APO004-6: Financial Analysis and Management of Qantas Airways Plc

VerifiedAdded on 2023/04/21

|12

|3449

|495

Report

AI Summary

This report offers a comprehensive financial analysis of Qantas Airways, an Australian aviation industry leader. It begins by outlining Qantas' corporate objectives and the challenges it faces. The analysis delves into the airline's capital structure and dividend policies, examining their impact on performance over the past three years (2016-2018), with data extracted from its financial statements. Key metrics such as debt-to-equity ratio, return on capital employed, interest cover ratio, and dividend payout ratio are scrutinized to evaluate the effectiveness of Qantas' financial strategies. The report also discusses various investment appraisal tools, including Net Present Value (NPV), Accounting Rate of Return (ARR), and Internal Rate of Return (IRR), that Qantas managers can utilize to ensure investment decisions align with corporate objectives. The document is contributed by a student and available on Desklib.

Running head: FINANCIAL ANALYSIS AND MANAGEMENT

Financial Analysis and Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Analysis and Management

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS AND MANAGEMENT

Table of Contents

Introduction:.......................................................................................................................2

Background to Qantas Airways:........................................................................................2

Capital structure and dividend policy:................................................................................3

Investment appraisal tools:................................................................................................7

Conclusion:........................................................................................................................8

References:......................................................................................................................10

Table of Contents

Introduction:.......................................................................................................................2

Background to Qantas Airways:........................................................................................2

Capital structure and dividend policy:................................................................................3

Investment appraisal tools:................................................................................................7

Conclusion:........................................................................................................................8

References:......................................................................................................................10

2FINANCIAL ANALYSIS AND MANAGEMENT

Introduction:

The current assignment would focus on providing a brief overview of a leading

retail organisation operating in the UK aviation industry, which is Qantas Airways. The

overview of the organisation would be provided in order to identify its key corporate

objectives, which would assist in revealing the type of problems confronted by the

organisation in the recent times. The second section would elaborate the capital

structure policy and dividend policy of Qantas Airways and the ways through which such

policies have affected the performance of the organisation in the past three years.

Finally, the paper would shed light on the tools of investment appraisal used by the

managers for undertaking investment decisions so that assurance could be provided

regarding the fulfilment of the key corporate objectives of the organisation.

Background to Qantas Airways:

Qantas Airways is a leading airline organisation operating in the aviation industry

of Australia. It is mainly engaged in providing passenger services and services related

to freight air transportation in Australia and in other global nations. It provides express

freight and air cargo services to its passengers along with programs related to customer

loyalty. Currently, it has a fleet of 313 aircrafts. The organisation has been established

in 1920 and the headquarter of the airline is located in Mascot, Australia (Qantas.com

2019).

The finance function of Qantas Airways is ascertained as the activities, which

include cash management existing through business. The finance function of the

organisation includes some primary functions, which could support management. Such

finance functions include financial management, financing, capital budgeting and

dividend policy. Firstly, the financing option of Qantas Plc includes raising capital to help

in its operation and investment schemes (Al-Najjar and Kilincarslan 2016). It is termed

as the capital structure, which includes the combination of debt and equity securities for

Introduction:

The current assignment would focus on providing a brief overview of a leading

retail organisation operating in the UK aviation industry, which is Qantas Airways. The

overview of the organisation would be provided in order to identify its key corporate

objectives, which would assist in revealing the type of problems confronted by the

organisation in the recent times. The second section would elaborate the capital

structure policy and dividend policy of Qantas Airways and the ways through which such

policies have affected the performance of the organisation in the past three years.

Finally, the paper would shed light on the tools of investment appraisal used by the

managers for undertaking investment decisions so that assurance could be provided

regarding the fulfilment of the key corporate objectives of the organisation.

Background to Qantas Airways:

Qantas Airways is a leading airline organisation operating in the aviation industry

of Australia. It is mainly engaged in providing passenger services and services related

to freight air transportation in Australia and in other global nations. It provides express

freight and air cargo services to its passengers along with programs related to customer

loyalty. Currently, it has a fleet of 313 aircrafts. The organisation has been established

in 1920 and the headquarter of the airline is located in Mascot, Australia (Qantas.com

2019).

The finance function of Qantas Airways is ascertained as the activities, which

include cash management existing through business. The finance function of the

organisation includes some primary functions, which could support management. Such

finance functions include financial management, financing, capital budgeting and

dividend policy. Firstly, the financing option of Qantas Plc includes raising capital to help

in its operation and investment schemes (Al-Najjar and Kilincarslan 2016). It is termed

as the capital structure, which includes the combination of debt and equity securities for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS AND MANAGEMENT

maximising the market value of the organisation. Thus, Qantas needs to maintain

healthy relationship with its shareholders for raising funds through equity.

Secondly, the financial management of Qantas is to assure that the organisation

has adequate funds on hand for assisting in regular operations. This includes supplier

payments, receiving seasonal funding, collections from customers and investment of

surplus cash (Barr and McClellan 2018). The financial activities need technical,

analytical and individual skills. The individual skills assist in maintaining, developing

relationships with the lenders and suppliers.

