Management Accounting Report: Galway Plc Financial Analysis

VerifiedAdded on 2023/01/23

|18

|4451

|27

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems for Galway Plc, a manufacturing firm. It begins by defining management accounting and its importance in decision-making, then delves into different types of systems like cost accounting, inventory management, and job costing, outlining their essential requirements. The report explores various management accounting reporting methods, including performance, cost managerial, budget, and accounts receivable aging reports, and discusses their benefits. It then presents a detailed calculation of income statements under both marginal and absorption costing methods for Galway Plc, including interpretations of the results. The report also defines and analyzes the advantages and disadvantages of different budgetary control planning tools, such as flexible budgets. Finally, it examines how management accounting techniques can be used to resolve financial problems within the organization, providing a complete overview of financial management strategies.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.................................................................................................................................3

MAIN BODY........................................................................................................................................3

LO 1......................................................................................................................................................3

P1. Explaining the essential requirement of different types of management accounting

systems...................................................................................................................................3

P2. Different methods used for Management Accounting reporting.....................................5

M1. Benefits of application of the management accounting system in an organisation........6

LO 2......................................................................................................................................................7

P 3 Calculation of income statement under marginal and absorption costing.......................7

LO 3....................................................................................................................................................11

P4. Defining advantages and disadvantages of different planning tools of budgetary

control...................................................................................................................................11

M3. Analysing uses and application of the different planning tools....................................13

LO 4....................................................................................................................................................14

P5 & M4. Different types of management accounting systems available for resolving the

financial problems................................................................................................................14

CONCLUSION...................................................................................................................................16

REFERENCES....................................................................................................................................17

INTRODUCTION.................................................................................................................................3

MAIN BODY........................................................................................................................................3

LO 1......................................................................................................................................................3

P1. Explaining the essential requirement of different types of management accounting

systems...................................................................................................................................3

P2. Different methods used for Management Accounting reporting.....................................5

M1. Benefits of application of the management accounting system in an organisation........6

LO 2......................................................................................................................................................7

P 3 Calculation of income statement under marginal and absorption costing.......................7

LO 3....................................................................................................................................................11

P4. Defining advantages and disadvantages of different planning tools of budgetary

control...................................................................................................................................11

M3. Analysing uses and application of the different planning tools....................................13

LO 4....................................................................................................................................................14

P5 & M4. Different types of management accounting systems available for resolving the

financial problems................................................................................................................14

CONCLUSION...................................................................................................................................16

REFERENCES....................................................................................................................................17

INTRODUCTION

Management accounting is defined as the process of analysis of the both the internal

management and financial accounting system. It further assists in the company in preparation

of managerial reports, records, and accounts with available information, statistics and other

financial as well as non-financial data. This helps the management and employees can in

decision making related to business operations and investment. The present report is based on

Galway Plc. which is a manufacturing firm. The present report will discuss different types of

management accounting systems for organization for making profit. Further the report will

discuss about the concept of management accounting reporting and its uses in decision

making. Income statement under Marginal and Absorption Costing of Galway Plc. Along

with interpretation will be disclosed. It will also define budgetary tools & advantages and

disadvantages from different budgetary planning tools. At last, the report will shed light on

solving the financial problems with the help of management accounting techniques.

MAIN BODY

LO 1

P1. Describing essential requirement of different types of management accounting systems.

Management accounting system is defined as the process of preparing internal

managerial reports for assisting the management. This system assists management of the

company in identifying, and recording statistical as well as financial information for

planning, decision-making process.

Essential requirements of different types of Management Accounting System in Galway Plc.

are as follows:

1. Cost Accounting System – This method of management accounting system is

basically related to the cost associated with the business operations and processes.

The cost accounting system helps Galway Plc. in evaluating cost value incurred for

carrying on all the manufacturing and production process. This method also helps in

assessing the level of profit margin with minimum operation cost by improving the

quality of product and service. Company should make effective business plans and

strategies for controlling cost expenses. This method consists of following sub parts:

1. Job Order Costing Method – This method of cost accounting system helps in

determining the cost amount as incurred for producing a specific product or group of

products by the company (Otley, 2016).

Management accounting is defined as the process of analysis of the both the internal

management and financial accounting system. It further assists in the company in preparation

of managerial reports, records, and accounts with available information, statistics and other

financial as well as non-financial data. This helps the management and employees can in

decision making related to business operations and investment. The present report is based on

Galway Plc. which is a manufacturing firm. The present report will discuss different types of

management accounting systems for organization for making profit. Further the report will

discuss about the concept of management accounting reporting and its uses in decision

making. Income statement under Marginal and Absorption Costing of Galway Plc. Along

with interpretation will be disclosed. It will also define budgetary tools & advantages and

disadvantages from different budgetary planning tools. At last, the report will shed light on

solving the financial problems with the help of management accounting techniques.

MAIN BODY

LO 1

P1. Describing essential requirement of different types of management accounting systems.

Management accounting system is defined as the process of preparing internal

managerial reports for assisting the management. This system assists management of the

company in identifying, and recording statistical as well as financial information for

planning, decision-making process.

Essential requirements of different types of Management Accounting System in Galway Plc.

are as follows:

1. Cost Accounting System – This method of management accounting system is

basically related to the cost associated with the business operations and processes.

The cost accounting system helps Galway Plc. in evaluating cost value incurred for

carrying on all the manufacturing and production process. This method also helps in

assessing the level of profit margin with minimum operation cost by improving the

quality of product and service. Company should make effective business plans and

strategies for controlling cost expenses. This method consists of following sub parts:

1. Job Order Costing Method – This method of cost accounting system helps in

determining the cost amount as incurred for producing a specific product or group of

products by the company (Otley, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Process Costing Method – This method assists in the process of collecting and

assigning of cost amount. This cost amount is assigned to units produced. This

method helps the companies especially in case of identical units where large

production process is carried out.

