STAT6003: Financial Decisions - Multiple Regression Analysis Report

VerifiedAdded on 2023/01/18

|15

|3055

|88

Report

AI Summary

This report presents a comprehensive analysis of financial data using multiple linear regression. The assignment involves developing a multiple linear regression model with one dependent variable (market price) and four independent variables (Sydney price index, annual % change, total number of square meters, and age of house) using Excel. The report includes data plotting, model development, interpretation of coefficients, and assessment of statistical significance, including R-squared and confidence intervals. It compares the full model with a newly estimated model, discussing the relationships between variables and their impact on market price predictions. The analysis aims to aid financial decision-making through the application of statistical techniques.

Running head: STATISTICS FOR FINANCIAL DECISIONS

1

Statistics for Financial Decisions Using Excel

Name of Author

Class Name

Name of School

1

Statistics for Financial Decisions Using Excel

Name of Author

Class Name

Name of School

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STATISTICS FOR FINANCIAL DECISIONS 2

Abstract

The requirement of this assignment is the analysis of financial data using excel to help

make appropriate financial decisions. In the process of analysis, a regression model is supposed

to be developed. The regression model by chance is supposed to have one dependent variable

and four independent variables. From the idea of regression models, a model with more than one

independent variable is a multiple linear regression model. Hence what we actually are expected

to have is a multiple linear regression model. The actual model will look something like;

Y = β0 + β1 X1 + β2 X2 + β3 X3 + β4 X4 + ε (Harrell, 2015). Where Y is treated as the value of the

dependent variable, β0 is treated as the regression constant, β1 partial regression coefficients of

the first variable, β2 partial regression coefficient of the second variable, β3 partial regression

coefficient of the third variable, β4 partial regression coefficient of the fourth coefficient and ε is

treated as the error term.

Introduction

In this section of one of them, a statement that we are supposed to do is the rationale of

the model that we have developed via analysis. Our model is a multiple linear regression which

basically has got four independent variables and one dependent variable, unlike simple linear

regression which has one independent variable. Multiple linear regressions, our model, is

basically tracing its foundation from the correlation analysis. The first independent variable, in

analysis, explains the most of variance whereas the second independent variable explains the

second most of the variance and so on. In summary, the independent variables, help in analysis

to explain a proportional percentage of the variance of the dependent variable. Our model

replicates the identification related to important independent variables (Riley, Jackson, Salanti,

Abstract

The requirement of this assignment is the analysis of financial data using excel to help

make appropriate financial decisions. In the process of analysis, a regression model is supposed

to be developed. The regression model by chance is supposed to have one dependent variable

and four independent variables. From the idea of regression models, a model with more than one

independent variable is a multiple linear regression model. Hence what we actually are expected

to have is a multiple linear regression model. The actual model will look something like;

Y = β0 + β1 X1 + β2 X2 + β3 X3 + β4 X4 + ε (Harrell, 2015). Where Y is treated as the value of the

dependent variable, β0 is treated as the regression constant, β1 partial regression coefficients of

the first variable, β2 partial regression coefficient of the second variable, β3 partial regression

coefficient of the third variable, β4 partial regression coefficient of the fourth coefficient and ε is

treated as the error term.

Introduction

In this section of one of them, a statement that we are supposed to do is the rationale of

the model that we have developed via analysis. Our model is a multiple linear regression which

basically has got four independent variables and one dependent variable, unlike simple linear

regression which has one independent variable. Multiple linear regressions, our model, is

basically tracing its foundation from the correlation analysis. The first independent variable, in

analysis, explains the most of variance whereas the second independent variable explains the

second most of the variance and so on. In summary, the independent variables, help in analysis

to explain a proportional percentage of the variance of the dependent variable. Our model

replicates the identification related to important independent variables (Riley, Jackson, Salanti,

STATISTICS FOR FINANCIAL DECISIONS 3

Burke, Price, Kirkham & White, 2017). One disadvantage is that the model replicates error as

well. As it is known though, there is no model that is always perfect in the analysis (Akinwande,

Dikko & Samson, 2015).

The sample size of the model developed is fifteen cases for each predictor. This means

that for each independent variable there are actually fifteen observations. This is evident even

when you look at the multiple linear regression results ( Bretz, Hothorn & Westfall, 2016).

The dependent variable is the market price with a unit measurement of US Dollars,

something that is supposed to be determined by the model. The independent variables are;

Sydney price index, annual % change measured in percentage, the total number of square meters

measured in square meters and age of house measured in years.

