Qantas & Air New Zealand: A Financial Case Study (2015-2017)

VerifiedAdded on 2023/04/21

|24

|4920

|133

Case Study

AI Summary

This financial case study provides an in-depth analysis of the financial conditions of Qantas Airways and Air New Zealand Limited between 2015 and 2017. It utilizes ratio analysis to evaluate their liquidity, solvency, and profitability, identifying issues such as liquidity problems, high financial leverage, and lower return on assets. The study examines key financial ratios including current ratio, quick ratio, accounts receivable turnover, number of days’ sales in receivables, inventory turnover, debt to assets ratio, debt to equity ratio, and profit margin ratio. Graphs and tables are used to illustrate the findings and compare the performance of the two airlines. The report concludes with recommendations to address the identified financial challenges, such as increasing the selling price to improve financial stability.

Running head: FINANCIAL CASE STUDY

Financial Case Study

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Case Study

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL CASE STUDY

Executive Summary:

The current report would intend to analyse the financial condition of two popular airline

companies operating in the aviation industry of Australia. Therefore, the airlines selected for

meeting the purpose of this report include Qantas Airways and Air New Zealand Limited. It

could be found that both Qantas Airways and Air New Zealand suffer from various financial

issues, which are evaluated from various calculated financial ratios. It has been observed that the

airlines suffer primarily from liquidity issues, high financial leverage issues and lower return on

assets. Some of the notable issues include liquidity problems, issues related to increased financial

leverage and lower return on assets. Certain recommendations have been provided to deal with

these identified issues; however, each alternative has its own pros and cons. However, out of the

provided recommendations, increasing the selling price is mainly necessary for dealing with the

financial troubles in the initial stage.

FINANCIAL CASE STUDY

Executive Summary:

The current report would intend to analyse the financial condition of two popular airline

companies operating in the aviation industry of Australia. Therefore, the airlines selected for

meeting the purpose of this report include Qantas Airways and Air New Zealand Limited. It

could be found that both Qantas Airways and Air New Zealand suffer from various financial

issues, which are evaluated from various calculated financial ratios. It has been observed that the

airlines suffer primarily from liquidity issues, high financial leverage issues and lower return on

assets. Some of the notable issues include liquidity problems, issues related to increased financial

leverage and lower return on assets. Certain recommendations have been provided to deal with

these identified issues; however, each alternative has its own pros and cons. However, out of the

provided recommendations, increasing the selling price is mainly necessary for dealing with the

financial troubles in the initial stage.

2

FINANCIAL CASE STUDY

Table of Contents

Introduction:....................................................................................................................................3

Findings:..........................................................................................................................................3

Discussions:...................................................................................................................................17

Conclusion:....................................................................................................................................19

Recommendation and implementation:.........................................................................................19

References:....................................................................................................................................21

FINANCIAL CASE STUDY

Table of Contents

Introduction:....................................................................................................................................3

Findings:..........................................................................................................................................3

Discussions:...................................................................................................................................17

Conclusion:....................................................................................................................................19

Recommendation and implementation:.........................................................................................19

References:....................................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL CASE STUDY

Introduction:

The current report would intend to analyse the financial condition of two popular airline

companies operating in the aviation industry of Australia. Therefore, the airlines selected for

meeting the purpose of this report include Qantas Airways and Air New Zealand Limited. Qantas

is considered as the Australian flag carrier and the biggest airline in terms of fleet size, global

flights and global destinations (Qantas.com, 2019). On the other hand, Air New Zealand is the

flag carrier airline of New Zealand operating in 19 global nations (Airnewzealand.com.au, 2019).

For conducting the financial analysis of the two chosen airlines, ratio analysis tool is used for

evaluating their performance in the operating markets. Finally, based on the valuation of ratios

and financial conditions, appropriate recommendations would have been provided in order to

improve their overall financial conditions.

Findings:

For analysing the financial conditions of Qantas Airways and Air New Zealand, various

financial ratios have been taken into consideration, which are described in details and the

findings are enumerated as follows:

