Financial Decision Making Report: Analysis of Alpha Ltd Finances

VerifiedAdded on 2021/02/20

|12

|3842

|84

Report

AI Summary

This report provides a comprehensive analysis of financial decision-making processes, emphasizing the crucial role of accounting and financial systems. The report delves into the application of various management accounting techniques, including financial planning, analysis of financial statements, historical cost accounting, standard costing, budgetary control, marginal costing, fund flow statements, cash flow statements, revaluation accounting, and statistical/graphical techniques, all of which are essential for effective planning, control, and decision-making within a business. The report also includes a case study focused on Alpha Ltd, examining the calculation and interpretation of various financial ratios to assess its financial performance. The conclusion highlights the importance of financial statement analysis for informed decision-making and the value of management accounting systems in supporting organizational goals.

Financial Decision

Making

Making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

TASK - 1 .........................................................................................................................................3

Role of the accounting / finance and management accounting system in planning, controlling

and decision making process: .....................................................................................................3

CONCLUSION: ..............................................................................................................................7

REFERENCES................................................................................................................................8

TASK – 2 ........................................................................................................................................9

(A) calculation of the different ratio of the Alpha Ltd for the two year: ....................................9

(B) Comment on the financial performance of the Alpha Ltd: .................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY ..................................................................................................................................3

TASK - 1 .........................................................................................................................................3

Role of the accounting / finance and management accounting system in planning, controlling

and decision making process: .....................................................................................................3

CONCLUSION: ..............................................................................................................................7

REFERENCES................................................................................................................................8

TASK – 2 ........................................................................................................................................9

(A) calculation of the different ratio of the Alpha Ltd for the two year: ....................................9

(B) Comment on the financial performance of the Alpha Ltd: .................................................10

REFERENCES..............................................................................................................................12

INTRODUCTION

The term finance is defined as management of the large amount of money by a particular

department in the firm (Loibl, 2018). It includes the management of the assets, liabilities,

revenue and expenses and debts of the business. It involves the procurement and utilization of

the funds in the so that a business can carry out the financial operation in a efficient manner. The

finance / accounting function based on the making the decision by the finance management with

the data and information by financial statement and reports. The financial decision involves the

decision related to raise the fund from the share capital and debentures. These are the

fundamental business information and system that help in decision making process related to

financial information and data. In the report, the management accounting system and techniques

that is relevant with financial and other information in respect of the organisation. It also covers

the financial ratio that is based on the financial statement like trading and p&l account and the

final account of the company. The accounting and financial system of an organisation play a

significant role in in order to prepare the financial statement and reports in the business.

To better understand the financial decision making concepts, company Zara is chosen to prepare

this report. The company is retail sector that is placed in the Spain. The company is founded in

the year of 1974 and the management of the company is planing to carried out its activities at

different location and the product are clothing, accessories, shoes, swimwear, beauty and

perfumes in upcoming years. It is crucial to the business management to measure the financial

statements and reports so they able to make the decision for the requirement of the financing

resources to expand the business.

The term finance is defined as management of the large amount of money by a particular

department in the firm (Loibl, 2018). It includes the management of the assets, liabilities,

revenue and expenses and debts of the business. It involves the procurement and utilization of

the funds in the so that a business can carry out the financial operation in a efficient manner. The

finance / accounting function based on the making the decision by the finance management with

the data and information by financial statement and reports. The financial decision involves the

decision related to raise the fund from the share capital and debentures. These are the

fundamental business information and system that help in decision making process related to

financial information and data. In the report, the management accounting system and techniques

that is relevant with financial and other information in respect of the organisation. It also covers

the financial ratio that is based on the financial statement like trading and p&l account and the

final account of the company. The accounting and financial system of an organisation play a

significant role in in order to prepare the financial statement and reports in the business.

To better understand the financial decision making concepts, company Zara is chosen to prepare

this report. The company is retail sector that is placed in the Spain. The company is founded in

the year of 1974 and the management of the company is planing to carried out its activities at

different location and the product are clothing, accessories, shoes, swimwear, beauty and

perfumes in upcoming years. It is crucial to the business management to measure the financial

statements and reports so they able to make the decision for the requirement of the financing

resources to expand the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MAIN BODY

TASK - 1

Role of the accounting / finance and management accounting system in planning, controlling and

decision making process:

The management accounting techniques and system are the basic business operation that

help in the devising the planning process, performance management and decision making

process and provides the structured expertise in the particular profession to control the reporting.