Thirdly, capital budgeting of Qantas, which is termed as investment function as

well, includes selecting suitable projects so that funds could be invested depending on

expected risk. Owing to the huge capital investment for prospering in a competitive

market, it is a very critical function for Qantas Plc. Therefore, the main issue that the

organisation might encounter is in dividing the level of investment in small scale for

better management. In opposition, the effect would be adverse on the growth and

development of the organisation (Bekaert and Hodrick 2017).

Finally, it is necessary to maintain sustainable dividend cover in future. This is

because if it is too low, there is a chance that the organisation would not be able to pay

out to its shareholders (Baker and Weigand 2015). Therefore, Qantas needs to maintain

high dividend cover for ensuring the interest of its investors.

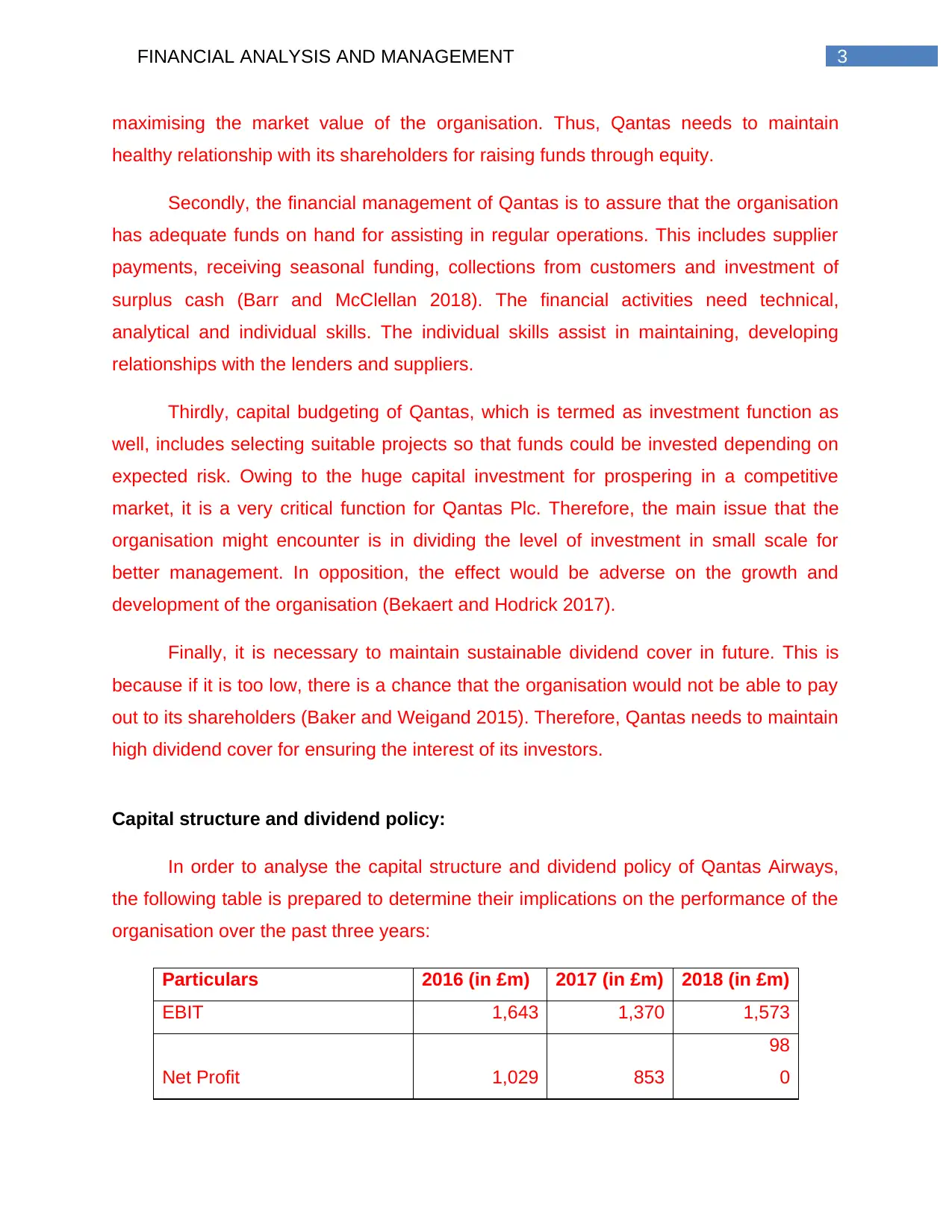

Capital structure and dividend policy:

In order to analyse the capital structure and dividend policy of Qantas Airways,

the following table is prepared to determine their implications on the performance of the

organisation over the past three years:

Particulars 2016 (in £m) 2017 (in £m) 2018 (in £m)

EBIT 1,643 1,370 1,573

Net Profit 1,029 853

98

0

maximising the market value of the organisation. Thus, Qantas needs to maintain

healthy relationship with its shareholders for raising funds through equity.