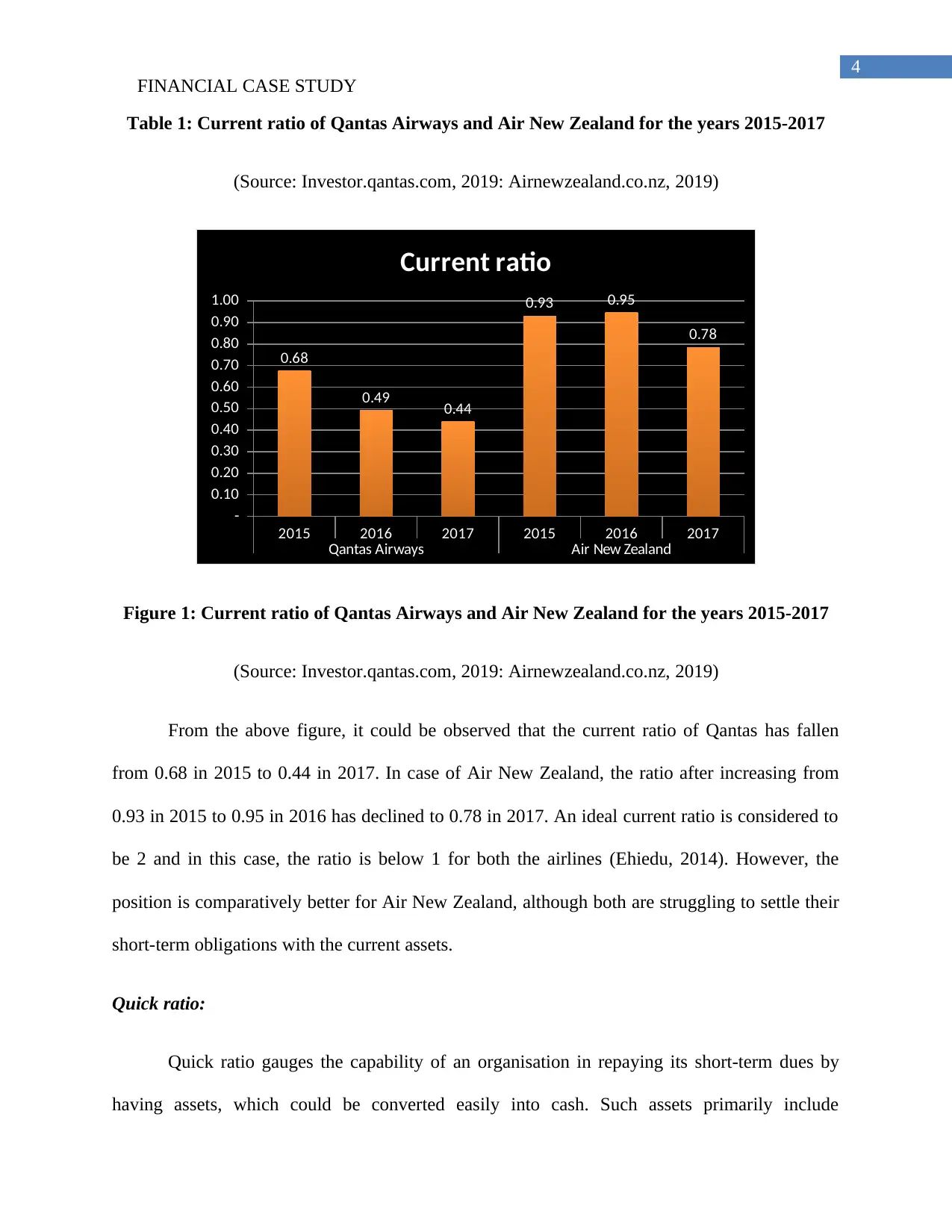

Current ratio:

Current ratio gauges the ability of a business organisation in covering its short-term

obligations, which are due within a year (Brigham et al., 2016). The current ratio of Qantas and

Air New Zealand is demonstrated briefly in tabular and diagrammatic forms as follows:

FINANCIAL CASE STUDY

Introduction:

The current report would intend to analyse the financial condition of two popular airline

companies operating in the aviation industry of Australia. Therefore, the airlines selected for

meeting the purpose of this report include Qantas Airways and Air New Zealand Limited. Qantas

is considered as the Australian flag carrier and the biggest airline in terms of fleet size, global

flights and global destinations (Qantas.com, 2019). On the other hand, Air New Zealand is the

flag carrier airline of New Zealand operating in 19 global nations (Airnewzealand.com.au, 2019).

For conducting the financial analysis of the two chosen airlines, ratio analysis tool is used for

evaluating their performance in the operating markets. Finally, based on the valuation of ratios

and financial conditions, appropriate recommendations would have been provided in order to

improve their overall financial conditions.

Findings:

For analysing the financial conditions of Qantas Airways and Air New Zealand, various

financial ratios have been taken into consideration, which are described in details and the

findings are enumerated as follows:

Current ratio:

Current ratio gauges the ability of a business organisation in covering its short-term

obligations, which are due within a year (Brigham et al., 2016). The current ratio of Qantas and

Air New Zealand is demonstrated briefly in tabular and diagrammatic forms as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL CASE STUDY

Table 1: Current ratio of Qantas Airways and Air New Zealand for the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.68

0.49 0.44

0.93 0.95

0.78

Current ratio

Figure 1: Current ratio of Qantas Airways and Air New Zealand for the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

From the above figure, it could be observed that the current ratio of Qantas has fallen

from 0.68 in 2015 to 0.44 in 2017. In case of Air New Zealand, the ratio after increasing from

0.93 in 2015 to 0.95 in 2016 has declined to 0.78 in 2017. An ideal current ratio is considered to

be 2 and in this case, the ratio is below 1 for both the airlines (Ehiedu, 2014). However, the

position is comparatively better for Air New Zealand, although both are struggling to settle their

short-term obligations with the current assets.

Quick ratio:

Quick ratio gauges the capability of an organisation in repaying its short-term dues by

having assets, which could be converted easily into cash. Such assets primarily include

FINANCIAL CASE STUDY

Table 1: Current ratio of Qantas Airways and Air New Zealand for the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.68

0.49 0.44

0.93 0.95

0.78

Current ratio

Figure 1: Current ratio of Qantas Airways and Air New Zealand for the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

From the above figure, it could be observed that the current ratio of Qantas has fallen

from 0.68 in 2015 to 0.44 in 2017. In case of Air New Zealand, the ratio after increasing from

0.93 in 2015 to 0.95 in 2016 has declined to 0.78 in 2017. An ideal current ratio is considered to

be 2 and in this case, the ratio is below 1 for both the airlines (Ehiedu, 2014). However, the

position is comparatively better for Air New Zealand, although both are struggling to settle their

short-term obligations with the current assets.

