Accounting for Managers: Financial Analysis, RFG Case Study

VerifiedAdded on 2023/06/05

|11

|1333

|99

Report

AI Summary

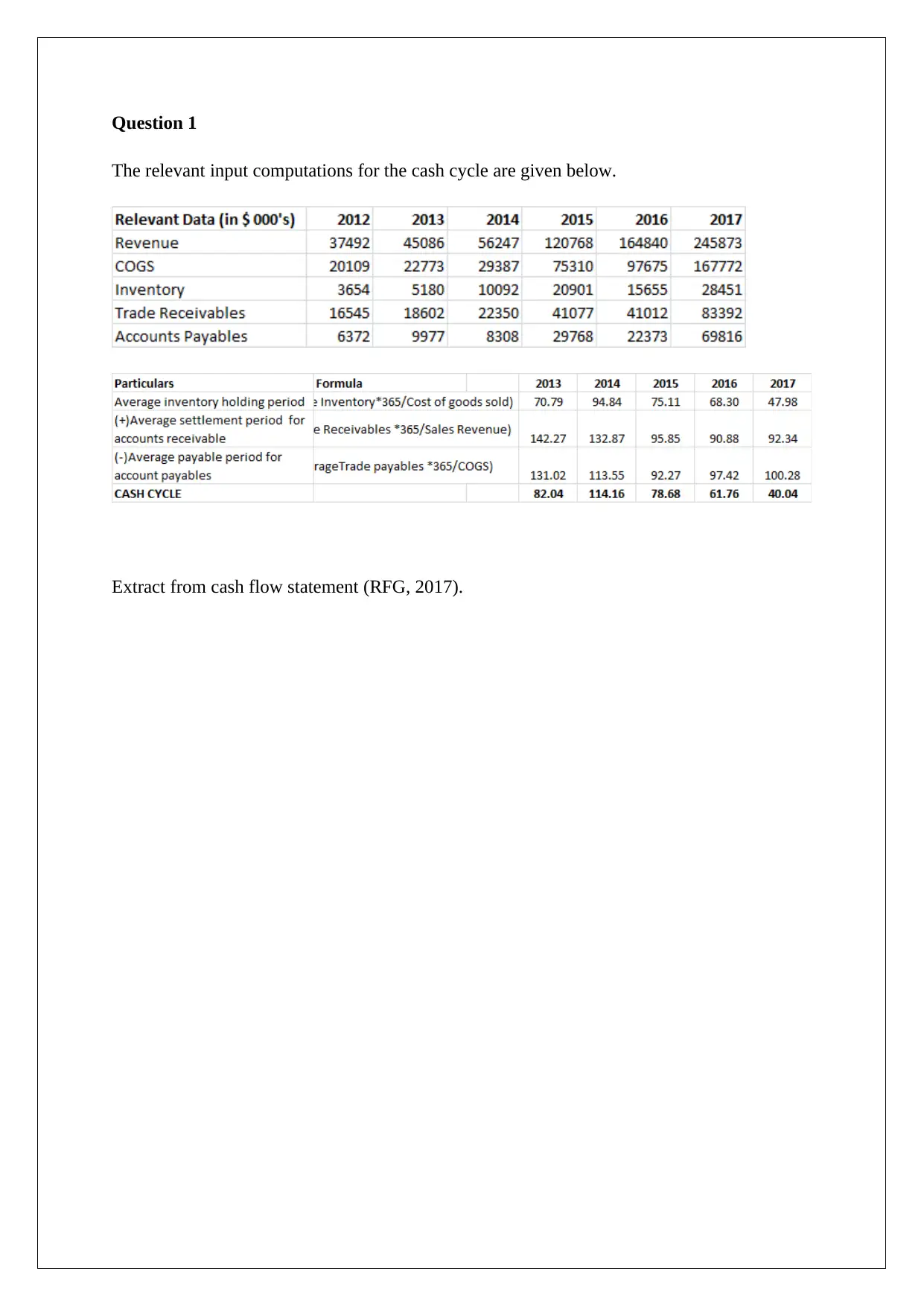

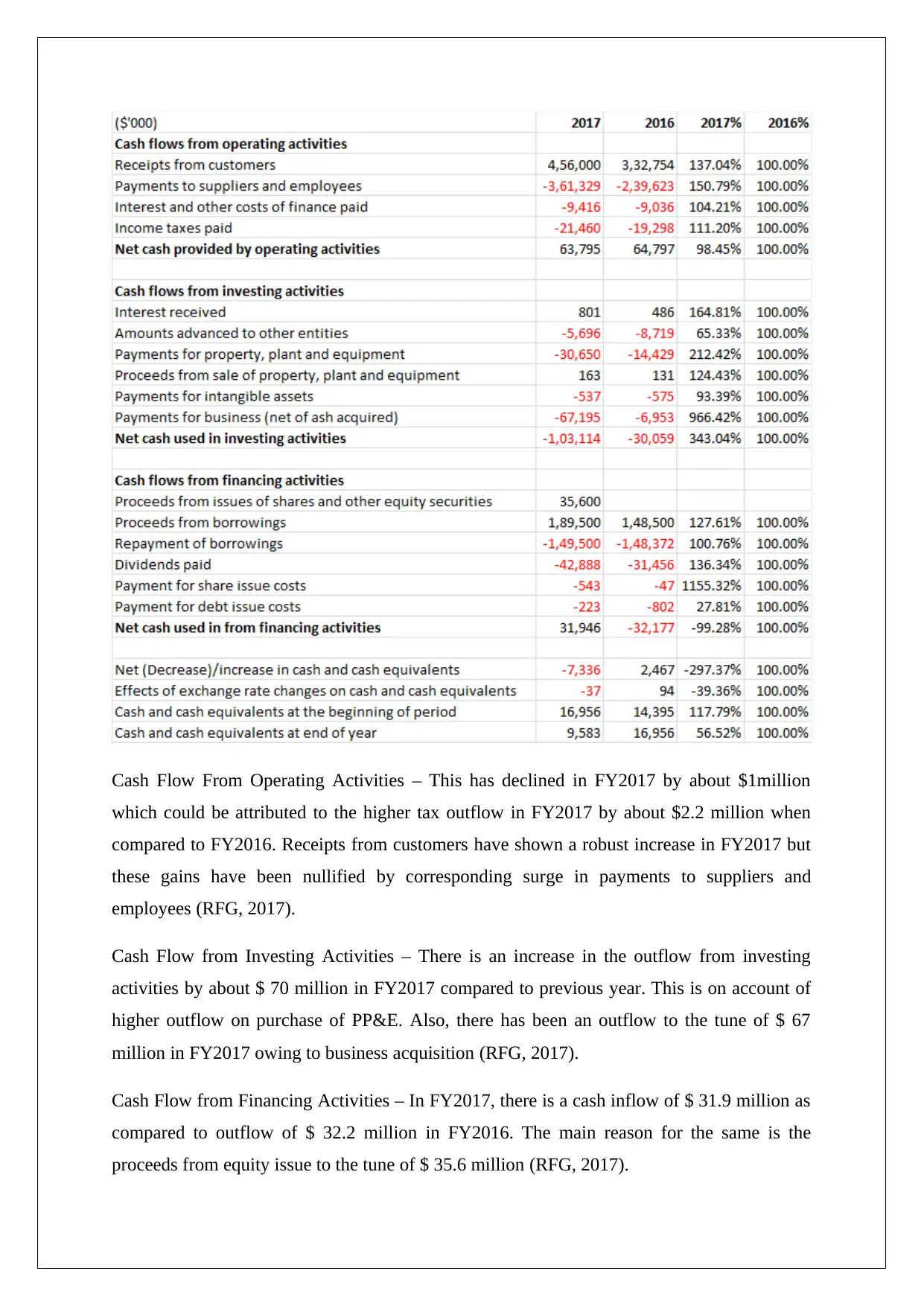

