Advanced Financial Accounting: Analysis of UK Pub Companies' Finances

VerifiedAdded on 2021/09/09

|12

|2799

|65

Report

AI Summary

This report provides a financial analysis of Greene King plc and Young & Co.'s Brewery PLC, both listed on the London Stock Exchange, focusing on their performance in 2018. The analysis includes an in-depth examination of liquidity, debt management, efficiency, and profitability ratios, comparing data from 2017 and 2018 to assess financial trends. The report highlights the companies' strengths and weaknesses based on the ratio analysis, discussing factors that have affected their performance, such as market position, management changes, and compliance with regulations. The report also includes a discussion of the performance factors for each company, including revenue streams, acquisitions, and operational strategies. The report concludes by offering insights into the financial health and performance of each company, drawing conclusions based on the analysis of financial statements and key ratios. The report also acknowledges the limitations of the analysis and the importance of considering non-financial factors that influence the company's performance.

Advanced Financial

Accounting

Assignment

Accounting

Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Introduction.................................................................................................................................................3

Discussion and Analysis...............................................................................................................................4

Performance Factors...................................................................................................................................9

References.................................................................................................................................................10

2 | P a g e

Contents

Introduction.................................................................................................................................................3

Discussion and Analysis...............................................................................................................................4

Performance Factors...................................................................................................................................9

References.................................................................................................................................................10

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Introduction

A report has been prepared on the financial analysis of the two companies listed on the London stock

exchange. The report highlights as to how the annual report of the companies meets the expectations of

the corporate stakeholders (Boccia & Leonardi, 2016). The year of analysis chosen in the report is 2018.

An in-depth ratio analysis has been done using 10 critical and significant ratios of the company, which

shows the financial status, and performance of the company from the viewpoints of various parties like

those of management, investors and lenders. A year-to-year comparison also helps in knowing if the

company has progressed or declined in terms of progress. The last section of the report discusses the

financial and non-financial factors that have affected the performance of the companies. The limitation

of the report is that it covers the financial and non-financial analysis of the company from the

perspective of the annual report, it does not focuses on many other areas of interest like those of

internal control, processes, market stability, etc. (Choy, 2018).

The two companies, which has been considered for analysis is Greene King plc and Young & Co's

Brewery PLC. Green King PLC is one of the largest pub retailer and brewer in United Kingdom. It is based

out of Bury St Edmunds, Suffolk, England and the company owns a number of hotels, pubs and

restaurants with the total number over 3100. It is listed on London Stock Exchange and is a major

constituent of FTSE 250 Index. It was formed back in 1799 and grown multiple times by the way of

mergers and acquisitions. It runs various apprentice and hospitality programme in order to address the

skill and the experience gap of those who are unemployed and has more than 9000 registrations until

date (Alexander, 2016). Some of the programmes are Greene King Apprenticeship Programme and Get

into Hospitality Programme. On the other hand, Young & Co.'s Brewery Plc is another pub chain

company again operating in United Kingdom with 220 pubs. It was established in 1831 and in the

company 40% stake is being held by Young & Co and Charles Wells own 60% stake. This company again

has had a number of major acquisitions, which puts it third on the list of premium ale brewery in the UK

(Chron, 2017).

3 | P a g e

Introduction

A report has been prepared on the financial analysis of the two companies listed on the London stock

exchange. The report highlights as to how the annual report of the companies meets the expectations of

the corporate stakeholders (Boccia & Leonardi, 2016). The year of analysis chosen in the report is 2018.

An in-depth ratio analysis has been done using 10 critical and significant ratios of the company, which

shows the financial status, and performance of the company from the viewpoints of various parties like

those of management, investors and lenders. A year-to-year comparison also helps in knowing if the

company has progressed or declined in terms of progress. The last section of the report discusses the

financial and non-financial factors that have affected the performance of the companies. The limitation

of the report is that it covers the financial and non-financial analysis of the company from the

perspective of the annual report, it does not focuses on many other areas of interest like those of

internal control, processes, market stability, etc. (Choy, 2018).

The two companies, which has been considered for analysis is Greene King plc and Young & Co's

Brewery PLC. Green King PLC is one of the largest pub retailer and brewer in United Kingdom. It is based

out of Bury St Edmunds, Suffolk, England and the company owns a number of hotels, pubs and

restaurants with the total number over 3100. It is listed on London Stock Exchange and is a major

constituent of FTSE 250 Index. It was formed back in 1799 and grown multiple times by the way of

mergers and acquisitions. It runs various apprentice and hospitality programme in order to address the

skill and the experience gap of those who are unemployed and has more than 9000 registrations until

date (Alexander, 2016). Some of the programmes are Greene King Apprenticeship Programme and Get

into Hospitality Programme. On the other hand, Young & Co.'s Brewery Plc is another pub chain

company again operating in United Kingdom with 220 pubs. It was established in 1831 and in the

company 40% stake is being held by Young & Co and Charles Wells own 60% stake. This company again

has had a number of major acquisitions, which puts it third on the list of premium ale brewery in the UK

(Chron, 2017).