2. Inventory Management System – This method of management accounting focuses

on controlling the cost as incurred on producing goods and services for meeting the

customer demands. It assists in managing inventory and stock level of the company.

By monitoring the quantity of inventory and stock through the supply chain, it helps

the company in making inventory valuation, improving the accuracy of inventory by

maintaining continuous workflow and its reorder so as to facilitate smooth

functioning of business operations. Valuation of inventory can be done with the help

of two methods:

1. LIFO – It is a method in which goods bought or purchased at last are available for

sale at the first place. LIFO stands for Last In First Out.

2. FIFO – This stands for First In First Out. It is related with the process of selling

stock on first priority which is purchase in first place.

3. Job Costing System – The job costing method of management accounting is a

business procedure focusing on the process of collecting and analysing all the

important information related to the cost expenses incurred. It emphasizes on

expenses associated with the production of specific product. It helps the company in

determining the cost of operations and corrective measures for minimising cost

expense (Chenhall and Moers, 2015). This method takes into consideration each part

of information related to the direct material, labour and overhead costs. Under this

system, information related to cost incurred for every job work completed is provided

to the customer for getting cost reimbursed as per the contract or agreement made.

P2. Different methods used for Management Accounting reporting.

Management Accounting Reporting is related with the process of preparing internal

managerial report. It provides correct & accurate internal information about the statistical and

financial aspect of the company. It also provides deep insight about the business operations

and procedures as required for making day to day decision making especially related to

investment purpose. Different methods which can be used by Galway Plc. for management

accounting reporting are as follows:

assigning of cost amount. This cost amount is assigned to units produced. This

method helps the companies especially in case of identical units where large

production process is carried out.

2. Inventory Management System – This method of management accounting focuses

on controlling the cost as incurred on producing goods and services for meeting the

customer demands. It assists in managing inventory and stock level of the company.

By monitoring the quantity of inventory and stock through the supply chain, it helps

the company in making inventory valuation, improving the accuracy of inventory by

maintaining continuous workflow and its reorder so as to facilitate smooth

functioning of business operations. Valuation of inventory can be done with the help

of two methods:

1. LIFO – It is a method in which goods bought or purchased at last are available for

sale at the first place. LIFO stands for Last In First Out.

2. FIFO – This stands for First In First Out. It is related with the process of selling

stock on first priority which is purchase in first place.

3. Job Costing System – The job costing method of management accounting is a

business procedure focusing on the process of collecting and analysing all the

important information related to the cost expenses incurred. It emphasizes on

expenses associated with the production of specific product. It helps the company in

determining the cost of operations and corrective measures for minimising cost

expense (Chenhall and Moers, 2015). This method takes into consideration each part

of information related to the direct material, labour and overhead costs. Under this

system, information related to cost incurred for every job work completed is provided

to the customer for getting cost reimbursed as per the contract or agreement made.

P2. Different methods used for Management Accounting reporting.

Management Accounting Reporting is related with the process of preparing internal

managerial report. It provides correct & accurate internal information about the statistical and

financial aspect of the company. It also provides deep insight about the business operations

and procedures as required for making day to day decision making especially related to

investment purpose. Different methods which can be used by Galway Plc. for management

accounting reporting are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Performance Report – The performance report is one of the most important report

which helps the company in monitoring, assessing and reviewing the performance, of

its business operations and processes. It also helps in evaluating the performance level

of employees and team as a whole involved in particular business activity. It helps the

management in making strategic decisions and plans for the betterment, growth of the

company. Performance related report provides a deep insight about the working

process as used in carrying on business activities (Craig and et.al., 2018). By framing

and implementing strategies and plans, business goals can be achieved and improved.

2. Cost Managerial Accounting Report – This type of management accounting report

helps in determining the amount of cost incurred for carrying on production function

of product or services of the company. While making this assessment, it takes into

account all the cost expenses related to raw material, overhead, labour and others

factors. This report helps the management of Galway Plc. in realizing the cost and

selling prices of their products and services and in estimating profit from them in the

near future.

3. Budget Report – The budget report helps in focusing on making projections and

estimation about the future related to the amount of money to be spent on carrying on

the business operations. Budget are prepared on the basis of previous experience

business has met with. Galway Plc. by making budgetary plans and strategies can

makes more profit and can conduct its business operations properly. It assists the

management of the company in making effective use of the limited budgeted amount

and resources (Maas, Schaltegger and Crutzen, 2016). With the help of budget report,

a company can make assessment of its performance as well as profitability level and

can deal with future contingencies and unproductive cost expenses.

4. Account Receivable Aging Report – This report helps in determining the amount

which is to be received from its customers to whom creditor sales has been made. It is

helpful to company especially in conducting its business operations by acquisition of

raw material etc. on credit basis. It also helps in determining the potential defaulters in

relation with the non-payment of money. Also it helps in evaluating the problem

which Galway Plc. is facing in the process of money collection as due.

which helps the company in monitoring, assessing and reviewing the performance, of

its business operations and processes. It also helps in evaluating the performance level

of employees and team as a whole involved in particular business activity. It helps the

management in making strategic decisions and plans for the betterment, growth of the

company. Performance related report provides a deep insight about the working

process as used in carrying on business activities (Craig and et.al., 2018). By framing

and implementing strategies and plans, business goals can be achieved and improved.

2. Cost Managerial Accounting Report – This type of management accounting report

helps in determining the amount of cost incurred for carrying on production function

of product or services of the company. While making this assessment, it takes into

account all the cost expenses related to raw material, overhead, labour and others

factors. This report helps the management of Galway Plc. in realizing the cost and

selling prices of their products and services and in estimating profit from them in the

near future.

3. Budget Report – The budget report helps in focusing on making projections and

estimation about the future related to the amount of money to be spent on carrying on

the business operations. Budget are prepared on the basis of previous experience

business has met with. Galway Plc. by making budgetary plans and strategies can

makes more profit and can conduct its business operations properly. It assists the

management of the company in making effective use of the limited budgeted amount

and resources (Maas, Schaltegger and Crutzen, 2016). With the help of budget report,

a company can make assessment of its performance as well as profitability level and

can deal with future contingencies and unproductive cost expenses.