It is controlling activities that help in formulation of the business strategies and implications of

the rules and operating process in the system. There are different types of the management

accounting system that are needed to operate the business activities. Some of the management

accounting system are described as under:

Financial Planning: This is long term process of estimating the required capital and funds

to invest in the particular projects. It frames the long term policies of the business related

to procurement of funds, investment and management of financial resources. The

financial plan covered the comprehensive statement of funds related to Alpha company

that described the long term objective, funds, saving, expenses and management of the

resources in order to uses in the future. The management of the Zara is needed to use the

financial resources in a effective manner in the future projects as per the financial

planning of the business (Danovi, Riv and Azzola, 2016).

Analysis of the financial statement: This process contents the analysing and inter-prate

the financial statement and reports in front of management of the company (Lichtenberg,

Qualls and Smyer, 2015). These financial statement covers the fundamental structure of

finance like final accounts as trading and p&l account, balance sheet and other reports of

the company. This is the particular process of measuring the financial statements for the

purposes of the decision making in the alpha Ltd These reports and statement are used by

the external stakeholder to understand the financial health as well as business

performance.

Historical cost accounting: It is a economic term that is defined in the cost accounting

that drives the value of an assets on the final accounts as per its original cost when assets

is purchased on the same amount. The historical cost method is used for the fix assets in

TASK - 1

Role of the accounting / finance and management accounting system in planning, controlling and

decision making process:

The management accounting techniques and system are the basic business operation that

help in the devising the planning process, performance management and decision making

process and provides the structured expertise in the particular profession to control the reporting.

It is controlling activities that help in formulation of the business strategies and implications of

the rules and operating process in the system. There are different types of the management

accounting system that are needed to operate the business activities. Some of the management

accounting system are described as under:

Financial Planning: This is long term process of estimating the required capital and funds

to invest in the particular projects. It frames the long term policies of the business related

to procurement of funds, investment and management of financial resources. The

financial plan covered the comprehensive statement of funds related to Alpha company

that described the long term objective, funds, saving, expenses and management of the

resources in order to uses in the future. The management of the Zara is needed to use the

financial resources in a effective manner in the future projects as per the financial

planning of the business (Danovi, Riv and Azzola, 2016).

Analysis of the financial statement: This process contents the analysing and inter-prate

the financial statement and reports in front of management of the company (Lichtenberg,

Qualls and Smyer, 2015). These financial statement covers the fundamental structure of

finance like final accounts as trading and p&l account, balance sheet and other reports of

the company. This is the particular process of measuring the financial statements for the

purposes of the decision making in the alpha Ltd These reports and statement are used by

the external stakeholder to understand the financial health as well as business

performance.

Historical cost accounting: It is a economic term that is defined in the cost accounting

that drives the value of an assets on the final accounts as per its original cost when assets

is purchased on the same amount. The historical cost method is used for the fix assets in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

various country by following GAAP generally accepted accounting principle. The

historical cost is not updated or changes on yearly basis (Danovi, Riv and Azzola, 2016).

Zara company is using this system for the cost accounting purpose by valuing the assets

on the cost of acquisition.

Standard costing: It is defined as premeditated cost that is forecasted on the performing of

business operating and activities for producing the goods and services at normal level of

production. It is used as planning tools that manage and control the cost activities at

normal production level (Bentley and Teeguarden, 2018). It estimates the cost of a

processing unit of the business. Zara Ltd is using this system to forecast the budgeted cost

for certain level of the production. And compare with actual output to find the variances.

Budgetary control: This is process of the management accounting system that estimate

figures the cost of production like cost of direct material, labour and overhead at

particular level of manufacturing and compare with the actual output of production

(Epstein, Buhovac and Yuthas, 2015). This is mechanism that control the spending limit

of an processing unit and make a favourable comparison between actual and standard to

find the deviation in the overall cost. In the Zara company, management is using this tool

in the accounting system to find the estimated cost of the particular task and project at

manufacturing unit.

Marginal costing: It refers to cost of the one extra unit of production. This cost is

calculated change in the cost which arise when total output is increased by certain unit of

manufactured. This cost covers both the cost fix and variable cost for the accounting

purpose. Fix cost are fix on the total production unit and variable may fluctuate as per

unit of output. In the Zara company, this techniques of the cost accounting is used in the

preparation of the marginal statement.

Fund flow statement: it is financial statement that shows the funds and resources

generated and allocated for the particular period of time. It includes the cash inflow and

outflow of the funds from the different operation of the business. And also represent the

sources and application of the fund from these activities. Company Zara is using this

tools to the know the flow of the money in the business.

Cash flow statement: It is statement that disclose the cash fund arise from the different

operation of the business over a period of time. It includes the business activities such as

historical cost is not updated or changes on yearly basis (Danovi, Riv and Azzola, 2016).

Zara company is using this system for the cost accounting purpose by valuing the assets

on the cost of acquisition.