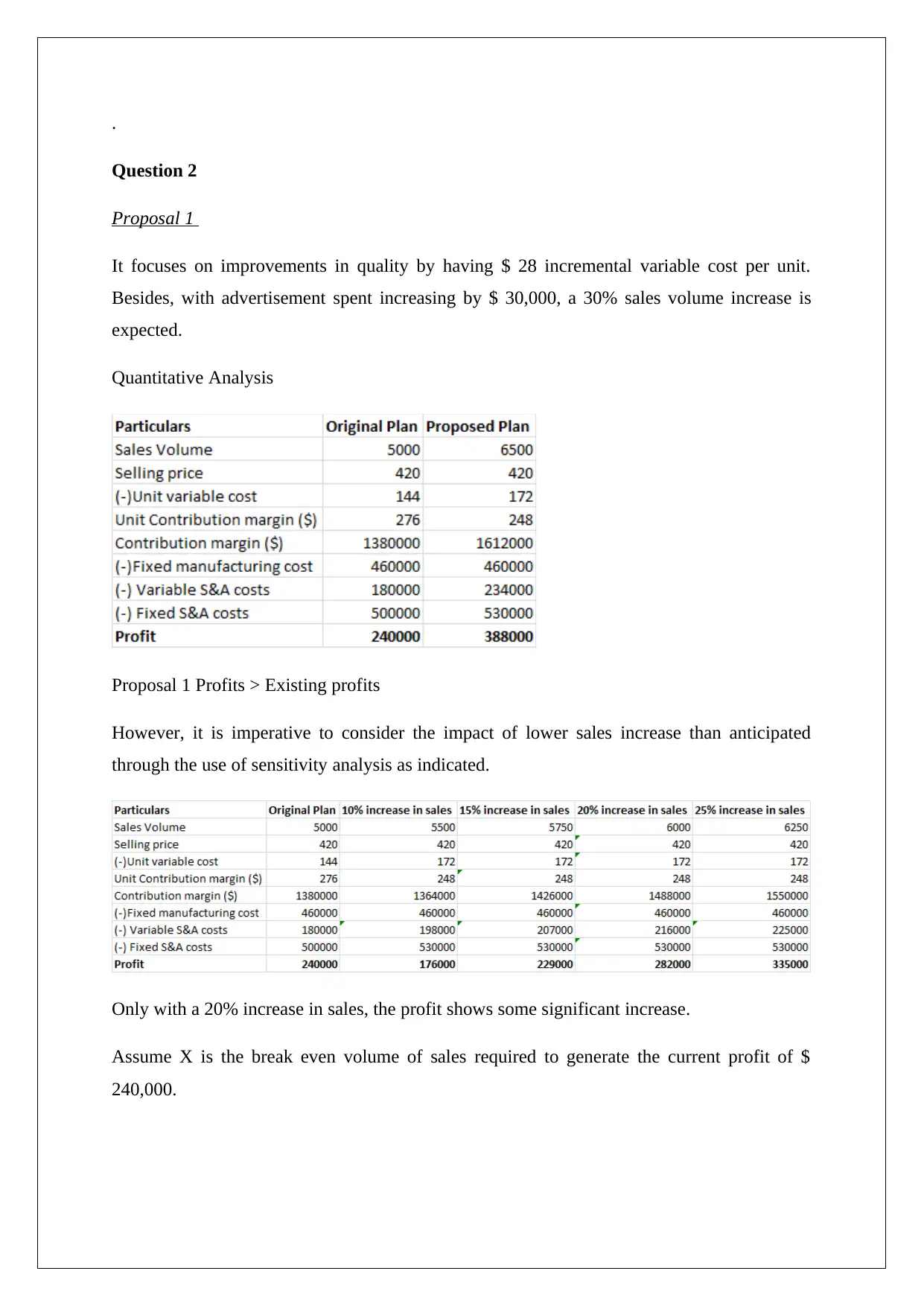

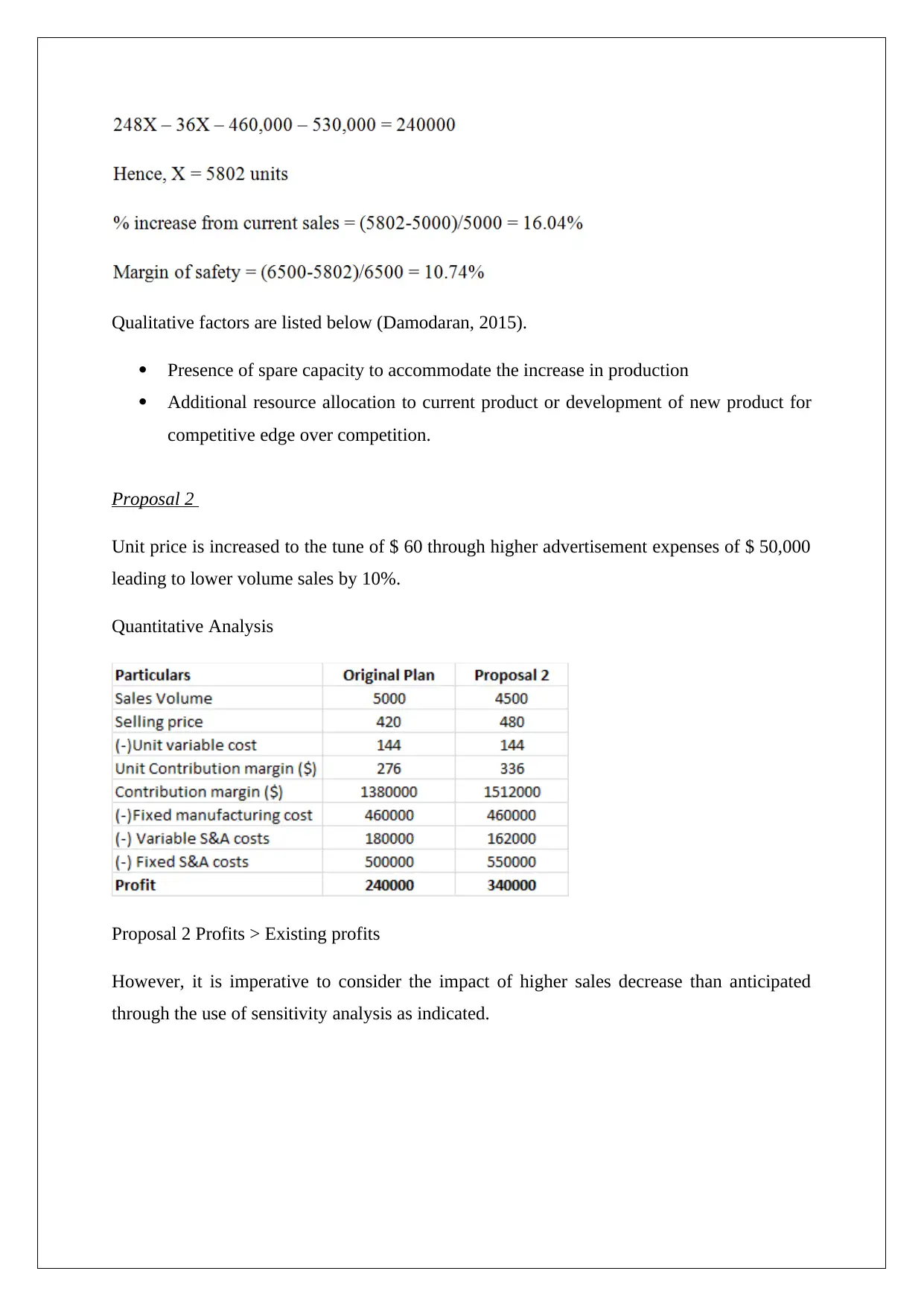

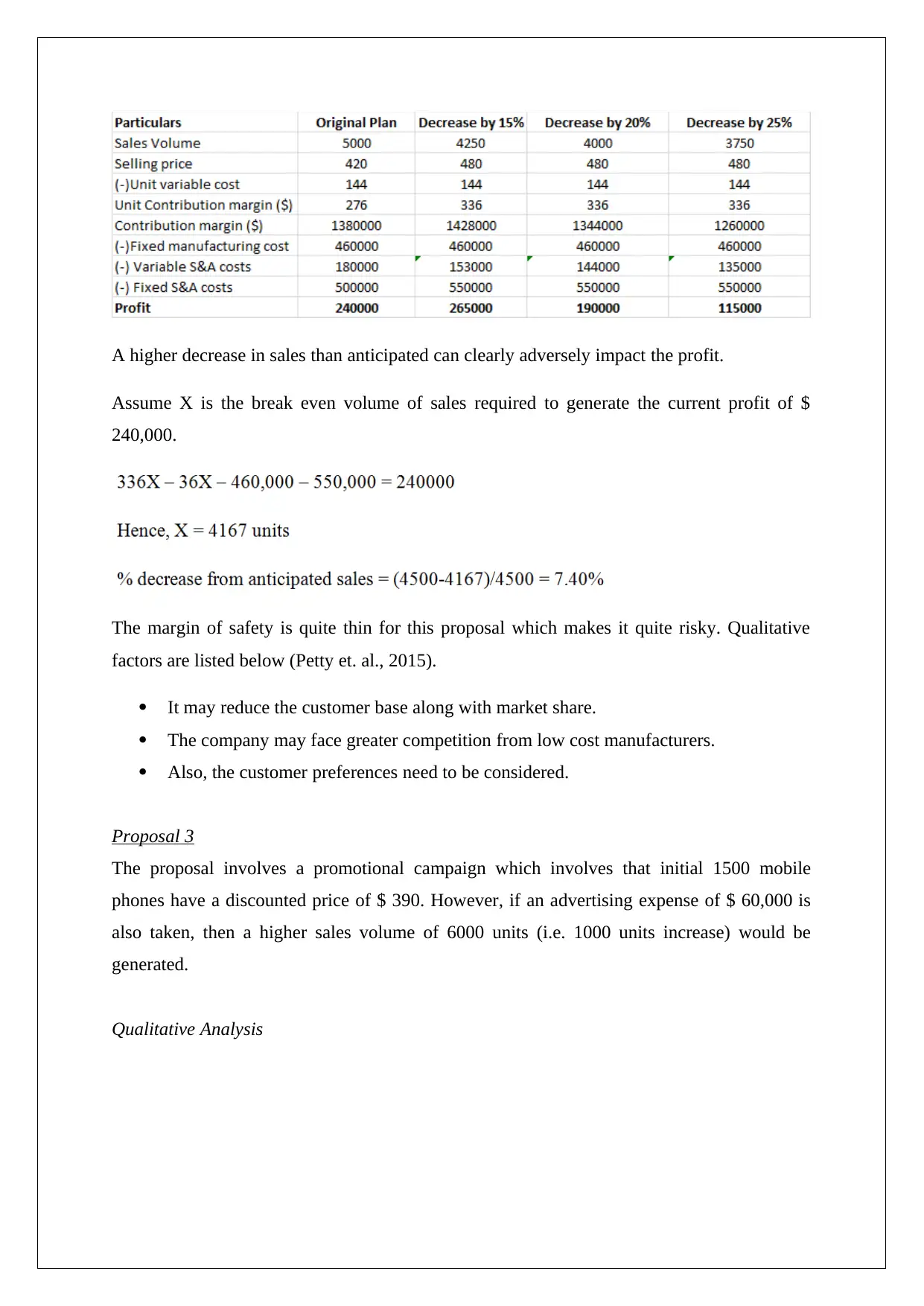

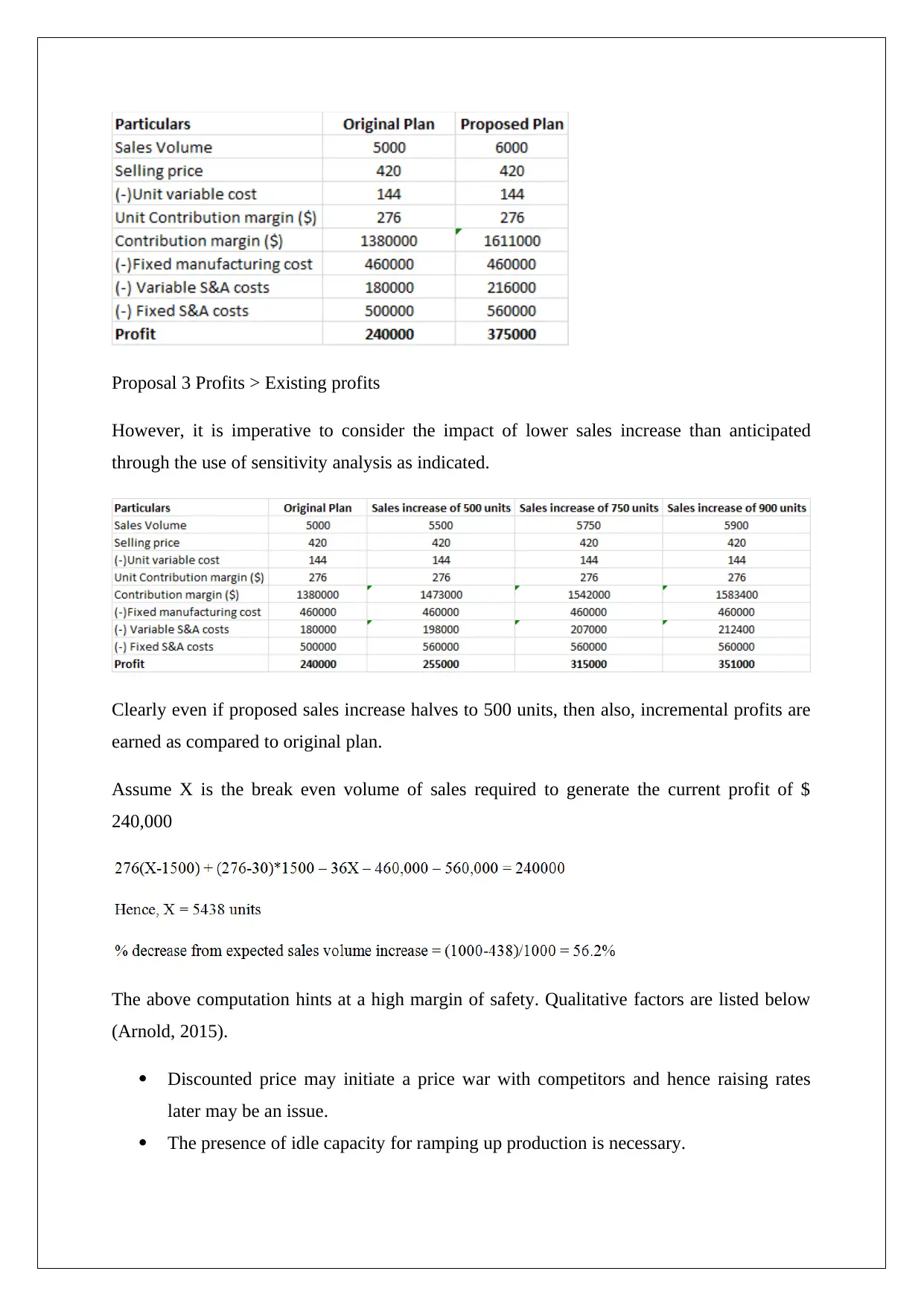

