Financial Ratio Analysis of PUMA and ADIDAS: A Comparative Study

VerifiedAdded on 2021/06/08

|24

|5291

|140

Report

AI Summary

This report provides a detailed financial analysis of the sportswear companies PUMA and ADIDAS, comparing their performance through various financial ratios. The analysis covers liquidity ratios (current ratio, quick ratio), asset management ratios (inventory turnover, days sales outstanding, fixed assets turnover, total assets turnover), and debt management ratios (total debt to capital, time interest earned). The report examines the companies' financial positions in 2019 and 2020, offering insights into their asset and liability management, capital structure, and overall financial health. The study aims to inform about the sportswear market and its characteristics, understanding how these corporations manage their assets, liabilities, capital, and investments by working on their financial reports. The comparison highlights differences in their financial strategies and the impact of globalization on the sports footwear industry, providing a comprehensive overview of their financial strengths and weaknesses.

SNHU 19E1

FINANCIAL ANALYSIS PAPER

PUMA and ADIDAS

PHẠM KHÁNH LINH – NGUYỄN PHƯƠNG ANH – NGUYỄN THỊ NGỌC LIÊN – TRẦN THỊ HỢP

3/5/2021

[This document is used for Fundamental of Finance Assignment]

FINANCIAL ANALYSIS PAPER

PUMA and ADIDAS

PHẠM KHÁNH LINH – NGUYỄN PHƯƠNG ANH – NGUYỄN THỊ NGỌC LIÊN – TRẦN THỊ HỢP

3/5/2021

[This document is used for Fundamental of Finance Assignment]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 | P a g e

AN ANALYSIS OF PUMA AND ADIDAS

FINANCIAL RATIOS

Table of contents

A. Sportswear Industry

B. Financial Ratios

C. Stock Price

D. Conclusions

E. Appendix

AN ANALYSIS OF PUMA AND ADIDAS

FINANCIAL RATIOS

Table of contents

A. Sportswear Industry

B. Financial Ratios

C. Stock Price

D. Conclusions

E. Appendix

2 | P a g e

A. SPORTSWEAR INDUSTRY:

The European sportswear industry, one of the biggest blocs, comprises over 21,000 companies that

employ 278,000 employees, generating €27.5 billion in turnover annually. European Confederation of the

Footwear Industry (CEC) chairman Luis Onofre asserts, “The fact that nine European countries rank

among the top 15 world exporters is a clear indicator of the success of European footwear products at the

global level.”

The dynamics and buying preferences to a certain extent are singular and peculiar to each market block.

In Europe, the “quality” factor is almost a leitmotif, and personalized and differentiated footwear has been

in high-demand for quite some time now.

German footwear market is also inherited characteristics of its bloc.

The two major sportswear and sports footwear industries in Germany are Adidas and Puma. These two

were owned by brothers Adolf Dassler and Rudolf Dassler where after the relationship between the

brothers deteriorated they decided to part ways in business, Adolf went on to open Adidas while Rudolf

established Puma. These two companies compete with each other internationally and are the most vibrant

current trend setters in the industry in Germany.

Globalization, as in any other industry the world over, has definitely impacted the sports footwear

industry in Germany. Leading companies in the production of sports footwear have been forced to

relocate internationally to take advantage of key opportunities internationally.

Globalization helps a firm to spread political and economic risk whereby, joint ventures have become

widespread as a way of meeting the need to tap the international market, technological knowledge, design

and skills.

Some of the major competitors of Adidas and Puma such as Nike relocated to countries in Asia such as

Thailand and China exclusively because of low labor cost in these countries comparative to those of

firm’s country of origin.

This has translated to low operating costs for these firms hence they are able to lower the price of their

products comparative to that of its competitors which in turn has given such firms an extra edge over their

competitors in terms of pricing. This means that such companies will chip away at some of Germanys’

leading producers of sportswear market share.

A. SPORTSWEAR INDUSTRY:

The European sportswear industry, one of the biggest blocs, comprises over 21,000 companies that

employ 278,000 employees, generating €27.5 billion in turnover annually. European Confederation of the

Footwear Industry (CEC) chairman Luis Onofre asserts, “The fact that nine European countries rank

among the top 15 world exporters is a clear indicator of the success of European footwear products at the

global level.”

The dynamics and buying preferences to a certain extent are singular and peculiar to each market block.

In Europe, the “quality” factor is almost a leitmotif, and personalized and differentiated footwear has been

in high-demand for quite some time now.

German footwear market is also inherited characteristics of its bloc.

The two major sportswear and sports footwear industries in Germany are Adidas and Puma. These two

were owned by brothers Adolf Dassler and Rudolf Dassler where after the relationship between the

brothers deteriorated they decided to part ways in business, Adolf went on to open Adidas while Rudolf

established Puma. These two companies compete with each other internationally and are the most vibrant

current trend setters in the industry in Germany.

Globalization, as in any other industry the world over, has definitely impacted the sports footwear

industry in Germany. Leading companies in the production of sports footwear have been forced to

relocate internationally to take advantage of key opportunities internationally.

Globalization helps a firm to spread political and economic risk whereby, joint ventures have become

widespread as a way of meeting the need to tap the international market, technological knowledge, design

and skills.

Some of the major competitors of Adidas and Puma such as Nike relocated to countries in Asia such as

Thailand and China exclusively because of low labor cost in these countries comparative to those of

firm’s country of origin.

This has translated to low operating costs for these firms hence they are able to lower the price of their

products comparative to that of its competitors which in turn has given such firms an extra edge over their

competitors in terms of pricing. This means that such companies will chip away at some of Germanys’

leading producers of sportswear market share.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3 | P a g e

Entry barriers into the sportswear market are relatively few. This scenario has led many investors trying

their luck in the lucrative sports footwear industry.

Consequently, the market has become fragmented due to a lot of competitors entering the industry and as

result, the market share of leading producers of sports foot wears are gradually loosing their market to

their ever increasing competitors. In turn this has prompted leaders in the industry of sports foot wear to

shift their focus to acquisition of additional brands merging with other firms in an effort of consolidating

their position as leaders of this lucrative industry.

By taking a deep dive into PUMA and ADIDAS operating results, we expect to be informed about sport

wear market and its characteristics. We also expect to comprehend how these corporations manage their

assets, liabilities, capital, and how investments and financial activities are performed by working on their

financial reports.

As the two corporations have a close relation with each other, we decided to study them as a main subject

(PUMA) and a standpoint (ADIDAS) for comparison.

This report presents a financial analysis of the sportswear company PUMA by

comparing different financial ratios over time and with its competitor. It further

reviews PUMA’s position in the financial markets and evaluates returns in relation to

the level of risk associated from an investor perspective.

Entry barriers into the sportswear market are relatively few. This scenario has led many investors trying

their luck in the lucrative sports footwear industry.

Consequently, the market has become fragmented due to a lot of competitors entering the industry and as

result, the market share of leading producers of sports foot wears are gradually loosing their market to

their ever increasing competitors. In turn this has prompted leaders in the industry of sports foot wear to

shift their focus to acquisition of additional brands merging with other firms in an effort of consolidating

their position as leaders of this lucrative industry.

By taking a deep dive into PUMA and ADIDAS operating results, we expect to be informed about sport

wear market and its characteristics. We also expect to comprehend how these corporations manage their

assets, liabilities, capital, and how investments and financial activities are performed by working on their

financial reports.

As the two corporations have a close relation with each other, we decided to study them as a main subject

(PUMA) and a standpoint (ADIDAS) for comparison.