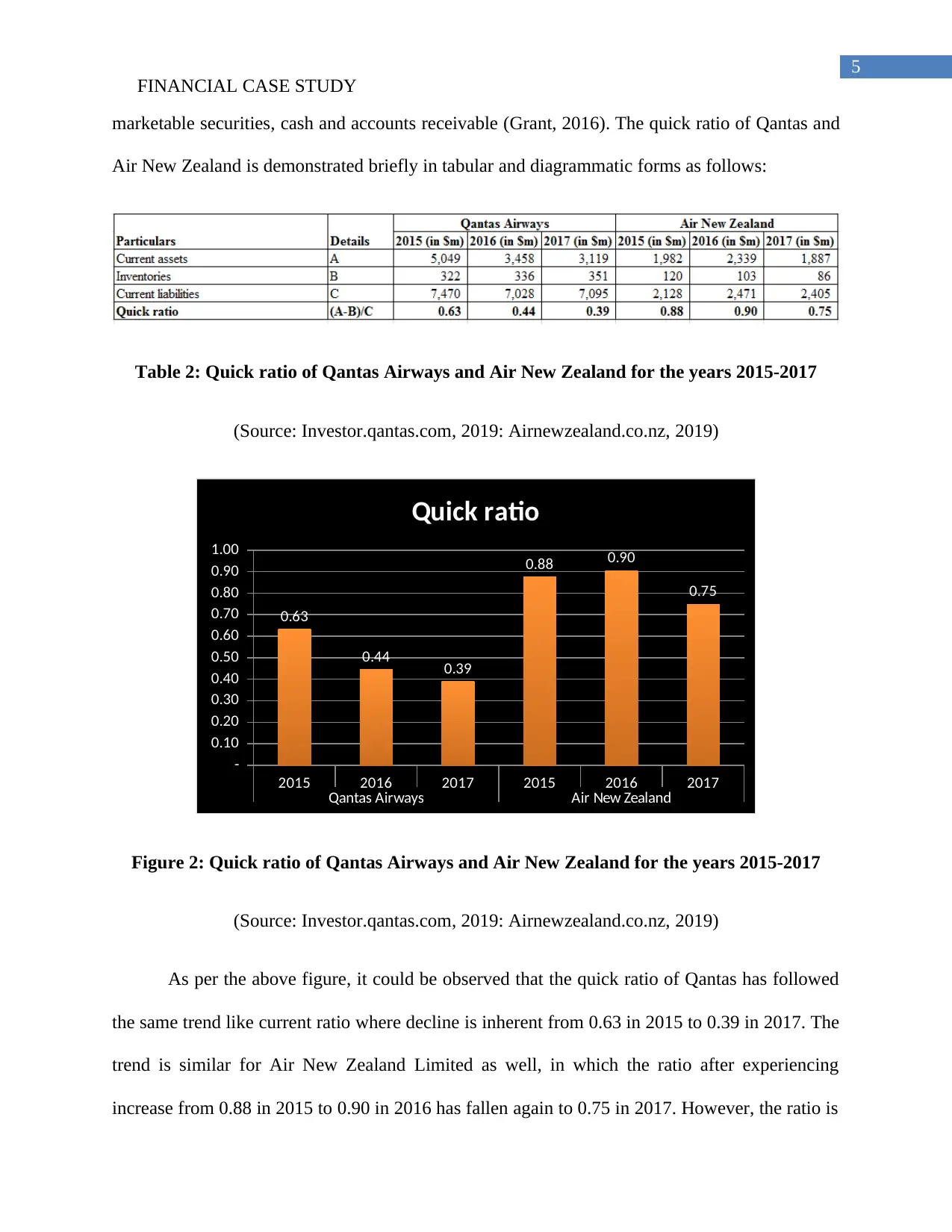

Quick ratio:

Quick ratio gauges the capability of an organisation in repaying its short-term dues by

having assets, which could be converted easily into cash. Such assets primarily include

5

FINANCIAL CASE STUDY

marketable securities, cash and accounts receivable (Grant, 2016). The quick ratio of Qantas and

Air New Zealand is demonstrated briefly in tabular and diagrammatic forms as follows:

Table 2: Quick ratio of Qantas Airways and Air New Zealand for the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.63

0.44 0.39

0.88 0.90

0.75

Quick ratio

Figure 2: Quick ratio of Qantas Airways and Air New Zealand for the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

As per the above figure, it could be observed that the quick ratio of Qantas has followed

the same trend like current ratio where decline is inherent from 0.63 in 2015 to 0.39 in 2017. The

trend is similar for Air New Zealand Limited as well, in which the ratio after experiencing

increase from 0.88 in 2015 to 0.90 in 2016 has fallen again to 0.75 in 2017. However, the ratio is

FINANCIAL CASE STUDY

marketable securities, cash and accounts receivable (Grant, 2016). The quick ratio of Qantas and

Air New Zealand is demonstrated briefly in tabular and diagrammatic forms as follows:

Table 2: Quick ratio of Qantas Airways and Air New Zealand for the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

0.63

0.44 0.39

0.88 0.90

0.75

Quick ratio

Figure 2: Quick ratio of Qantas Airways and Air New Zealand for the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

As per the above figure, it could be observed that the quick ratio of Qantas has followed

the same trend like current ratio where decline is inherent from 0.63 in 2015 to 0.39 in 2017. The

trend is similar for Air New Zealand Limited as well, in which the ratio after experiencing

increase from 0.88 in 2015 to 0.90 in 2016 has fallen again to 0.75 in 2017. However, the ratio is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL CASE STUDY

below the ideal standard of 1 for both airlines (Islam, 2014). In this case, the ratio for Air New

Zealand is close to the ideal standard, while Qantas is facing liquidity issues for clearing its

short-term obligations.