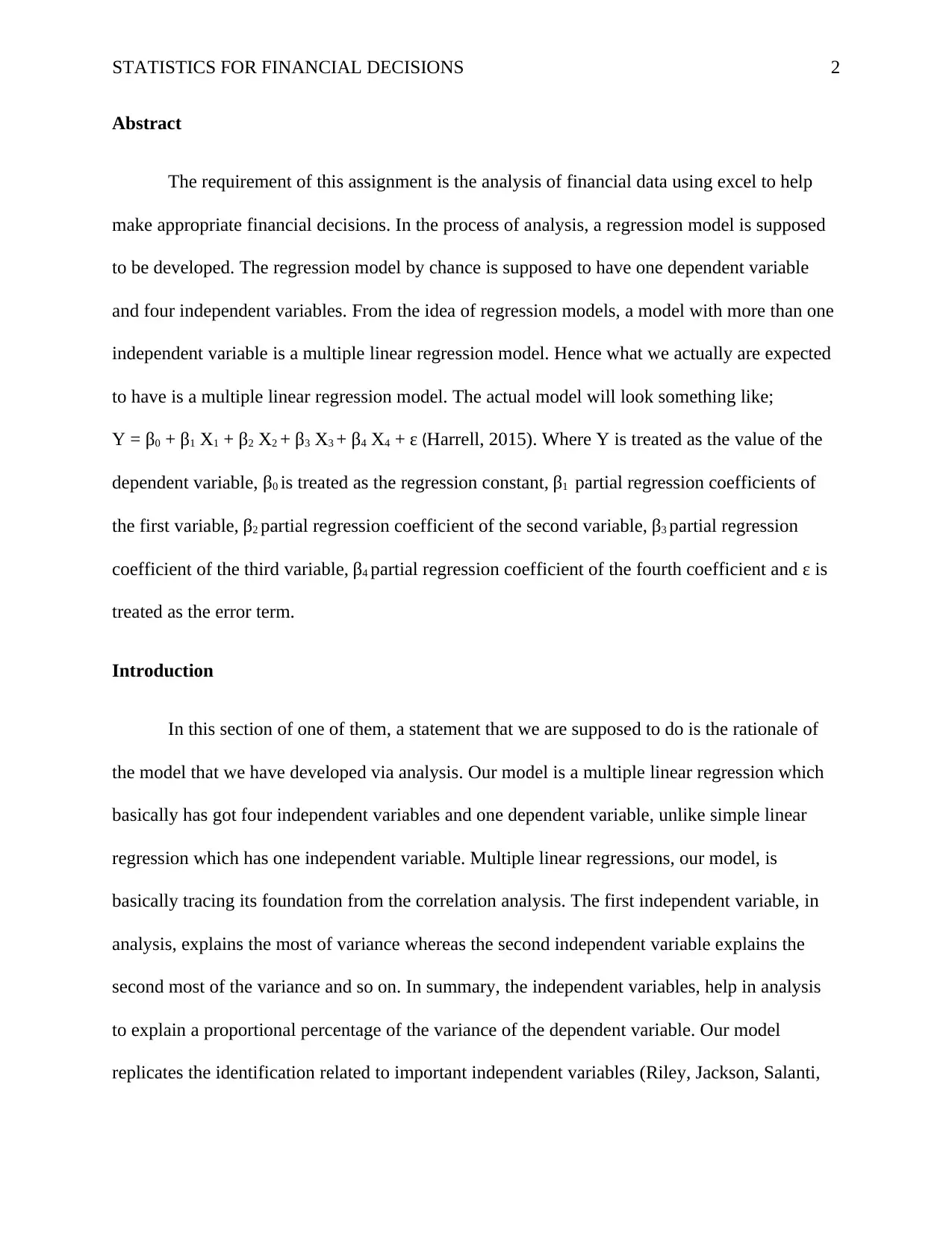

Plotting

0 50 100 150 200 250 300 350 400

0

200

400

600

800

1000

1200

Age of house (years) Total number of square meters

Annual % change Sydney price Index Figure 1

One of the requirements of the assignment was that the dependent is to be plotted against

each independent variable (Manly & Alberto, 2016). This is illustrated in figure 1 where all the

Burke, Price, Kirkham & White, 2017). One disadvantage is that the model replicates error as

well. As it is known though, there is no model that is always perfect in the analysis (Akinwande,

Dikko & Samson, 2015).