This report presents a financial analysis of the sportswear company PUMA by

comparing different financial ratios over time and with its competitor. It further

reviews PUMA’s position in the financial markets and evaluates returns in relation to

the level of risk associated from an investor perspective.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4 | P a g e

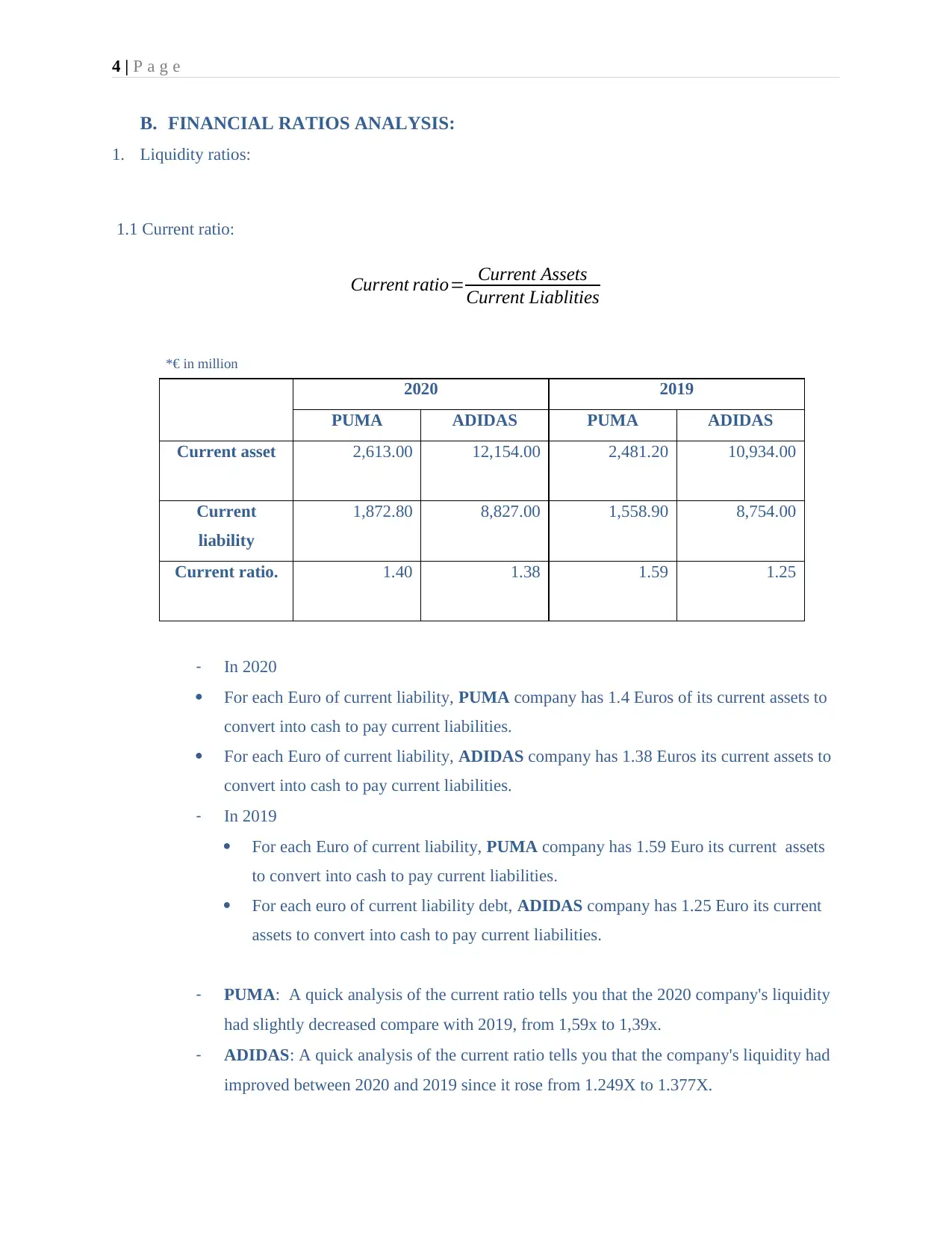

B. FINANCIAL RATIOS ANALYSIS:

1. Liquidity ratios:

1.1 Current ratio:

Current ratio= Current Assets

Current Liablities

2020 2019

PUMA ADIDAS PUMA ADIDAS

Current asset 2,613.00 12,154.00 2,481.20 10,934.00

Current

liability

1,872.80 8,827.00 1,558.90 8,754.00

Current ratio. 1.40 1.38 1.59 1.25

- In 2020

For each Euro of current liability, PUMA company has 1.4 Euros of its current assets to

convert into cash to pay current liabilities.

For each Euro of current liability, ADIDAS company has 1.38 Euros its current assets to

convert into cash to pay current liabilities.

- In 2019

For each Euro of current liability, PUMA company has 1.59 Euro its current assets

to convert into cash to pay current liabilities.

For each euro of current liability debt, ADIDAS company has 1.25 Euro its current

assets to convert into cash to pay current liabilities.

- PUMA: A quick analysis of the current ratio tells you that the 2020 company's liquidity

had slightly decreased compare with 2019, from 1,59x to 1,39x.

- ADIDAS: A quick analysis of the current ratio tells you that the company's liquidity had

improved between 2020 and 2019 since it rose from 1.249X to 1.377X.

*€ in million

B. FINANCIAL RATIOS ANALYSIS:

1. Liquidity ratios:

1.1 Current ratio:

Current ratio= Current Assets

Current Liablities

2020 2019

PUMA ADIDAS PUMA ADIDAS

Current asset 2,613.00 12,154.00 2,481.20 10,934.00

Current

liability

1,872.80 8,827.00 1,558.90 8,754.00

Current ratio. 1.40 1.38 1.59 1.25

- In 2020

For each Euro of current liability, PUMA company has 1.4 Euros of its current assets to

convert into cash to pay current liabilities.

For each Euro of current liability, ADIDAS company has 1.38 Euros its current assets to

convert into cash to pay current liabilities.

- In 2019

For each Euro of current liability, PUMA company has 1.59 Euro its current assets

to convert into cash to pay current liabilities.

For each euro of current liability debt, ADIDAS company has 1.25 Euro its current

assets to convert into cash to pay current liabilities.

- PUMA: A quick analysis of the current ratio tells you that the 2020 company's liquidity

had slightly decreased compare with 2019, from 1,59x to 1,39x.

- ADIDAS: A quick analysis of the current ratio tells you that the company's liquidity had

improved between 2020 and 2019 since it rose from 1.249X to 1.377X.

*€ in million

5 | P a g e

- Comparision : Puma’s current ratio (1,395x) is greater than Adidas’s current ratio

(1.377x) proves that Puma’s liquidity is better (2020) . This shows that Puma has

managed their liabilities and short-term assets more effectively (PUMA's current ratio

relative to ADIDAS's is almost equivalent in 2020.)

- With this competitive difference between their Current Ratios, investors will face a give-

and-take situation while creditors like to see high current ratio, shareholders commonly

okay with lower Current Ratio because that means probably not a surplus of unused

inventories and inefficiency in productivities. Therefore investors must carefully consider

where to fall in this particular ratio.