Standard costing: It is defined as premeditated cost that is forecasted on the performing of

business operating and activities for producing the goods and services at normal level of

production. It is used as planning tools that manage and control the cost activities at

normal production level (Bentley and Teeguarden, 2018). It estimates the cost of a

processing unit of the business. Zara Ltd is using this system to forecast the budgeted cost

for certain level of the production. And compare with actual output to find the variances.

Budgetary control: This is process of the management accounting system that estimate

figures the cost of production like cost of direct material, labour and overhead at

particular level of manufacturing and compare with the actual output of production

(Epstein, Buhovac and Yuthas, 2015). This is mechanism that control the spending limit

of an processing unit and make a favourable comparison between actual and standard to

find the deviation in the overall cost. In the Zara company, management is using this tool

in the accounting system to find the estimated cost of the particular task and project at

manufacturing unit.

Marginal costing: It refers to cost of the one extra unit of production. This cost is

calculated change in the cost which arise when total output is increased by certain unit of

manufactured. This cost covers both the cost fix and variable cost for the accounting

purpose. Fix cost are fix on the total production unit and variable may fluctuate as per

unit of output. In the Zara company, this techniques of the cost accounting is used in the

preparation of the marginal statement.

Fund flow statement: it is financial statement that shows the funds and resources

generated and allocated for the particular period of time. It includes the cash inflow and

outflow of the funds from the different operation of the business. And also represent the

sources and application of the fund from these activities. Company Zara is using this

tools to the know the flow of the money in the business.

Cash flow statement: It is statement that disclose the cash fund arise from the different

operation of the business over a period of time. It includes the business activities such as

operational, investment and financing. It signify the changes in the balance sheet and

income statement affects the cash and cash equivalent. Company Zara is using this tools

to know cash fund on the annually basis.

Revaluation accounting: It represent the positive changes between fair market value and

original cost of the particular assets(Lee and Lee, 2015). The increment in the price of the

assets reflects through current market value that need to be adjusted by the revaluation

account. In the same manner company alpha is finding the correct market value of its

assets.

Statical and graphical techniques: This is the practical approaches that is related with

analysing and measuring the financial data and information by the help of bar graph and

charts. In this tools, the interpretation is presented by evaluating the financial states and

graph. Zara is using this tool to better representation of the financial statement and

reports.

Communicating: As per this management accounting tools, management are required the

the financial statement and data to make the business decision. It further, they published

the final data to make available for the end user.

Critical analysis- All the data and information that are required to management in order to

make a business decision related to future (Walter, 2016). So all the management accounting

techniques and system are mandatory as it provides support to the business management in order

to further analyse and determine the financial position of the business. Here, some importance of

these accounting tools and techniques are mentioned as under:

Performance measurement - These accounting tools provides a supports on the measuring

the actual performance of an entity. By applying the method of standard costing and

budgetary control system at the level of production, the estimated data and information

can be attained to understand the situation of the manufacturing unit. Alpha is using these

tools to know the actual performance of the particular unit.

Increment in the efficiency of the business: The management accounting tools and

techniques are really helpful in enhancement the business functional and operational

activities of the production unit. It increases the business performance by elevating the

operational productivity of the manufacturing unit. Company is using accounting tool to

increase the effectiveness of the business.

income statement affects the cash and cash equivalent. Company Zara is using this tools

to know cash fund on the annually basis.

Revaluation accounting: It represent the positive changes between fair market value and

original cost of the particular assets(Lee and Lee, 2015). The increment in the price of the

assets reflects through current market value that need to be adjusted by the revaluation

account. In the same manner company alpha is finding the correct market value of its

assets.

Statical and graphical techniques: This is the practical approaches that is related with

analysing and measuring the financial data and information by the help of bar graph and

charts. In this tools, the interpretation is presented by evaluating the financial states and

graph. Zara is using this tool to better representation of the financial statement and

reports.

Communicating: As per this management accounting tools, management are required the

the financial statement and data to make the business decision. It further, they published

the final data to make available for the end user.

Critical analysis- All the data and information that are required to management in order to

make a business decision related to future (Walter, 2016). So all the management accounting

techniques and system are mandatory as it provides support to the business management in order

to further analyse and determine the financial position of the business. Here, some importance of

these accounting tools and techniques are mentioned as under:

Performance measurement - These accounting tools provides a supports on the measuring

the actual performance of an entity. By applying the method of standard costing and

budgetary control system at the level of production, the estimated data and information

can be attained to understand the situation of the manufacturing unit. Alpha is using these

tools to know the actual performance of the particular unit.

