Financial Reporting Analysis: Arnold Hill & Co. Case Study

VerifiedAdded on 2020/12/10

|19

|5235

|361

Report

AI Summary

This financial reporting report provides a comprehensive overview of financial reporting, starting with its context and purpose, and then delving into the conceptual and regulatory frameworks that govern it. The report identifies key stakeholders and their needs for financial reports, analyzing how financial reporting contributes to meeting organizational objectives and fostering growth. It explains international accounting standards (IAS) and international financial reporting standards (IFRS), highlighting their benefits and evaluating the degree of compliance by different organizations. The report also examines differences in financial reporting across the world and the factors that influence these differences. The report concludes with a case study of Arnold Hill & Co., a UK-based accounting firm, illustrating practical applications of financial reporting principles and their impact on financial services. The report covers various aspects of financial reporting, including its importance in economic decision-making and its role in providing relevant and useful information to stakeholders.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Context and purpose of financial reporting........................................................................1

2. Conceptual and regulatory frameworks of financial reporting with their purpose and

requirements...........................................................................................................................3

3. Identification of key stakeholder of organisation and their need for financial reports......5

4. Analysis of financial reporting for meeting organisational objectives and growth............7

5. Explanation of international accounting standards and international financial reporting

standards with their benefits...................................................................................................8

6. Evaluating financial reporting in organisation with appropriate theories and model......10

7. Identification of differences in financial reporting across the world and evaluation of factors

which influence these differences........................................................................................11

8. Evaluating the degree of compliance with IFRS by different organisations across the world

..............................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Context and purpose of financial reporting........................................................................1

2. Conceptual and regulatory frameworks of financial reporting with their purpose and

requirements...........................................................................................................................3

3. Identification of key stakeholder of organisation and their need for financial reports......5

4. Analysis of financial reporting for meeting organisational objectives and growth............7

5. Explanation of international accounting standards and international financial reporting

standards with their benefits...................................................................................................8

6. Evaluating financial reporting in organisation with appropriate theories and model......10

7. Identification of differences in financial reporting across the world and evaluation of factors

which influence these differences........................................................................................11

8. Evaluating the degree of compliance with IFRS by different organisations across the world

..............................................................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial reporting is the process of disclosing financial results and information to users

(external stakeholder) and to management about performance of company in business market.

Company usually issued financial reports on quarterly and annual basis with mainly three

statements that is income statement, balance sheet and cash flow statement (Armstrong and et.al.,

2016). Therefore, this assessment will be develop to provide better understanding relates to

financial reporting where context and its purpose will be discussed. Further, explanation is to be

provided on conceptual and regulatory frameworks of financial reporting with its value to meet

organisational objectives.

In this report, international accounting standards and international financial reporting

standard will be explained for evaluating their benefits. Further, with appropriate theories better

understanding of financial reporting will be provided. Lastly, degree of compliance is also to be

discussed in this report. Chosen reputed accounting firm of UK in this report is Arnold Hill &

Co., which deals in providing effective and responsible financial services to clients which

seeking help relates to personal taxation.

MAIN BODY

1. Context and purpose of financial reporting

Financial reporting is a vital term and also plays an important role in the world of

economies. Its main purpose is to provide information which is relevant and useful for the

owners and for external stakeholders of the company. Through this accounting, companies will

provide information based on the result of business operations (Abbott and et.al., 2016). Context

of financial reporting is to comply with regulatory frameworks while preparing financial

statement of the company. These are the proper rules and regulations in order to disclose specific

information relates to company.

Key participants in financial reporting includes management, directors, external auditors

and stakeholders where each participant have personal allotted duty in terms of financial

reporting. Management is responsible for preparing financial statement and for business

operations of company. Directors are responsible to oversee methods which has been taken by

management to prepare financial statement.

1

Financial reporting is the process of disclosing financial results and information to users

(external stakeholder) and to management about performance of company in business market.