POSITION: Moderate

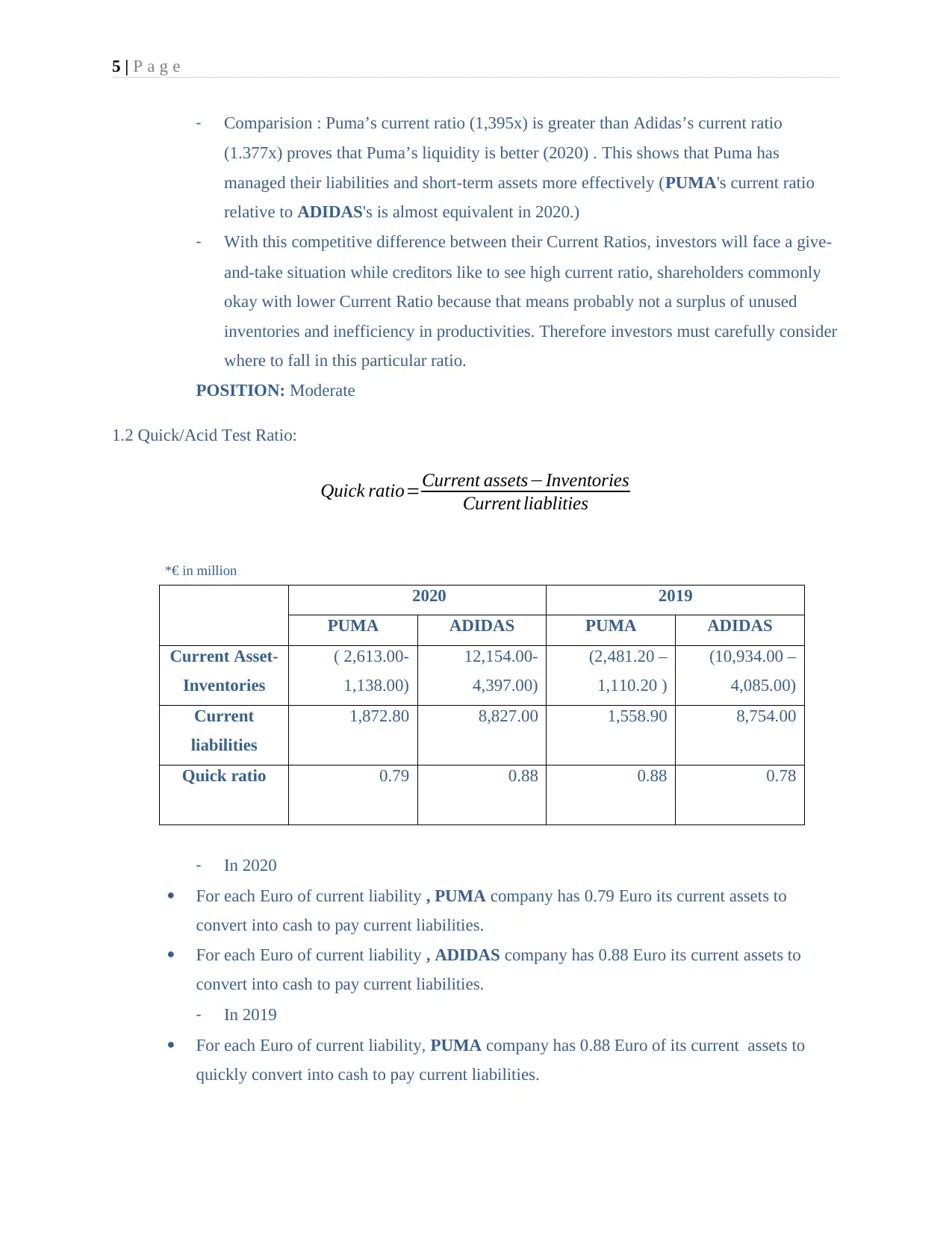

1.2 Quick/Acid Test Ratio:

Quick ratio=Current assets−Inventories

Current liablities

2020 2019

PUMA ADIDAS PUMA ADIDAS

Current Asset-

Inventories

( 2,613.00-

1,138.00)

12,154.00-

4,397.00)

(2,481.20 –

1,110.20 )

(10,934.00 –

4,085.00)

Current

liabilities

1,872.80 8,827.00 1,558.90 8,754.00

Quick ratio 0.79 0.88 0.88 0.78

- In 2020

For each Euro of current liability , PUMA company has 0.79 Euro its current assets to

convert into cash to pay current liabilities.

For each Euro of current liability , ADIDAS company has 0.88 Euro its current assets to

convert into cash to pay current liabilities.

- In 2019

For each Euro of current liability, PUMA company has 0.88 Euro of its current assets to

quickly convert into cash to pay current liabilities.

*€ in million

- Comparision : Puma’s current ratio (1,395x) is greater than Adidas’s current ratio

(1.377x) proves that Puma’s liquidity is better (2020) . This shows that Puma has

managed their liabilities and short-term assets more effectively (PUMA's current ratio

relative to ADIDAS's is almost equivalent in 2020.)

- With this competitive difference between their Current Ratios, investors will face a give-

and-take situation while creditors like to see high current ratio, shareholders commonly

okay with lower Current Ratio because that means probably not a surplus of unused

inventories and inefficiency in productivities. Therefore investors must carefully consider

where to fall in this particular ratio.

POSITION: Moderate

1.2 Quick/Acid Test Ratio:

Quick ratio=Current assets−Inventories

Current liablities

2020 2019

PUMA ADIDAS PUMA ADIDAS

Current Asset-

Inventories

( 2,613.00-

1,138.00)

12,154.00-

4,397.00)

(2,481.20 –

1,110.20 )

(10,934.00 –

4,085.00)

Current

liabilities

1,872.80 8,827.00 1,558.90 8,754.00

Quick ratio 0.79 0.88 0.88 0.78

- In 2020

For each Euro of current liability , PUMA company has 0.79 Euro its current assets to

convert into cash to pay current liabilities.

For each Euro of current liability , ADIDAS company has 0.88 Euro its current assets to

convert into cash to pay current liabilities.

- In 2019

For each Euro of current liability, PUMA company has 0.88 Euro of its current assets to

quickly convert into cash to pay current liabilities.

*€ in million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6 | P a g e

For each Euro of current liability, ADIDAS company has 0.78 Euro of its current assets to

quickly convert into cash to pay current liabilities.

- PUMA: A quick analysis of the current ratio will tell you that the company's quick

liquidity has gotten just a little bit worse between 2020 and 2019.

- ADIDAS: A quick analysis of the current ratio will tell you that the company's quick

liquidity has gotten just a little bit better between 2020 and 2019 since it rose from 0,78X

to 0,88X.

- Comparison: Puma’s quick ratio (0.79X) is lower than Adidas’s quick ratio (0.88X)

proves that Puma’s ability of paying off short-term debt is worse (2020).

- Both corporations have Quick ratio smaller than 1 which suggests they have trouble with

paying current liabilities. This could be unfavorable if the company couldn’t manage to

satisfy the debts, yet could be understandable if the company feel safe and choose to

invest their money in profitable projects.

- Fell below 1, their quick ratios could be a warning sign of troubles, therefore they should

adjust this ratio as soon as possible.

