Managerial Finance Report: Company Performance, Ratios and Investment

VerifiedAdded on 2023/01/17

|17

|4009

|20

Report

AI Summary

This report delves into managerial finance, comparing the financial performance of Reckitt Benckiser Group Plc and Glaxo Smith Kline Plc. It begins with a comprehensive calculation of ten key financial ratios, including current ratio, quick ratio, net profit margin, gross profit margin, gearing ratio, P/E ratio, earnings per share, return on capital employed, average inventories turnover period, and dividend payout ratio for both companies across two years. The analysis then presents a comparative assessment of the companies' performance, financial positions, and investment potential, using charts to illustrate the trends of the calculated ratios. Based on the ratio analysis, recommendations are provided to improve the financial performance of the underperforming company, alongside a discussion of the limitations of relying solely on financial ratios for company interpretation. The report further explores investment appraisal techniques, advising senior management on project selection and discussing the limitations of these techniques in long-term decision-making. The conclusion synthesizes the findings, providing a final assessment and recommendations based on the financial analysis conducted.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PORTFOLIO 1.................................................................................................................................1

a. Calculation of 10 different financial ratios..............................................................................1

b. Analysis of the performance, financial position and investment potential..............................4

c. Recommendation of the way in which financial performance of the poorly performing

business can be improved............................................................................................................9

d. Discussion of the limitation of relaying on financial ratios to interpret a company's

performance...............................................................................................................................10

PORTFOLIO 2...............................................................................................................................10

a. Use of appropriate investment appraisal techniques and advise to senior management on

whether project a or b should be selected..................................................................................10

b. Discussion of limitation of using investment appraisal technique to help in long term

decision making.........................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

PORTFOLIO 1.................................................................................................................................1

a. Calculation of 10 different financial ratios..............................................................................1

b. Analysis of the performance, financial position and investment potential..............................4

c. Recommendation of the way in which financial performance of the poorly performing

business can be improved............................................................................................................9

d. Discussion of the limitation of relaying on financial ratios to interpret a company's

performance...............................................................................................................................10

PORTFOLIO 2...............................................................................................................................10

a. Use of appropriate investment appraisal techniques and advise to senior management on

whether project a or b should be selected..................................................................................10

b. Discussion of limitation of using investment appraisal technique to help in long term

decision making.........................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION

Managerial finance can be defined as an approach which is used for the purpose of

managing monetary resources which are used by an organisation for the purpose of executing

business in systematic manner. With the help of it complexities in the process of allocation of

finance could be reduced as it guides to assure that funds are allocated properly to all the

operations according to their requirements (Ahmed and Malik, 2015). Present report is based

upon comparison of two different companies which are Reckitt Benckiser Group Plc and Glaxo

Smith Kline Plc. Both the enterprises are mainly established in United Kingdom. First one is

having headquarter in England and another one is having in London. This assignment cover

various topics such as calculation of financial ratios, analysis of performance, recommendations

and limitation of relaying upon financial ratios for interpreting position of a company in the

market. Additionally, advice is also provided to the senior manager to opt option A or B with the

help of investment appraisal techniques along with limitations of relaying upon them are also

covered in this report.

PORTFOLIO 1

a. Calculation of 10 different financial ratios

Ratio analysis can be defined as a financial tool which is used by organisations to

determine their actual position. For the purpose of making investment in a profitable enterprise

finance manager of a company is being asked by the chief financial officer to selected one best

suitable option from two organisations (Alhassan, 2015). In order to analyse position of them in

the market different ratios are calculated by the manager. Calculation of them is as follows:

Current ratios:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Current assets

Current assets /

current

liabilities

15907 16927 5424 4952

Current

liabilities

26569 22491 6576 7614

0.6 0.75 0.82 0.65Current ratio

1

Managerial finance can be defined as an approach which is used for the purpose of

managing monetary resources which are used by an organisation for the purpose of executing

business in systematic manner. With the help of it complexities in the process of allocation of

finance could be reduced as it guides to assure that funds are allocated properly to all the

operations according to their requirements (Ahmed and Malik, 2015). Present report is based

upon comparison of two different companies which are Reckitt Benckiser Group Plc and Glaxo

Smith Kline Plc. Both the enterprises are mainly established in United Kingdom. First one is

having headquarter in England and another one is having in London. This assignment cover

various topics such as calculation of financial ratios, analysis of performance, recommendations

and limitation of relaying upon financial ratios for interpreting position of a company in the

market. Additionally, advice is also provided to the senior manager to opt option A or B with the

help of investment appraisal techniques along with limitations of relaying upon them are also

covered in this report.

PORTFOLIO 1

a. Calculation of 10 different financial ratios

Ratio analysis can be defined as a financial tool which is used by organisations to

determine their actual position. For the purpose of making investment in a profitable enterprise

finance manager of a company is being asked by the chief financial officer to selected one best

suitable option from two organisations (Alhassan, 2015). In order to analyse position of them in

the market different ratios are calculated by the manager. Calculation of them is as follows:

Current ratios:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Current assets

Current assets /

current

liabilities

15907 16927 5424 4952

Current

liabilities

26569 22491 6576 7614

0.6 0.75 0.82 0.65Current ratio

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick ratios:

Particulars Formula Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Quick assets

Quick assets /

current

liabilities

10042 11121 4223 3676

Current

liabilities

26569 22491 6576 7614

0.38 0.49 0.64 0.48Quick ratio

Net Profit Margin:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net profit

Net profit / net

sales * 100

1532 3623 6172 2161

Net sales 30186 30821 11512 12597

Net profit ratio 5.07% 11.75% 53.61% 17.15%

Gross Profit margin:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Gross profit

Gross profit /

net sales * 100

19844 20580 6870 7635

Net sales 30186 30821 11512 12597

Gross profit

margin 65.74% 66.77% 59.68% 60.61%

Gearing ratio:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total Debt Total debt /

equity

56449 53706 23480 22908

Equity -68 4360 13533 14742

2

Particulars Formula Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Quick assets

Quick assets /

current

liabilities

10042 11121 4223 3676

Current

liabilities

26569 22491 6576 7614

0.38 0.49 0.64 0.48Quick ratio

Net Profit Margin:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net profit