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

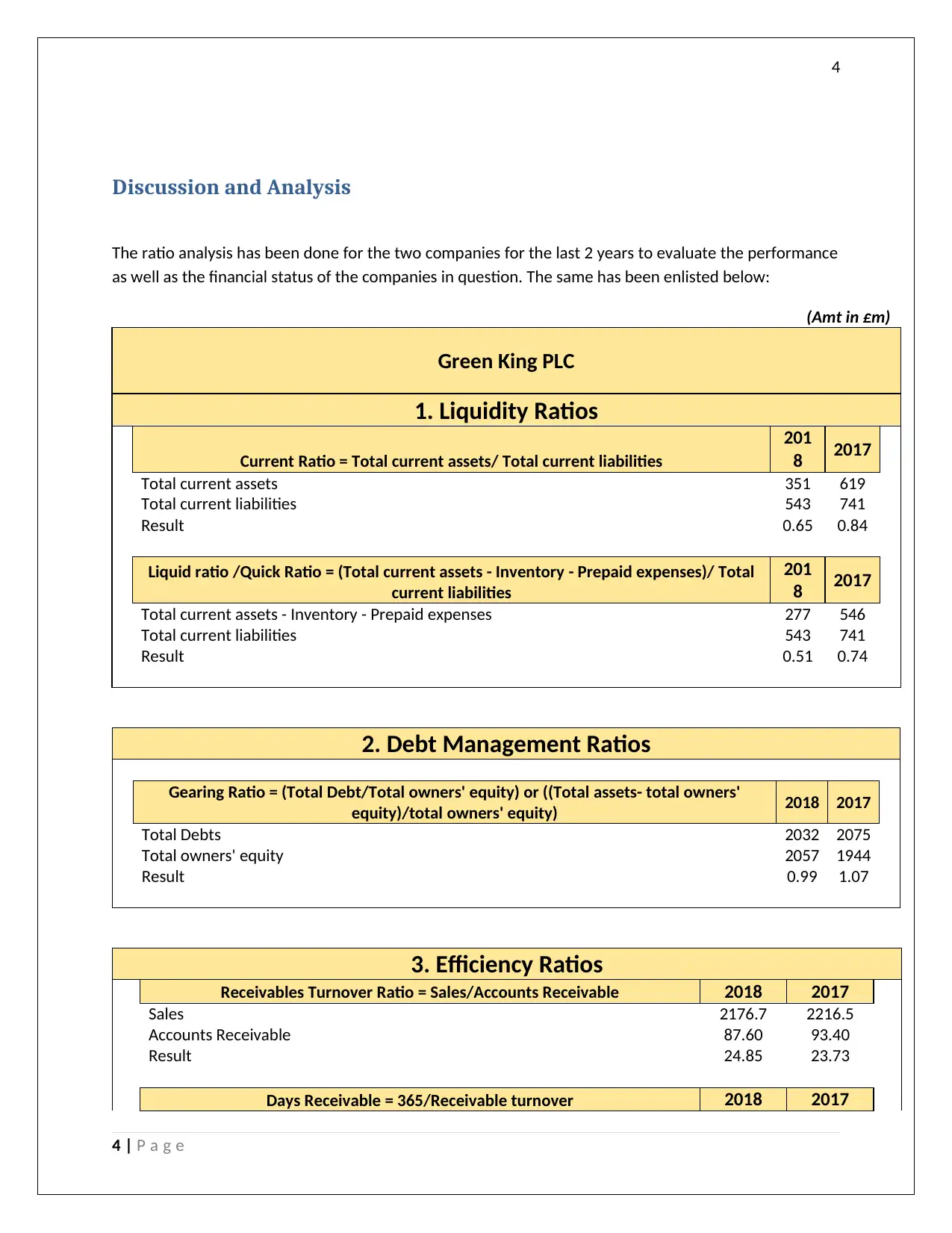

Discussion and Analysis

The ratio analysis has been done for the two companies for the last 2 years to evaluate the performance

as well as the financial status of the companies in question. The same has been enlisted below:

(Amt in £m)

Green King PLC

1. Liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities

201

8 2017

Total current assets 351 619

Total current liabilities 543 741

Result 0.65 0.84

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid expenses)/ Total

current liabilities

201

8 2017

Total current assets - Inventory - Prepaid expenses 277 546

Total current liabilities 543 741

Result 0.51 0.74

2. Debt Management Ratios

Gearing Ratio = (Total Debt/Total owners' equity) or ((Total assets- total owners'

equity)/total owners' equity) 2018 2017

Total Debts 2032 2075

Total owners' equity 2057 1944

Result 0.99 1.07

3. Efficiency Ratios

Receivables Turnover Ratio = Sales/Accounts Receivable 2018 2017

Sales 2176.7 2216.5

Accounts Receivable 87.60 93.40

Result 24.85 23.73

Days Receivable = 365/Receivable turnover 2018 2017

4 | P a g e

Discussion and Analysis

The ratio analysis has been done for the two companies for the last 2 years to evaluate the performance

as well as the financial status of the companies in question. The same has been enlisted below:

(Amt in £m)