4. Account Receivable Aging Report – This report helps in determining the amount

which is to be received from its customers to whom creditor sales has been made. It is

helpful to company especially in conducting its business operations by acquisition of

raw material etc. on credit basis. It also helps in determining the potential defaulters in

relation with the non-payment of money. Also it helps in evaluating the problem

which Galway Plc. is facing in the process of money collection as due.

M1. Benefits of application of the management accounting system in an organisation.

Management Accounting system helps in managing, controlling and evaluating the

business operations of the company and suggest improvement requires if any. Galway Plc.by

using this system can get benefits in following ways:

Management Accounting

System

Benefits

Cost Accounting System 1. It helps Galway Plc. in framing budget

and ensures its compliance in every

accounting period. Also, it helps in

comparing the actual costs incurred with

budgeted cost for assessing most cost

incurring part of business.

2. It helps in determining the operational

efficiency and improvement required if

any in the business (Novas, Alves and

Sousa, 2017).

Inventory Management System 1. It can help the company in minimizing the

cost related expenses which are associated

with the business operations.

2. By managing inventory, company can

improve its delivery performance among its

customer and market and increase

profitability.

3. By using this system the stock out situation

can be avoided and management can have

proper inventory level.

Job Costing System 1. The job costing system helps in evaluating

cost per job as assigned for making

effective decision process.

2. This system of management accounting

helps in monitoring and tracking the

performance level of the individual

Management Accounting system helps in managing, controlling and evaluating the

business operations of the company and suggest improvement requires if any. Galway Plc.by

using this system can get benefits in following ways:

Management Accounting

System

Benefits

Cost Accounting System 1. It helps Galway Plc. in framing budget

and ensures its compliance in every

accounting period. Also, it helps in

comparing the actual costs incurred with

budgeted cost for assessing most cost

incurring part of business.

2. It helps in determining the operational

efficiency and improvement required if

any in the business (Novas, Alves and

Sousa, 2017).

Inventory Management System 1. It can help the company in minimizing the

cost related expenses which are associated

with the business operations.

2. By managing inventory, company can

improve its delivery performance among its

customer and market and increase

profitability.

3. By using this system the stock out situation

can be avoided and management can have

proper inventory level.

Job Costing System 1. The job costing system helps in evaluating

cost per job as assigned for making

effective decision process.

2. This system of management accounting

helps in monitoring and tracking the

performance level of the individual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

employee as well as of the team for making

changes related to cost control, improving

business efficiency and productivity (King

and Clarkson, 2015).