Net profit / net

sales * 100

1532 3623 6172 2161

Net sales 30186 30821 11512 12597

Net profit ratio 5.07% 11.75% 53.61% 17.15%

Gross Profit margin:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Gross profit

Gross profit /

net sales * 100

19844 20580 6870 7635

Net sales 30186 30821 11512 12597

Gross profit

margin 65.74% 66.77% 59.68% 60.61%

Gearing ratio:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Total Debt Total debt /

equity

56449 53706 23480 22908

Equity -68 4360 13533 14742

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

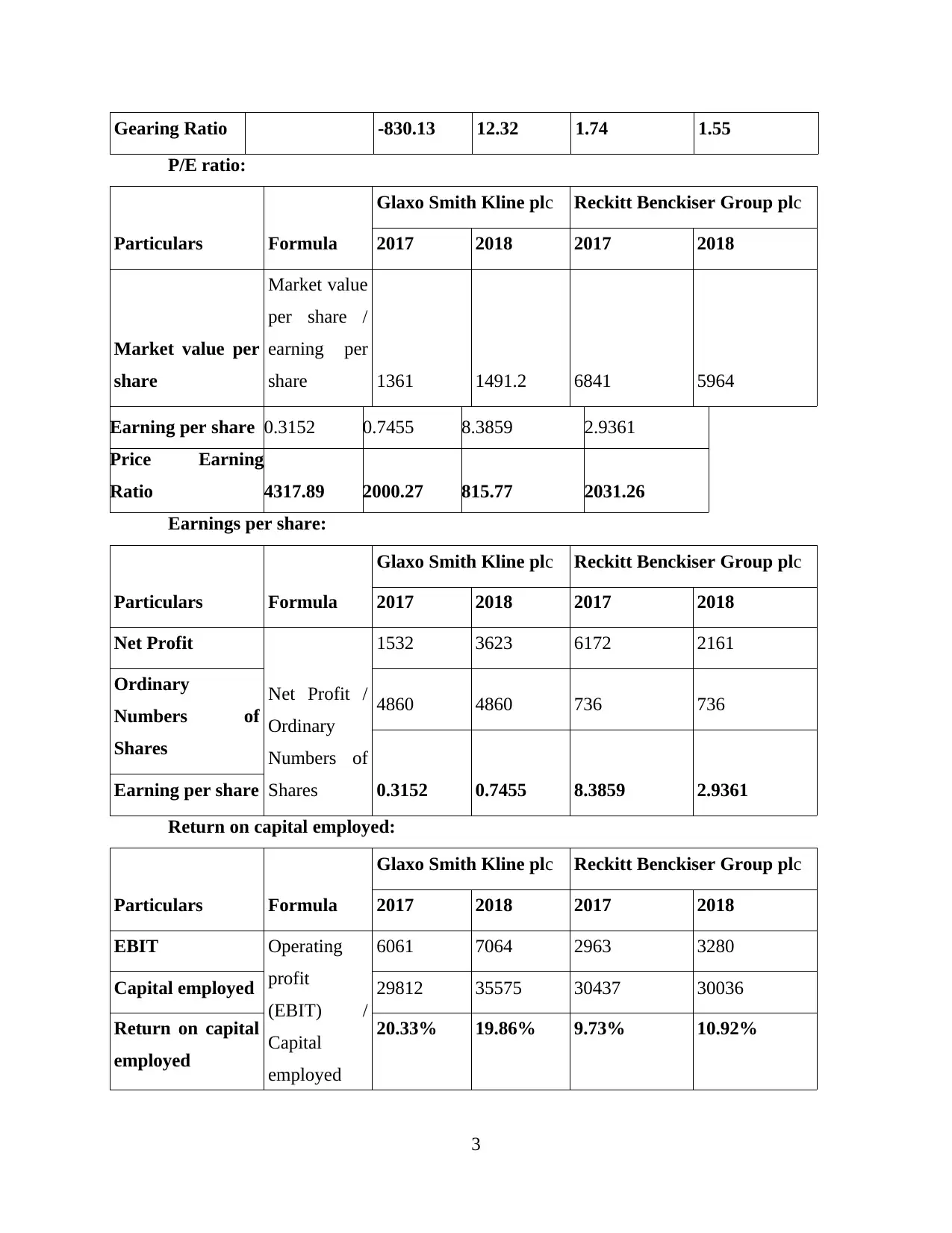

Gearing Ratio -830.13 12.32 1.74 1.55

P/E ratio:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Market value per

share

Market value

per share /

earning per

share 1361 1491.2 6841 5964

Earning per share 0.3152 0.7455 8.3859 2.9361

Price Earning

Ratio 4317.89 2000.27 815.77 2031.26

Earnings per share:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net Profit

Net Profit /

Ordinary

Numbers of

Shares

1532 3623 6172 2161

Ordinary

Numbers of

Shares

4860 4860 736 736

0.3152 0.7455 8.3859 2.9361Earning per share

Return on capital employed:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

EBIT Operating

profit

(EBIT) /

Capital

employed

6061 7064 2963 3280

Capital employed 29812 35575 30437 30036

Return on capital

employed

20.33% 19.86% 9.73% 10.92%

3

P/E ratio:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Market value per

share

Market value

per share /

earning per

share 1361 1491.2 6841 5964

Earning per share 0.3152 0.7455 8.3859 2.9361

Price Earning

Ratio 4317.89 2000.27 815.77 2031.26

Earnings per share:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Net Profit

