Business Finance: Profit, Cashflow, and Working Capital

VerifiedAdded on 2021/01/01

|15

|3760

|125

Report

AI Summary

This report provides a comprehensive analysis of business finance, focusing on profit, cash flow, and working capital management. Part 1 explains the meaning of profit and cash flow, highlighting their differences, and defines key concepts like working capital, receivables, inventory, and payables. It details how changes in working capital impact cash flow and explores strategies to improve cash flow through better working capital management. Part 2 delves into financial ratios, including sales growth and profit margins, and assesses financial performance. The report uses case studies of Uber Tools Ltd and Madagascar Industries Ltd to illustrate these concepts, providing a practical understanding of financial analysis and management. The report concludes by summarizing the importance of profit, cash flow, working capital management, and financial ratios in maintaining business operations and assessing a company's financial health.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

PART 1.......................................................................................................................................3

Executive summary....................................................................................................................3

MAIN BODY.............................................................................................................................3

1- Explain:..............................................................................................................................3

a. Meaning of profit and Cashflow and difference between the both.....................................3

b. Meaning of Working Capital, Receivables, inventory and payables..................................4

c. changes in working capital impacts the cash flow..............................................................5

2) Working capital management influence the financial results of the firm........................5

3) Steps to be taken to improve company’s cash flow through better working capital

management............................................................................................................................5

CONCLUSION..........................................................................................................................6

REFERENCES...........................................................................................................................7

PART 2.......................................................................................................................................8

EXECUTIVE SUMMARY........................................................................................................8

MAIN BODY.............................................................................................................................8

1) Financial ratios...................................................................................................................8

b) Calculation of ratios...........................................................................................................9

c) Interpretation-...................................................................................................................11

2) Assessment of financial performance-.............................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................13

PART 1.......................................................................................................................................3

Executive summary....................................................................................................................3

MAIN BODY.............................................................................................................................3

1- Explain:..............................................................................................................................3

a. Meaning of profit and Cashflow and difference between the both.....................................3

b. Meaning of Working Capital, Receivables, inventory and payables..................................4

c. changes in working capital impacts the cash flow..............................................................5

2) Working capital management influence the financial results of the firm........................5

3) Steps to be taken to improve company’s cash flow through better working capital

management............................................................................................................................5

CONCLUSION..........................................................................................................................6

REFERENCES...........................................................................................................................7

PART 2.......................................................................................................................................8

EXECUTIVE SUMMARY........................................................................................................8

MAIN BODY.............................................................................................................................8

1) Financial ratios...................................................................................................................8

b) Calculation of ratios...........................................................................................................9

c) Interpretation-...................................................................................................................11

2) Assessment of financial performance-.............................................................................12

CONCLUSION........................................................................................................................13

REFERENCES.........................................................................................................................13

PART 1

Executive summary

Business finance is that business activity which is concerned with the acquisition and

conservation of capital funds in meeting financial needs and overall objectives of the business

enterprises. Present study based on Uber tool limited which deals in producing power tool

and Madagascar industry limited which is a UK listed company deals in gems and jewellery

segment. Further it explain the working capital management and financial ratios.

MAIN BODY

1- Explain:

a. Meaning of profit and Cashflow and difference between the both

Profit- The surplus that is realized when the revenue exceeds the expenses, taxes and costs of

the business. It is the difference between total revenue and total costs. Profit is a residual

income, so its size varies (Connolly and Jackman, 2017). Profit may be zero or even negative.

It is the financial gain that is used for the purpose of further investment. Higher profits leads

to the growth of the business.

Cash-flow- It is defined as the summary of receipts and expenditures of cash for a particular

period. Cash-flows are the cash inflows and outflows of the Uber Tools Ltd. Increase in cash

and cash equivalent reflects the inflows while decrease in cash and cash equivalent reflects

the outgoing of cash from the business (Roberts, 2015). These statements are prepared as per

the Accounting standards 3. It enables the firm in knowing the cash position of its business.

Difference:-

Profit Cashflow

It is the money left after the payment of all

the expenses, taxes and costs.

It represents money from several sources.

Profitability indicates the growth of the

Uber tools Ltd.

Cash-flow states the operating, investing

and financing activities of the company.

It is not critical to the firm’s survival. It is critical for the firm’s survival.

It reflects the financial performance of the

business.

It demonstrates the cash position of the

enterprise.

Executive summary

Business finance is that business activity which is concerned with the acquisition and

conservation of capital funds in meeting financial needs and overall objectives of the business

enterprises. Present study based on Uber tool limited which deals in producing power tool

and Madagascar industry limited which is a UK listed company deals in gems and jewellery

segment. Further it explain the working capital management and financial ratios.

MAIN BODY

1- Explain:

a. Meaning of profit and Cashflow and difference between the both

Profit- The surplus that is realized when the revenue exceeds the expenses, taxes and costs of

the business. It is the difference between total revenue and total costs. Profit is a residual

income, so its size varies (Connolly and Jackman, 2017). Profit may be zero or even negative.

