Qantas Airways: Non-Current Assets Valuation and Depreciation Analysis

VerifiedAdded on 2022/09/17

|18

|2350

|40

Report

AI Summary

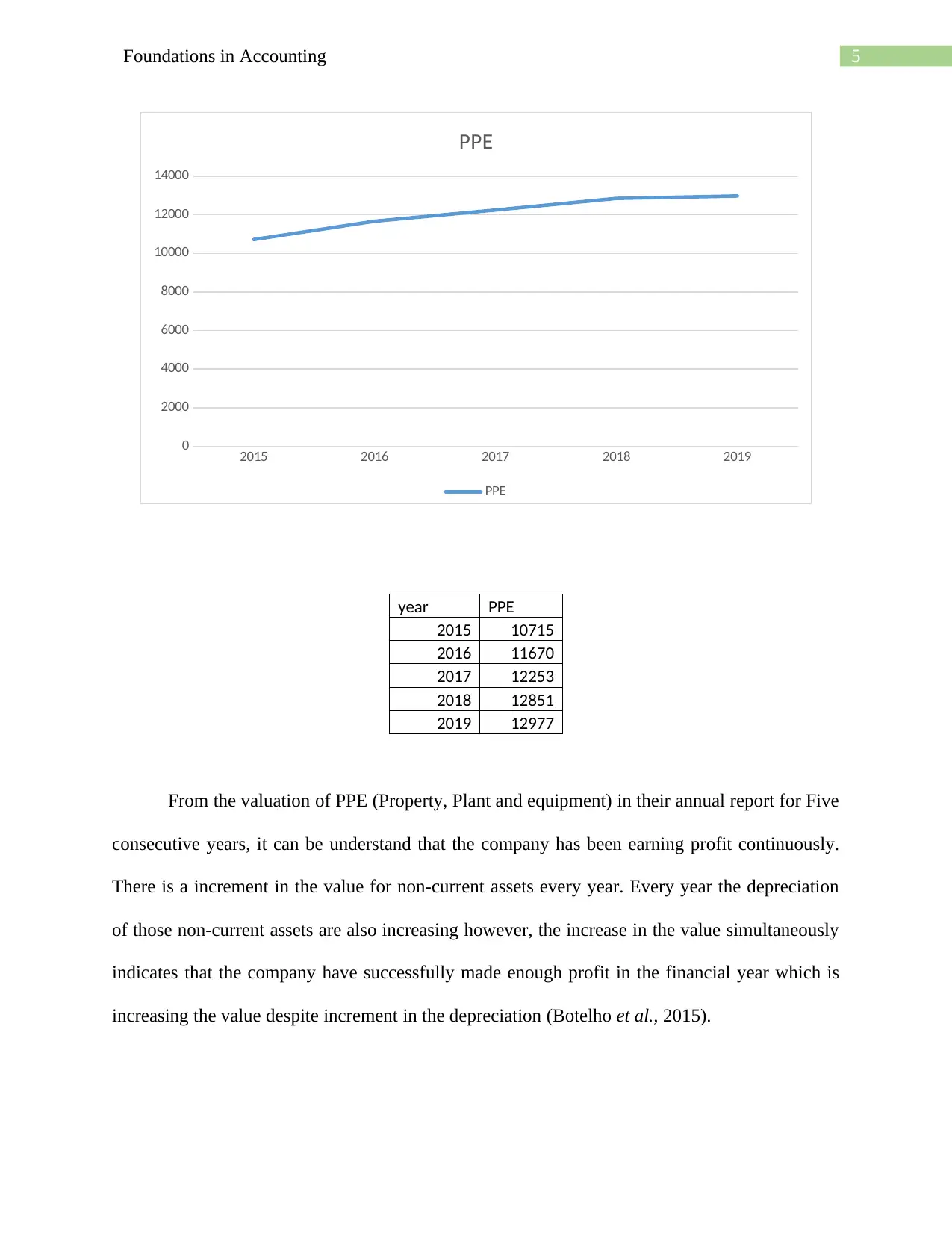

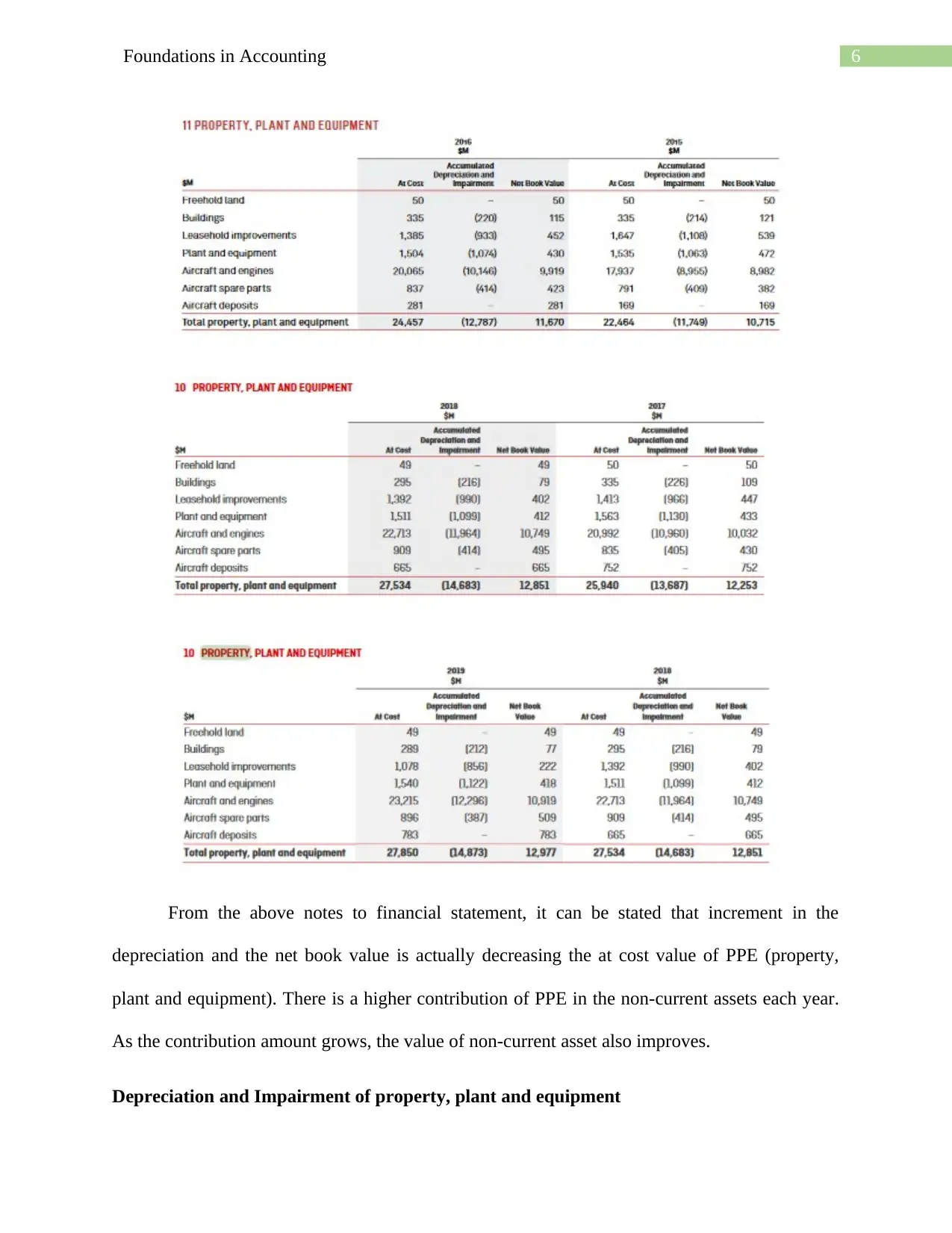