Secondly, the financial management of Qantas is to assure that the organisation

has adequate funds on hand for assisting in regular operations. This includes supplier

payments, receiving seasonal funding, collections from customers and investment of

surplus cash (Barr and McClellan 2018). The financial activities need technical,

analytical and individual skills. The individual skills assist in maintaining, developing

relationships with the lenders and suppliers.

Thirdly, capital budgeting of Qantas, which is termed as investment function as

well, includes selecting suitable projects so that funds could be invested depending on

expected risk. Owing to the huge capital investment for prospering in a competitive

market, it is a very critical function for Qantas Plc. Therefore, the main issue that the

organisation might encounter is in dividing the level of investment in small scale for

better management. In opposition, the effect would be adverse on the growth and

development of the organisation (Bekaert and Hodrick 2017).

Finally, it is necessary to maintain sustainable dividend cover in future. This is

because if it is too low, there is a chance that the organisation would not be able to pay

out to its shareholders (Baker and Weigand 2015). Therefore, Qantas needs to maintain

high dividend cover for ensuring the interest of its investors.

Capital structure and dividend policy:

In order to analyse the capital structure and dividend policy of Qantas Airways,

the following table is prepared to determine their implications on the performance of the

organisation over the past three years:

Particulars 2016 (in £m) 2017 (in £m) 2018 (in £m)

