Financial Analysis and Property Investment Decision Making Report

VerifiedAdded on 2023/01/05

|10

|2955

|83

Report

AI Summary

This report provides a comprehensive financial analysis of a property investment decision. It begins with a client's requirements for a home, including space for a garden, parking, and a private room for recording YouTube videos. The report identifies a suitable property in Barking and Dagenham, analyzing its features and associated costs. A detailed analysis of the London real estate market is presented, including price trends and forecasts. A spreadsheet model is developed to assess the financial viability of the investment, calculating disposable income, expenses, and net present value (NPV). The analysis considers both a static scenario and a scenario with increasing salaries and expenses. The report concludes with a consultancy report summarizing the findings and offering recommendations based on financial and non-financial analyses, including the impact of inflation and potential rental income.

ACCOUNTING

FOR

DECISION MAKING

FOR

DECISION MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

1. Decision on property....................................................................................................................3

2. Detailed analysis of Real State market in London.......................................................................4

3. Spreadsheet model for the decision.............................................................................................4

4. Consultancy report.......................................................................................................................6

References......................................................................................................................................10

1. Decision on property....................................................................................................................3

2. Detailed analysis of Real State market in London.......................................................................4

3. Spreadsheet model for the decision.............................................................................................4

4. Consultancy report.......................................................................................................................6

References......................................................................................................................................10

1. Decision on property

Client requires a home with enough space for garden and parking space. Additional to this David

requires private room to record YouTube videos. Overall, it would be required one bedroom,

kitchen, bathroom, garden space, parking space, guest hall and one private room. In external

requirement, client needs good transport links to Central London and a car to travel to their

office few days a week.

Below is the shortlisted property which best suited with client’s requirement:

The best suited place to purchase housing property is Barking and Dagenham with an average

price of £300,000. From here it will take only 29 minutes with car to reach Central London as it

is only 13 miles far away from central city. All the internal demand of client’s such as one

bedroom, attach toilet, modular kitchen, one private room, garden and parking space can be

fulfilled after investing £302,445 overall money in Barking and Dagenham. The average price of

property other than this started with £325,000. Additional to this; client will also get facility of

excellent transport links into Central London with Cross rail to Chadwell Heath and the over

ground extension to Barking Riverside (Right move, 2020).

Other details:

Kitchen size: 12’9 × 12’ double glazed window

Lounge: 12’9 × 12’

Entrance: Front floor door in, radiator, stairs to first floor

Bedroom: 8.2 × 4’4 obscure double glazed window

Parking: On road permitted

Rear Garden: Paved patio area with small path, remainder laid to lawn, shrubs and flowerbeds

either side with shed to rear.

Loan: Available at monthly repayments of £1,298; annual interest @2.4% and 25 years

repayment period and at 10% down payment (Right move, 2020).

Client requires a home with enough space for garden and parking space. Additional to this David

requires private room to record YouTube videos. Overall, it would be required one bedroom,

kitchen, bathroom, garden space, parking space, guest hall and one private room. In external

requirement, client needs good transport links to Central London and a car to travel to their

office few days a week.

Below is the shortlisted property which best suited with client’s requirement:

The best suited place to purchase housing property is Barking and Dagenham with an average

price of £300,000. From here it will take only 29 minutes with car to reach Central London as it

is only 13 miles far away from central city. All the internal demand of client’s such as one

bedroom, attach toilet, modular kitchen, one private room, garden and parking space can be

fulfilled after investing £302,445 overall money in Barking and Dagenham. The average price of

property other than this started with £325,000. Additional to this; client will also get facility of

excellent transport links into Central London with Cross rail to Chadwell Heath and the over

ground extension to Barking Riverside (Right move, 2020).

Other details:

Kitchen size: 12’9 × 12’ double glazed window

Lounge: 12’9 × 12’

Entrance: Front floor door in, radiator, stairs to first floor

Bedroom: 8.2 × 4’4 obscure double glazed window

Parking: On road permitted

Rear Garden: Paved patio area with small path, remainder laid to lawn, shrubs and flowerbeds

either side with shed to rear.

Loan: Available at monthly repayments of £1,298; annual interest @2.4% and 25 years

repayment period and at 10% down payment (Right move, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Detailed analysis of Real State market in London

House prices in London will end the year with an overall increase of 2.5%, according to a study

by Hamptons International. In its latest housing market report the estate agent chain expects

prices in the UK to rise 2% in 2020, up from 0.9% in 2019. Wales (3%) and London (2.5%) will

see the strongest house price growth this year (London house prices, 2020).

“London’s market rebounded quickly after the easing of lockdown, buoyed by pent-up demand

over the last few years and an increase in the number of people bringing forward a decision to

move,” Hamptons said in the study. “This is also the region where buyers enjoy the greatest

benefit from the stamp duty holiday.”

As a result, Hamptons expects house prices in London will rise 2.5% in 2020, offsetting the

decline of -0.4% in 2019. However, the number of homes coming onto the market for sale in the

capital is climbing. In August there were 78% more new instructions than at the same time last

year (London house prices, 2020).

Hamptons forecasts that this may contribute to a 1% house price fall in 2021, when combined

with “existing affordability barriers, lack of international buyers, the end of the stamp duty

holiday and an increase in the number of households seeking to relocate elsewhere”.

The report also says that the economy recovers, and it is expected that London’s market to return

to its longer-term cycle. Since prices have risen by 53% in the city over the last ten years

compared with an average of 10% in the north, it is expected that London will underperform

northern regions. House prices in London will rise 1.5% in 2022 and 3% in 2023, putting four-

year growth at 5.5%.”

Based on above report; the couple will try to purchase new home before 2022 to avoid the price

rise of 1.5%. At this time, market is facing recession and hence price of real estate property is

also low. Therefore, it is the right time to purchase property at low price (London house prices,

2020).