It is the financial gain that is used for the purpose of further investment. Higher profits leads

to the growth of the business.

Cash-flow- It is defined as the summary of receipts and expenditures of cash for a particular

period. Cash-flows are the cash inflows and outflows of the Uber Tools Ltd. Increase in cash

and cash equivalent reflects the inflows while decrease in cash and cash equivalent reflects

the outgoing of cash from the business (Roberts, 2015). These statements are prepared as per

the Accounting standards 3. It enables the firm in knowing the cash position of its business.

Difference:-

Profit Cashflow

It is the money left after the payment of all

the expenses, taxes and costs.

It represents money from several sources.

Profitability indicates the growth of the

Uber tools Ltd.

Cash-flow states the operating, investing

and financing activities of the company.

It is not critical to the firm’s survival. It is critical for the firm’s survival.

It reflects the financial performance of the

business.

It demonstrates the cash position of the

enterprise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b. Meaning of Working Capital, Receivables, inventory and payables

Working Capital- It is that capital which is involved in the current assets of the

business. It is the capital which is required to meet the day-to-day expenses of the entity.

Working Capital includes those assets and liabilities which can be converted into cash within

one year. Net working capital is the difference between the current assets and current

liabilities (What Is the Meaning of Business Finance,2019). Current assets include the cash,

receivables and inventory etc. while current liabilities includes the creditors, payable and

overdraft. It is essential for every organization to manage its working capital effectively and

efficiently to reach the sound liquidity position and to achieve higher profits.

Receivables- Account receivables are the asset accounts representing amount owed to

the firm as a result of the sale of goods or services in the ordinary course of business

(Mathuva, 2015). It represents the claims of the firm against its customers and is

carried to the “asset side” of the balance sheet under the titles such as bills

receivables, customer receivables or book debts. It is the result of extension of credit

facility to the customers for a reasonable period of time in which they can pay for the

goods purchased by them. Accounts receivables are created because of credited sales.

Hence, the purpose of receivables is directly connected with the objectives of making

credited sales.

Inventory- It means stock of goods, or a list of goods. It may include raw material,

work-in-progress and finished goods. A stock of items held to meet future demand.

Inventory is a list for goods and materials that are available as stock by a business.

Inventory management is important for the firm to attain and uphold an optimal

inventory of goods while also taking note of all orders, shipping, handling and other

associated costs (Connolly and Jackman, 2017).

Payables- Accounts payable is the amount owed for the purchase of goods or services

at a specific date. It is the money that a company owes to vendors for products and

services purchased on credit extended in the normal course of business. Supplier

offers credit to their customers, which is an arrangement of payment to pay for a

product or service after it has already been received. Payables are presented as current

liabilities under the liability section of the balance sheet. It represents a negative cash

flow for the company. It is considered as the short term credit extended to the

business expected to be fulfilled in less than a year.

Working Capital- It is that capital which is involved in the current assets of the

business. It is the capital which is required to meet the day-to-day expenses of the entity.

Working Capital includes those assets and liabilities which can be converted into cash within

one year. Net working capital is the difference between the current assets and current

liabilities (What Is the Meaning of Business Finance,2019). Current assets include the cash,

receivables and inventory etc. while current liabilities includes the creditors, payable and

overdraft. It is essential for every organization to manage its working capital effectively and

efficiently to reach the sound liquidity position and to achieve higher profits.

Receivables- Account receivables are the asset accounts representing amount owed to

the firm as a result of the sale of goods or services in the ordinary course of business

(Mathuva, 2015). It represents the claims of the firm against its customers and is

carried to the “asset side” of the balance sheet under the titles such as bills

receivables, customer receivables or book debts. It is the result of extension of credit

facility to the customers for a reasonable period of time in which they can pay for the

goods purchased by them. Accounts receivables are created because of credited sales.

Hence, the purpose of receivables is directly connected with the objectives of making

credited sales.

Inventory- It means stock of goods, or a list of goods. It may include raw material,

work-in-progress and finished goods. A stock of items held to meet future demand.

Inventory is a list for goods and materials that are available as stock by a business.

Inventory management is important for the firm to attain and uphold an optimal

inventory of goods while also taking note of all orders, shipping, handling and other

associated costs (Connolly and Jackman, 2017).

Payables- Accounts payable is the amount owed for the purchase of goods or services

at a specific date. It is the money that a company owes to vendors for products and

services purchased on credit extended in the normal course of business. Supplier

offers credit to their customers, which is an arrangement of payment to pay for a

product or service after it has already been received. Payables are presented as current

liabilities under the liability section of the balance sheet. It represents a negative cash

flow for the company. It is considered as the short term credit extended to the

business expected to be fulfilled in less than a year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c. changes in working capital impacts the cash flow

As the working capital reflects the difference between the short term assets and short

term liabilities and the changes in the working capital are recorded in the operating cash flow

segment of the cash flow statement. Cash inflows and outflows get affected with changes in

the current assets and liabilities. The figure of working capital is said to be positive when

current assets exceeds the current liability which states that cash inflows are higher than cash

outflow. On the contrary, negative resultant of working capital indicates that cash outflows

are greater than cash inflows. If the short term assets and liability increases or decreases with

the same amount then the working capital will not have any effect (Durand, 2019. ).