EBIT 1,643 1,370 1,573

Net Profit 1,029 853

98

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

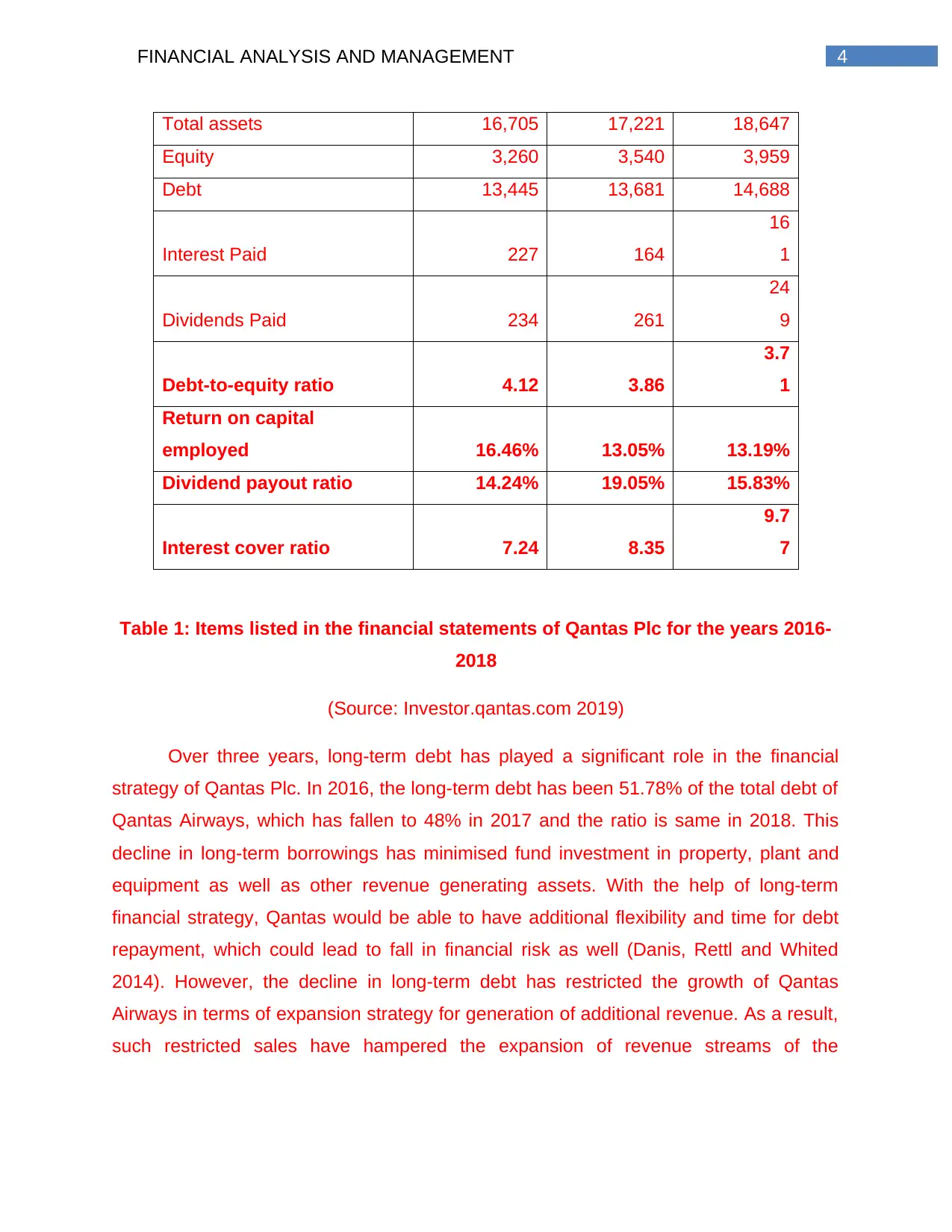

4FINANCIAL ANALYSIS AND MANAGEMENT

Total assets 16,705 17,221 18,647

Equity 3,260 3,540 3,959

Debt 13,445 13,681 14,688

Interest Paid 227 164

16

1

Dividends Paid 234 261

24

9

Debt-to-equity ratio 4.12 3.86

3.7

1

Return on capital

employed 16.46% 13.05% 13.19%

Dividend payout ratio 14.24% 19.05% 15.83%

Interest cover ratio 7.24 8.35

9.7

7

Table 1: Items listed in the financial statements of Qantas Plc for the years 2016-

2018

(Source: Investor.qantas.com 2019)

Over three years, long-term debt has played a significant role in the financial

strategy of Qantas Plc. In 2016, the long-term debt has been 51.78% of the total debt of

Qantas Airways, which has fallen to 48% in 2017 and the ratio is same in 2018. This

decline in long-term borrowings has minimised fund investment in property, plant and

equipment as well as other revenue generating assets. With the help of long-term

financial strategy, Qantas would be able to have additional flexibility and time for debt

repayment, which could lead to fall in financial risk as well (Danis, Rettl and Whited

2014). However, the decline in long-term debt has restricted the growth of Qantas

Airways in terms of expansion strategy for generation of additional revenue. As a result,

such restricted sales have hampered the expansion of revenue streams of the

Total assets 16,705 17,221 18,647

Equity 3,260 3,540 3,959

Debt 13,445 13,681 14,688

Interest Paid 227 164

16

1

Dividends Paid 234 261

24

9

Debt-to-equity ratio 4.12 3.86

3.7

1

Return on capital

employed 16.46% 13.05% 13.19%

Dividend payout ratio 14.24% 19.05% 15.83%

Interest cover ratio 7.24 8.35

9.7

7

Table 1: Items listed in the financial statements of Qantas Plc for the years 2016-

2018

(Source: Investor.qantas.com 2019)

Over three years, long-term debt has played a significant role in the financial

strategy of Qantas Plc. In 2016, the long-term debt has been 51.78% of the total debt of

Qantas Airways, which has fallen to 48% in 2017 and the ratio is same in 2018. This

decline in long-term borrowings has minimised fund investment in property, plant and

equipment as well as other revenue generating assets. With the help of long-term

financial strategy, Qantas would be able to have additional flexibility and time for debt

repayment, which could lead to fall in financial risk as well (Danis, Rettl and Whited

2014). However, the decline in long-term debt has restricted the growth of Qantas

Airways in terms of expansion strategy for generation of additional revenue. As a result,

such restricted sales have hampered the expansion of revenue streams of the

5FINANCIAL ANALYSIS AND MANAGEMENT

organisation, which would minimise long-term sustainability and thus, business risk has

increased.

On the other hand, short-term liabilities are observed to be increased over the

years for Qantas Airways owing to increase in trade payables and unearned revenue.

Such rise would reduce financial flexibility coupled with staggering market growth and

tough trading conditions. This policy, if continued, would restrict long-term growth and

flexibility. Therefore, Qantas Airways needs to undertake corrective measures for

improving the debt position over the long-term in order to minimise its financial risk.

In terms of equity, it could be observed that the total equity of the organisation

has increased by 8.59% in 2017 and by 11.84% in 2018 compared to the previous

years. This clearly implies that Qantas Airways has been focusing on raising more funds

through issuing new equity shares in the market rather than undertaking loans from

banks and other financial institutions. However, the debt level of the organisation has

increased over time and recent rise in debt level could be related to funding of new

revenue generating assets like purchase of new fleets as well as other relevant

property, plant and equipment. As such, when these assets reach their entire operating

capacity, there would be decline in debt-to-equity ratio with the progress of time.

On the other hand, it is seen that both EBIT and net profit of Qantas Airways

have fallen from 2016 to 2017 considerably owing to rise in operating expenses;

however, slight improvement could be observed in the year 2018. This would have

adverse impact on return on capital employed, which is not attractive to long-term

investors planning to base their returns on increased dividend yields through raising

capital value (Belo, Collin‐Dufresne and Goldstein 2015). Moreover, with the fall in

return on capital employed in comparison to 2016, both liabilities and equity of the

organisation are observed to increase over three-year period. This implies that Qantas

Plc has not invested additional funds appropriately in revenue generating assets for

maintaining stable return.

In current years, there has been increase in both long-term cost of debt as well

as cost of equity, which has lead to rise in cost of capital (Faccio and Xu 2015).

organisation, which would minimise long-term sustainability and thus, business risk has

increased.

On the other hand, short-term liabilities are observed to be increased over the

years for Qantas Airways owing to increase in trade payables and unearned revenue.