Increment in the efficiency of the business: The management accounting tools and

techniques are really helpful in enhancement the business functional and operational

activities of the production unit. It increases the business performance by elevating the

operational productivity of the manufacturing unit. Company is using accounting tool to

increase the effectiveness of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Above discussed point are the ordinary benefit of these system here some of the other

benefit that used in the planning, controlling and decision making process are as below:Effective

Planning: The importance of the management accounting system and tools in effective

planning of the business strategies that help in the financial decision making by the management

of the processing unit. There are wide system in the organisation that needs to apply in the

business to make the decision related to effective planning. These business planing and strategies

are making in proper forecasting the long term business goal.

Controlling: The main importance of the management accounting process is to better

control on the business functional and operational activities. In the Zara company, management

uses tools in controlling the processing and manufacturing unit of the business.

Decision making: These management accounting system and tools help in the decision

making process to the management of the company. In the Zara the management can take the

decision from analysed reports and statement for their upcoming projects in next 10 year.

All these are the benefits of the management accounting tools in relevance with Alpha

Ltd that help in the planing and controlling the business activities as well as the decision making

the process on the behalf of the organisational future model.

CONCLUSION:

From this report it is concluded as analysis of the financial statement and reports of a

business is really helpful in the financial decision making system. It is concluded the

management accounting process and system provides to management a full understanding of the

business concepts and function. So that they apply these system in the business operation to

planning, control and decision making process. In this report further concluded ans measurement

of the ratio analysis and its interpretation of the financial data of the company alpha Ltd for the

two years.

benefit that used in the planning, controlling and decision making process are as below:Effective

Planning: The importance of the management accounting system and tools in effective

planning of the business strategies that help in the financial decision making by the management

of the processing unit. There are wide system in the organisation that needs to apply in the

business to make the decision related to effective planning. These business planing and strategies

are making in proper forecasting the long term business goal.

Controlling: The main importance of the management accounting process is to better

control on the business functional and operational activities. In the Zara company, management

uses tools in controlling the processing and manufacturing unit of the business.

Decision making: These management accounting system and tools help in the decision

making process to the management of the company. In the Zara the management can take the

decision from analysed reports and statement for their upcoming projects in next 10 year.

All these are the benefits of the management accounting tools in relevance with Alpha

Ltd that help in the planing and controlling the business activities as well as the decision making

the process on the behalf of the organisational future model.

CONCLUSION:

From this report it is concluded as analysis of the financial statement and reports of a

business is really helpful in the financial decision making system. It is concluded the

management accounting process and system provides to management a full understanding of the

business concepts and function. So that they apply these system in the business operation to

planning, control and decision making process. In this report further concluded ans measurement

of the ratio analysis and its interpretation of the financial data of the company alpha Ltd for the

two years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals:

Loibl, C., 2018. 26 Living in Poverty: Understanding the Financial Behaviour of Vulnerable

Groups. CENTRE FOR DECISION RESEARCH, UNIVERSITY OF LEEDS, UK, p.421.

Bentley, W .R. and Teeguarden, D .E., 2018. Financial maturity: a theoretical review. In

Economics of Forestry. (pp. 67-78). Routledge.

Lichtenberg, P. A., Qualls, S. H. and Smyer, M. A., 2015. Competency and decision-making

capacity: Negotiating health and financial decision making.

Epstein, M. J., Buhovac, A .R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long range planning. 48(1). pp.35-45.

Lee, S .W. and Lee, K. H., 2015. Decision Making Model for Selecting Financial Company

Server Privilege Account Operations. Journal of the Korea Institute of Information

Security and Cryptology. 25(6). pp.1607-1620.

Walter, C., 2016. The financial Logos: The framing of financial decision-making by

mathematical modelling. Research in International Business and Finance. 37. pp.597-

604.

Finke, M .S., Howe, J. S. and Huston, S .J., 2016. Old age and the decline in financial literacy.

Management Science. 63(1). pp.213-230.

Brounen, D., Koedijk, K .G. and Pownall, R .A., 2016. Household financial planning and savings

behavior. Journal of International Money and Finance. 69. pp.95-107.

Correia, T., Dussault, G. and Pontes, C., 2015. The impact of the financial crisis on human

resources for health policies in three southern-Europe countries. Health Policy. 119(12).

pp.1600-1605.

Wald, D .J. and Franco, G., 2016. Money matters: Rapid post-earthquake financial decision-

making. Natural Hazards Observer. 40(7). pp.24-27.

Baker, H .K. and Ricciardi, V., 2015. Understanding behavioral aspects of financial planning and

investing. Journal of financial Planning. 28(3). pp.22-26.

Loerwald, D. and Stemmann, A., 2016. Behavioral finance and financial literacy: Educational

implications of biases in financial decision making. In International Handbook of

Financial Literacy. (pp. 25-38). Springer, Singapore.