POSITION: weak

o Both PUMA and ADIDAS with a quick ratio less than 1 is unlikely to be

able to repay current liabilities and must be carefully considered

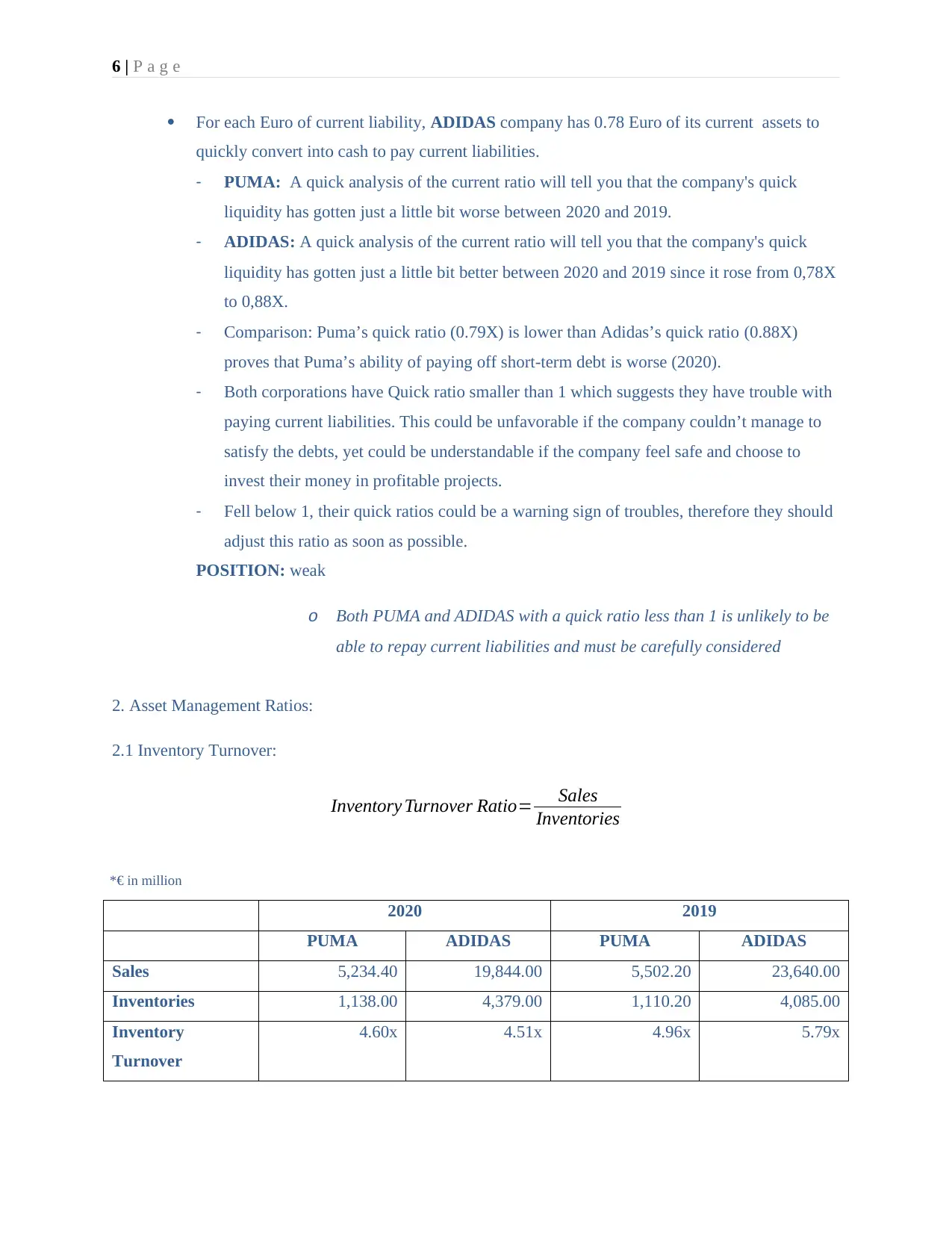

2. Asset Management Ratios:

2.1 Inventory Turnover:

Inventory Turnover Ratio= Sales

Inventories

2020 2019

PUMA ADIDAS PUMA ADIDAS

Sales 5,234.40 19,844.00 5,502.20 23,640.00

Inventories 1,138.00 4,379.00 1,110.20 4,085.00

Inventory

Turnover

4.60x 4.51x 4.96x 5.79x

*€ in million

For each Euro of current liability, ADIDAS company has 0.78 Euro of its current assets to

quickly convert into cash to pay current liabilities.

- PUMA: A quick analysis of the current ratio will tell you that the company's quick

liquidity has gotten just a little bit worse between 2020 and 2019.

- ADIDAS: A quick analysis of the current ratio will tell you that the company's quick

liquidity has gotten just a little bit better between 2020 and 2019 since it rose from 0,78X

to 0,88X.

- Comparison: Puma’s quick ratio (0.79X) is lower than Adidas’s quick ratio (0.88X)

proves that Puma’s ability of paying off short-term debt is worse (2020).

- Both corporations have Quick ratio smaller than 1 which suggests they have trouble with

paying current liabilities. This could be unfavorable if the company couldn’t manage to

satisfy the debts, yet could be understandable if the company feel safe and choose to

invest their money in profitable projects.

- Fell below 1, their quick ratios could be a warning sign of troubles, therefore they should

adjust this ratio as soon as possible.

POSITION: weak

o Both PUMA and ADIDAS with a quick ratio less than 1 is unlikely to be

able to repay current liabilities and must be carefully considered

2. Asset Management Ratios:

2.1 Inventory Turnover:

Inventory Turnover Ratio= Sales

Inventories

2020 2019

PUMA ADIDAS PUMA ADIDAS

Sales 5,234.40 19,844.00 5,502.20 23,640.00

Inventories 1,138.00 4,379.00 1,110.20 4,085.00

Inventory

Turnover

4.60x 4.51x 4.96x 5.79x

*€ in million

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7 | P a g e

PUMA’s 2020 Inventories turnover is relatively equal with its 2019, and is slightly higher than ADIDAS

for both 2020 and 2019. This ratio indicates that they had comparatively maintained the level of sales and

their inventories. But still, the low turnover suggests PUMA and ADIDAS have too much low value

inventories. They should improve this ratio by releasing new design, enhancing marketing activities if the

expense budget allow, or adjust their managing strategy to boost this ratio.

