Comprehensive Financial Analysis Report: Effective Distributors Ltd

VerifiedAdded on 2020/04/01

|15

|3066

|170

Report

AI Summary

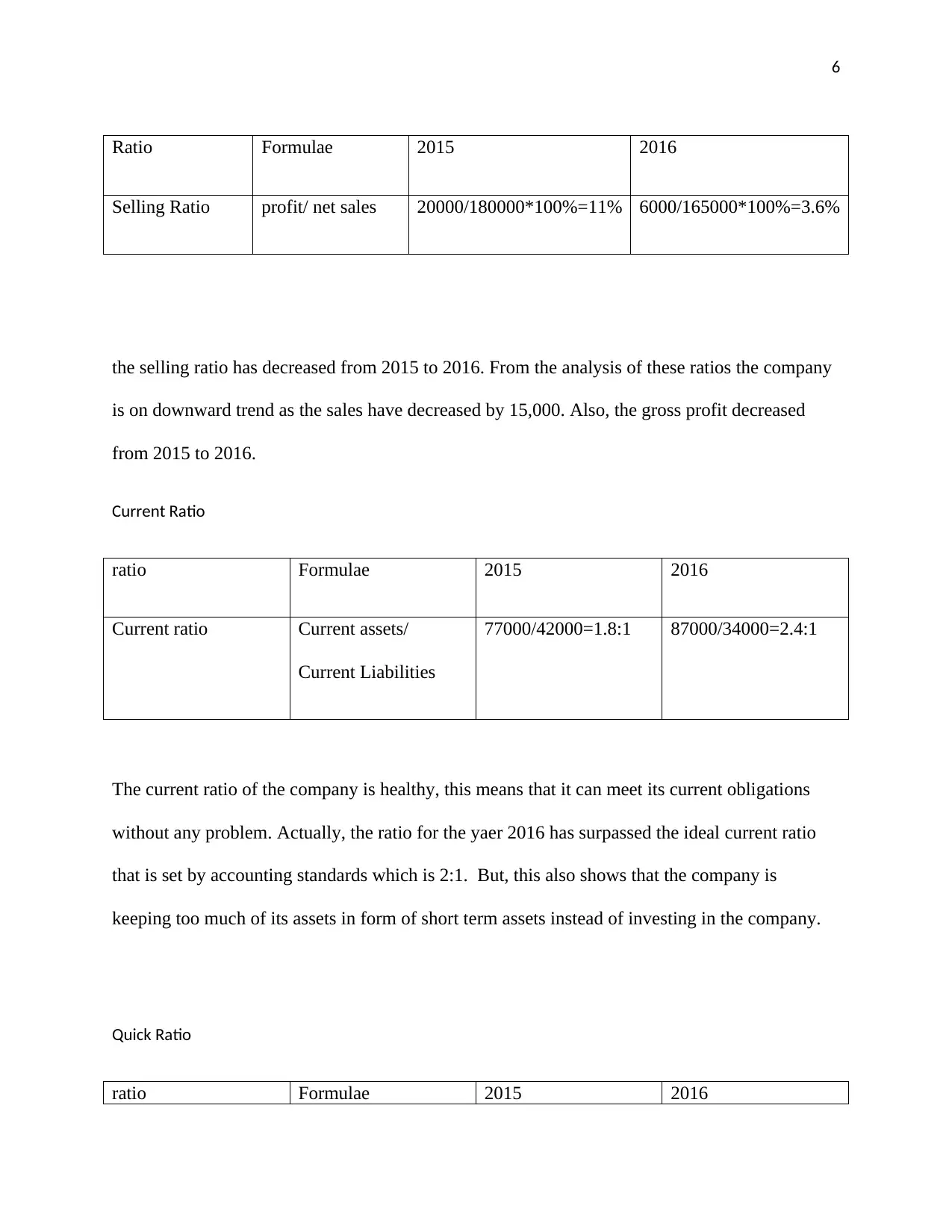

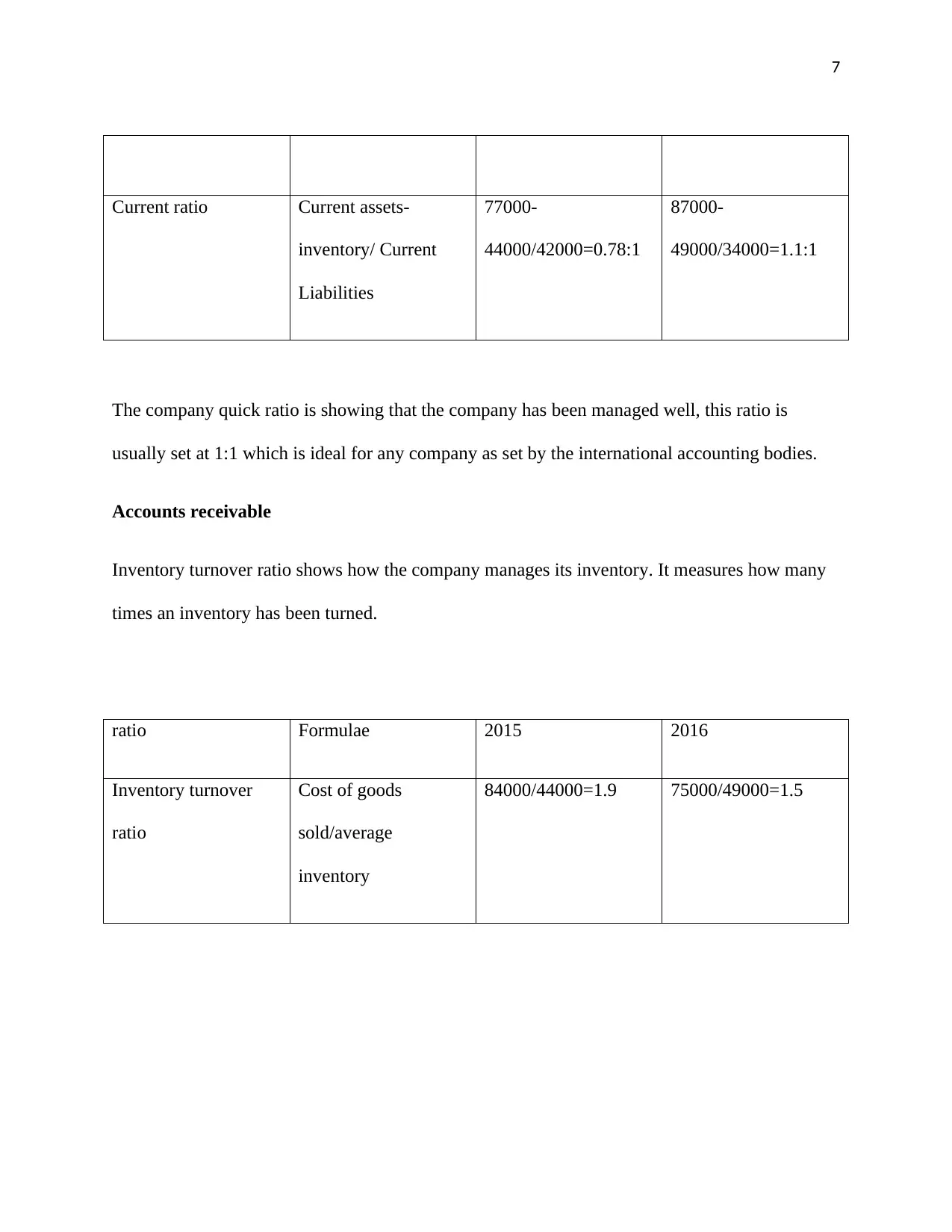

This accounting report presents a comprehensive financial analysis of Effective Distributors Ltd. It begins with an executive summary highlighting key issues and then delves into a detailed examination of profitability ratios (ROE, ROA, net profit margin), inventory management, and other relevant financial ratios. The analysis covers the years 2015 and 2016, offering insights into the company's performance and identifying areas for improvement. The report also addresses ethical issues, specifically financial statement misrepresentation and accounting fraud, discussing the responsibilities of accountants and the potential consequences of unethical practices. The report further explores the role of computerized accounting systems, emphasizing their importance in managerial decision-making and overall business operations. Recommendations for cost reduction, customer acquisition, and inventory management are provided, offering practical strategies for enhancing the company's financial health and operational efficiency.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.