Company usually issued financial reports on quarterly and annual basis with mainly three

statements that is income statement, balance sheet and cash flow statement (Armstrong and et.al.,

2016). Therefore, this assessment will be develop to provide better understanding relates to

financial reporting where context and its purpose will be discussed. Further, explanation is to be

provided on conceptual and regulatory frameworks of financial reporting with its value to meet

organisational objectives.

In this report, international accounting standards and international financial reporting

standard will be explained for evaluating their benefits. Further, with appropriate theories better

understanding of financial reporting will be provided. Lastly, degree of compliance is also to be

discussed in this report. Chosen reputed accounting firm of UK in this report is Arnold Hill &

Co., which deals in providing effective and responsible financial services to clients which

seeking help relates to personal taxation.

MAIN BODY

1. Context and purpose of financial reporting

Financial reporting is a vital term and also plays an important role in the world of

economies. Its main purpose is to provide information which is relevant and useful for the

owners and for external stakeholders of the company. Through this accounting, companies will

provide information based on the result of business operations (Abbott and et.al., 2016). Context

of financial reporting is to comply with regulatory frameworks while preparing financial

statement of the company. These are the proper rules and regulations in order to disclose specific

information relates to company.

Key participants in financial reporting includes management, directors, external auditors

and stakeholders where each participant have personal allotted duty in terms of financial

reporting. Management is responsible for preparing financial statement and for business

operations of company. Directors are responsible to oversee methods which has been taken by

management to prepare financial statement.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Incorporated businesses has to comply with financial reporting guidelines while

preparing financial statement because it is considered as separate legal entity where members did

not personally hold liable for its business operations. On the contrary, unincorporated businesses

have their own separate legal entity and will also hold personally liable for the association of

debt and defaults (Page and Spira, 2016). Therefore, such company also have to maintain

financial statements in order to analyse their own performance.

Purpose of financial reporting:

Purpose of financial reporting is to meet users expectations and legislation in order to

evaluate company's performance. This helps investors and shareholders to make effective

decision to managing business operations. Three main goals of reporting includes:

Meet user's expectation and legislation: user and government always wanted to know

about company's strategy in order to reinvest cash in business and how efficiently

business is using its capital. Thus, financial reporting helps in meeting their expectation

where they will able to decide performance of business is in good place or not.

Track cash flow: financial reporting helps management and owners of company to

analyse flow of money in organisation. With this information they will able to analyse

performance of business for recovering its debt and to achieve growth.

Predict future financial position and cash flow: by monitoring assets, liabilities and

owner's equity, directors and management will able to predict future position and

availability of resources for achieving future growth (Tassadaq and Malik, 2015).

Therefore, financial reporting considered as the main tool to analyse company's performance. In

order to meet needs of the shareholders and users of company, it is necessary for organisation to

comply with rules and regulations of financial reporting providing necessary business

information in appropriate format which is more useful in terms of economic decision.

2

preparing financial statement because it is considered as separate legal entity where members did

not personally hold liable for its business operations. On the contrary, unincorporated businesses

have their own separate legal entity and will also hold personally liable for the association of

debt and defaults (Page and Spira, 2016). Therefore, such company also have to maintain

financial statements in order to analyse their own performance.

Purpose of financial reporting:

Purpose of financial reporting is to meet users expectations and legislation in order to

evaluate company's performance. This helps investors and shareholders to make effective

decision to managing business operations. Three main goals of reporting includes:

Meet user's expectation and legislation: user and government always wanted to know

about company's strategy in order to reinvest cash in business and how efficiently

business is using its capital. Thus, financial reporting helps in meeting their expectation

where they will able to decide performance of business is in good place or not.

Track cash flow: financial reporting helps management and owners of company to

analyse flow of money in organisation. With this information they will able to analyse

performance of business for recovering its debt and to achieve growth.

Predict future financial position and cash flow: by monitoring assets, liabilities and

owner's equity, directors and management will able to predict future position and

availability of resources for achieving future growth (Tassadaq and Malik, 2015).

Therefore, financial reporting considered as the main tool to analyse company's performance. In

order to meet needs of the shareholders and users of company, it is necessary for organisation to

comply with rules and regulations of financial reporting providing necessary business

information in appropriate format which is more useful in terms of economic decision.