Net Profit /

Ordinary

Numbers of

Shares

1532 3623 6172 2161

Ordinary

Numbers of

Shares

4860 4860 736 736

0.3152 0.7455 8.3859 2.9361Earning per share

Return on capital employed:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

EBIT Operating

profit

(EBIT) /

Capital

employed

6061 7064 2963 3280

Capital employed 29812 35575 30437 30036

Return on capital

employed

20.33% 19.86% 9.73% 10.92%

3

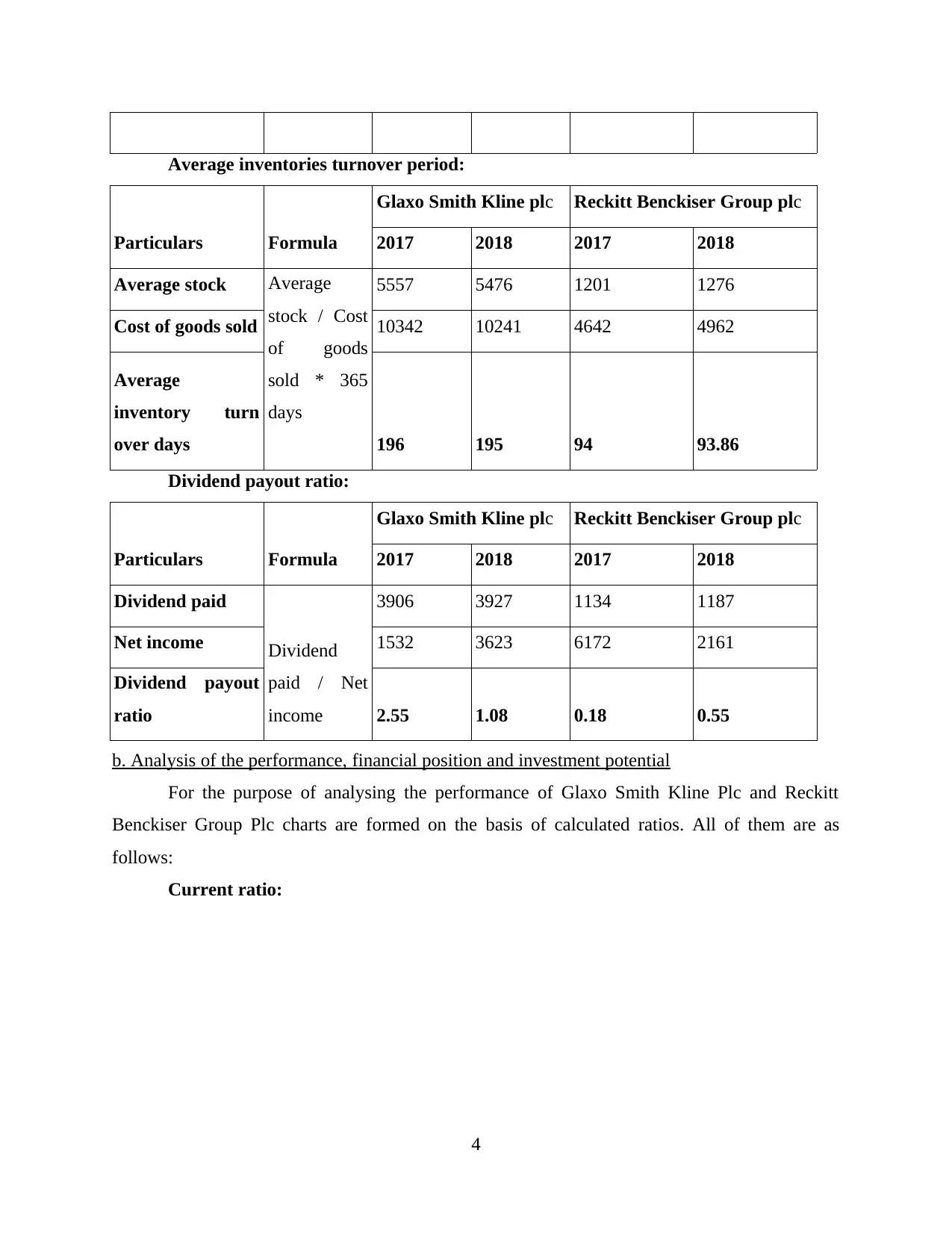

Average inventories turnover period:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Average stock Average

stock / Cost

of goods

sold * 365

days

5557 5476 1201 1276

Cost of goods sold 10342 10241 4642 4962

Average

inventory turn

over days 196 195 94 93.86

Dividend payout ratio:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Dividend paid

Dividend

paid / Net

income

3906 3927 1134 1187

Net income 1532 3623 6172 2161

Dividend payout

ratio 2.55 1.08 0.18 0.55

b. Analysis of the performance, financial position and investment potential

For the purpose of analysing the performance of Glaxo Smith Kline Plc and Reckitt

Benckiser Group Plc charts are formed on the basis of calculated ratios. All of them are as

follows:

Current ratio:

4

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Average stock Average

stock / Cost

of goods

sold * 365

days

5557 5476 1201 1276

Cost of goods sold 10342 10241 4642 4962

Average

inventory turn

over days 196 195 94 93.86

Dividend payout ratio:

Particulars Formula

Glaxo Smith Kline plc Reckitt Benckiser Group plc

2017 2018 2017 2018

Dividend paid

Dividend

paid / Net

income

3906 3927 1134 1187

Net income 1532 3623 6172 2161

Dividend payout

ratio 2.55 1.08 0.18 0.55

b. Analysis of the performance, financial position and investment potential

For the purpose of analysing the performance of Glaxo Smith Kline Plc and Reckitt

Benckiser Group Plc charts are formed on the basis of calculated ratios. All of them are as

follows:

Current ratio:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.6

0.75

0.82 0.85

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

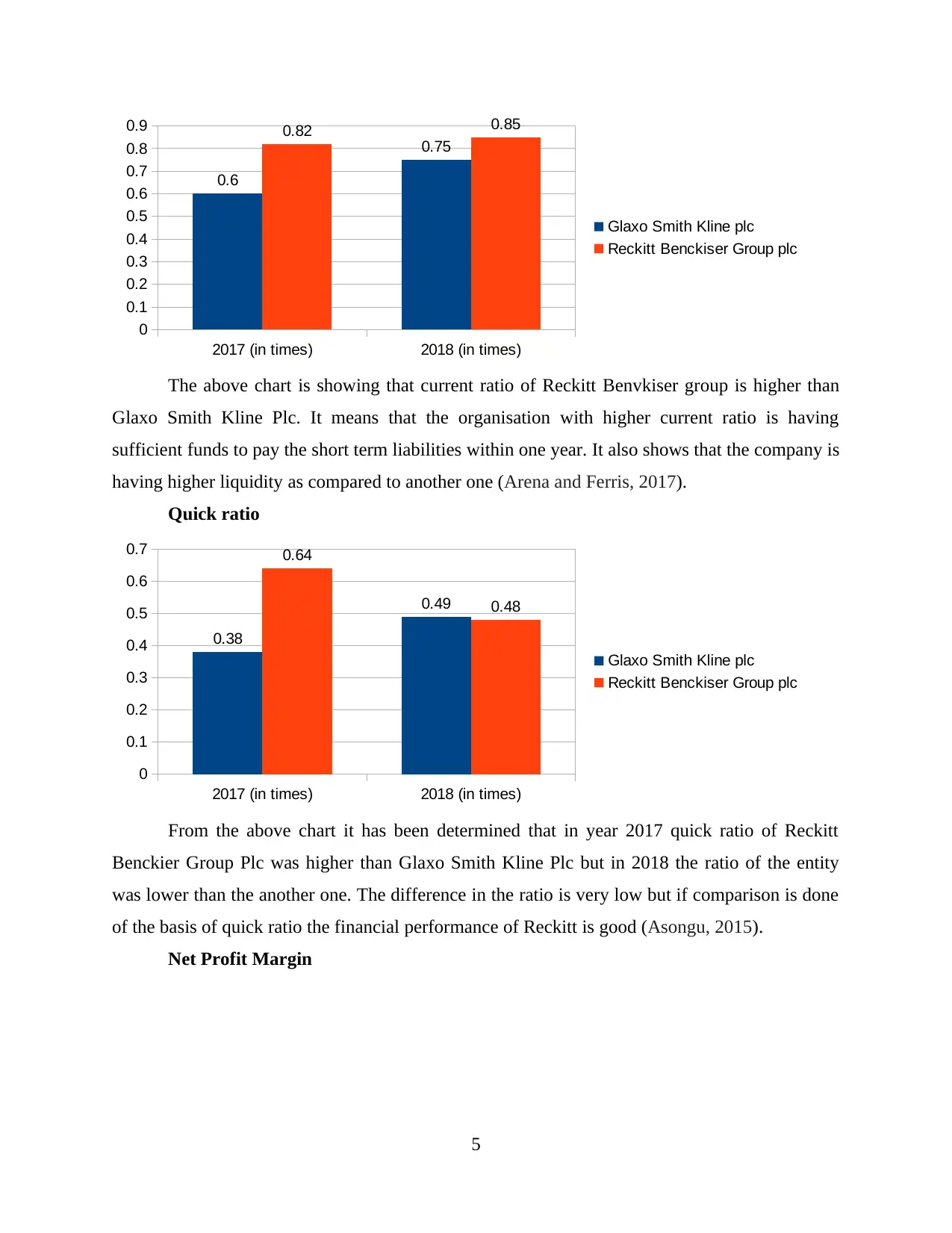

The above chart is showing that current ratio of Reckitt Benvkiser group is higher than

Glaxo Smith Kline Plc. It means that the organisation with higher current ratio is having

sufficient funds to pay the short term liabilities within one year. It also shows that the company is

having higher liquidity as compared to another one (Arena and Ferris, 2017).

Quick ratio

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.38

0.49

0.64

0.48

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

From the above chart it has been determined that in year 2017 quick ratio of Reckitt

Benckier Group Plc was higher than Glaxo Smith Kline Plc but in 2018 the ratio of the entity

was lower than the another one. The difference in the ratio is very low but if comparison is done

of the basis of quick ratio the financial performance of Reckitt is good (Asongu, 2015).

Net Profit Margin

5

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

0.6

0.75

0.82 0.85

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

The above chart is showing that current ratio of Reckitt Benvkiser group is higher than

Glaxo Smith Kline Plc. It means that the organisation with higher current ratio is having

sufficient funds to pay the short term liabilities within one year. It also shows that the company is

having higher liquidity as compared to another one (Arena and Ferris, 2017).

Quick ratio

2017 (in times) 2018 (in times)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.38

0.49

0.64

0.48

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

From the above chart it has been determined that in year 2017 quick ratio of Reckitt

Benckier Group Plc was higher than Glaxo Smith Kline Plc but in 2018 the ratio of the entity

was lower than the another one. The difference in the ratio is very low but if comparison is done

of the basis of quick ratio the financial performance of Reckitt is good (Asongu, 2015).

Net Profit Margin

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017 (in %) 2018 (in %)