For example- Purchase of inventory leads to payment of cash while selling of stock leads to

receivable of cash.

2) Working capital management influence the financial results of the firm

Working capital management is an accounting strategy that focuses on managing the

firm’s current assets and liabilities efficiently and effectively. It enables the organization in

ensuring the adequate cash flow in relation to meeting the short term obligations and routine

expenses. Working capital management is an important aspect of finance as it directly linked

with the liquidity and profitability position of the firm. The current assets of the entity should

be managed adequately. Excess of current assets leads to standard income on investment

while too low current assets results difficulty in functioning of operations smoothly. Working

capital management assists the firm in creating the value and to achieve the competitive

advantage by maintaining the optimal balance between the components of working capital

that are cash, receivables, inventory and payables. A well managed working capital impacts

positively to the financial performance of the enterprise. Excessive investment in the working

capital causes a reduction in the profits of the business because too much amount will be

engaged in the inventory and other current assets (Brown, 2019). On the other side too little

investment in working capital increases the risk in meeting the commitments. Therefore, it is

very essential for every company to maintain an adequate level of working capital so that any

uncertaininty or risk gets eliminated in the near future and the operations run smoothly.

3) Steps to be taken to improve company’s cash flow through better working capital

management

Working capital management refers to the management of current assets and current

liabilities with the objective of maintaining liquidity and attaining profitability of the Uber

As the working capital reflects the difference between the short term assets and short

term liabilities and the changes in the working capital are recorded in the operating cash flow

segment of the cash flow statement. Cash inflows and outflows get affected with changes in

the current assets and liabilities. The figure of working capital is said to be positive when

current assets exceeds the current liability which states that cash inflows are higher than cash

outflow. On the contrary, negative resultant of working capital indicates that cash outflows

are greater than cash inflows. If the short term assets and liability increases or decreases with

the same amount then the working capital will not have any effect (Durand, 2019. ).

For example- Purchase of inventory leads to payment of cash while selling of stock leads to

receivable of cash.

2) Working capital management influence the financial results of the firm

Working capital management is an accounting strategy that focuses on managing the

firm’s current assets and liabilities efficiently and effectively. It enables the organization in

ensuring the adequate cash flow in relation to meeting the short term obligations and routine

expenses. Working capital management is an important aspect of finance as it directly linked

with the liquidity and profitability position of the firm. The current assets of the entity should

be managed adequately. Excess of current assets leads to standard income on investment

while too low current assets results difficulty in functioning of operations smoothly. Working

capital management assists the firm in creating the value and to achieve the competitive

advantage by maintaining the optimal balance between the components of working capital

that are cash, receivables, inventory and payables. A well managed working capital impacts

positively to the financial performance of the enterprise. Excessive investment in the working

capital causes a reduction in the profits of the business because too much amount will be

engaged in the inventory and other current assets (Brown, 2019). On the other side too little

investment in working capital increases the risk in meeting the commitments. Therefore, it is

very essential for every company to maintain an adequate level of working capital so that any

uncertaininty or risk gets eliminated in the near future and the operations run smoothly.

3) Steps to be taken to improve company’s cash flow through better working capital

management

Working capital management refers to the management of current assets and current

liabilities with the objective of maintaining liquidity and attaining profitability of the Uber

tools Ltd. Working capital management establishes the best possible trade-off between the

profitability from net current assets employed and the ability for paying the current liabilities

as they become due.

Incentivize Receivables- Giving incentives to those customers who make payment on

time. Not transacting with such customers who has defaulted in the past years

regarding the payment. Timely action should be taken for delay in payment to

prevent the account from aging.

Fulfilling Debt obligation- By meeting the short term obligation on time using e-

payment techniques helps the Uber tools Ltd in improving the cash flow as it avoids

the penalty for delayed payments.

Manage inventory- Maintaining adequate level of inventory improves the cash flow as

it helps in cutting those products that are idle or not performing (Harris, 2019). The

inventory should not be overstocked and the finished goods need to be sold as quickly

as possible so that idle stocks are not left over in the warehouse.

Analyze costs- identifying the wasteful expenditure and taking necessary steps to

reduce such costs so that firm can reach the better liquidity position. This also helps in

increasing the revenue of the company.

Examining interest payments- Early payment of the interest on loans helps the firm in

reducing the future cost of installment. Borrowing loans at lower interest rate acts as a

saving to the Uber tools Ltd cash flow and leads to better working capital.

Using financial information- updating the financial statements and evaluating the

quick ratio at a regular interval enables the firm in knowing its financial position. By

this the entity can take timely action for any improvement (Harris, 2019).

CONCLUSION

From the above report it is concluded that profits and the cash flow are the essential part of

the business in maintaining the operations and for investing the money into various growth

channels so that Uber tools Ltd can functions its business with sustainability in the future.