LO 2

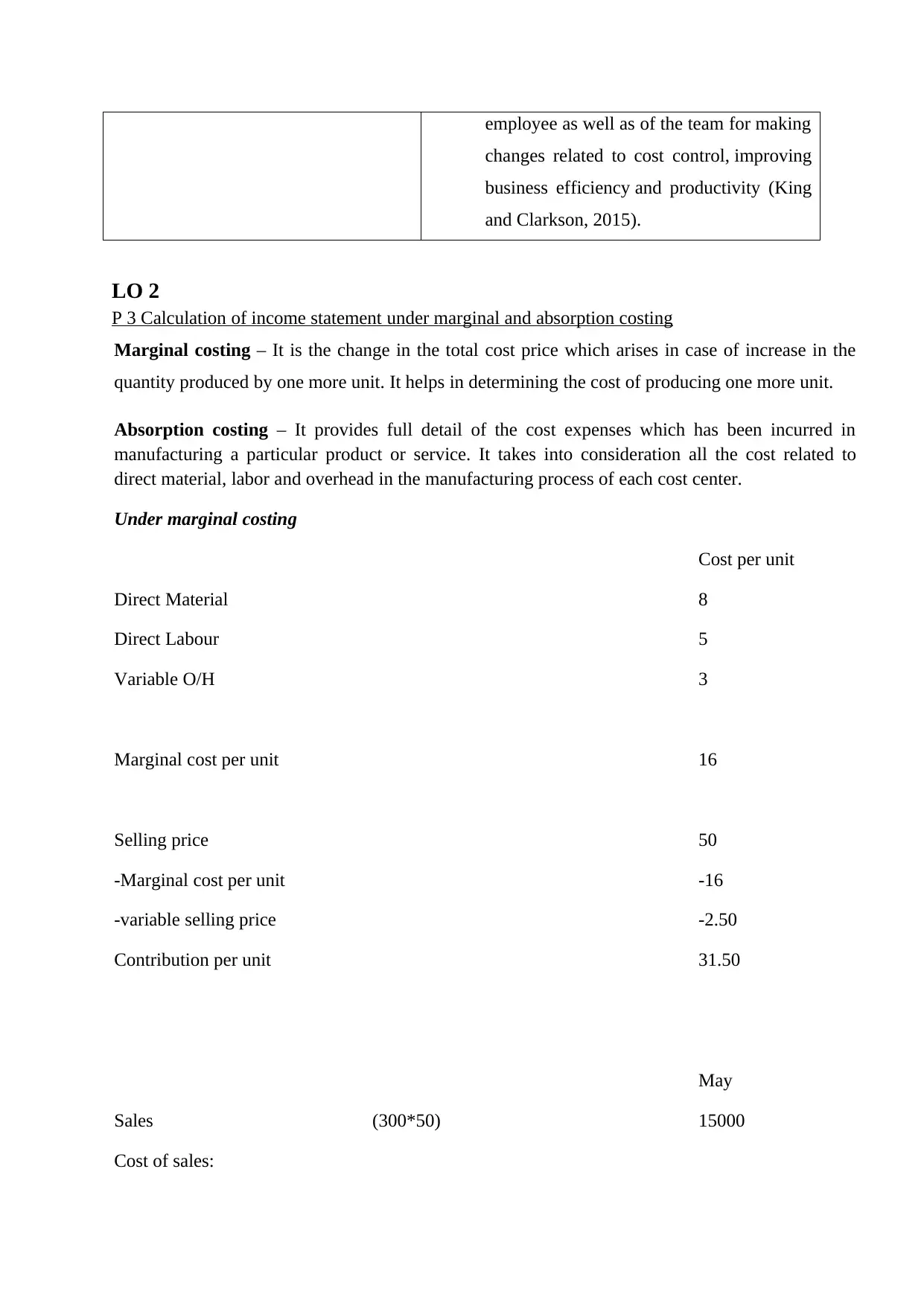

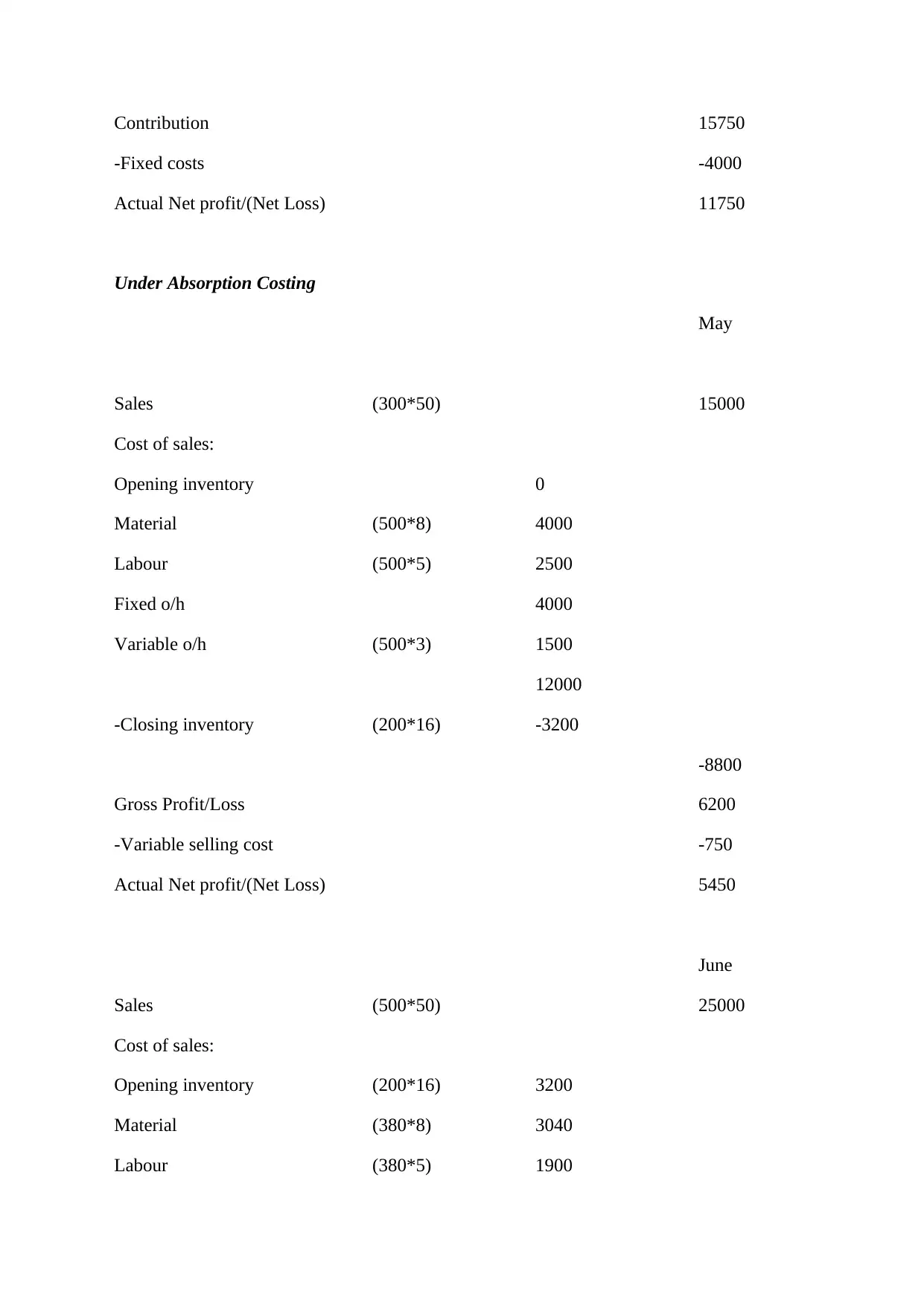

P 3 Calculation of income statement under marginal and absorption costing

Marginal costing – It is the change in the total cost price which arises in case of increase in the

quantity produced by one more unit. It helps in determining the cost of producing one more unit.

Absorption costing – It provides full detail of the cost expenses which has been incurred in

manufacturing a particular product or service. It takes into consideration all the cost related to

direct material, labor and overhead in the manufacturing process of each cost center.

Under marginal costing

Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

May

Sales (300*50) 15000

Cost of sales:

changes related to cost control, improving

business efficiency and productivity (King

and Clarkson, 2015).

LO 2

P 3 Calculation of income statement under marginal and absorption costing

Marginal costing – It is the change in the total cost price which arises in case of increase in the

quantity produced by one more unit. It helps in determining the cost of producing one more unit.

Absorption costing – It provides full detail of the cost expenses which has been incurred in

manufacturing a particular product or service. It takes into consideration all the cost related to

direct material, labor and overhead in the manufacturing process of each cost center.

