Financial Analysis Report: AstraZeneca vs. GSK, MBA Finance Module

VerifiedAdded on 2021/09/18

|29

|4389

|80

Report

AI Summary

This report presents a comprehensive financial analysis of AstraZeneca plc, comparing its performance with that of GlaxoSmithKline (GSK). The analysis examines key financial statements and calculates various ratios, including profitability (gross profit, net profit, ROCE, ROA, and operating profit), liquidity (current ratio and quick ratio), leverage (gearing ratio and debt-equity ratio), and investment ratios (EPS and P/E ratio). The report analyzes trends from 2011 to 2014, identifying factors influencing these ratios, such as revenue fluctuations, acquisitions, and financial expenses. The analysis provides insights into AstraZeneca's financial position, highlighting its strengths and weaknesses, and offers potential areas for improvement. The report also touches upon the company's history, controversies, and market position. The report concludes with a discussion on the option of purchasing shares of a competitor and the reasons behind it.

Student Electronic Assignment Cover Sheet

Student (s) Number as per your student card:10332343

Course Title: MBA (FINANCE STREAM)

Lecturer Name: ENDA MURPHY

Module/Subject Code: B9AC106

Module/Subject Title: FINANCIAL ANALYSIS

Assignment Title: FINANCIAL ANALYSIS OF ASTRAZENECA AND GSK

No. of words:2956

Date of Submission: 20/03/2016

0 | P a g e

Student (s) Number as per your student card:10332343

Course Title: MBA (FINANCE STREAM)

Lecturer Name: ENDA MURPHY

Module/Subject Code: B9AC106

Module/Subject Title: FINANCIAL ANALYSIS

Assignment Title: FINANCIAL ANALYSIS OF ASTRAZENECA AND GSK

No. of words:2956

Date of Submission: 20/03/2016

0 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS:

INTRODUCTION……………………………………………………………2

FINANCIAL PERFORMANCE AND POSITION………………………….4

OPTION OF PURCHASING SHARES OF COMPETITOR……………….13

REASONS……………………………………………………………………15

CONCLUSION……………………………………………………………….19

BIBLIOGRAPHY…………………………………………………………….20

APPENDIX…………………………………………………………………22

Figures:12

Tables:5

1 | P a g e

INTRODUCTION……………………………………………………………2

FINANCIAL PERFORMANCE AND POSITION………………………….4

OPTION OF PURCHASING SHARES OF COMPETITOR……………….13

REASONS……………………………………………………………………15

CONCLUSION……………………………………………………………….19

BIBLIOGRAPHY…………………………………………………………….20

APPENDIX…………………………………………………………………22

Figures:12

Tables:5

1 | P a g e

Introduction:

Astrazeneca plc is one of the biggest pharmaceutical companies in the

world. It is a British-Swedish company. Astra-AB of Sweden (founded in

1913) and Zeneca group plc of the UK (founded in 1993), who were long

established with a passion for science and a clear vision of the

pharmaceutical industry which led them to merge together, and a new

company, Astrazeneca plc, which was founded on April 6 th, 1999.It’s

headquarter is situated in London while the R & D are both in Sweden

and UK. Astrazeneca’s CEO is Pascal Soriot and Leif Johansson is the

Chairman.

Astrazeneca manufactures medicines for cardiovascular and metabolic

disorders, gastrointestinal and neuroscience and infection problems,

Autoimmunity inflammation and respiratory upsets, infection and

cancer.

Astrazeneca plc has also acquired companies which are as follows:

2005-Kudos pharmaceutical company.(£120m)

2006-Cambridge antibody technology.(£702m).

2007-Arrow Therapeutics($150 m) & MedImmune($15.2m).

2010-Novexel corp (antibiotic developing co.).

2011-Guangdong Beijing (Chinese company).

The company has also had controversies where in, in the year 2010, it

2 | P a g e

Astrazeneca plc is one of the biggest pharmaceutical companies in the

world. It is a British-Swedish company. Astra-AB of Sweden (founded in

1913) and Zeneca group plc of the UK (founded in 1993), who were long

established with a passion for science and a clear vision of the

pharmaceutical industry which led them to merge together, and a new

company, Astrazeneca plc, which was founded on April 6 th, 1999.It’s

headquarter is situated in London while the R & D are both in Sweden

and UK. Astrazeneca’s CEO is Pascal Soriot and Leif Johansson is the

Chairman.

Astrazeneca manufactures medicines for cardiovascular and metabolic

disorders, gastrointestinal and neuroscience and infection problems,

Autoimmunity inflammation and respiratory upsets, infection and

cancer.

Astrazeneca plc has also acquired companies which are as follows:

2005-Kudos pharmaceutical company.(£120m)

2006-Cambridge antibody technology.(£702m).

2007-Arrow Therapeutics($150 m) & MedImmune($15.2m).

2010-Novexel corp (antibiotic developing co.).

2011-Guangdong Beijing (Chinese company).

The company has also had controversies where in, in the year 2010, it

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

settled a lawsuit for $520m to settle allegations that the company

defrauded Medicaid and Medicare, and other government-funded

health care programs. In 2011, it settled a lawsuit of $68.5m in US.