Working capital management is also an important aspect of the company as it leads to

effective and efficient developing of cash flow and the liquidity and profitability can be

assessed with execellence.

profitability from net current assets employed and the ability for paying the current liabilities

as they become due.

Incentivize Receivables- Giving incentives to those customers who make payment on

time. Not transacting with such customers who has defaulted in the past years

regarding the payment. Timely action should be taken for delay in payment to

prevent the account from aging.

Fulfilling Debt obligation- By meeting the short term obligation on time using e-

payment techniques helps the Uber tools Ltd in improving the cash flow as it avoids

the penalty for delayed payments.

Manage inventory- Maintaining adequate level of inventory improves the cash flow as

it helps in cutting those products that are idle or not performing (Harris, 2019). The

inventory should not be overstocked and the finished goods need to be sold as quickly

as possible so that idle stocks are not left over in the warehouse.

Analyze costs- identifying the wasteful expenditure and taking necessary steps to

reduce such costs so that firm can reach the better liquidity position. This also helps in

increasing the revenue of the company.

Examining interest payments- Early payment of the interest on loans helps the firm in

reducing the future cost of installment. Borrowing loans at lower interest rate acts as a

saving to the Uber tools Ltd cash flow and leads to better working capital.

Using financial information- updating the financial statements and evaluating the

quick ratio at a regular interval enables the firm in knowing its financial position. By

this the entity can take timely action for any improvement (Harris, 2019).

CONCLUSION

From the above report it is concluded that profits and the cash flow are the essential part of

the business in maintaining the operations and for investing the money into various growth

channels so that Uber tools Ltd can functions its business with sustainability in the future.

Working capital management is also an important aspect of the company as it leads to

effective and efficient developing of cash flow and the liquidity and profitability can be

assessed with execellence.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Connolly, E. and Jackman, B., 2017. The Availability of Business Finance. RBA Bulletin,

pp.55-66.

Durand, P., 2019. On the impact of capital and liquidity ratios on financial stability (No.

2019-4). University of Paris Nanterre, EconomiX.

Locker, A. and Grosse-Ruyken, P. T., 2019. Working Capital Management. In Chefsache

Finanzen in Einkauf und Supply Chain (pp. 135-171). Springer Gabler, Wiesbaden.

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Roberts, R., 2015. Finance for small and entrepreneurial business. Routledge.

Online

What Is the Meaning of Business Finance.2019.[Online].Available through. <

https://smallbusiness.chron.com/meaning-business-finance-4108.html >

Connolly, E. and Jackman, B., 2017. The Availability of Business Finance. RBA Bulletin,

pp.55-66.

Durand, P., 2019. On the impact of capital and liquidity ratios on financial stability (No.

2019-4). University of Paris Nanterre, EconomiX.

Locker, A. and Grosse-Ruyken, P. T., 2019. Working Capital Management. In Chefsache

Finanzen in Einkauf und Supply Chain (pp. 135-171). Springer Gabler, Wiesbaden.

Mathuva, D., 2015. The Influence of working capital management components on corporate

profitability.

Roberts, R., 2015. Finance for small and entrepreneurial business. Routledge.

Online

What Is the Meaning of Business Finance.2019.[Online].Available through. <

https://smallbusiness.chron.com/meaning-business-finance-4108.html >

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART 2

EXECUTIVE SUMMARY

The ratio analysis is one of the most powerful tools of financial analysis. It is use as a device

to analysis and interprets the financial health of the Madagascar industries Ltd. It is very

helpful in financial forecasting and facilitates the evaluation of the financial position and

performance. The report summarizes that the performance of the industry is ascertained by

assessing the ratios and the changes in each of the ratio impacts the operations, profitability

and the liquidity of the industry.

MAIN BODY

1) Financial ratios

a) Description of the financial performance of the ratios

Sales growth- It indicates the percentage change in the revenue growth between the

current year sales and the past year sales. It depicts the increase and decrease in the sales of

the Madagascar Industries Ltd from one period to another. This ratio shows the revenue

trends of the business.

Gross profit margin- It is a profitability ratio that states the relationship between the

net sales and the gross profit of the Madagascar industries Ltd. It is a tool that helps in

evaluating the operational profits of the business. It is calculated by dividing the gross profits

by net sales. When the ratio is depicted in percentage form it is called as gross profit margin.

Gross profit is computed as subtracting cost of goods sold from the net sales.

Operating profit margin- operating margin ratio is the ratio of operating income to

the revenue of the business. It highlights the operating income of the Madagascar industries

Ltd as a percentage of the revenue. It tells about the contribution of company’s operations

towards the profitability. The higher the ratio, the better it is. A high operating profit margin

indicates that a firm can make a reasonable profit on sales, as long as it does good tax

planning.

EXECUTIVE SUMMARY

The ratio analysis is one of the most powerful tools of financial analysis. It is use as a device

to analysis and interprets the financial health of the Madagascar industries Ltd. It is very

helpful in financial forecasting and facilitates the evaluation of the financial position and

performance. The report summarizes that the performance of the industry is ascertained by

assessing the ratios and the changes in each of the ratio impacts the operations, profitability

and the liquidity of the industry.