Under marginal costing

Cost per unit

Direct Material 8

Direct Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

May

Sales (300*50) 15000

Cost of sales:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

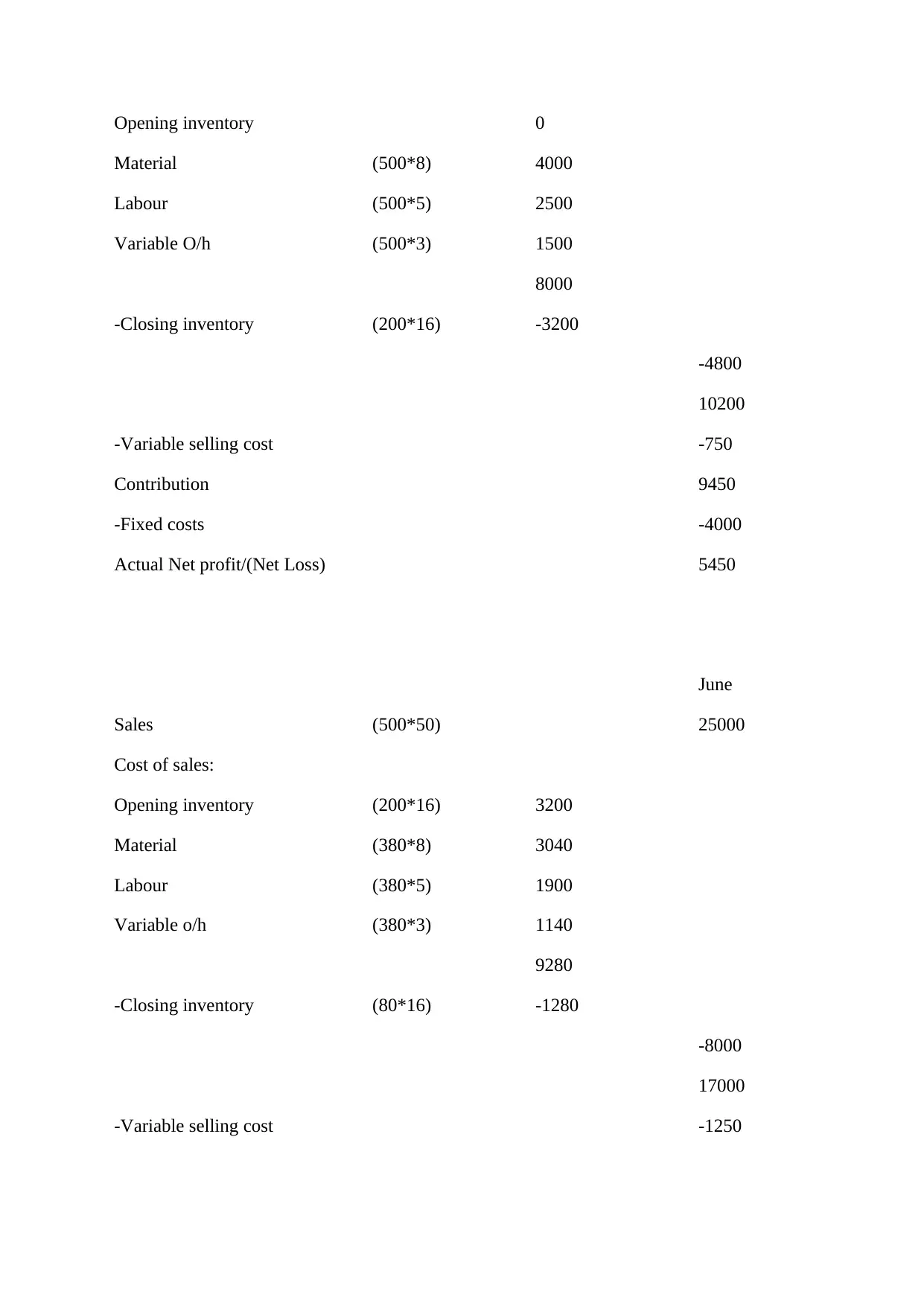

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable O/h (500*3) 1500

8000

-Closing inventory (200*16) -3200

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -4000

Actual Net profit/(Net Loss) 5450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Material (500*8) 4000

Labour (500*5) 2500

Variable O/h (500*3) 1500

8000

-Closing inventory (200*16) -3200

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -4000

Actual Net profit/(Net Loss) 5450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -4000

Actual Net profit/(Net Loss) 11750

Under Absorption Costing

May

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 4000

Variable o/h (500*3) 1500

12000

-Closing inventory (200*16) -3200

-8800

Gross Profit/Loss 6200

-Variable selling cost -750

Actual Net profit/(Net Loss) 5450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