Green King PLC

1. Liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities

201

8 2017

Total current assets 351 619

Total current liabilities 543 741

Result 0.65 0.84

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid expenses)/ Total

current liabilities

201

8 2017

Total current assets - Inventory - Prepaid expenses 277 546

Total current liabilities 543 741

Result 0.51 0.74

2. Debt Management Ratios

Gearing Ratio = (Total Debt/Total owners' equity) or ((Total assets- total owners'

equity)/total owners' equity) 2018 2017

Total Debts 2032 2075

Total owners' equity 2057 1944

Result 0.99 1.07

3. Efficiency Ratios

Receivables Turnover Ratio = Sales/Accounts Receivable 2018 2017

Sales 2176.7 2216.5

Accounts Receivable 87.60 93.40

Result 24.85 23.73

Days Receivable = 365/Receivable turnover 2018 2017

4 | P a g e

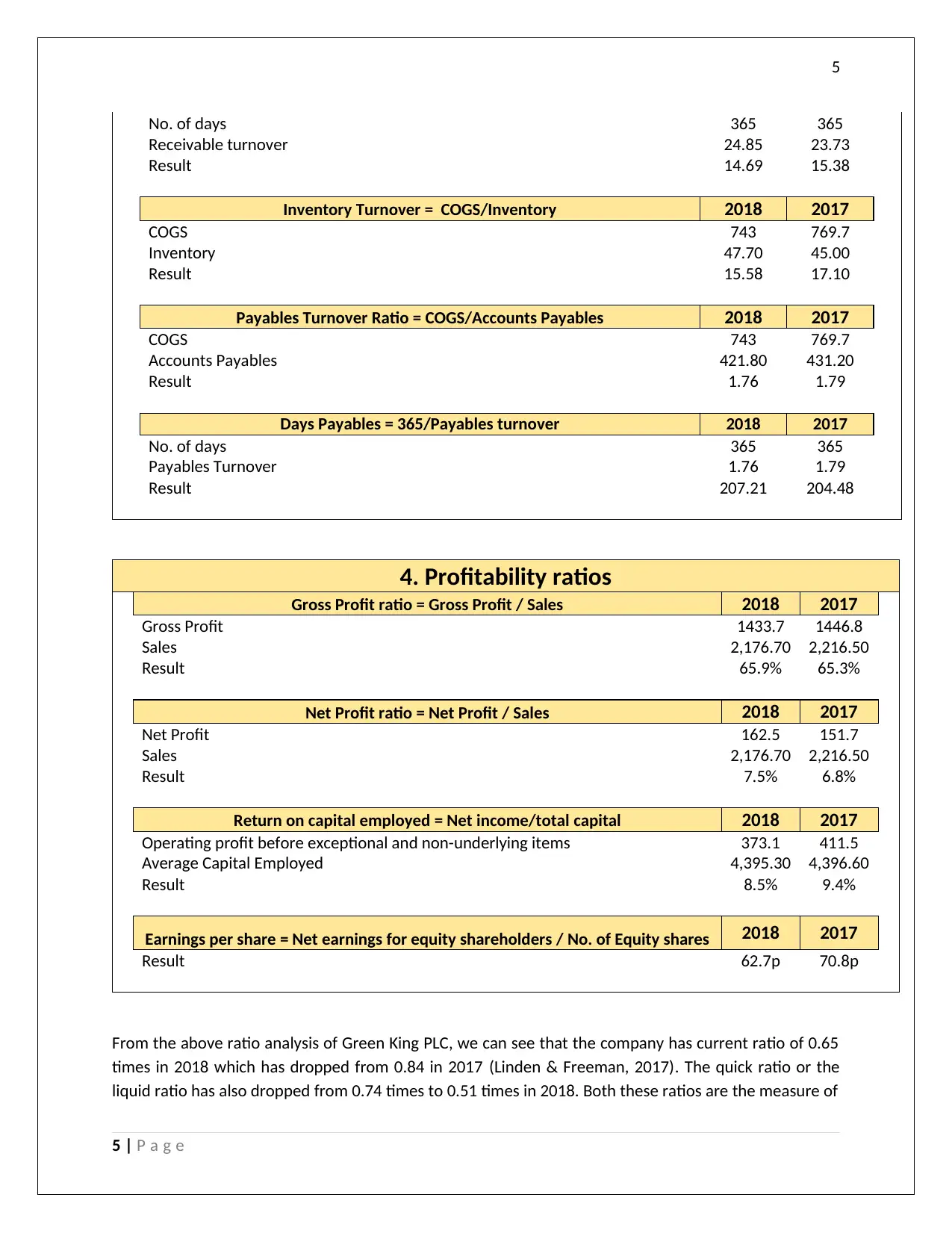

5

No. of days 365 365

Receivable turnover 24.85 23.73

Result 14.69 15.38

Inventory Turnover = COGS/Inventory 2018 2017

COGS 743 769.7

Inventory 47.70 45.00

Result 15.58 17.10

Payables Turnover Ratio = COGS/Accounts Payables 2018 2017

COGS 743 769.7

Accounts Payables 421.80 431.20

Result 1.76 1.79

Days Payables = 365/Payables turnover 2018 2017

No. of days 365 365

Payables Turnover 1.76 1.79

Result 207.21 204.48

4. Profitability ratios

Gross Profit ratio = Gross Profit / Sales 2018 2017

Gross Profit 1433.7 1446.8

Sales 2,176.70 2,216.50

Result 65.9% 65.3%

Net Profit ratio = Net Profit / Sales 2018 2017

Net Profit 162.5 151.7

Sales 2,176.70 2,216.50

Result 7.5% 6.8%

Return on capital employed = Net income/total capital 2018 2017

Operating profit before exceptional and non-underlying items 373.1 411.5

Average Capital Employed 4,395.30 4,396.60

Result 8.5% 9.4%

Earnings per share = Net earnings for equity shareholders / No. of Equity shares 2018 2017

