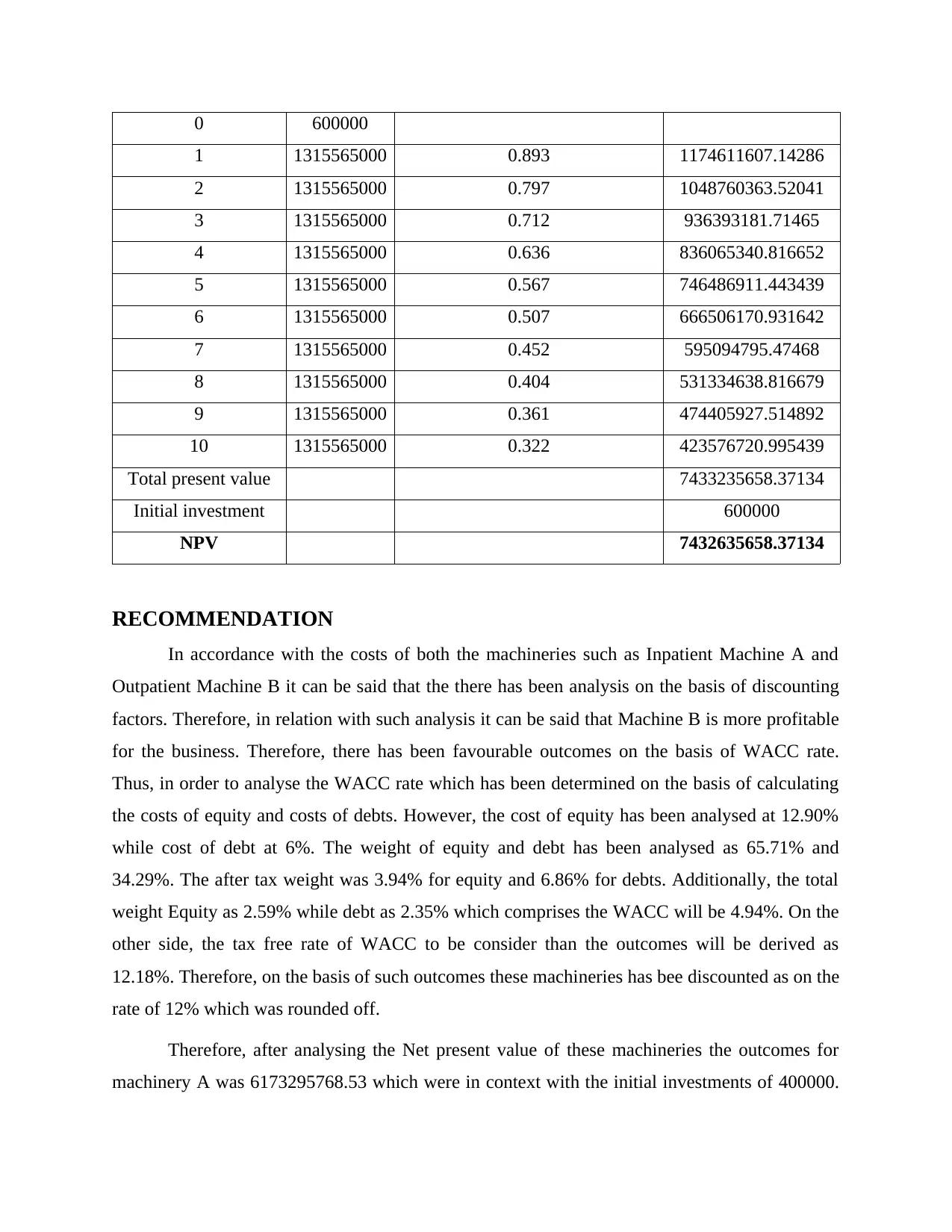

This financial analysis project evaluates two machine investment options (Machine A and Machine B) using Weighted Average Cost of Capital (WACC) and Net Present Value (NPV) calculations. The project begins with the calculation of WACC, considering the cost of equity (12.90%) and cost of debt (6%), along with their respective weights. The analysis then proceeds to calculate the NPV for each machine over a period of 8-10 years, using a discounting rate of 12.18%. Machine B demonstrates a significantly higher NPV (7432635658.37) compared to Machine A (6173295768.53), leading to the recommendation that the firm invest in Machine B due to its potential for greater profitability and positive future cash flows. The project highlights the importance of NPV as a key metric in investment decision-making.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.