POSITION: Moderate

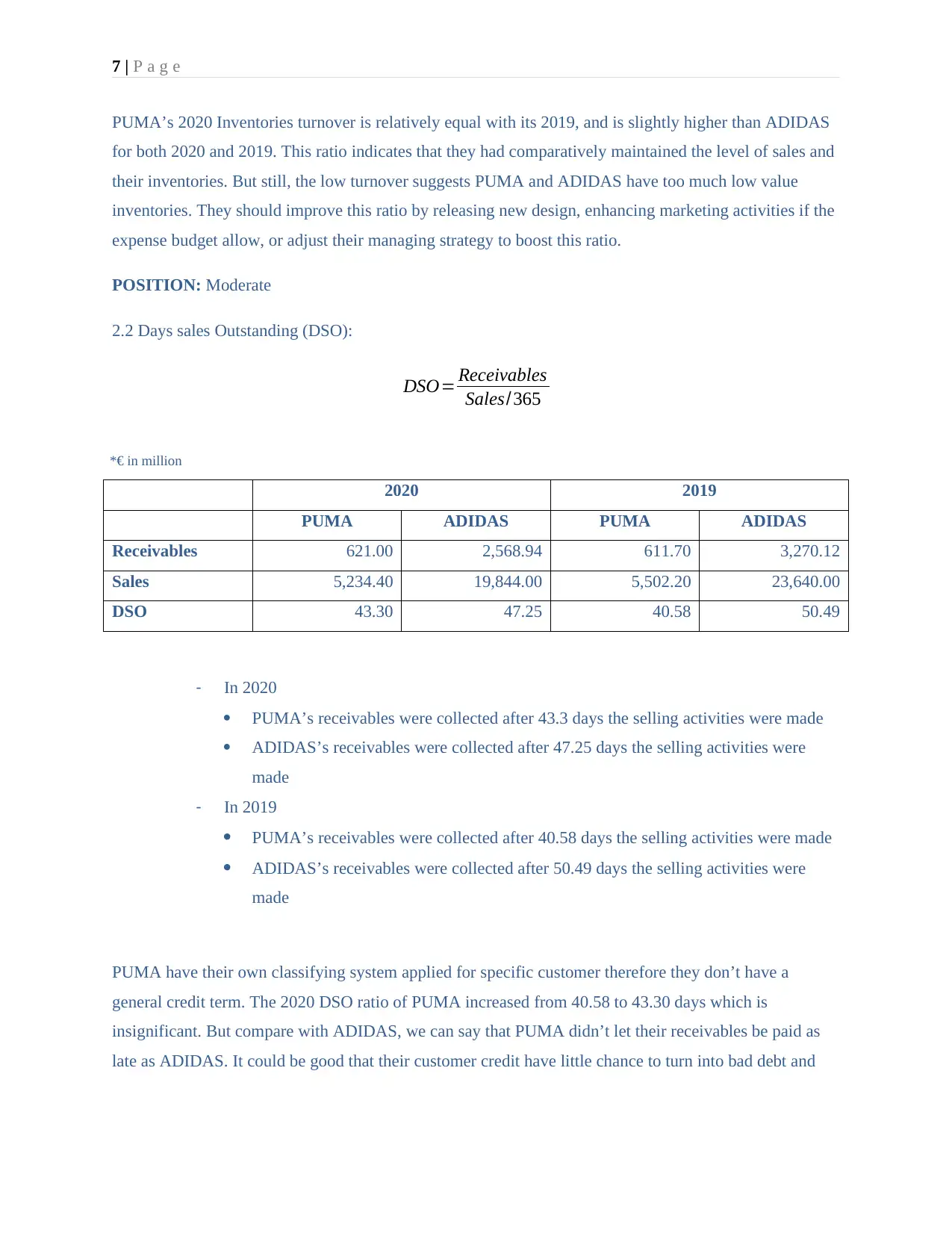

2.2 Days sales Outstanding (DSO):

DSO= Receivables

Sales/365

2020 2019

PUMA ADIDAS PUMA ADIDAS

Receivables 621.00 2,568.94 611.70 3,270.12

Sales 5,234.40 19,844.00 5,502.20 23,640.00

DSO 43.30 47.25 40.58 50.49

- In 2020

PUMA’s receivables were collected after 43.3 days the selling activities were made

ADIDAS’s receivables were collected after 47.25 days the selling activities were

made

- In 2019

PUMA’s receivables were collected after 40.58 days the selling activities were made

ADIDAS’s receivables were collected after 50.49 days the selling activities were

made

PUMA have their own classifying system applied for specific customer therefore they don’t have a

general credit term. The 2020 DSO ratio of PUMA increased from 40.58 to 43.30 days which is

insignificant. But compare with ADIDAS, we can say that PUMA didn’t let their receivables be paid as

late as ADIDAS. It could be good that their customer credit have little chance to turn into bad debt and

*€ in million

PUMA’s 2020 Inventories turnover is relatively equal with its 2019, and is slightly higher than ADIDAS

for both 2020 and 2019. This ratio indicates that they had comparatively maintained the level of sales and

their inventories. But still, the low turnover suggests PUMA and ADIDAS have too much low value

inventories. They should improve this ratio by releasing new design, enhancing marketing activities if the

expense budget allow, or adjust their managing strategy to boost this ratio.

POSITION: Moderate

2.2 Days sales Outstanding (DSO):

DSO= Receivables

Sales/365

2020 2019

PUMA ADIDAS PUMA ADIDAS

Receivables 621.00 2,568.94 611.70 3,270.12

Sales 5,234.40 19,844.00 5,502.20 23,640.00

DSO 43.30 47.25 40.58 50.49

- In 2020

PUMA’s receivables were collected after 43.3 days the selling activities were made

ADIDAS’s receivables were collected after 47.25 days the selling activities were

made

- In 2019

PUMA’s receivables were collected after 40.58 days the selling activities were made

ADIDAS’s receivables were collected after 50.49 days the selling activities were

made

PUMA have their own classifying system applied for specific customer therefore they don’t have a

general credit term. The 2020 DSO ratio of PUMA increased from 40.58 to 43.30 days which is

insignificant. But compare with ADIDAS, we can say that PUMA didn’t let their receivables be paid as

late as ADIDAS. It could be good that their customer credit have little chance to turn into bad debt and

*€ in million

8 | P a g e

become uncollectible. And because of the small distance of this ratio between PUMA and ADIDAS, we

can see that their credit policies quite keep pace with each other.