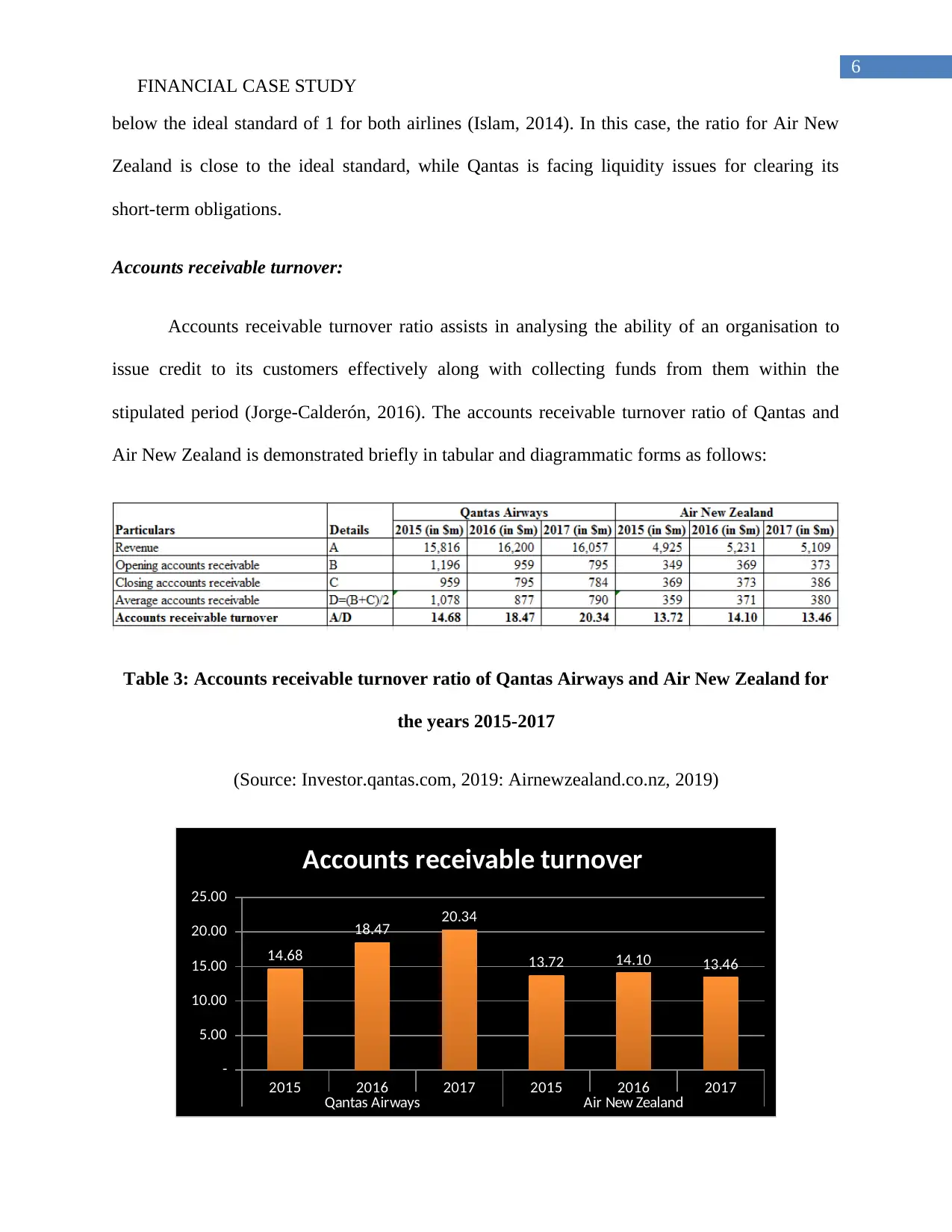

Accounts receivable turnover:

Accounts receivable turnover ratio assists in analysing the ability of an organisation to

issue credit to its customers effectively along with collecting funds from them within the

stipulated period (Jorge-Calderón, 2016). The accounts receivable turnover ratio of Qantas and

Air New Zealand is demonstrated briefly in tabular and diagrammatic forms as follows:

Table 3: Accounts receivable turnover ratio of Qantas Airways and Air New Zealand for

the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

5.00

10.00

15.00

20.00

25.00

14.68

18.47 20.34

13.72 14.10 13.46

Accounts receivable turnover

FINANCIAL CASE STUDY

below the ideal standard of 1 for both airlines (Islam, 2014). In this case, the ratio for Air New

Zealand is close to the ideal standard, while Qantas is facing liquidity issues for clearing its

short-term obligations.

Accounts receivable turnover:

Accounts receivable turnover ratio assists in analysing the ability of an organisation to

issue credit to its customers effectively along with collecting funds from them within the

stipulated period (Jorge-Calderón, 2016). The accounts receivable turnover ratio of Qantas and

Air New Zealand is demonstrated briefly in tabular and diagrammatic forms as follows:

Table 3: Accounts receivable turnover ratio of Qantas Airways and Air New Zealand for

the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

5.00

10.00

15.00

20.00

25.00

14.68

18.47 20.34

13.72 14.10 13.46

Accounts receivable turnover

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL CASE STUDY

Figure 3: Accounts receivable turnover ratio of Qantas Airways and Air New Zealand for

the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

The above figure clearly states that the accounts receivable turnover ratio of Qantas has

increased from 14.68% in 2015 to 20.34 in 2017, while the same for Air New Zealand has

declined from 13.72% in 2015 to 13.46% in 2017. A higher turnover indicates that the

organisation has been generating sales at a faster rate, which is the case with Qantas, as opposed

to Air New Zealand. Hence, the position of Qantas is deemed to be favourable in terms of

accounts receivable turnover compared to Air New Zealand.