House prices in London will end the year with an overall increase of 2.5%, according to a study

by Hamptons International. In its latest housing market report the estate agent chain expects

prices in the UK to rise 2% in 2020, up from 0.9% in 2019. Wales (3%) and London (2.5%) will

see the strongest house price growth this year (London house prices, 2020).

“London’s market rebounded quickly after the easing of lockdown, buoyed by pent-up demand

over the last few years and an increase in the number of people bringing forward a decision to

move,” Hamptons said in the study. “This is also the region where buyers enjoy the greatest

benefit from the stamp duty holiday.”

As a result, Hamptons expects house prices in London will rise 2.5% in 2020, offsetting the

decline of -0.4% in 2019. However, the number of homes coming onto the market for sale in the

capital is climbing. In August there were 78% more new instructions than at the same time last

year (London house prices, 2020).

Hamptons forecasts that this may contribute to a 1% house price fall in 2021, when combined

with “existing affordability barriers, lack of international buyers, the end of the stamp duty

holiday and an increase in the number of households seeking to relocate elsewhere”.

The report also says that the economy recovers, and it is expected that London’s market to return

to its longer-term cycle. Since prices have risen by 53% in the city over the last ten years

compared with an average of 10% in the north, it is expected that London will underperform

northern regions. House prices in London will rise 1.5% in 2022 and 3% in 2023, putting four-

year growth at 5.5%.”

Based on above report; the couple will try to purchase new home before 2022 to avoid the price

rise of 1.5%. At this time, market is facing recession and hence price of real estate property is

also low. Therefore, it is the right time to purchase property at low price (London house prices,

2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

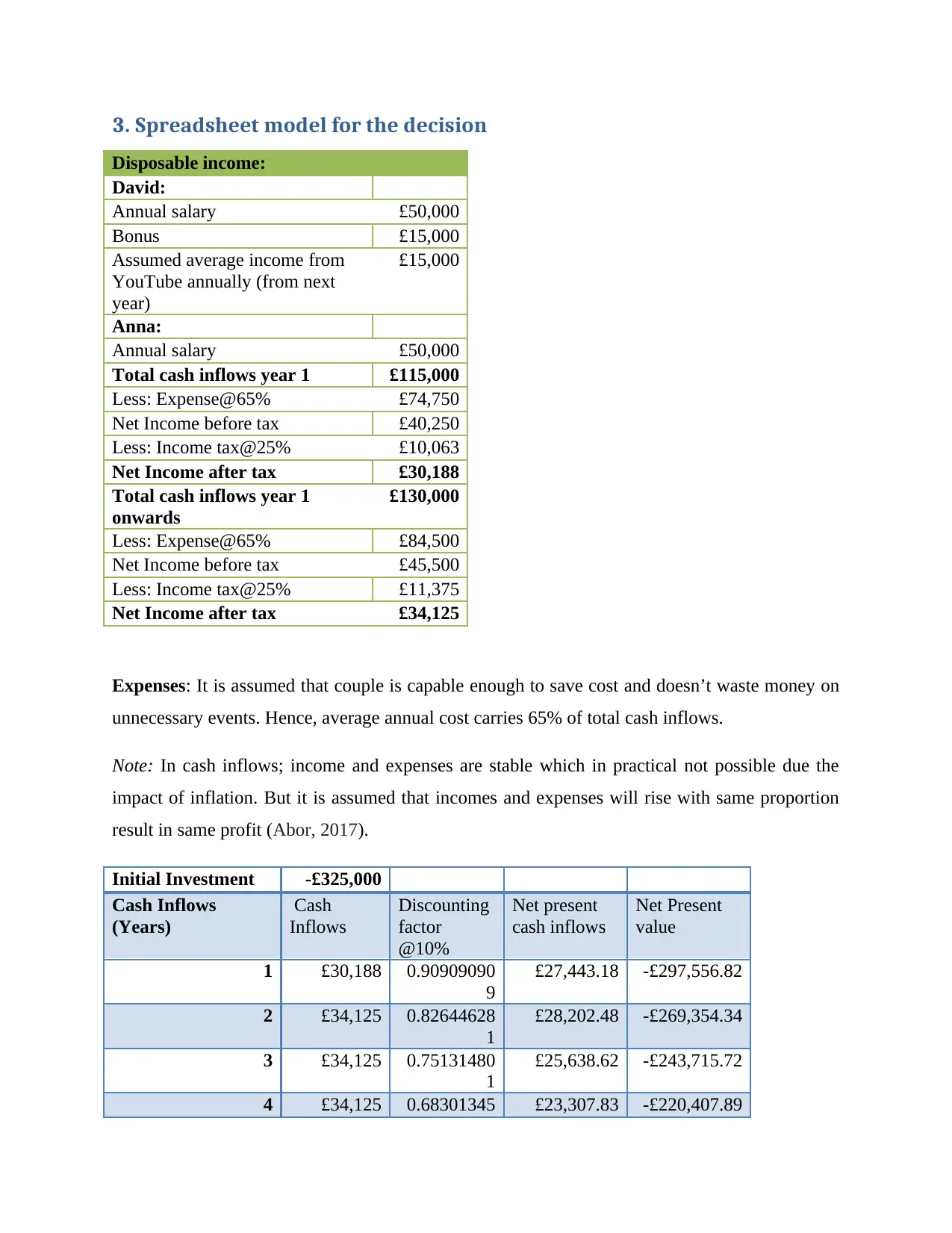

3. Spreadsheet model for the decision

Disposable income:

David:

Annual salary £50,000

Bonus £15,000

Assumed average income from

YouTube annually (from next

year)

£15,000

Anna:

Annual salary £50,000

Total cash inflows year 1 £115,000

Less: Expense@65% £74,750

Net Income before tax £40,250

Less: Income tax@25% £10,063

Net Income after tax £30,188

Total cash inflows year 1

onwards

£130,000

Less: Expense@65% £84,500

Net Income before tax £45,500

Less: Income tax@25% £11,375

Net Income after tax £34,125

Expenses: It is assumed that couple is capable enough to save cost and doesn’t waste money on

unnecessary events. Hence, average annual cost carries 65% of total cash inflows.