The sample size of the model developed is fifteen cases for each predictor. This means

that for each independent variable there are actually fifteen observations. This is evident even

when you look at the multiple linear regression results ( Bretz, Hothorn & Westfall, 2016).

The dependent variable is the market price with a unit measurement of US Dollars,

something that is supposed to be determined by the model. The independent variables are;

Sydney price index, annual % change measured in percentage, the total number of square meters

measured in square meters and age of house measured in years.

Plotting

0 50 100 150 200 250 300 350 400

0

200

400

600

800

1000

1200

Age of house (years) Total number of square meters

Annual % change Sydney price Index Figure 1

One of the requirements of the assignment was that the dependent is to be plotted against

each independent variable (Manly & Alberto, 2016). This is illustrated in figure 1 where all the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STATISTICS FOR FINANCIAL DECISIONS 4

plots for the respective variables are made. The variable; the age of house ranges from 0 to a

maximum of 45 hence the clustering to the extreme left. The actual data values when plotted will

produce a curve that crosses itself more than once. The total number of square meters being a

complete larger set of values, you find that the curve is out farther in the graph. It too has

crossing points on itself. Sydney price index keeps on rising, but the percentage change rises and

drops with it being at the extreme left as the changes are minimal but also produces a curve that

crosses itself (Mirman, 2017).