Such rise would reduce financial flexibility coupled with staggering market growth and

tough trading conditions. This policy, if continued, would restrict long-term growth and

flexibility. Therefore, Qantas Airways needs to undertake corrective measures for

improving the debt position over the long-term in order to minimise its financial risk.

In terms of equity, it could be observed that the total equity of the organisation

has increased by 8.59% in 2017 and by 11.84% in 2018 compared to the previous

years. This clearly implies that Qantas Airways has been focusing on raising more funds

through issuing new equity shares in the market rather than undertaking loans from

banks and other financial institutions. However, the debt level of the organisation has

increased over time and recent rise in debt level could be related to funding of new

revenue generating assets like purchase of new fleets as well as other relevant

property, plant and equipment. As such, when these assets reach their entire operating

capacity, there would be decline in debt-to-equity ratio with the progress of time.

On the other hand, it is seen that both EBIT and net profit of Qantas Airways

have fallen from 2016 to 2017 considerably owing to rise in operating expenses;

however, slight improvement could be observed in the year 2018. This would have

adverse impact on return on capital employed, which is not attractive to long-term

investors planning to base their returns on increased dividend yields through raising

capital value (Belo, Collin‐Dufresne and Goldstein 2015). Moreover, with the fall in

return on capital employed in comparison to 2016, both liabilities and equity of the

organisation are observed to increase over three-year period. This implies that Qantas

Plc has not invested additional funds appropriately in revenue generating assets for

maintaining stable return.

In current years, there has been increase in both long-term cost of debt as well

as cost of equity, which has lead to rise in cost of capital (Faccio and Xu 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS AND MANAGEMENT

However, stability could be observed owing to the rising costs of maintaining equity,

which is offset by lower cost of debt. On the other hand, these costs might not remain

stable for future as long as debt-to-equity ratio remains stable. In this case, debt-to-

equity ratio is observed to decline from 4.46 in 2016 to 3.71 in 2018 for Qantas Plc,

which is well above the ideal standard of 1. Hence, this has increased the bankruptcy

risk and financial risk along with raising its cost of equity. However, if the debt is made

up of short-term debt, this would free the existing interest rate for greater timeframe.

Hence, Qantas Airways needs to undertake corrective actions as soon as possible

(Finkler, Smith and Calabrese 2019).

In terms of interest cover ratio, the ratio has increased from 7.24 in 2016 to 8.35

in 2017, which has increased further to 9.77 in 2018 for Qantas Airways. This implies

that the existing business model of the organisation has been effective with no

corrective actions required. This has minimised the potential for threats of the

organisation, as it has been highly effective in cover its finance cost with the help of

operating income.

From the above table, it could be seen that the dividend payout ratio of Qantas

Airways has risen from 14.24% in 2016 to 19.05% in 2017; however, it has fallen to

15.83% in 2018. As commented by Fairchild, Guney and Thanatawee (2014), dividend

payout ratio gauges the percentage of net income, which is distributed to the

shareholders of an organisation as dividends during the year. The investors want to

gain information about dividend payout ratio to know if the organisation pays a

reasonable portion of net profit to the investors. It has been identified that Qantas Plc

has been paying increased dividends to its shareholders over the years.

This kind of dividend policy is more appealing for the long-term investors like

pension funds. This is owing to their desire for high dividend paying investments with

little requirements of cash out. Hence, significant changes in stock prices might not be

an overwhelming factor in the process of decision making (McKinney 2015). On the

other hand, short-term investors would not be satisfied with this type of policy, as they

desire for increased capital growth rather than dividend payments. Hence, Qantas

Airways is considering the interests of its long-term investors for raising maximum funds

However, stability could be observed owing to the rising costs of maintaining equity,

which is offset by lower cost of debt. On the other hand, these costs might not remain

stable for future as long as debt-to-equity ratio remains stable. In this case, debt-to-

equity ratio is observed to decline from 4.46 in 2016 to 3.71 in 2018 for Qantas Plc,

which is well above the ideal standard of 1. Hence, this has increased the bankruptcy

risk and financial risk along with raising its cost of equity. However, if the debt is made

up of short-term debt, this would free the existing interest rate for greater timeframe.

Hence, Qantas Airways needs to undertake corrective actions as soon as possible

(Finkler, Smith and Calabrese 2019).

In terms of interest cover ratio, the ratio has increased from 7.24 in 2016 to 8.35

in 2017, which has increased further to 9.77 in 2018 for Qantas Airways. This implies

that the existing business model of the organisation has been effective with no

corrective actions required. This has minimised the potential for threats of the

organisation, as it has been highly effective in cover its finance cost with the help of

operating income.

From the above table, it could be seen that the dividend payout ratio of Qantas

Airways has risen from 14.24% in 2016 to 19.05% in 2017; however, it has fallen to

15.83% in 2018. As commented by Fairchild, Guney and Thanatawee (2014), dividend

payout ratio gauges the percentage of net income, which is distributed to the

shareholders of an organisation as dividends during the year. The investors want to

gain information about dividend payout ratio to know if the organisation pays a

reasonable portion of net profit to the investors. It has been identified that Qantas Plc

has been paying increased dividends to its shareholders over the years.