Note: In cash inflows; income and expenses are stable which in practical not possible due the

impact of inflation. But it is assumed that incomes and expenses will rise with same proportion

result in same profit (Abor, 2017).

Initial Investment -£325,000

Cash Inflows

(Years)

Cash

Inflows

Discounting

factor

@10%

Net present

cash inflows

Net Present

value

1 £30,188 0.90909090

9

£27,443.18 -£297,556.82

2 £34,125 0.82644628

1

£28,202.48 -£269,354.34

3 £34,125 0.75131480

1

£25,638.62 -£243,715.72

4 £34,125 0.68301345 £23,307.83 -£220,407.89

Disposable income:

David:

Annual salary £50,000

Bonus £15,000

Assumed average income from

YouTube annually (from next

year)

£15,000

Anna:

Annual salary £50,000

Total cash inflows year 1 £115,000

Less: Expense@65% £74,750

Net Income before tax £40,250

Less: Income tax@25% £10,063

Net Income after tax £30,188

Total cash inflows year 1

onwards

£130,000

Less: Expense@65% £84,500

Net Income before tax £45,500

Less: Income tax@25% £11,375

Net Income after tax £34,125

Expenses: It is assumed that couple is capable enough to save cost and doesn’t waste money on

unnecessary events. Hence, average annual cost carries 65% of total cash inflows.

Note: In cash inflows; income and expenses are stable which in practical not possible due the

impact of inflation. But it is assumed that incomes and expenses will rise with same proportion

result in same profit (Abor, 2017).

Initial Investment -£325,000

Cash Inflows

(Years)

Cash

Inflows

Discounting

factor

@10%

Net present

cash inflows

Net Present

value

1 £30,188 0.90909090

9

£27,443.18 -£297,556.82

2 £34,125 0.82644628

1

£28,202.48 -£269,354.34

3 £34,125 0.75131480

1

£25,638.62 -£243,715.72

4 £34,125 0.68301345 £23,307.83 -£220,407.89

5

5 £34,125 0.62092132

3

£21,188.94 -£199,218.95

6 £34,125 0.56447393 £19,262.67 -£179,956.27

7 £34,125 0.51315811

8

£17,511.52 -£162,444.75

8 £34,125 0.46650738 £15,919.56 -£146,525.19

9 £34,125 0.42409761

8

£14,472.33 -£132,052.86

10 £34,125 0.38554328

9

£13,156.66 -£118,896.19

The above results show that net present value is negative by £118,896.19. This indicates that

price of the house has not been covered by couple in 10 years of period and it will take more

time. To get positive net present value; it is necessary to either increase net cash inflows or

reduce expenses (Abor, 2017).

4. Consultancy report

Executive Summary

This report is based on the analysis of investment decision based on financial and non-financial

analyses. The decision has to be made about whether to buy or rent house. The report is ended

with recommendation in the form of advice to the client with explanation of reason behind

particular decision.

Financial Analyses

Financial analysis is the method of evaluating organizations, commitments, spending plans and

other money-related exchanges to determine their presentation and appropriateness. Monetary

analysis is routinely used to determine whether an item is stable, soluble, mobile, or productive

enough to warrant a financial firm.

Financial analysis is used to evaluate liquidity models, set a budgeting approach, develop

slow long-term plans for the movement of businesses, and identify profitable businesses or

organizations. This is done by combining numbers and information relating to money. A budget

expert analyzes an organization's tax records: the payroll call, accounting report, and revenue.

Money analysis can be conducted for both business accounts and business money. One of the

best known methods for analyzing financial information is to extract quotes from information in

tax reports to think whether against certain groups or against the harmful performance of

financial information own organization (Abernathy and et.al., 2019).

For calculating disposable income; it is assumed that couple pays taxes at the rate of 25%.

Couple will get stable cash inflows without any increment over the year and from YouTube also

5 £34,125 0.62092132

3

£21,188.94 -£199,218.95

6 £34,125 0.56447393 £19,262.67 -£179,956.27

7 £34,125 0.51315811

8

£17,511.52 -£162,444.75

8 £34,125 0.46650738 £15,919.56 -£146,525.19

9 £34,125 0.42409761

8

£14,472.33 -£132,052.86

10 £34,125 0.38554328

9

£13,156.66 -£118,896.19

The above results show that net present value is negative by £118,896.19. This indicates that

price of the house has not been covered by couple in 10 years of period and it will take more

time. To get positive net present value; it is necessary to either increase net cash inflows or

reduce expenses (Abor, 2017).

4. Consultancy report

Executive Summary

This report is based on the analysis of investment decision based on financial and non-financial

analyses. The decision has to be made about whether to buy or rent house. The report is ended

with recommendation in the form of advice to the client with explanation of reason behind

particular decision.

Financial Analyses

Financial analysis is the method of evaluating organizations, commitments, spending plans and

other money-related exchanges to determine their presentation and appropriateness. Monetary

analysis is routinely used to determine whether an item is stable, soluble, mobile, or productive

enough to warrant a financial firm.

Financial analysis is used to evaluate liquidity models, set a budgeting approach, develop

slow long-term plans for the movement of businesses, and identify profitable businesses or

organizations. This is done by combining numbers and information relating to money. A budget

expert analyzes an organization's tax records: the payroll call, accounting report, and revenue.