Result 62.7p 70.8p

From the above ratio analysis of Green King PLC, we can see that the company has current ratio of 0.65

times in 2018 which has dropped from 0.84 in 2017 (Linden & Freeman, 2017). The quick ratio or the

liquid ratio has also dropped from 0.74 times to 0.51 times in 2018. Both these ratios are the measure of

5 | P a g e

No. of days 365 365

Receivable turnover 24.85 23.73

Result 14.69 15.38

Inventory Turnover = COGS/Inventory 2018 2017

COGS 743 769.7

Inventory 47.70 45.00

Result 15.58 17.10

Payables Turnover Ratio = COGS/Accounts Payables 2018 2017

COGS 743 769.7

Accounts Payables 421.80 431.20

Result 1.76 1.79

Days Payables = 365/Payables turnover 2018 2017

No. of days 365 365

Payables Turnover 1.76 1.79

Result 207.21 204.48

4. Profitability ratios

Gross Profit ratio = Gross Profit / Sales 2018 2017

Gross Profit 1433.7 1446.8

Sales 2,176.70 2,216.50

Result 65.9% 65.3%

Net Profit ratio = Net Profit / Sales 2018 2017

Net Profit 162.5 151.7

Sales 2,176.70 2,216.50

Result 7.5% 6.8%

Return on capital employed = Net income/total capital 2018 2017

Operating profit before exceptional and non-underlying items 373.1 411.5

Average Capital Employed 4,395.30 4,396.60

Result 8.5% 9.4%

Earnings per share = Net earnings for equity shareholders / No. of Equity shares 2018 2017

Result 62.7p 70.8p

From the above ratio analysis of Green King PLC, we can see that the company has current ratio of 0.65

times in 2018 which has dropped from 0.84 in 2017 (Linden & Freeman, 2017). The quick ratio or the

liquid ratio has also dropped from 0.74 times to 0.51 times in 2018. Both these ratios are the measure of

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

the company’s capability to pay off the short term debts and current liabilities on short notice and the

ideal ratio as per industry trend is 2 times and 1 times respectively (Goldmann, 2016). However, in the

given case, the same is exceptionally low and therefore it shows the inability of the company to pay off

the current debts and trade creditors on time. Therefore, the company needs to improve on the same.

For Young & Co's Brewery PLC, the situation is even worse as the current ratio and the liquid ratio is 0.38

times (2017: 0.24) and 0.332 times (2017: 0.20) respectively in 2018. Thus, in case of need, the company

may be required to erode or liquidate its fixed assets in order to pay off these liabilities.

In terms of the debt management ratios, the gearing ratio stands at 0.99 times and 1.07 times for 2018

and 2017 respectively for Green King PLC and for Young & Co's Brewery PLC, it has been 0.26 and 0.23

respectively for 2018 and 2017 (Trieu, 2017). The ratio shows the proportion of debt and equity in the

entire capital, the ideal industry trend being 2:1 times in favour of debt. For both the companies, it can

be said to be under control but the situation of Young & Co's Brewery PLC is better than Green King PLC

as the former has the cushion of using more of debt capital in future and reducing weighted average the

cost of capital.

In terms of the efficiency ratios, we can see that for Green King Plc, the receivable days has reduced

from 15.38 to 14.69 days, which is a positive indicator and reflects that the efficiency of collection has

increased (Heminway, 2017). However, the inventory turnover has decreased from 17.10 times to 15.58

times which indicates that the company is not being able to convert the inventory to sales readily and

thereby incurring the inventory carrying costs. Similarly, though the payable days has increased from

204.48 to 207.21 days and has had a positive impact on the cash cycle but such a higher payable days is

not recommended. This shows deficiency in the internal control. On the other hand, for Young & Co's

Brewery PLC, the receivable days has decreased marginally from 9.77 to 9.15 days. Similarly the

payables days has also decreased from 201.64 to 173.78 days indicating the efficiency of operations and

good internal control. The inventory turnover has declined marginally from 22.82 times to 21.63 times,

indicating a larger holding time and more carrying cost for the company but comparatively Young and

Co. has been better off than the Green King PLC (Jefferson, 2017).