2

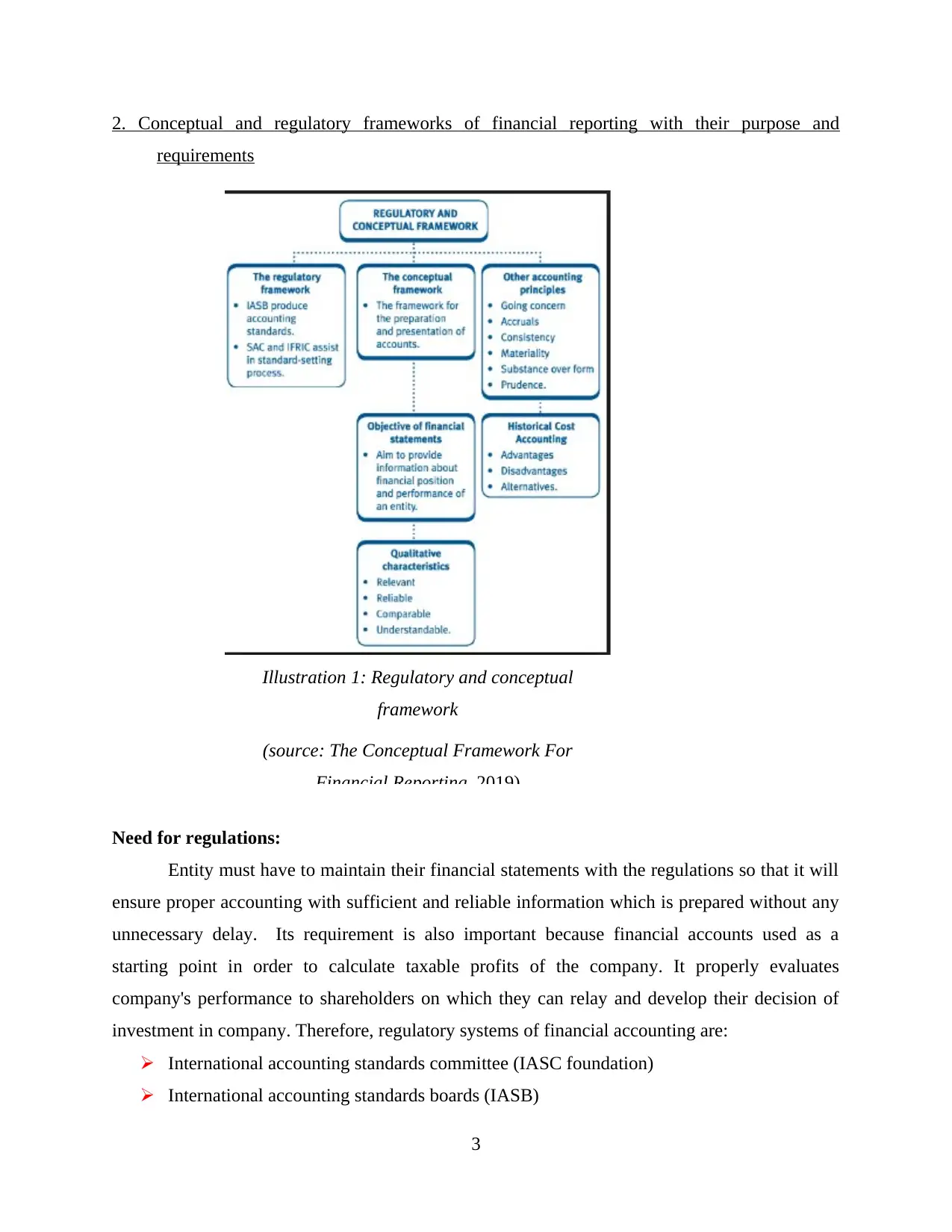

2. Conceptual and regulatory frameworks of financial reporting with their purpose and

requirements

Need for regulations:

Entity must have to maintain their financial statements with the regulations so that it will

ensure proper accounting with sufficient and reliable information which is prepared without any

unnecessary delay. Its requirement is also important because financial accounts used as a

starting point in order to calculate taxable profits of the company. It properly evaluates

company's performance to shareholders on which they can relay and develop their decision of

investment in company. Therefore, regulatory systems of financial accounting are:

International accounting standards committee (IASC foundation)

International accounting standards boards (IASB)

3

Illustration 1: Regulatory and conceptual

framework

(source: The Conceptual Framework For

Financial Reporting, 2019)

requirements

Need for regulations:

Entity must have to maintain their financial statements with the regulations so that it will

ensure proper accounting with sufficient and reliable information which is prepared without any

unnecessary delay. Its requirement is also important because financial accounts used as a

starting point in order to calculate taxable profits of the company. It properly evaluates

company's performance to shareholders on which they can relay and develop their decision of

investment in company. Therefore, regulatory systems of financial accounting are:

International accounting standards committee (IASC foundation)

International accounting standards boards (IASB)

3

Illustration 1: Regulatory and conceptual

framework

(source: The Conceptual Framework For

Financial Reporting, 2019)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

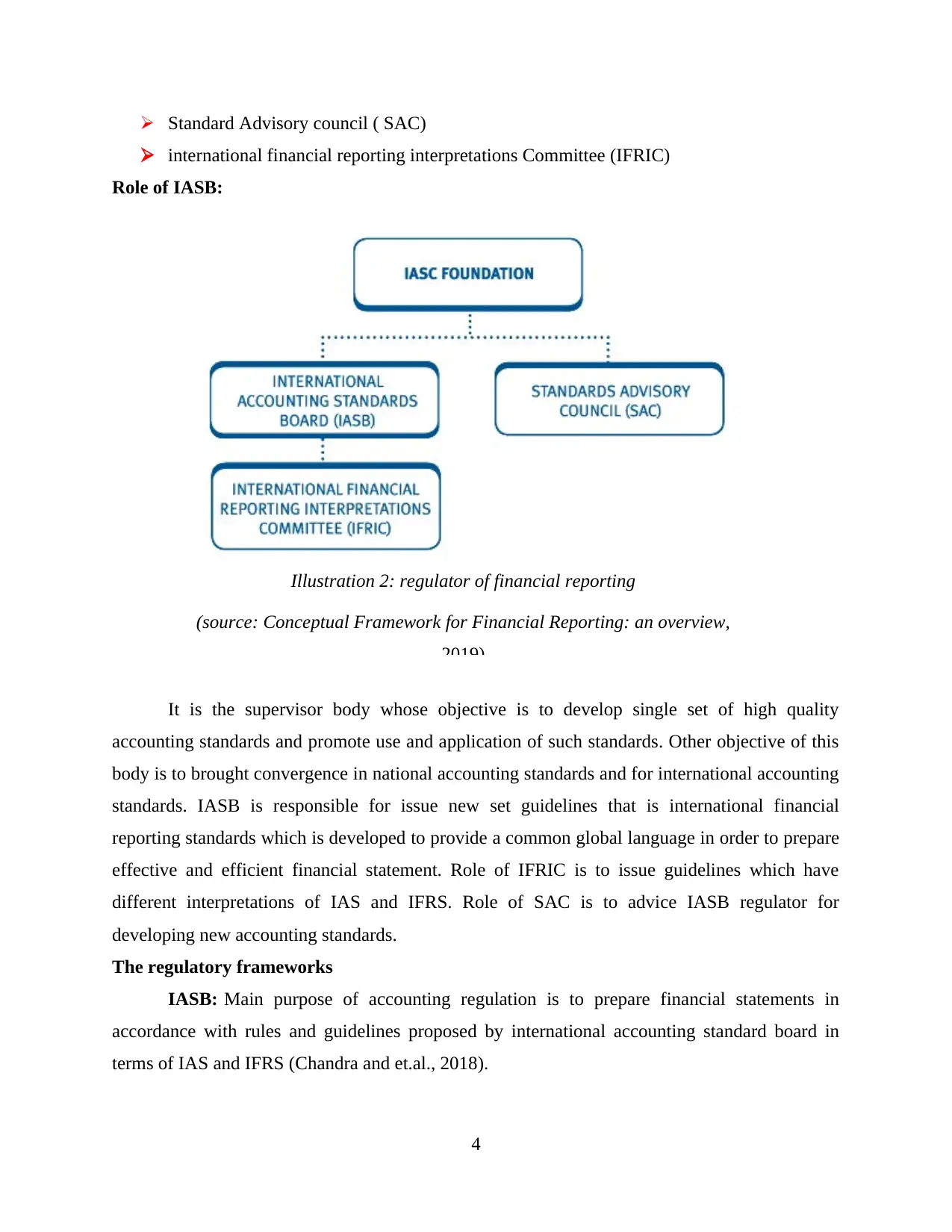

Standard Advisory council ( SAC)

international financial reporting interpretations Committee (IFRIC)

Role of IASB:

It is the supervisor body whose objective is to develop single set of high quality

accounting standards and promote use and application of such standards. Other objective of this

body is to brought convergence in national accounting standards and for international accounting

standards. IASB is responsible for issue new set guidelines that is international financial

reporting standards which is developed to provide a common global language in order to prepare

effective and efficient financial statement. Role of IFRIC is to issue guidelines which have

different interpretations of IAS and IFRS. Role of SAC is to advice IASB regulator for

developing new accounting standards.

The regulatory frameworks

IASB: Main purpose of accounting regulation is to prepare financial statements in

accordance with rules and guidelines proposed by international accounting standard board in

terms of IAS and IFRS (Chandra and et.al., 2018).

4

Illustration 2: regulator of financial reporting

(source: Conceptual Framework for Financial Reporting: an overview,

2019)

international financial reporting interpretations Committee (IFRIC)

Role of IASB:

It is the supervisor body whose objective is to develop single set of high quality

accounting standards and promote use and application of such standards. Other objective of this

body is to brought convergence in national accounting standards and for international accounting

standards. IASB is responsible for issue new set guidelines that is international financial

reporting standards which is developed to provide a common global language in order to prepare

effective and efficient financial statement. Role of IFRIC is to issue guidelines which have

different interpretations of IAS and IFRS. Role of SAC is to advice IASB regulator for

developing new accounting standards.

The regulatory frameworks

IASB: Main purpose of accounting regulation is to prepare financial statements in

accordance with rules and guidelines proposed by international accounting standard board in

terms of IAS and IFRS (Chandra and et.al., 2018).

4

Illustration 2: regulator of financial reporting

(source: Conceptual Framework for Financial Reporting: an overview,

2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

IFRIC: Main task and purpose of this accounting body is to interpret applicability of IAS

and IFRS, if any kind of difficulty got arise. Before, finalizing any issue, such regulator will

firstly issue draft in terms of public interest.

SAC: Role of SAC is to provide advice to IASB for setting any type of guidelines or

project on any matter relates to financial accounting.

GAAP: these are the set of accounting principles which now mainly applied in US

companies in order to prepare their financial statement. It is an accounting standard where entity

applied for business which they conduct with long term perspective.

Conceptual Framework:

In order to prepare and present financial information, conceptual framework sets out the

concept in order to prepare financial statement. Its main purpose is:

To help IASB board for developing new set of accounting standards and to amend

previous one.

To develop harmonising set of accounting standard and procedure.

To assist accountants and people to prepare financial statement with the applicability of

IAS and IFRS (Macve, 2015).

To insist users for interpreting financial statements of company.

3. Identification of key stakeholder of organisation and their need for financial reports

Stakeholders are the group of individuals who has the interest in business performance

and outcomes of the organisation. These are the people who affected in some way if business get

failed in future because they mainly stake for success and failure of the organisation. Such

common example of the key stakeholder are as follows:

5

and IFRS, if any kind of difficulty got arise. Before, finalizing any issue, such regulator will

firstly issue draft in terms of public interest.

SAC: Role of SAC is to provide advice to IASB for setting any type of guidelines or

project on any matter relates to financial accounting.

