Financial Analysis and Investment Appraisal Report for BA 4008

VerifiedAdded on 2023/01/09

|16

|2344

|1

Report

AI Summary

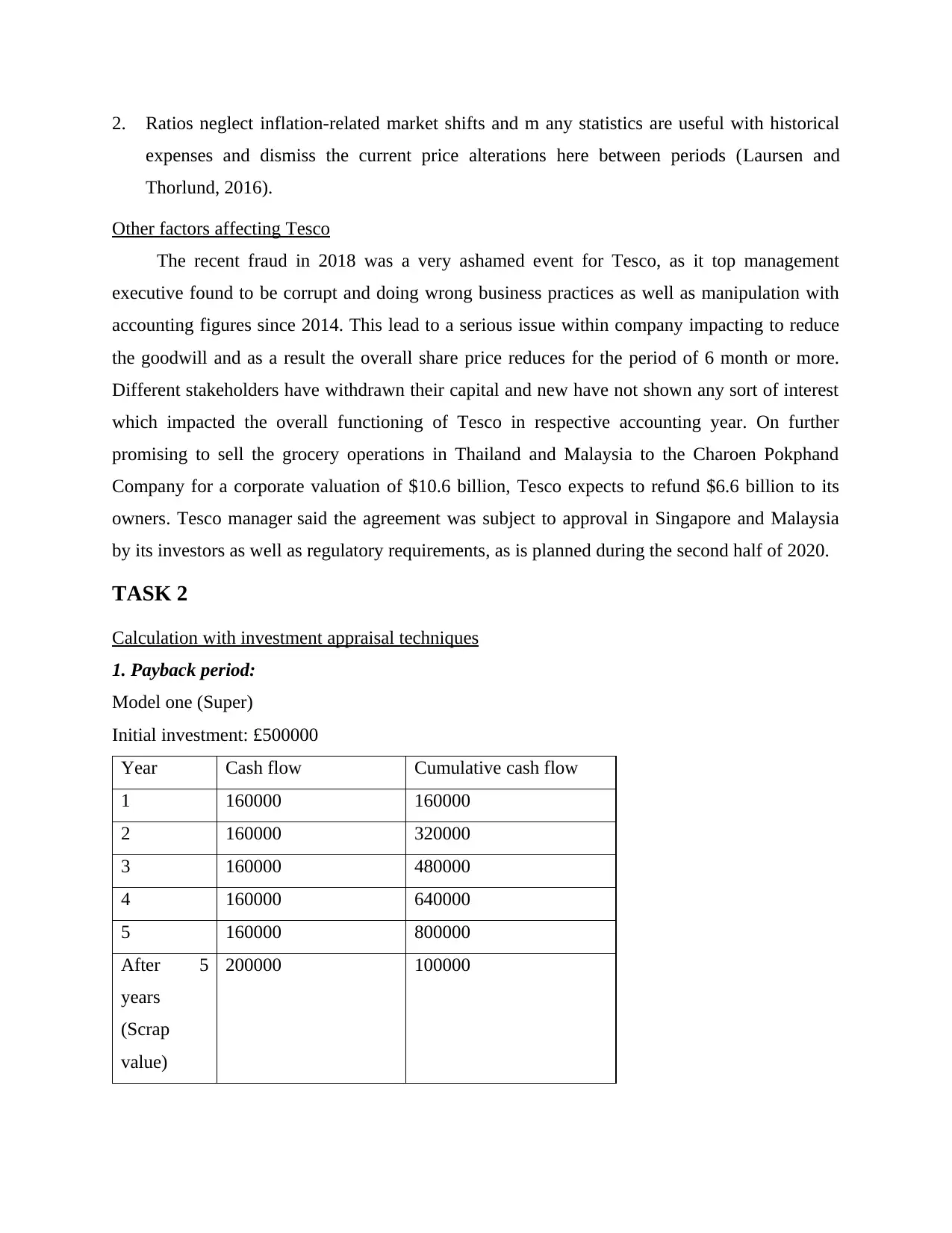