Money analysis can be conducted for both business accounts and business money. One of the

best known methods for analyzing financial information is to extract quotes from information in

tax reports to think whether against certain groups or against the harmful performance of

financial information own organization (Abernathy and et.al., 2019).

For calculating disposable income; it is assumed that couple pays taxes at the rate of 25%.

Couple will get stable cash inflows without any increment over the year and from YouTube also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

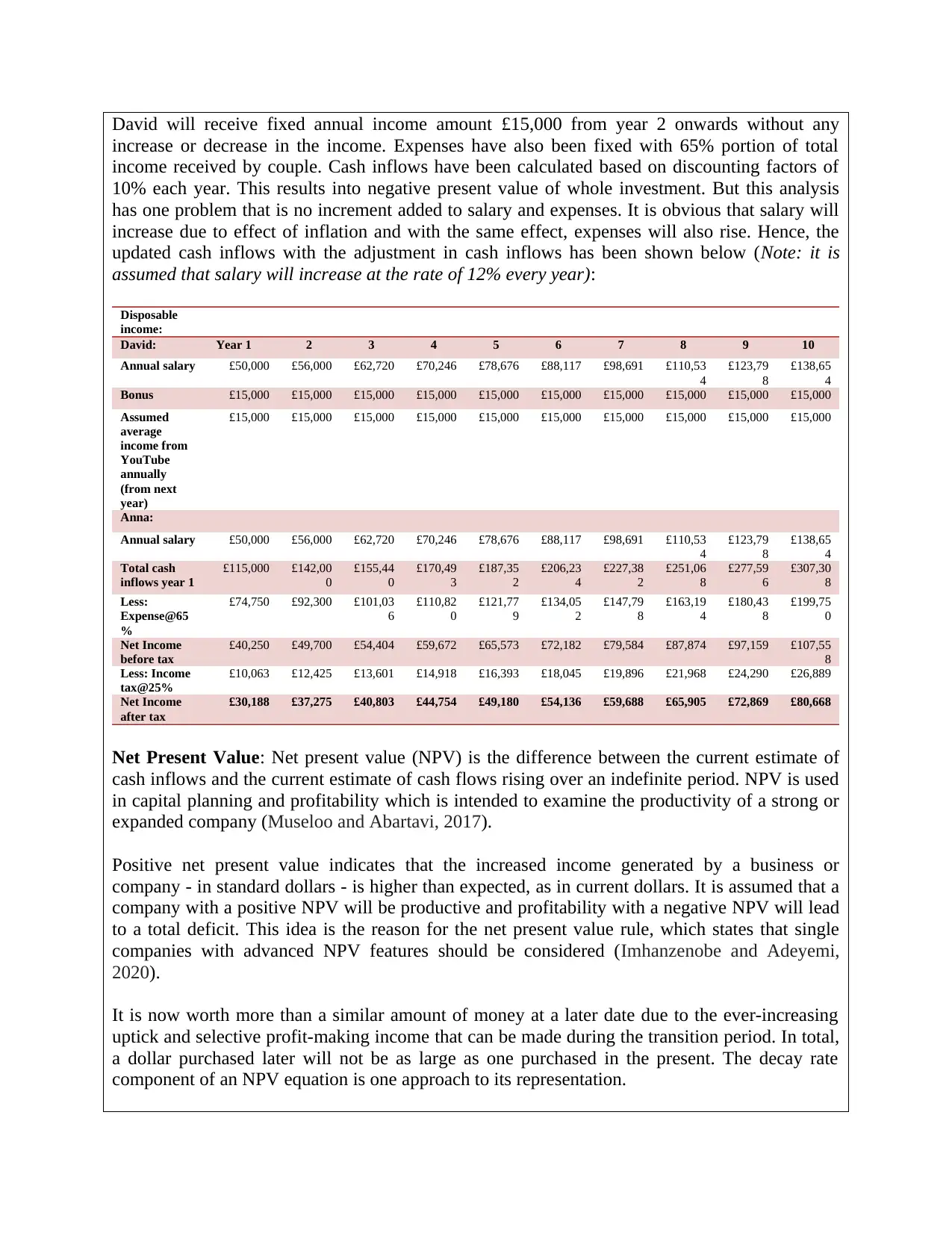

David will receive fixed annual income amount £15,000 from year 2 onwards without any

increase or decrease in the income. Expenses have also been fixed with 65% portion of total

income received by couple. Cash inflows have been calculated based on discounting factors of

10% each year. This results into negative present value of whole investment. But this analysis

has one problem that is no increment added to salary and expenses. It is obvious that salary will

increase due to effect of inflation and with the same effect, expenses will also rise. Hence, the

updated cash inflows with the adjustment in cash inflows has been shown below (Note: it is

assumed that salary will increase at the rate of 12% every year):

Disposable

income:

David: Year 1 2 3 4 5 6 7 8 9 10

Annual salary £50,000 £56,000 £62,720 £70,246 £78,676 £88,117 £98,691 £110,53

4

£123,79

8

£138,65

4

Bonus £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000

Assumed

average

income from

YouTube

annually

(from next

year)

£15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000

Anna:

Annual salary £50,000 £56,000 £62,720 £70,246 £78,676 £88,117 £98,691 £110,53

4

£123,79

8

£138,65

4

Total cash

inflows year 1

£115,000 £142,00

0

£155,44

0

£170,49

3

£187,35

2

£206,23

4

£227,38

2

£251,06

8

£277,59

6

£307,30

8

Less:

Expense@65

%

£74,750 £92,300 £101,03

6

£110,82

0

£121,77

9

£134,05

2

£147,79

8

£163,19

4

£180,43

8

£199,75

0

Net Income

before tax

£40,250 £49,700 £54,404 £59,672 £65,573 £72,182 £79,584 £87,874 £97,159 £107,55

8

Less: Income

tax@25%

£10,063 £12,425 £13,601 £14,918 £16,393 £18,045 £19,896 £21,968 £24,290 £26,889

Net Income

after tax

£30,188 £37,275 £40,803 £44,754 £49,180 £54,136 £59,688 £65,905 £72,869 £80,668

Net Present Value: Net present value (NPV) is the difference between the current estimate of

cash inflows and the current estimate of cash flows rising over an indefinite period. NPV is used

in capital planning and profitability which is intended to examine the productivity of a strong or

expanded company (Museloo and Abartavi, 2017).