GAAP: these are the set of accounting principles which now mainly applied in US

companies in order to prepare their financial statement. It is an accounting standard where entity

applied for business which they conduct with long term perspective.

Conceptual Framework:

In order to prepare and present financial information, conceptual framework sets out the

concept in order to prepare financial statement. Its main purpose is:

To help IASB board for developing new set of accounting standards and to amend

previous one.

To develop harmonising set of accounting standard and procedure.

To assist accountants and people to prepare financial statement with the applicability of

IAS and IFRS (Macve, 2015).

To insist users for interpreting financial statements of company.

3. Identification of key stakeholder of organisation and their need for financial reports

Stakeholders are the group of individuals who has the interest in business performance

and outcomes of the organisation. These are the people who affected in some way if business get

failed in future because they mainly stake for success and failure of the organisation. Such

common example of the key stakeholder are as follows:

5

Customers: Mainly customers are the actual stakeholders of the organisation because business

exist to serve their consumer only. They are mainly affected with the quality of service and its

value in organisation. These group of stakeholder need financial report of company in order to

select supplier of some major contracts. They want financial statement to analyse financial

ability of supplier with the perspective to remain long term in market and to provide goods and

services long enough in market.

Employees: This is the another group of stakeholder who are interested in business operation of

company. Employees develop their interest by depending upon the nature of business conduct by

any organisation. Employees needs financial statement to analyse financial ability of company to

pay their income. This analysis also helps them to increase their level of involvement and to

understand nature of business (Barker and Teixeira, 2018).

6

Illustration 3: key stakeholder of organisation

( source: Who are the key stakeholder in an organisation, 2018)

exist to serve their consumer only. They are mainly affected with the quality of service and its

value in organisation. These group of stakeholder need financial report of company in order to

select supplier of some major contracts. They want financial statement to analyse financial

ability of supplier with the perspective to remain long term in market and to provide goods and

services long enough in market.

Employees: This is the another group of stakeholder who are interested in business operation of

company. Employees develop their interest by depending upon the nature of business conduct by

any organisation. Employees needs financial statement to analyse financial ability of company to

pay their income. This analysis also helps them to increase their level of involvement and to

understand nature of business (Barker and Teixeira, 2018).

6

Illustration 3: key stakeholder of organisation

( source: Who are the key stakeholder in an organisation, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Investors: it includes both shareholders and debt holders. These are the group of people who

invest in the business operation of company with the expectation that they will earn a certain

amount of rate of return on capital. Mainly investor need financial reports in order to develop

decision on the basis of financial ability of company. They decide whether to invest more or to

stop investment which they have done previously.

Suppliers and Vendors: this is the group of stakeholder which sells goods and services to

businesses and will only relay on revenue which get generate with ongoing business activities

(Level, 2018). They require financial reports in order to decide whether is it safe to extend credit

and to estimate ability to pay back their all loaned and funds.

Communities: In large businesses, these are the major stakeholder group which are impact by

large range of things such as employment, economic development and also on health and safety.

Such group also require financial reports of company to analyse their contribution towards

development of society and environment where its business is established.

Government: Government also considered as company's stakeholder as they collect tax from

company as well as to people which employed in such company. Government also require

financial reports of the company in order to determine that whether company is paying

appropriate amount of tax or not.

4. Analysis of financial reporting for meeting organisational objectives and growth

The main function of financial reporting is to provide information regarding entity's

performance in business market. It discloses information about organisation's ability to meet its

objectives and goals. It is generally considered as end product of accounting which has main

three components that is balance sheet, profit and loss and cash flow. It also helps management

to make economic decision with the future perspective of business goals (Barth and et.al., 2018).

Its importance cannot be overemphasized because financial reporting is the requirement of each

and every stakeholder for various types of reason. One among them is regarding their decision to

invest in the business affairs of company. Thus, its importance to meet organisational growth and

objectives is as follows-

Financial reporting helps organisations to comply with rules and regulation which

developed by regulatory bodies. Every entity requires filing their statements to

government agencies and if it is listed company then such statements needs to be filled on

7

invest in the business operation of company with the expectation that they will earn a certain

amount of rate of return on capital. Mainly investor need financial reports in order to develop

decision on the basis of financial ability of company. They decide whether to invest more or to

stop investment which they have done previously.