0

10

20

30

40

50

60

5.07

11.75

53.61

17.15

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

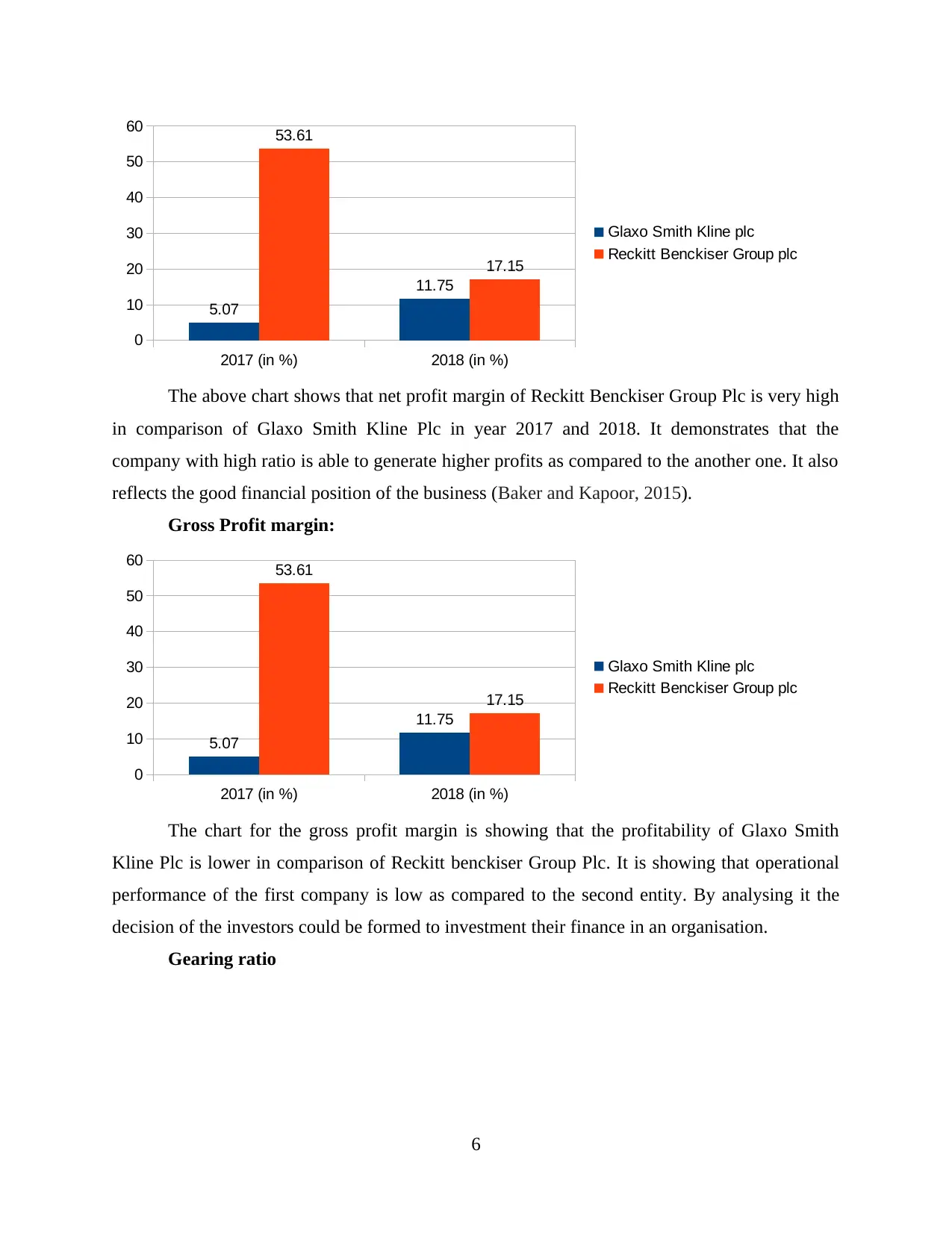

The above chart shows that net profit margin of Reckitt Benckiser Group Plc is very high

in comparison of Glaxo Smith Kline Plc in year 2017 and 2018. It demonstrates that the

company with high ratio is able to generate higher profits as compared to the another one. It also

reflects the good financial position of the business (Baker and Kapoor, 2015).

Gross Profit margin:

2017 (in %) 2018 (in %)

0

10

20

30

40

50

60

5.07

11.75

53.61

17.15

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

The chart for the gross profit margin is showing that the profitability of Glaxo Smith

Kline Plc is lower in comparison of Reckitt benckiser Group Plc. It is showing that operational

performance of the first company is low as compared to the second entity. By analysing it the

decision of the investors could be formed to investment their finance in an organisation.

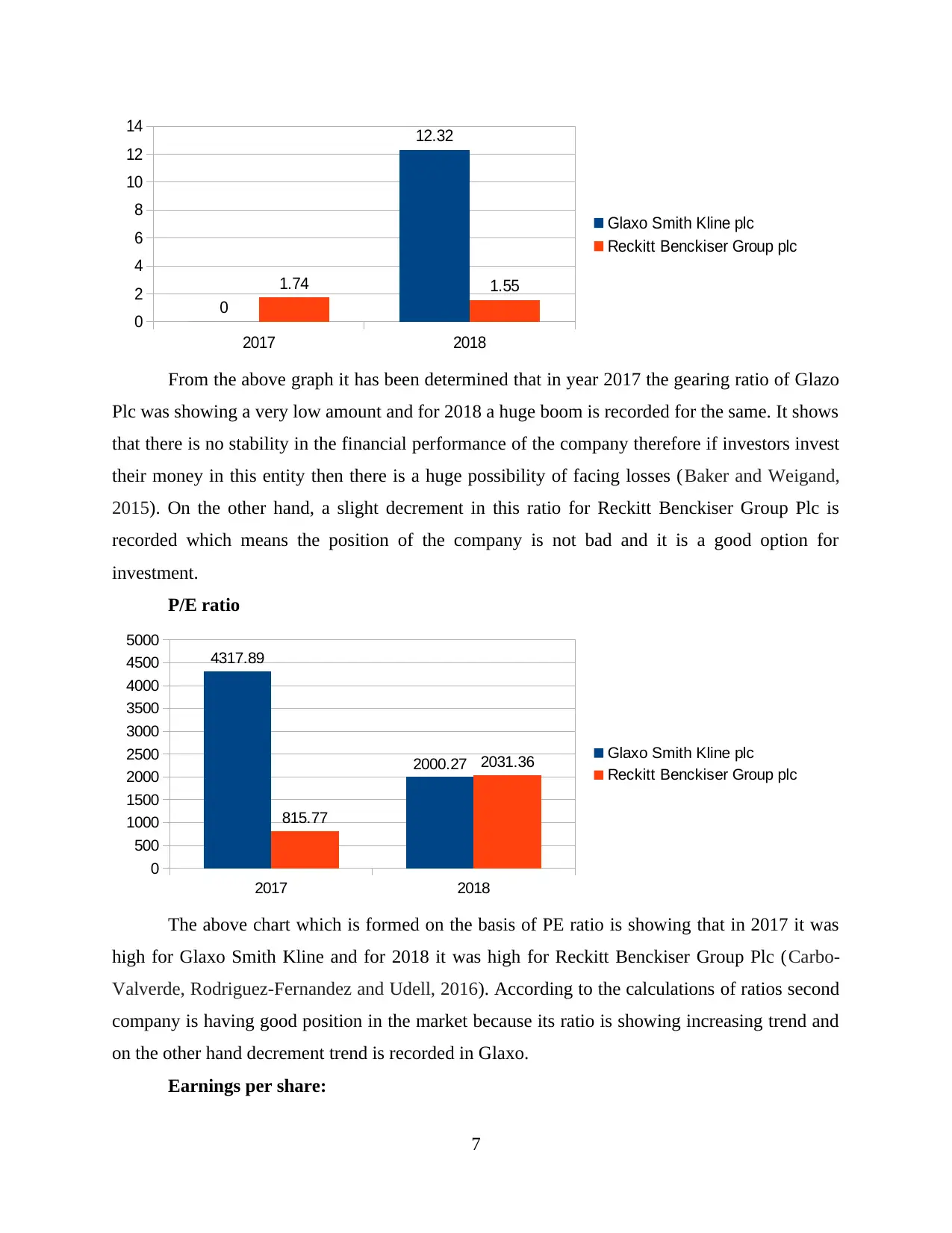

Gearing ratio

6

0

10

20

30

40

50

60

5.07

11.75

53.61

17.15

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

The above chart shows that net profit margin of Reckitt Benckiser Group Plc is very high