Lastly, in case the profitability ratios are being compared, we can see that the gross profit ratio for

Green King Plc has been more or less constant whereas the net profit ratio has increased from 6.8% to

7.5% in 2018. The return on capital employed which measures the rate of return on the invested capital

has declined from 9.4% to 8.5% (Lessambo, 2018). The capital employed includes both the loan as well

as the own capital. The earnings per share has also declined from 70.8p in 2017 to 62.7p in 2017. On the

other hand, the net profit as well as the gross profit has been on higher side for Young & Co at 10.8%

and 76.8% respectively. The return on capital employed has declined from 6.1% to 5.4% in 2018 and the

earnings per share has been more or less constant at 61.5p for both the years. The profitability ratios do

indicate that the performance for both the companies has declined in 2018 but the profitability is better

for Young and Co whereas the return on capital is better for Green King PLC (Marques, 2018).

6 | P a g e

the company’s capability to pay off the short term debts and current liabilities on short notice and the

ideal ratio as per industry trend is 2 times and 1 times respectively (Goldmann, 2016). However, in the

given case, the same is exceptionally low and therefore it shows the inability of the company to pay off

the current debts and trade creditors on time. Therefore, the company needs to improve on the same.

For Young & Co's Brewery PLC, the situation is even worse as the current ratio and the liquid ratio is 0.38

times (2017: 0.24) and 0.332 times (2017: 0.20) respectively in 2018. Thus, in case of need, the company

may be required to erode or liquidate its fixed assets in order to pay off these liabilities.

In terms of the debt management ratios, the gearing ratio stands at 0.99 times and 1.07 times for 2018

and 2017 respectively for Green King PLC and for Young & Co's Brewery PLC, it has been 0.26 and 0.23

respectively for 2018 and 2017 (Trieu, 2017). The ratio shows the proportion of debt and equity in the

entire capital, the ideal industry trend being 2:1 times in favour of debt. For both the companies, it can

be said to be under control but the situation of Young & Co's Brewery PLC is better than Green King PLC

as the former has the cushion of using more of debt capital in future and reducing weighted average the

cost of capital.

In terms of the efficiency ratios, we can see that for Green King Plc, the receivable days has reduced

from 15.38 to 14.69 days, which is a positive indicator and reflects that the efficiency of collection has

increased (Heminway, 2017). However, the inventory turnover has decreased from 17.10 times to 15.58

times which indicates that the company is not being able to convert the inventory to sales readily and

thereby incurring the inventory carrying costs. Similarly, though the payable days has increased from

204.48 to 207.21 days and has had a positive impact on the cash cycle but such a higher payable days is

not recommended. This shows deficiency in the internal control. On the other hand, for Young & Co's

Brewery PLC, the receivable days has decreased marginally from 9.77 to 9.15 days. Similarly the

payables days has also decreased from 201.64 to 173.78 days indicating the efficiency of operations and

good internal control. The inventory turnover has declined marginally from 22.82 times to 21.63 times,

indicating a larger holding time and more carrying cost for the company but comparatively Young and

Co. has been better off than the Green King PLC (Jefferson, 2017).

Lastly, in case the profitability ratios are being compared, we can see that the gross profit ratio for

Green King Plc has been more or less constant whereas the net profit ratio has increased from 6.8% to

7.5% in 2018. The return on capital employed which measures the rate of return on the invested capital

has declined from 9.4% to 8.5% (Lessambo, 2018). The capital employed includes both the loan as well

as the own capital. The earnings per share has also declined from 70.8p in 2017 to 62.7p in 2017. On the

other hand, the net profit as well as the gross profit has been on higher side for Young & Co at 10.8%

and 76.8% respectively. The return on capital employed has declined from 6.1% to 5.4% in 2018 and the

earnings per share has been more or less constant at 61.5p for both the years. The profitability ratios do

indicate that the performance for both the companies has declined in 2018 but the profitability is better

for Young and Co whereas the return on capital is better for Green King PLC (Marques, 2018).