MAIN BODY

1) Financial ratios

a) Description of the financial performance of the ratios

Sales growth- It indicates the percentage change in the revenue growth between the

current year sales and the past year sales. It depicts the increase and decrease in the sales of

the Madagascar Industries Ltd from one period to another. This ratio shows the revenue

trends of the business.

Gross profit margin- It is a profitability ratio that states the relationship between the

net sales and the gross profit of the Madagascar industries Ltd. It is a tool that helps in

evaluating the operational profits of the business. It is calculated by dividing the gross profits

by net sales. When the ratio is depicted in percentage form it is called as gross profit margin.

Gross profit is computed as subtracting cost of goods sold from the net sales.

Operating profit margin- operating margin ratio is the ratio of operating income to

the revenue of the business. It highlights the operating income of the Madagascar industries

Ltd as a percentage of the revenue. It tells about the contribution of company’s operations

towards the profitability. The higher the ratio, the better it is. A high operating profit margin

indicates that a firm can make a reasonable profit on sales, as long as it does good tax

planning.

Gearing ratio- The gearing ratio looks at the financial leverage of the business. It

compares the proportion of equity v/s debt that the business is using to finance its assets. A

high ratio often indicates that the business has been aggressive in financing growth via debt

(Penman, 2015). This can be an issue due to interest expenses, especially in volatile

economic times. It compares owner’s equity to borrowed funds and shows how risky the

company is financially.

Interest cover- It measures a Madagascar industries Ltd operating profit relative to the

amount of interest charges which the company pays. It indicates the comfort with which the

firm may be able to service he interest expense on its outstanding debt. Higher the interest

coverage ratio, higher the capability of the company to meet its interest expenses pertaining

to its debt obligations and vice versa.

Liquidity ratio- These ratios analyze the short-term financial position of a firm and

indicate the ability of the firm to meet its short-term commitments out of its current

resources. They are also known as solvency ratios. Current ratio and quick ratio comes under

the purview f liquidity ratio. Higher the liquidity ratio, higher the cash holding in the business

that can be utilized in future and other areas while low liquidity ratio indicates that the firm is

facing trouble in meeting its current obligations.

Return on equity- It means the amount of net income returned as a percentage of

shareholders equity. Return on equity measures a corporation’s profitability by revealing how

much profit a company generates with the money shareholders have invested. Generally

return on equity of around 15-20% is considered as a good ratio.

Return on capital employed- This is the most appropriate indicator of the earning

power of the capital employed in the business. It also acts as a pointer to the management

showing the progress or deterioration in the earning capacity and efficiency of the business

(Brown, 2019). An ideal capital employed ratio is equal to 15% or above and reflects the

higher productivity of the capital employed and vice versa.

b) Calculation of ratios

Ratio Analysis

particular Formula 2009 2010 2011

compares the proportion of equity v/s debt that the business is using to finance its assets. A

high ratio often indicates that the business has been aggressive in financing growth via debt

(Penman, 2015). This can be an issue due to interest expenses, especially in volatile

economic times. It compares owner’s equity to borrowed funds and shows how risky the

company is financially.

Interest cover- It measures a Madagascar industries Ltd operating profit relative to the

amount of interest charges which the company pays. It indicates the comfort with which the

firm may be able to service he interest expense on its outstanding debt. Higher the interest

coverage ratio, higher the capability of the company to meet its interest expenses pertaining

to its debt obligations and vice versa.

Liquidity ratio- These ratios analyze the short-term financial position of a firm and

indicate the ability of the firm to meet its short-term commitments out of its current

resources. They are also known as solvency ratios. Current ratio and quick ratio comes under

the purview f liquidity ratio. Higher the liquidity ratio, higher the cash holding in the business

that can be utilized in future and other areas while low liquidity ratio indicates that the firm is

facing trouble in meeting its current obligations.

Return on equity- It means the amount of net income returned as a percentage of

shareholders equity. Return on equity measures a corporation’s profitability by revealing how

much profit a company generates with the money shareholders have invested. Generally

return on equity of around 15-20% is considered as a good ratio.

Return on capital employed- This is the most appropriate indicator of the earning

power of the capital employed in the business. It also acts as a pointer to the management

showing the progress or deterioration in the earning capacity and efficiency of the business

(Brown, 2019). An ideal capital employed ratio is equal to 15% or above and reflects the

higher productivity of the capital employed and vice versa.

