Financial Analysis Report: XYZ Investment - Tender Review and Decision

VerifiedAdded on 2022/10/19

|9

|1888

|36

Report

AI Summary

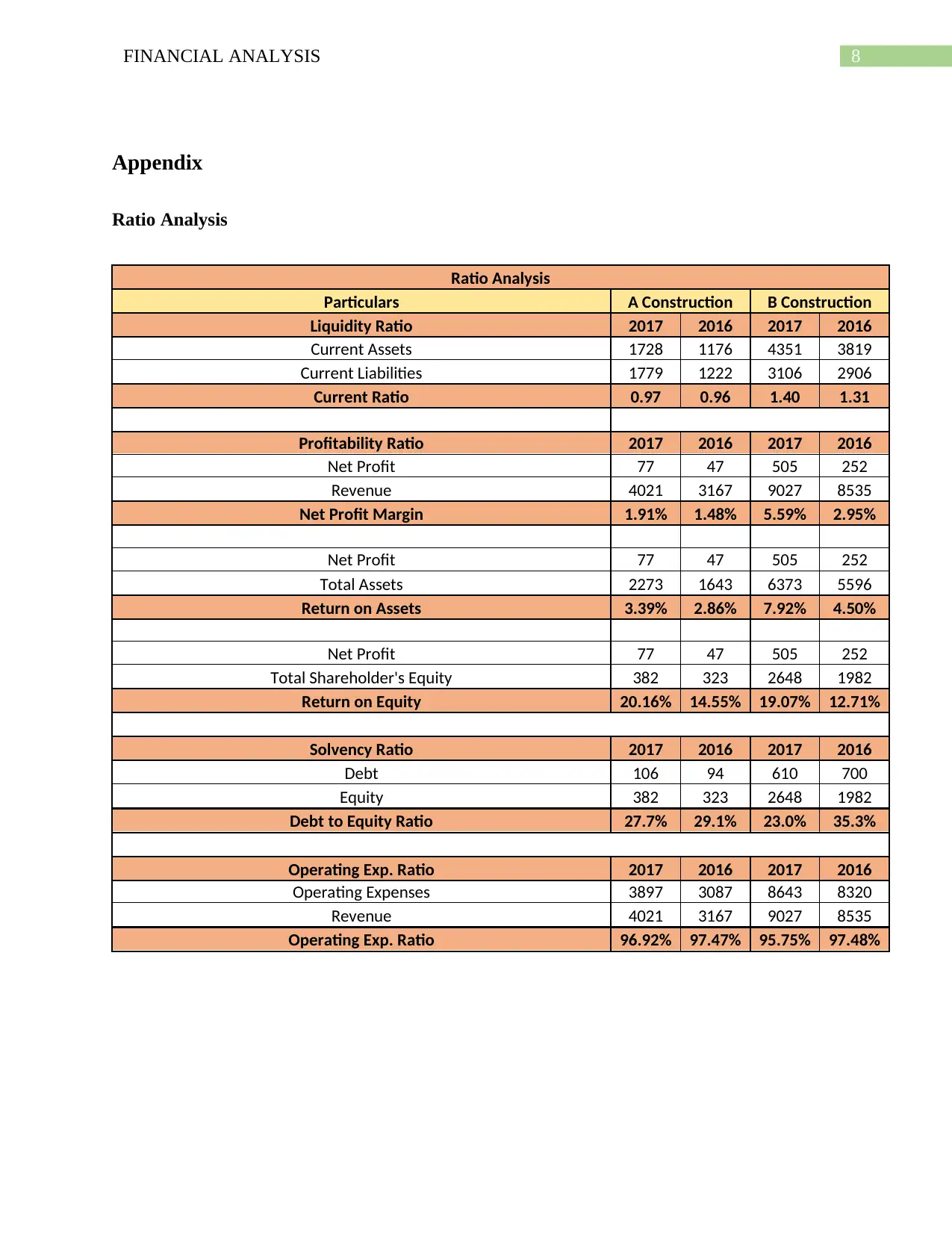

This report presents a comprehensive financial analysis of XYZ Investment, focusing on the performance of two construction companies, A Construction and B Construction, for the years 2016 and 2017. The analysis encompasses a detailed examination of liquidity, profitability, and solvency ratios, including current ratios, net profit margins, return on assets, return on equity, and debt-to-equity ratios. The report also considers operating expense ratios and earnings per share (EPS) for each construction unit. Financial considerations, such as tender prices and return on investment (ROI), are evaluated to determine the best investment option. Non-financial considerations, including employee base, business risk, and financial stability, are also addressed. The report concludes with a recommendation to invest in Construction B due to its superior financial performance and position, supported by a comparative analysis of key financial metrics and risk factors.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.