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

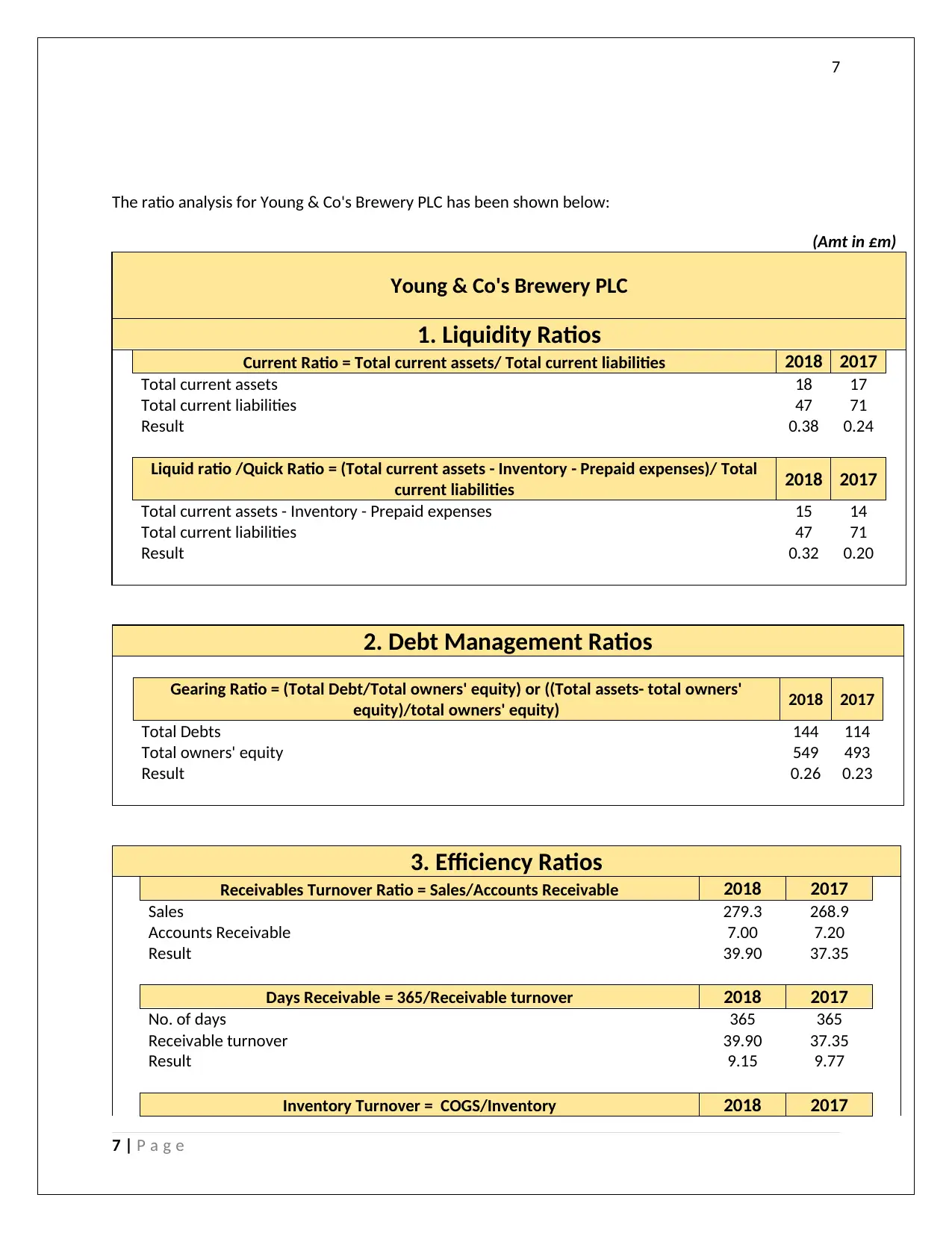

The ratio analysis for Young & Co's Brewery PLC has been shown below:

(Amt in £m)

Young & Co's Brewery PLC

1. Liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities 2018 2017

Total current assets 18 17

Total current liabilities 47 71

Result 0.38 0.24

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid expenses)/ Total

current liabilities 2018 2017

Total current assets - Inventory - Prepaid expenses 15 14

Total current liabilities 47 71

Result 0.32 0.20

2. Debt Management Ratios

Gearing Ratio = (Total Debt/Total owners' equity) or ((Total assets- total owners'

equity)/total owners' equity) 2018 2017

Total Debts 144 114

Total owners' equity 549 493

Result 0.26 0.23

3. Efficiency Ratios

Receivables Turnover Ratio = Sales/Accounts Receivable 2018 2017

Sales 279.3 268.9

Accounts Receivable 7.00 7.20

Result 39.90 37.35

Days Receivable = 365/Receivable turnover 2018 2017

No. of days 365 365

Receivable turnover 39.90 37.35

Result 9.15 9.77

Inventory Turnover = COGS/Inventory 2018 2017

7 | P a g e

The ratio analysis for Young & Co's Brewery PLC has been shown below:

(Amt in £m)

Young & Co's Brewery PLC

1. Liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities 2018 2017

Total current assets 18 17

Total current liabilities 47 71

Result 0.38 0.24

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid expenses)/ Total

current liabilities 2018 2017

Total current assets - Inventory - Prepaid expenses 15 14

Total current liabilities 47 71

Result 0.32 0.20

2. Debt Management Ratios

Gearing Ratio = (Total Debt/Total owners' equity) or ((Total assets- total owners'