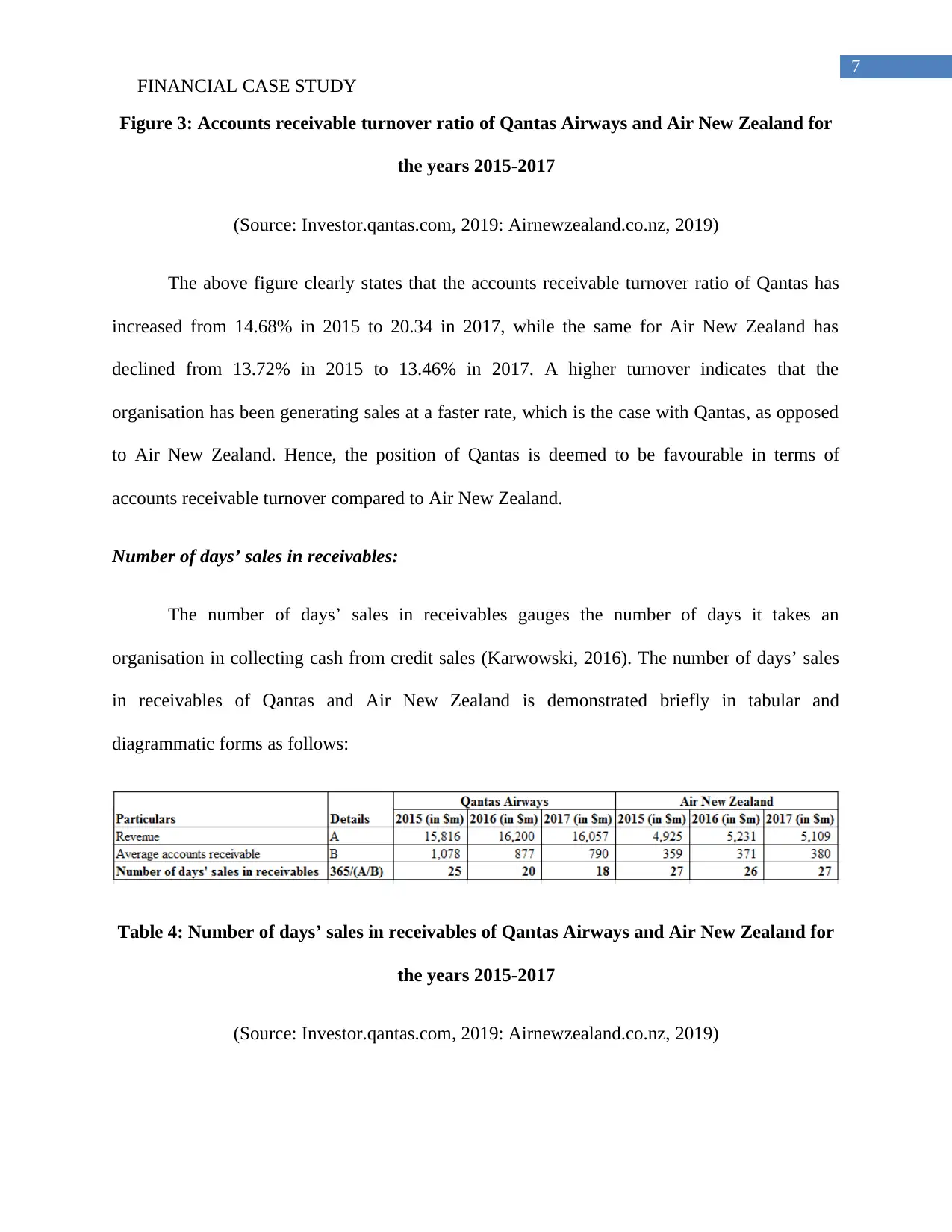

Number of days’ sales in receivables:

The number of days’ sales in receivables gauges the number of days it takes an

organisation in collecting cash from credit sales (Karwowski, 2016). The number of days’ sales

in receivables of Qantas and Air New Zealand is demonstrated briefly in tabular and

diagrammatic forms as follows:

Table 4: Number of days’ sales in receivables of Qantas Airways and Air New Zealand for

the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

FINANCIAL CASE STUDY

Figure 3: Accounts receivable turnover ratio of Qantas Airways and Air New Zealand for

the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

The above figure clearly states that the accounts receivable turnover ratio of Qantas has

increased from 14.68% in 2015 to 20.34 in 2017, while the same for Air New Zealand has

declined from 13.72% in 2015 to 13.46% in 2017. A higher turnover indicates that the

organisation has been generating sales at a faster rate, which is the case with Qantas, as opposed

to Air New Zealand. Hence, the position of Qantas is deemed to be favourable in terms of

accounts receivable turnover compared to Air New Zealand.

Number of days’ sales in receivables:

The number of days’ sales in receivables gauges the number of days it takes an

organisation in collecting cash from credit sales (Karwowski, 2016). The number of days’ sales

in receivables of Qantas and Air New Zealand is demonstrated briefly in tabular and

diagrammatic forms as follows:

Table 4: Number of days’ sales in receivables of Qantas Airways and Air New Zealand for

the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

8

FINANCIAL CASE STUDY

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

5

10

15

20

25

30

25

20 18

27 26 27

Number of days' sales in receivables

Figure 4: Number of days’ sales in receivables of Qantas Airways and Air New Zealand for

the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

From the above figure, it is evident that the number of days’ sales in receivables for

Qantas has declined from 25 days in 2015 to 18 days in 2017, while it has remained almost same

between 26 days and 27 days from 2015 to 2017. If the number of days’ receivables is lower, it

is desirable, since the organisation is collecting dues from its customers at a faster rate (Williams

& Dobelman, 2017). Thus, it denotes that Qantas is performing better than Air New Zealand in

collecting due amounts from its customers.