Despite the uncertanities Astrazeneca faced in the past, it has managed

to keep up the good work and has continued effective research to cure

serious diseases.

The company operates in the UK, US, France, Sweden, Canada, Brazil,

China, Japan and India. The company’s largest single R & D site is based

at Alderly park, Cheshire, England with over 4,500 staff. All together,

there are over 50,000 people who work for Astrazeneca. Astrazeneca is

listed at #239 Global 2000.In 2014, company revenue was $26.09B and

net income was $1.23B. Today, Astrazeneca is listed in the 100 FTSE

index and it’s market capital is £54.8 billion which makes it 6 th in the

primary L.S.E.

Astrazeneca supplies medicines to over 100 countries and sells products

under brands Losec, Crestor, Entocort, Onglysa, Citanest, Atacand,

Nexium and Diprivan. It continues to do well in diabetes franchises and

has gained a lot of profit in the years compared to the other products.

3 | P a g e

defrauded Medicaid and Medicare, and other government-funded

health care programs. In 2011, it settled a lawsuit of $68.5m in US.

Despite the uncertanities Astrazeneca faced in the past, it has managed

to keep up the good work and has continued effective research to cure

serious diseases.

The company operates in the UK, US, France, Sweden, Canada, Brazil,

China, Japan and India. The company’s largest single R & D site is based

at Alderly park, Cheshire, England with over 4,500 staff. All together,

there are over 50,000 people who work for Astrazeneca. Astrazeneca is

listed at #239 Global 2000.In 2014, company revenue was $26.09B and

net income was $1.23B. Today, Astrazeneca is listed in the 100 FTSE

index and it’s market capital is £54.8 billion which makes it 6 th in the

primary L.S.E.

Astrazeneca supplies medicines to over 100 countries and sells products

under brands Losec, Crestor, Entocort, Onglysa, Citanest, Atacand,

Nexium and Diprivan. It continues to do well in diabetes franchises and

has gained a lot of profit in the years compared to the other products.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