POSITION: Moderate

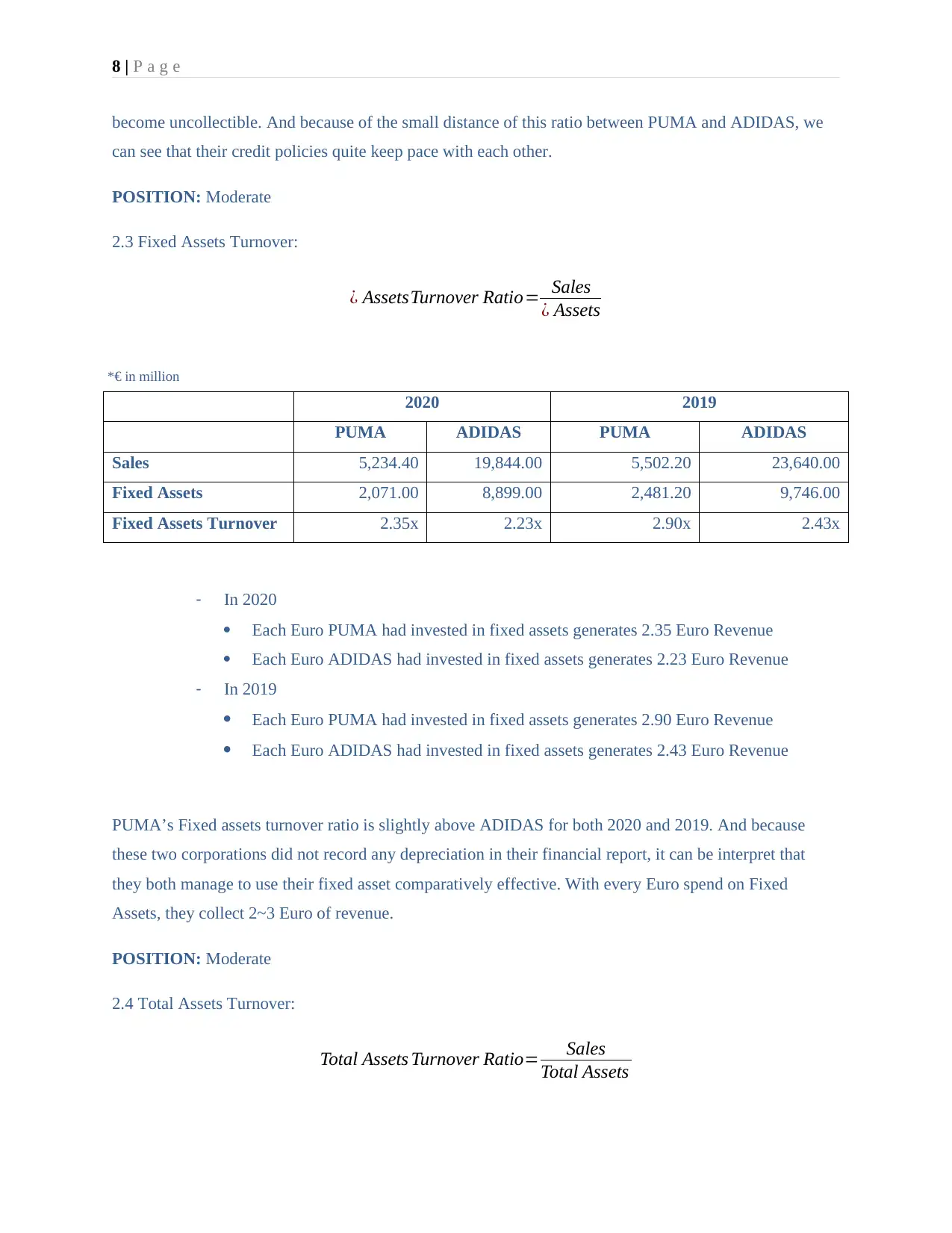

2.3 Fixed Assets Turnover:

¿ AssetsTurnover Ratio= Sales

¿ Assets

2020 2019

PUMA ADIDAS PUMA ADIDAS

Sales 5,234.40 19,844.00 5,502.20 23,640.00

Fixed Assets 2,071.00 8,899.00 2,481.20 9,746.00

Fixed Assets Turnover 2.35x 2.23x 2.90x 2.43x

- In 2020

Each Euro PUMA had invested in fixed assets generates 2.35 Euro Revenue

Each Euro ADIDAS had invested in fixed assets generates 2.23 Euro Revenue

- In 2019

Each Euro PUMA had invested in fixed assets generates 2.90 Euro Revenue

Each Euro ADIDAS had invested in fixed assets generates 2.43 Euro Revenue

PUMA’s Fixed assets turnover ratio is slightly above ADIDAS for both 2020 and 2019. And because

these two corporations did not record any depreciation in their financial report, it can be interpret that

they both manage to use their fixed asset comparatively effective. With every Euro spend on Fixed

Assets, they collect 2~3 Euro of revenue.

POSITION: Moderate

2.4 Total Assets Turnover:

Total Assets Turnover Ratio= Sales

Total Assets

*€ in million

become uncollectible. And because of the small distance of this ratio between PUMA and ADIDAS, we

can see that their credit policies quite keep pace with each other.

POSITION: Moderate

2.3 Fixed Assets Turnover:

¿ AssetsTurnover Ratio= Sales

¿ Assets

2020 2019

PUMA ADIDAS PUMA ADIDAS

Sales 5,234.40 19,844.00 5,502.20 23,640.00

Fixed Assets 2,071.00 8,899.00 2,481.20 9,746.00

Fixed Assets Turnover 2.35x 2.23x 2.90x 2.43x

- In 2020

Each Euro PUMA had invested in fixed assets generates 2.35 Euro Revenue

Each Euro ADIDAS had invested in fixed assets generates 2.23 Euro Revenue

- In 2019

Each Euro PUMA had invested in fixed assets generates 2.90 Euro Revenue

Each Euro ADIDAS had invested in fixed assets generates 2.43 Euro Revenue

PUMA’s Fixed assets turnover ratio is slightly above ADIDAS for both 2020 and 2019. And because

these two corporations did not record any depreciation in their financial report, it can be interpret that

they both manage to use their fixed asset comparatively effective. With every Euro spend on Fixed

Assets, they collect 2~3 Euro of revenue.

POSITION: Moderate

2.4 Total Assets Turnover:

Total Assets Turnover Ratio= Sales

Total Assets

*€ in million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9 | P a g e

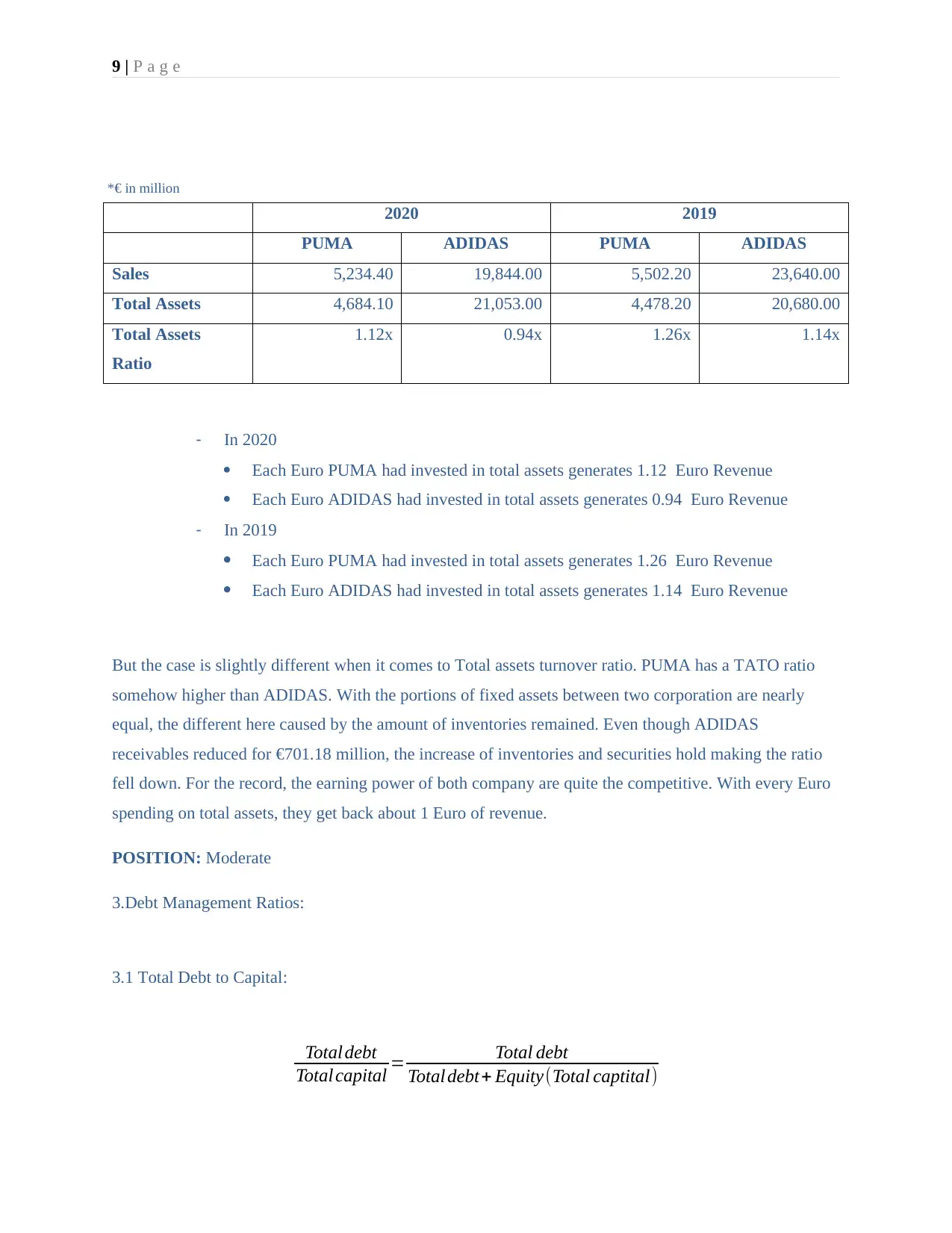

2020 2019

PUMA ADIDAS PUMA ADIDAS

Sales 5,234.40 19,844.00 5,502.20 23,640.00

Total Assets 4,684.10 21,053.00 4,478.20 20,680.00

Total Assets

Ratio

1.12x 0.94x 1.26x 1.14x

- In 2020

Each Euro PUMA had invested in total assets generates 1.12 Euro Revenue

Each Euro ADIDAS had invested in total assets generates 0.94 Euro Revenue

- In 2019

Each Euro PUMA had invested in total assets generates 1.26 Euro Revenue

Each Euro ADIDAS had invested in total assets generates 1.14 Euro Revenue

But the case is slightly different when it comes to Total assets turnover ratio. PUMA has a TATO ratio

somehow higher than ADIDAS. With the portions of fixed assets between two corporation are nearly

equal, the different here caused by the amount of inventories remained. Even though ADIDAS

receivables reduced for €701.18 million, the increase of inventories and securities hold making the ratio

fell down. For the record, the earning power of both company are quite the competitive. With every Euro

spending on total assets, they get back about 1 Euro of revenue.