Positive net present value indicates that the increased income generated by a business or

company - in standard dollars - is higher than expected, as in current dollars. It is assumed that a

company with a positive NPV will be productive and profitability with a negative NPV will lead

to a total deficit. This idea is the reason for the net present value rule, which states that single

companies with advanced NPV features should be considered (Imhanzenobe and Adeyemi,

2020).

It is now worth more than a similar amount of money at a later date due to the ever-increasing

uptick and selective profit-making income that can be made during the transition period. In total,

a dollar purchased later will not be as large as one purchased in the present. The decay rate

component of an NPV equation is one approach to its representation.

increase or decrease in the income. Expenses have also been fixed with 65% portion of total

income received by couple. Cash inflows have been calculated based on discounting factors of

10% each year. This results into negative present value of whole investment. But this analysis

has one problem that is no increment added to salary and expenses. It is obvious that salary will

increase due to effect of inflation and with the same effect, expenses will also rise. Hence, the

updated cash inflows with the adjustment in cash inflows has been shown below (Note: it is

assumed that salary will increase at the rate of 12% every year):

Disposable

income:

David: Year 1 2 3 4 5 6 7 8 9 10

Annual salary £50,000 £56,000 £62,720 £70,246 £78,676 £88,117 £98,691 £110,53

4

£123,79

8

£138,65

4

Bonus £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000

Assumed

average

income from

YouTube

annually

(from next

year)

£15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000 £15,000

Anna:

Annual salary £50,000 £56,000 £62,720 £70,246 £78,676 £88,117 £98,691 £110,53

4

£123,79

8

£138,65

4

Total cash

inflows year 1

£115,000 £142,00

0

£155,44

0

£170,49

3

£187,35

2

£206,23

4

£227,38

2

£251,06

8

£277,59

6

£307,30

8

Less:

Expense@65

%

£74,750 £92,300 £101,03

6

£110,82

0

£121,77

9

£134,05

2

£147,79

8

£163,19

4

£180,43

8

£199,75

0

Net Income

before tax

£40,250 £49,700 £54,404 £59,672 £65,573 £72,182 £79,584 £87,874 £97,159 £107,55

8

Less: Income

tax@25%

£10,063 £12,425 £13,601 £14,918 £16,393 £18,045 £19,896 £21,968 £24,290 £26,889

Net Income

after tax

£30,188 £37,275 £40,803 £44,754 £49,180 £54,136 £59,688 £65,905 £72,869 £80,668

Net Present Value: Net present value (NPV) is the difference between the current estimate of

cash inflows and the current estimate of cash flows rising over an indefinite period. NPV is used

in capital planning and profitability which is intended to examine the productivity of a strong or

expanded company (Museloo and Abartavi, 2017).

Positive net present value indicates that the increased income generated by a business or

company - in standard dollars - is higher than expected, as in current dollars. It is assumed that a

company with a positive NPV will be productive and profitability with a negative NPV will lead

to a total deficit. This idea is the reason for the net present value rule, which states that single

companies with advanced NPV features should be considered (Imhanzenobe and Adeyemi,

2020).

It is now worth more than a similar amount of money at a later date due to the ever-increasing

uptick and selective profit-making income that can be made during the transition period. In total,

a dollar purchased later will not be as large as one purchased in the present. The decay rate

component of an NPV equation is one approach to its representation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