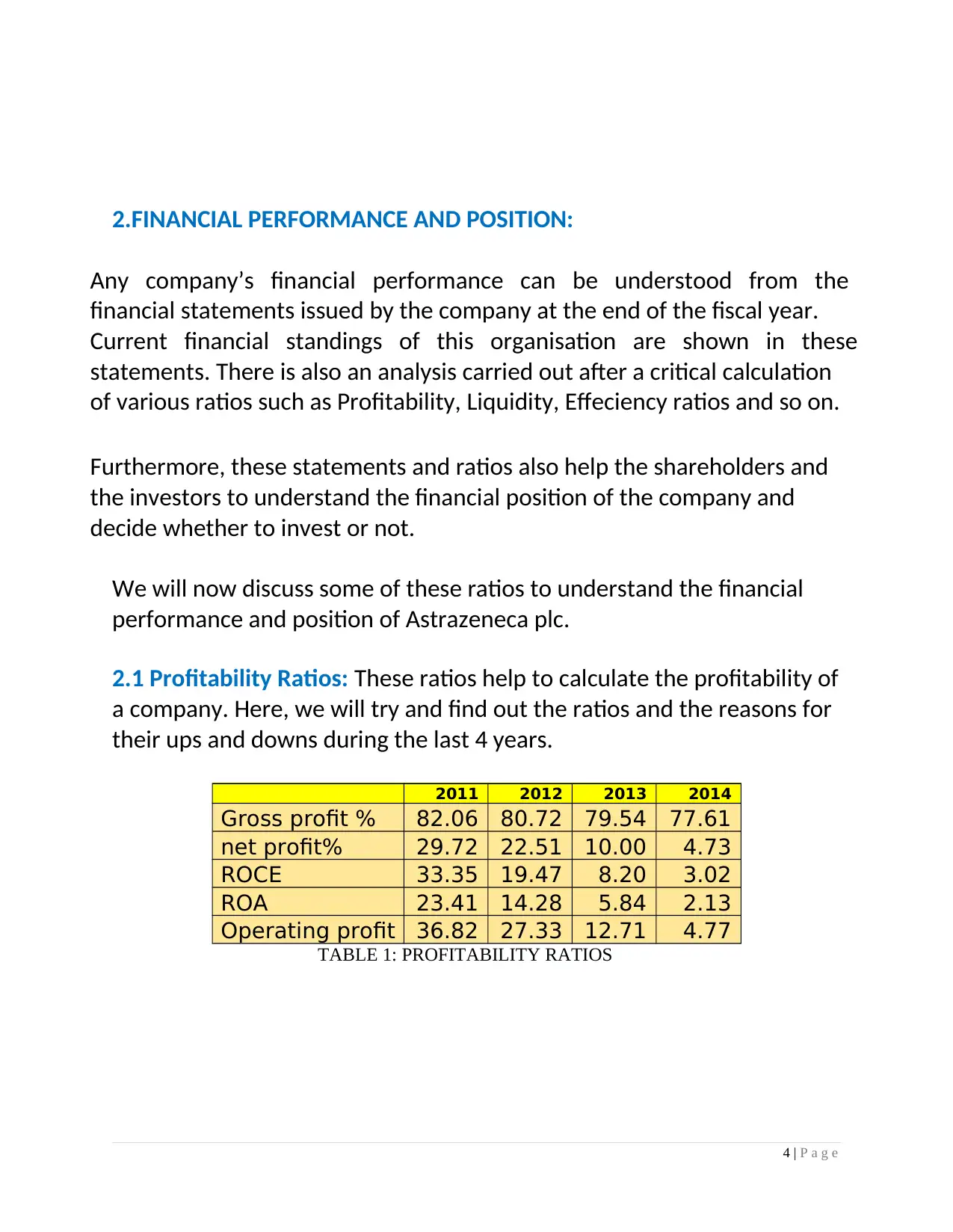

2.FINANCIAL PERFORMANCE AND POSITION:

Any company’s financial performance can be understood from the

financial statements issued by the company at the end of the fiscal year.

Current financial standings of this organisation are shown in these

statements. There is also an analysis carried out after a critical calculation

of various ratios such as Profitability, Liquidity, Effeciency ratios and so on.

Furthermore, these statements and ratios also help the shareholders and

the investors to understand the financial position of the company and

decide whether to invest or not.

We will now discuss some of these ratios to understand the financial

performance and position of Astrazeneca plc.

2.1 Profitability Ratios: These ratios help to calculate the profitability of

a company. Here, we will try and find out the ratios and the reasons for

their ups and downs during the last 4 years.

2011 2012 2013 2014

Gross profit % 82.06 80.72 79.54 77.61

net profit% 29.72 22.51 10.00 4.73

ROCE 33.35 19.47 8.20 3.02

ROA 23.41 14.28 5.84 2.13

Operating profit 36.82 27.33 12.71 4.77

TABLE 1: PROFITABILITY RATIOS

4 | P a g e

Any company’s financial performance can be understood from the

financial statements issued by the company at the end of the fiscal year.

Current financial standings of this organisation are shown in these

statements. There is also an analysis carried out after a critical calculation

of various ratios such as Profitability, Liquidity, Effeciency ratios and so on.

Furthermore, these statements and ratios also help the shareholders and

the investors to understand the financial position of the company and

decide whether to invest or not.

We will now discuss some of these ratios to understand the financial

performance and position of Astrazeneca plc.

2.1 Profitability Ratios: These ratios help to calculate the profitability of

a company. Here, we will try and find out the ratios and the reasons for

their ups and downs during the last 4 years.