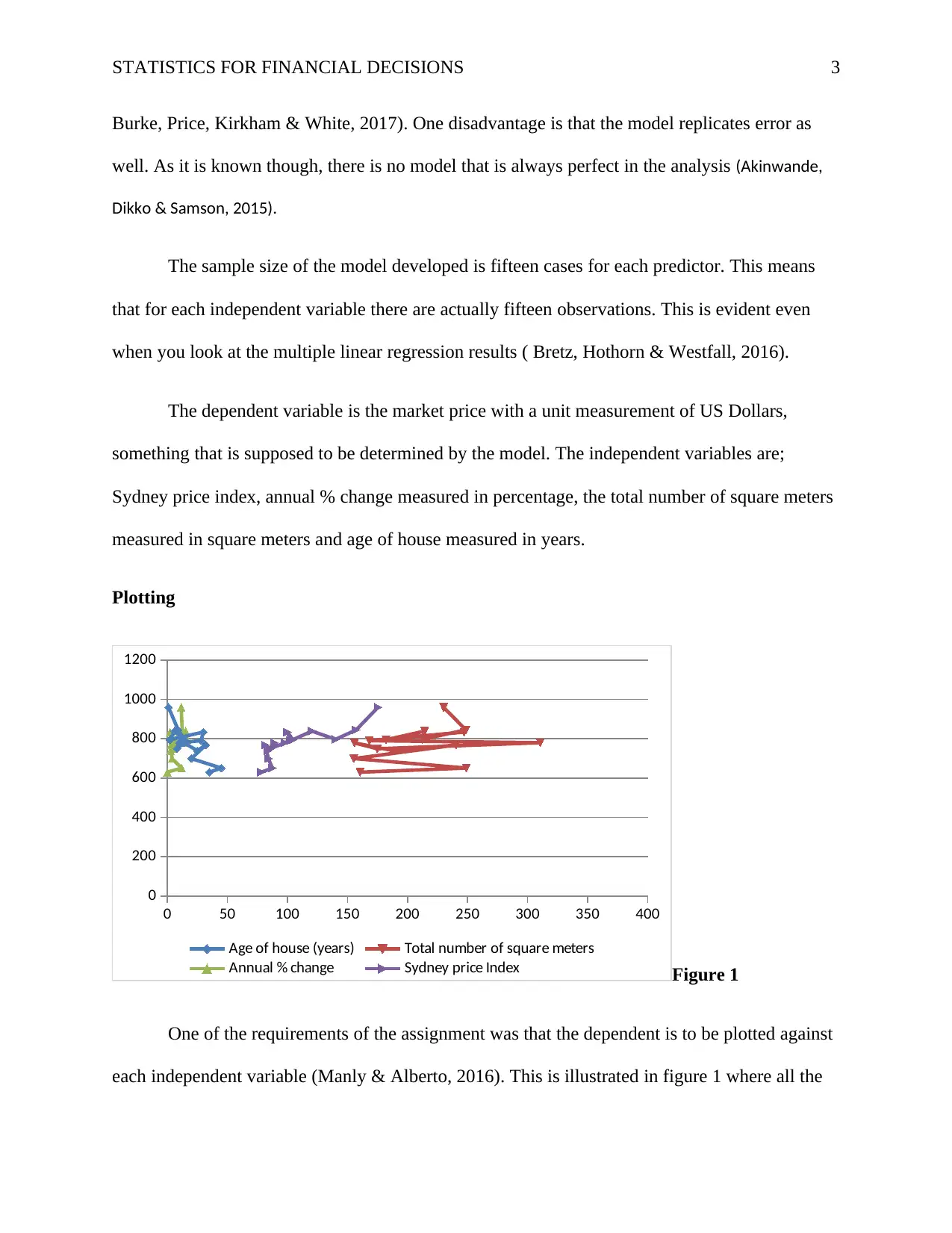

Full Model

The model that is to be presented here is to be withdrawn from the results of the multiple

linear regression analysis.

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.889164809

R Square 0.790614058

Adjusted R Square 0.706859681

Standard Error 43.88782615

Observations 15

ANOVA

df SS MS F Significance F

Regression 4 72728.58716 18182.14679 9.439674515 0.001993481

Residual 10 19261.41284 1926.141284

Total 14 91990

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

Intercept 548.978108 81.13153739 6.766519231 4.94032E-05 368.2057774 729.7504386 368.2057774 729.7504386

Sydney price Index 1.963493894 0.583205471 3.366727492 0.007160758 0.664031125 3.262956664 0.664031125 3.262956664

Annual % change -5.622204236 3.240109357 -1.735189655 0.113361729 -12.84161778 1.597209306 -12.84161778 1.597209306

Total number of square meters 0.519145629 0.3239088 1.60275247 0.140071458 -0.202568152 1.240859409 -0.202568152 1.240859409

Age of house (years) -2.48786597 1.129750872 -2.2021368 0.052251738 -5.005107781 0.029375841 -5.005107781 0.029375841

Figure 2

plots for the respective variables are made. The variable; the age of house ranges from 0 to a

maximum of 45 hence the clustering to the extreme left. The actual data values when plotted will

produce a curve that crosses itself more than once. The total number of square meters being a

complete larger set of values, you find that the curve is out farther in the graph. It too has

crossing points on itself. Sydney price index keeps on rising, but the percentage change rises and

drops with it being at the extreme left as the changes are minimal but also produces a curve that

crosses itself (Mirman, 2017).

Full Model

The model that is to be presented here is to be withdrawn from the results of the multiple

linear regression analysis.

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.889164809

R Square 0.790614058

Adjusted R Square 0.706859681

Standard Error 43.88782615

Observations 15

ANOVA

df SS MS F Significance F

Regression 4 72728.58716 18182.14679 9.439674515 0.001993481

Residual 10 19261.41284 1926.141284

Total 14 91990

Coefficients Standard Error t Stat P-value Lower 95% Upper 95% Lower 95.0% Upper 95.0%

Intercept 548.978108 81.13153739 6.766519231 4.94032E-05 368.2057774 729.7504386 368.2057774 729.7504386

Sydney price Index 1.963493894 0.583205471 3.366727492 0.007160758 0.664031125 3.262956664 0.664031125 3.262956664

Annual % change -5.622204236 3.240109357 -1.735189655 0.113361729 -12.84161778 1.597209306 -12.84161778 1.597209306

Total number of square meters 0.519145629 0.3239088 1.60275247 0.140071458 -0.202568152 1.240859409 -0.202568152 1.240859409

Age of house (years) -2.48786597 1.129750872 -2.2021368 0.052251738 -5.005107781 0.029375841 -5.005107781 0.029375841

Figure 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STATISTICS FOR FINANCIAL DECISIONS 5

Going by the requirement of the question to this section we will follow the model of the

representative model that we had written in the abstract section but this time we will include the

coefficients with the intercept being β0 and the Sydney price index representing β1, a partial

regression coefficient and so on. Therefore our actual model for the assignment will be;

Y = 548.98 + 1.96X1 -5.62X2 + 0.52X3 -2.49X4 + ε. As you can see the coefficients and the

intercept are all drawn from the coefficient column of the results of the regression model

analysis. X1 is Sydney price index, X2 annual % change, X3 is the total number of square meters,

X4 is an age of a house in years and Y is the market price (Faraway, 2016).

Least Squares Regression Model

Least squares regression model too just like multiple linear regressions was founded on

correlation analysis. Only that it has one and only one independent variable. By this we get the

model; Y = β0 + β1 X1 + ε. β0 is the intercept parameter and β1 is the slope parameter. ε is the error

term. Y is the predicted value (Carroll, 2017).