This kind of dividend policy is more appealing for the long-term investors like

pension funds. This is owing to their desire for high dividend paying investments with

little requirements of cash out. Hence, significant changes in stock prices might not be

an overwhelming factor in the process of decision making (McKinney 2015). On the

other hand, short-term investors would not be satisfied with this type of policy, as they

desire for increased capital growth rather than dividend payments. Hence, Qantas

Airways is considering the interests of its long-term investors for raising maximum funds

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS AND MANAGEMENT

at cheaper cost along with the signalling effects. Based on this evaluation, it could be

stated that Qantas Airways has maintained stable dividend policy by paying increased

dividends to its shareholders with no corrective measures needed.

Investment appraisal tools:

There are various investment appraisal techniques that the managers of Qantas

Plc could use for ensuring that the corporate objectives are met and they are

demonstrated briefly as follows:

Net present value (NPV):

This technique gauges the cash inflow whether shortfall or excess after meeting

the routine finance commitments. All capital investment appraisals have only one

objective, which is driving towards a positive NPV (Andor, Mohanty and Toth 2015). The

managers of Qantas Airways could utilise this technique by involving net cash flow at a

specific present time and a specific discount rate. This implies that there is inverse

association between NPV and discount rate. If the discount rate is high, it could

minimise the NPV of capital for Qantas Plc. An increased interest rate might increase

discount rate over a timeframe and therefore, the managers need to be wary of such

increase in order to ensure the fulfilment of the corporate objectives of the organisation.

Accounting rate of return (ARR):

This method of capital investment appraisal contrasts the profit that could be

made by the concerned project to the initial investment amount, which would be needed

for the project. In case, when the managers have a number of projects for evaluation,

the ones providing increased rate of return would be preferred over ones having lower

rate of return. However, this method is a non-discounted technique of capital budgeting

in that it fails to take into account the time value of money (Daunfeldt and Hartwig

2014). Therefore, the managers of Qantas Airways need to take into consideration the

other factors as well for ensuring that the corporate objectives of the organisation are

met.

at cheaper cost along with the signalling effects. Based on this evaluation, it could be

stated that Qantas Airways has maintained stable dividend policy by paying increased

dividends to its shareholders with no corrective measures needed.

Investment appraisal tools:

There are various investment appraisal techniques that the managers of Qantas

Plc could use for ensuring that the corporate objectives are met and they are

demonstrated briefly as follows:

Net present value (NPV):

This technique gauges the cash inflow whether shortfall or excess after meeting

the routine finance commitments. All capital investment appraisals have only one

objective, which is driving towards a positive NPV (Andor, Mohanty and Toth 2015). The

managers of Qantas Airways could utilise this technique by involving net cash flow at a

specific present time and a specific discount rate. This implies that there is inverse

association between NPV and discount rate. If the discount rate is high, it could

minimise the NPV of capital for Qantas Plc. An increased interest rate might increase

discount rate over a timeframe and therefore, the managers need to be wary of such

increase in order to ensure the fulfilment of the corporate objectives of the organisation.

Accounting rate of return (ARR):

This method of capital investment appraisal contrasts the profit that could be

made by the concerned project to the initial investment amount, which would be needed

for the project. In case, when the managers have a number of projects for evaluation,

the ones providing increased rate of return would be preferred over ones having lower

rate of return. However, this method is a non-discounted technique of capital budgeting

in that it fails to take into account the time value of money (Daunfeldt and Hartwig

2014). Therefore, the managers of Qantas Airways need to take into consideration the

other factors as well for ensuring that the corporate objectives of the organisation are

met.

8FINANCIAL ANALYSIS AND MANAGEMENT

Internal rate of return (IRR):

Internal rate of return is defined as the rate of discount, which provides no value

to NPV. Among all the techniques of capital investment appraisal, IRR is primarily taken

into account for measuring the efficacy of capital investment (Wang 2014). Therefore, if

the investment related to cost of capital is found to be more than the value of IRR, the

project need not be accepted by the managers of Qantas Airways. On the other hand, a

project having low cost of capital has increased chances of acceptance (De Andrés, De

Fuente and San Martín 2015). Hence, when a positive IRR is found in a project, the

managers of the organisation would accept the project, as it would assist in maximising

the profitability by fulfilling its corporate objectives.

Payback period:

This method is involved in appraising capital investment based on time, which

would be required for regaining initial investment made (Mwangi, Makau and Kosimbei

2014). It is one of the easiest techniques of capital investment appraisal. If the

managers of Qantas Airways find projects with a shorter payback period, they would be

preferred for investment in contrast to the ones having longer payback periods. If the

managers find payback period to be more than the useful life of the project, the project

should be rejected. In opposition, it would minimise the profitability of the organisation,

which would have unfavourable impact on the corporate goals of the organisation

(Rossi 2014).