2011 2012 2013 2014

Gross profit % 82.06 80.72 79.54 77.61

net profit% 29.72 22.51 10.00 4.73

ROCE 33.35 19.47 8.20 3.02

ROA 23.41 14.28 5.84 2.13

Operating profit 36.82 27.33 12.71 4.77

TABLE 1: PROFITABILITY RATIOS

4 | P a g e

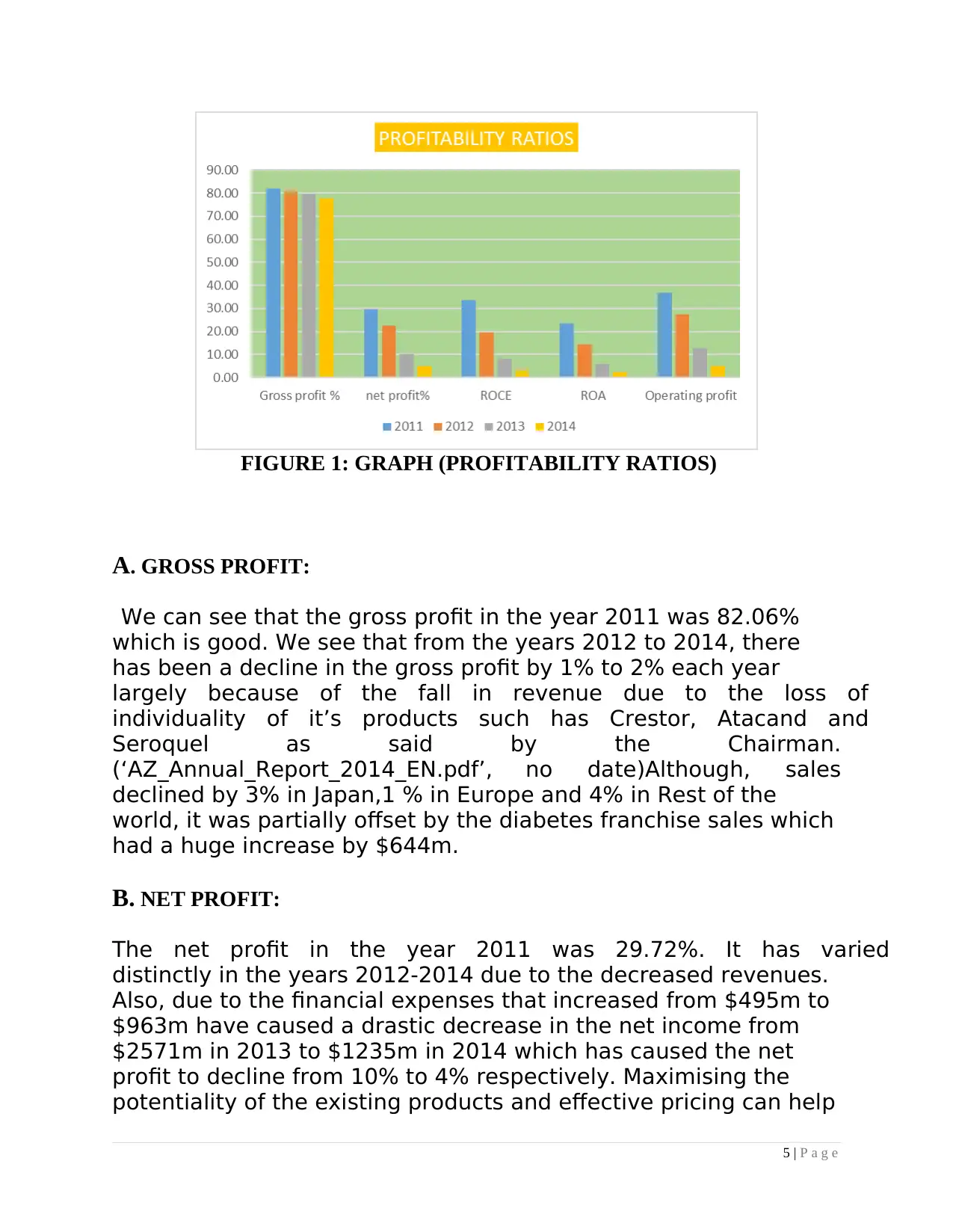

FIGURE 1: GRAPH (PROFITABILITY RATIOS)

A. GROSS PROFIT:

We can see that the gross profit in the year 2011 was 82.06%

which is good. We see that from the years 2012 to 2014, there

has been a decline in the gross profit by 1% to 2% each year

largely because of the fall in revenue due to the loss of

individuality of it’s products such has Crestor, Atacand and

Seroquel as said by the Chairman.

(‘AZ_Annual_Report_2014_EN.pdf’, no date)Although, sales

declined by 3% in Japan,1 % in Europe and 4% in Rest of the

world, it was partially offset by the diabetes franchise sales which

had a huge increase by $644m.

B. NET PROFIT:

The net profit in the year 2011 was 29.72%. It has varied

distinctly in the years 2012-2014 due to the decreased revenues.

Also, due to the financial expenses that increased from $495m to

$963m have caused a drastic decrease in the net income from

$2571m in 2013 to $1235m in 2014 which has caused the net

profit to decline from 10% to 4% respectively. Maximising the

potentiality of the existing products and effective pricing can help

5 | P a g e

A. GROSS PROFIT:

We can see that the gross profit in the year 2011 was 82.06%

which is good. We see that from the years 2012 to 2014, there

has been a decline in the gross profit by 1% to 2% each year

largely because of the fall in revenue due to the loss of

individuality of it’s products such has Crestor, Atacand and

Seroquel as said by the Chairman.

(‘AZ_Annual_Report_2014_EN.pdf’, no date)Although, sales

declined by 3% in Japan,1 % in Europe and 4% in Rest of the

world, it was partially offset by the diabetes franchise sales which

had a huge increase by $644m.

B. NET PROFIT:

The net profit in the year 2011 was 29.72%. It has varied

distinctly in the years 2012-2014 due to the decreased revenues.

Also, due to the financial expenses that increased from $495m to

$963m have caused a drastic decrease in the net income from

$2571m in 2013 to $1235m in 2014 which has caused the net

profit to decline from 10% to 4% respectively. Maximising the

potentiality of the existing products and effective pricing can help

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the in the improvement of net profit.

C. RETURN ON CAPITAL EMPLOYED:

This ratio is used for the comparison of the profits of the

competing companies through the capital used by them.

We can see that the ROCE of Astrazeneca has been

decreasing from 2011 to 2014 which was 33.35% and

3.02% respectively. In my analysis, the ROCE has

declined due to less profits made and also the acquisitons

of Pearl Therapeutics for $569million, 100% of Omthera

pharmaceutical’s shares for $323million. Also, there was

an acquisition of Almirall Sofotec for $878million was

made in 2014. High investments tend to produce low

return on capital than the existing business.

D. RETURN ON ASSETS:

This ratio helps us to understand whether how profitable

a company is with relation to their assets. We can see

that Astrazeneca’s ROA has been low from 2012 to 2014

i.e 14.28% and 2.13% respectively. The reason for this

has been the share of after tax losses in it’s joint ventures

and also the financial expenses have been more in the

year 2014 of $963 million which has led to a decline in

the profit before tax.

6 | P a g e

C. RETURN ON CAPITAL EMPLOYED:

This ratio is used for the comparison of the profits of the

competing companies through the capital used by them.

We can see that the ROCE of Astrazeneca has been

decreasing from 2011 to 2014 which was 33.35% and

3.02% respectively. In my analysis, the ROCE has

declined due to less profits made and also the acquisitons

of Pearl Therapeutics for $569million, 100% of Omthera

pharmaceutical’s shares for $323million. Also, there was

an acquisition of Almirall Sofotec for $878million was

made in 2014. High investments tend to produce low

return on capital than the existing business.