POSITION: Moderate

3.Debt Management Ratios:

3.1 Total Debt to Capital:

Total debt

Total capital = Total debt

Total debt+ Equity(Total captital)

*€ in million

2020 2019

PUMA ADIDAS PUMA ADIDAS

Sales 5,234.40 19,844.00 5,502.20 23,640.00

Total Assets 4,684.10 21,053.00 4,478.20 20,680.00

Total Assets

Ratio

1.12x 0.94x 1.26x 1.14x

- In 2020

Each Euro PUMA had invested in total assets generates 1.12 Euro Revenue

Each Euro ADIDAS had invested in total assets generates 0.94 Euro Revenue

- In 2019

Each Euro PUMA had invested in total assets generates 1.26 Euro Revenue

Each Euro ADIDAS had invested in total assets generates 1.14 Euro Revenue

But the case is slightly different when it comes to Total assets turnover ratio. PUMA has a TATO ratio

somehow higher than ADIDAS. With the portions of fixed assets between two corporation are nearly

equal, the different here caused by the amount of inventories remained. Even though ADIDAS

receivables reduced for €701.18 million, the increase of inventories and securities hold making the ratio

fell down. For the record, the earning power of both company are quite the competitive. With every Euro

spending on total assets, they get back about 1 Euro of revenue.

POSITION: Moderate

3.Debt Management Ratios:

3.1 Total Debt to Capital:

Total debt

Total capital = Total debt

Total debt+ Equity(Total captital)

*€ in million

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10 | P a g e

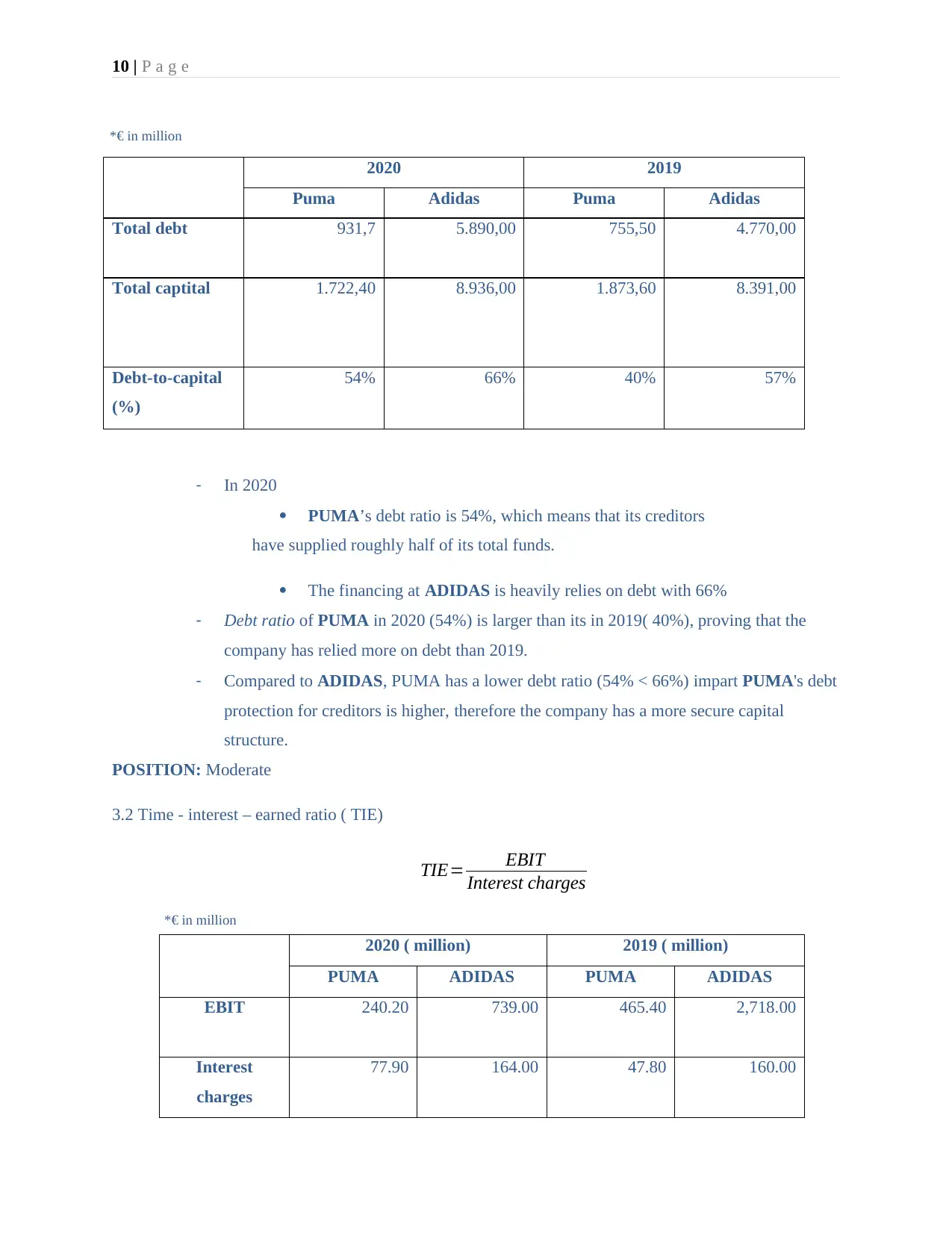

2020 2019

Puma Adidas Puma Adidas

Total debt 931,7 5.890,00 755,50 4.770,00

Total captital 1.722,40 8.936,00 1.873,60 8.391,00

Debt-to-capital

(%)

54% 66% 40% 57%

- In 2020

PUMA’s debt ratio is 54%, which means that its creditors

have supplied roughly half of its total funds.

The financing at ADIDAS is heavily relies on debt with 66%

- Debt ratio of PUMA in 2020 (54%) is larger than its in 2019( 40%), proving that the

company has relied more on debt than 2019.

- Compared to ADIDAS, PUMA has a lower debt ratio (54% < 66%) impart PUMA's debt

protection for creditors is higher, therefore the company has a more secure capital

structure.

POSITION: Moderate

3.2 Time - interest – earned ratio ( TIE)

TIE= EBIT

Interest charges

2020 ( million) 2019 ( million)

PUMA ADIDAS PUMA ADIDAS

EBIT 240.20 739.00 465.40 2,718.00

Interest

charges

77.90 164.00 47.80 160.00

*€ in million

*€ in million

2020 2019

Puma Adidas Puma Adidas

Total debt 931,7 5.890,00 755,50 4.770,00

Total captital 1.722,40 8.936,00 1.873,60 8.391,00

Debt-to-capital

(%)

54% 66% 40% 57%

- In 2020

PUMA’s debt ratio is 54%, which means that its creditors

have supplied roughly half of its total funds.