Books and journals:

Loibl, C., 2018. 26 Living in Poverty: Understanding the Financial Behaviour of Vulnerable

Groups. CENTRE FOR DECISION RESEARCH, UNIVERSITY OF LEEDS, UK, p.421.

Bentley, W .R. and Teeguarden, D .E., 2018. Financial maturity: a theoretical review. In

Economics of Forestry. (pp. 67-78). Routledge.

Lichtenberg, P. A., Qualls, S. H. and Smyer, M. A., 2015. Competency and decision-making

capacity: Negotiating health and financial decision making.

Epstein, M. J., Buhovac, A .R. and Yuthas, K., 2015. Managing social, environmental and

financial performance simultaneously. Long range planning. 48(1). pp.35-45.

Lee, S .W. and Lee, K. H., 2015. Decision Making Model for Selecting Financial Company

Server Privilege Account Operations. Journal of the Korea Institute of Information

Security and Cryptology. 25(6). pp.1607-1620.

Walter, C., 2016. The financial Logos: The framing of financial decision-making by

mathematical modelling. Research in International Business and Finance. 37. pp.597-

604.

Finke, M .S., Howe, J. S. and Huston, S .J., 2016. Old age and the decline in financial literacy.

Management Science. 63(1). pp.213-230.

Brounen, D., Koedijk, K .G. and Pownall, R .A., 2016. Household financial planning and savings

behavior. Journal of International Money and Finance. 69. pp.95-107.

Correia, T., Dussault, G. and Pontes, C., 2015. The impact of the financial crisis on human

resources for health policies in three southern-Europe countries. Health Policy. 119(12).

pp.1600-1605.

Wald, D .J. and Franco, G., 2016. Money matters: Rapid post-earthquake financial decision-

making. Natural Hazards Observer. 40(7). pp.24-27.

Baker, H .K. and Ricciardi, V., 2015. Understanding behavioral aspects of financial planning and

investing. Journal of financial Planning. 28(3). pp.22-26.

Loerwald, D. and Stemmann, A., 2016. Behavioral finance and financial literacy: Educational

implications of biases in financial decision making. In International Handbook of

Financial Literacy. (pp. 25-38). Springer, Singapore.