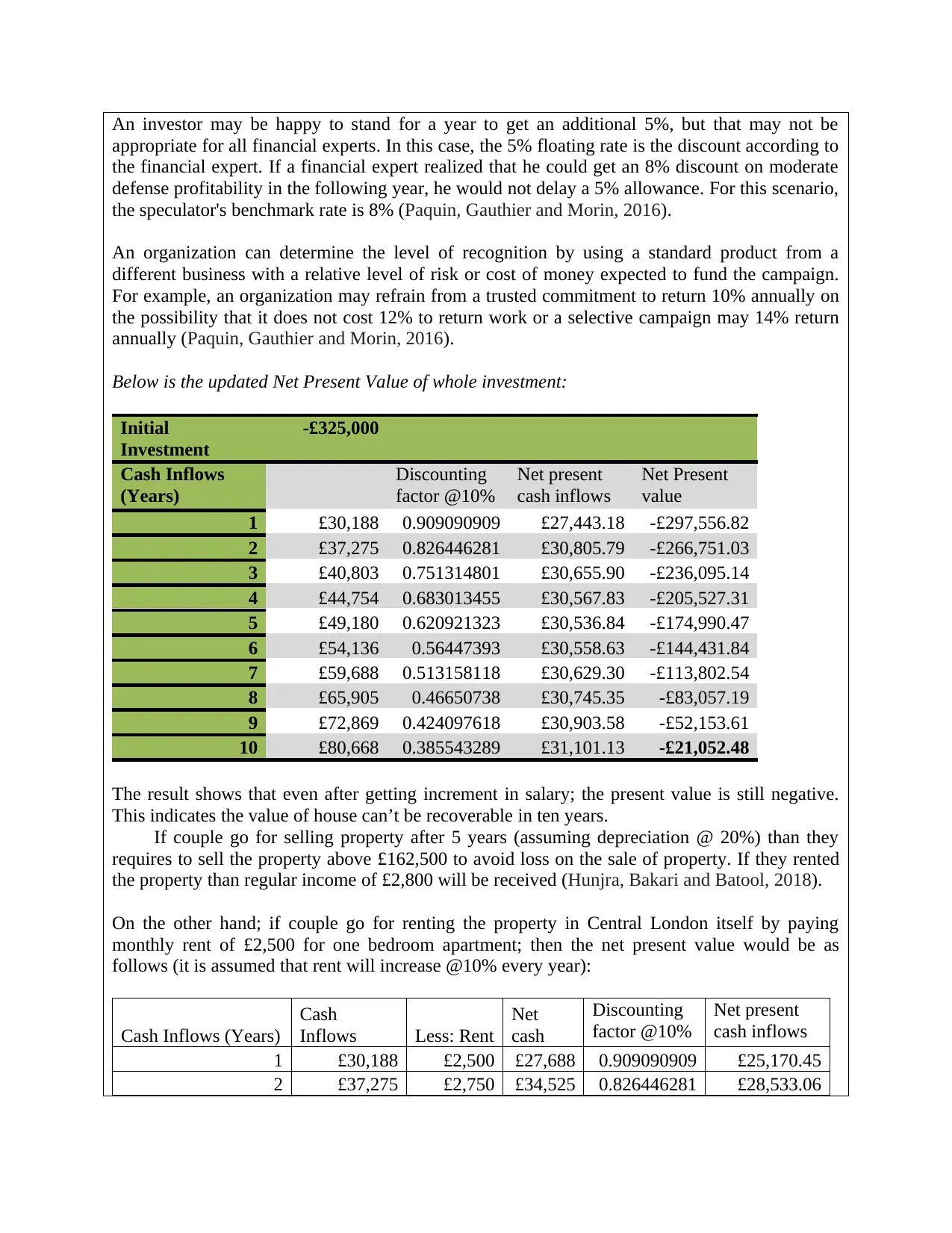

An investor may be happy to stand for a year to get an additional 5%, but that may not be

appropriate for all financial experts. In this case, the 5% floating rate is the discount according to

the financial expert. If a financial expert realized that he could get an 8% discount on moderate

defense profitability in the following year, he would not delay a 5% allowance. For this scenario,

the speculator's benchmark rate is 8% (Paquin, Gauthier and Morin, 2016).

An organization can determine the level of recognition by using a standard product from a

different business with a relative level of risk or cost of money expected to fund the campaign.

For example, an organization may refrain from a trusted commitment to return 10% annually on

the possibility that it does not cost 12% to return work or a selective campaign may 14% return

annually (Paquin, Gauthier and Morin, 2016).

Below is the updated Net Present Value of whole investment:

Initial

Investment

-£325,000

Cash Inflows

(Years)

Discounting

factor @10%

Net present

cash inflows

Net Present

value

1 £30,188 0.909090909 £27,443.18 -£297,556.82

2 £37,275 0.826446281 £30,805.79 -£266,751.03

3 £40,803 0.751314801 £30,655.90 -£236,095.14

4 £44,754 0.683013455 £30,567.83 -£205,527.31

5 £49,180 0.620921323 £30,536.84 -£174,990.47

6 £54,136 0.56447393 £30,558.63 -£144,431.84

7 £59,688 0.513158118 £30,629.30 -£113,802.54

8 £65,905 0.46650738 £30,745.35 -£83,057.19

9 £72,869 0.424097618 £30,903.58 -£52,153.61

10 £80,668 0.385543289 £31,101.13 -£21,052.48

The result shows that even after getting increment in salary; the present value is still negative.

This indicates the value of house can’t be recoverable in ten years.

If couple go for selling property after 5 years (assuming depreciation @ 20%) than they

requires to sell the property above £162,500 to avoid loss on the sale of property. If they rented

the property than regular income of £2,800 will be received (Hunjra, Bakari and Batool, 2018).

On the other hand; if couple go for renting the property in Central London itself by paying

monthly rent of £2,500 for one bedroom apartment; then the net present value would be as

follows (it is assumed that rent will increase @10% every year):