Estimated coefficients and significant values

In this section, we will interpret the estimated coefficients and discuss their significant

values. Before doing anything, we must inspect the p-values that correspond to the coefficients

of our independent variables. The p-value that is 0.05 or greater is going to be excluded. This

value shows that the predictive value that corresponds to that particular independent variable is

not of significance in predicting our outcomes. From the values of the table, the only p-values

values that are equal to 0.05 or over are those that correspond to annual % change and the total

number of square meters. Only these are statistically insignificant whereas the rest are. It is

Going by the requirement of the question to this section we will follow the model of the

representative model that we had written in the abstract section but this time we will include the

coefficients with the intercept being β0 and the Sydney price index representing β1, a partial

regression coefficient and so on. Therefore our actual model for the assignment will be;

Y = 548.98 + 1.96X1 -5.62X2 + 0.52X3 -2.49X4 + ε. As you can see the coefficients and the

intercept are all drawn from the coefficient column of the results of the regression model

analysis. X1 is Sydney price index, X2 annual % change, X3 is the total number of square meters,

X4 is an age of a house in years and Y is the market price (Faraway, 2016).

Least Squares Regression Model

Least squares regression model too just like multiple linear regressions was founded on

correlation analysis. Only that it has one and only one independent variable. By this we get the

model; Y = β0 + β1 X1 + ε. β0 is the intercept parameter and β1 is the slope parameter. ε is the error

term. Y is the predicted value (Carroll, 2017).

Estimated coefficients and significant values

In this section, we will interpret the estimated coefficients and discuss their significant

values. Before doing anything, we must inspect the p-values that correspond to the coefficients

of our independent variables. The p-value that is 0.05 or greater is going to be excluded. This

value shows that the predictive value that corresponds to that particular independent variable is

not of significance in predicting our outcomes. From the values of the table, the only p-values

values that are equal to 0.05 or over are those that correspond to annual % change and the total

number of square meters. Only these are statistically insignificant whereas the rest are. It is

STATISTICS FOR FINANCIAL DECISIONS 6

advisable to drop the respective variables in order to rerun the model for better results (Wood,

2017).

From the above fact of keeping all the coefficients of the independent variables as supported by

their p-values, it shows that the coefficients are statistically significant in doing predictions.

Looking at the overall p-value or the significance F which stand at 0.001993481, shows that the

model is statistically significant.

The values of the coefficients, whether negative or positive shows that an additional point

of the independent variable will be affected by how much the value of the coefficient is. (Hayes,

2017)

Coefficient of determination for the relationship

The coefficient of determination is gotten in the regression statistics section of the results

of the multiple regression model determination. This is represented by the R squared potion. The

R squared value is 0.790614058. It is also called the covariance, meaning the variations between

the dependent variable and the independent variable. It is the proportional variability in y that

can be explained by the independent variable in the model. By 0.790614058 we are explaining a

79% correlation between the dependent variable and each independent variable (Dellicour, Rose

& Pybus, 2016).

Confidence Interval

The confidence interval is the correlation of the associated variables in a statistical model.

In our case, we will use the 95% confidence interval. Looking at the column of the lower

confidence interval in figure 2, you will realize that the last three independent variables, unlike

advisable to drop the respective variables in order to rerun the model for better results (Wood,

2017).

From the above fact of keeping all the coefficients of the independent variables as supported by

their p-values, it shows that the coefficients are statistically significant in doing predictions.

Looking at the overall p-value or the significance F which stand at 0.001993481, shows that the

model is statistically significant.

The values of the coefficients, whether negative or positive shows that an additional point

of the independent variable will be affected by how much the value of the coefficient is. (Hayes,

2017)

Coefficient of determination for the relationship

The coefficient of determination is gotten in the regression statistics section of the results

of the multiple regression model determination. This is represented by the R squared potion. The

R squared value is 0.790614058. It is also called the covariance, meaning the variations between

the dependent variable and the independent variable. It is the proportional variability in y that

can be explained by the independent variable in the model. By 0.790614058 we are explaining a

79% correlation between the dependent variable and each independent variable (Dellicour, Rose

& Pybus, 2016).

Confidence Interval

The confidence interval is the correlation of the associated variables in a statistical model.