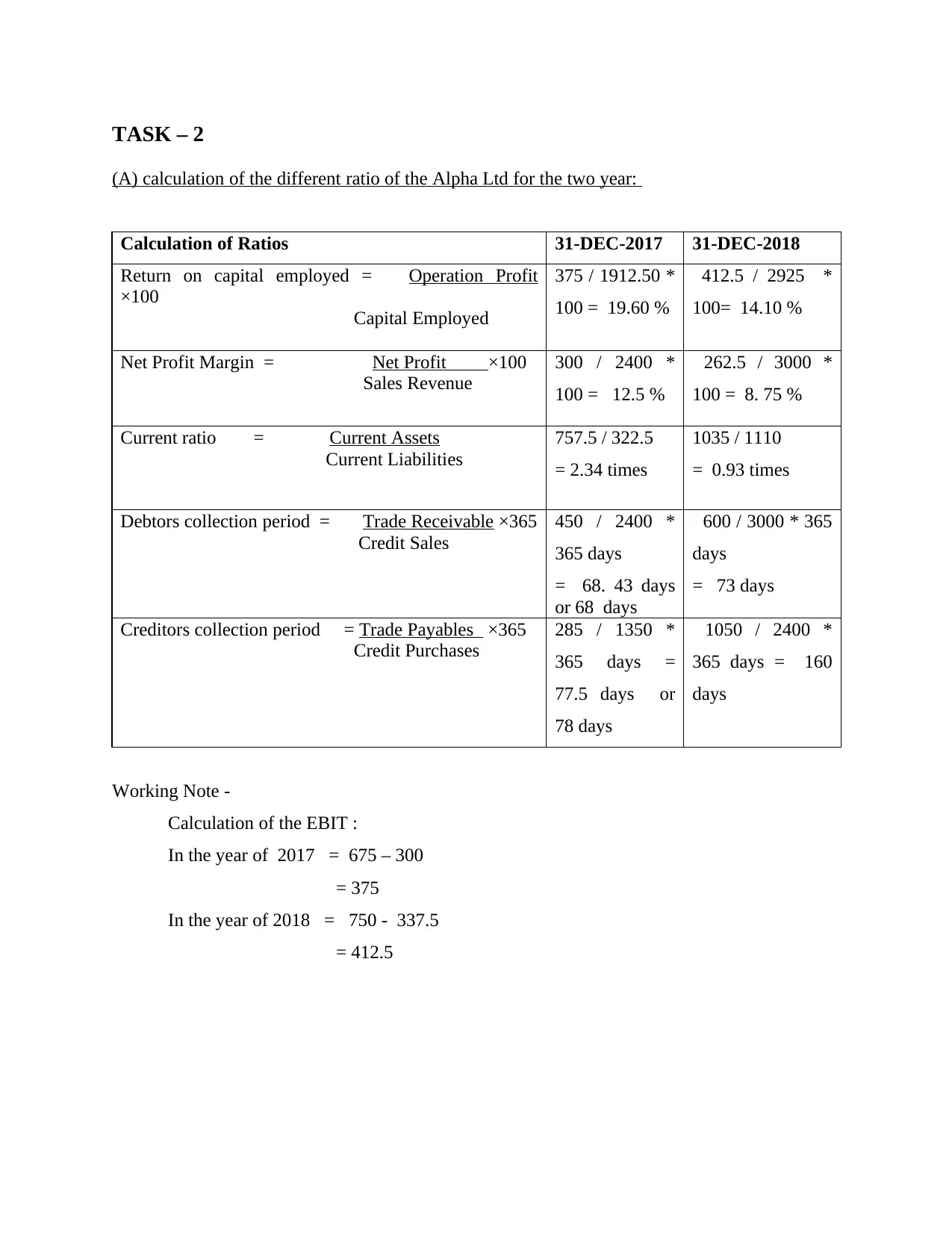

TASK – 2

(A) calculation of the different ratio of the Alpha Ltd for the two year:

Calculation of Ratios 31-DEC-2017 31-DEC-2018

Return on capital employed = Operation Profit

×100

Capital Employed

375 / 1912.50 *

100 = 19.60 %

412.5 / 2925 *

100= 14.10 %

Net Profit Margin = Net Profit ×100

Sales Revenue

300 / 2400 *

100 = 12.5 %

262.5 / 3000 *

100 = 8. 75 %

Current ratio = Current Assets

Current Liabilities

757.5 / 322.5

= 2.34 times

1035 / 1110

= 0.93 times

Debtors collection period = Trade Receivable ×365

Credit Sales

450 / 2400 *

365 days

= 68. 43 days

or 68 days

600 / 3000 * 365

days

= 73 days

Creditors collection period = Trade Payables ×365

Credit Purchases

285 / 1350 *

365 days =

77.5 days or

78 days

1050 / 2400 *

365 days = 160

days

Working Note -

Calculation of the EBIT :

In the year of 2017 = 675 – 300

= 375

In the year of 2018 = 750 - 337.5

= 412.5

(A) calculation of the different ratio of the Alpha Ltd for the two year:

Calculation of Ratios 31-DEC-2017 31-DEC-2018

Return on capital employed = Operation Profit

×100

Capital Employed

375 / 1912.50 *

100 = 19.60 %

412.5 / 2925 *

100= 14.10 %

Net Profit Margin = Net Profit ×100

Sales Revenue

300 / 2400 *

100 = 12.5 %

262.5 / 3000 *

100 = 8. 75 %

Current ratio = Current Assets

Current Liabilities

757.5 / 322.5

= 2.34 times

1035 / 1110

= 0.93 times

Debtors collection period = Trade Receivable ×365

Credit Sales

450 / 2400 *

365 days

= 68. 43 days

or 68 days

600 / 3000 * 365

days

= 73 days

Creditors collection period = Trade Payables ×365

Credit Purchases

285 / 1350 *

365 days =

77.5 days or

78 days

1050 / 2400 *

365 days = 160

days

Working Note -

Calculation of the EBIT :

In the year of 2017 = 675 – 300

= 375

In the year of 2018 = 750 - 337.5

= 412.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(B) Comment on the financial performance of the Alpha Ltd:

In this section, interpretation of the financial position of the company made by

considering the ratio analysis of the alpha Ltd. Management of the company can address the

financial issue and problem that are arises around the organisation ( Finke, Howe and Huston,

2016). The ratio analysis help in assertion the sales related issues and problem so that internal;

and external stakeholder can understand the actual performance and situation of the business.

Here, analysation and interpretation of the different ratio are made for the two years:

Return on the capital employed (ROCE) - This is the profitability ratio that measure the

effectiveness of an organisation (Brounen, Koedijk and Pownall, 2016). It shows how effectively

a firm generating its profits from its capital employed. It compares the net generated net profit

with total capital employed. It shows the long term profitability that is based on the owners

capital and outsider loans. Net profit is assumed on the capital employed before tax and interest.

In the relevance with alpha Ltd, management can make the future decision by considering this

ratio of probability. In the year of 2017, ROCE ratio is around 19 %, but it is decreased in the

next year and become the ratio is 14 % . EBIT is 375 in the year of 2017 and it increased to

412.5 in the next year. So it show income is increasing but not the capital employed by

considering these two year data. Company is needs to increase the comprehensive sales and

reduce the operating expenses (ATTOM, 2016).