Inventory turnover:

Inventory turnover is an efficiency ratio, which denotes the number of times an

organisation has sold and replaced inventory during a stipulated timeframe (Marti, Puertas &

FINANCIAL CASE STUDY

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

5

10

15

20

25

30

25

20 18

27 26 27

Number of days' sales in receivables

Figure 4: Number of days’ sales in receivables of Qantas Airways and Air New Zealand for

the years 2015-2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

From the above figure, it is evident that the number of days’ sales in receivables for

Qantas has declined from 25 days in 2015 to 18 days in 2017, while it has remained almost same

between 26 days and 27 days from 2015 to 2017. If the number of days’ receivables is lower, it

is desirable, since the organisation is collecting dues from its customers at a faster rate (Williams

& Dobelman, 2017). Thus, it denotes that Qantas is performing better than Air New Zealand in

collecting due amounts from its customers.

Inventory turnover:

Inventory turnover is an efficiency ratio, which denotes the number of times an

organisation has sold and replaced inventory during a stipulated timeframe (Marti, Puertas &

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

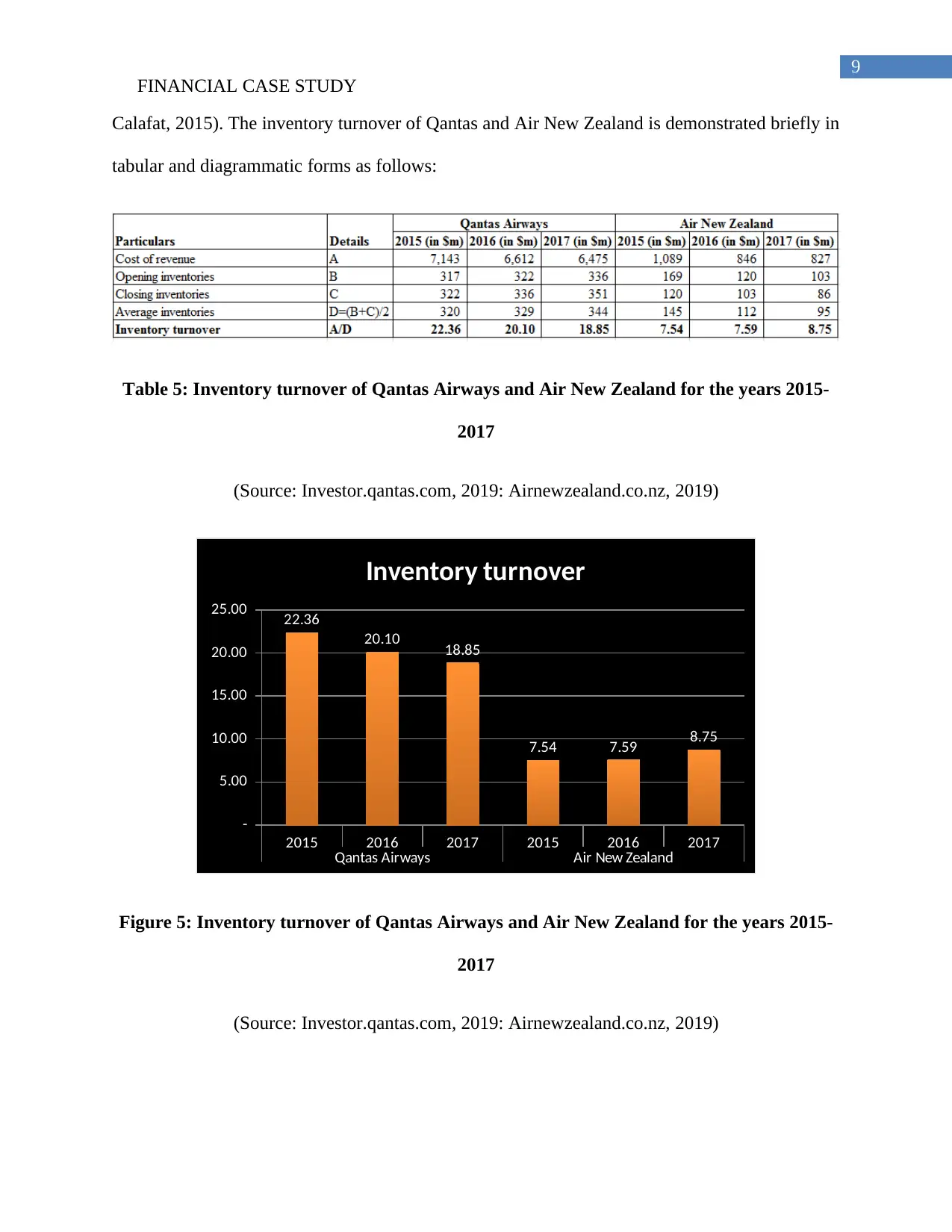

FINANCIAL CASE STUDY

Calafat, 2015). The inventory turnover of Qantas and Air New Zealand is demonstrated briefly in

tabular and diagrammatic forms as follows:

Table 5: Inventory turnover of Qantas Airways and Air New Zealand for the years 2015-

2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

5.00

10.00

15.00

20.00

25.00 22.36

20.10 18.85

7.54 7.59 8.75

Inventory turnover

Figure 5: Inventory turnover of Qantas Airways and Air New Zealand for the years 2015-

2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

FINANCIAL CASE STUDY

Calafat, 2015). The inventory turnover of Qantas and Air New Zealand is demonstrated briefly in

tabular and diagrammatic forms as follows:

Table 5: Inventory turnover of Qantas Airways and Air New Zealand for the years 2015-

2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

-

5.00

10.00

15.00

20.00

25.00 22.36

20.10 18.85

7.54 7.59 8.75

Inventory turnover

Figure 5: Inventory turnover of Qantas Airways and Air New Zealand for the years 2015-

2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL CASE STUDY

According to the above figure, it could be witnessed that the inventory turnover of Qantas

has declined from 22.36 times in 2015 to 18.85 times in 2017. On the other hand, the turnover of

Air New Zealand has increased from 7.54 times in 2015 to 8.75 times in 2017. A higher figure is

always desirable, since it indicates increased market demand, which causes the organisation to

release its stock at a quicker rate (Mayes, 2014). In this case, although the figure is falling over

the years for Qantas, it is still much higher compared to Air New Zealand. Hence, in terms of

inventory turnover, Qantas is having competitive edge over Air New Zealand in the global

markets.