b) Calculation of ratios

Ratio Analysis

particular Formula 2009 2010 2011

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

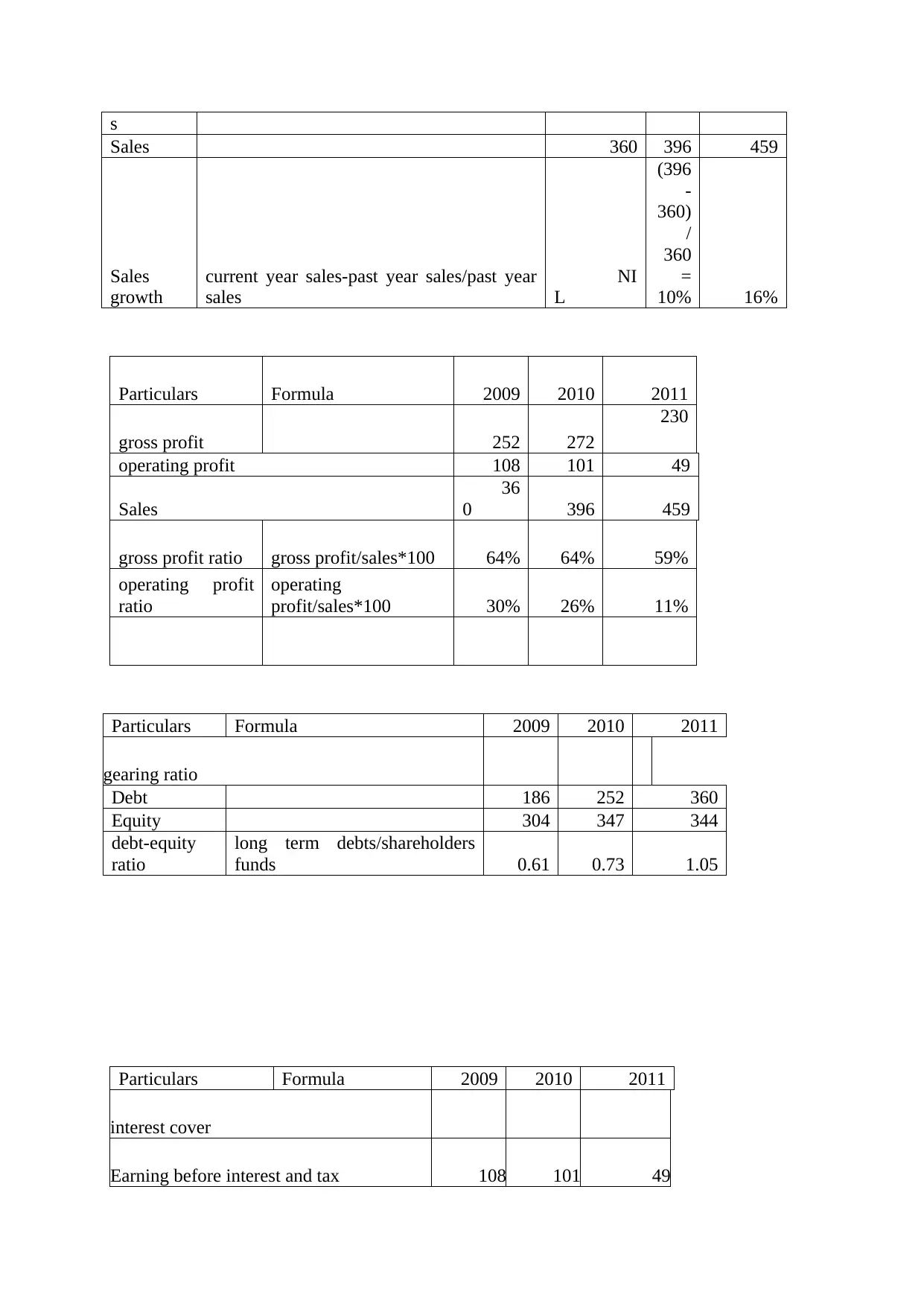

s

Sales 360 396 459

Sales

growth

current year sales-past year sales/past year

sales

NI

L

(396

-

360)

/

360

=

10% 16%

Particulars Formula 2009 2010 2011

gross profit 252 272

230

operating profit 108 101 49

Sales

36

0 396 459

gross profit ratio gross profit/sales*100 64% 64% 59%

operating profit

ratio

operating

profit/sales*100 30% 26% 11%

Particulars Formula 2009 2010 2011

gearing ratio

Debt 186 252 360

Equity 304 347 344

debt-equity

ratio

long term debts/shareholders

funds 0.61 0.73 1.05

Particulars Formula 2009 2010 2011

interest cover

Earning before interest and tax 108 101 49

Sales 360 396 459

Sales

growth

current year sales-past year sales/past year

sales

NI

L

(396

-

360)

