Project Analysis and Financial Valuation Report: Finance Module

VerifiedAdded on 2022/09/02

|13

|1633

|18

Report

AI Summary

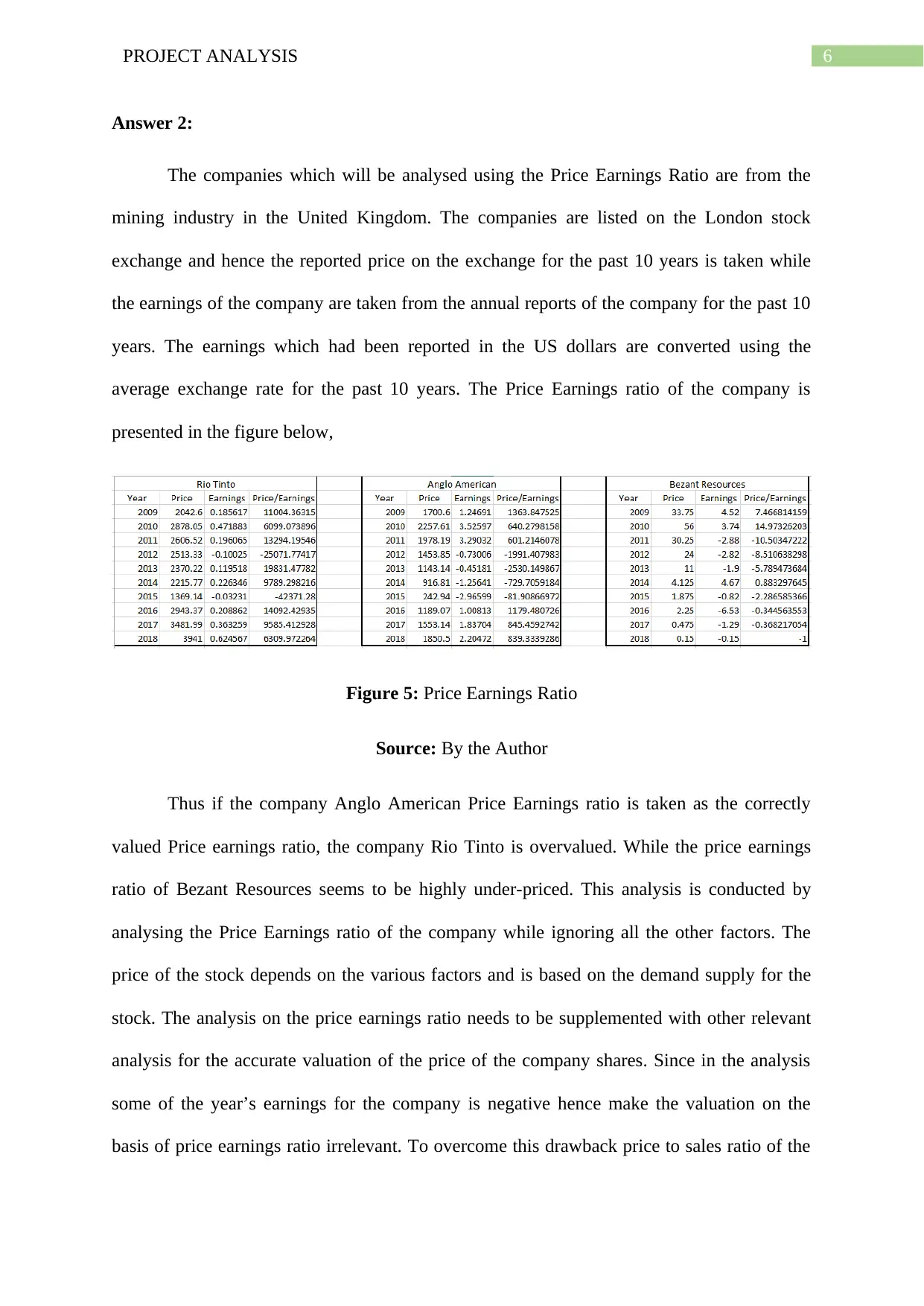

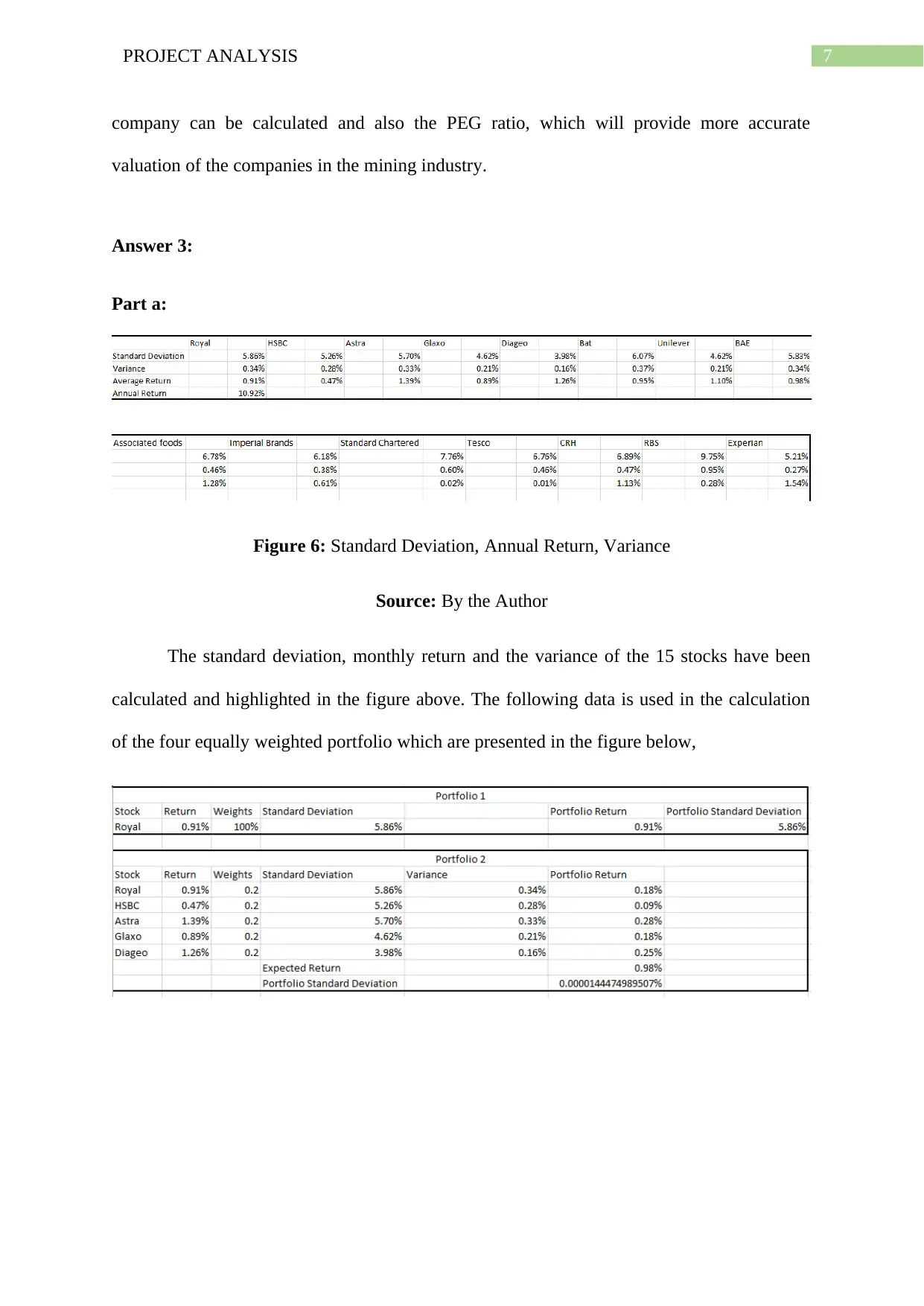

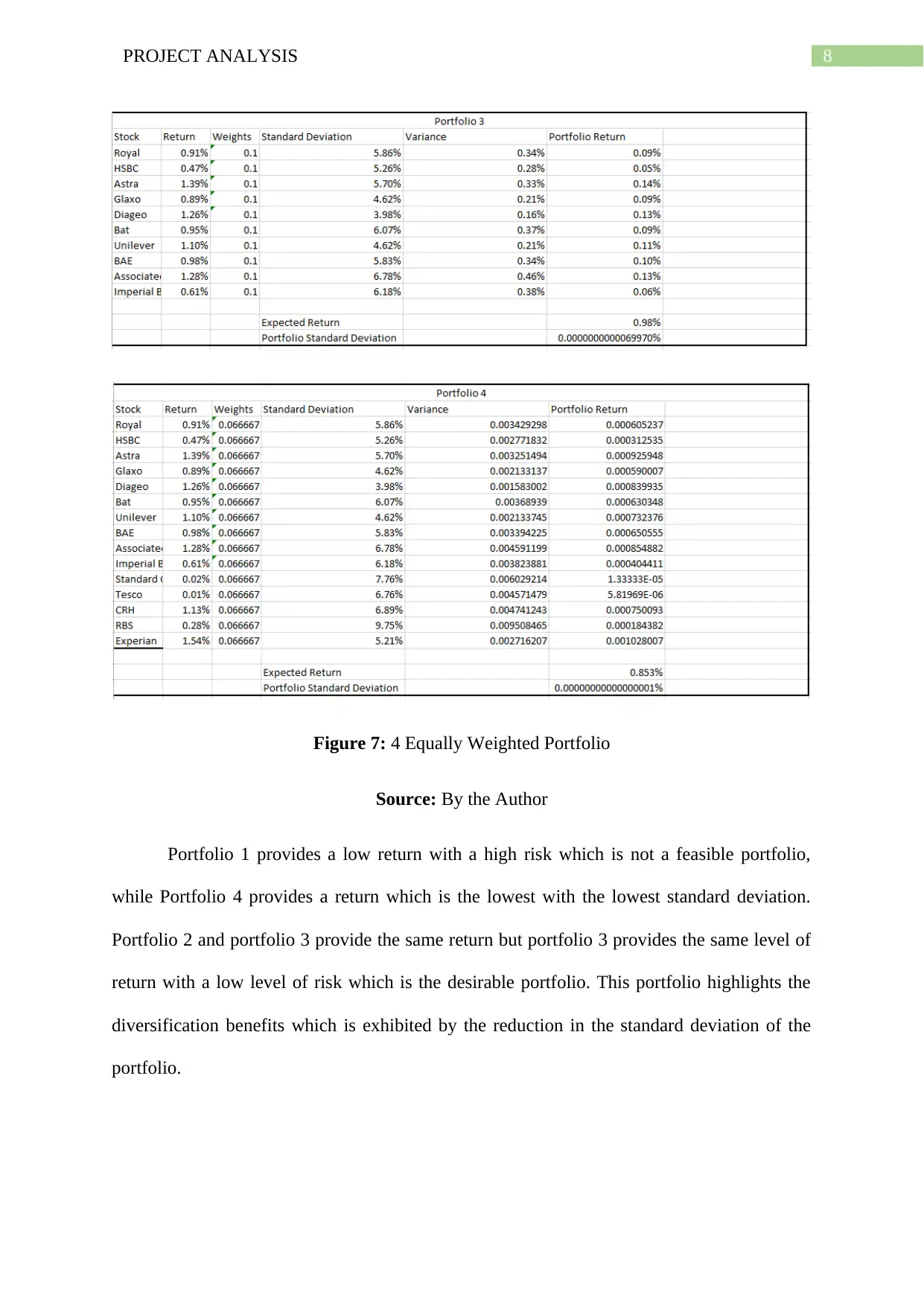