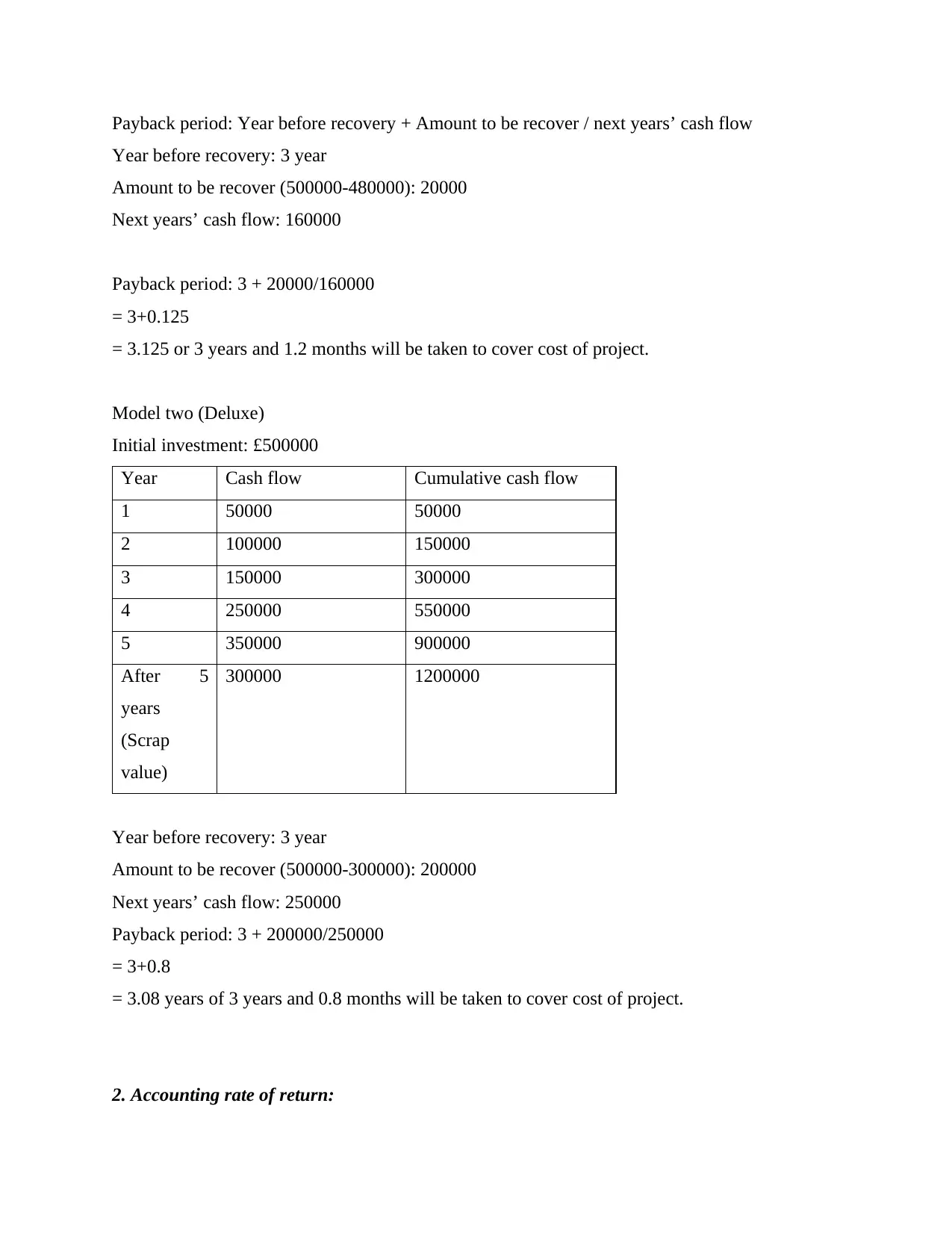

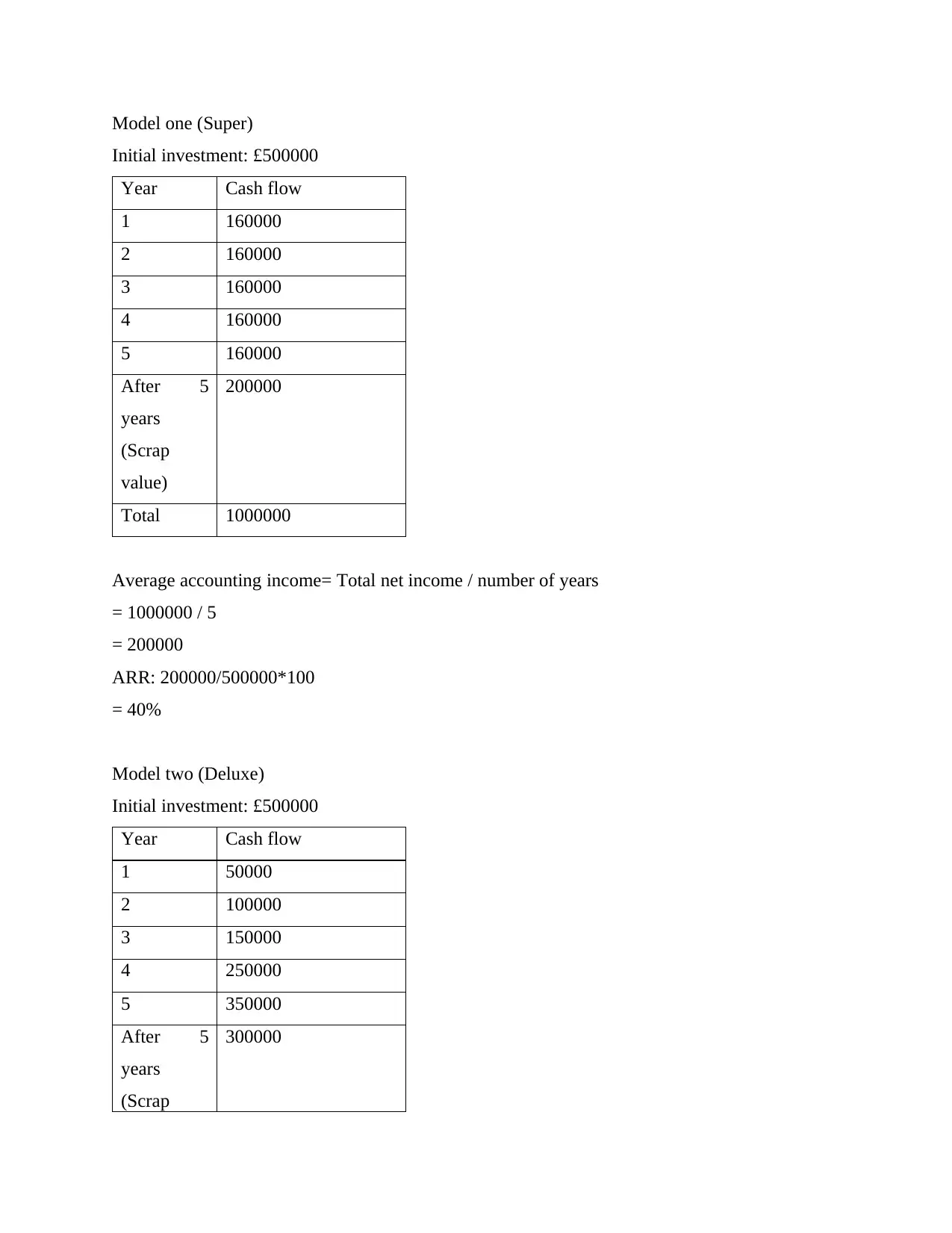

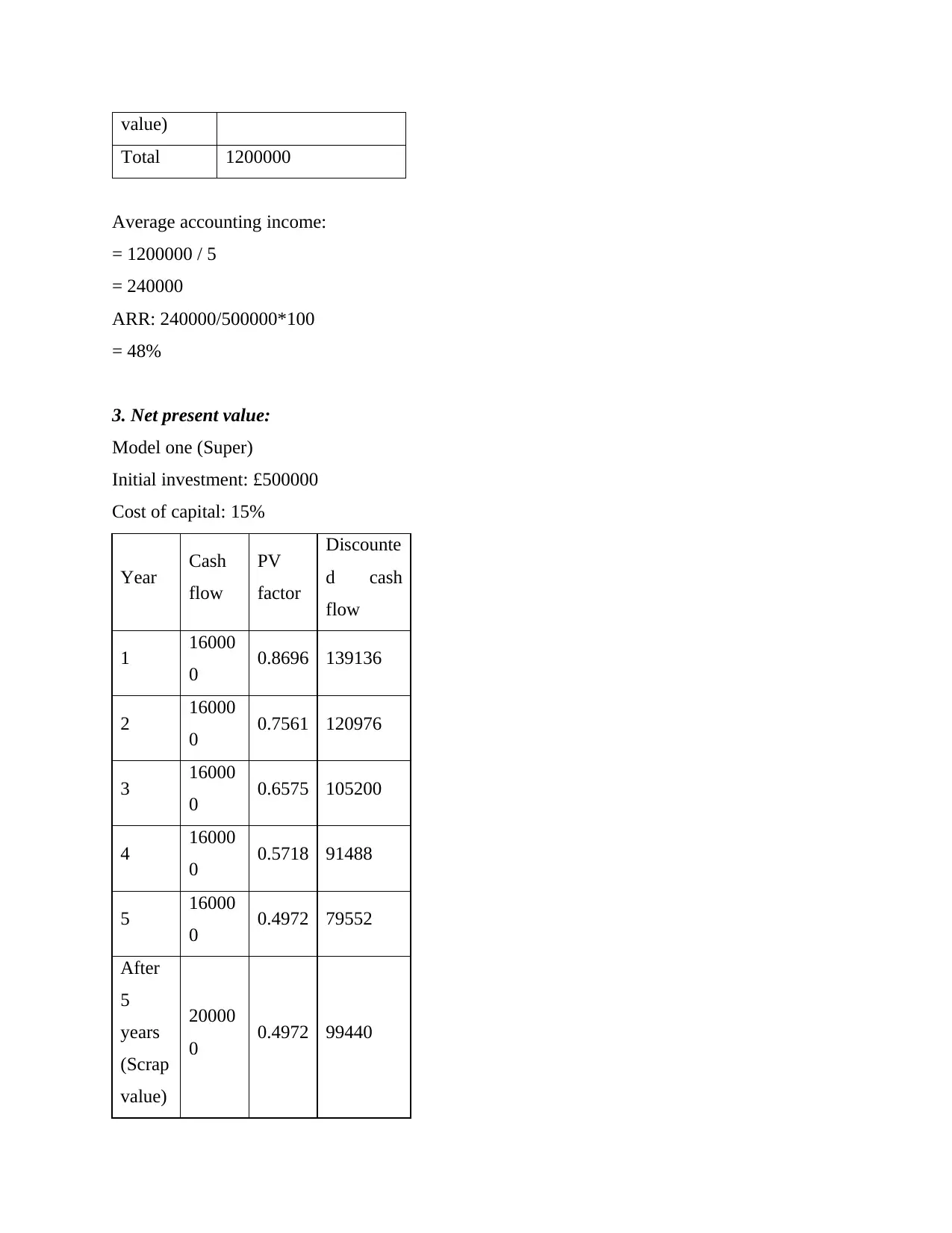

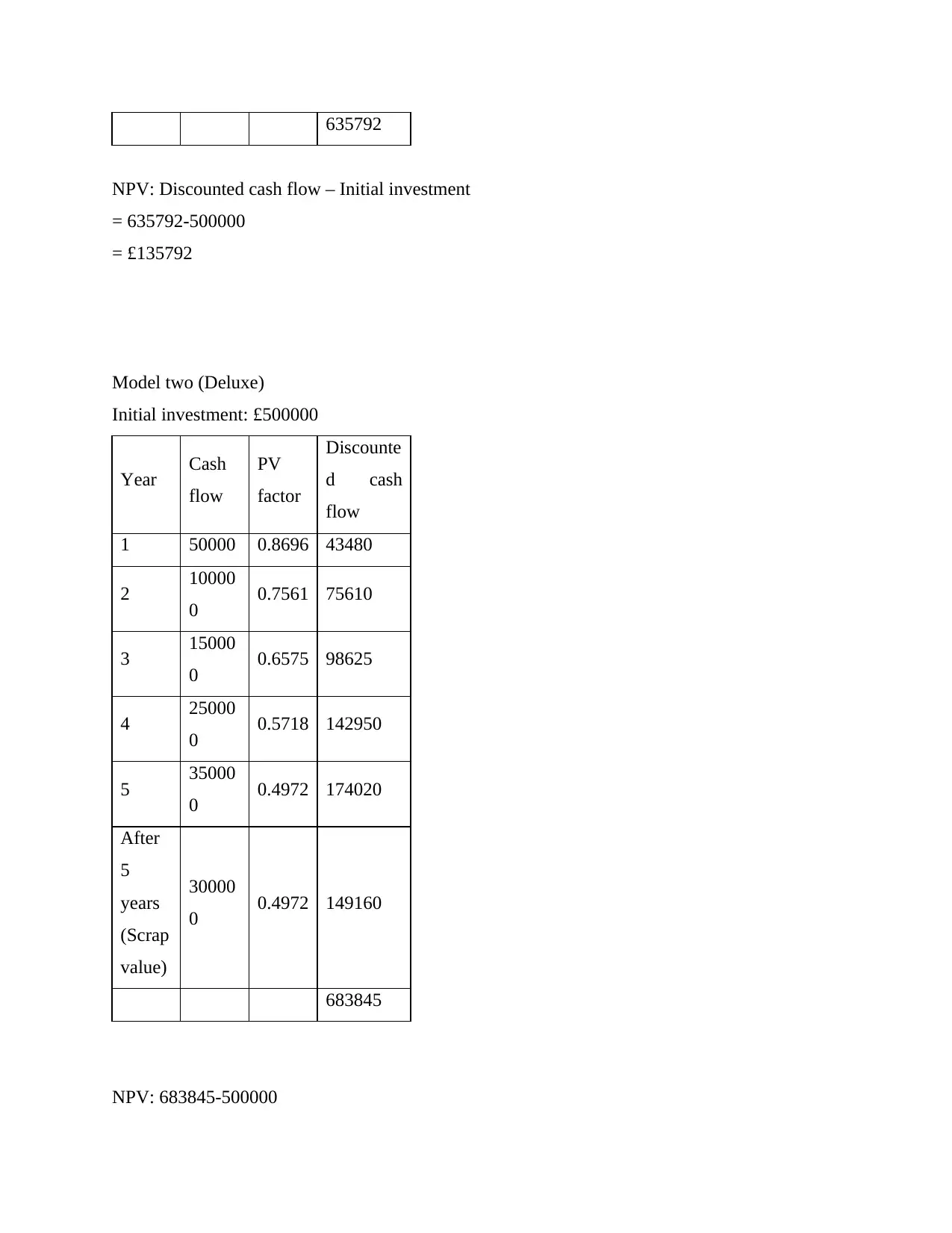

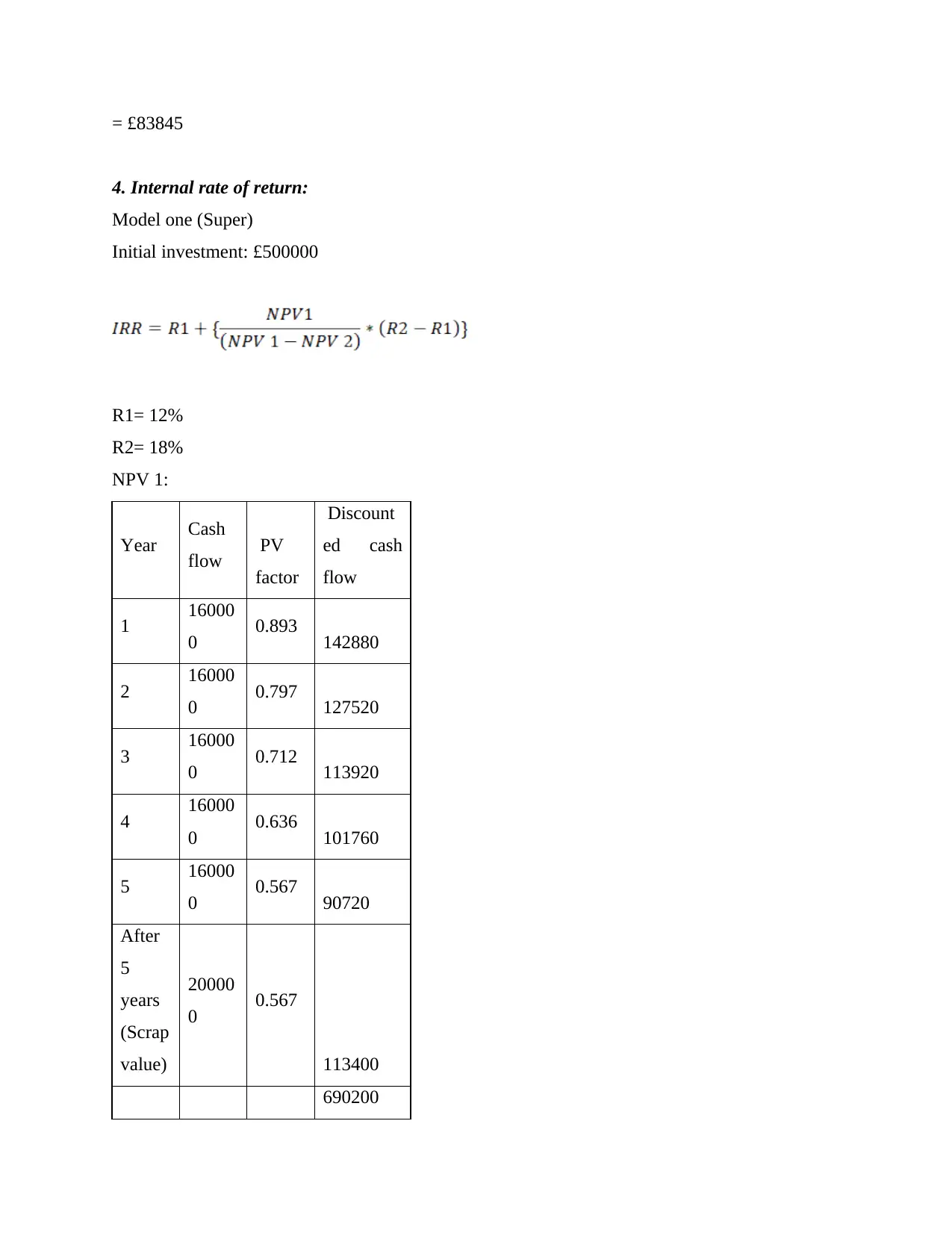