Net profit margin : This is the basic term in the business that is defined as earning of the

profit on the total sales revenue (Correia, Dussault and Pontes, 2015). This ratio evaluates the

efficiency of the business by considering the profit earning abilities from its capital employed.

Higher the ratio, profitability of business is also higher. In respect of the alpha company, net

profit margin of the company is around 12 % in the year of 2017 but in the next year it will

become 8.75 %. so it is assessed that the net margin of profit will be decreased in the next year as

compare to previous one. The sales is increased by 25 % but the net profit decreased in the 2018

as compare to previous year. So it is important to the management of the company to provide the

attention on the fix cost and variable cost. As comprehensive net profit margin is reduced due to

increment in the operating costs.

Current ratio: this is financial term that defined as liquidity ratio which measure the

ability of short times assets to pay the obligation or liabilities those due in the one year (Wald,

In this section, interpretation of the financial position of the company made by

considering the ratio analysis of the alpha Ltd. Management of the company can address the

financial issue and problem that are arises around the organisation ( Finke, Howe and Huston,

2016). The ratio analysis help in assertion the sales related issues and problem so that internal;

and external stakeholder can understand the actual performance and situation of the business.

Here, analysation and interpretation of the different ratio are made for the two years:

Return on the capital employed (ROCE) - This is the profitability ratio that measure the

effectiveness of an organisation (Brounen, Koedijk and Pownall, 2016). It shows how effectively

a firm generating its profits from its capital employed. It compares the net generated net profit

with total capital employed. It shows the long term profitability that is based on the owners

capital and outsider loans. Net profit is assumed on the capital employed before tax and interest.

In the relevance with alpha Ltd, management can make the future decision by considering this

ratio of probability. In the year of 2017, ROCE ratio is around 19 %, but it is decreased in the

next year and become the ratio is 14 % . EBIT is 375 in the year of 2017 and it increased to

412.5 in the next year. So it show income is increasing but not the capital employed by

considering these two year data. Company is needs to increase the comprehensive sales and

reduce the operating expenses (ATTOM, 2016).

Net profit margin : This is the basic term in the business that is defined as earning of the

profit on the total sales revenue (Correia, Dussault and Pontes, 2015). This ratio evaluates the

efficiency of the business by considering the profit earning abilities from its capital employed.

Higher the ratio, profitability of business is also higher. In respect of the alpha company, net

profit margin of the company is around 12 % in the year of 2017 but in the next year it will

become 8.75 %. so it is assessed that the net margin of profit will be decreased in the next year as

compare to previous one. The sales is increased by 25 % but the net profit decreased in the 2018

as compare to previous year. So it is important to the management of the company to provide the

attention on the fix cost and variable cost. As comprehensive net profit margin is reduced due to

increment in the operating costs.

Current ratio: this is financial term that defined as liquidity ratio which measure the

ability of short times assets to pay the obligation or liabilities those due in the one year (Wald,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and Franco, 2016). company can maximize its current assets to pay the short term obligation of

the business. It compare the firm's current assets and liabilities. The ideal ratio is 2 : 1. In respect

to company alpha Ltd, current ratio in the year of 2017 is above 2 which shows a ideal situation.

In this condition company have enough assets to pay the its current liabilities. But in the year

2018, current ratio decreased to 0.93 times which is below 2. that means company is not able to

pay its liabilities. It need to improve the current assets by the management of Alpha Ltd (Habib

and Huang, 2019).

Debtors collection period: This is defined as average amount of days it takes to cover the

owned money from its customers (Loerwald and Stemmann, 2016). It shows the how many days

it will take to cover the amount of debt from its debtors. The main objectives behind it to know

the solvent customers which will pay the the amount with in given credit time period. In

particular company alpha Ltd the debtors collection period is 68 day in the year of 2017 which is

around 2.25 month. This is good for the organisation. But in the next year they paid the credit

amount in 73 days. It is almost same in both the year (Hendri, 2015).

Creditors payment period- The term creditors payment period has been defined as a type

of ratio whose purpose of calculation is to find out the average time period taken by company

(Baker and Ricciardi, 2015). With the use of this ratio companies' efficiency to make payment

can be assessed. This ratio is being calculated in terms of days which means if this ratio is in

higher days then it is estimated that company's ability to make payment is lower. On the other

hand if this ratio is in lower days then it is estimated that company's efficiency is good. Herein,

the aspect of above Alpha limited company, this ratio is of 73 days in year 2017 which increased

in further year 2018 and became of 160 days. It is indicating that company's debt payment

efficiency has been decreased which is needed to be improved. So it is recommended to

company's finance department that they should try to make their transactions in cash so that their

ratio can be improve (Wu, Wei and Peng, 2015).

the business. It compare the firm's current assets and liabilities. The ideal ratio is 2 : 1. In respect

to company alpha Ltd, current ratio in the year of 2017 is above 2 which shows a ideal situation.