/

360

=

10% 16%

Particulars Formula 2009 2010 2011

gross profit 252 272

230

operating profit 108 101 49

Sales

36

0 396 459

gross profit ratio gross profit/sales*100 64% 64% 59%

operating profit

ratio

operating

profit/sales*100 30% 26% 11%

Particulars Formula 2009 2010 2011

gearing ratio

Debt 186 252 360

Equity 304 347 344

debt-equity

ratio

long term debts/shareholders

funds 0.61 0.73 1.05

Particulars Formula 2009 2010 2011

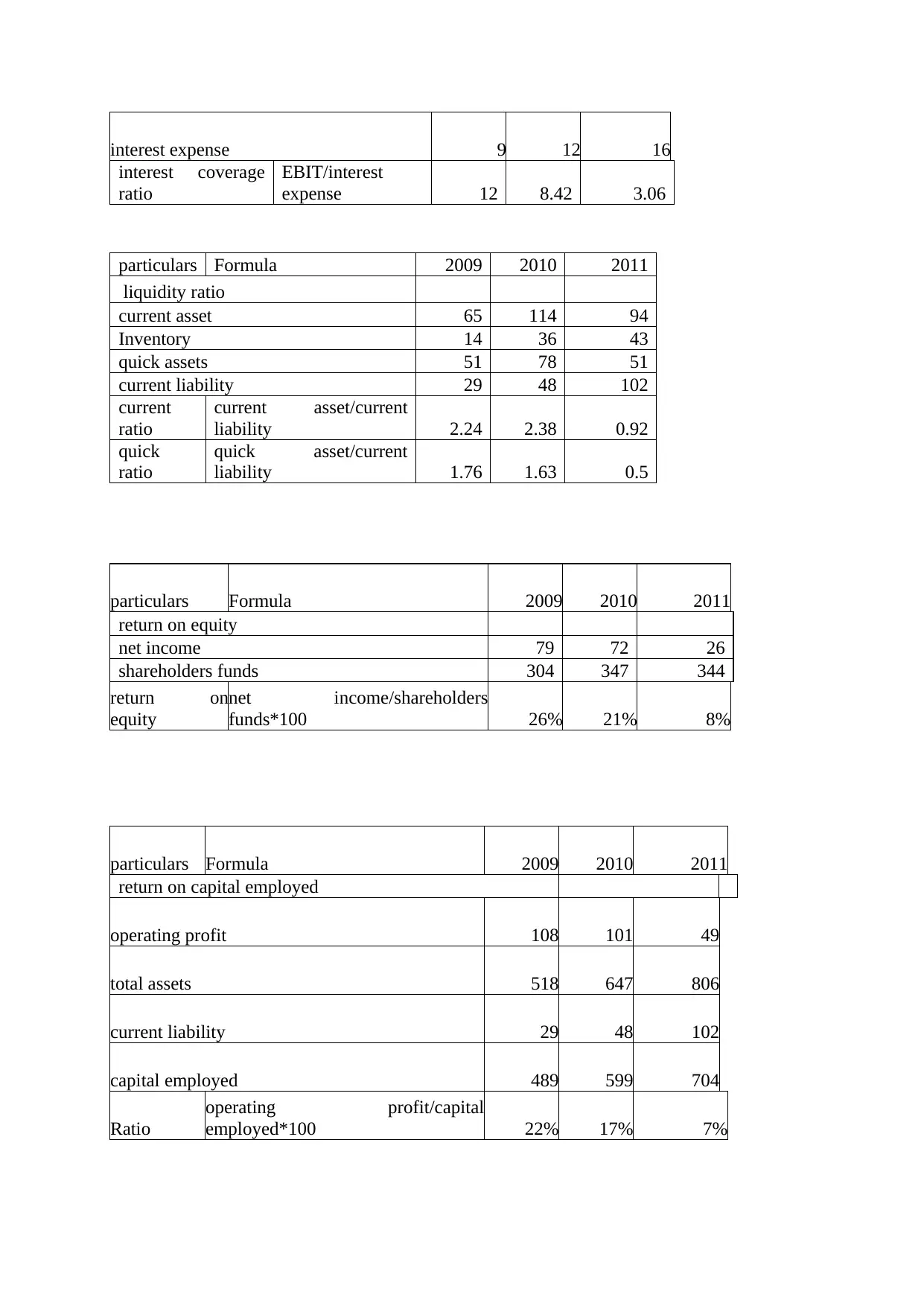

interest cover

Earning before interest and tax 108 101 49

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

interest expense 9 12 16

interest coverage

ratio

EBIT/interest

expense 12 8.42 3.06

particulars Formula 2009 2010 2011

liquidity ratio

current asset 65 114 94

Inventory 14 36 43

quick assets 51 78 51

current liability 29 48 102

current

ratio

current asset/current

liability 2.24 2.38 0.92

quick

ratio

quick asset/current

liability 1.76 1.63 0.5

particulars Formula 2009 2010 2011

return on equity

net income 79 72 26

shareholders funds 304 347 344

return on

equity

net income/shareholders

funds*100 26% 21% 8%

particulars Formula 2009 2010 2011

return on capital employed

operating profit 108 101 49

total assets 518 647 806

current liability 29 48 102

capital employed 489 599 704

Ratio

operating profit/capital

employed*100 22% 17% 7%

interest coverage

ratio

EBIT/interest

expense 12 8.42 3.06

particulars Formula 2009 2010 2011

liquidity ratio

current asset 65 114 94

Inventory 14 36 43

quick assets 51 78 51

current liability 29 48 102

current

ratio

current asset/current

liability 2.24 2.38 0.92

quick

ratio

quick asset/current

liability 1.76 1.63 0.5

particulars Formula 2009 2010 2011

return on equity

net income 79 72 26

shareholders funds 304 347 344

return on

equity

net income/shareholders

funds*100 26% 21% 8%

particulars Formula 2009 2010 2011

return on capital employed

operating profit 108 101 49

total assets 518 647 806

current liability 29 48 102

capital employed 489 599 704

Ratio

operating profit/capital

employed*100 22% 17% 7%

c) Interpretation-

From the above analysis it is interpreted that the sales of the Madagascar industries