D. RETURN ON ASSETS:

This ratio helps us to understand whether how profitable

a company is with relation to their assets. We can see

that Astrazeneca’s ROA has been low from 2012 to 2014

i.e 14.28% and 2.13% respectively. The reason for this

has been the share of after tax losses in it’s joint ventures

and also the financial expenses have been more in the

year 2014 of $963 million which has led to a decline in

the profit before tax.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

E. OPERATING PROFIT:

The operating profit from 2011 to 2014 was 36.82% to

4.77% respectively. The decline of operating profit was

due to the expenditure associated with the growth

platforms such as research and development expenses of

$5579m in 2014.The increase in selling, administrative

and distribution costs have led to a decline in the net

operating margin. One of the reasons for this is the

denominations in the currencies as the cash is converted

and held in US dollars. Thus, operating profit can be

affected in US dollars by movement in exchange rates.

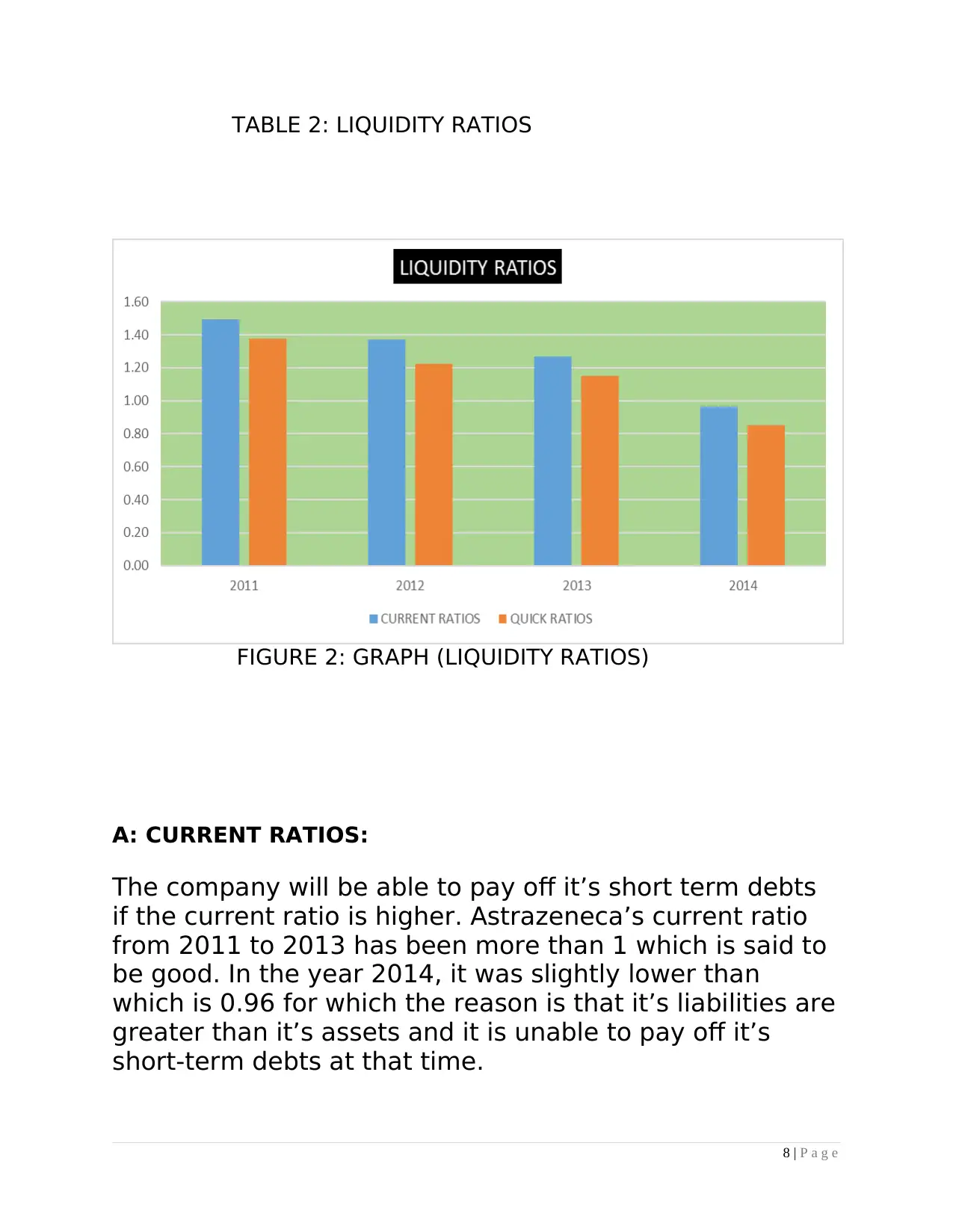

2.2. LIQUIDITY RATIOS:

These ratios are used to determine a company’s ability to

pay off it’s short term debts. The margin of safety for the

company to cover it’s short-term debts is higher when the

value of the ratio is high. Testing a company’s liquidity is

an important step in it’s analysis. Here, we will calculate

the ratios which is Current ratio and Quick ratio (Acid test

ratio).