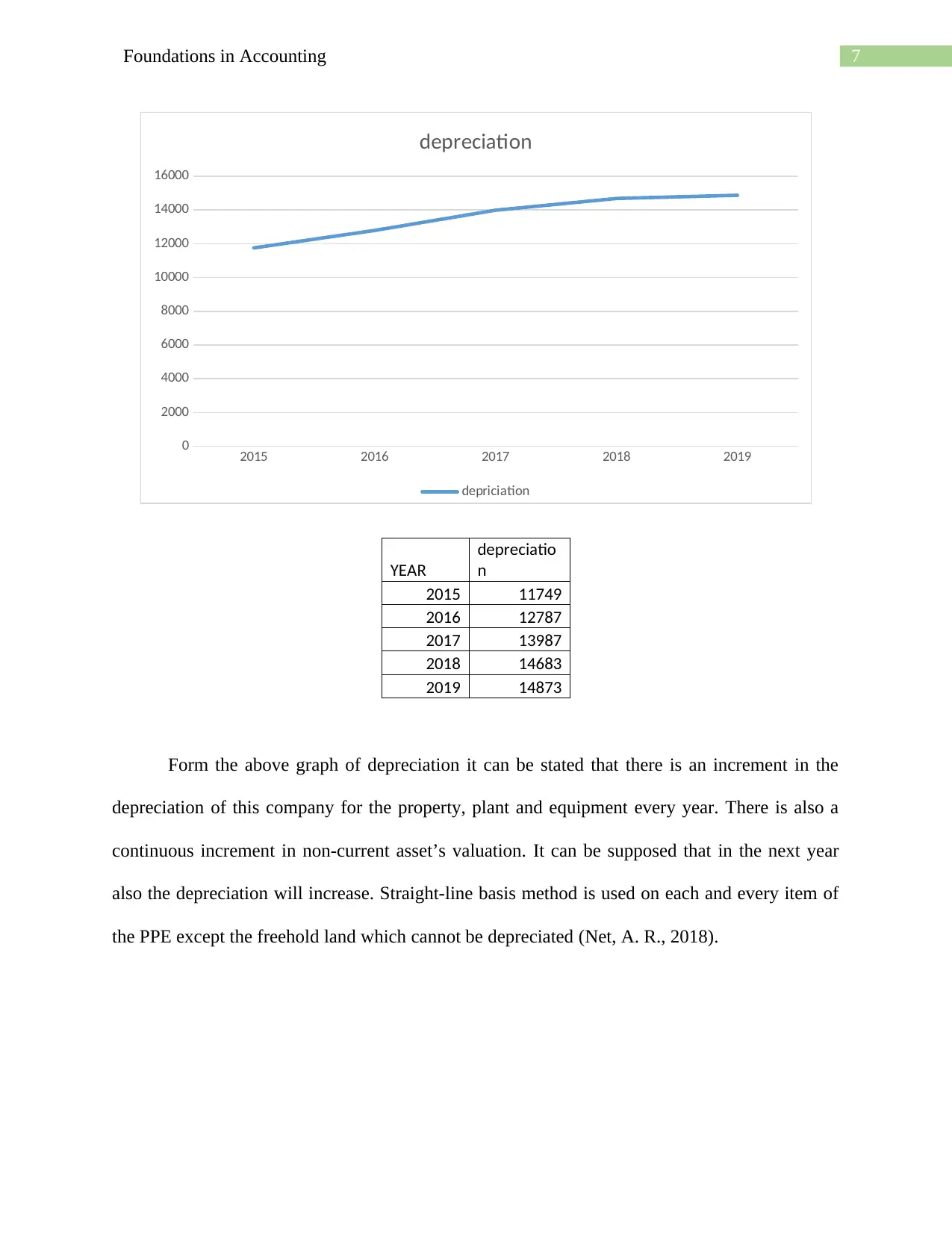

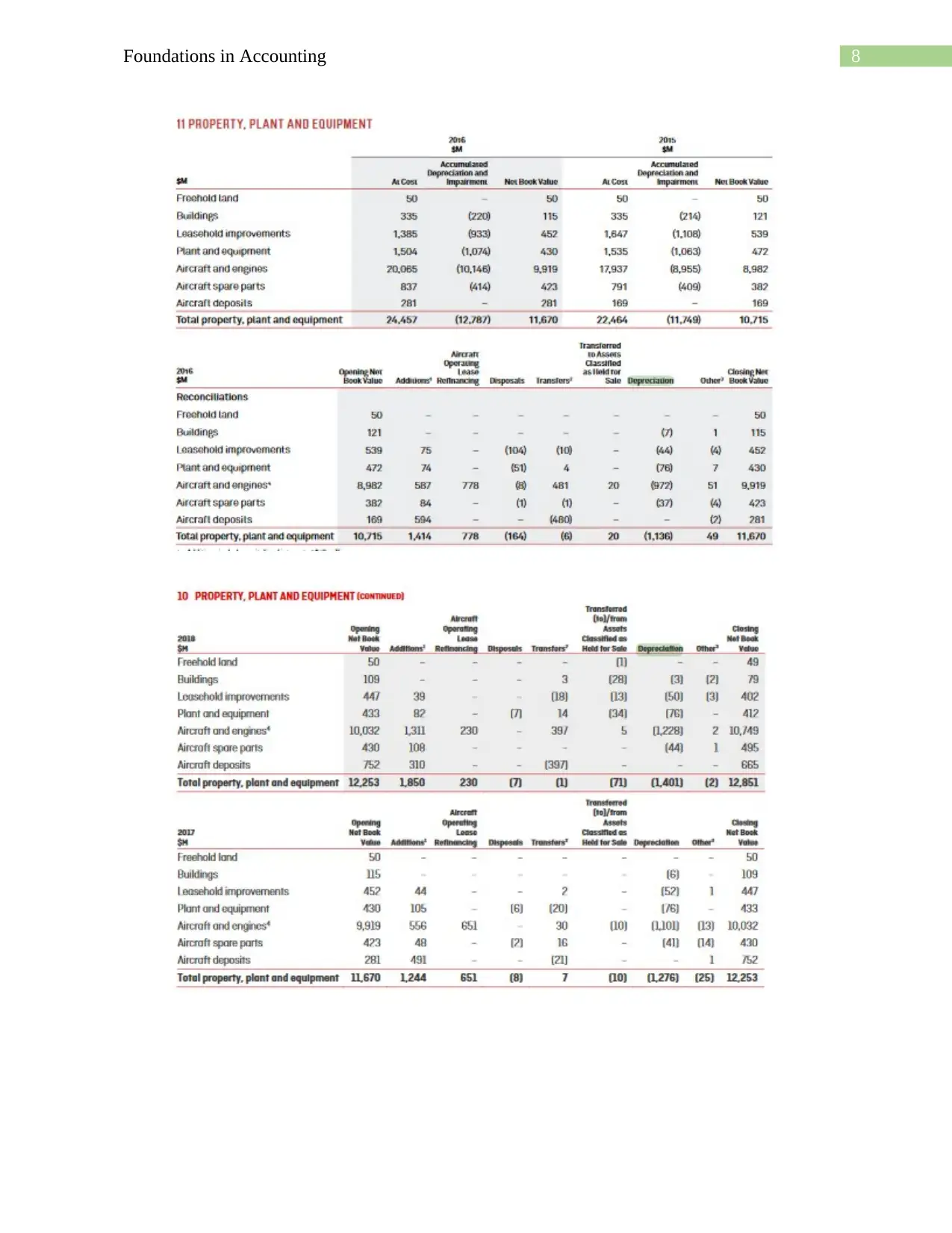

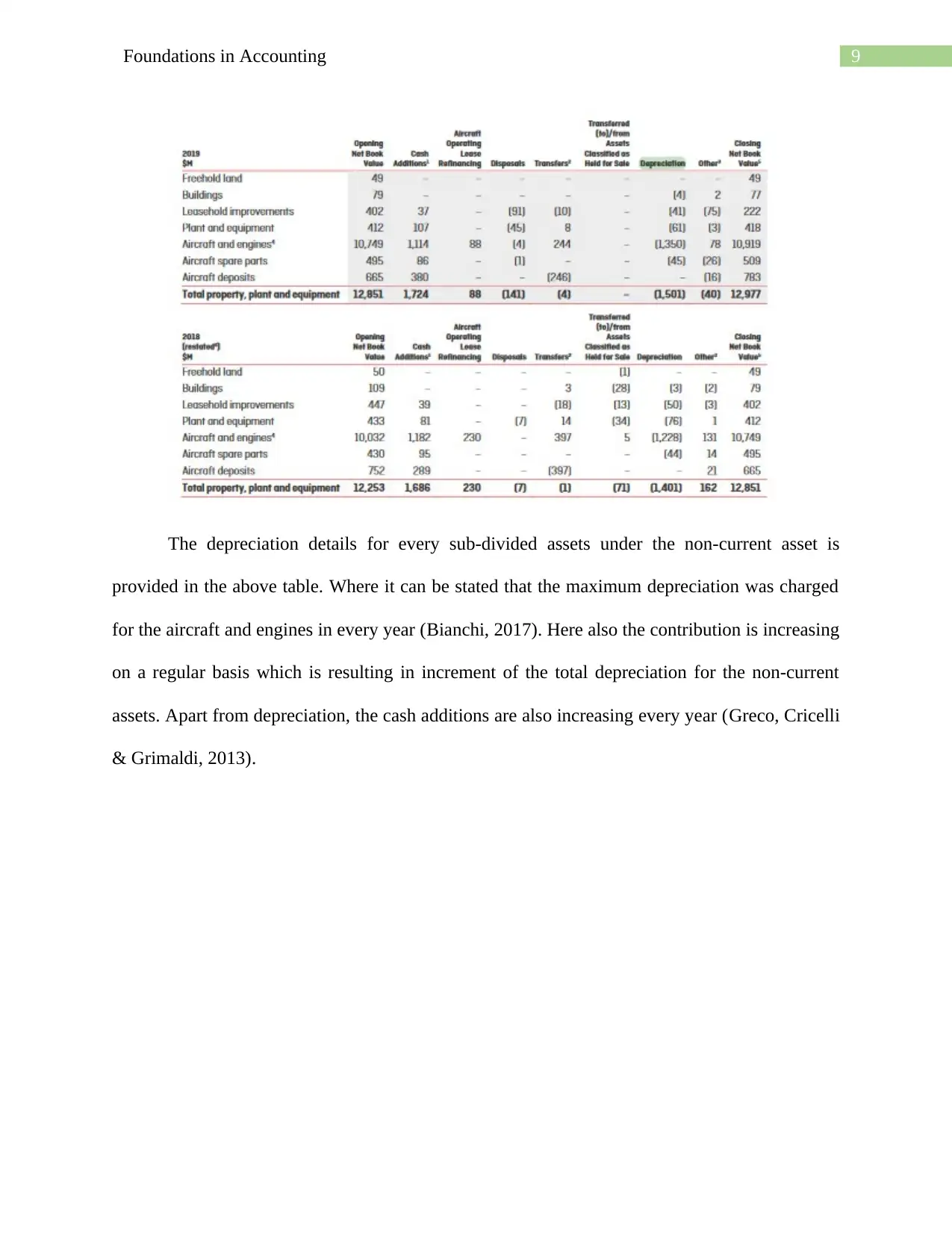

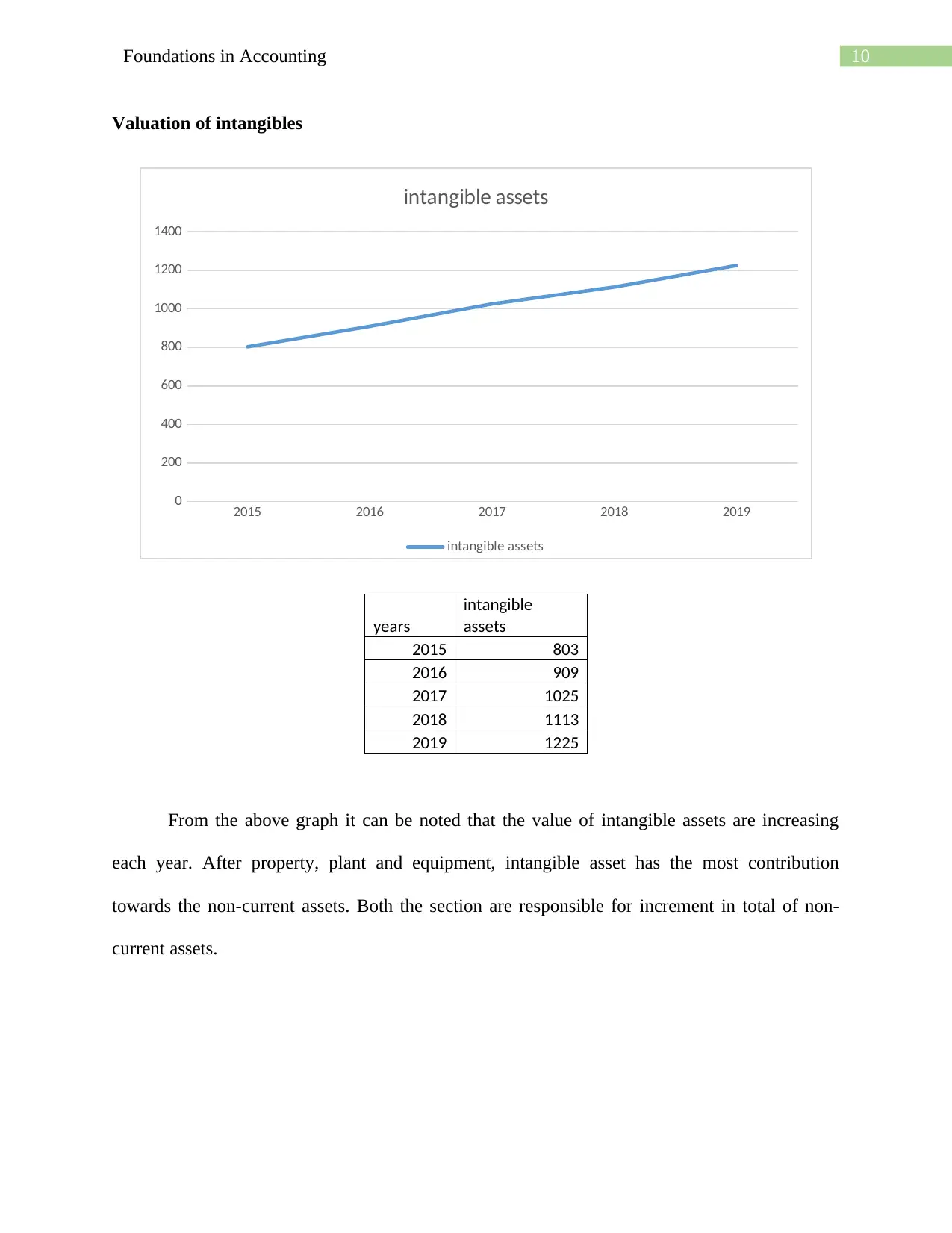

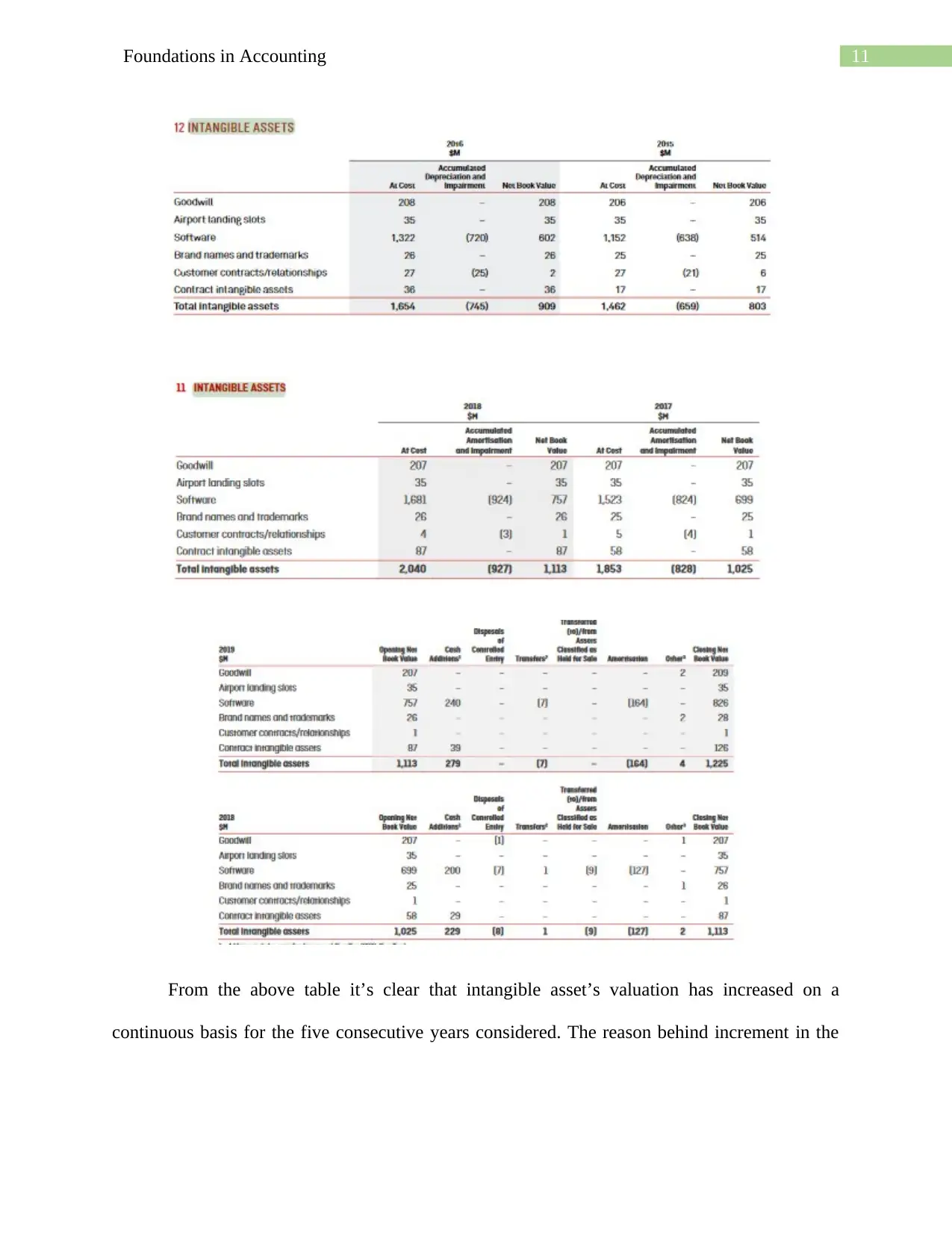

This report provides a comprehensive financial analysis of Qantas Airways, focusing on the valuation and depreciation of its non-current assets from 2015 to 2019. The report begins with a brief overview of Qantas, its industry, and its operational context, including the impact of the COVID-19 pandemic. It then delves into the company's property, plant, and equipment (PPE) and intangible assets, examining their valuation trends and the methods of depreciation and amortization used. The analysis reveals an increasing trend in the value of both PPE and intangible assets, along with corresponding increases in depreciation and amortization expenses. The report highlights the straight-line method used for depreciation and amortization and discusses the implications of these trends on Qantas's financial performance, concluding that despite increased depreciation and amortization, the overall value of the non-current assets has been maintained, indicating the company's growth and market position. The report references relevant accounting standards and financial concepts to support its findings.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.