In this condition company have enough assets to pay the its current liabilities. But in the year

2018, current ratio decreased to 0.93 times which is below 2. that means company is not able to

pay its liabilities. It need to improve the current assets by the management of Alpha Ltd (Habib

and Huang, 2019).

Debtors collection period: This is defined as average amount of days it takes to cover the

owned money from its customers (Loerwald and Stemmann, 2016). It shows the how many days

it will take to cover the amount of debt from its debtors. The main objectives behind it to know

the solvent customers which will pay the the amount with in given credit time period. In

particular company alpha Ltd the debtors collection period is 68 day in the year of 2017 which is

around 2.25 month. This is good for the organisation. But in the next year they paid the credit

amount in 73 days. It is almost same in both the year (Hendri, 2015).

Creditors payment period- The term creditors payment period has been defined as a type

of ratio whose purpose of calculation is to find out the average time period taken by company

(Baker and Ricciardi, 2015). With the use of this ratio companies' efficiency to make payment

can be assessed. This ratio is being calculated in terms of days which means if this ratio is in

higher days then it is estimated that company's ability to make payment is lower. On the other

hand if this ratio is in lower days then it is estimated that company's efficiency is good. Herein,

the aspect of above Alpha limited company, this ratio is of 73 days in year 2017 which increased

in further year 2018 and became of 160 days. It is indicating that company's debt payment

efficiency has been decreased which is needed to be improved. So it is recommended to

company's finance department that they should try to make their transactions in cash so that their

ratio can be improve (Wu, Wei and Peng, 2015).

REFERENCES

Books and journals:

ATTOM, B.E., 2016. WORKING CAPITAL MANAGEMENT AS A FINANCIAL

STRATEGY TO IMPROVE PROFITABILITY AND GROWTH OF MICRO AND

SMALL-SCALE ENTERPRISES (MSEs) OPERATING IN THE CENTRAL REGION

OF GHANA. CLEAR International Journal of Research in Commerce & Management.

7(7).

Danovi, A., Riva, P. and Azzola, M., 2016. Avoiding bankruptcy in Italy: Preventive

arrangement with creditors. In Contemporary issues in finance: Current challenges from

across Europe (pp. 77-94). Emerald Group Publishing Limited.

Habib, A. and Huang, H.J., 2019. Abnormally long audit report lags and future stock price crash

risk: evidence from China. International Journal of Managerial Finance.

Hendri, E., 2015. Pengaruh Debt To Asset Ratio (DAR), Long Term Debt To Equity Ratio

(LTDER) dan Net Profit Margin (NPM) Terhadap Harga Saham Pada Perusahan

Perbankan Yang Terdaftar di Bursa Efek Indonesia. Jurnal Media Wahana Ekonomika.

12(2).

Wu, G., Wei, X., Zhang, Z., Chen, Q. and Peng, L., 2015. A Graphene‐Based Vacuum Transistor

with a High ON/OFF Current Ratio. Advanced Functional Materials. 25(37). pp.5972-

5978.

Books and journals:

ATTOM, B.E., 2016. WORKING CAPITAL MANAGEMENT AS A FINANCIAL

STRATEGY TO IMPROVE PROFITABILITY AND GROWTH OF MICRO AND

SMALL-SCALE ENTERPRISES (MSEs) OPERATING IN THE CENTRAL REGION

OF GHANA. CLEAR International Journal of Research in Commerce & Management.

7(7).

Danovi, A., Riva, P. and Azzola, M., 2016. Avoiding bankruptcy in Italy: Preventive

arrangement with creditors. In Contemporary issues in finance: Current challenges from

across Europe (pp. 77-94). Emerald Group Publishing Limited.

Habib, A. and Huang, H.J., 2019. Abnormally long audit report lags and future stock price crash

risk: evidence from China. International Journal of Managerial Finance.

Hendri, E., 2015. Pengaruh Debt To Asset Ratio (DAR), Long Term Debt To Equity Ratio

(LTDER) dan Net Profit Margin (NPM) Terhadap Harga Saham Pada Perusahan

Perbankan Yang Terdaftar di Bursa Efek Indonesia. Jurnal Media Wahana Ekonomika.

12(2).

Wu, G., Wei, X., Zhang, Z., Chen, Q. and Peng, L., 2015. A Graphene‐Based Vacuum Transistor

with a High ON/OFF Current Ratio. Advanced Functional Materials. 25(37). pp.5972-

5978.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.