2011 2012 2013 2014

CURRENT RATIO 1.49 1.37 1.27 0.96

QUICK RATIO 1.37 1.22 1.15 0.85

7 | P a g e

The operating profit from 2011 to 2014 was 36.82% to

4.77% respectively. The decline of operating profit was

due to the expenditure associated with the growth

platforms such as research and development expenses of

$5579m in 2014.The increase in selling, administrative

and distribution costs have led to a decline in the net

operating margin. One of the reasons for this is the

denominations in the currencies as the cash is converted

and held in US dollars. Thus, operating profit can be

affected in US dollars by movement in exchange rates.

2.2. LIQUIDITY RATIOS:

These ratios are used to determine a company’s ability to

pay off it’s short term debts. The margin of safety for the

company to cover it’s short-term debts is higher when the

value of the ratio is high. Testing a company’s liquidity is

an important step in it’s analysis. Here, we will calculate

the ratios which is Current ratio and Quick ratio (Acid test

ratio).

2011 2012 2013 2014

CURRENT RATIO 1.49 1.37 1.27 0.96

QUICK RATIO 1.37 1.22 1.15 0.85

7 | P a g e

TABLE 2: LIQUIDITY RATIOS

FIGURE 2: GRAPH (LIQUIDITY RATIOS)

A: CURRENT RATIOS:

The company will be able to pay off it’s short term debts

if the current ratio is higher. Astrazeneca’s current ratio

from 2011 to 2013 has been more than 1 which is said to

be good. In the year 2014, it was slightly lower than

which is 0.96 for which the reason is that it’s liabilities are

greater than it’s assets and it is unable to pay off it’s

short-term debts at that time.

8 | P a g e

FIGURE 2: GRAPH (LIQUIDITY RATIOS)

A: CURRENT RATIOS:

The company will be able to pay off it’s short term debts

if the current ratio is higher. Astrazeneca’s current ratio

from 2011 to 2013 has been more than 1 which is said to

be good. In the year 2014, it was slightly lower than

which is 0.96 for which the reason is that it’s liabilities are

greater than it’s assets and it is unable to pay off it’s

short-term debts at that time.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