Suppliers and Vendors: this is the group of stakeholder which sells goods and services to

businesses and will only relay on revenue which get generate with ongoing business activities

(Level, 2018). They require financial reports in order to decide whether is it safe to extend credit

and to estimate ability to pay back their all loaned and funds.

Communities: In large businesses, these are the major stakeholder group which are impact by

large range of things such as employment, economic development and also on health and safety.

Such group also require financial reports of company to analyse their contribution towards

development of society and environment where its business is established.

Government: Government also considered as company's stakeholder as they collect tax from

company as well as to people which employed in such company. Government also require

financial reports of the company in order to determine that whether company is paying

appropriate amount of tax or not.

4. Analysis of financial reporting for meeting organisational objectives and growth

The main function of financial reporting is to provide information regarding entity's

performance in business market. It discloses information about organisation's ability to meet its

objectives and goals. It is generally considered as end product of accounting which has main

three components that is balance sheet, profit and loss and cash flow. It also helps management

to make economic decision with the future perspective of business goals (Barth and et.al., 2018).

Its importance cannot be overemphasized because financial reporting is the requirement of each

and every stakeholder for various types of reason. One among them is regarding their decision to

invest in the business affairs of company. Thus, its importance to meet organisational growth and

objectives is as follows-

Financial reporting helps organisations to comply with rules and regulation which

developed by regulatory bodies. Every entity requires filing their statements to

government agencies and if it is listed company then such statements needs to be filled on

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

quarterly and annual basis. This will help company to effectively monitor their

performance and carry out strategies to meeting organisational objectives.

This reporting facilitates statutory audit. In these auditors has been appointed to audit

financial statement for expressing their opinion on company's performance and areas

which needs to improve for achieving organisational goals.

Financial reporting considered as the backbone for developing effective planning,

analysing, bench marking and in decision-making process of the company (Ewert and

Wagenhofer, 2016). With this reporting shareholders, investors and creditors take

decision to invest in the company on the basis of their performance. Investment by such

investor and creditor provide a major support to entity for operating effective business

operations.

It helps organisation to raise their capital where management, directors with help of

statistical figure develop their decision by comparing it with past performance. Such

analysis helps them to improve function of business area which has less productivity.

Financial reporting also track amount of flow of money in an organisation. It provides

information related to flow of money coming from and where it is going., how much

amount of profit or loss company is bearing with its business operations. Such

identification helps directors and management to develop decision where profitability get

increases and business achieve its growth.

This reporting monitors any type of change arises in assets, liabilities and in owner's

equity by which owner will able to work out on strategies which helps in improving

business operations in the future (Whittington, 2017). This will also help in developing

availability of resources in order to achieve future growth.

5. Explanation of international accounting standards and international financial reporting

standards with their benefits

International accounting standard (IAS):

IAS is the set of accounting standards which guides entities regarding accounting

transaction to be record and reported in financial statement of organisation. In order to develop

reliable and effective set of information in financial statement, entity must have to prepare its

statement with the guidelines of IAS. Main motive to this regulatory body is to reduce

8

performance and carry out strategies to meeting organisational objectives.

This reporting facilitates statutory audit. In these auditors has been appointed to audit

financial statement for expressing their opinion on company's performance and areas

which needs to improve for achieving organisational goals.

Financial reporting considered as the backbone for developing effective planning,

analysing, bench marking and in decision-making process of the company (Ewert and

Wagenhofer, 2016). With this reporting shareholders, investors and creditors take

decision to invest in the company on the basis of their performance. Investment by such

investor and creditor provide a major support to entity for operating effective business

operations.

It helps organisation to raise their capital where management, directors with help of

statistical figure develop their decision by comparing it with past performance. Such

analysis helps them to improve function of business area which has less productivity.

