Financial Management Assignment: Risk, Return, NPV, and Financing

VerifiedAdded on 2023/01/09

|8

|1263

|26

Report

AI Summary

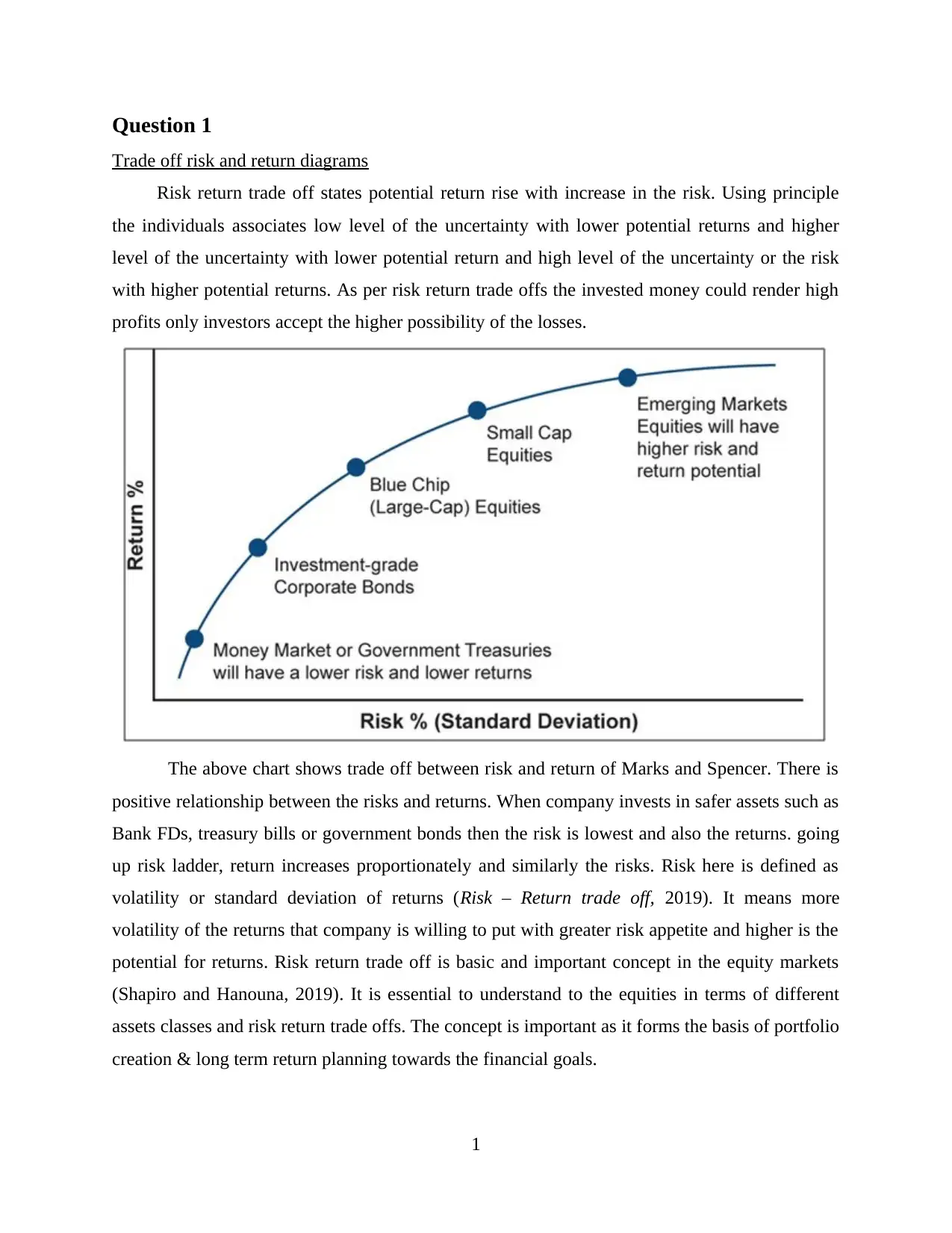

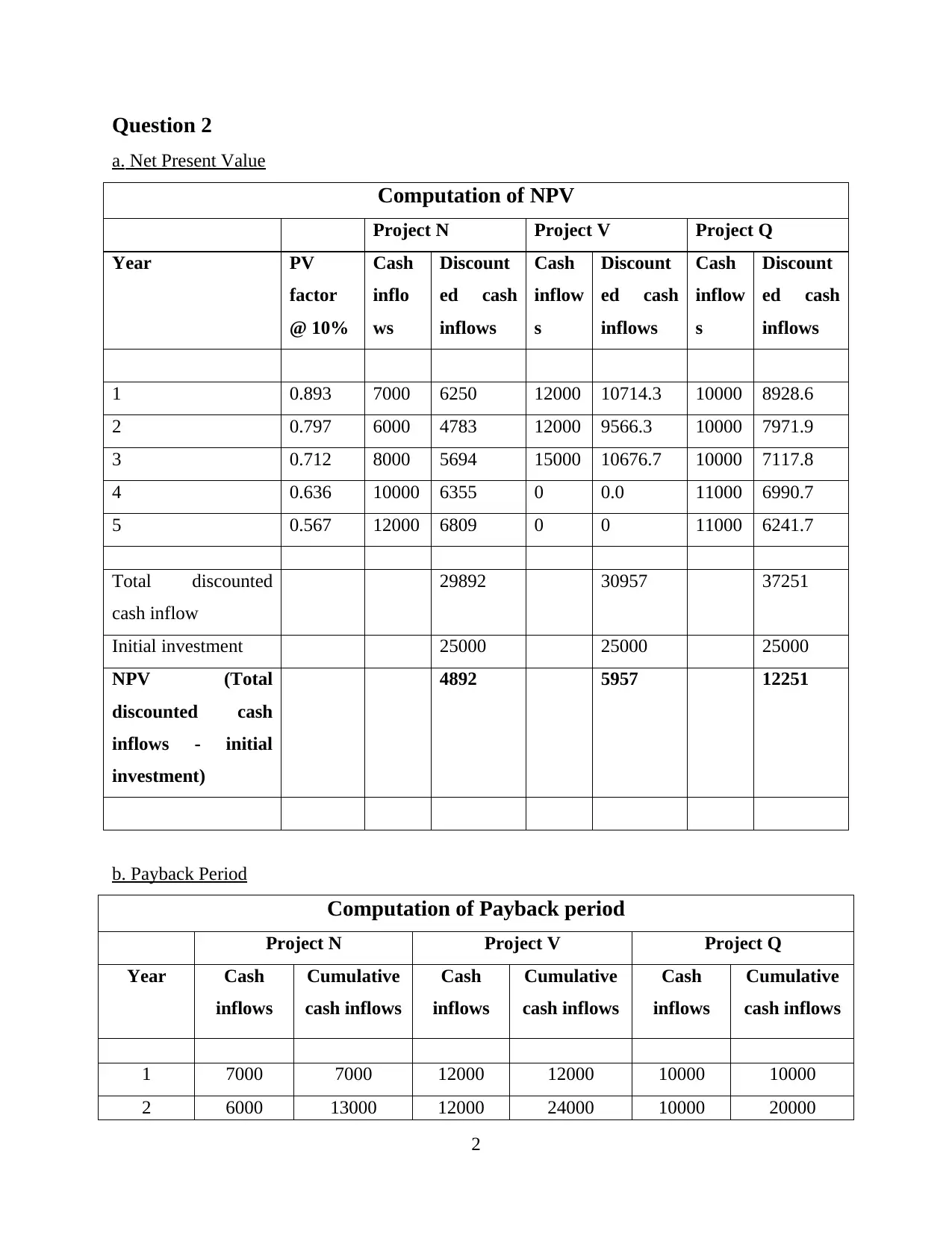

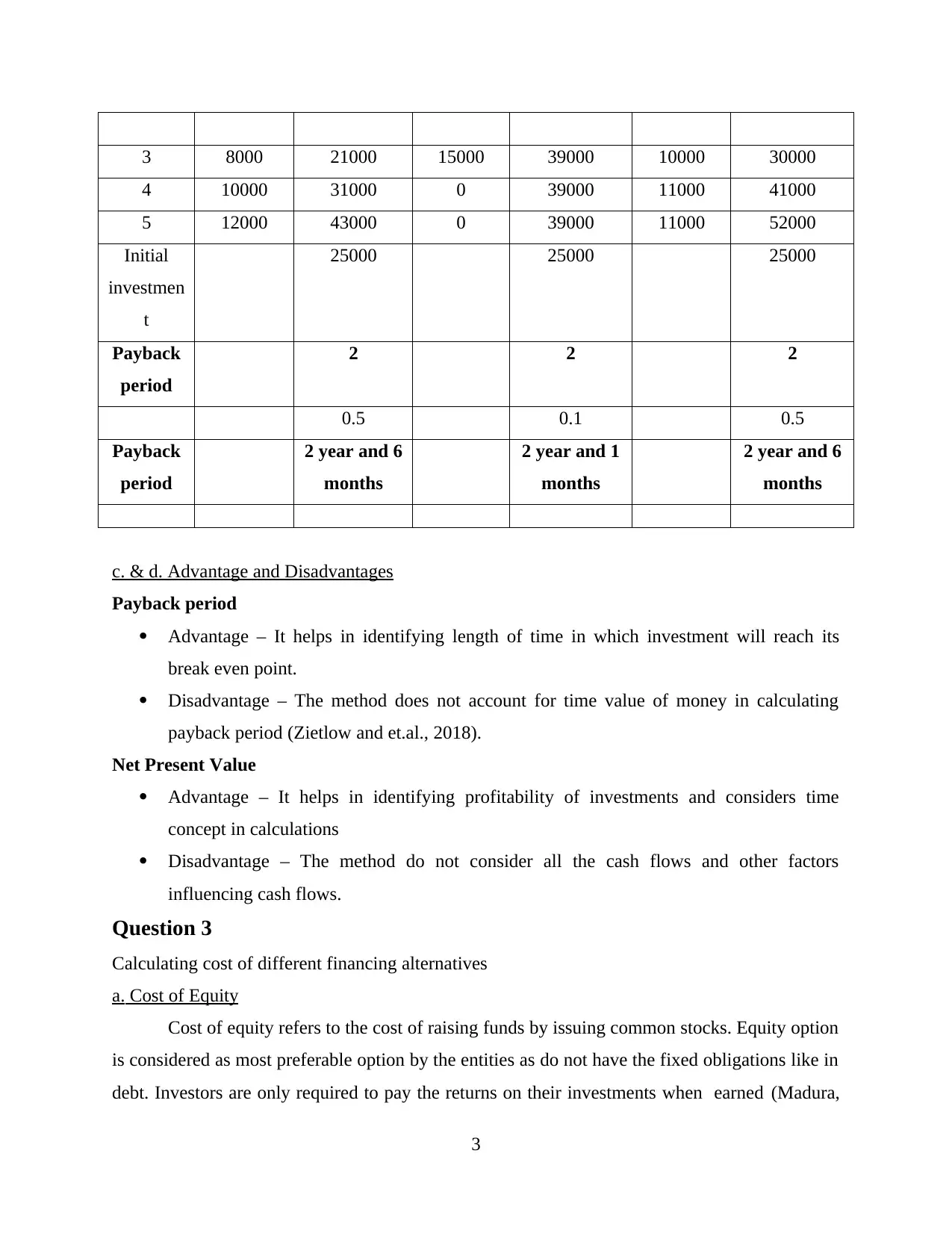

This financial management report comprehensively addresses key concepts in finance. It begins with an explanation of the risk-return trade-off using diagrams and a real-world example of Marks and Spencer, illustrating the positive relationship between risk and potential return. The report then delves into project evaluation techniques, calculating the Net Present Value (NPV) and Payback Period for three different projects (N, V, and Q), along with the advantages and disadvantages of each method. Furthermore, the assignment explores the cost of different financing alternatives, including the cost of equity, cost of debt, and cost of preferred stock, providing formulas and calculations for each. Finally, the report analyzes financing proposals, recommending the most suitable option based on the calculated costs and financial risks, concluding with a discussion on the advantages of issuing common stock over preferred stock. The report is well-referenced, using Harvard style citations throughout.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.