in comparison of Glaxo Smith Kline Plc in year 2017 and 2018. It demonstrates that the

company with high ratio is able to generate higher profits as compared to the another one. It also

reflects the good financial position of the business (Baker and Kapoor, 2015).

Gross Profit margin:

2017 (in %) 2018 (in %)

0

10

20

30

40

50

60

5.07

11.75

53.61

17.15

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

The chart for the gross profit margin is showing that the profitability of Glaxo Smith

Kline Plc is lower in comparison of Reckitt benckiser Group Plc. It is showing that operational

performance of the first company is low as compared to the second entity. By analysing it the

decision of the investors could be formed to investment their finance in an organisation.

Gearing ratio

6

2017 2018

0

2

4

6

8

10

12

14

0

12.32

1.74 1.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

From the above graph it has been determined that in year 2017 the gearing ratio of Glazo

Plc was showing a very low amount and for 2018 a huge boom is recorded for the same. It shows

that there is no stability in the financial performance of the company therefore if investors invest

their money in this entity then there is a huge possibility of facing losses (Baker and Weigand,

2015). On the other hand, a slight decrement in this ratio for Reckitt Benckiser Group Plc is

recorded which means the position of the company is not bad and it is a good option for

investment.

P/E ratio

2017 2018

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

4317.89

2000.27

815.77

2031.36 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

The above chart which is formed on the basis of PE ratio is showing that in 2017 it was

high for Glaxo Smith Kline and for 2018 it was high for Reckitt Benckiser Group Plc (Carbo‐

Valverde, Rodriguez‐Fernandez and Udell, 2016). According to the calculations of ratios second

company is having good position in the market because its ratio is showing increasing trend and

on the other hand decrement trend is recorded in Glaxo.

Earnings per share:

7

0

2

4

6

8

10

12

14

0

12.32

1.74 1.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

From the above graph it has been determined that in year 2017 the gearing ratio of Glazo

Plc was showing a very low amount and for 2018 a huge boom is recorded for the same. It shows

that there is no stability in the financial performance of the company therefore if investors invest

their money in this entity then there is a huge possibility of facing losses (Baker and Weigand,

2015). On the other hand, a slight decrement in this ratio for Reckitt Benckiser Group Plc is

recorded which means the position of the company is not bad and it is a good option for

investment.

P/E ratio

2017 2018

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

4317.89

2000.27

815.77

2031.36 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

The above chart which is formed on the basis of PE ratio is showing that in 2017 it was

high for Glaxo Smith Kline and for 2018 it was high for Reckitt Benckiser Group Plc (Carbo‐

Valverde, Rodriguez‐Fernandez and Udell, 2016). According to the calculations of ratios second

company is having good position in the market because its ratio is showing increasing trend and

on the other hand decrement trend is recorded in Glaxo.