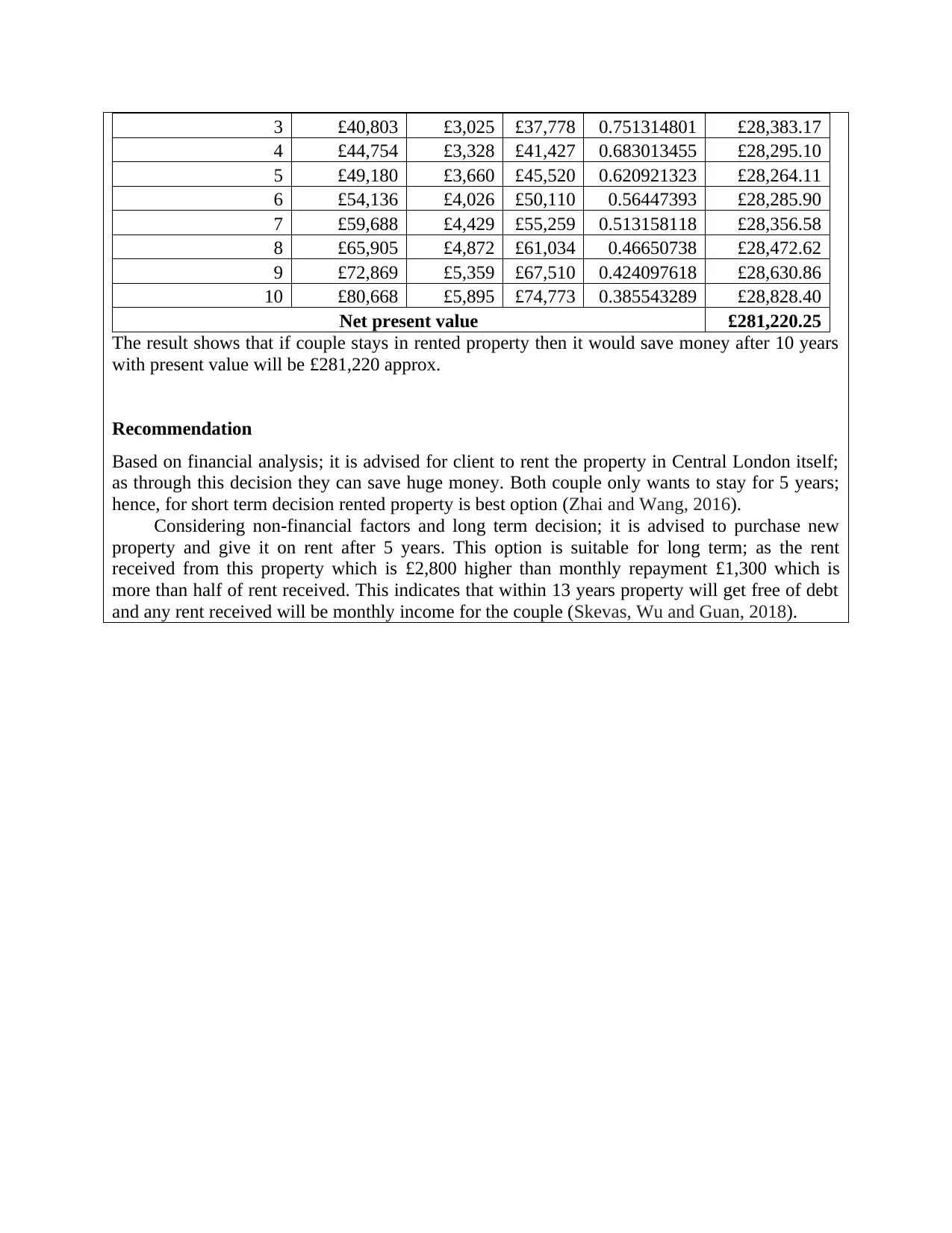

Cash Inflows (Years)

Cash

Inflows Less: Rent

Net

cash

Discounting

factor @10%

Net present

cash inflows

1 £30,188 £2,500 £27,688 0.909090909 £25,170.45

2 £37,275 £2,750 £34,525 0.826446281 £28,533.06

appropriate for all financial experts. In this case, the 5% floating rate is the discount according to

the financial expert. If a financial expert realized that he could get an 8% discount on moderate

defense profitability in the following year, he would not delay a 5% allowance. For this scenario,

the speculator's benchmark rate is 8% (Paquin, Gauthier and Morin, 2016).

An organization can determine the level of recognition by using a standard product from a

different business with a relative level of risk or cost of money expected to fund the campaign.

For example, an organization may refrain from a trusted commitment to return 10% annually on

the possibility that it does not cost 12% to return work or a selective campaign may 14% return

annually (Paquin, Gauthier and Morin, 2016).

Below is the updated Net Present Value of whole investment:

Initial

Investment

-£325,000

Cash Inflows

(Years)

Discounting

factor @10%

Net present

cash inflows

Net Present

value

1 £30,188 0.909090909 £27,443.18 -£297,556.82

2 £37,275 0.826446281 £30,805.79 -£266,751.03

3 £40,803 0.751314801 £30,655.90 -£236,095.14

4 £44,754 0.683013455 £30,567.83 -£205,527.31

5 £49,180 0.620921323 £30,536.84 -£174,990.47

6 £54,136 0.56447393 £30,558.63 -£144,431.84

7 £59,688 0.513158118 £30,629.30 -£113,802.54

8 £65,905 0.46650738 £30,745.35 -£83,057.19

9 £72,869 0.424097618 £30,903.58 -£52,153.61

10 £80,668 0.385543289 £31,101.13 -£21,052.48

The result shows that even after getting increment in salary; the present value is still negative.

This indicates the value of house can’t be recoverable in ten years.

If couple go for selling property after 5 years (assuming depreciation @ 20%) than they

requires to sell the property above £162,500 to avoid loss on the sale of property. If they rented

the property than regular income of £2,800 will be received (Hunjra, Bakari and Batool, 2018).

On the other hand; if couple go for renting the property in Central London itself by paying

monthly rent of £2,500 for one bedroom apartment; then the net present value would be as

follows (it is assumed that rent will increase @10% every year):

Cash Inflows (Years)

Cash

Inflows Less: Rent

Net

cash

Discounting

factor @10%

Net present

cash inflows

1 £30,188 £2,500 £27,688 0.909090909 £25,170.45

2 £37,275 £2,750 £34,525 0.826446281 £28,533.06

3 £40,803 £3,025 £37,778 0.751314801 £28,383.17

4 £44,754 £3,328 £41,427 0.683013455 £28,295.10

5 £49,180 £3,660 £45,520 0.620921323 £28,264.11

6 £54,136 £4,026 £50,110 0.56447393 £28,285.90

7 £59,688 £4,429 £55,259 0.513158118 £28,356.58

8 £65,905 £4,872 £61,034 0.46650738 £28,472.62

9 £72,869 £5,359 £67,510 0.424097618 £28,630.86

10 £80,668 £5,895 £74,773 0.385543289 £28,828.40

Net present value £281,220.25

The result shows that if couple stays in rented property then it would save money after 10 years

with present value will be £281,220 approx.

Recommendation

Based on financial analysis; it is advised for client to rent the property in Central London itself;

as through this decision they can save huge money. Both couple only wants to stay for 5 years;

hence, for short term decision rented property is best option (Zhai and Wang, 2016).