equity)/total owners' equity) 2018 2017

Total Debts 144 114

Total owners' equity 549 493

Result 0.26 0.23

3. Efficiency Ratios

Receivables Turnover Ratio = Sales/Accounts Receivable 2018 2017

Sales 279.3 268.9

Accounts Receivable 7.00 7.20

Result 39.90 37.35

Days Receivable = 365/Receivable turnover 2018 2017

No. of days 365 365

Receivable turnover 39.90 37.35

Result 9.15 9.77

Inventory Turnover = COGS/Inventory 2018 2017

7 | P a g e

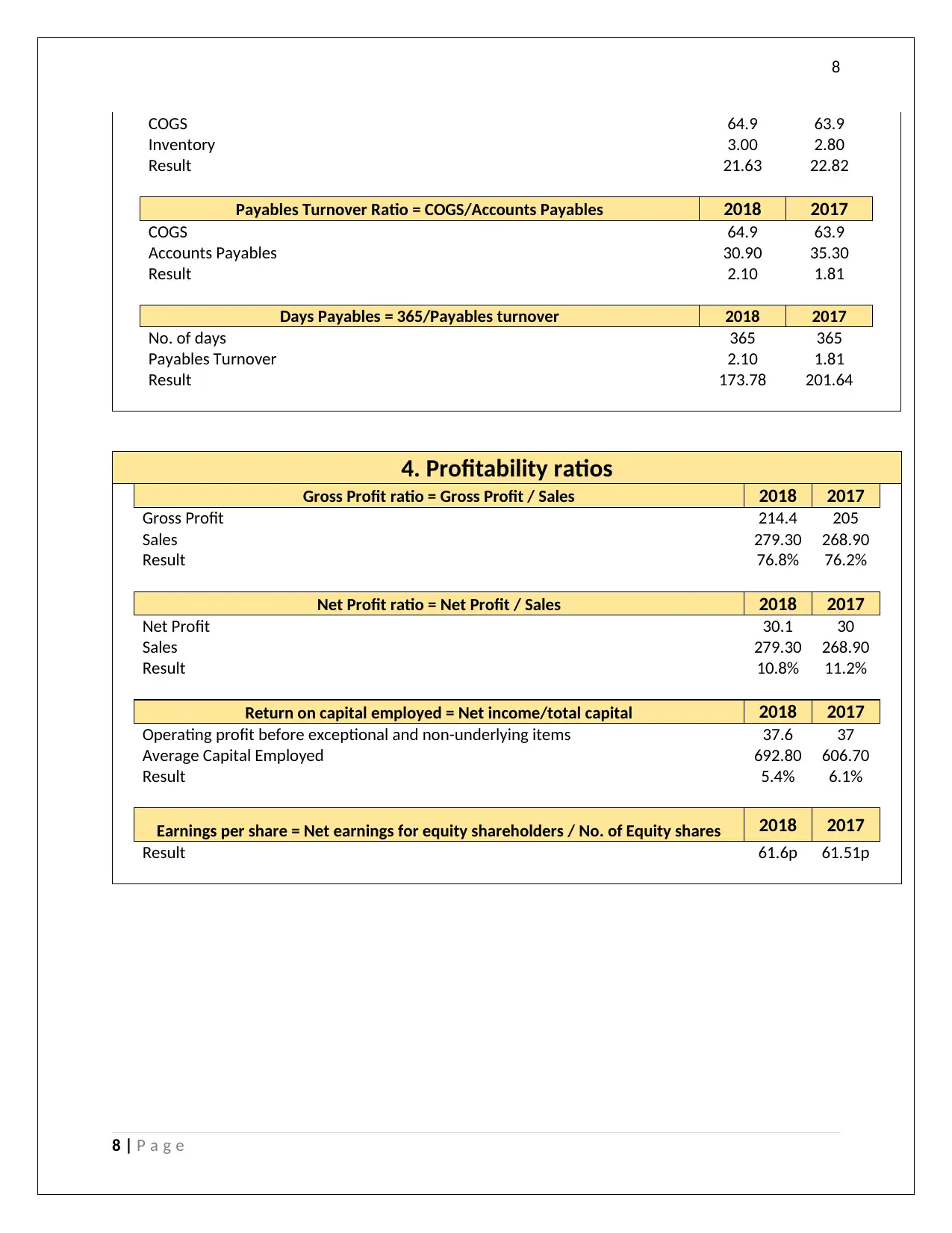

8

COGS 64.9 63.9

Inventory 3.00 2.80

Result 21.63 22.82

Payables Turnover Ratio = COGS/Accounts Payables 2018 2017

COGS 64.9 63.9

Accounts Payables 30.90 35.30

Result 2.10 1.81

Days Payables = 365/Payables turnover 2018 2017

No. of days 365 365

Payables Turnover 2.10 1.81

Result 173.78 201.64

4. Profitability ratios

Gross Profit ratio = Gross Profit / Sales 2018 2017

Gross Profit 214.4 205

Sales 279.30 268.90

Result 76.8% 76.2%

Net Profit ratio = Net Profit / Sales 2018 2017

Net Profit 30.1 30

Sales 279.30 268.90

Result 10.8% 11.2%

Return on capital employed = Net income/total capital 2018 2017

Operating profit before exceptional and non-underlying items 37.6 37

Average Capital Employed 692.80 606.70

Result 5.4% 6.1%

Earnings per share = Net earnings for equity shareholders / No. of Equity shares 2018 2017

Result 61.6p 61.51p

8 | P a g e

COGS 64.9 63.9

Inventory 3.00 2.80

Result 21.63 22.82

Payables Turnover Ratio = COGS/Accounts Payables 2018 2017

COGS 64.9 63.9

Accounts Payables 30.90 35.30

Result 2.10 1.81

Days Payables = 365/Payables turnover 2018 2017

No. of days 365 365

Payables Turnover 2.10 1.81

Result 173.78 201.64

4. Profitability ratios

Gross Profit ratio = Gross Profit / Sales 2018 2017

Gross Profit 214.4 205

Sales 279.30 268.90

Result 76.8% 76.2%

Net Profit ratio = Net Profit / Sales 2018 2017

Net Profit 30.1 30

Sales 279.30 268.90

Result 10.8% 11.2%

Return on capital employed = Net income/total capital 2018 2017

Operating profit before exceptional and non-underlying items 37.6 37

Average Capital Employed 692.80 606.70

Result 5.4% 6.1%

Earnings per share = Net earnings for equity shareholders / No. of Equity shares 2018 2017