The financing at ADIDAS is heavily relies on debt with 66%

- Debt ratio of PUMA in 2020 (54%) is larger than its in 2019( 40%), proving that the

company has relied more on debt than 2019.

- Compared to ADIDAS, PUMA has a lower debt ratio (54% < 66%) impart PUMA's debt

protection for creditors is higher, therefore the company has a more secure capital

structure.

POSITION: Moderate

3.2 Time - interest – earned ratio ( TIE)

TIE= EBIT

Interest charges

2020 ( million) 2019 ( million)

PUMA ADIDAS PUMA ADIDAS

EBIT 240.20 739.00 465.40 2,718.00

Interest

charges

77.90 164.00 47.80 160.00

*€ in million

*€ in million

11 | P a g e

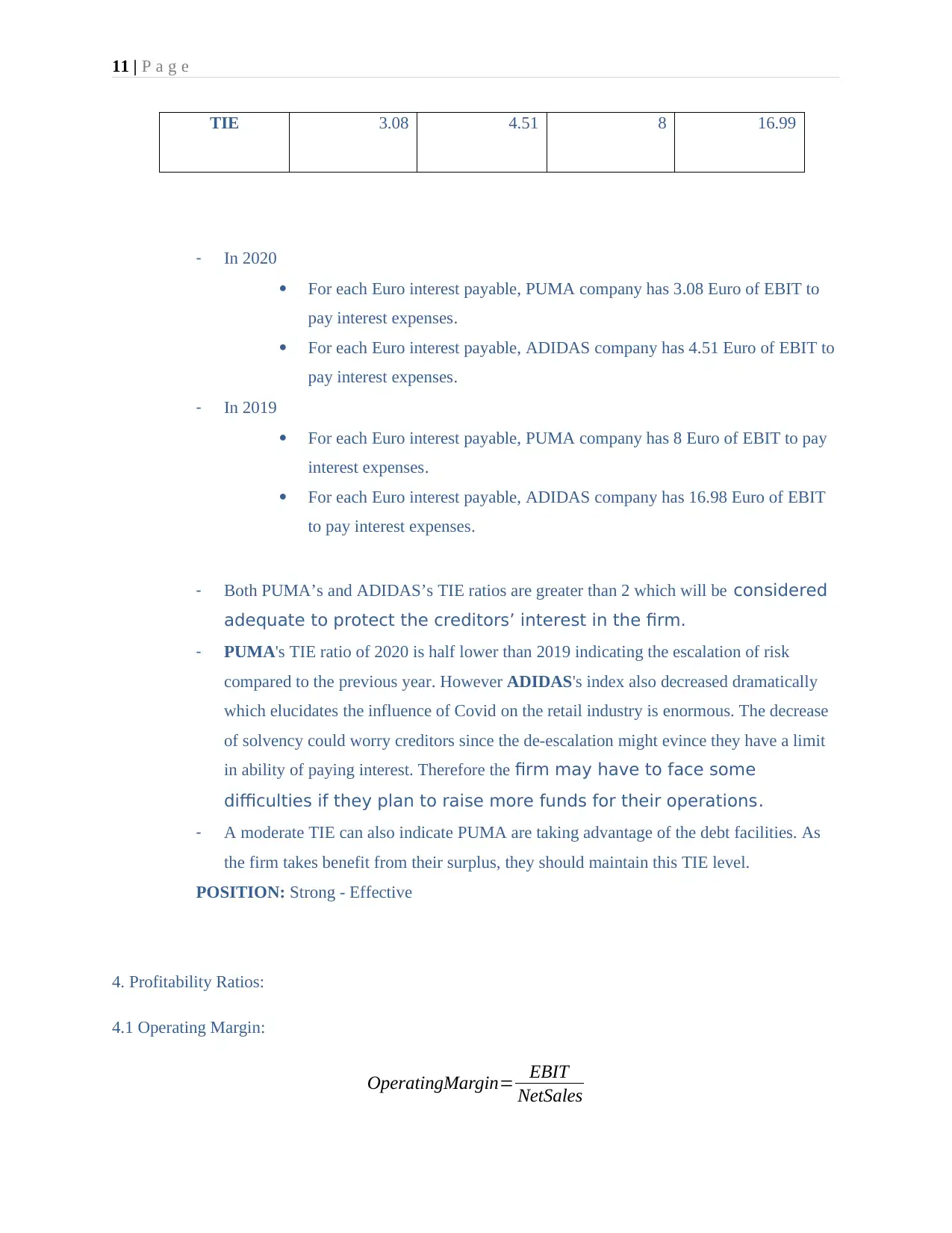

TIE 3.08 4.51 8 16.99

- In 2020

For each Euro interest payable, PUMA company has 3.08 Euro of EBIT to

pay interest expenses.

For each Euro interest payable, ADIDAS company has 4.51 Euro of EBIT to

pay interest expenses.

- In 2019

For each Euro interest payable, PUMA company has 8 Euro of EBIT to pay

interest expenses.

For each Euro interest payable, ADIDAS company has 16.98 Euro of EBIT

to pay interest expenses.

- Both PUMA’s and ADIDAS’s TIE ratios are greater than 2 which will be considered

adequate to protect the creditors’ interest in the firm.

- PUMA's TIE ratio of 2020 is half lower than 2019 indicating the escalation of risk

compared to the previous year. However ADIDAS's index also decreased dramatically

which elucidates the influence of Covid on the retail industry is enormous. The decrease

of solvency could worry creditors since the de-escalation might evince they have a limit

in ability of paying interest. Therefore the firm may have to face some

difficulties if they plan to raise more funds for their operations.

- A moderate TIE can also indicate PUMA are taking advantage of the debt facilities. As

the firm takes benefit from their surplus, they should maintain this TIE level.

POSITION: Strong - Effective

4. Profitability Ratios:

4.1 Operating Margin:

OperatingMargin= EBIT

NetSales

TIE 3.08 4.51 8 16.99

- In 2020

For each Euro interest payable, PUMA company has 3.08 Euro of EBIT to

pay interest expenses.

For each Euro interest payable, ADIDAS company has 4.51 Euro of EBIT to

pay interest expenses.

- In 2019

For each Euro interest payable, PUMA company has 8 Euro of EBIT to pay

interest expenses.

For each Euro interest payable, ADIDAS company has 16.98 Euro of EBIT

to pay interest expenses.

- Both PUMA’s and ADIDAS’s TIE ratios are greater than 2 which will be considered

adequate to protect the creditors’ interest in the firm.

- PUMA's TIE ratio of 2020 is half lower than 2019 indicating the escalation of risk

compared to the previous year. However ADIDAS's index also decreased dramatically

which elucidates the influence of Covid on the retail industry is enormous. The decrease

of solvency could worry creditors since the de-escalation might evince they have a limit

in ability of paying interest. Therefore the firm may have to face some

difficulties if they plan to raise more funds for their operations.

- A moderate TIE can also indicate PUMA are taking advantage of the debt facilities. As

the firm takes benefit from their surplus, they should maintain this TIE level.

POSITION: Strong - Effective

4. Profitability Ratios:

4.1 Operating Margin:

OperatingMargin= EBIT

NetSales

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.