-Fixed costs -4000

Actual Net profit/(Net Loss) 11750

Under Absorption Costing

May

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 4000

Variable o/h (500*3) 1500

12000

-Closing inventory (200*16) -3200

-8800

Gross Profit/Loss 6200

-Variable selling cost -750

Actual Net profit/(Net Loss) 5450

June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

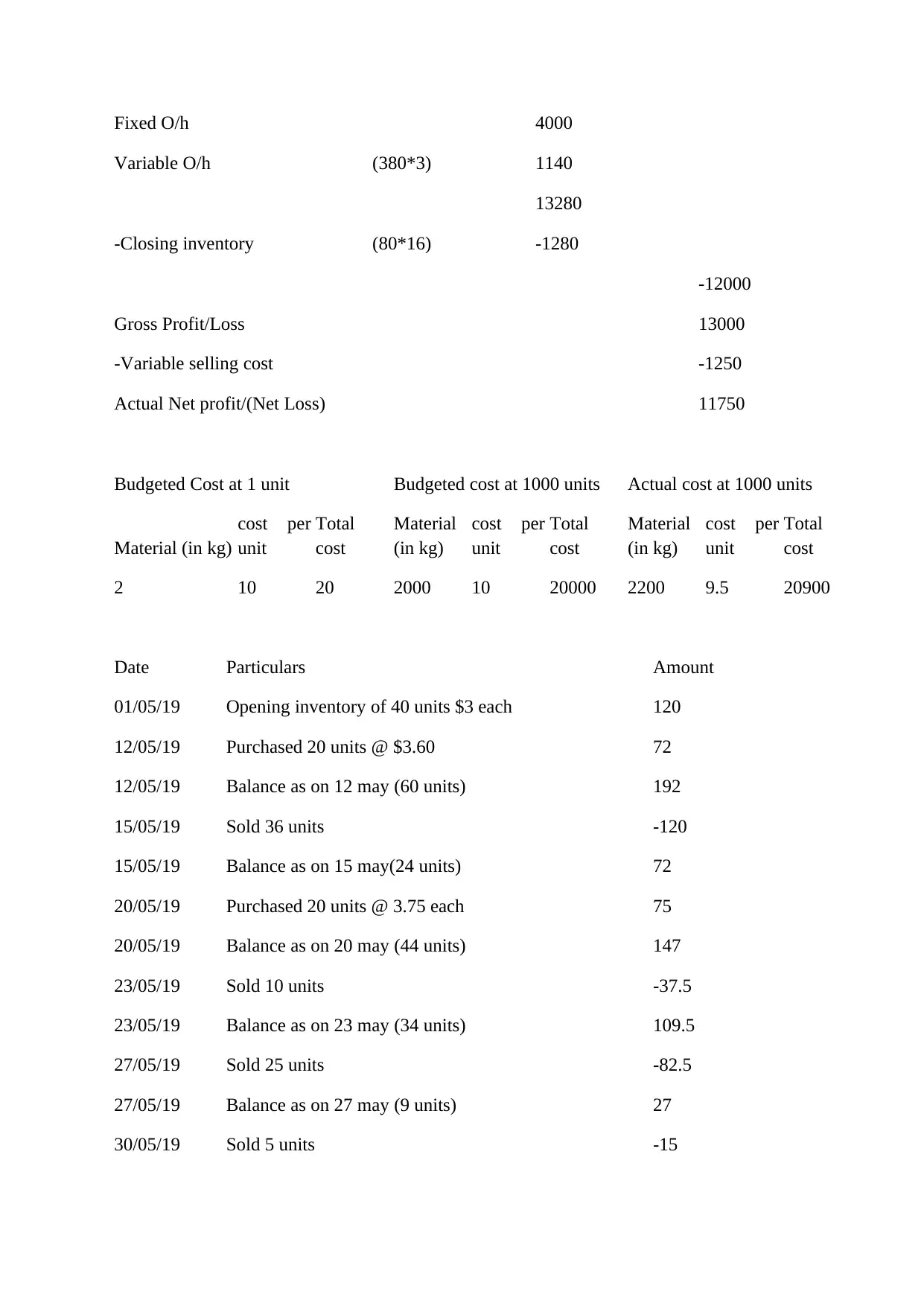

Fixed O/h 4000

Variable O/h (380*3) 1140

13280

-Closing inventory (80*16) -1280

-12000

Gross Profit/Loss 13000

-Variable selling cost -1250

Actual Net profit/(Net Loss) 11750

Budgeted Cost at 1 unit Budgeted cost at 1000 units Actual cost at 1000 units

Material (in kg)

cost per

unit

Total

cost

Material

(in kg)

cost per

unit

Total

cost

Material

(in kg)

cost per

unit

Total

cost

2 10 20 2000 10 20000 2200 9.5 20900

Date Particulars Amount

01/05/19 Opening inventory of 40 units $3 each 120

12/05/19 Purchased 20 units @ $3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

27/05/19 Balance as on 27 may (9 units) 27

30/05/19 Sold 5 units -15

Variable O/h (380*3) 1140

13280

-Closing inventory (80*16) -1280

-12000

Gross Profit/Loss 13000

-Variable selling cost -1250

Actual Net profit/(Net Loss) 11750

Budgeted Cost at 1 unit Budgeted cost at 1000 units Actual cost at 1000 units

Material (in kg)

cost per

unit

Total

cost

Material

(in kg)

cost per

unit

Total

cost

Material

(in kg)