In our case, we will use the 95% confidence interval. Looking at the column of the lower

confidence interval in figure 2, you will realize that the last three independent variables, unlike

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STATISTICS FOR FINANCIAL DECISIONS 7

the first independent variable, have got negative values associated with them. This definitely

shows that the actual correlation relation that the respective independent variables with negative

values have with the dependent variable is actually negative. That of the other independent

variable is actually posing a positive correlation.

Moving to the other upper confidence interval you will realize that all the values that are

there are all positive values. This shows that on the upper side the correlation is actually positive

all through for all the independent variables.

The value of 0 in the confidence interval shows that there is no correlation at all. But in our

interval values of the confidence interval, there is no such value in the confidence interval range.

This shows that there lacks no un-correlation. ( Farinotti, Longuevergne, Moholdt, Duethmann,

Mölg, Bolch & Güntner, 2015).

Relationship between the market price and the land size

As per the newly estimated model, the actual relationship between the market price and

the land size in total square meters is that the land size is correlated to the market price 9.8% of

the time. This is shown in the R squared value. For every additional unit of a square meter, the

market price will be an additional of 0.563603274 of the market price that was initially allocated

to the initial square meter value. The standard error, which is the variability of the actual y-

values from the predicted y-values, stands at 0.473897199. This shows that the actual error made

while predicting the market price is 47%. Moving to the p-value, which is the significant value

corresponding to each variable. The p-value of each and every independent variable should be

less than or equal to 5% or 0.05. Looking at the total number of square meters, the p-value is

greater than 0.05 and is standing at 0.25. From the 0.25 p-value, this shows that the independent

the first independent variable, have got negative values associated with them. This definitely

shows that the actual correlation relation that the respective independent variables with negative

values have with the dependent variable is actually negative. That of the other independent

variable is actually posing a positive correlation.

Moving to the other upper confidence interval you will realize that all the values that are

there are all positive values. This shows that on the upper side the correlation is actually positive

all through for all the independent variables.

The value of 0 in the confidence interval shows that there is no correlation at all. But in our

interval values of the confidence interval, there is no such value in the confidence interval range.

This shows that there lacks no un-correlation. ( Farinotti, Longuevergne, Moholdt, Duethmann,

Mölg, Bolch & Güntner, 2015).

Relationship between the market price and the land size

As per the newly estimated model, the actual relationship between the market price and

the land size in total square meters is that the land size is correlated to the market price 9.8% of

the time. This is shown in the R squared value. For every additional unit of a square meter, the

market price will be an additional of 0.563603274 of the market price that was initially allocated

to the initial square meter value. The standard error, which is the variability of the actual y-

values from the predicted y-values, stands at 0.473897199. This shows that the actual error made

while predicting the market price is 47%. Moving to the p-value, which is the significant value

corresponding to each variable. The p-value of each and every independent variable should be

less than or equal to 5% or 0.05. Looking at the total number of square meters, the p-value is

greater than 0.05 and is standing at 0.25. From the 0.25 p-value, this shows that the independent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STATISTICS FOR FINANCIAL DECISIONS 8

variable is not statistically significant for analysis and therefore should be dropped to pick

another variable to be used in the running of the model. The two variables correlate negatively to

the lower side but positively to the upper side (Skoog, Holler & Crouch 2017).

The actual graph as shown below in figure 3, shows multiple crosses of the points. This shows

different areas were sold during different financial, hence the crosses at different points of the

curve (Yandell, 2017).

0 2 4 6 8 10 12

0

2

4

6

8

10

12

Total number of square meters

Total number of square

meters

Estimated Model against the New Model

I comparing the newly estimated model to the old model, using the coefficient of

determination which is the R squared we will realize that the old model is a better model to use

in the correlation process for the business decision because the independent variable dataset, that

is the total number of square meters is correlated to the dependent variable more of the time and

at 79% that the newly estimated model where the correlation between the said independent

variable and the dependent variable stands at 9.8% of the time. In the new model, it is evident to

see that it is less important to use the total number of square meters to determine the market

variable is not statistically significant for analysis and therefore should be dropped to pick

another variable to be used in the running of the model. The two variables correlate negatively to

the lower side but positively to the upper side (Skoog, Holler & Crouch 2017).

The actual graph as shown below in figure 3, shows multiple crosses of the points. This shows

different areas were sold during different financial, hence the crosses at different points of the

curve (Yandell, 2017).