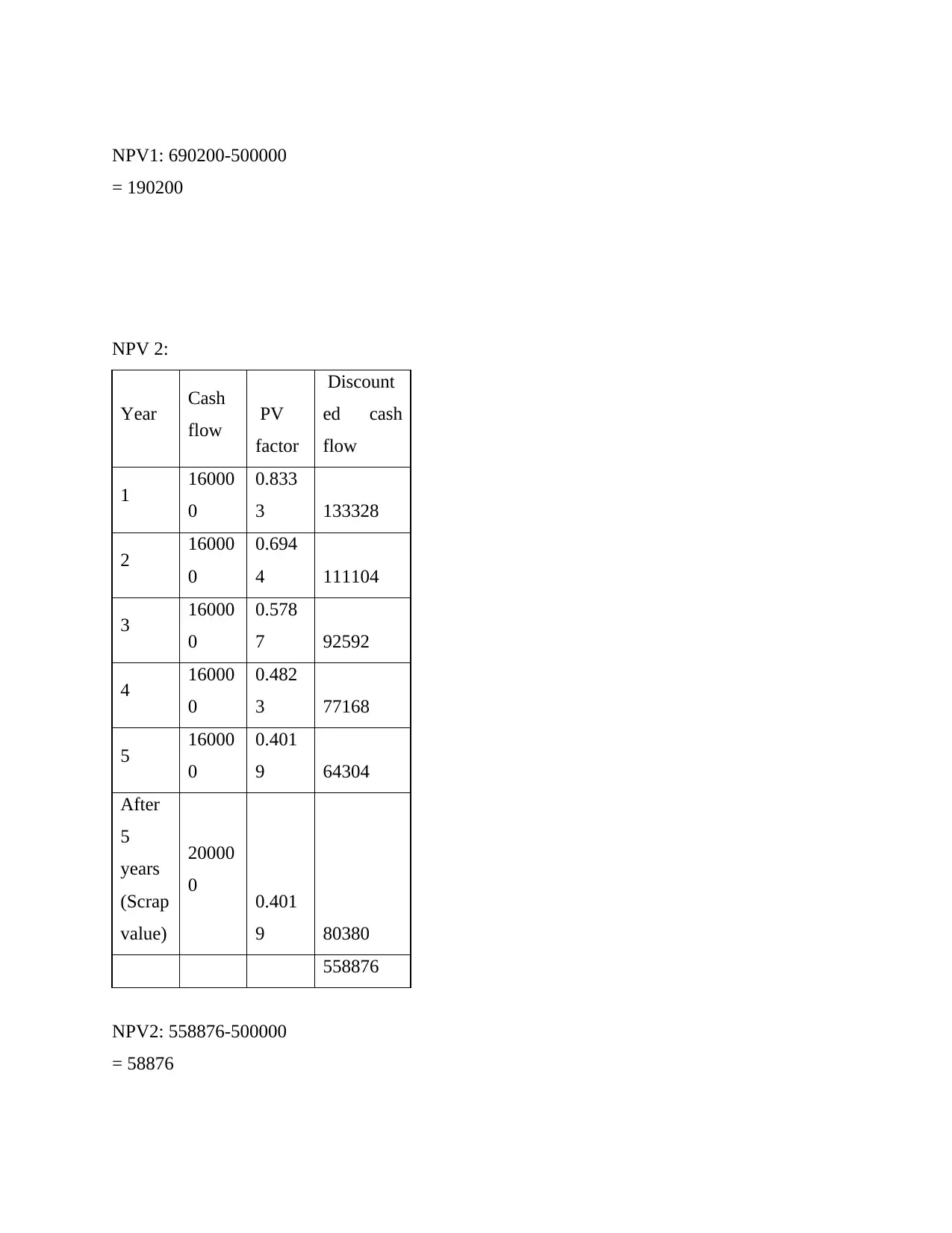

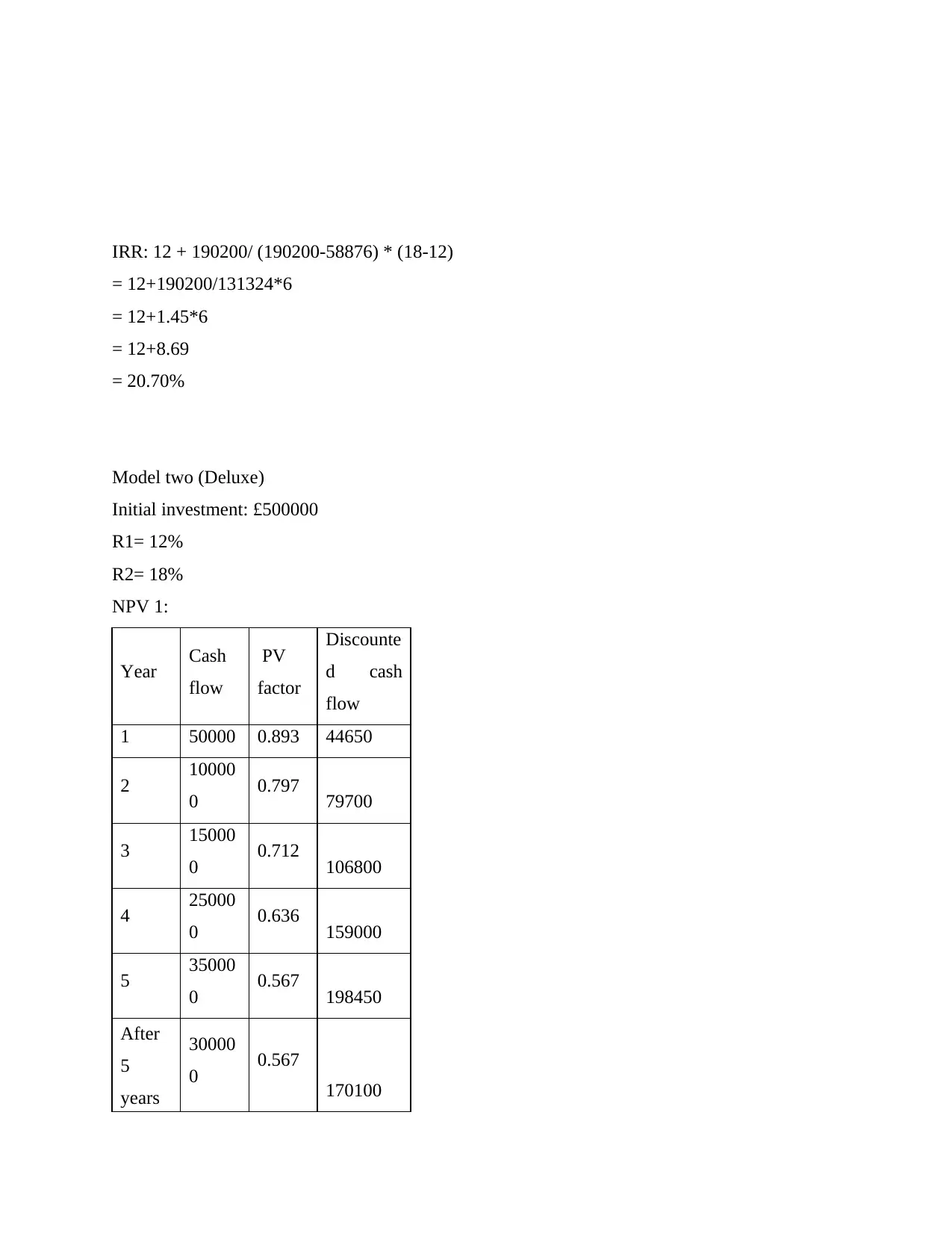

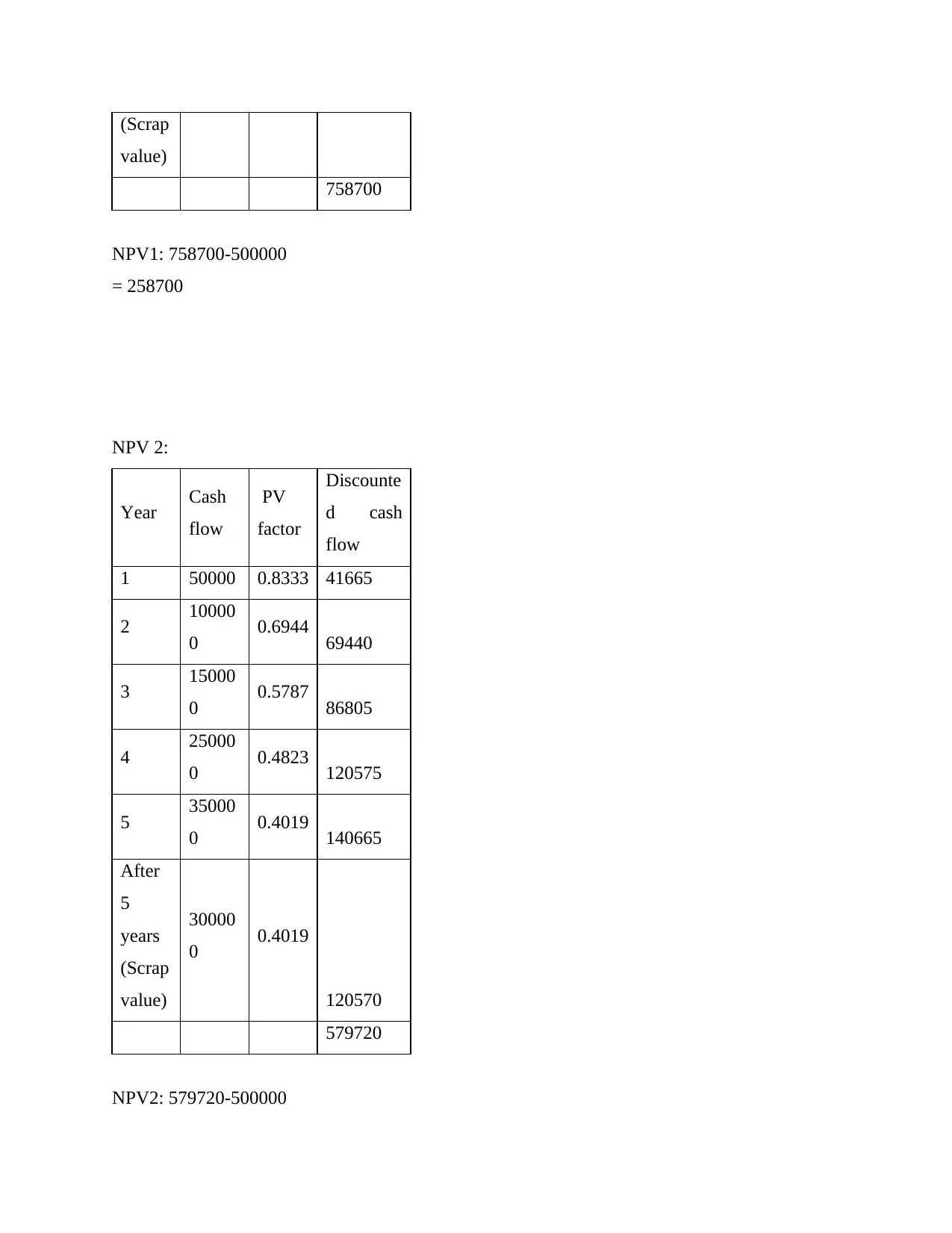

This report provides a detailed analysis of business decision-making, focusing on financial analysis and investment appraisal. The report begins with an examination of accounting ratios, including profitability, liquidity, and gearing, and their implications for a company like Tesco. It also addresses the limitations of using accounting ratios and discusses other factors that can affect a business. The core of the report centers on investment appraisal techniques such as payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR). Each technique is explained, applied to two investment models (Super and Deluxe), and evaluated based on its advantages and disadvantages. The report concludes with a recommendation for Sunderland Plc, based on the investment appraisal results, suggesting which investment model would be more beneficial. The report utilizes financial data and calculations to support its findings and recommendations.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.