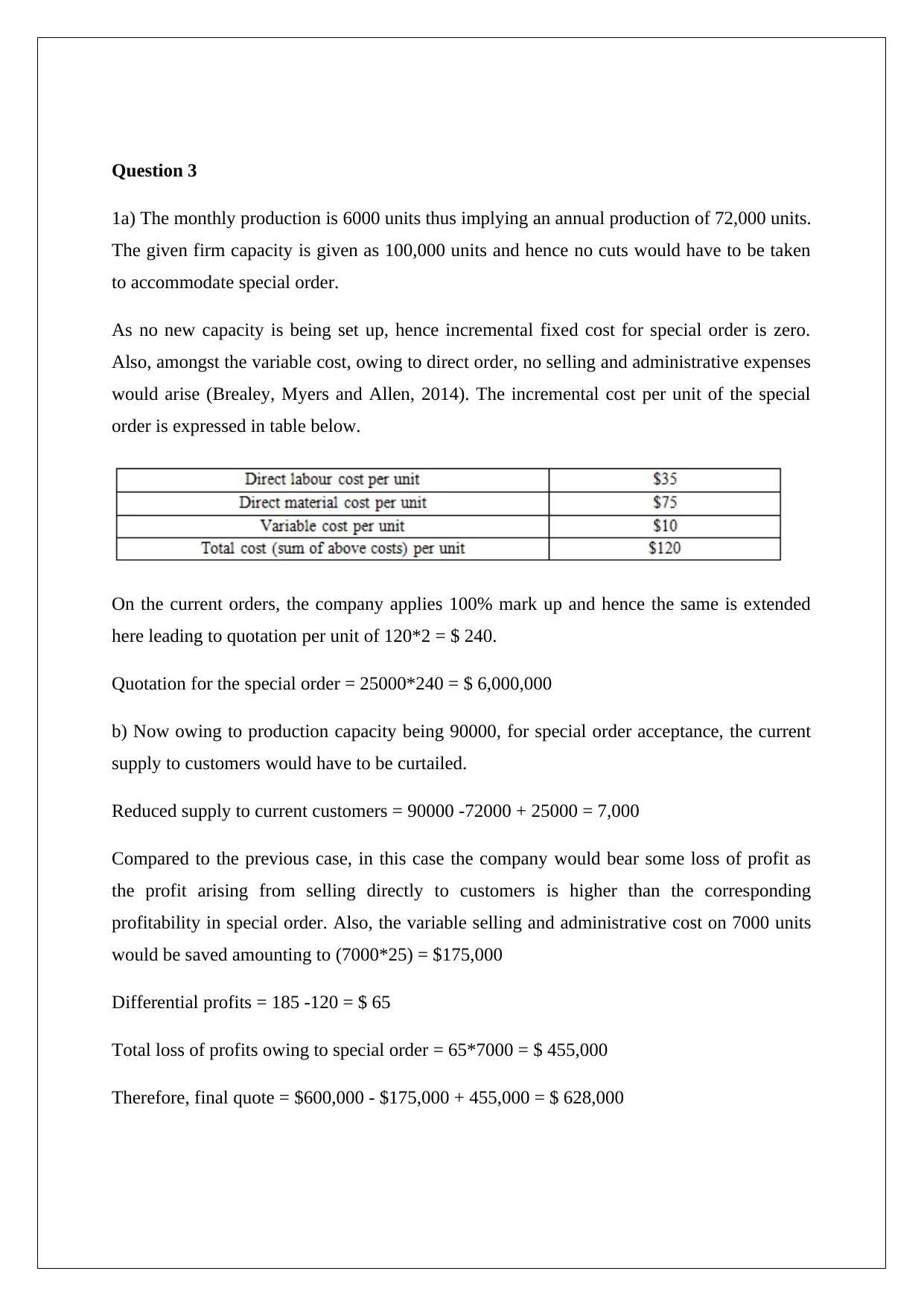

This report provides a financial analysis of RFG, focusing on cash flow statements, evaluating financial proposals, and determining special order quotations. The cash flow analysis examines operating, investing, and financing activities, noting key changes in FY2017. Three proposals are quantitatively and qualitatively analyzed, considering factors like sales volume, pricing, and competition. Sensitivity analysis is used to assess the impact of varying sales scenarios. The report also addresses a special order request, calculating incremental costs and providing a quotation based on capacity constraints and markup policies. Opportunities and disadvantages of accepting the special order are discussed, including capacity utilization, profit margins, and customer relationships. Desklib is your go-to platform for accessing solved assignments and study tools.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.