Profitability index:

This method of capital budgeting is involved in analysing a project depending on

computation of value per unit of investment (Rossi 2015). This method is termed as

profit investment or value investment ratio. This method is a ratio of amount of money

invested to profit or project payoff. At the time of undertaking a project, the managers of

Qantas Airways need to evaluate whether the index is above or below 1. If it is above 1,

the project could be accepted and vice-versa. Thus, this technique would assist the

organisation in fulfilling its corporate objectives (Zietlow et al. 2018).

Internal rate of return (IRR):

Internal rate of return is defined as the rate of discount, which provides no value

to NPV. Among all the techniques of capital investment appraisal, IRR is primarily taken

into account for measuring the efficacy of capital investment (Wang 2014). Therefore, if

the investment related to cost of capital is found to be more than the value of IRR, the

project need not be accepted by the managers of Qantas Airways. On the other hand, a

project having low cost of capital has increased chances of acceptance (De Andrés, De

Fuente and San Martín 2015). Hence, when a positive IRR is found in a project, the

managers of the organisation would accept the project, as it would assist in maximising

the profitability by fulfilling its corporate objectives.

Payback period:

This method is involved in appraising capital investment based on time, which

would be required for regaining initial investment made (Mwangi, Makau and Kosimbei

2014). It is one of the easiest techniques of capital investment appraisal. If the

managers of Qantas Airways find projects with a shorter payback period, they would be

preferred for investment in contrast to the ones having longer payback periods. If the

managers find payback period to be more than the useful life of the project, the project

should be rejected. In opposition, it would minimise the profitability of the organisation,

which would have unfavourable impact on the corporate goals of the organisation

(Rossi 2014).

Profitability index:

This method of capital budgeting is involved in analysing a project depending on

computation of value per unit of investment (Rossi 2015). This method is termed as

profit investment or value investment ratio. This method is a ratio of amount of money

invested to profit or project payoff. At the time of undertaking a project, the managers of

Qantas Airways need to evaluate whether the index is above or below 1. If it is above 1,

the project could be accepted and vice-versa. Thus, this technique would assist the

organisation in fulfilling its corporate objectives (Zietlow et al. 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS AND MANAGEMENT

Conclusion:

Based on the above discussion, it could be found that the decline in long-term

debt has restricted the growth of Qantas Airways in global expansion. As a result, such

restricted sales have hampered the expansion of revenue streams of the organisation,

which would minimise long-term sustainability and thus, business risk has increased. In

current years, there has been increase in both long-term cost of debt as well as cost of

equity, which has lead to rise in cost of capital. However, stability could be observed

owing to the rising costs of maintaining equity, which is offset by lower cost of debt. On

the other hand, these costs might not remain stable for future as long as debt-to-equity

ratio remains stable. In this case, debt-to-equity ratio is observed to increase from 1.67

in 2016 to 1.97 in 2018 for Qantas Airways. Hence, this has increased the bankruptcy

risk and financial risk along with raising its cost of equity. However, if the debt is made

up of short-term debt, this would free the existing interest rate for greater timeframe.

Hence, Qantas Airways needs to undertake corrective actions as soon as possible

Conclusion:

Based on the above discussion, it could be found that the decline in long-term

debt has restricted the growth of Qantas Airways in global expansion. As a result, such

restricted sales have hampered the expansion of revenue streams of the organisation,

which would minimise long-term sustainability and thus, business risk has increased. In

current years, there has been increase in both long-term cost of debt as well as cost of

equity, which has lead to rise in cost of capital. However, stability could be observed

owing to the rising costs of maintaining equity, which is offset by lower cost of debt. On

the other hand, these costs might not remain stable for future as long as debt-to-equity

ratio remains stable. In this case, debt-to-equity ratio is observed to increase from 1.67

in 2016 to 1.97 in 2018 for Qantas Airways. Hence, this has increased the bankruptcy

risk and financial risk along with raising its cost of equity. However, if the debt is made

up of short-term debt, this would free the existing interest rate for greater timeframe.

Hence, Qantas Airways needs to undertake corrective actions as soon as possible

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS AND MANAGEMENT

References:

Investor.qantas.com., 2019. Qantas Investors | Investor Centre. [online] Available at:

https://investor.qantas.com/investors/?page=annual-reports [Accessed 13 Jan. 2019].

Qantas.com., 2019. Fly with Australia’s most popular airline | Qantas AU. [online]

Available at: https://www.qantas.com/au/en.html [Accessed 13 Jan. 2019].

Al-Najjar, B. and Kilincarslan, E., 2016. The effect of ownership structure on dividend

policy: Evidence from Turkey. Corporate Governance: The international journal of

business in society, 16(1), pp.135-161.

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of

Central and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Baker, H.K. and Weigand, R., 2015. Corporate dividend policy revisited. Managerial

Finance, 41(2), pp.126-144.

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher

education. John Wiley & Sons.