0 2 4 6 8 10 12

0

2

4

6

8

10

12

Total number of square meters

Total number of square

meters

Estimated Model against the New Model

I comparing the newly estimated model to the old model, using the coefficient of

determination which is the R squared we will realize that the old model is a better model to use

in the correlation process for the business decision because the independent variable dataset, that

is the total number of square meters is correlated to the dependent variable more of the time and

at 79% that the newly estimated model where the correlation between the said independent

variable and the dependent variable stands at 9.8% of the time. In the new model, it is evident to

see that it is less important to use the total number of square meters to determine the market

STATISTICS FOR FINANCIAL DECISIONS 9

price. For the old model, it is advisable to use the said independent variable as this would

definitely bring forth.

The standard error of the correlation of the independent and the dependent variables increases

when you use from the old model to the estimated model. Hence the old model is statistically

significant in making estimations. This is because when using the old model, the minimal error

will be encountered as compared to when using the newly estimated model.

The p-value or the significance F for the overall model for the new model stands at

0.2555933 which is more than 0.05, yet that of the old model stands at 0.001993481 which is

less than 0.05. Hence by convention, it is very easy to see that the old model is statistically

significant as opposed to the new estimated model.

From the conclusion, the newly estimated model is the least square regression model. This by

evidence is proven to be less efficient as compared to the multiple linear regressions. Even

though there is no model that is in all averagely statistically perfect but comparing the two, one

surely stands out to be better than the other (Danish, 2016).

Predicting Market Price of a House of 400 Square Meters

Here we will use the least square regression model that we have estimated. The model

system is; Y = β0 + β1 X1 + ε which is actually accorded Y= 659.144 + 0.5636 X1 + 0.4739. The

value of X1 which is the total number of square meters of the house is 400. Replacing 400 in the

equation gives; Y= 659.144 + 0.5636(400) + 0.4739, which then equals 1,885.0579. Since the

value was measured in thousand US dollars the actual value will be $ 1,885,058 (Little & Rubin,

2019).

price. For the old model, it is advisable to use the said independent variable as this would

definitely bring forth.

The standard error of the correlation of the independent and the dependent variables increases

when you use from the old model to the estimated model. Hence the old model is statistically

significant in making estimations. This is because when using the old model, the minimal error

will be encountered as compared to when using the newly estimated model.

The p-value or the significance F for the overall model for the new model stands at

0.2555933 which is more than 0.05, yet that of the old model stands at 0.001993481 which is

less than 0.05. Hence by convention, it is very easy to see that the old model is statistically

significant as opposed to the new estimated model.

From the conclusion, the newly estimated model is the least square regression model. This by

evidence is proven to be less efficient as compared to the multiple linear regressions. Even

though there is no model that is in all averagely statistically perfect but comparing the two, one

surely stands out to be better than the other (Danish, 2016).

Predicting Market Price of a House of 400 Square Meters

Here we will use the least square regression model that we have estimated. The model

system is; Y = β0 + β1 X1 + ε which is actually accorded Y= 659.144 + 0.5636 X1 + 0.4739. The

value of X1 which is the total number of square meters of the house is 400. Replacing 400 in the

equation gives; Y= 659.144 + 0.5636(400) + 0.4739, which then equals 1,885.0579. Since the

value was measured in thousand US dollars the actual value will be $ 1,885,058 (Little & Rubin,

2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

STATISTICS FOR FINANCIAL DECISIONS 10

Conclusion

From the above analysis, it is very evident to see that the actual model that would best fit

regression analysis is the multiple regression model. Given a chance to advise, if there were

several variables, instead of using the least square regression model it is advisable to use multiple

regression model as it gives the best statistical results and it is more statistically significant. The

overall p-value for both cases shows that the real value that is associated to the re-estimated

model is less statistically significant as the value is totally more than the significant value that

stands at 5% or is 0.05.

Conclusion

From the above analysis, it is very evident to see that the actual model that would best fit

regression analysis is the multiple regression model. Given a chance to advise, if there were

several variables, instead of using the least square regression model it is advisable to use multiple

regression model as it gives the best statistical results and it is more statistically significant. The

overall p-value for both cases shows that the real value that is associated to the re-estimated

model is less statistically significant as the value is totally more than the significant value that

stands at 5% or is 0.05.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

STATISTICS FOR FINANCIAL DECISIONS 11

References

Akinwande, M. O., Dikko, H. G., & Samson, A. (2015). Variance inflation factor: as a condition

for the inclusion of suppressor variable (s) in regression analysis. Open Journal of

Statistics, 5(07), 754.

Bretz, F., Hothorn, T., & Westfall, P. (2016). Multiple comparisons using R. Chapman and

Hall/CRC.