Earnings per share:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017 2018

0

1

2

3

4

5

6

7

8

9

0.31 0.74

8.38

2.93

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

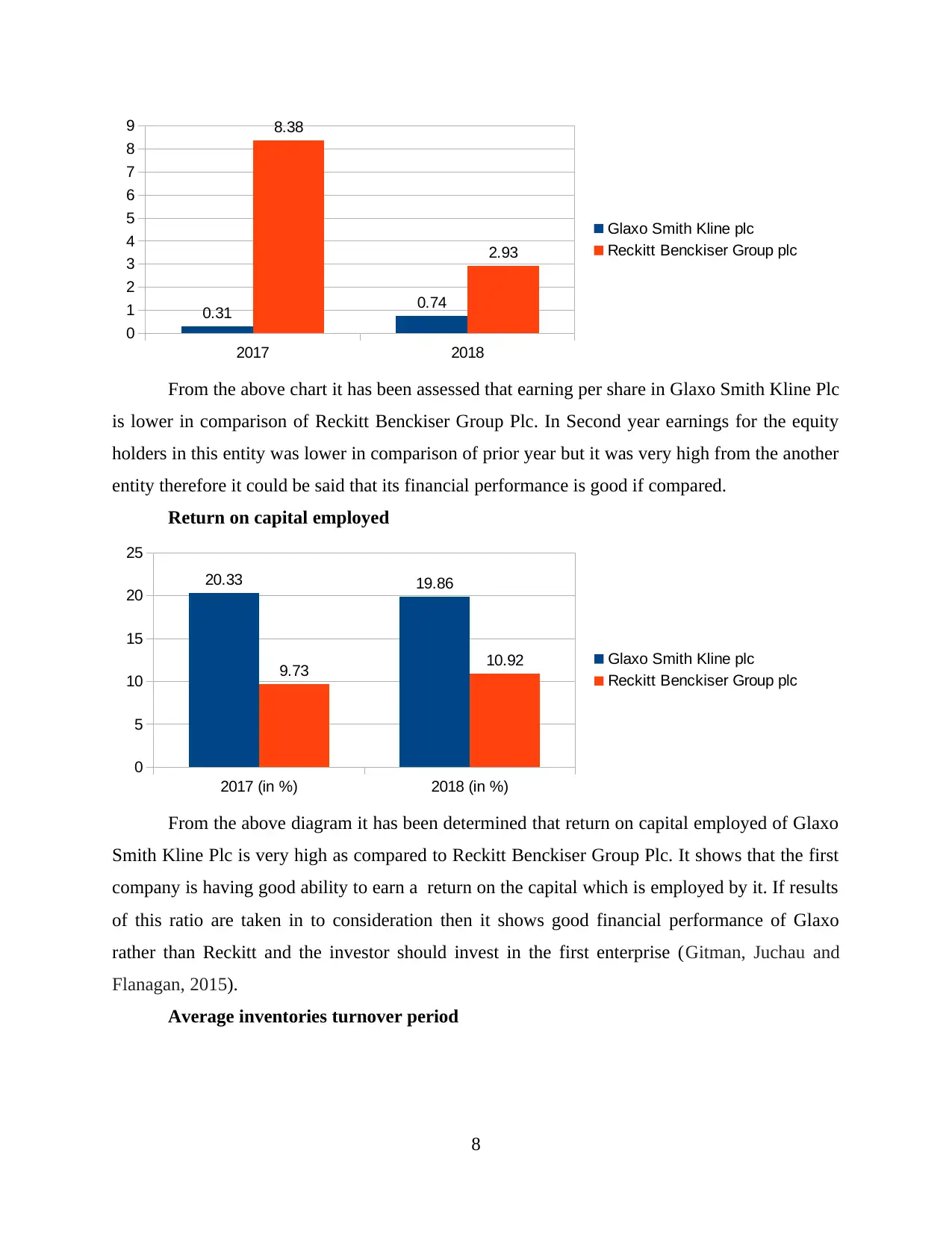

From the above chart it has been assessed that earning per share in Glaxo Smith Kline Plc

is lower in comparison of Reckitt Benckiser Group Plc. In Second year earnings for the equity

holders in this entity was lower in comparison of prior year but it was very high from the another

entity therefore it could be said that its financial performance is good if compared.

Return on capital employed

2017 (in %) 2018 (in %)

0

5

10

15

20

25

20.33 19.86

9.73 10.92 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

From the above diagram it has been determined that return on capital employed of Glaxo

Smith Kline Plc is very high as compared to Reckitt Benckiser Group Plc. It shows that the first

company is having good ability to earn a return on the capital which is employed by it. If results

of this ratio are taken in to consideration then it shows good financial performance of Glaxo

rather than Reckitt and the investor should invest in the first enterprise (Gitman, Juchau and

Flanagan, 2015).

Average inventories turnover period

8

0

1

2

3

4

5

6

7

8

9

0.31 0.74

8.38

2.93

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

From the above chart it has been assessed that earning per share in Glaxo Smith Kline Plc

is lower in comparison of Reckitt Benckiser Group Plc. In Second year earnings for the equity

holders in this entity was lower in comparison of prior year but it was very high from the another

entity therefore it could be said that its financial performance is good if compared.

Return on capital employed

2017 (in %) 2018 (in %)

0

5

10

15

20

25

20.33 19.86

9.73 10.92 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

From the above diagram it has been determined that return on capital employed of Glaxo

Smith Kline Plc is very high as compared to Reckitt Benckiser Group Plc. It shows that the first

company is having good ability to earn a return on the capital which is employed by it. If results

of this ratio are taken in to consideration then it shows good financial performance of Glaxo

rather than Reckitt and the investor should invest in the first enterprise (Gitman, Juchau and

Flanagan, 2015).

Average inventories turnover period

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017 (in days) 2018 (in days)