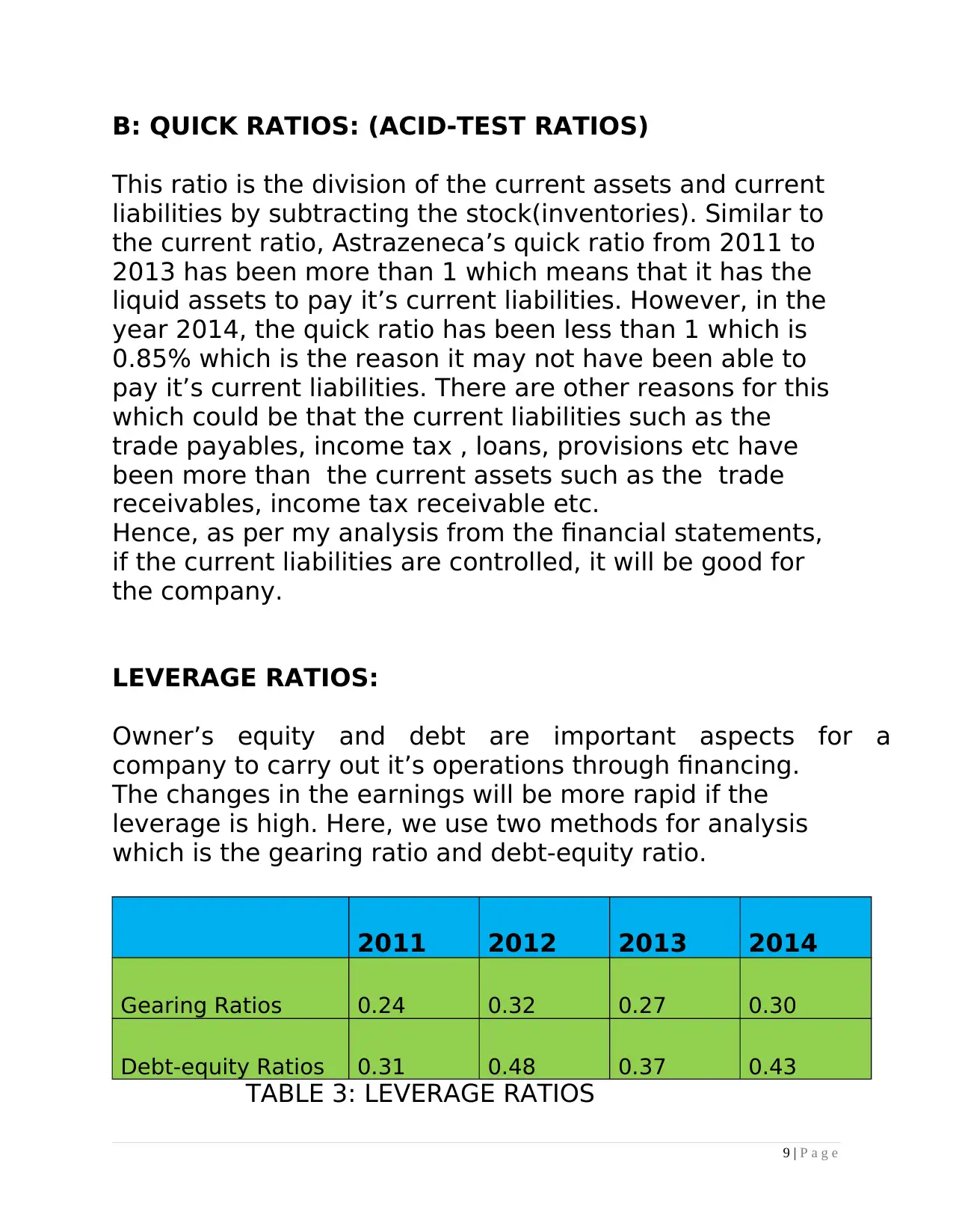

B: QUICK RATIOS: (ACID-TEST RATIOS)

This ratio is the division of the current assets and current

liabilities by subtracting the stock(inventories). Similar to

the current ratio, Astrazeneca’s quick ratio from 2011 to

2013 has been more than 1 which means that it has the

liquid assets to pay it’s current liabilities. However, in the

year 2014, the quick ratio has been less than 1 which is

0.85% which is the reason it may not have been able to

pay it’s current liabilities. There are other reasons for this

which could be that the current liabilities such as the

trade payables, income tax , loans, provisions etc have

been more than the current assets such as the trade

receivables, income tax receivable etc.

Hence, as per my analysis from the financial statements,

if the current liabilities are controlled, it will be good for

the company.

LEVERAGE RATIOS:

Owner’s equity and debt are important aspects for a

company to carry out it’s operations through financing.

The changes in the earnings will be more rapid if the

leverage is high. Here, we use two methods for analysis

which is the gearing ratio and debt-equity ratio.

2011 2012 2013 2014

Gearing Ratios 0.24 0.32 0.27 0.30

Debt-equity Ratios 0.31 0.48 0.37 0.43

TABLE 3: LEVERAGE RATIOS

9 | P a g e

This ratio is the division of the current assets and current

liabilities by subtracting the stock(inventories). Similar to

the current ratio, Astrazeneca’s quick ratio from 2011 to

2013 has been more than 1 which means that it has the

liquid assets to pay it’s current liabilities. However, in the

year 2014, the quick ratio has been less than 1 which is

0.85% which is the reason it may not have been able to

pay it’s current liabilities. There are other reasons for this

which could be that the current liabilities such as the

trade payables, income tax , loans, provisions etc have

been more than the current assets such as the trade

receivables, income tax receivable etc.

Hence, as per my analysis from the financial statements,

if the current liabilities are controlled, it will be good for

the company.

LEVERAGE RATIOS:

Owner’s equity and debt are important aspects for a

company to carry out it’s operations through financing.

The changes in the earnings will be more rapid if the

leverage is high. Here, we use two methods for analysis

which is the gearing ratio and debt-equity ratio.

2011 2012 2013 2014

Gearing Ratios 0.24 0.32 0.27 0.30

Debt-equity Ratios 0.31 0.48 0.37 0.43

TABLE 3: LEVERAGE RATIOS

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FIGURE 3:GRAPH (LEVERAGE RATIOS)

A.GEARING RATIOS:

A company is considered more risky if it’s degree of

leverage is high. Also, if the gearing is high, the company

is prone to the downward side of the business cycle as it

has to continue to service it’s debt even if the sales are

bad. There have been ups and downs from year 2011 to

2013 with regards to the equity and debt. In year 2014,

there was a fall in both equity and debt which resulted in

gearing ratio to be higher which is 0.30% compared to

2013 which was 0.27%. Overall, the gearing ratios have

been low and in my analysis of the financial statements

the reason for this is that Astrazeneca requires more

redemption capital because of the merger acquisition it

has had and also the earnings need to be increased.

10 | P a g e

A.GEARING RATIOS:

A company is considered more risky if it’s degree of

leverage is high. Also, if the gearing is high, the company

is prone to the downward side of the business cycle as it

has to continue to service it’s debt even if the sales are

bad. There have been ups and downs from year 2011 to

2013 with regards to the equity and debt. In year 2014,

there was a fall in both equity and debt which resulted in

gearing ratio to be higher which is 0.30% compared to

2013 which was 0.27%. Overall, the gearing ratios have

been low and in my analysis of the financial statements

the reason for this is that Astrazeneca requires more

redemption capital because of the merger acquisition it

has had and also the earnings need to be increased.