Considering non-financial factors and long term decision; it is advised to purchase new

property and give it on rent after 5 years. This option is suitable for long term; as the rent

received from this property which is £2,800 higher than monthly repayment £1,300 which is

more than half of rent received. This indicates that within 13 years property will get free of debt

and any rent received will be monthly income for the couple (Skevas, Wu and Guan, 2018).

4 £44,754 £3,328 £41,427 0.683013455 £28,295.10

5 £49,180 £3,660 £45,520 0.620921323 £28,264.11

6 £54,136 £4,026 £50,110 0.56447393 £28,285.90

7 £59,688 £4,429 £55,259 0.513158118 £28,356.58

8 £65,905 £4,872 £61,034 0.46650738 £28,472.62

9 £72,869 £5,359 £67,510 0.424097618 £28,630.86

10 £80,668 £5,895 £74,773 0.385543289 £28,828.40

Net present value £281,220.25

The result shows that if couple stays in rented property then it would save money after 10 years

with present value will be £281,220 approx.

Recommendation

Based on financial analysis; it is advised for client to rent the property in Central London itself;

as through this decision they can save huge money. Both couple only wants to stay for 5 years;

hence, for short term decision rented property is best option (Zhai and Wang, 2016).

Considering non-financial factors and long term decision; it is advised to purchase new

property and give it on rent after 5 years. This option is suitable for long term; as the rent

received from this property which is £2,800 higher than monthly repayment £1,300 which is

more than half of rent received. This indicates that within 13 years property will get free of debt

and any rent received will be monthly income for the couple (Skevas, Wu and Guan, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Abor, J.Y., 2017. Evaluating Capital Investment Decisions: Capital Budgeting.

In Entrepreneurial Finance for MSMEs (pp. 293-320). Palgrave Macmillan, Cham.

Paquin, J.P., Gauthier, C. and Morin, P.P., 2016. The downside risk of project portfolios: The

impact of capital investment projects and the value of project efficiency and project risk

management programmes. International Journal of Project Management, 34(8), pp.1460-

1470.

Abernathy, J.L., Beyer, B., Downes, J.F. and Rapley, E.T., 2019. High-Quality Information

Technology and Capital Investment Decisions. Journal of Information Systems, pp.0000-

0000.

Imhanzenobe, J.O. and Adeyemi, S.B., 2020. Financial decisions and sustainable cash flows in

Nigerian manufacturing companies. International Journal of Management, Economics

and Social Sciences (IJMESS), 9(2), pp.90-112.

Hunjra, A.I., Bakari, H. and Batool, I., 2018. Application of Financial Decisions, their

Determinants, and Financial Performance: A Tabular Summary of Systematic Literature

Review. Empirical Economic Review, 1(2), pp.91-142.

Skevas, T., Wu, F. and Guan, Z., 2018. Farm Capital Investment and Deviations from the

Optimal Path. Journal of Agricultural Economics, 69(2), pp.561-577.

Zhai, J. and Wang, Y., 2016. Accounting information quality, governance efficiency and capital

investment choice. China Journal of Accounting Research, 9(4), pp.251-266.

Museloo, K.A. and Abartavi, S., 2017. Incorrect pricing impact on investment and the capital

structure of companies with financial constraints. International Journal of Economics

and Financial Issues, 7(2), p.319.

Right move, 2020; Available online through:

https://www.rightmove.co.uk/property-for-sale/Barking-And-Dagenham.html

London house prices, 2020; Available online through: https://www.theweek.co.uk/london-house-

prices#:~:text=House%20prices%20in%20London%20will%20rise%201.5%25%20in

%202022%20and,postcodes%2C%20but%20activity%20is%20returning.

Abor, J.Y., 2017. Evaluating Capital Investment Decisions: Capital Budgeting.

In Entrepreneurial Finance for MSMEs (pp. 293-320). Palgrave Macmillan, Cham.

Paquin, J.P., Gauthier, C. and Morin, P.P., 2016. The downside risk of project portfolios: The

impact of capital investment projects and the value of project efficiency and project risk

management programmes. International Journal of Project Management, 34(8), pp.1460-

1470.

Abernathy, J.L., Beyer, B., Downes, J.F. and Rapley, E.T., 2019. High-Quality Information

Technology and Capital Investment Decisions. Journal of Information Systems, pp.0000-

0000.

Imhanzenobe, J.O. and Adeyemi, S.B., 2020. Financial decisions and sustainable cash flows in

Nigerian manufacturing companies. International Journal of Management, Economics

and Social Sciences (IJMESS), 9(2), pp.90-112.

Hunjra, A.I., Bakari, H. and Batool, I., 2018. Application of Financial Decisions, their

Determinants, and Financial Performance: A Tabular Summary of Systematic Literature

Review. Empirical Economic Review, 1(2), pp.91-142.

Skevas, T., Wu, F. and Guan, Z., 2018. Farm Capital Investment and Deviations from the

Optimal Path. Journal of Agricultural Economics, 69(2), pp.561-577.

Zhai, J. and Wang, Y., 2016. Accounting information quality, governance efficiency and capital

investment choice. China Journal of Accounting Research, 9(4), pp.251-266.

Museloo, K.A. and Abartavi, S., 2017. Incorrect pricing impact on investment and the capital

structure of companies with financial constraints. International Journal of Economics

and Financial Issues, 7(2), p.319.

Right move, 2020; Available online through:

https://www.rightmove.co.uk/property-for-sale/Barking-And-Dagenham.html

London house prices, 2020; Available online through: https://www.theweek.co.uk/london-house-

prices#:~:text=House%20prices%20in%20London%20will%20rise%201.5%25%20in

%202022%20and,postcodes%2C%20but%20activity%20is%20returning.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.