Carroll, R. J. (2017). Transformation and weighting in regression. Routledge.

Danish, N. P. S. Z. M. (2016). Support vector regression model for predicting the. Bioresour.

Technol, 96, 1292-1296.

Dellicour, S., Rose, R., & Pybus, O. G. (2016). Explaining the geographic spread of emerging

epidemics: a framework for comparing viral phylogenies and environmental landscape

data. BMC Bioinformatics, 17(1), 82.

Faraway, J. J. (2016). Linear models with R. Chapman and Hall/CRC.

Farinotti, D., Longuevergne, L., Moholdt, G., Duethmann, D., Mölg, T., Bolch, T., ... & Güntner,

A. (2015). Substantial glacier mass loss in the Tien Shan over the past 50 years. Nature

Geoscience, 8(9), 716.

Harrell Jr, F. E. (2015). Regression modelling strategies: with applications to linear models,

logistic and ordinal regression, and survival analysis. Springer.

Hayes, A. F. (2017). Introduction to mediation, moderation, and conditional process analysis: A

regression-based approach. Guilford Publications.

References

Akinwande, M. O., Dikko, H. G., & Samson, A. (2015). Variance inflation factor: as a condition

for the inclusion of suppressor variable (s) in regression analysis. Open Journal of

Statistics, 5(07), 754.

Bretz, F., Hothorn, T., & Westfall, P. (2016). Multiple comparisons using R. Chapman and

Hall/CRC.

Carroll, R. J. (2017). Transformation and weighting in regression. Routledge.

Danish, N. P. S. Z. M. (2016). Support vector regression model for predicting the. Bioresour.

Technol, 96, 1292-1296.

Dellicour, S., Rose, R., & Pybus, O. G. (2016). Explaining the geographic spread of emerging

epidemics: a framework for comparing viral phylogenies and environmental landscape

data. BMC Bioinformatics, 17(1), 82.

Faraway, J. J. (2016). Linear models with R. Chapman and Hall/CRC.

Farinotti, D., Longuevergne, L., Moholdt, G., Duethmann, D., Mölg, T., Bolch, T., ... & Güntner,

A. (2015). Substantial glacier mass loss in the Tien Shan over the past 50 years. Nature

Geoscience, 8(9), 716.

Harrell Jr, F. E. (2015). Regression modelling strategies: with applications to linear models,

logistic and ordinal regression, and survival analysis. Springer.

Hayes, A. F. (2017). Introduction to mediation, moderation, and conditional process analysis: A

regression-based approach. Guilford Publications.

STATISTICS FOR FINANCIAL DECISIONS 12

Little, R. J., & Rubin, D. B. (2019). Statistical analysis with missing data (Vol. 793). Wiley.

Manly, B. F., & Alberto, J. A. N. (2016). Multivariate statistical methods: a primer. Chapman

and Hall/CRC.

Mirman, D. (2017). Growth curve analysis and visualization using R. Chapman and Hall/CRC.

Riley, R. D., Jackson, D., Salanti, G., Burke, D. L., Price, M., Kirkham, J., & White, I. R. (2017).

Multivariate and network meta-analysis of multiple outcomes and multiple treatments:

rationale, concepts, and examples. BMJ, 358, j3932.

Skoog, D. A., Holler, F. J., & Crouch, S. R. (2017). Principles of instrumental analysis. Cengage

Learning.

Wood, S. N. (2017). Generalized additive models: an introduction with R. Chapman and

Hall/CRC.

Yandell, B. (2017). Practical data analysis for designed experiments. Routledge.

Little, R. J., & Rubin, D. B. (2019). Statistical analysis with missing data (Vol. 793). Wiley.

Manly, B. F., & Alberto, J. A. N. (2016). Multivariate statistical methods: a primer. Chapman

and Hall/CRC.

Mirman, D. (2017). Growth curve analysis and visualization using R. Chapman and Hall/CRC.

Riley, R. D., Jackson, D., Salanti, G., Burke, D. L., Price, M., Kirkham, J., & White, I. R. (2017).

Multivariate and network meta-analysis of multiple outcomes and multiple treatments:

rationale, concepts, and examples. BMJ, 358, j3932.

Skoog, D. A., Holler, F. J., & Crouch, S. R. (2017). Principles of instrumental analysis. Cengage

Learning.

Wood, S. N. (2017). Generalized additive models: an introduction with R. Chapman and

Hall/CRC.

Yandell, B. (2017). Practical data analysis for designed experiments. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.