10 | P a g e

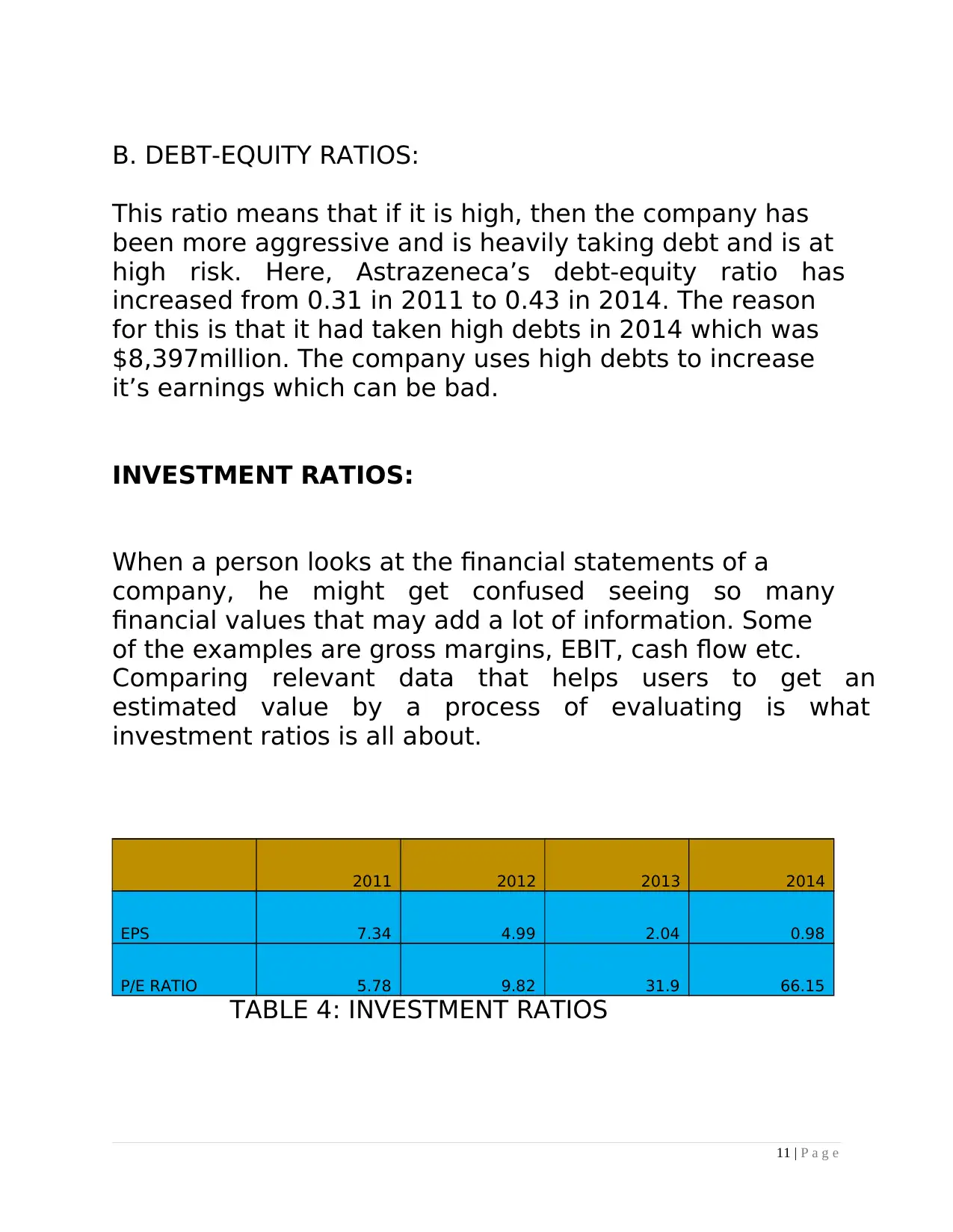

B. DEBT-EQUITY RATIOS:

This ratio means that if it is high, then the company has

been more aggressive and is heavily taking debt and is at

high risk. Here, Astrazeneca’s debt-equity ratio has

increased from 0.31 in 2011 to 0.43 in 2014. The reason

for this is that it had taken high debts in 2014 which was

$8,397million. The company uses high debts to increase

it’s earnings which can be bad.

INVESTMENT RATIOS:

When a person looks at the financial statements of a

company, he might get confused seeing so many

financial values that may add a lot of information. Some

of the examples are gross margins, EBIT, cash flow etc.

Comparing relevant data that helps users to get an

estimated value by a process of evaluating is what

investment ratios is all about.

2011 2012 2013 2014

EPS 7.34 4.99 2.04 0.98

P/E RATIO 5.78 9.82 31.9 66.15

TABLE 4: INVESTMENT RATIOS

11 | P a g e

This ratio means that if it is high, then the company has

been more aggressive and is heavily taking debt and is at

high risk. Here, Astrazeneca’s debt-equity ratio has

increased from 0.31 in 2011 to 0.43 in 2014. The reason

for this is that it had taken high debts in 2014 which was

$8,397million. The company uses high debts to increase

it’s earnings which can be bad.

INVESTMENT RATIOS:

When a person looks at the financial statements of a

company, he might get confused seeing so many

financial values that may add a lot of information. Some

of the examples are gross margins, EBIT, cash flow etc.

Comparing relevant data that helps users to get an

estimated value by a process of evaluating is what

investment ratios is all about.

2011 2012 2013 2014

EPS 7.34 4.99 2.04 0.98

P/E RATIO 5.78 9.82 31.9 66.15

TABLE 4: INVESTMENT RATIOS

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.