Financial reporting also track amount of flow of money in an organisation. It provides

information related to flow of money coming from and where it is going., how much

amount of profit or loss company is bearing with its business operations. Such

identification helps directors and management to develop decision where profitability get

increases and business achieve its growth.

This reporting monitors any type of change arises in assets, liabilities and in owner's

equity by which owner will able to work out on strategies which helps in improving

business operations in the future (Whittington, 2017). This will also help in developing

availability of resources in order to achieve future growth.

5. Explanation of international accounting standards and international financial reporting

standards with their benefits

International accounting standard (IAS):

IAS is the set of accounting standards which guides entities regarding accounting

transaction to be record and reported in financial statement of organisation. In order to develop

reliable and effective set of information in financial statement, entity must have to prepare its

statement with the guidelines of IAS. Main motive to this regulatory body is to reduce

8

differences which arise while transacting accounting records and when preparing financial

statements.

Purpose of this establishment is to ensure effective regulations in financial market of the

businesses where entities across the world are interconnected and use only global financial

reporting framework for disclosing financial statement in the market. By having such financial

statement, businesses which are established in different jurisdiction will able to create most

efficient capital flows (Capkun Collins and Jeanjean, 2016). This standard was created and

issued by board of international accounting standard committee to advice some guidelines to

company for preparing and presenting their financial statement in appropriate format.

Its benefits are as follows-

Facilitate ethics compliance: different countries have their different regions with their

different culture and norms, because of which it gets manifested in the culture of business

across the world. Thus, these accounting standards are the set of unified code of ethics in

accounting which needs to be followed by each and every country. These set of

guidelines do not favour one culture over other and develops proper ethical practises in

order to prepare financial statement of the company.

Improves international investment: when entities prepare its financial statement with the

one set of common global language, it helps them to capture support of international

investors. They compare financial statement of the company by following guidelines of

IAS. Multinational companies: this set of guideline simplify accounting method for the MNC's

which facilitate its operations in multiple countries of the world. Such companies use this

accounting standards in order to avoid confusion and to develop accuracy and efficiency

in financial statement of the company (De Luca and Prather-Kinsey, 2018).

International financial reporting standards (IFRS)

These are the set of accounting standards which provide a particular guideline to

company in order to record financial transaction in their books of accounts. IASB has issued this

standard in order to develop transparency and reliability in financial statements of companies

which conduct business globally. Main motive behind this development is to provide a common

global language in financial world. Currently, this framework has been applied in 120 countries

except in US because they follow GAAP in order to prepare financial reports.

9

statements.

Purpose of this establishment is to ensure effective regulations in financial market of the

businesses where entities across the world are interconnected and use only global financial

reporting framework for disclosing financial statement in the market. By having such financial

statement, businesses which are established in different jurisdiction will able to create most

efficient capital flows (Capkun Collins and Jeanjean, 2016). This standard was created and

issued by board of international accounting standard committee to advice some guidelines to

company for preparing and presenting their financial statement in appropriate format.

Its benefits are as follows-

Facilitate ethics compliance: different countries have their different regions with their

different culture and norms, because of which it gets manifested in the culture of business

across the world. Thus, these accounting standards are the set of unified code of ethics in

accounting which needs to be followed by each and every country. These set of

guidelines do not favour one culture over other and develops proper ethical practises in

order to prepare financial statement of the company.

Improves international investment: when entities prepare its financial statement with the

one set of common global language, it helps them to capture support of international

investors. They compare financial statement of the company by following guidelines of

IAS. Multinational companies: this set of guideline simplify accounting method for the MNC's

which facilitate its operations in multiple countries of the world. Such companies use this

accounting standards in order to avoid confusion and to develop accuracy and efficiency

in financial statement of the company (De Luca and Prather-Kinsey, 2018).

International financial reporting standards (IFRS)

These are the set of accounting standards which provide a particular guideline to

company in order to record financial transaction in their books of accounts. IASB has issued this

standard in order to develop transparency and reliability in financial statements of companies

which conduct business globally. Main motive behind this development is to provide a common

global language in financial world. Currently, this framework has been applied in 120 countries

except in US because they follow GAAP in order to prepare financial reports.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.