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge

University Press.

Belo, F., Collin‐Dufresne, P. and Goldstein, R.S., 2015. Dividend dynamics and the term

structure of dividend strips. The Journal of Finance, 70(3), pp.1115-1160.

Danis, A., Rettl, D.A. and Whited, T.M., 2014. Refinancing, profitability, and capital

structure. Journal of Financial Economics, 114(3), pp.424-443.

Daunfeldt, S.O. and Hartwig, F., 2014. What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4), pp.101-112.

De Andrés, P., De Fuente, G. and San Martín, P., 2015. Capital budgeting practices in

Spain. BRQ Business Research Quarterly, 18(1), pp.37-56.

References:

Investor.qantas.com., 2019. Qantas Investors | Investor Centre. [online] Available at:

https://investor.qantas.com/investors/?page=annual-reports [Accessed 13 Jan. 2019].

Qantas.com., 2019. Fly with Australia’s most popular airline | Qantas AU. [online]

Available at: https://www.qantas.com/au/en.html [Accessed 13 Jan. 2019].

Al-Najjar, B. and Kilincarslan, E., 2016. The effect of ownership structure on dividend

policy: Evidence from Turkey. Corporate Governance: The international journal of

business in society, 16(1), pp.135-161.

Andor, G., Mohanty, S.K. and Toth, T., 2015. Capital budgeting practices: A survey of

Central and Eastern European firms. Emerging Markets Review, 23, pp.148-172.

Baker, H.K. and Weigand, R., 2015. Corporate dividend policy revisited. Managerial

Finance, 41(2), pp.126-144.

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher

education. John Wiley & Sons.

Bekaert, G. and Hodrick, R., 2017. International financial management. Cambridge

University Press.

Belo, F., Collin‐Dufresne, P. and Goldstein, R.S., 2015. Dividend dynamics and the term

structure of dividend strips. The Journal of Finance, 70(3), pp.1115-1160.

Danis, A., Rettl, D.A. and Whited, T.M., 2014. Refinancing, profitability, and capital

structure. Journal of Financial Economics, 114(3), pp.424-443.

Daunfeldt, S.O. and Hartwig, F., 2014. What determines the use of capital budgeting

methods?: Evidence from Swedish listed companies. Journal of Finance and

Economics, 2(4), pp.101-112.

De Andrés, P., De Fuente, G. and San Martín, P., 2015. Capital budgeting practices in

Spain. BRQ Business Research Quarterly, 18(1), pp.37-56.

11FINANCIAL ANALYSIS AND MANAGEMENT

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Fairchild, R., Guney, Y. and Thanatawee, Y., 2014. Corporate dividend policy in

Thailand: Theory and evidence. International Review of Financial Analysis, 31, pp.129-

151.

Finkler, S.A., Smith, D.L. and Calabrese, T.D., 2019. Financial management for public,

health, and not-for-profit organizations. CQ Press.

McKinney, J.B., 2015. Effective financial management in public and nonprofit agencies.

ABC-CLIO.

Mwangi, L.W., Makau, M.S. and Kosimbei, G., 2014. Relationship between capital

structure and performance of non-financial companies listed in the Nairobi Securities

Exchange, Kenya. Global Journal of Contemporary Research in Accounting, Auditing

and Business Ethics, 1(2), pp.72-90.

Rossi, M., 2014. Capital budgeting in Europe: confronting theory with

practice. International Journal of Managerial and Financial Accounting, 6(4), pp.341-

356.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from

Italy. International Journal of Management Practice, 8(1), pp.43-56.

Wang, X.S., 2014. Financial management in the public sector: tools, applications and

cases. Routledge.

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for

nonprofit organizations: Policies and practices. John Wiley & Sons.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Fairchild, R., Guney, Y. and Thanatawee, Y., 2014. Corporate dividend policy in

Thailand: Theory and evidence. International Review of Financial Analysis, 31, pp.129-

151.

Finkler, S.A., Smith, D.L. and Calabrese, T.D., 2019. Financial management for public,

health, and not-for-profit organizations. CQ Press.

McKinney, J.B., 2015. Effective financial management in public and nonprofit agencies.

ABC-CLIO.

Mwangi, L.W., Makau, M.S. and Kosimbei, G., 2014. Relationship between capital

structure and performance of non-financial companies listed in the Nairobi Securities

Exchange, Kenya. Global Journal of Contemporary Research in Accounting, Auditing

and Business Ethics, 1(2), pp.72-90.

Rossi, M., 2014. Capital budgeting in Europe: confronting theory with

practice. International Journal of Managerial and Financial Accounting, 6(4), pp.341-

356.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from

Italy. International Journal of Management Practice, 8(1), pp.43-56.

Wang, X.S., 2014. Financial management in the public sector: tools, applications and

cases. Routledge.

Zietlow, J., Hankin, J.A., Seidner, A. and O'Brien, T., 2018. Financial management for

nonprofit organizations: Policies and practices. John Wiley & Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.