cost per

unit

Total

cost

2 10 20 2000 10 20000 2200 9.5 20900

Date Particulars Amount

01/05/19 Opening inventory of 40 units $3 each 120

12/05/19 Purchased 20 units @ $3.60 72

12/05/19 Balance as on 12 may (60 units) 192

15/05/19 Sold 36 units -120

15/05/19 Balance as on 15 may(24 units) 72

20/05/19 Purchased 20 units @ 3.75 each 75

20/05/19 Balance as on 20 may (44 units) 147

23/05/19 Sold 10 units -37.5

23/05/19 Balance as on 23 may (34 units) 109.5

27/05/19 Sold 25 units -82.5

27/05/19 Balance as on 27 may (9 units) 27

30/05/19 Sold 5 units -15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

30/05/19 Balance as on 30 may (4 units) 12

LO 3

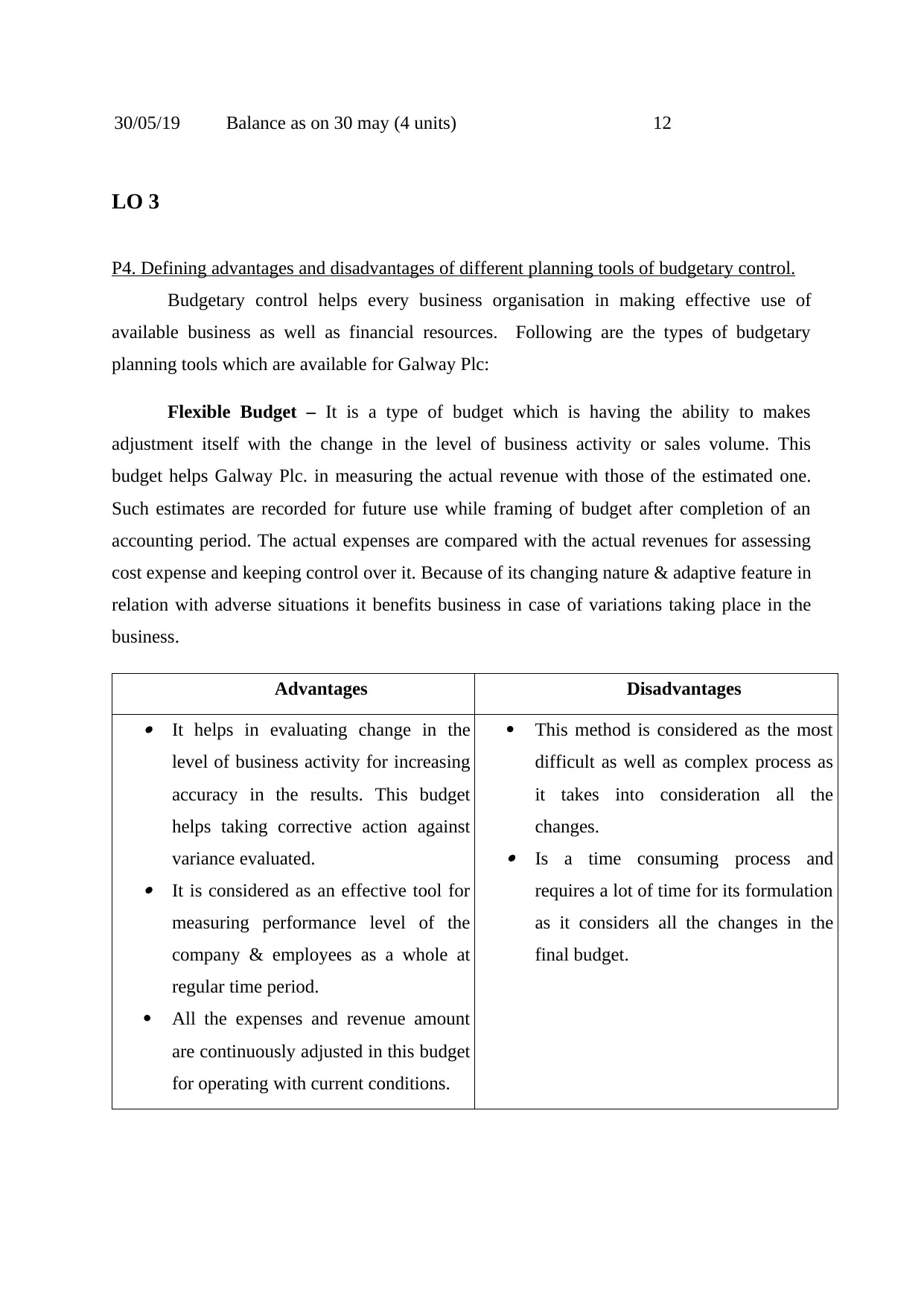

P4. Defining advantages and disadvantages of different planning tools of budgetary control.

Budgetary control helps every business organisation in making effective use of

available business as well as financial resources. Following are the types of budgetary

planning tools which are available for Galway Plc:

Flexible Budget – It is a type of budget which is having the ability to makes

adjustment itself with the change in the level of business activity or sales volume. This

budget helps Galway Plc. in measuring the actual revenue with those of the estimated one.

Such estimates are recorded for future use while framing of budget after completion of an

accounting period. The actual expenses are compared with the actual revenues for assessing

cost expense and keeping control over it. Because of its changing nature & adaptive feature in

relation with adverse situations it benefits business in case of variations taking place in the

business.

Advantages Disadvantages It helps in evaluating change in the

level of business activity for increasing

accuracy in the results. This budget

helps taking corrective action against

variance evaluated. It is considered as an effective tool for

measuring performance level of the

company & employees as a whole at

regular time period.

All the expenses and revenue amount

are continuously adjusted in this budget

for operating with current conditions.

This method is considered as the most

difficult as well as complex process as

it takes into consideration all the

changes.

Is a time consuming process and

requires a lot of time for its formulation

as it considers all the changes in the

final budget.

LO 3

P4. Defining advantages and disadvantages of different planning tools of budgetary control.

Budgetary control helps every business organisation in making effective use of

available business as well as financial resources. Following are the types of budgetary

planning tools which are available for Galway Plc:

Flexible Budget – It is a type of budget which is having the ability to makes

adjustment itself with the change in the level of business activity or sales volume. This

budget helps Galway Plc. in measuring the actual revenue with those of the estimated one.

Such estimates are recorded for future use while framing of budget after completion of an

accounting period. The actual expenses are compared with the actual revenues for assessing

cost expense and keeping control over it. Because of its changing nature & adaptive feature in

relation with adverse situations it benefits business in case of variations taking place in the

business.

Advantages Disadvantages It helps in evaluating change in the

level of business activity for increasing

accuracy in the results. This budget

helps taking corrective action against

variance evaluated. It is considered as an effective tool for

measuring performance level of the

company & employees as a whole at

regular time period.

All the expenses and revenue amount

are continuously adjusted in this budget

for operating with current conditions.

This method is considered as the most

difficult as well as complex process as

it takes into consideration all the

changes.

Is a time consuming process and

requires a lot of time for its formulation

as it considers all the changes in the

final budget.