Result 61.6p 61.51p

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Performance Factors

In case of the Young and Co., the company is divided into several segments as if Young’s managed

houses; Geronimo managed houses and Ram Pub Company. Revenue generally comes from food, drink

and accommodation whereas the Ram Pub Company generates revenue by leasing the pubs to third

parties. The company has had a major change in the management due to the merger and acquisition

over the past few years and off late the company has stabilized (Kew & Stredwick, 2017). Besides this, as

per the annual report, sustainability report and the audit report of the company, it can be mentioned

that the company has complied with all the rules and regulations, accounting standards and the legal

requirements while preparing the books of accounts. However, the company’s valuation policy,

computation of deferred tax and the supplier rebates and revenue recognition criteria were all

challenged and it was seen that the company has adequate back up of the same (Kachelmeier, et al.,

2018). In addition, the company has been contributing to the corporate governance and has made

adequate disclosures in this regard.

On the other hand, Green King PLC has been the market leader off late in UK because of the synergies in

investment and acquisitions. The focus of the company has been on cost mitigation programmes and

strengthen the capital structure, improve the underlying sales (Sithole, et al., 2017). The company has

also been compliant in terms of corporate governance and sustainability and has come up with various

programmes and incentives for the betterment of the company as well its human resource. In terms of

auditor opinion in audit report, the company has complied and followed all the rules, regulations,

accounting standards and the legal requirements as therefore the auditors have issued a clear opinion

and mentioned the entity as going concern (Raiborn, et al., 2016). The auditor did identify few of the

risks in the financial statements like those of capital expenditure accounting, impairment calculations of

property, plant and equipment, revenue recognition, etc. bit post the additional audit procedures by the

auditors, all these were found to be justifiable.

9 | P a g e

Performance Factors

In case of the Young and Co., the company is divided into several segments as if Young’s managed

houses; Geronimo managed houses and Ram Pub Company. Revenue generally comes from food, drink

and accommodation whereas the Ram Pub Company generates revenue by leasing the pubs to third

parties. The company has had a major change in the management due to the merger and acquisition

over the past few years and off late the company has stabilized (Kew & Stredwick, 2017). Besides this, as

per the annual report, sustainability report and the audit report of the company, it can be mentioned

that the company has complied with all the rules and regulations, accounting standards and the legal

requirements while preparing the books of accounts. However, the company’s valuation policy,

computation of deferred tax and the supplier rebates and revenue recognition criteria were all

challenged and it was seen that the company has adequate back up of the same (Kachelmeier, et al.,

2018). In addition, the company has been contributing to the corporate governance and has made

adequate disclosures in this regard.

On the other hand, Green King PLC has been the market leader off late in UK because of the synergies in

investment and acquisitions. The focus of the company has been on cost mitigation programmes and

strengthen the capital structure, improve the underlying sales (Sithole, et al., 2017). The company has

also been compliant in terms of corporate governance and sustainability and has come up with various

programmes and incentives for the betterment of the company as well its human resource. In terms of

auditor opinion in audit report, the company has complied and followed all the rules, regulations,

accounting standards and the legal requirements as therefore the auditors have issued a clear opinion

and mentioned the entity as going concern (Raiborn, et al., 2016). The auditor did identify few of the

risks in the financial statements like those of capital expenditure accounting, impairment calculations of

property, plant and equipment, revenue recognition, etc. bit post the additional audit procedures by the

auditors, all these were found to be justifiable.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Boccia, F. & Leonardi, R., 2016. The Challenge of the Digital Economy. Markets, Taxation and

Appropriate Economic Models, pp. 1-16.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Chron, 2017. five-common-features-internal-control-system-business. [Online]

Available at: http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kachelmeier, S., Schmidt, J. & Valentine, K., 2018. The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), pp. 1-39.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. second ed.

London: Chartered Institute of Personnel and Development.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

10 | P a g e

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Boccia, F. & Leonardi, R., 2016. The Challenge of the Digital Economy. Markets, Taxation and

Appropriate Economic Models, pp. 1-16.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview Analysis.

Ecological Economics, p. 145.

Chron, 2017. five-common-features-internal-control-system-business. [Online]

Available at: http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kachelmeier, S., Schmidt, J. & Valentine, K., 2018. The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), pp. 1-39.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. second ed.

London: Chartered Institute of Personnel and Development.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

10 | P a g e

11

Marques, R. P. F., 2018. Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, pp. 820-830.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), pp. 111-124.

11 | P a g e

Marques, R. P. F., 2018. Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, pp. 820-830.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Sithole, S., Chandler, P., Abeysekera, I. & Paas, F., 2017. Benefits of guided self-management of attention

on learning accounting. Journal of Educational Psychology, 109(2), p. 220.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), pp. 111-124.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.