0

50

100

150

200

250

196 195

94 93.86 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

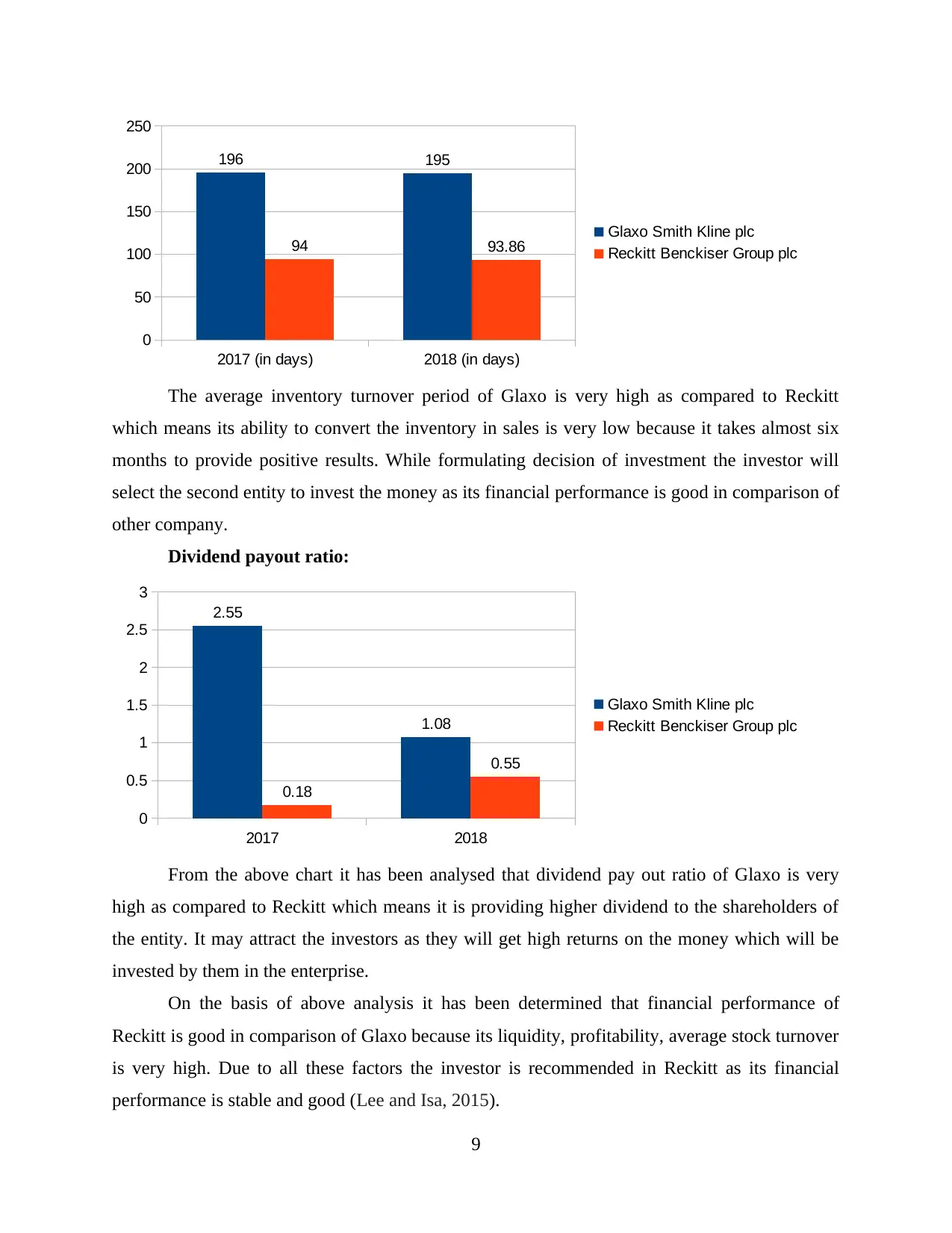

The average inventory turnover period of Glaxo is very high as compared to Reckitt

which means its ability to convert the inventory in sales is very low because it takes almost six

months to provide positive results. While formulating decision of investment the investor will

select the second entity to invest the money as its financial performance is good in comparison of

other company.

Dividend payout ratio:

2017 2018

0

0.5

1

1.5

2

2.5

3

2.55

1.08

0.18

0.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

From the above chart it has been analysed that dividend pay out ratio of Glaxo is very

high as compared to Reckitt which means it is providing higher dividend to the shareholders of

the entity. It may attract the investors as they will get high returns on the money which will be

invested by them in the enterprise.

On the basis of above analysis it has been determined that financial performance of

Reckitt is good in comparison of Glaxo because its liquidity, profitability, average stock turnover

is very high. Due to all these factors the investor is recommended in Reckitt as its financial

performance is stable and good (Lee and Isa, 2015).

9

0

50

100

150

200

250

196 195

94 93.86 Glaxo Smith Kline plc

Reckitt Benckiser Group plc

The average inventory turnover period of Glaxo is very high as compared to Reckitt

which means its ability to convert the inventory in sales is very low because it takes almost six

months to provide positive results. While formulating decision of investment the investor will

select the second entity to invest the money as its financial performance is good in comparison of

other company.

Dividend payout ratio:

2017 2018

0

0.5

1

1.5

2

2.5

3

2.55

1.08

0.18

0.55

Glaxo Smith Kline plc

Reckitt Benckiser Group plc

From the above chart it has been analysed that dividend pay out ratio of Glaxo is very

high as compared to Reckitt which means it is providing higher dividend to the shareholders of

the entity. It may attract the investors as they will get high returns on the money which will be

invested by them in the enterprise.

On the basis of above analysis it has been determined that financial performance of

Reckitt is good in comparison of Glaxo because its liquidity, profitability, average stock turnover

is very high. Due to all these factors the investor is recommended in Reckitt as its financial

performance is stable and good (Lee and Isa, 2015).

9

c. Recommendation of the way in which financial performance of the poorly performing

business can be improved

On the basis of ratio analysis it has been determined that Glaxo Smith Kline Plc's

performance is very poor in the market and the top level executives of the organisation are

required to take proper actions to enhance the performance. There are various recommendations

are provided to the which could be adopted by them to enhance financial status in the market. All

of them are as follows:

Managers of Glaxo should pay attention towards increment of liquid assets so that level

of liquidity could be increased. It will help to meet the short term obligations properly

and in less time.

The management should formulate effective strategies so that they can make efforts to

increase the earning per share (Osterhoff and Kaserer, 2016).

Gross profit margin of the entity is very low therefore it is very important for the

managers to form new policies which may result in increased profitability so that it can

result in good financial performance of the company.

Average inventory period of the company is very high so it is essential for management

to find ways in which the period could be decreased. They can form new strategies to

improve it as it will be beneficial for improvement of financial position of the company.

d. Discussion of the limitation of relaying on financial ratios to interpret a company's

performance

Ratio analysis is an effective technique which could be used by organisations for the

purpose of determining financial position. It is very important for the managers not to relay upon

them wholly as there are some limitations of it to interpret performance of a company. In order to

reach to the best suitable conclusion it is vital for them to be aware of all the weaknesses of it.

Some of them are discussed below:

Ratio analysis does not focus upon inflationary effects which means it is not possible that

it provides exact results to the researchers.

If an investor is having two different options for investment of two companies of

different sectors then in this case it will not be beneficial for them to get exact and

appropriate results to reach a conclusion (Limitations of Ratio analysis for decision

making, 2019).

10

business can be improved

On the basis of ratio analysis it has been determined that Glaxo Smith Kline Plc's

performance is very poor in the market and the top level executives of the organisation are

required to take proper actions to enhance the performance. There are various recommendations

are provided to the which could be adopted by them to enhance financial status in the market. All

of them are as follows:

Managers of Glaxo should pay attention towards increment of liquid assets so that level

of liquidity could be increased. It will help to meet the short term obligations properly

and in less time.

The management should formulate effective strategies so that they can make efforts to

increase the earning per share (Osterhoff and Kaserer, 2016).

Gross profit margin of the entity is very low therefore it is very important for the

managers to form new policies which may result in increased profitability so that it can

result in good financial performance of the company.

Average inventory period of the company is very high so it is essential for management

to find ways in which the period could be decreased. They can form new strategies to

improve it as it will be beneficial for improvement of financial position of the company.

d. Discussion of the limitation of relaying on financial ratios to interpret a company's

performance

Ratio analysis is an effective technique which could be used by organisations for the

purpose of determining financial position. It is very important for the managers not to relay upon

them wholly as there are some limitations of it to interpret performance of a company. In order to

reach to the best suitable conclusion it is vital for them to be aware of all the weaknesses of it.

Some of them are discussed below:

Ratio analysis does not focus upon inflationary effects which means it is not possible that

it provides exact results to the researchers.

If an investor is having two different options for investment of two companies of

different sectors then in this case it will not be beneficial for them to get exact and

appropriate results to reach a conclusion (Limitations of Ratio analysis for decision

making, 2019).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.