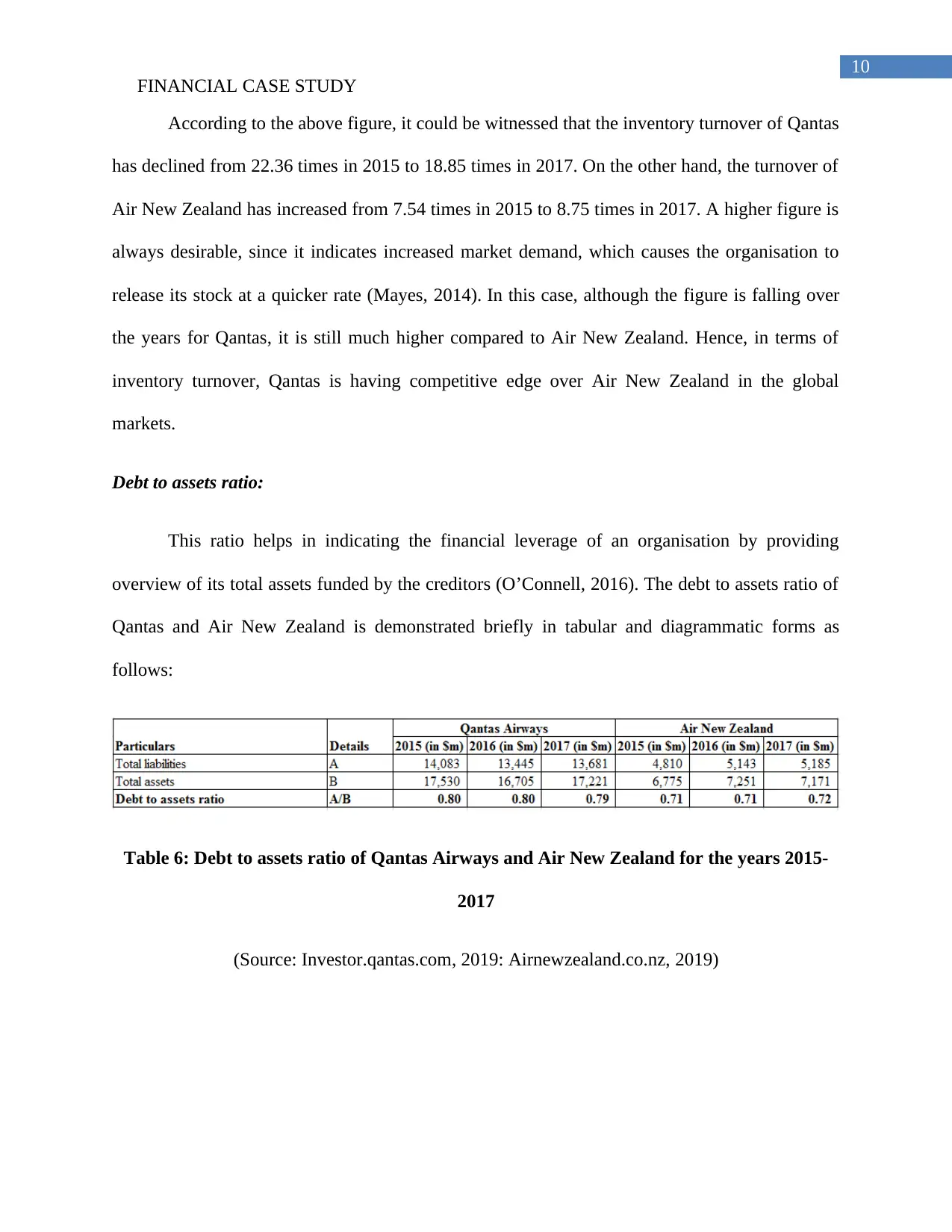

Debt to assets ratio:

This ratio helps in indicating the financial leverage of an organisation by providing

overview of its total assets funded by the creditors (O’Connell, 2016). The debt to assets ratio of

Qantas and Air New Zealand is demonstrated briefly in tabular and diagrammatic forms as

follows:

Table 6: Debt to assets ratio of Qantas Airways and Air New Zealand for the years 2015-

2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

FINANCIAL CASE STUDY

According to the above figure, it could be witnessed that the inventory turnover of Qantas

has declined from 22.36 times in 2015 to 18.85 times in 2017. On the other hand, the turnover of

Air New Zealand has increased from 7.54 times in 2015 to 8.75 times in 2017. A higher figure is

always desirable, since it indicates increased market demand, which causes the organisation to

release its stock at a quicker rate (Mayes, 2014). In this case, although the figure is falling over

the years for Qantas, it is still much higher compared to Air New Zealand. Hence, in terms of

inventory turnover, Qantas is having competitive edge over Air New Zealand in the global

markets.