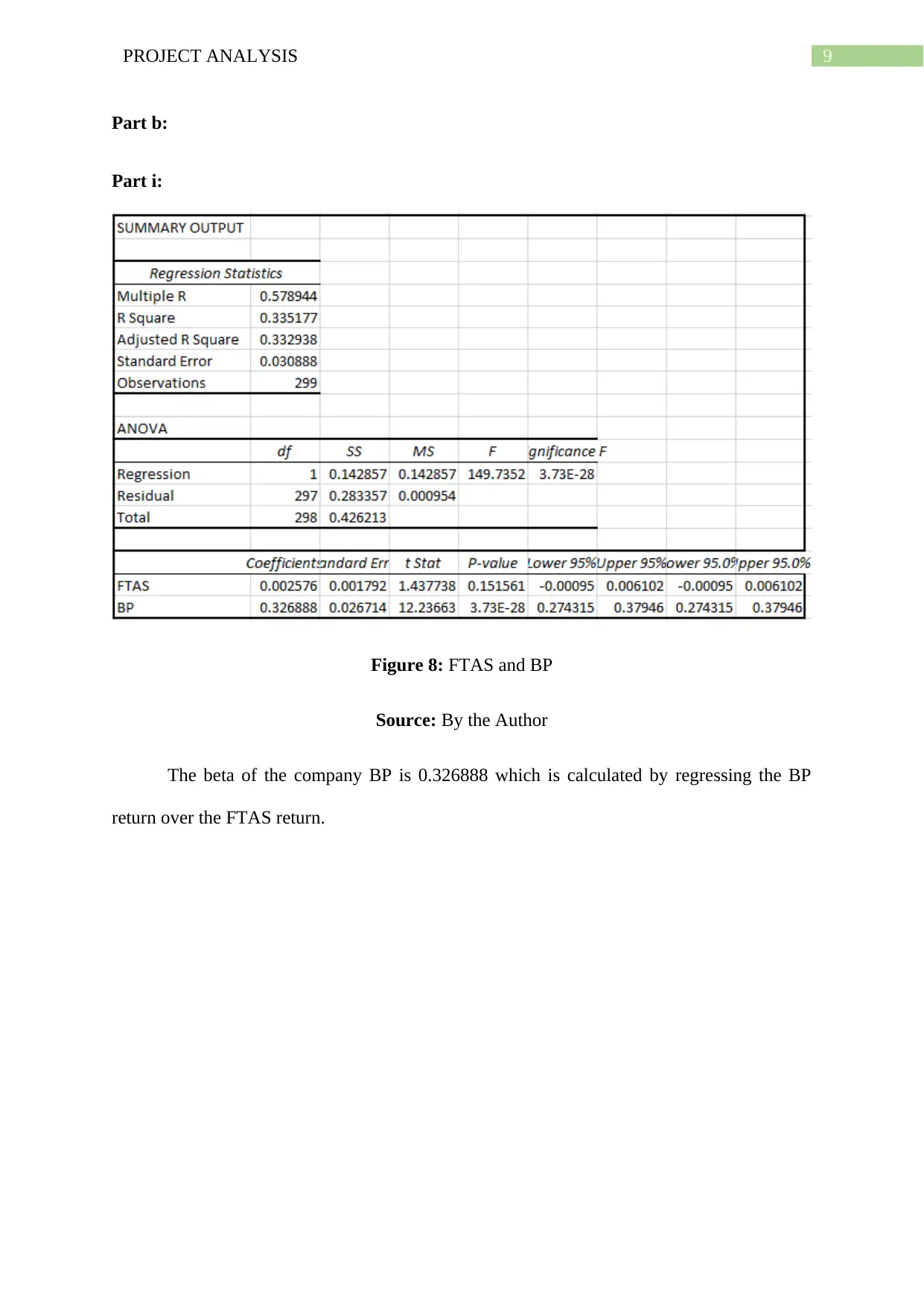

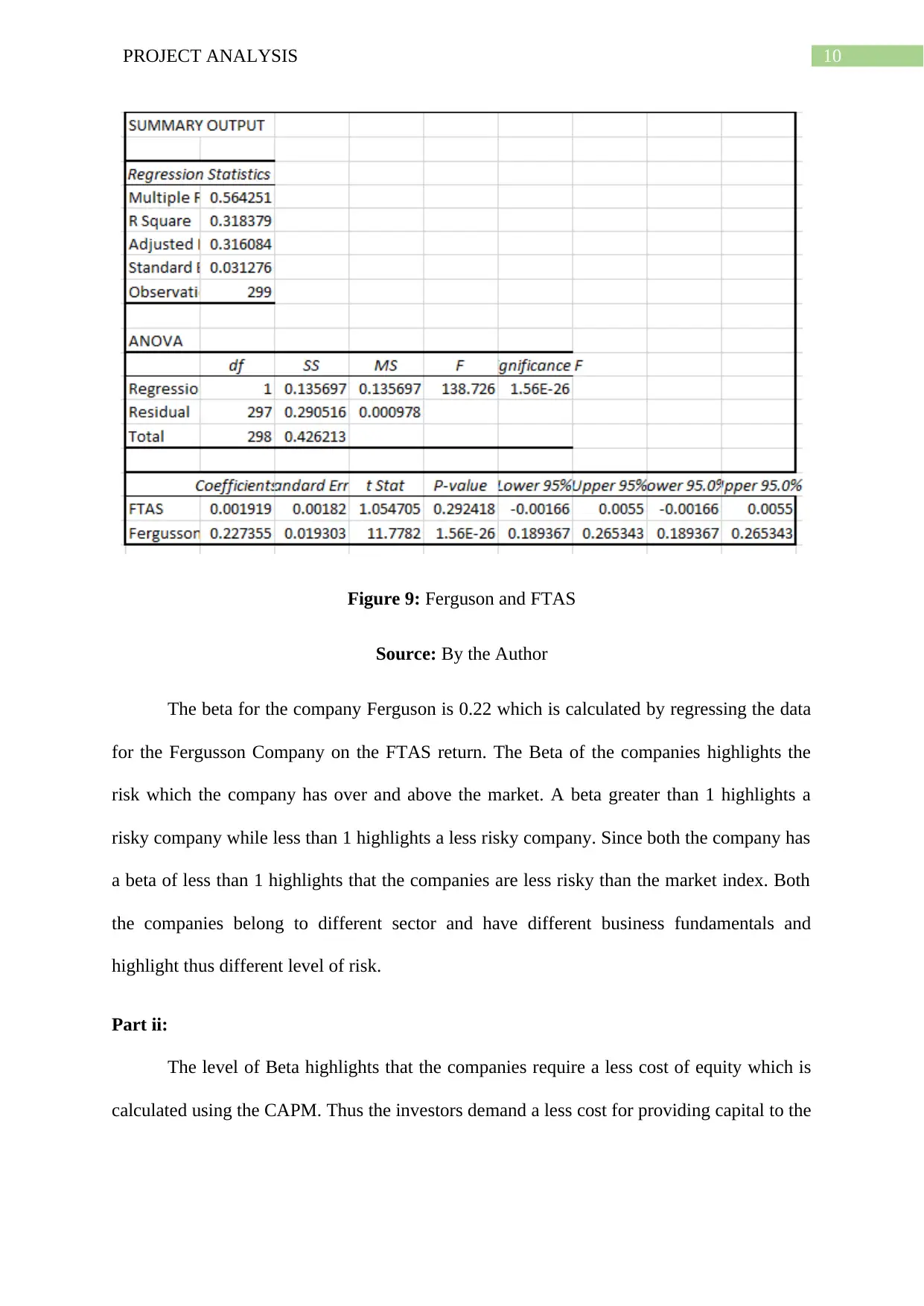

This report presents a comprehensive project analysis, encompassing financial valuation, sensitivity analysis, and portfolio management. The analysis begins with the calculation of Net Present Value (NPV) for a project, considering various data inputs and assumptions. A sensitivity analysis is performed to assess the impact of changes in sale price on the project's NPV. The report then explores the use of Price-Earnings (P/E) ratios for valuation of companies in the mining industry, acknowledging the limitations and suggesting alternative metrics like price-to-sales and PEG ratios. Finally, the report delves into portfolio analysis, calculating standard deviation, returns, and variance for various portfolios. Beta calculations are performed for two companies, and the implications of beta on cost of equity are discussed. The report concludes with a bibliography of relevant sources.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.