Ltd has been increased from 10% to 16% in the current year which states that the revenue of

the company has increased by reaching higher sales in 2011. The profitability ratio includes

the gross profit and operating profit ratio that is decreased from the past year resulted as 64%

to 59% and from 30% to 11%. It means a huge decrease in the margin which indicates a

negative sign for the entity as the profitability of the business is at downfall. The gearing

ratio of the Madagascar industries Ltd is at increasing trend year by year that is from 0.61 to

1.05 in the current year which depicts a negative sign for the organization as it is more

moving towards the borrowed funds and more of the financing is done through leveraging

which makes risky for the industry to run sustainably in the future. The interest coverage ratio

of the enterprise is decreasing from 12 to 3.06 which indicate that the firm is losing its ability

to meet its interest expense in coming years which can cause a negative impact on the image

of the company. The liquidity ratio involves the current ratio that is resulted as reducing from

2.24 to 0.92 and the quick ratio is also reducing from 1.76 to 0.5 that means the ability of the

Madagascar in meeting its short term obligation is reducing from previous years. The return

on equity is also at a decreasing trend that is from 26% to 8% which affects the entity’s

growth adversely. The return on capital employed is lowering from 22% to 7% which

demonstrates the negative effect on the investments made by the firm.

2) Assessment of financial performance-

The Madagascar industries Ltd can assess the financial performance by analyzing the

financial ratios. The sales growth enables the firm in knowing its changing trends in the sales

so that it can determine its increase or decrease in revenue. The gross profit ratio helps the

company in evaluating the operational performance of its business. The operating profit ratio

assists the industry in attaining the results relating to its operating profits so that overall

profitability could be known by the company (Harris, 2019.). The gearing ratio measures the

leverage position of the firm so that necessary steps can be taken if the company is facing

high borrowed funds. Interest coverage ratio helps the Madagascar industries limited in

ascertaining its ability to meet its interest expenses so that it could maintain and keep control

over its expenses. Liquidity ratio ensures the liquidity position of the firm. The return on

equity ratio enables the enterprise in determining its income from the shareholders funds that

directly links to the financial performance of the business. The return on capital employed

helps the industry in assessing the income generated from its capital employed so that it could

From the above analysis it is interpreted that the sales of the Madagascar industries

Ltd has been increased from 10% to 16% in the current year which states that the revenue of

the company has increased by reaching higher sales in 2011. The profitability ratio includes

the gross profit and operating profit ratio that is decreased from the past year resulted as 64%

to 59% and from 30% to 11%. It means a huge decrease in the margin which indicates a

negative sign for the entity as the profitability of the business is at downfall. The gearing

ratio of the Madagascar industries Ltd is at increasing trend year by year that is from 0.61 to

1.05 in the current year which depicts a negative sign for the organization as it is more

moving towards the borrowed funds and more of the financing is done through leveraging

which makes risky for the industry to run sustainably in the future. The interest coverage ratio

of the enterprise is decreasing from 12 to 3.06 which indicate that the firm is losing its ability

to meet its interest expense in coming years which can cause a negative impact on the image

of the company. The liquidity ratio involves the current ratio that is resulted as reducing from

2.24 to 0.92 and the quick ratio is also reducing from 1.76 to 0.5 that means the ability of the

Madagascar in meeting its short term obligation is reducing from previous years. The return

on equity is also at a decreasing trend that is from 26% to 8% which affects the entity’s

growth adversely. The return on capital employed is lowering from 22% to 7% which

demonstrates the negative effect on the investments made by the firm.

2) Assessment of financial performance-

The Madagascar industries Ltd can assess the financial performance by analyzing the

financial ratios. The sales growth enables the firm in knowing its changing trends in the sales

so that it can determine its increase or decrease in revenue. The gross profit ratio helps the

company in evaluating the operational performance of its business. The operating profit ratio

assists the industry in attaining the results relating to its operating profits so that overall

profitability could be known by the company (Harris, 2019.). The gearing ratio measures the

leverage position of the firm so that necessary steps can be taken if the company is facing

high borrowed funds. Interest coverage ratio helps the Madagascar industries limited in

ascertaining its ability to meet its interest expenses so that it could maintain and keep control

over its expenses. Liquidity ratio ensures the liquidity position of the firm. The return on

equity ratio enables the enterprise in determining its income from the shareholders funds that

directly links to the financial performance of the business. The return on capital employed

helps the industry in assessing the income generated from its capital employed so that it could

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.