Debt to assets ratio:

This ratio helps in indicating the financial leverage of an organisation by providing

overview of its total assets funded by the creditors (O’Connell, 2016). The debt to assets ratio of

Qantas and Air New Zealand is demonstrated briefly in tabular and diagrammatic forms as

follows:

Table 6: Debt to assets ratio of Qantas Airways and Air New Zealand for the years 2015-

2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

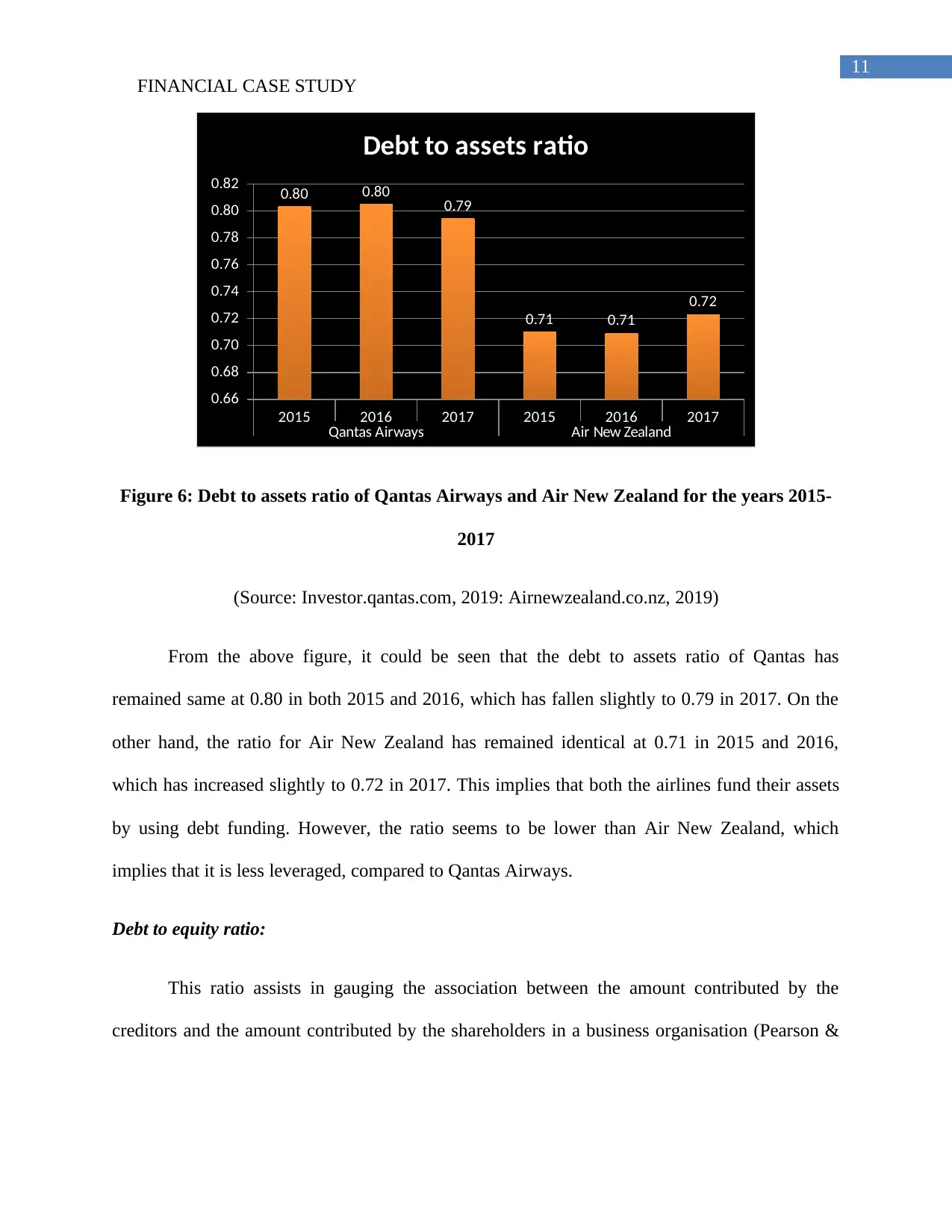

11

FINANCIAL CASE STUDY

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

0.66

0.68

0.70

0.72

0.74

0.76

0.78

0.80

0.82 0.80 0.80 0.79

0.71 0.71

0.72

Debt to assets ratio

Figure 6: Debt to assets ratio of Qantas Airways and Air New Zealand for the years 2015-

2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

From the above figure, it could be seen that the debt to assets ratio of Qantas has

remained same at 0.80 in both 2015 and 2016, which has fallen slightly to 0.79 in 2017. On the

other hand, the ratio for Air New Zealand has remained identical at 0.71 in 2015 and 2016,

which has increased slightly to 0.72 in 2017. This implies that both the airlines fund their assets

by using debt funding. However, the ratio seems to be lower than Air New Zealand, which

implies that it is less leveraged, compared to Qantas Airways.

Debt to equity ratio:

This ratio assists in gauging the association between the amount contributed by the

creditors and the amount contributed by the shareholders in a business organisation (Pearson &

FINANCIAL CASE STUDY

2015 2016 2017 2015 2016 2017

Qantas Airways Air New Zealand

0.66

0.68

0.70

0.72

0.74

0.76

0.78

0.80

0.82 0.80 0.80 0.79

0.71 0.71

0.72

Debt to assets ratio

Figure 6: Debt to assets ratio of Qantas Airways and Air New Zealand for the years 2015-

2017

(Source: Investor.qantas.com, 2019: Airnewzealand.co.nz, 2019)

From the above figure, it could be seen that the debt to assets ratio of Qantas has

remained same at 0.80 in both 2015 and 2016, which has fallen slightly to 0.79 in 2017. On the

other hand, the ratio for Air New Zealand has remained identical at 0.71 in 2015 and 2016,

which has increased slightly to 0.72 in 2017. This implies that both the airlines fund their assets

by using debt funding. However, the ratio seems to be lower than Air New Zealand, which

implies that it is less leveraged, compared to Qantas Airways.

Debt to equity ratio:

This ratio assists in gauging the association between the amount contributed by the

creditors and the amount contributed by the shareholders in a business organisation (Pearson &

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.