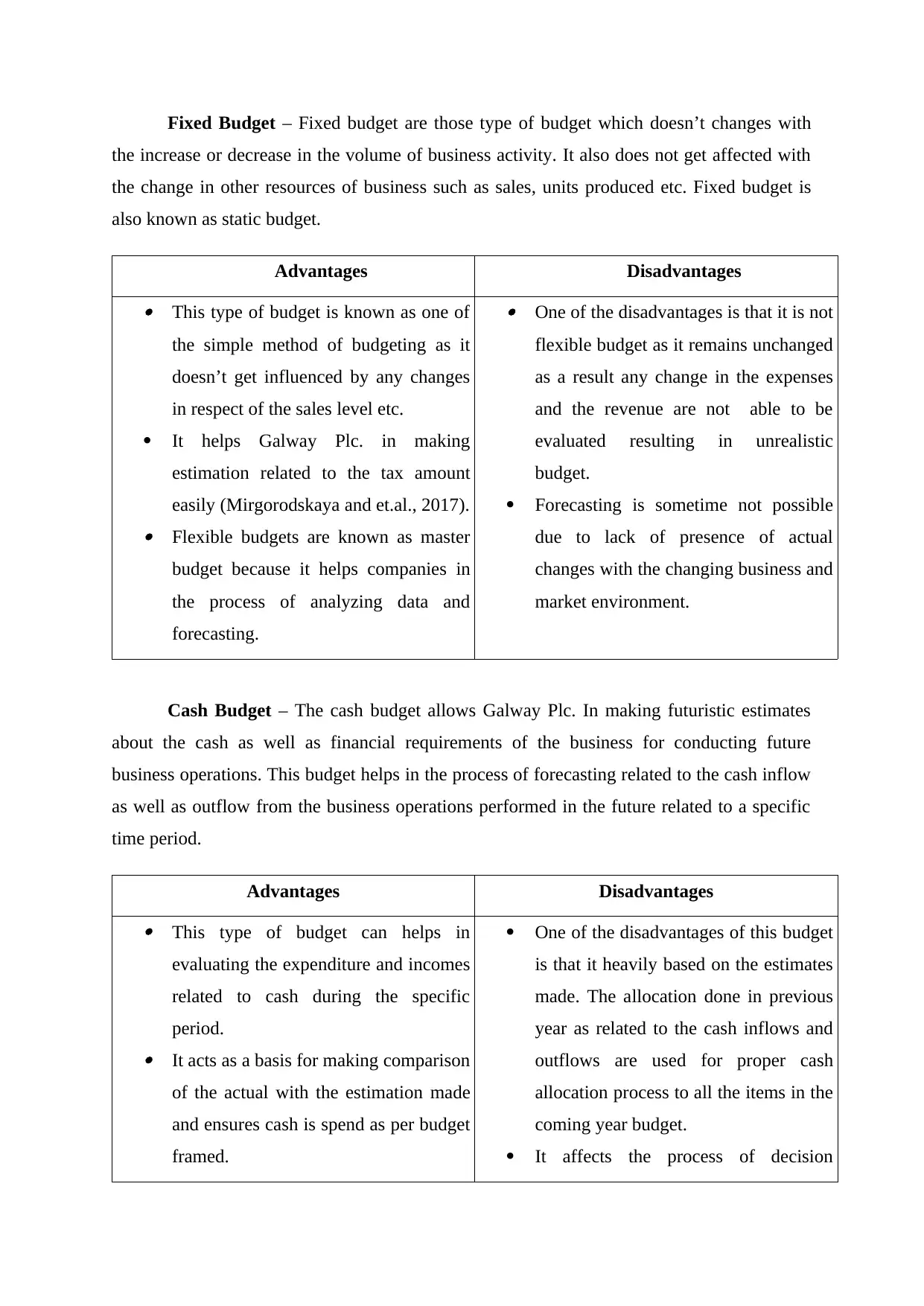

Fixed Budget – Fixed budget are those type of budget which doesn’t changes with

the increase or decrease in the volume of business activity. It also does not get affected with

the change in other resources of business such as sales, units produced etc. Fixed budget is

also known as static budget.

Advantages Disadvantages This type of budget is known as one of

the simple method of budgeting as it

doesn’t get influenced by any changes

in respect of the sales level etc.

It helps Galway Plc. in making

estimation related to the tax amount

easily (Mirgorodskaya and et.al., 2017). Flexible budgets are known as master

budget because it helps companies in

the process of analyzing data and

forecasting.

One of the disadvantages is that it is not

flexible budget as it remains unchanged

as a result any change in the expenses

and the revenue are not able to be

evaluated resulting in unrealistic

budget.

Forecasting is sometime not possible

due to lack of presence of actual

changes with the changing business and

market environment.

Cash Budget – The cash budget allows Galway Plc. In making futuristic estimates

about the cash as well as financial requirements of the business for conducting future

business operations. This budget helps in the process of forecasting related to the cash inflow

as well as outflow from the business operations performed in the future related to a specific

time period.

Advantages Disadvantages This type of budget can helps in

evaluating the expenditure and incomes

related to cash during the specific

period. It acts as a basis for making comparison

of the actual with the estimation made

and ensures cash is spend as per budget

framed.

One of the disadvantages of this budget

is that it heavily based on the estimates

made. The allocation done in previous

year as related to the cash inflows and

outflows are used for proper cash

allocation process to all the items in the

coming year budget.

It affects the process of decision

the increase or decrease in the volume of business activity. It also does not get affected with

the change in other resources of business such as sales, units produced etc. Fixed budget is

also known as static budget.

Advantages Disadvantages This type of budget is known as one of

the simple method of budgeting as it

doesn’t get influenced by any changes

in respect of the sales level etc.

It helps Galway Plc. in making

estimation related to the tax amount

easily (Mirgorodskaya and et.al., 2017). Flexible budgets are known as master

budget because it helps companies in

the process of analyzing data and

forecasting.

One of the disadvantages is that it is not

flexible budget as it remains unchanged

as a result any change in the expenses

and the revenue are not able to be

evaluated resulting in unrealistic

budget.

Forecasting is sometime not possible

due to lack of presence of actual

changes with the changing business and

market environment.

Cash Budget – The cash budget allows Galway Plc. In making futuristic estimates

about the cash as well as financial requirements of the business for conducting future

business operations. This budget helps in the process of forecasting related to the cash inflow

as well as outflow from the business operations performed in the future related to a specific

time period.

Advantages Disadvantages This type of budget can helps in

evaluating the expenditure and incomes

related to cash during the specific

period. It acts as a basis for making comparison

of the actual with the estimation made

and ensures cash is spend as per budget

framed.

One of the disadvantages of this budget

is that it heavily based on the estimates

made. The allocation done in previous

year as related to the cash inflows and

outflows are used for proper cash

allocation process to all the items in the

coming year budget.

It affects the process of decision

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.